Apparently, history is rhyming. Sadly, governments are preparing to confiscate their citizens’ gold, as they are tightening the net around private ownership. Seeing that they’re maneuvering in a rather deceptive manner, Ronnie calls this the age of “soft gold confiscation”.

In China, the commies’ VAT reforms have made bullion more tax-efficient than jewelry, effectively steering savers into official channels of gold accumulation. Similarly, Italy’s proposed one-off levy on private gold creates a national registry in disguise. Unsurprisingly, in its latest stability report, the ECB warns that gold markets may require “closer monitoring”; which just sounds like bureaucratic code for increased control.

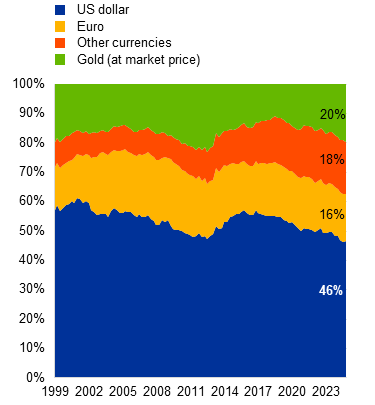

Behind these moves is a simple reality: currencies are losing purchasing power faster than institutions can justify. Even the ECB admits the euro’s global share has stagnated, while gold’s value in official reserves has risen to rival — and in some measures surpass — the euro.

Seemingly, markets are rediscovering what some monetary authorities and politicians have known for a while: gold is the only monetary asset no government can print.

Ronnie’s reference to Bretton Woods III — originally coined by Zoltan Pozsar — captures the essence of today’s shift. When the U.S. and EU froze Russia’s foreign reserves in 2022, something irreversible happened: trust in fiat-denominated reserves cracked.

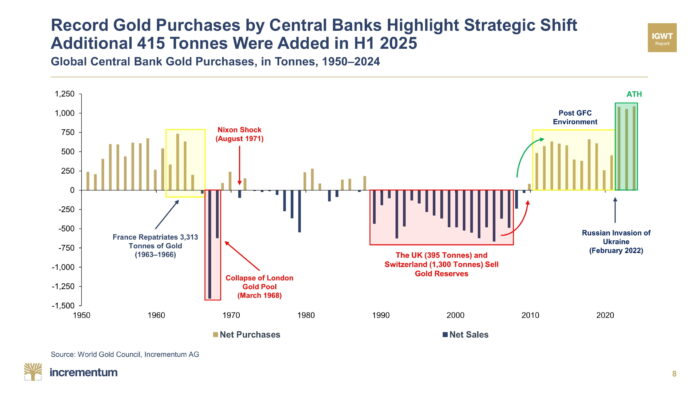

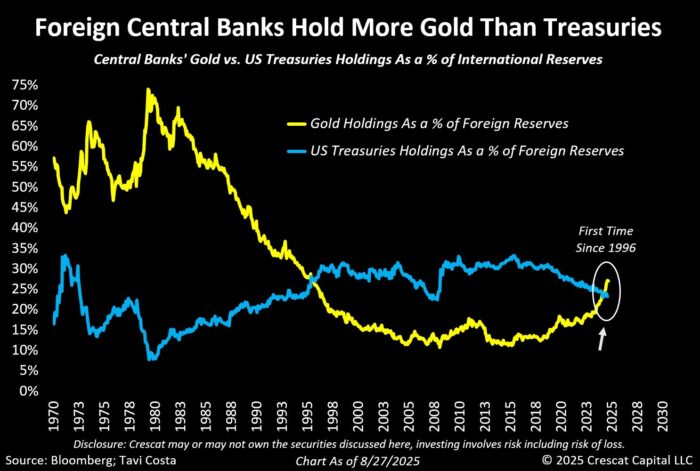

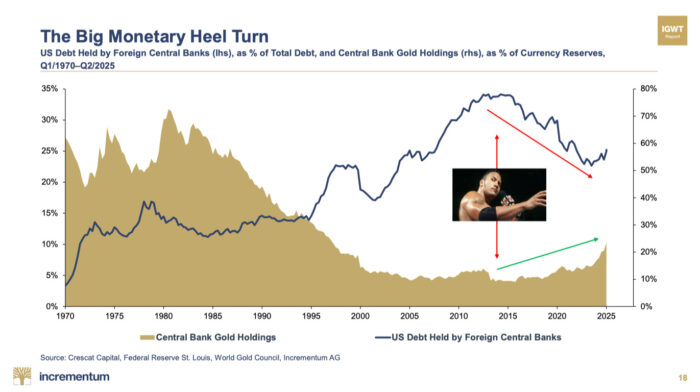

The global reaction is measurable. Central banks bought over 1,000 tonnes of gold each year in 2022, 2023, and 2024. Foreign central banks now hold more gold than U.S. Treasuries, which is the first time this happened since 1996. In the latest WGC Central Bank Gold Reserves Survey, 95% of them expect global gold reserves to rise further, while a record 43% plan to increase their own.

Meanwhile, the Trump administration has signaled — through advisers like Stephen Miran — that the current monetary framework is outdated. The proposed “Mar-a-Lago Accord” hints at a controlled dollar devaluation, which cannot happen without a neutral anchor. Unquestionably, that anchor is gold.

Demonstrably, they’re not de-dollarizing into the yuan. As a matter of fact, this is de-dollarization into neutral, apolitical collateral.

The 2025 BRICS Summit made one thing clear: the bloc’s power lies not in creating a new currency, but in reshaping settlement infrastructure. The agenda focused on local-currency platforms, cross-border payment rails, and collateral frameworks. Clearly, talks of a unified BRICS coin were dropped.

At any rate, emerging economies have steadily increased their gold share of reserves, while reducing reliance on U.S. Treasuries. In truth, they’ve grown afraid of having the same treatment as Russia.

Thus, BRICS doesn’t need a single currency. The group’s influence comes from breaking the monopoly of Western financial plumbing and using gold as the neutral intermediary is a crucial step.

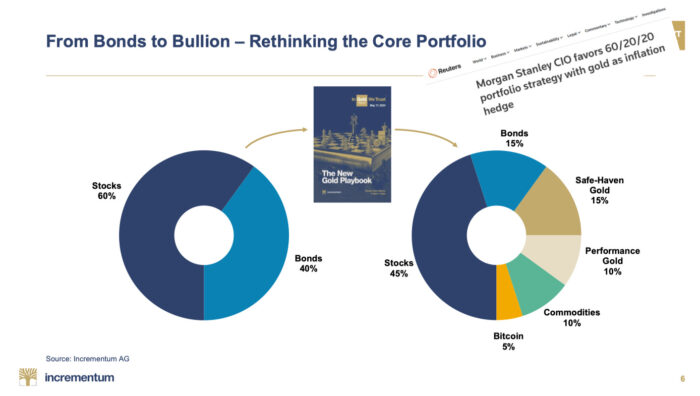

The traditional 60/40 portfolio collapsed in 2022, when bonds failed to hedge equities. As our research shows, a world of structural inflation, geopolitical fragmentation, and rising debt demands a redesigned allocation model.

Here is the New 60/40 Portfolio, introduced in IGWT 2024 and reaffirmed in the 2025 edition:

45% equities

15% bonds

15% safe-haven gold

10% performance gold (silver + miners)

10% commodities

5% Bitcoin

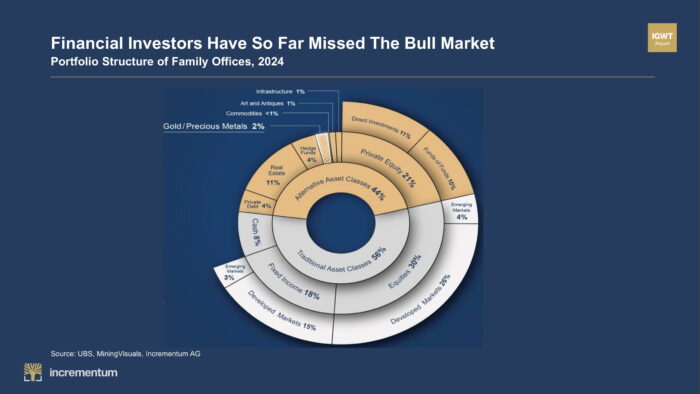

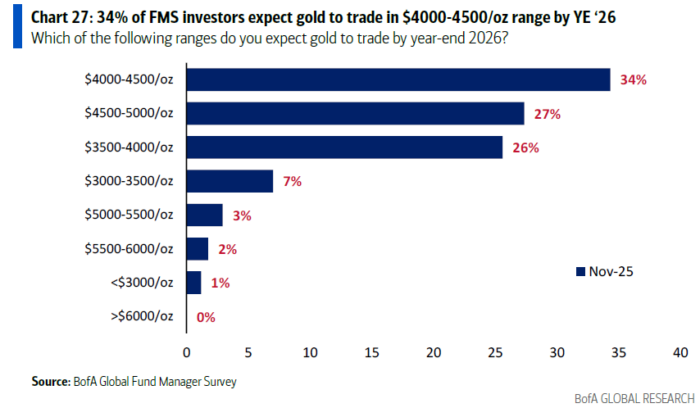

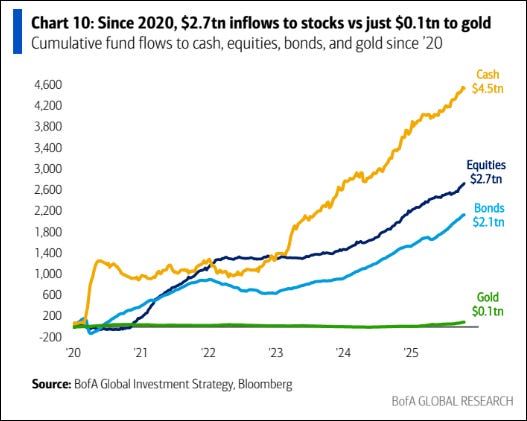

Nevertheless, professional investors remain dramatically under-exposed. The UBS Global Family Office Report 2025 shows an allocation of just 2% to precious metals. Although being higher than the 1% of last year’s report, it’s still below the 3% level seen in 2019. Undoubtedly, this gap between optimal and actual positioning, instead of being an obstacle, is the fuel of the next leg of the bull market.

If family offices and wealthy individuals choose to snub precious metals, it’s their loss. Citi’s latest research offers one of the most striking insights in the entire gold market: a mere 0.1% increase in global household gold allocations would require doubling annual mine production. In other words, if Western households move slightly toward gold, the market breaks.

So far, the bull market has been carried overwhelmingly by central banks and Asian physical demand. This means the Western demand wave has yet to really begin. When it does, supply will not be able to meet it.

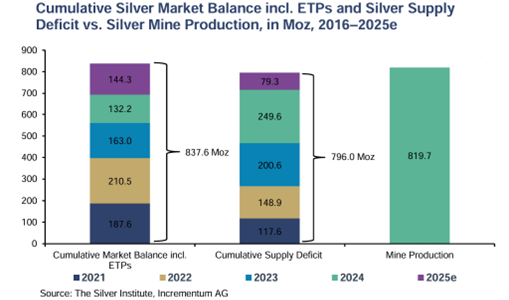

As the energy transition bumps along, silver is turning out to be its quiet bottleneck. On its own, solar consumed 198 million ounces in 2024. Demand from EVs, batteries, aerospace, and defense electronics continues expanding, even at higher prices.

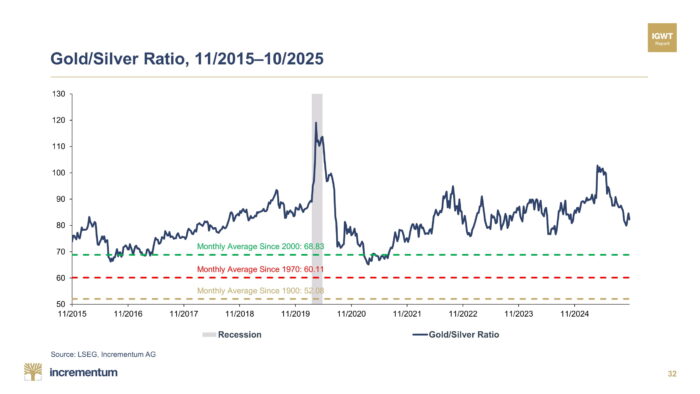

In his Sound Money Report, Ted Butler’s latest article highlights that while the historic 30:1 gold/silver ratio is unlikely, a move into the 50–60 range is realistic. At current gold prices, this points to silver in the USD 70–82 range, which is still conservative.

In short, silver’s volatility masks a simple truth: structural deficits are now a permanent feature of the market.

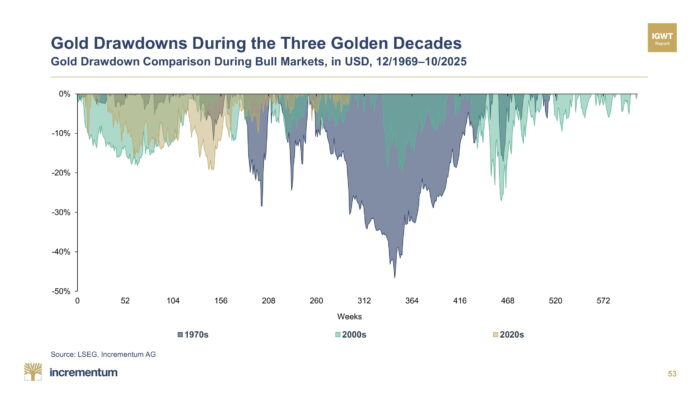

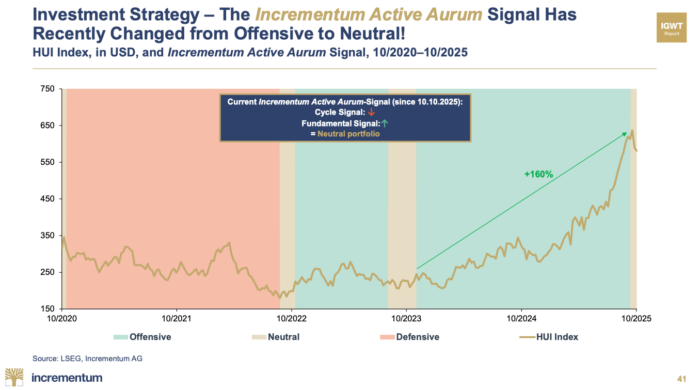

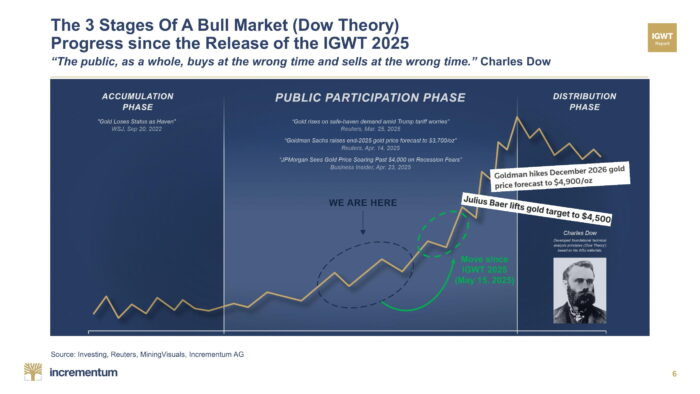

The violent October pullback rattled traders but didn’t touch the fundamentals. Our IGWT Chartbook shows that such corrections — even 20–40% in magnitude — are textbook behavior in long-term bull markets.

Moreover, Incrementum’s Active Aurum Signal shifted from Offensive to Neutral, reflecting technical overheating, but not a macro shift. Meanwhile, central banks continued buying, miners posted record margins, and bullion inventories stayed tight.

If a bull market rises in a straight line, it wouldn’t just be a bull market. Plainly, anyone would regard it as a bubble. Hence, corrections are a necessary, but painful condition for this Golden Decade to materialize.

The central point made by Ronnie is often misunderstood: the drivers of the gold bull market are structural, not political. Regardless of administration, inflationary pressures persist, debt grows faster than GDP, demographics worsen, and fiscal dominance forces central banks into increasingly reactive behavior. One of the conclusions we’d already taken from the IGWT 2025: politics changes the narrative, not the math. In fact, the world is in a permanent monetary transition, far beyond a mere inflation cycle.

All that is left is for investors, especially institutional and professional ones, to jump on the golden bandwagon. Sooner or later, it will happen, even though the scene looks gloomy right now.

Ronald-Peter Stöferle’s insights all converge on one unmistakable conclusion:

Central banks are accumulating gold at the fastest pace in modern history.

Governments are quietly reasserting control over private bullion.

Western institutional allocations remain far below equilibrium.

Silver is structurally undersupplied for the decade ahead.

Geopolitical fragmentation is accelerating the return to neutral, commodity-based collateral.

Having said this, the end of the bull market isn’t set. In any event, what we can assert is that this bull market is still in its participation phase. On this account, the mania stage is yet to arrive.

Speaking of manias, Michael Burry — the quintessential contrarian — has just closed his fund and publicly warned that the AI boom is unsustainable. His fund was revealed to be shorting the “hyperscalers” driving this cycle. In 2008, his early exit marked the top of the credit mania. In 2025, his exit may well mark the turning point of the AI bubble.

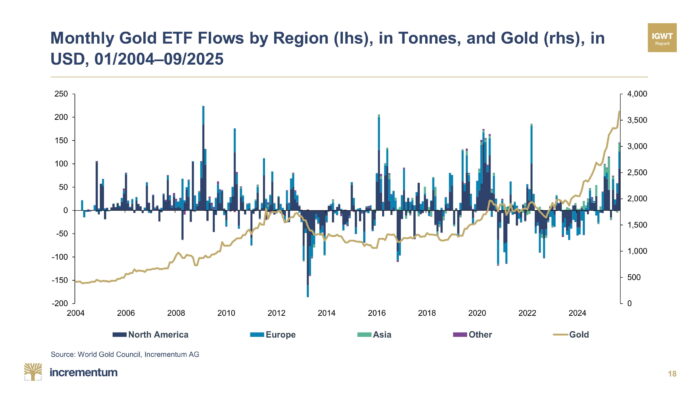

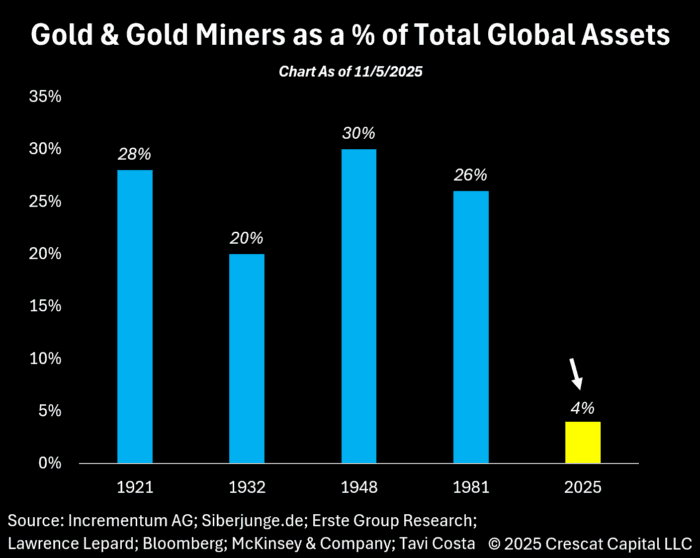

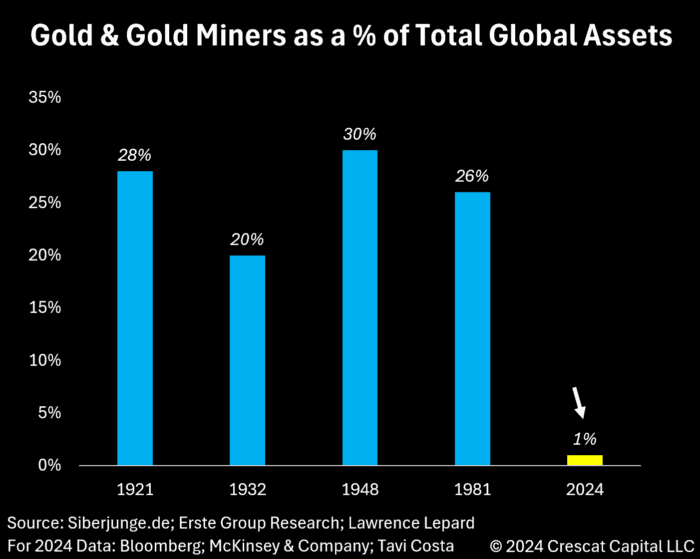

If the equity mania is peaking just as monetary instability deepens, the rotation into real assets will only accelerate. By the way, this was something recently flagged by Tavi Costa with the graph below; gold’s share is rising, albeit from a very low level.

Succintly, gold has proven to be, time and time again, that it’s not a barbarous relic. With the erosion of trust and uncertainty on the rise, gold is becoming the central piece of the next monetary system.

And the world is only beginning to position for it.

#GoldSurge #SilverRally #MiningStocks #SoundMoney #HardAssets #AlternativeAssets #FiatCurrencies #DeDollarization #FinancialRepression #DevelopedMarkets #EmergingMarkets #Geopolitics #Geoeconomics #FinancialSantions #TradeWar #EconomicStatecraft #CentralBanks #SafeHaven #PortfolioStrategy #GlobalTrade #Commodities #Inflation #MacroTrends #EconomicInsights #PortfolioStrategy #WealthManagement #TheBigLong #IGWT24 #IGWT25