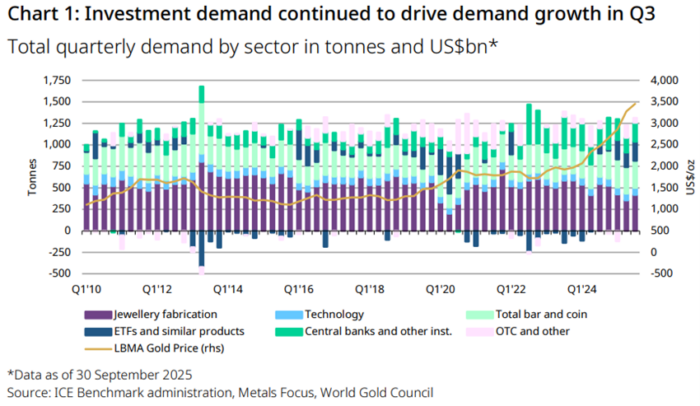

The WGC’s Q3 2025 report confirmed what many gold bulls suspected: global gold demand surged 3% year-over-year to 1,313 tonnes, the highest quarterly total in history. In terms of value, that equated to an astonishing USD 146 billion, up 44% year-over-year.

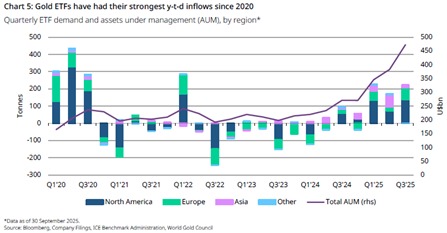

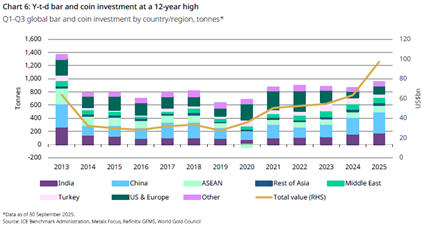

Undoubtedly, investment demand was the standout, rising 47% y/y, driven by 222 tonnes of ETF inflows and 316 tonnes of bar and coin buying, marking the fourth consecutive quarter above the 300-tonne level.

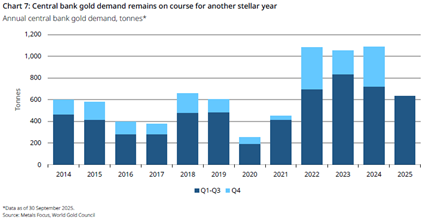

Meanwhile, central banks remained steadfast, purchasing 220 tonnes in Q3, being up 28% from Q2. Year-to-date, their buying totals 634 tonnes, which is slightly below 2024’s record pace, but still extraordinarily strong.

Remarkably, the LBMA gold price hit 13 new all-time highs, averaging USD 3,456/oz (+40% y/y, +5% q/q).

These figures reflect a world increasingly wary of paper promises. Arguably, gold is again reclaiming its role as real money.

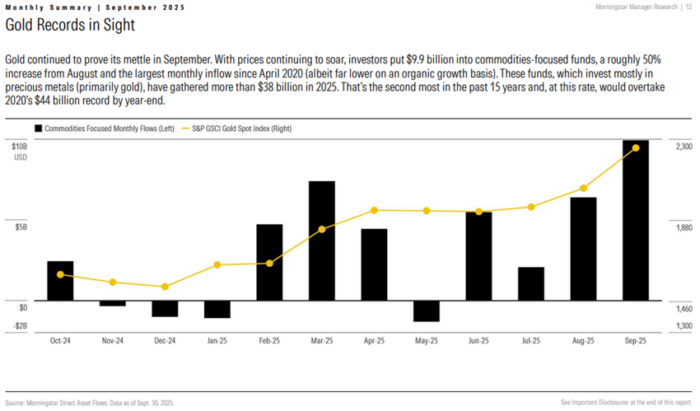

The WGC’s findings were echoed by Morningstar’s September 2025 Fund Flows Chartbook, which documented nearly USD 10 billion in inflows into commodities-focused funds, the largest since April 2020. Of these, gold-linked ETFs were the clear winners.

Investors poured money into “safe havens” — gold and bonds —, while withdrawing over USD 18 billion from U.S. equity funds in the same month.

This rotation was hardly random. Obviously, this was a reaction to a world of dovish central banks, mounting fiscal dominance, and political interference with the Federal Reserve. Add to that the re-escalation of the US-China trade war, and it’s no wonder investors began to see that the fiat monetary system is running on fumes.

Although it took a while for markets to wake up, it’s still better late than never.

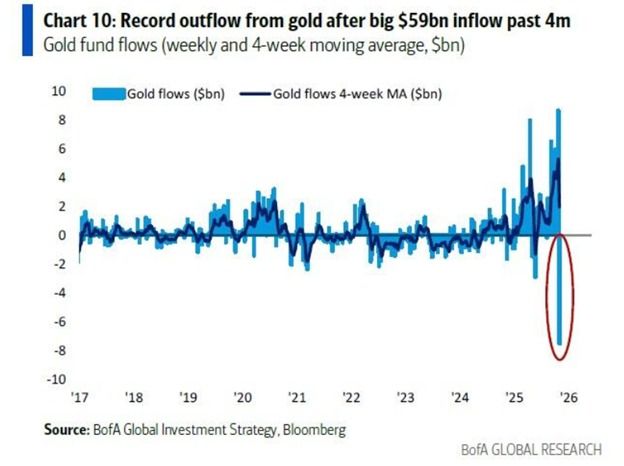

However, since the beginning of Q4 2025, the tone has shifted sharply.

After gold’s parabolic rally through the onset of October, technical indicators signaled an overbought market. Many traders, particularly in ETFs and futures, took profits. The result? A massive sell-off that pushed gold and silver prices down by roughly 11% from their peaks.

Despite this correction may feel dramatic, as we showed in the In Gold We Trust 2025 report, and then reminded again in the IGWT Chartbook 2025, even 20–40% pullbacks are normal within long-term bull markets.

In short, the euphoria has faded, and speculators have been shaken out. Most importantly, though, the underlying fundamentals remain as robust as ever.

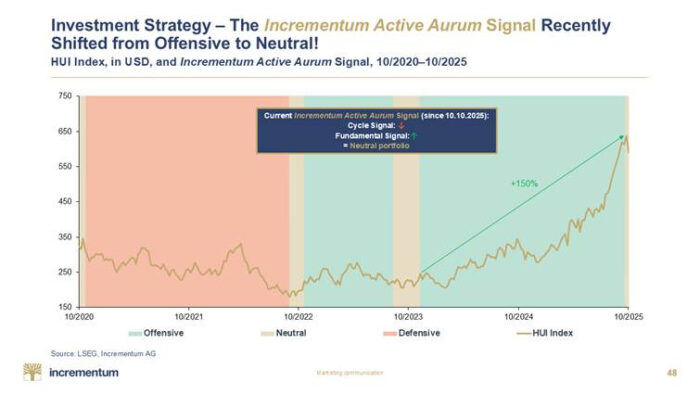

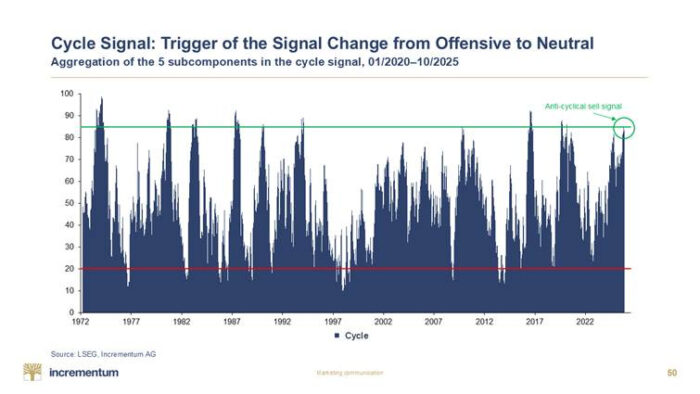

As noted in The Big Long: The Pause That Strengthens the Climb, our Incrementum Active Aurum Signal shifted from Offensive to Neutral on October 10, 2025, as our Cycle Signal spiked above 85. This represents an overheating threshold, historically consistent with mid-cycle pauses.

Instead of a sell signal, this is a call for discipline.

Needless to say, markets don’t sprint forever. Hence, this phase is what we call a re-accumulation window: a time for positioning, not panic. Usually, such pauses have been followed by renewed rallies once speculative froth clears.

Essentially, fundamentals remain overwhelmingly bullish:

Margins and free cash flow for miners are at record highs.

Central banks continue buying at record levels.

Real rates remain negative.

And fiscal dominance has eroded the last illusions of monetary restraint.

Just last week, we covered these dynamics in our article, The Great Silver Squeeze of October 2025, where we explained how structural deficits and industrial demand drove silver to historic highs above USD 50/oz.

Since then, the frenzy has cooled, though the setup remains powerful. Zooming in, industrial and investment demand are still outrunning supply, and our friend Ted Butler wrote in his Substack article Silver’s Golden Moment Has Arrived, the structural underpinnings of the silver bull market are intact.

Thus, another squeeze may well be on the horizon.

Simply put, corrections test conviction.

Definitely, the long-term thesis for precious metals — gold, silver, and miners — has never been stronger. To wit, central banks are diversifying away from the dollar, governments are trapped in debt, and investors are awakening to the silent debasement of fiat money.

This Golden Decade is only halfway through, and history suggests there will be many more rallies — and yes, some hair-raising corrections — along the way. In truth, those who view volatility as opportunity, rather than danger, will emerge the strongest.

At Incrementum AG, we believe that the current consolidation is a welcome pause, being merely a chance to catch the breath before the next ascent.

The World Gold Council’s Q3 2025 report may have marked the crescendo of this phase, but it also reinforces one timeless truth: gold remains the mirror of monetary excess.

When confidence in paper fades, gold doesn’t just shine, it dominates.

As the dust settles from October’s sell-off, our stance remains clear:

All in all, the end of the bull market is not even appearing on the horizon. In fact, this is the pause that strengthens the climb.

#GoldInvesting #GoldSurge #SilverRally #PreciousMetals #MiningStocks #Commodities #GoldETFs #FundFlows #MarketTrends #CentralBanks #MonetaryPolicy #SafeHaven #DebasementTrade #Dedollarization #DebtGrowth #GlobalTrade #Protectionism #Geopolitics #Geoeconomics #MarketCorrection #InvestmentInsights #FinancialMarkets #MarketAnalysis #PortfolioStrategy #WealthManagement #IGWT25