In Bitcoin We Trust?

“Spend some time with Bitcoin. Learn it, challenge it, and use it. You can assume no government wants you adopting this system in any capacity, and for that reason alone it’s worth consideration by honest, moral, and industrious people.”

Erik Voorhees

Key Takeaways

- Bitcoin and cryptocurrencies may become an integral part of wealth management from the perspective of portfolio diversification.

- Bitcoin represents an entirely different asset class, with different risks and different benefits. The correlation between gold and Bitcoin has been low and slightly negative.

- Ambiguity aversion may be negatively biasing the price of bitcoin downwards. As time passes, uncertainty and the subsequent

- discount it wields on the price of bitcoin should decrease.

We want to sincerely thank Demelza Hays for contributing this chapter.

Biography of Demelza: Demelza Hays is a blockchain researcher at the Centre for Global Finance and Technology at the Imperial College in London, and she operates the only Bitcoin ATM in Liechtenstein. At the University of Liechtenstein, Demelza is completing her doctoral thesis on the role of cryptocurrency in asset management, and she teaches a course for bachelors and masters students on Bitcoin and the Blockchain technology. In partnership with Incrementum, Demelza is working on cryptocurrency research and a bitcoin-based investment fund.

After being ridiculed as money for computer nerds and a conduit for illegal activity, investors are finally beginning to take notice of bitcoin[1] and the underlying technology, the blockchain.[2] After 20 years of failed attempts at making a private virtual currency, Bitcoin emerged triumphantly out of the 2007/08 global banking crisis. The creator of Bitcoin, who is still unknown but goes by the pseudonym Satoshi Nakamoto, was determined to provide a decentralized, private, and secure means of transferring value online that did not rely on trusting sovereign entities, central banks, or financial intermediaries.[3] Although Bitcoin and the underlying blockchain were originally designed to replicate the traits of gold that make it uniquely suited to be money, Bitcoin represents a unique asset class and can be an integral part of wealth management from the perspective of portfolio diversification.

a. To Bitcoin or Not to Bitcoin?

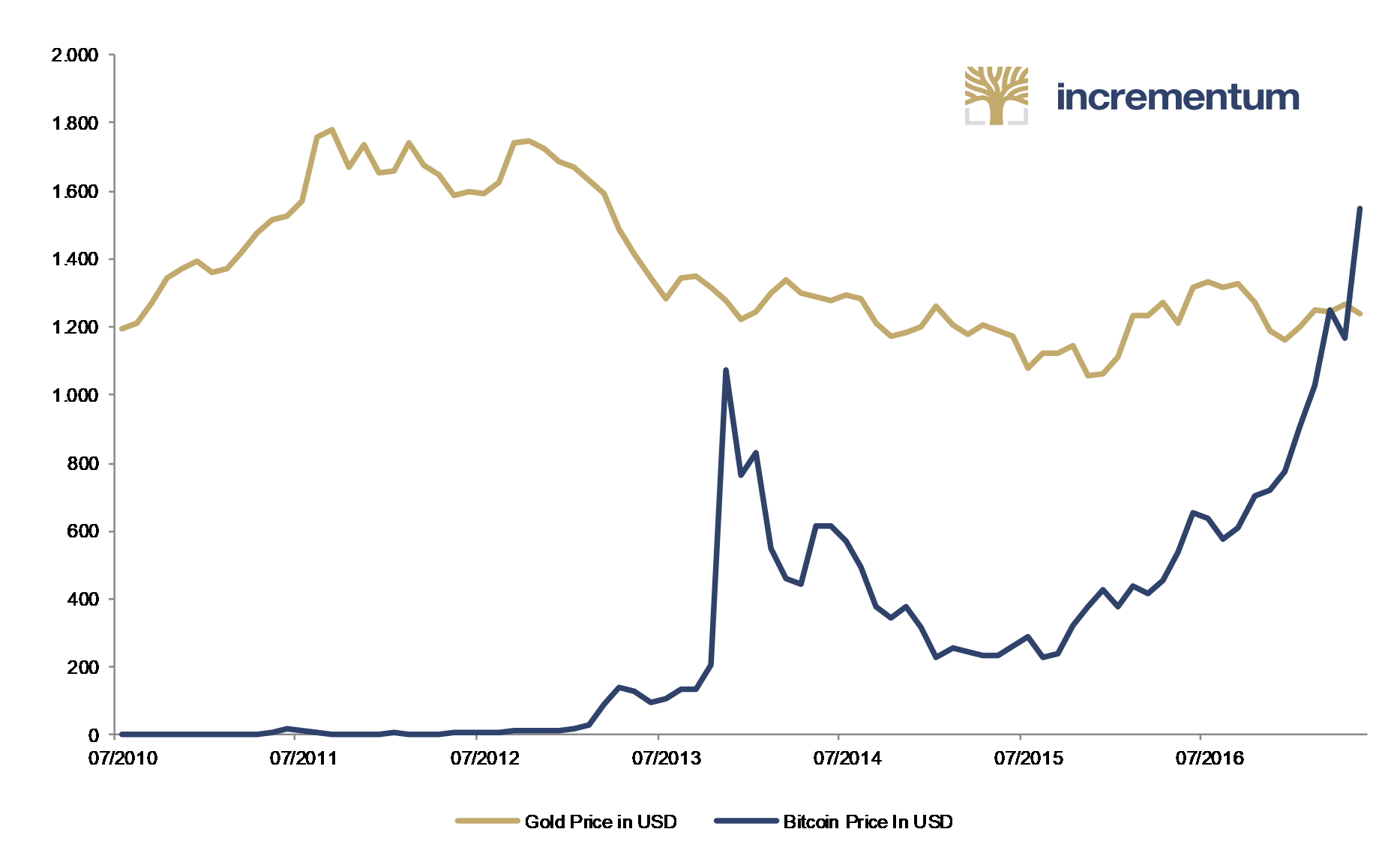

Two years ago, Bitcoin was considered a fringe technology for libertarians and computer geeks. Now, Bitcoin and other cryptocurrencies, such as Ethereum, are gaining mainstream adoption. Bitcoin’s market capitalization of $36 billion has already surpassed the market cap of several fiat currencies such as Icelandic krónas and Guatemalan quetzals. In March of 2017, the price of bitcoin soared above the price of an ounce of gold for the first time. While gold was trading around $1,225, bitcoin jumped up to $1290.

In May, the price of bitcoin breached €2,400. However, as I wrote in Forbes Austria , comparing gold and bitcoin is akin to comparing apples and oranges. Gold is measured in weight, whereas bitcoin is only measured in bitcoin.[1] For example, the price of one bitcoin surpassed the price of a gram of gold in 2011. However, the price of bitcoin has not surpassed the price of one ton of gold. Not yet at least.

Exchange Rates of Gold and Bitcoin against USD (Monthly Averages)

Sources: Quandl.com, Demelza Hays, Incrementum AG

The price of bitcoin is determined in the same way as the price of all other goods: by the forces of supply and demand. However, bitcoin’s limited supply means that changes in demand directly impact the price, and as can be seen by the price of bitcoin, demand has been growing substantially. Demand is growing for two main reasons. Fundamentally, the technology provides a useful service to users who want to trade value across the world without an intermediary. Bitcoin transactions can be sent at any time of day, to any place in the world, for a transaction fee ranging from $0.00 to $0.40 regardless of the transaction size. Bitcoin’s growing popularity as a payment system can be seen by the increasing number of transactions. Every day, approximately 315,000 transactions occur worldwide with a volume of roughly $100 million.

Secondly, speculators are buying bitcoin in hopes of profiting from price fluctuations. However, the recent price hike to more than €2,400 per bitcoin has left investors wondering if it is too late to get in on the action. Despite the strong growth in the price, exposure to Bitcoin is still a good decision in 2017.

- New Asset Class – Bitcoin represents a distinct asset class with unique fundamental and statistical characteristics. ARK Invest has outlined 4 main reasons that Bitcoin provides portfolio diversification: investability, politico-economic features, correlation of returns, and the risk-reward profile.[5] Although only a limited amount of data is available, the historic prices of bitcoin have a low correlation with other asset classes. As stylized by Burton Gordon Malkiel in his fantastic book “Random Walk Down Wall Street”, adding an asset class with a low correlation with the other portfolio holdings can minimize the downside risk of the overall allocation.

- Ambiguity Aversion – Bitcoin is so young and nobody knows exactly how this invention will impact the world. Bitcoin’s price data only covers the past six years, which means there is basically no data available for statistical analysis. The Ellsberg paradox shows that people prefer outcomes with known probability distributions compared to outcomes where the probabilities are unknown.[6] The estimation error associated with forecasts of bitcoin’s risks and returns may be negatively biasing the price downward. As time passes, people will become more “experienced” with bitcoin, which may reduce uncertainty and the subsequent discount it wields on the price of bitcoin.

- Big Investors – Bitcoin has a positive feedback loop. The more people that use bitcoin, the more valuable each Bitcoin is, which makes more people want to use it. In 2014, the New York Stock Exchange (NYSE) invested in the U.S. based bitcoin exchange, Coinbase. In 2015, the NYSE launched the Bitcoin Investment Trust that enabled IRA and Roth IRA investments. In 2016, over ten universities, including Stanford and Princeton, offered courses specifically on Bitcoin. In addition to compelling historical price data, the future prospects look encouraging. New business models, such as bitcoin banks, brokers, and custodians are being developed that enhance Bitcoin’s user experience and popularity.

- Negative interest rates – Hostility from government and banks towards bitcoin underscores the value of this technology. The ECB is printing €60bn per month and shows no sign of abatement. The ECB’s deposit rate of -0.4pc is effectively a tax on storing your money in a bank. The SNB is following suit in order to prop up Swiss exports to the Eurozone. Bitcoin provides an alternative to inflationary fiat currencies that incur fees for fractional reserve storage. Bitcoin’s total supply is fixed to 21 million and can be stored for free.

- Cashless Society – We are slowly moving towards a cashless society. The majority of fiat currency only exists digitally. As governments demonetize physical bills, more transactions will be made digitally. Bitcoin presents an alternative to credit card companies and banks that are frequently hacked, charge high fees, and freeze accounts. Offline or “cold” bitcoin wallets are protected by military grade cryptography and require no fees or paperwork.

b. Bitcoin – Digital Gold or Fool’s Gold?

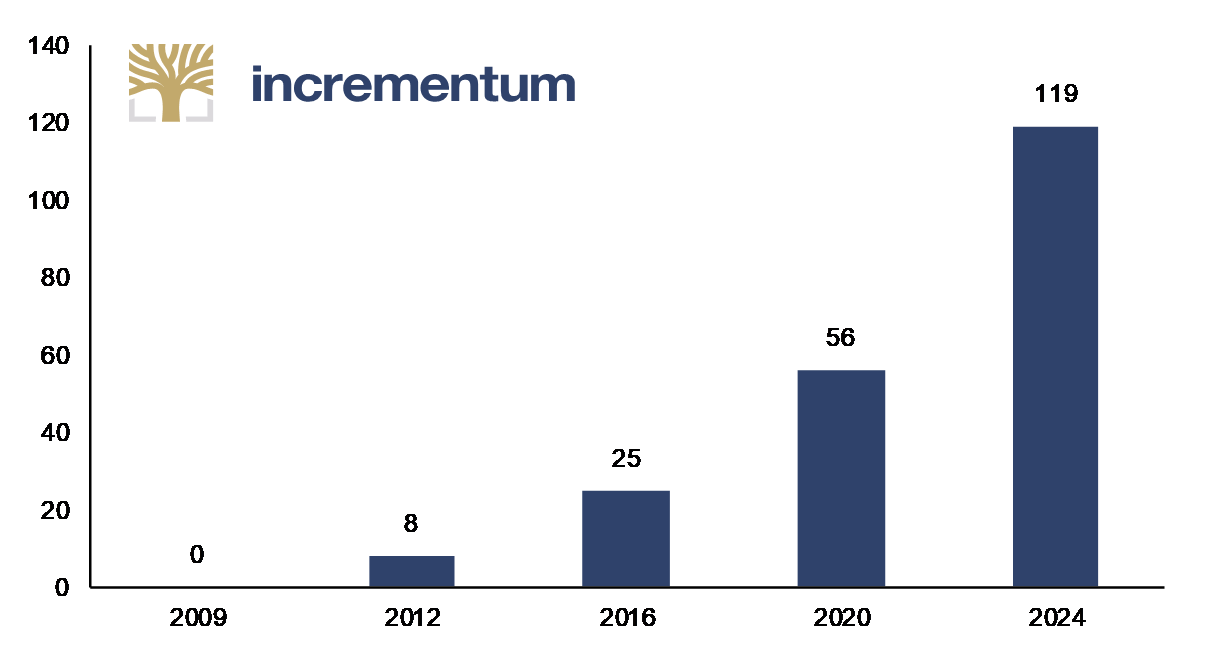

Like bitcoin, gold also provides protection from negative interest rates and fiat demonetization. Importantly, the stock to flow ratio (StFR) of bitcoin is similar to gold’s. Gold has a StFR of approximately 64 years, while bitcoin’s is approximately 25 years. The entire amount of bitcoin ever mined totals approximately 16.32 million. That is the stock. Every ten minutes, the network mints 12.5 new bitcoins. Therefore, there is a daily inflation of 1800 new coins. In 2017, annual production will be approximately 657,000 bitcoin. That is the flow. By dividing the stock by the flow, we can see that bitcoin’s StFR is lower than gold’s. The StFR shows that a large gap exists between the annual production of bitcoin and total supply available. Not only is bitcoin scarce but also the available stock is relatively constant over time, which generates confidence in the money.

The StFR of bitcoin is expected to rise further over time because every four years the amount of bitcoin minted every is halved. The last programmed “halving” occurred in June of 2016. Therefore, the next halving will occur in 2020. At this time, the StFR ratio will increase to approximately 56 years.[7] The StFR of bitcoin should surpass gold’s during the next five years. Figure 2 below shows the stock flow ratio of bitcoin over time. Prior to January 3, 2009, no bitcoin existed. Therefore, the stock to flow ratio was effectively zero. However, the rapid reduction in the amount of bitcoin mining over time is increasing the StFR. By 2024, only 3.125 bitcoin will be mined every ten minutes resulting in a StFR of approximately 119 years.

Bitcoin’s Stock to Flow Ratio

Source: Demelza Hays, Incrementum AG

The inverse of this calculation, the inflation rate, shows that the stock of bitcoin is being increased by approximately 4% annually. The supply of newly minted bitcoin follows a predictable inflation rate. Satoshi modeled the flow of new bitcoin as a Poisson process[8], which will result in a discernible inflation rate compared to the stock of existing bitcoin by 2020.

The low and steady inflation rate of bitcoin is one of the most attractive features of this experiment in monetary technology. Like gold, decisions concerning the issuance of money and control of the money supply are not left in the hands of fallible humans. Bitcoin transfers this responsibility from humans to computers whereas gold relies on nature. Algorithmic or programmable money takes passive “digital money”[9] controlled by banks and governments and makes it active “virtual currency”[10] that is controlled by software protocols and cryptographic algorithms that are inherent to the currency itself.[11]

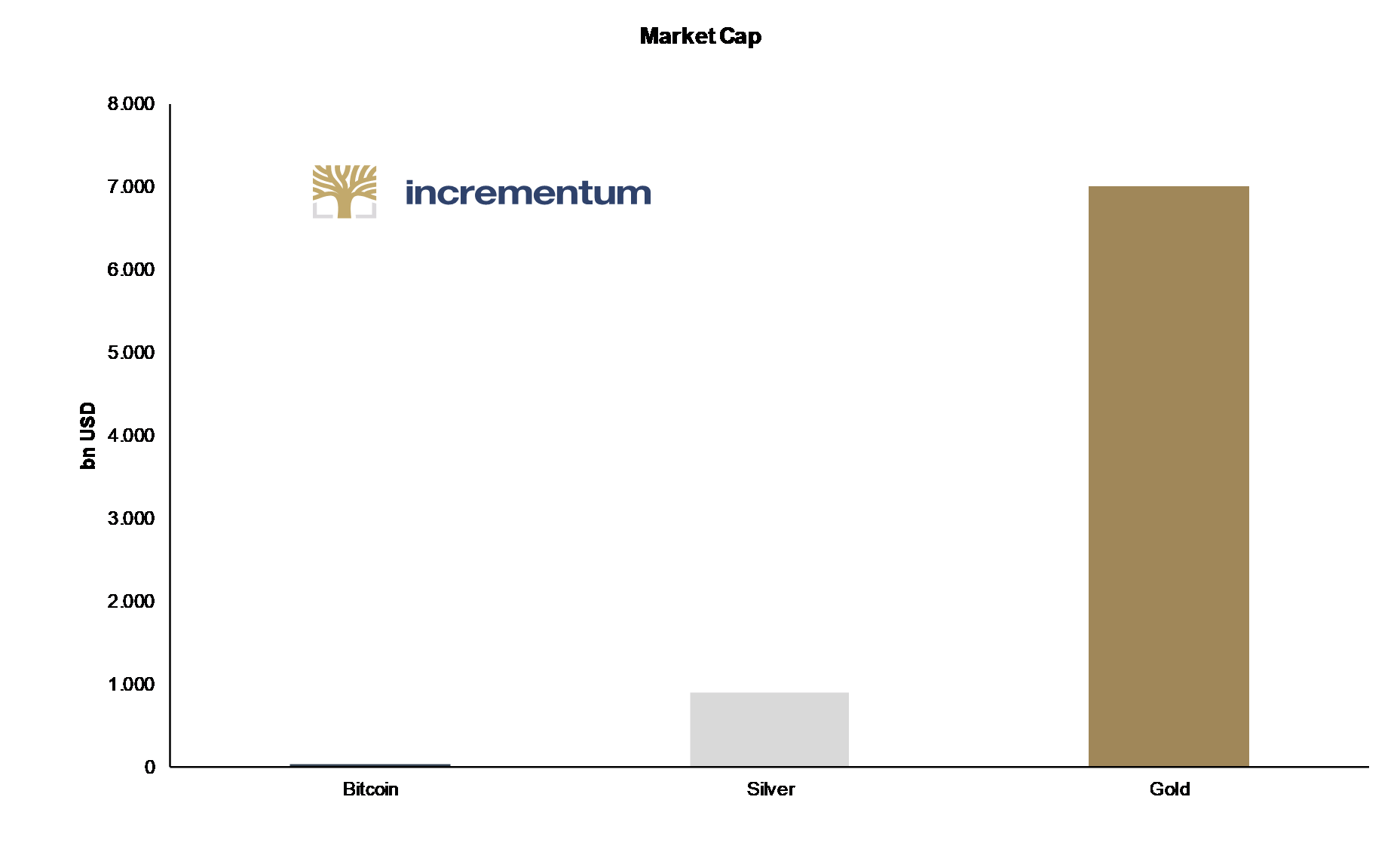

However, gold’s market capitalization of $7 trillion puts bitcoin’s market cap of $66 billion into perspective. The next chart shows the market caps of gold, silver, and bitcoin. Although, bitcoin’s market cap has been rallying, it is still a mere 0.5% of golds market capitalization.

Market Capitalization: Bitcoin, Silver, Gold (bn. USD)

Source: Demelza Hays, Incrementum AG

As money, bitcoin has three main advantages and four main disadvantages in comparison to gold.

Bitcoin’s Pluses:

- Fast clearance and settlement of transactions – Bitcoin offers immediate clearance because anyone can make an account at any time without any identification documents. Today, over 125,000 merchants worldwide accept bitcoin. In contrast, a Google search for merchants that accept gold as payment leads you to a few dusty goldbug forums that discuss ways to make gold great again.

- Low shipping costs – Transaction fees for “shipping” bitcoin from one account holder to another ranges from free to forty cents regardless of the amount of bitcoin being sent. What matters for a payment network and a medium of exchange is how quickly you can put the media to use. In this sense, gold is slow money. The physical aspect of gold is great, until you try to stuff it into your USB port in order to send it to someone across the globe.

- Low storage costs – Storing bitcoin amounts to storing a large string of numbers that represent digital data. Online, paper, and brain wallets are completely free of charge. Hardware wallets can range from €15 to €240; however, this is often a fraction of the cost of storing physical gold.

Bitcoin’s Drawbacks:

- Risk of a 51 percent attack – This is when one miner, a group of miners, or a mining pool gains a majority of the power on the network. Volatility in the price of bitcoin during the past few weeks has stemmed from this risk. A bitcoin miner is an individual or group of people that run a version of the Bitcoin software on a hardware device specifically designed for mining bitcoin called an application-specific integrated circuit (ASIC). Mining is the process of adding new transactions to the Bitcoin database of previous transactions. The debate between big blockers from the Bitcoin Unlimited (BU) camp and little blockers from the segregated witness (SegWit) camp amounts to what version of the Bitcoin software should be run on the hardware devices. The most popular software being run by miners, Bitcoin Core, has a data cap of 1 MB per block of transactions. A new block of transactions is mined approximately every 10 minutes, which equates to a limit on the new data that the network can record of 1 MB every ten minutes. The BU miners want to raise this limit while the SegWit camps wants to decrease the data size of each transaction. The president of the largest Bitcoin mining pool, who is a proponent of Bitcoin Unlimited, threatened that “… [a 51%] attack it is always an option.”[12]

- Risk of altcoins taking market share – Cryptocurrencies, like Bitcoin and Ethereum, embody the 20th century economist Friedrich von Hayek’s dream of privately competing currencies.[13] Over 1,000 new cryptocurrencies have been invented since Bitcoin’s inception. Each new coin promises to improve over bitcoin in one way or another. However, none have been able to surpass bitcoin (yet). Computers advanced from ENIACs in the 1950s to laptops in the early 2000s to Raspberry Pi’s that cost $5 and fit in the palm of your hand. The Bitcoin blockchain is a slow energy hogging database, and entrepreneurs from around the world are vying to make a coin that can steal bitcoin’s market share. The market will choose the winners and losers.

- Risk of changes in regulations – In Europe and in the US, the regulatory outlook is bleak. In spring, the SEC rejected the Winklevoss Bitcoin ETF, and the European Union’s 4th Anti-Money Laundering Directive (AMLD) argues for stricter monitoring of cryptocurrency users, miners, exchanges and wallet providers.

- Reliance on internet, electricity, and hardware devices – Without internet, the speed of broadcasting a transaction to all of the nodes across the network would decline steeply. The increased latency would result in more forks of the Bitcoin network because miners would build blocks with an incomplete list of recent transactions. Similarly, Bitcoin’s proof-of-work mining is estimated to cost $400 million in electricity and hardware per year.[14]

Conclusion

Overall, Bitcoin and gold represent two distinct asset classes – and should be treated as such by investors. The medium-term outlook for both of these classes is positive because they are both deflationary monies that allow investors to counter expansionary fiat currencies and artificially low interest rates. Future generations may store gold while employing a cryptocurrency as a medium of exchange or cryptocurrency may even replace gold as the best vehicle for wealth accumulation if debasement or expropriation of gold becomes widespread. However, buyers beware: A growing body of academic research recommends 2-4 percent of a diversified portfolio should be in Bitcoin[15] compared to up to 20 percent that may be invested in gold. Bitcoin faces several hurdles; however, this nascent technology may provide a glimpse of what will eclipse our current system of fiat currencies.

At Incrementum, our interest in bitcoin and cryptocurrencies has evolved from a mere curiosity to a legitimate investment case. Due to the lack of institutional grade investment vehicles for bitcoin, Incrementum has begun working on a cryptocurrency investment fund. Official news about the cryptofund is expected to be released in the third quarter.

[1] The concept of Bitcoin is written with a capital B while bitcoin, with a lower-case “b” refers to the monetary unit. Therefore, bitcoin is the cryptocurrency used on the Bitcoin network.

[2] Also referred to as the distributed ledger technology (DLT)

[3] Stephanie Lo & J Christina Wang, Currency Policy Perspectives: Bitcoin as Money?, 14-4 FED. RESERVE BANK OF Bos. 2 (Sept. 4, 2014), http://www.bostonfed.org/economic/currentpolicyperspectives/2014/cppl404.pdf.

[4] Wieler. (2017). Goldmoney.com

[5] Burniske/White. 2017. Bitcoin: Ringing the Bell for a New Asset Class.

[6] As noted by John Maynard Keynes (1921), and later Daniel Ellsberg (1961), the Ellsberg Paradox describes a situation in which people prefer to bet on the outcome with a high level of known risk compared to an unknown risk.

[7] 18, 279,000 stock divided by 328500 flow in 2020.

[8] https://en.wikipedia.org/wiki/Poisson_point_process

[9] “Digital money is electronic money or in other words so called fiat money stored electronically i.e. money in bank accounts in various currencies like Swiss Francs, US Dollars, Euros, etc, used to make payments. When you pay cash into your bank account it becomes digital (electronic) money for you.” Kremeth. 2016. Incrementum.

[10] According to the ECB virtual currencies, such as bitcoin, are, “a type of unregulated, digital money, which is issued and usually controlled by its developers, and used and accepted among the members of a specific virtual community.” European Central Bank. 2012. Virtual Currency Schemes.

[11] King. 2016. On the Use of Computer Programs as Money.

[12] Shin. 2017. “Is This Massive Power Struggle About To Blow Up Bitcoin?” Forbes.

[13] Hayek. 1978. Denationalization of Money: The Argument Refined. London: Inst. of Economic Affairs. Print.

[14] Aste. 2016. The Fair Cost of Bitcoin Proof of Work.

[15] Hong. 2016. Bitcoin as an alternative investment vehicle; Brière, Oosterlinck, & Szafarz. 2013. Virtual Currency, Tangible Return: Portfolio Diversification with Bitcoin; Pandey. 2014. The Value of Bitcoin in enhancing the efficiency of an investor’s portfolio.