October 9, 2025, will go down as one of the most memorable days in the history of precious metals. On that day, silver broke its 1980 price record, touching a new all-time high above USD 50 per ounce and briefly peaking near USD 56. More than a speculative surge, this rally was the culmination of years of mounting structural imbalances finally boiling over.

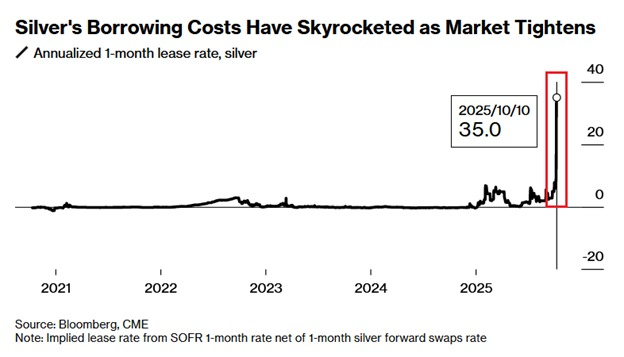

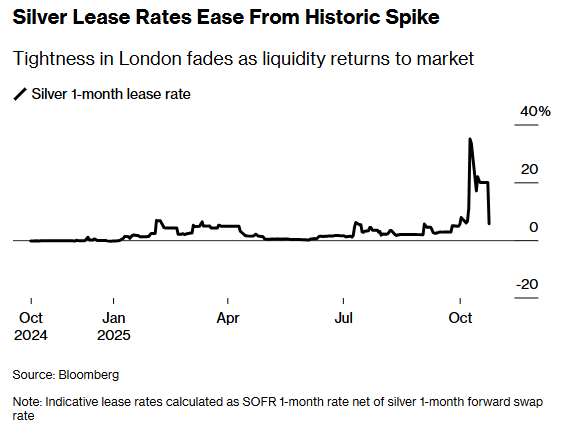

In the same fateful session, the 1-month silver lease rate in London skyrocketed to 39%, signaling extreme scarcity. For perspective, that figure is roughly seven times higher than typical levels, and as Bloomberg reported earlier this week, such rates “signaled panic and acute scarcity” before easing back toward 5.6% as liquidity returned.

Was it coincidence that record prices and record lease rates occurred on the same day? Hardly. This was a textbook short squeeze driven by a physical shortage of metal rather than speculative hype.

According to The Great Silver Shortage: How Bullion Banks Are Navigating a Perfect Storm, the roots of this crisis stretch back months. The U.S. trade war reignited under the Trump administration led to a reconfiguration of global bullion flows. As tariffs and logistical bottlenecks hit Swiss refiners and London vaults, enormous quantities of gold — and silver — were shipped from the London Bullion Market Association (LBMA) to New York’s COMEX.

This transatlantic drain left London’s silver liquidity threadbare. Meanwhile, relentless industrial demand and large speculative short positions on COMEX set the stage for a violent squeeze. As the spread between London spot and COMEX futures widened to more than USD 3 per ounce, traders resorted to airlifting metal across the Atlantic, which is a measure usually reserved for gold arbitrage.

The structural imbalance was unmistakable. By early October, COMEX silver inventories had logged their largest single-day withdrawal in four years, while LBMA holdings had fallen to their lowest level since recordkeeping began, at about 711 million ounces in April. Incredibly, this is nearly 400 million ounces below the 2021 peak.

At the same time, global silver production has been in deficit for five consecutive years, accumulating an estimated 800 million-ounce shortfall since 2021. With mine output stagnant and recycling flat, the physical market could no longer keep pace with industrial and investment demand.

The result? A market running on fumes — and a paper-based futures system suddenly exposed as fragile.

For decades, silver’s price discovery occurred on COMEX, where “paper silver” trading often overpowered real-world fundamentals. But in October 2025, that relationship flipped. Silver entered backwardation, meaning spot prices traded higher than futures. Unmistakably, this is a rare, but powerful signal that the physical market had seized control.

In practical terms, this meant futures traders could no longer dictate the price. Those short silver found themselves trapped: unable to borrow the metal at any reasonable cost and forced to buy back futures or acquire physical silver at elevated prices.

This squeeze on short positions triggered a self-reinforcing rally, pushing silver to its record high before easing once physical shipments from New York began replenishing London vaults.

Beneath the price fireworks lies a deeper story: the transformation of silver into a strategic industrial commodity.

As the In Gold We Trust 2025 report highlights, the solar sector consumed nearly 198 million ounces of silver in 2024, thanks to next-generation “TopCon” panels that use up to 40% more silver per unit. On top of that, solid-state batteries, aerospace systems, and defense electronics are becoming new engines of demand.

With industrial use increasingly inelastic — unable to fall even when prices rise — silver is no longer just a precious metal. It’s a core input in the global electrification and clean-energy revolution.

No squeeze story would be complete without India. In 2024, Indian imports of silver doubled from the previous year to 225 million ounces, and in 2025 they surged again. The timing was crucial: Dhanteras and Diwali celebrations in early October coincided with the height of the squeeze.

Reuters reported that Indian silver premiums and imports soared to record levels during the festival, only to cool sharply once festivities ended — a dynamic that helped ease the global shortage by late October. Indeed, as the celebrations wrapped up, silver lease rates fell back and the market returned to contango, signaling restored balance.

The Great Silver Squeeze wasn’t just about logistics. Although it’s too soon to tell, this episode may mark a seismic shift in how silver’s price is set. For years, the futures market’s dominance meant that price reflected leverage and speculation. October 2025 demonstrated the opposite: when real metal becomes scarce, physical demand dictates price.

In the end, this episode exposed the fragility of the bullion banking model, one that juggles massive synthetic exposures backed by limited physical reserves. The next time shortages reappear, the adjustment may be even more violent.

The dust is settling. Silver has retreated to the upper-USD 40s, lease rates have normalized, and arbitrage between London and New York has largely unwound. At any rate, the structural drivers — industrial demand, monetary uncertainty, and tightening supply — remain firmly in place.

Whether October 2025 proves to be a blow-off top or the opening act of a longer bull market will depend on how quickly inventories can rebuild, as well as whether global policymakers manage to avoid further disruptions to trade and supply chains.

Either way, the message is clear: the silver market is no longer a sleepy corner of the commodities world. It has become a battleground where physical reality trumps paper promises.

#SilverSqueeze #SilverRally #SilverDemand #PreciousMetals #BullionBanks #COMEX #LBMA #IndustrialMetals #Commodities #CriticalMinerals #EnergyTransition #Diwali2025 #FuturesMarket #FinancialMarkets #PriceArbitrage #SoundMoney #EconomicShift #MarketTrends #TradeWar #Protectionism #Geoeconomics #IGWT25