After months of speculation, only two candidates remain credible:

Kevin Warsh 🎓 A former Federal Reserve Governor, Warsh brings deep institutional credibility. Since leaving the Fed, he has served as a distinguished visiting fellow at Stanford University’s Hoover Institution and as a lecturer at Stanford’s Graduate School of Business. His experience inside the Fed gives him instant legitimacy with markets and foreign central banks.

Kevin Hassett 📊 Currently the Director of the National Economic Council, Hassett is one of President Donald Trump’s closest economic advisors. Like Warsh, he is also a distinguished visiting fellow at the Hoover Institution. His proximity to the president initially made him the clear market favorite to succeed Powell.

For a while, the consensus view was simple: Hassett was the frontrunner.

The backdrop to this leadership decision is a pivotal Federal Open Market Committee meeting.

On December 10, 2025, the Fed:

Cut the federal funds rate by 25 basis points, bringing the target range to 3.5%–3.75%.

Announced the resumption of USD 40 billion in Treasury securities purchases, starting December 12, with elevated buying expected for several months.

Delivered a 9–3 vote, revealing notable internal divisions.

The dissenters were telling:

Governor Stephen Miran, author of the so-called Mar-a-Lago Accord framework, dissented in favor of a larger 50 bp cut.

Chicago Fed President Austan Goolsbee and Kansas City Fed President Jeffrey Schmid dissented in the opposite direction, opposing any rate cut at all.

Despite the easing, Chair Jerome Powell struck a cautious tone, emphasizing a “wait-and-see” approach and signaling that further cuts may be hard to justify in the near term. For President Trump, that stance reinforced a long-held view: Powell is simply too hawkish.

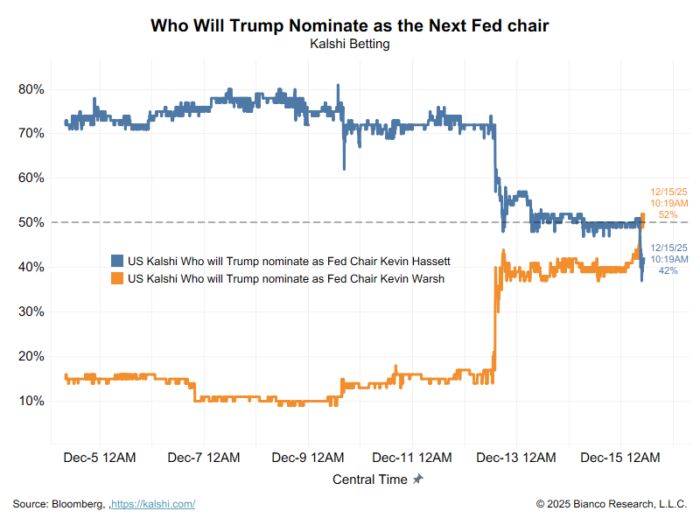

Kevin Hassett’s candidacy, once viewed as almost inevitable, has recently encountered resistance.

According to multiple reports, high-level figures close to President Trump have raised concerns that Hassett may be too close to the president. Ironically, this closeness – initially his biggest advantage – has become a liability. The fear is straightforward: bond markets could revolt if investors conclude that a Hassett-led Fed would lack sufficient independence.

The risk? Rising long-term yields driven by doubts about the Fed’s willingness to fight inflation if price pressures return. Hassett has publicly pushed back on this narrative, insisting that Fed independence would not be compromised under his leadership.

Against this backdrop, Kevin Warsh has surged ahead in prediction markets, including Kalshi. President Trump himself surprised investors on December 12 by telling The Wall Street Journal that Warsh had moved to the top tier of candidates alongside Hassett.

Warsh’s appeal is clear:

He is aligned with Trump politically, but

less exposed to accusations of being a White House proxy.

For markets sensitive to credibility, optics matter. Hence, Warsh’s Fed pedigree counts.

As discussed in depth in this year’s In Gold We Trust report, the Trump administration appears sympathetic to Stephen Miran’s Mar-a-Lago Accord concept. In this framework, fiscal policy takes primacy over monetary policy, with the Fed playing a more supportive role in a broader economic strategy.

Here’s the key constraint: No Fed Chair – Warsh or Hassett – can unilaterally make that vision a reality.

The Fed’s dual mandate, governance structure, and operational independence are all creatures of Congress. While the Supreme Court has reinforced the Fed’s unique legal status – protecting governors from removal except “for cause” – Congress ultimately holds the power to revise the Fed’s mandate or structure.

Although such changes are possible, they are politically difficult, given longstanding bipartisan support for central bank independence.

For decades, mainstream economics has treated central banks, especially the Federal Reserve, as near-omnipotent institutions. In this view, policymakers can fine-tune the economy almost at will: raise or cut interest rates to steer growth, expand or contract the money supply to tame inflation, and stabilize markets whenever turbulence appears. However, reality is far less flattering.

In truth, central banks do not directly control the economy. In spite of controlling administered rates (such as the policy rate) and influence liquidity conditions, the transmission from these levers to real economic outcomes is indirect, lagged, and highly uncertain.

Let’s consider interest rates. The Fed sets the federal funds target range, but:

Long-term yields are largely determined by bond markets, inflation expectations, and fiscal credibility.

Credit creation depends primarily on private banks’ willingness to lend and borrowers’ willingness to take on debt—not on policy rates alone.

Likewise, “money printing” is widely misunderstood. Plainly, central bank balance sheet expansion creates bank reserves, not spendable money in the real economy. Whether those reserves translate into broader money growth depends on:

Bank capital constraints

Regulatory frameworks

Risk appetite

Demand for credit

This is precisely why massive quantitative easing after 2008 coexisted with subdued consumer-price inflation for years, in addition to why inflation later surged once fiscal policy, supply shocks, and credit dynamics aligned. Naturally, helicopter money came from governments, not central banks.

In short, central banks react far more than they command. They respond to:

Fiscal dominance and exploding public debt

Demographic headwinds

Global capital flows

Geopolitical fragmentation

Market-imposed constraints

Inasmuch as there’s a growing reliance on phrases like “data dependence,” “scenario analysis,” and “wait and see”, this is an implicit admission of limited control by central bankers. Certainly, it’s not an expression of humility.

This matters enormously for the Fed chair debate. No matter whether the next chair is Kevin Warsh or Kevin Hassett, expectations that a single individual can engineer growth, suppress yields, or permanently control inflation are misplaced. The era of effortless monetary management is over – that is, if there ever was one.

Despite the race between Kevin Warsh and Kevin Hassett being undeniably important, it should not be misunderstood. While both men are allies of President Trump and perceived as more hawkish than Jerome Powell, neither would inherit an all-powerful institution capable of bending the economy to political will.

Undoubtedly, the Federal Reserve today operates under binding constraints:

Heavy fiscal dominance

Market-driven long-term rates

Structural inflation volatility

Global capital mobility

Legal and institutional limits imposed by Congress

Replacing Powell may change the tone of monetary policy, but not its underlying reality. Implementing a vision akin to the Mar-a-Lago Accord would require legislative action, not merely a new chair. Evidently, it’s Congress, not the Fed, that ultimately defines the central bank’s mandate, structure, and authority.

The deeper takeaway is this: central banks are far less powerful than commonly believed, yet more politically exposed than ever.

Importantly, markets are slowly recognizing that monetary policy cannot offset structural imbalances indefinitely. As this realization spreads, confidence – not rates alone – will become the decisive variable. Obviously, that has profound implications not only for bonds and currencies, but also for assets that exist outside the discretionary control of central banks.

In that sense, the Kevin vs. Kevin contest is less about who controls the Fed and more about how much control the Fed truly has left. When will the markets peek behind the curtain and realize these monetary wizards are merely illusionists?

#FederalReserve #FedChair #MonetaryPolicy #FOMC #InterestRates #HawkishCut #HawksVsDoves #TrumpEconomy #FedIndependence #BondMarkets #MarALagoAccord #CentralBanking #MacroEconomics #Keynesianism #QuantitativeEasing #AssetPurchases #MoneySupply #MonetaryReserves #Inflation #EconomicStatecraft #GrandStrategy #FinancialRepression #ExpectationManagement