On November 14, 2025, the Financial Times confirmed what attentive observers have long suspected: China’s official gold reporting dramatically understates its real accumulation. Analysts cited in the article argue that China may be buying over ten times more gold than its public disclosures suggest, a conclusion drawn from trade data, refining flows, and import patterns.

This aligns with the work of gold analyst Jan Nieuwenhuijs, who for several years has argued that China routinely underreports its gold purchases. Nearly a year ago, Nieuwenhuijs estimated China’s true gold reserves at 5,000 tonnes, far above its officially communicated holdings, and which would place the country second globally, only behind the US.

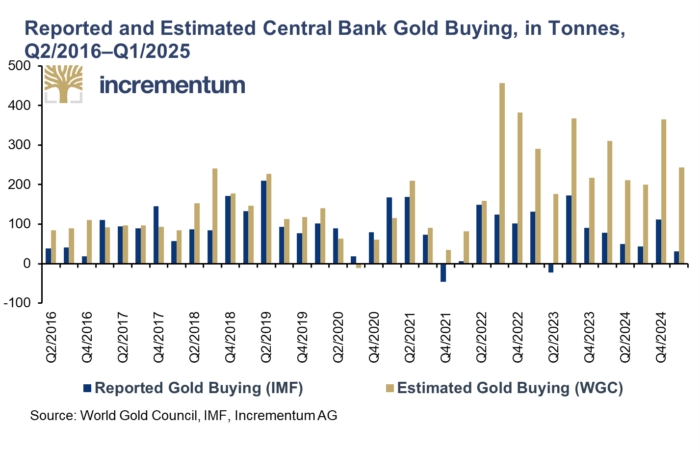

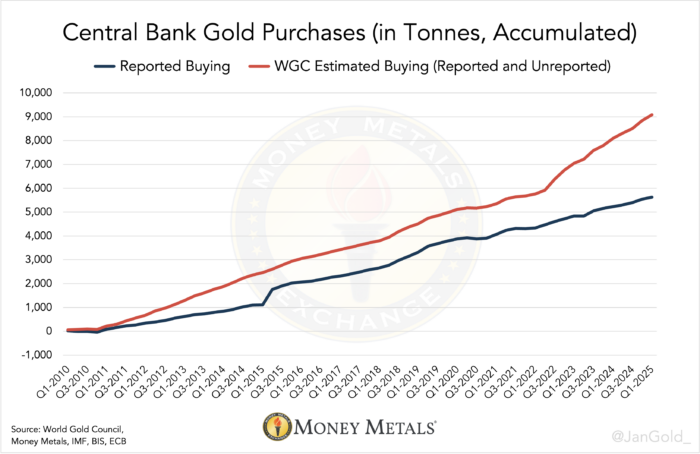

The FT’s reporting corroborates a pattern: in recent years, only one-third of global central bank gold buying has been publicly reported, down from 90% four years earlier. China is the least transparent major buyer, with purchases often attributed to the PBoC, SAFE, sovereign wealth funds, and even the military; all entities that do not provide timely or complete disclosures.

All the same, it’s not just the FT that’s paying attention. For the last two year, other news outlets have reported on this, like Bloomberg, and even Goldman Sachs has began inspecting the covert Chinese gold acquisitions, ending up with similar conclusions as Nieuwenhuijs.

This opacity significantly complicates price discovery. As the FT article notes, gold is uniquely hard to track because it leaves no satellite-visible footprints — no tanker shipments, no pipeline flows. Hence, analysts increasingly rely on “proxy indicators”, such as serialized 400-ounce bar movements through Swiss refineries and London vaults.

Moreover, the In Gold We Trust 2025 report showed that China has been among the largest annual buyers, contributing to global central bank purchases that reached a record 1,086 tonnes in 2024. The motivations include de-dollarization, geopolitical hedging, and a structural repositioning of national reserves, all accelerated by the West’s 2022 freezing of Russian FX reserves.

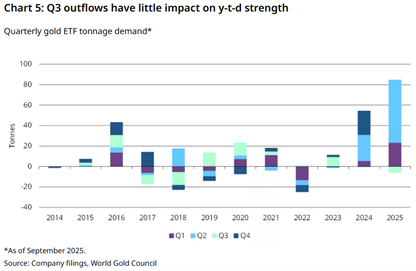

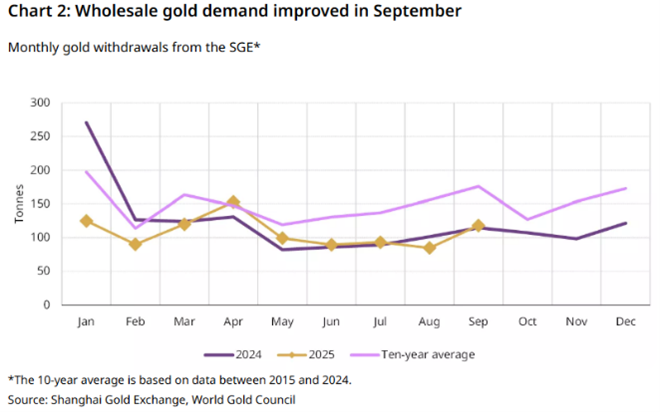

Beyond the official reserves, China’s private sector has also intensified gold accumulation. As the World Gold Council reveals, purchases of bars and coins remain strong, even as jewelry and industrial demand softened in 2024–25. As a result, the gold withdrawals from the Shanghai Gold Exchange (SGE) have been lower than the norm of previous years.

On the flip side, investment demand has been driven by concerns over trade tensions, property market weakness, and geopolitical instability. Needless to say, these same factors are the cause of the flagging wholesale demand for gold.

The silver market has undergone a parallel, albeit even more dramatic, shift. As analyzed in last month’s The Great Silver Squeeze of October 2025, the London Bullion Market Association (LBMA) reached a historic crisis point. According to analyst David Jensen, London’s freely available silver “free float” effectively fell to zero on October 10.

In October alone:

COMEX inventories fell by 46 million oz

SGE and SHFE inventories fell by 22 million oz

Some of this metal was shipped to London to temporarily relieve the acute pressure caused by unprecedented global demand.

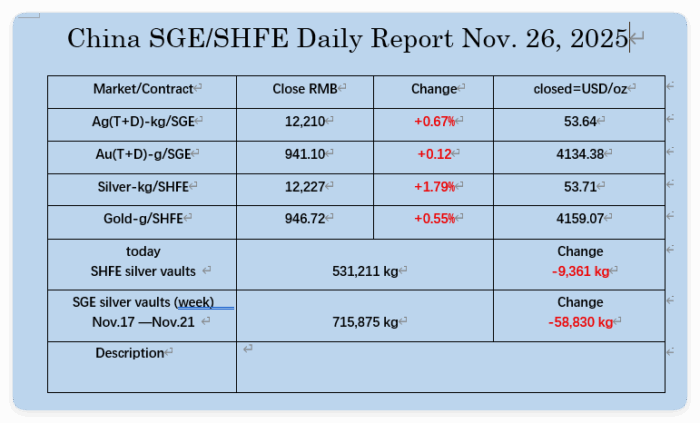

Even today, that drain continues. Based on SGE and SHFE data from the daily vault reports provided by Bai Xiaojun, Chinese exchange inventories collapsed from ~77.5 million oz on October 9 to just over 40 million oz by November 21. This is a staggering 48% decline in just six weeks.

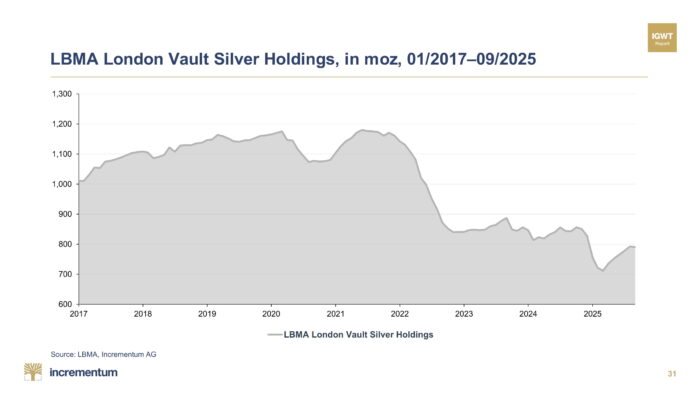

Meanwhile, LBMA London vault holdings have hovered near multi-year lows, as seen in the chart below, demonstrating a persistent structural deficit.

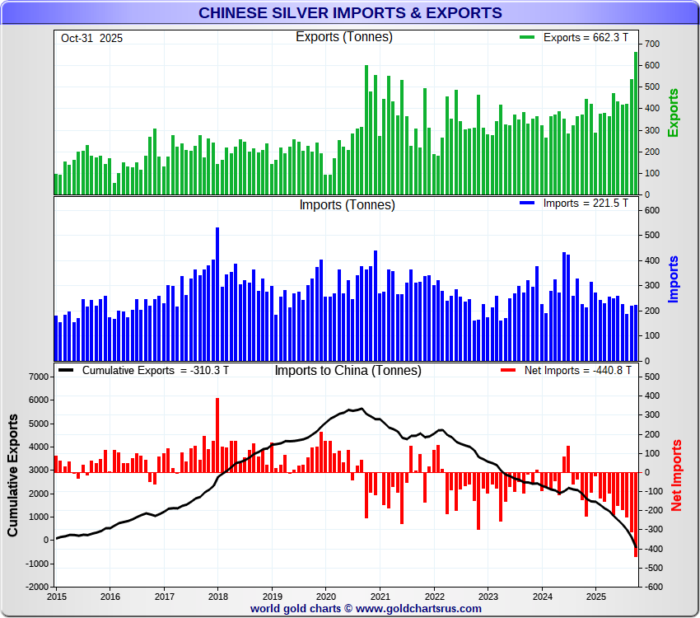

Curiously, Chinese silver exports have surged to record levels, far outpacing imports. The export/import chart clearly shows exploding outbound shipments, making this a strong evidence that silver has been flowing from China to Western vaults to cover shortages.

All this is happening while London continues trading around 700 million oz per day in cash/spot synthetic silver claims, despite having only a fraction of that amount in physical metal. As Jensen notes, “the math simply does not work.”

Despite China’s growing dominance in physical markets, global price discovery remains anchored in the West — primarily London (LBMA) and New York (COMEX). These markets offer deeper liquidity, more transparent legal frameworks, stronger rule-of-law protections, and unrestricted capital flows.

Nevertheless, China is steadily building an alternative ecosystem.

As detailed in the In Gold We Trust 2025’s chapter “Focus on System Rivalry: Where Is China Heading?”, both private investors and the PBoC have dramatically increased their gold exposure, reflecting broader structural and geopolitical shifts.

China’s key strategic initiatives include:

Expanding the Shanghai Gold Exchange’s (SGE) international role

Increasing OTC and exchange-traded gold market share — now 18.8% globally, as of October 2025, while on April it stood at 17%

Enhancing cross-border financial services

Developing internationalized SGE delivery systems and overseas warehouses

These steps are part of a broader move to elevate Shanghai as a global financial center and gradually challenge Western dominance in precious metals settlement and pricing. Furthermore, it may also reflect the ambition of internationalizing the yuan by, eventually, linking the RMB with gold.

Despite China’s production strength, as it is the world’s largest gold producer and second-largest silver producer, as well as the highest gold-consuming country, Shanghai still lags behind in global pricing power. The reason isn’t the quantities or qualities of the metals. In truth, trust, transparency, and capital mobility are the factors that matter.

Plainly, London and New York remain preferable for international institutions because:

They operate under robust legal systems.

Capital controls do not impede transactions.

Market data is more transparent.

Derivatives and hedging tools are deeper and more liquid.

Conversely, China’s political environment, which is marked by heavy state intervention, censorship, and potential capital restrictions, renders Shanghai less attractive for foreign financial institutions, even as China’s role in physical flows grows.

Indeed, China’s influence on gold and silver is hardly a mere marginal factor. Regarding gold, China is now the world’s most important buyer, both publicly and in the shadows. Whereas in silver, it has become a key supplier to global markets during crises, with its own inventories draining at an extraordinary pace.

Nevertheless, Western markets still set the price.

Undoubtedly, we are entering a world where physical flows are increasingly Eastern, while financial price discovery remains Western. This divergence cannot continue indefinitely. Whether the future brings convergence, fragmentation, or a new multipolar pricing regime, one thing is clear:

China is reshaping the precious metals landscape, and the world is only beginning to wake up to this fact.

#GoldDemand #GoldReserves #SilverDemand #SilverSqueeze #PreciousMetals #Commodities #HardAssets #SafeHaven #InflationHedge #FuturesTrading #ChinaEconomy #EmergingMarkets #MacroTrends #EconomicInsights #Geopolitics #Geoeconomics #WestVsEast #Dedollarization #CentralBanks #MonetaryPolicy #IGWT25