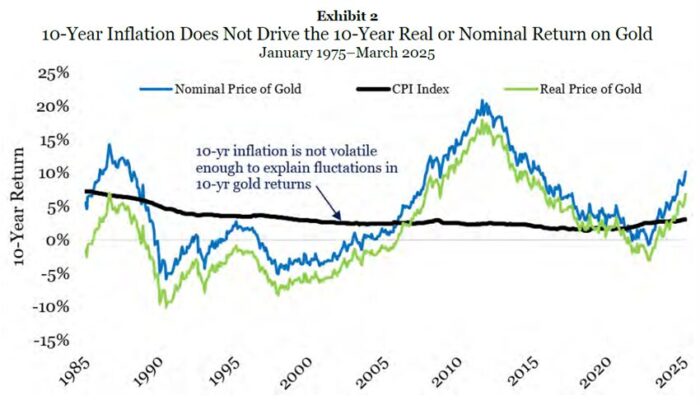

To begin with, let’s see how Erb and Harvey analyze gold’s relationship with inflation. They acknowledge that over thousands of years, gold has broadly maintained its purchasing power: the “golden constant.” Nevertheless, they argue that gold is “an unreliable inflation hedge over short time spans” because its price is far more volatile than inflation itself. While inflation hovers around 2%, they note, gold’s annual volatility is roughly 15%. The mismatch in volatility leads them to conclude that gold’s short-term inflation-hedging ability is weak, though in the long run its purchasing power remains intact.

Be that as it may, this reasoning rests on a crucial misconception. Like much of mainstream Keynesian thought, it equates inflation with a rise in consumer prices. In truth, inflation begins with expansion of the money supply. Prices rise only later, with a lag. When liquidity surges or is expected to mushroom suddenly, whether through central bank balance sheet expansion or fiscal stimulus, gold reacts almost instantly, because it is priced in monetary units that are being diluted.

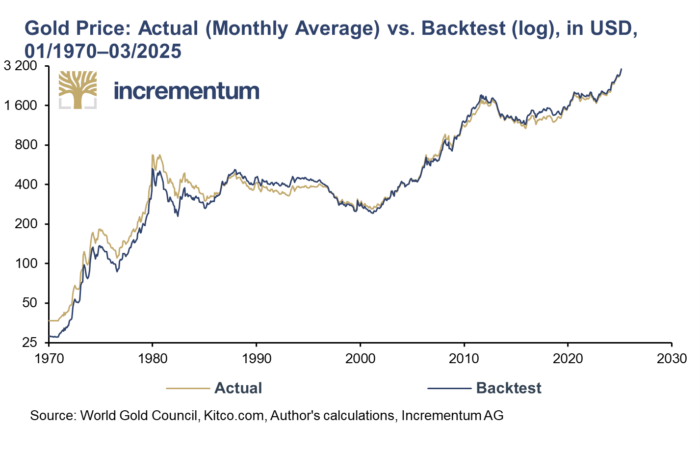

Our In Gold We Trust 2025 (IGWT 2025) report dedicates an entire chapter to demystifying this mechanism. Dietmar Knoll demonstrates that the trend in the gold price can be modeled using two variables: liquidity (the M2 money supply) and investor confidence. Both equities and gold respond positively to liquidity, but when confidence wanes, equities underperform while gold shines. In this light, gold’s apparent short-term “unreliability” is merely a reflection of analysts looking at the wrong definition of inflation.

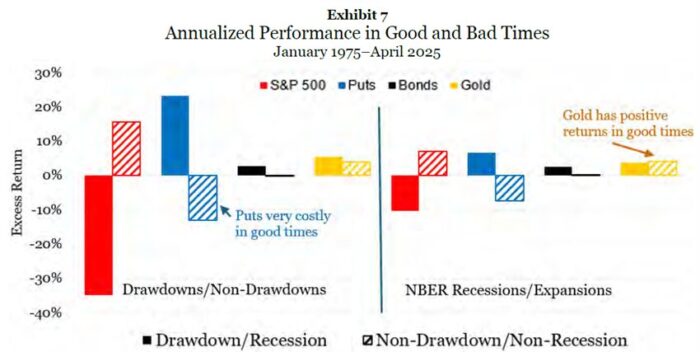

Erb and Harvey’s analysis on portfolio construction is very compelling. Gold, they find, behaves as a reliable diversifier within equity portfolios, insofar as its correlation with stocks is low and often negative in turbulent times. Historically, gold tends to post positive returns during recessions and financial crises, which is the mirror image of equity performance.

In short, this safe-haven quality is why gold repeatedly acts as a crisis hedge. From the 1970s oil shocks to the 2008 GFC and the pandemic turmoil of 2020, gold has preserved wealth when financial assets faltered. As the IGWT 2025 report emphasizes, this defensive character coexists with offensive potential: gold can protect and perform simultaneously.

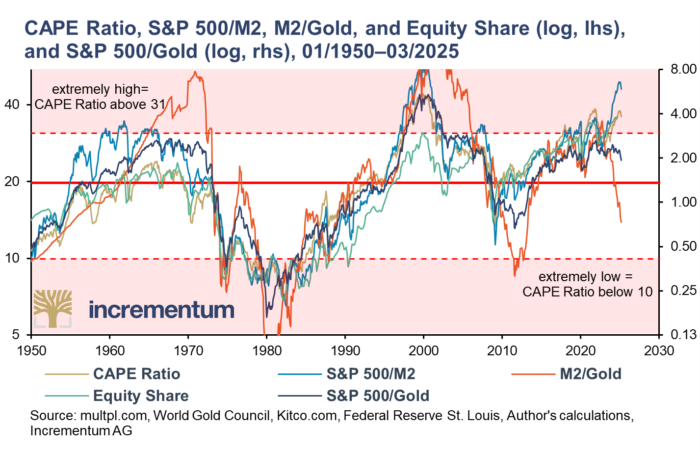

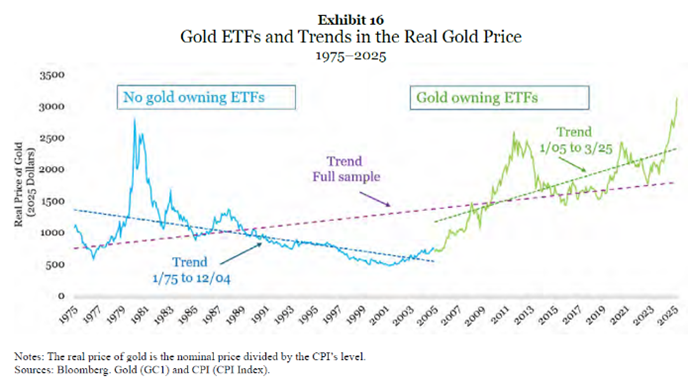

Another major theme in Understanding Gold is the “financialization” of the metal, especially through the introduction of gold-backed exchange-traded funds (ETFs). The authors test whether ETF demand has permanently lifted the real price of gold. Comparing the pre- and post-ETF eras, they observe that the real gold price (price adjusted for CPI inflation) has trended upward since ETFs were launched, and conclude that financialization led to a “permanently higher price,” albeit with some recent divergence.

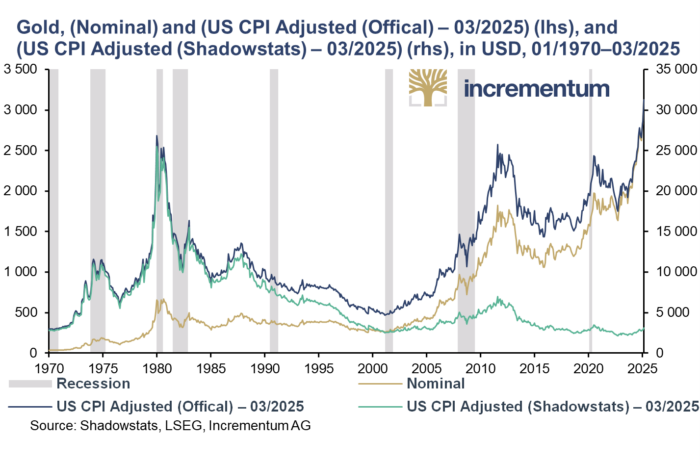

However, the “real gold price” depends entirely on how one measures “inflation”. If official CPI figures understate true inflation – as Shadowstats and other independent sources suggest – then the supposed upward drift largely disappears. Using Shadowstats’ CPI series, the real gold price has been broadly flat since ETF introduction.

What actually changed was not merely the total demand for gold, but its composition. Investment demand shifted: while ETFs attracted Western institutional investors, coin and bar purchases softened. Since the 2008 crisis, central banks have returned as net buyers, while jewelry demand has plateaued due to higher nominal prices. In essence, financialization mostly redistributed demand, while also expanding it (in tandem with larger supply, of course).

Erb and Harvey briefly touch on Basel III, hinting at potential regulatory shifts that could increase institutional demand. The question is whether gold might one day qualify as a High-Quality Liquid Asset (HQLA) under the Basel framework.

Ronald-Peter Stöferle’s analysis in Gold’s Treatment Under Basel III clarifies the situation. He points out that gold already enjoys a 0% risk weight for capital-adequacy purposes: it is a Tier 1 asset, comparable to cash. But for liquidity ratios, gold is not classified as HQLA. Actually, it carries an 85% Required Stable Funding factor under the NSFR, reflecting regulators’ skepticism about its short-term liquidity.

If gold were ever upgraded to Tier 1 Level 1 HQLA, banks would be able to hold it to meet liquidity-coverage requirements. Such a move would likely alter the composition of demand, banks and ETFs accumulating more metal. Nonetheless, as with the ETF revolution, it would not fundamentally change gold’s long-term equilibrium value. Using a properly measured real-price series (again, Shadowstats-adjusted), it’s reasonable to assume that the trend would remain largely steady.

From an Austrian school standpoint, gold’s value does not arise from regulatory classification or financial engineering, but from its role as sound money: a scarce, durable, and reliable store of value. As long as the global monetary system is built on debt and perpetual inflation, gold will continue to serve as its counterweight.

However, to propel the real gold price to a permanently higher plateau, mere policy tweaks or financial innovations are insufficient. What is required is a fundamental shift in monetary philosophy. Simply put, a return to principles of sound money, fiscal discipline, and respect for savings. Only when society moves away from collectivist redistribution and unrelenting credit expansion will gold (and genuine capital formation) reclaim their rightful centrality.

Such a transformation would echo the teachings of Mises, Hayek and other lumaries: prosperity arises not from inflation-driven spending, but from productivity, savings, and trust in money that cannot be debased. Until then, gold remains both a mirror and a refuge, reflecting the fragilities of our current system, while offering protection against its excesses.

Erb and Harvey’s Understanding Gold succeeds in reaffirming gold’s enduring role as a diversifier and crisis hedge. Yet, its inflation analysis overlooks the monetary roots of price dynamics. Basically, gold’s behavior makes perfect sense once we shift the lens from consumer prices to money supply and confidence.

In the coming years, as discussions around Basel III, de-dollarization, and financial instability intensify, gold’s relevance will only grow. Whether held in physical form, ETFs, or as central-bank reserves, gold will continue to stand as the ultimate test of trust in our monetary order.

#GoldDemand #GoldInvesting #PhysicalGold #SoundMoney #AustrianEconomics #Keynesianism #GovermentInterventionism #PriceDiscovery #BaselIII #InflationHedge #SafeHaven #HardAssets #FinancialMarkets #MonetaryReserves #DeDollarization #MonetaryPolicy #WealthPreservation #FinancialEngineering #GoldSupply #IGWT2025