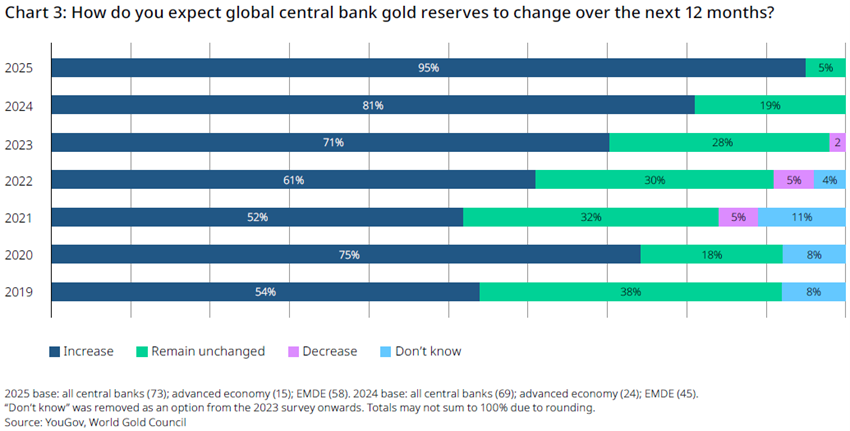

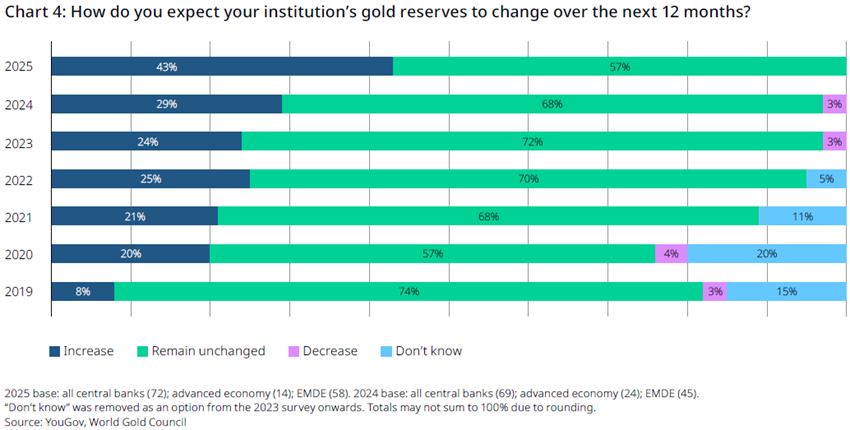

Central banks have acquired more than 1,000 tonnes of gold annually for the past three years—well above the decade-long average of 400–500 tonnes. This year, 95% of survey respondents believe global gold reserves will continue to rise over the next 12 months. Notably, 43% expect their own institutions to increase gold holdings—the highest percentage ever recorded by the survey. Moreover, no respondent takes the view that their own central bank will reduce the amount of gold in reserve.

This enthusiasm is especially strong among emerging market and developing economy (EMDE) central banks, which are more likely than their advanced economy peers to actively accumulate gold.

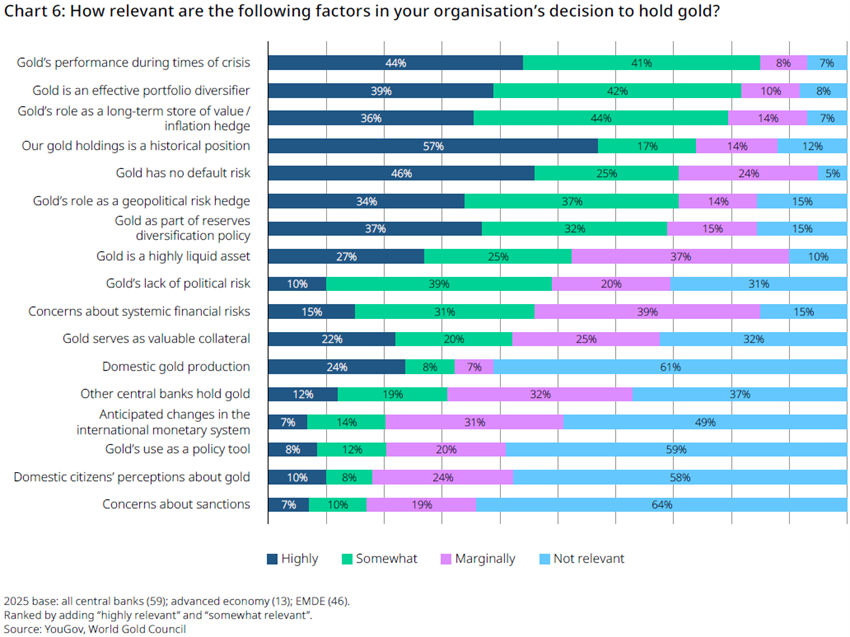

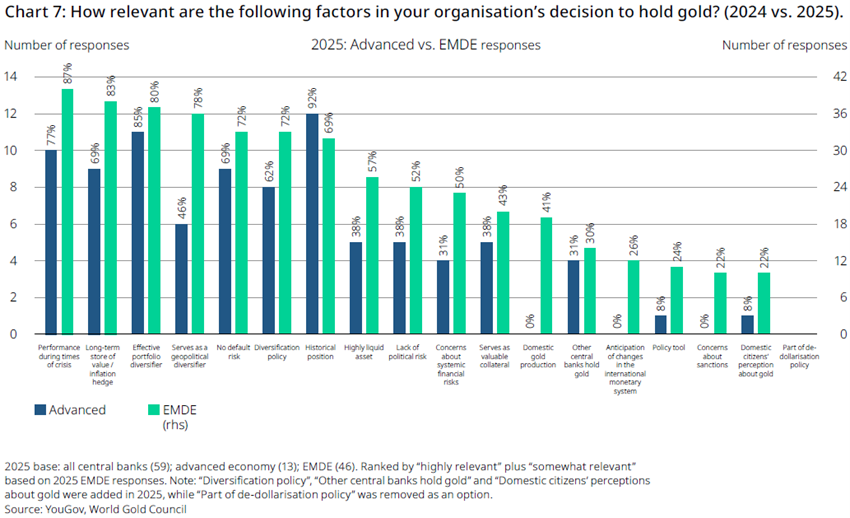

When asked why they hold gold, respondents overwhelmingly cited its performance during times of crisis (85%), role as an effective portfolio diversifier (81%), and value as a long-term store of value and inflation hedge (80%).

Other key drivers include:

This shift is underpinned by a shared belief that gold can mitigate systemic risk, especially as uncertainty lingers around interest rates, trade disputes, and global monetary stability.

Curiously, the option “Part of de-dollarisation policy” was removed as one of the factors weighing of these institutions’ decision to hold gold. Nevertheless, we note that the option “Anticipated changes in the international monetary system” jumped by 26% among the EMDE central banks, which almost amounts to the sum of the affirmative answers in the 2024 survey. On the whole, 32% of the organizations – 11% “Somewhat” and 21% “Marginally” relevant – reported to holding gold to follow de-dollarization measures, in 2024.

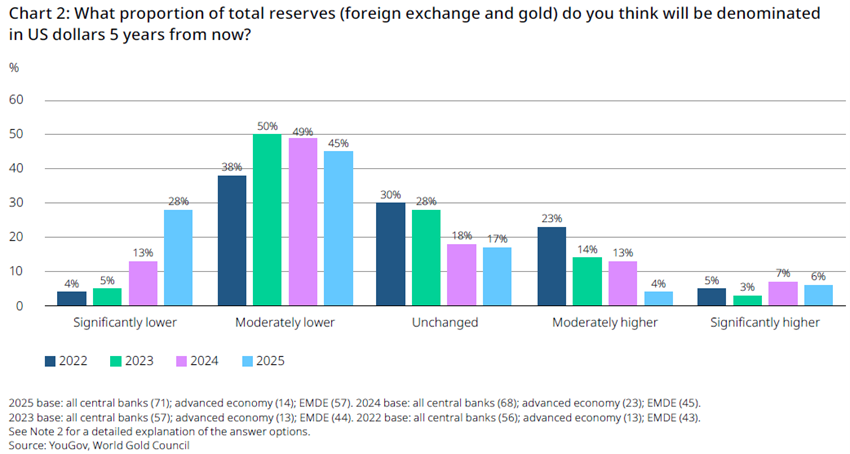

The US dollar remains the dominant global reserve currency, but its grip may be weakening. Nearly three-quarters (73%) of respondents expect its share of global reserves to decline over the next five years. In contrast, many see increased allocations to gold, the euro, and the Chinese renminbi.

Comments from respondents suggest the move away from the dollar is not ideological but strategic—aimed at navigating trade tensions, sanctions risk, and macroeconomic volatility.

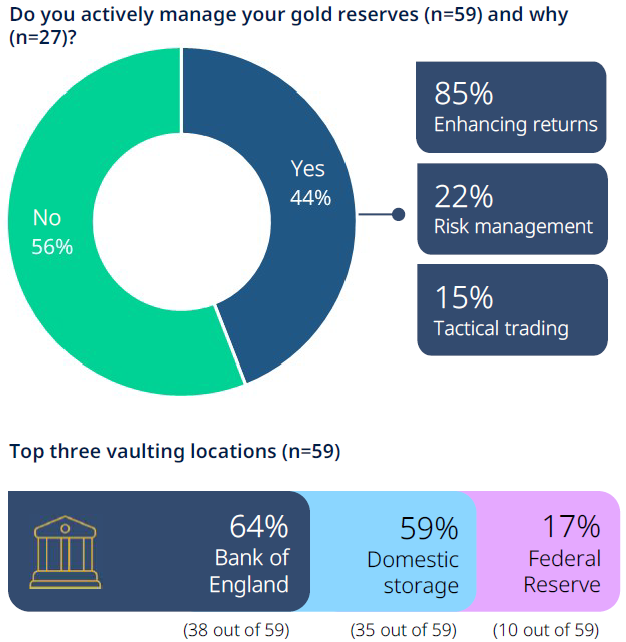

The survey also highlights a rise in active management of gold reserves, now practiced by 44% of central banks—up from 37% last year. While enhancing returns remains the primary motive, risk management has overtaken tactical trading as the second most important driver.

London remains the top gold vaulting location (64%), but domestic storage is on the rise (59% vs. 41% in 2024). Still, only 7% plan to increase domestic storage in the coming year.

Furthermore, 75% of respondents manage gold separately from other assets—reflecting its unique role as a strategic and historical reserve. “Good Delivery” bars remain the gold standard, preferred by 88% of respondents for both purchasing and holding.

As economic and political risks multiply, gold continues to offer a compelling combination of safety, liquidity, and performance. Whether as a hedge against inflation, a shield from geopolitical shocks, or a cornerstone of diversification, central banks clearly see gold as an irreplaceable part of their long-term strategy.

With demand set to remain robust and confidence steadily rising, 2025 reinforces a simple truth: in uncertain times, central banks still trust gold.

📘 Read the full 2025 In Gold We Trust Report: 🔗 https://ingoldwetrust.report/in-gold-we-trust-report/?lang=en

#CentralBanks #GoldDemand #GoldReserves #Geopolitics #InflationHedge #GoldStrategy #MonetaryReset #MonetaryPolicy #IGWT25