This group encompasses a remarkably diverse and ideologically heterogeneous set of voices. Despite differing backgrounds — ranging from mainstream Keynesian economics to Austrian-influenced macro analysis, from commodity markets to political economy — they share a core conviction: China is structurally positioned to outmaneuver the United States in the emerging global order.

To be clear, by “cheerleader” I don’t mean that these individuals are advocating or desiring that China becomes the hegemonic power. Whether they may feel this way or not is immaterial to this discussion.

All the same, this camp includes:

Macro analysts: Luke Gromen, Louis-Vincent Gave, Martin Armstrong

Mainstream economists: Thomas Piketty, Paul Krugman, Nouriel Roubini

Gold market specialists: Alasdair Macleod, Willem Middelkoop

Public intellectuals and political economists: Nassim Nicholas Taleb, Richard Wolff, Ben Norton

Despite their ideological diversity — from socialist to Keynesian to hard-money perspectives — China cheerleaders broadly argue that:

U.S. fiscal and debt dynamics are unsustainable,

The US dollar’s reserve status is gradually eroding,

China’s industrial and commodity dominance provides strategic leverage, and

The geopolitical center of gravity is shifting toward the East.

Unmistakenly, their views function as intellectual counterweights to the traditional Western narrative of enduring U.S. hegemony.

On the opposite end of the spectrum are analysts, economists, and strategists who maintain that the United States retains unparalleled structural advantages, ensuring its continued dominance in finance, trade, technology, and geopolitics.

To wit, this camp includes:

Macro analysts: Brent Johnson, Jeff Snider, Doomberg

Economists: Daniel Lacalle, Holger Zschaepitz

Geopolitical strategists: Michael Every, Marko Papic, Michael McNair

Authors/commentators: James Rickards

While ideologically more homogenous, as most lean conservative, market-oriented, or classical-liberal, U.S. supporters argue that:

The US dollar remains irreplaceable due to liquidity, deep capital markets, and rule of law,

China faces systemic economic constraints (property crisis, demographics, capital controls),

The U.S. wields unmatched financial extraterritoriality (sanctions, SWIFT, dollar clearing), and

Global volatility ultimately reinforces the U.S. position, not China’s.

In short, this worldview sees the Trade War as a necessary correction, not a threat to U.S. primacy.

Between these poles lies a sophisticated middle group: analysts who avoid deterministic forecasts and instead focus on structural uncertainties. Their frameworks emphasize path dependency, institutional fragility, and the complex feedback loops driving both U.S. and Chinese power.

This group includes:

Michael Pettis

Niall Ferguson

Mohamed El-Erian

Lyn Alden

Russell Napier

Velina Tchakarova

and several other prominent macro thinkers

These analysts highlight:

China’s internal contradictions (e.g., over-investment, demographic contraction),

U.S. political polarization and fiscal deterioration,

The multipolar restructuring of global trade and capital systems,

And the non-linear, unpredictable nature of historical transitions.

In spite of their “centrist” position implying, above all, indecision or incomprehension, it actually reflects a sophisticated recognition that neither power is structurally invincible nor structurally doomed. Understanding these three camps is essential because their contrasting frameworks increasingly shape the decision-making of investors, corporations, governments, and multilateral institutions.

In order to understand the predicament we’re in, we must decipher the concept known as the Mar-a-Lago Accord. In case you don’t know, this framework was introduced by Stephen Miran in his November 2024 paper A User’s Guide to Restructuring the Global Trading System, which we analyzed in IGWT 2025.

Since its publication, the framework has received growing recognition, not only among market strategists, but also as a coherent articulation of principles already reflected in the recommendations of the G20’s International Task Force on Global Public Goods. As noted by Michael McNair, Miran’s proposals align closely with the Task Force’s argument that public goods such as global security, financial stability, and open trade are chronically underprovided due to free-rider incentives.

Under this perspective, U.S. tariffs, defense conditions, and financial leverage are not merely nationalistic tools. In truth, they are economic statecraft mechanisms to rebalance the cost of maintaining global order.

This refined landscape, populated by China Cheerleaders, U.S. Supporters, and On-the-Fence Analysts, provides a more accurate intellectual map of the forces shaping contemporary debate. Essentially, it highlights the ideological, methodological, and geopolitical diversity underpinning competing narratives of global power.

Furthermore, it helps clarify why the Trade War is no longer about incremental policy disagreements. Simply put, this is a system-level conflict, driven by divergent visions of international order, economic sovereignty, reserve currency dynamics, and the future architecture of globalization.

With this context established, Part I of our article proceeds to analyze the economic rationale behind Washington’s escalation, the evolving structure of tariffs, and the strategic competition for critical resources.

Analysts in the “China Cheerleader” camp share a common thesis: China is strategically better positioned for the emerging global order than the United States.

Their argument rests on several pillars.

1. Industrial Scale and Strategic Commodities

China dominates global supply chains across electronics, batteries, solar components, and critical minerals, which are inputs essential for both the energy transition and defense industries. Its control of rare earth processing, graphite, gallium, and magnesium grants it leverage that the U.S. cannot easily replicate in the short term. For analysts like Gave, this industrial depth mirrors the “Sherman tank” strategy: China wins by scale, not elegance.

2. De-Dollarization and Monetary Autonomy

Gromen and others argue that China has systemically reduced vulnerability to U.S. financial power by expanding RMB settlement, building alternative clearing systems (CIPS), bilateral currency swaps, and increasing gold reserves. The weaponization of the dollar — evident in sanctions and reserve freezes — has only accelerated this shift.

3. Fiscal Stress and Dollar Fragility

China cheerleaders emphasize the unsustainable trajectory of U.S. debt, deficits, and entitlement spending. They argue that Washington’s reliance on foreign capital has reached a critical point, making the U.S. structurally more fragile than markets acknowledge.

4. Global South Alignment

Commentators such as Ben Norton and Richard Wolff highlight China’s appeal among emerging markets: infrastructure diplomacy, non-interference, and the BRICS+ expansion have increased Beijing’s geopolitical reach as many nations seek alternatives to Western-led institutions.

Together, these factors underpin the cheerleaders’ conclusion: the balance of global power is shifting and China is structurally advantaged in the long game.

Analysts in the “U.S. Supporter” camp argue that despite rising geopolitical frictions, the United States retains decisive structural advantages that will sustain its global dominance.

1. Dollar Centrality and Financial Depth

Jeff Snider and Brent Johnson emphasize that no other currency matches the dollar’s global liquidity, deep collateral markets, convertibility, or legal protections. Even during periods of geopolitical stress, capital flows toward U.S. assets, reinforcing dollar strength. Plainly, efforts at de-dollarization remain fragmented and lack scale; global trade and finance continue to depend on dollar funding markets and U.S. institutions.

2. U.S. Innovation, Productivity, and Capital Markets

The U.S. leads in frontier technologies, like AI, semiconductors, biotechnology, etc., which are supported by world-class research ecosystems and venture capital networks. Analysts argue that China’s tightening political controls, restricted private-sector autonomy, and weakening demographics undermine its long-term innovative capacity.

3. Geopolitical Leverage and Alliances

Strategists like Papic and Every note that the U.S. retains unique geopolitical instruments: NATO, intelligence-sharing networks, global basing rights, and unmatched naval power. Furthermore, the U.S. operates the world’s most powerful system of financial extraterritoriality, from SWIFT access to sanctions enforcement; all tools that China cannot replicate.

4. China’s Structural Vulnerabilities

Lacalle, Zschaepitz, and McNair highlight persistent Chinese weaknesses: a deflationary property bust, high non-transparent leverage, youth unemployment, capital controls, and demographic contraction. These issues constrain China’s policy flexibility and limit its ability to sustain global leadership.

For U.S. supporters, these factors lead to a clear conclusion: China faces hard structural limits, while the United States continues to anchor the global financial and security architecture, ensuring its hegemonic role endures.

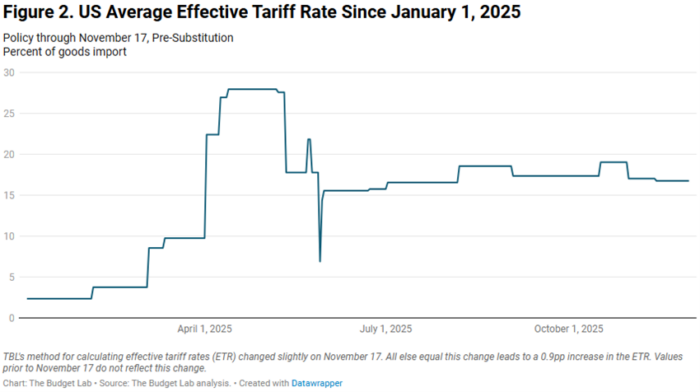

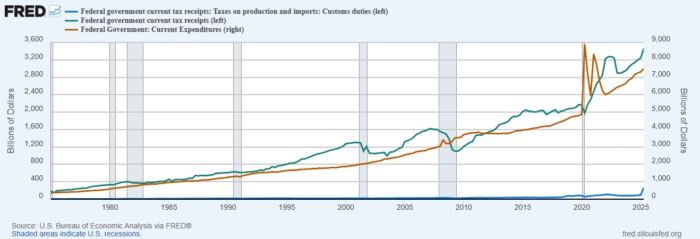

As Miran notes, tariff revenue is effectively financed by foreign producers when currency offset occurs. Apparently, Miran was hardly off base when elaborating this framework, as this was something that characterized the 2018–2019 tariff episode as well.

The Trump administration’s sweeping tariff measures, which are currently at a pre-substitution effective rate of 16.8% (after briefly peaking at 28% in April and May), have materially lifted customs duty receipts, as reflected in the sharp uptick in the U.S. federal receipts. However, the contribution remains marginal relative to federal expenditures, which continue to rise steeply.

In scale, tariff revenues remain immaterial relative to U.S. fiscal deficits. Therefore, tariffs help finance geopolitical ambitions, but they do not repair public finances.

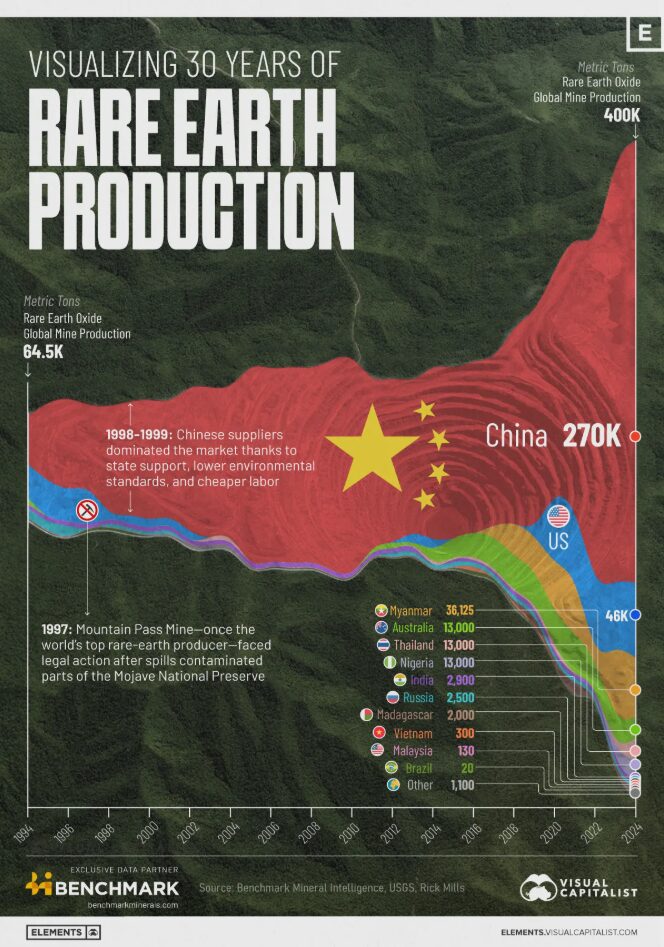

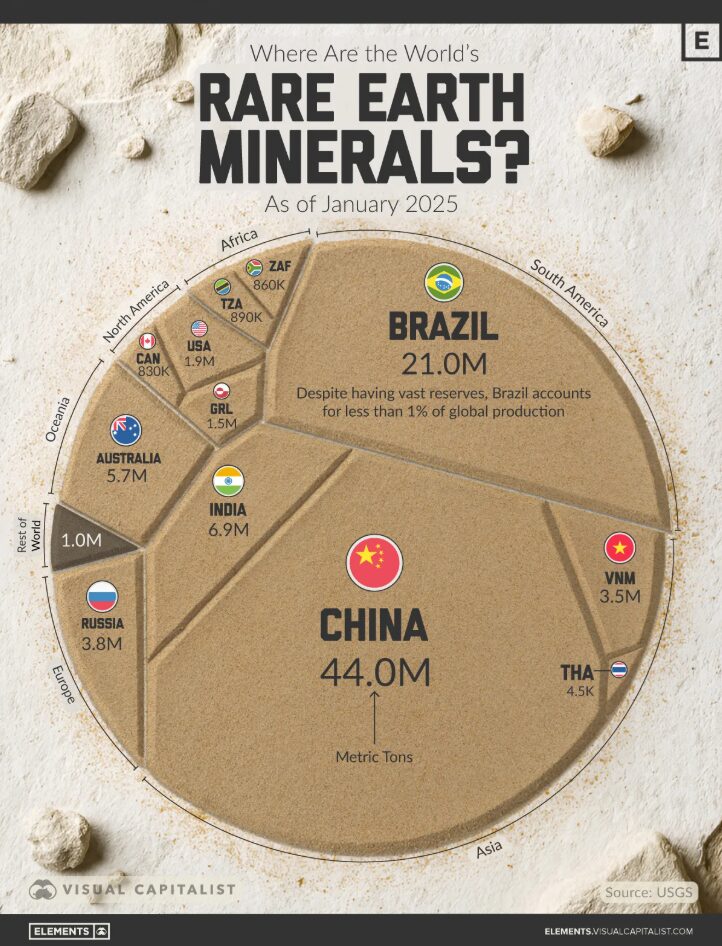

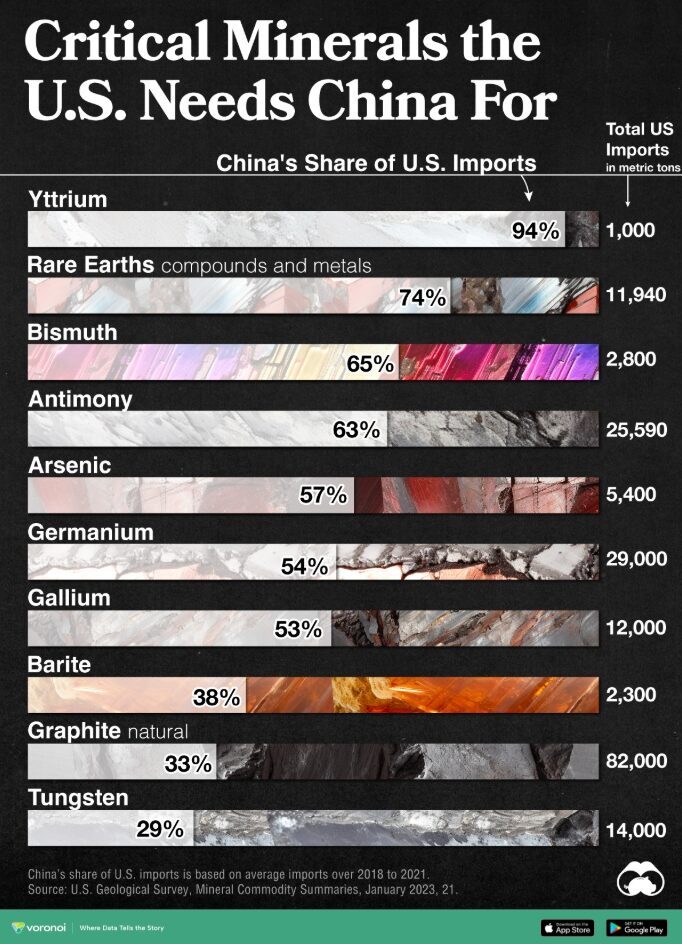

Rare earths and critical minerals have emerged as one of the most strategically consequential battlegrounds of the U.S.–China Trade War. While not inherently scarce, these minerals — 17 rare earth elements plus key inputs such as graphite, gallium, germanium, and magnesium — are extraordinarily difficult, costly, and environmentally hazardous to extract and separate. China has leveraged this reality to build a commanding lead across the entire supply chain.

Today, China accounts for roughly 70% of global rare earth production and nearly half of global reserves, alongside overwhelming dominance in processing capacity. Its market shares in specific inputs are even more striking: graphite (~79%), magnesium (95%), gallium (98.7%), and the majority of the world’s midstream conversion capabilities. These materials underpin semiconductors, EV batteries, satellites, military guidance systems, solar panels, and virtually every high-tech manufacturing ecosystem.

For the United States, the strategic vulnerability is stark: 74% of U.S. rare earth imports originate from China, creating a single-point dependency that tariffs alone cannot remedy. Without large-scale investment, regulatory flexibility, or technological breakthroughs in alternative processing, reshoring remains slow and capital-intensive.

Washington’s recent elevation of silver to the U.S. Critical Minerals List further underscores how resource security is converging with national security Naturally, this broadens the scope beyond rare earths to a wider suite of industrially vital base, and even precious, metals.

In short, critical minerals represent the Trade War’s deepest structural asymmetry. Seemingly, this obstacle is turning out to be the hardest for the U.S. to tackle.

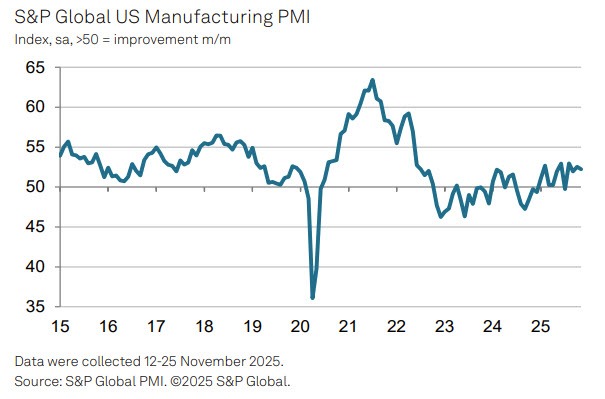

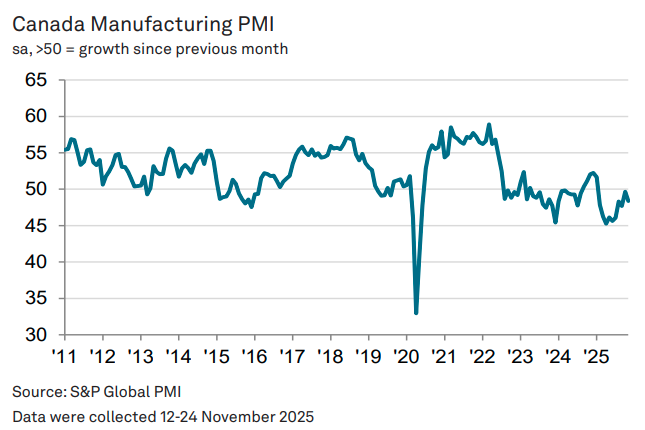

The Trade War’s effects are increasingly visible across manufacturing and logistics, both within the United States and among its closest trading partners. U.S. manufacturing has stabilized in marginal expansion territory, with the S&P Global U.S. Manufacturing PMI hovering just above 50. However, the broader North American picture reveals more strain.

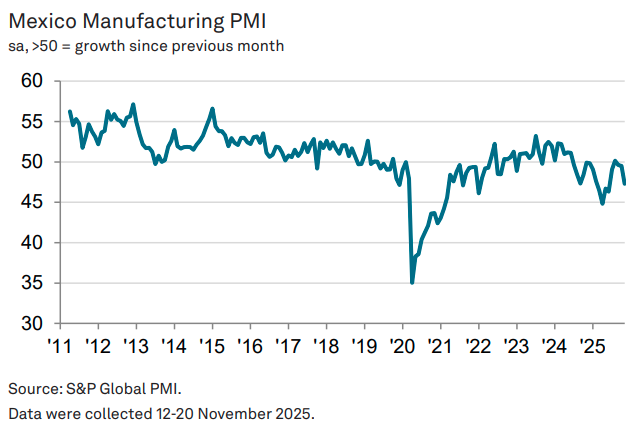

North of the border, Canada’s manufacturing sector has been in contraction for most of 2024–2025, with its PMI consistently below 50. Weaker external demand, tariff-driven input cost pressures, and reduced export competitiveness have weighed heavily on output. Similarly, Mexico shows a familiar pattern, with its PMI printing multiple sub-50 readings, reflecting soft new orders, rising input costs, and a slowdown in U.S.-bound manufacturing activity.

Freight indicators echo this softness. Monthly U.S. container imports for 2025 have generally trailed 2024 levels, particularly through late summer and autumn, pointing to weaker goods demand and inventory caution. Total annual TEU forecasts show a moderation from the post-pandemic highs of 2021–2022, highlighting a normalization, if not outright cooling, of trade volumes.

![]()

![]()

For Canada and Mexico, deeply integrated into U.S. supply chains, the tariffs have amplified frictions: costlier intermediate goods, disrupted sourcing patterns, and slower cross-border volumes. The result is a region-wide manufacturing slowdown that contrasts with the initial optimism of nearshoring narratives.

One year into Trump’s second term, the Trade War has matured into a broader systemic restructuring. Owing to chronic inertia and misplaced incentives, mechanisms of coercive leverage have been employed as the ugly solution. In the end, the world may not have been ready for this paradigm shift, but both analytical camps reflect the crux of the matter: globalization as we knew it has ended.

What remains contested is who is structurally better positioned for the world that follows.

That is the focus of Part II, where we will evaluate economic performance indicators, capital flows, FX dynamics, commodity behavior, and structural resilience to assess which side — if either — is truly “winning” the Trade War.

#TradeWar #TradeBarriers #GlobalTrade #WorldEconomy #ChinaEconomy #AdvancedEconomies #EmergingMarkets #MonetarySystem #MacroTrends #Geopolitics #Geoeconomics #EconomicStatecraft #Tariffs #SupplyChains #CriticalMinerals #RareEarths #ResourceNationalism #Commodities #EconomicPolicy #HardAssets #SilverDemand #MultipolarWorld #IGWT25