On February 20, 2026, the U.S. Supreme Court delivered a decisive 6-3 ruling: the International Emergency Economic Powers Act (IEEPA) does not authorize the President to impose tariffs. In doing so, the Court struck down all tariffs imposed under that statute, including the so-called “Liberation Day” tariffs.

The decision capped a long legal process. The U.S. Court of International Trade ruled unanimously against the tariffs in May 2025; that ruling was upheld by the Court of Appeals in August. While the tariffs remained in force during the appeals process, the Supreme Court has now rendered them legally void and returned the case to the Court of International Trade to address the thorny issue of refunds.

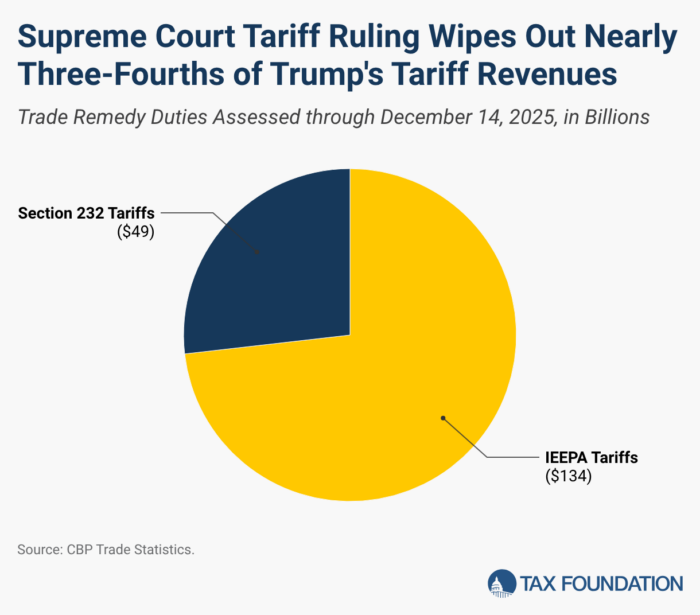

The numbers are large, of course. According to the Tax Foundation, IEEPA tariffs are estimated to have generated at least USD 160 billion through February 2026 and were projected to raise USD 1.4 trillion over the next decade. If refunds are ultimately granted in full, nearly three-quarters of the new tariff revenues from the Trump administration would effectively disappear. Importantly, the Court offered no guidance on whether or how refunds should be paid, prompting warnings from trade attorneys that the process could take years and devolve into administrative chaos.

Crucially, Section 232 tariffs remain untouched. These industry-specific levies on steel, aluminum, autos, and heavy trucks are expected to raise roughly USD 635 billion over the next decade and will continue to weigh on global trade flows.

At first glance, the removal of IEEPA tariffs should be growth-positive. Unmistakenly, tariffs function as taxes on imports, depressing investment and productivity. Their removal reduces a drag on U.S. growth and marginal tax rates on capital and labor.

Notwithstanding, markets rarely trade first-order effects alone. In the near term, uncertainty has increased rather than declined. President Trump has already indicated his willingness to pursue alternative trade tools, including Section 232, Section 301, and even Section 122 of the Trade Act of 1974. Some of these authorities have never been used before, which only compounds uncertainty for global supply chains.

For investors, this matters. While the immediate trade shock that fueled last year’s surge in precious metals has eased, the policy unpredictability that underpins strategic demand has not disappeared.

The Trade War was a major catalyst behind last year’s price action. Whereas gold benefited from safe haven flows amid escalating institutional conflict, silver experienced a unique surge as industrial demand collided with supply fragility, culminating in the silver squeeze.

With some trade barriers now removed, near-term demand has cooled. Industrial users face fewer incentives to front-load inventories, while investors have partially unwound crisis hedges. As a result, gold and silver prices have come under modest pressure, and the market appears to be digesting last year’s gains.

In the short run, this dynamic may cap upside in both metals. However, this should not be mistaken for a reversal of the broader thesis. Rather, it represents a tactical pause within a structurally altered landscape.

If trade tensions have temporarily eased, geopolitical risk has not. Quite the opposite.

Recently, U.S. military forces have taken up positions across the Middle East, with two aircraft carrier strike groups and hundreds of aircraft now within striking distance of Iran. President Trump has openly suggested that a limited strike could be used to pressure Tehran into abandoning its nuclear program, warning that “bad things will happen” if negotiations fail.

Talks between U.S. and Iranian negotiators are scheduled for tomorrow, February 26, in Geneva, widely viewed as last-ditch efforts to avoid conflict. Reports indicate that U.S. options range from targeted strikes on enrichment and missile facilities to broader regime change scenarios. Intelligence assessments suggest that last year’s attacks merely set Iran back, rather than dismantling its nuclear capabilities.

Unsurprisingly, markets have taken note. Heightened expectations of conflict, along with the risk of wider Middle East destabilization, have reintroduced a geopolitical risk premium, particularly for gold. Even as trade-related safe haven demand wanes, security-driven demand remains alive.

Likewise, silver has also responded. While less sensitive than gold to pure geopolitical fear, silver prices are supported by concerns over supply-chain disruptions and the strategic importance of the metal in defense, energy, and advanced manufacturing.

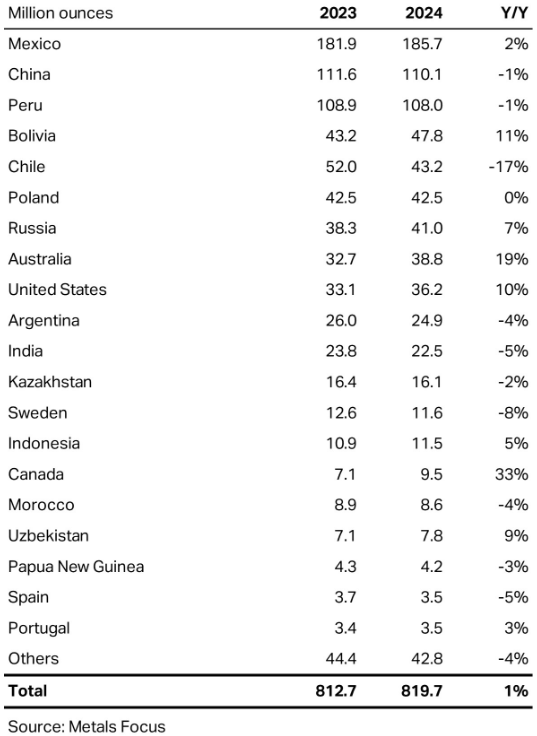

Another underappreciated factor lies on the supply side. Mexico is the world’s largest silver producer and the seventh-largest gold producer, as of 2024, accounting for roughly 22.7% of global silver output, though only 2.8% of total gold mining.

The recent killing of cartel leader Nemesio Oseguera (“El Mencho”) of the Jalisco New Generation Cartel, in an operation reportedly supported by U.S. intelligence, has triggered a wave of violence and disinformation campaigns by these criminal groups. While authorities emphasize that order is being restored, the episode has heightened concerns about security, investment confidence, and operational continuity.

For mining, perception matters as much as reality. Rising tensions, capital flight, and disrupted logistics can quickly translate into lower output or delayed investment, particularly in a sector already grappling with declining ore grades and permitting challenges.

The timing is telling. Jalisco, home to Guadalajara which is a host city for four matches of the 2026 FIFA World Cup, has been a focal point of recent operations. Be that as it may, ensuring stability ahead of the tournament is a political imperative, but the broader message is clear: silver supply remains vulnerable.

The Supreme Court ruling has removed a key pillar of the Trade War that helped ignite last year’s precious metals rally. In the near term, this has reduced some of the urgency that drove both safe haven buying in gold and panic-style industrial demand for silver.

At any rate, the deeper forces remain intact: geopolitical instability, institutional uncertainty, fragile supply chains, and structurally constrained mine supply. Hence, gold and silver may consolidate, although they are no longer priced in a world of assumed stability.

📌 For readers looking to revisit the full framework behind the silver squeeze and its two-act structure, we strongly encourage you to read our earlier piece.

The pause may be tactical, but the story is far from over.

#GoldSurge #GoldMarket #GoldMining #SilverSqueeze #SilverDemand #SilverSupply #PreciousMetals #Commodities #CriticalMinerals #TradeWar #SafeHaven #InflationHedge #MacroTrends #SupplyChains #GlobalTrade #ResourceNationalism #EconomicStatecraft #Protectionism #Geopolitics #Geoeconomics #BullMarket #GoldenDecade #TheBigLong #IGWT25