One of the most striking developments after the 2011 peak was the collapse in profitability across the mining sector.

In earlier reports, we had expected the operational leverage of gold miners to significantly boost their earnings as the gold price remained elevated. Instead, the opposite happened.

Mining revenues peaked in 2012

Net income turned negative in 2013

Losses persisted until 2016

The reason was straightforward: during the boom years, many mining companies had dramatically expanded capital expenditures, assuming that gold and silver prices would remain permanently high.

When prices corrected, margins collapsed.

Undoubtedly, markets have a way of humbling even the most confident forecasts, reminding us that commodity industries are deeply cyclical.

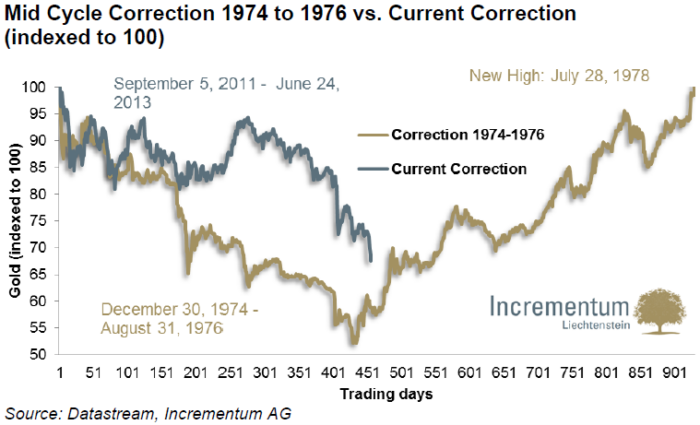

When IGWT 2013 was published, the market was still adjusting to the dramatic peaks of 2011. At the time, we believed the correction resembled the mid-cycle pullback of the 1970s bull market, which occurred between 1974 and 1976.

That correction had been severe but temporary, with gold falling nearly 50% over roughly 20 months before resuming its powerful upward trajectory. However, the analogy turned out to be misleading.

The decline that began in 2011 did not prove to be a mid-cycle correction. Instead, it evolved into a multi-year bear market, with gold and silver prices ultimately bottoming in November 2015, after a drawdown of roughly 45%.

Despite the correction, the report maintained a long-term gold price target of USD 2,230, derived from scenarios related to the potential remonetization of gold.

In hindsight, the direction of the forecast proved correct, though the timing did not. Ultimately, more than a decade after the forecast was made, gold finally reached that level on March 28, 2024.

The experience reinforced an important lesson for investors:

Forecasting price levels is difficult. Forecasting time horizons is even harder.

One important trend identified in the report proved to be remarkably accurate.

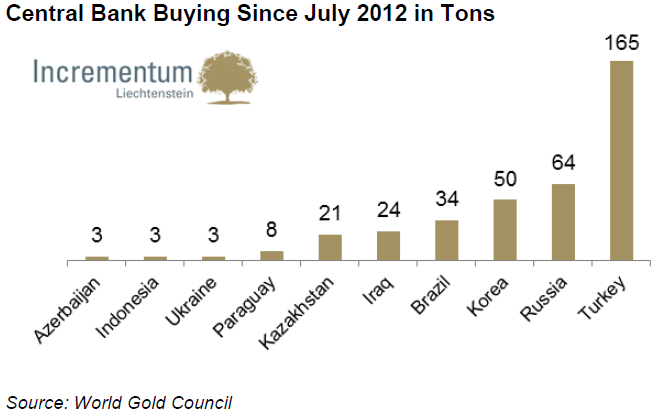

By 2013, central banks had already shifted from net sellers to structural buyers of gold. This trend began after the Global Financial Crisis and continued throughout the 2010s.

Emerging market central banks played a particularly important role in this shift. Visibly, countries such as China steadily increased their gold reserves, contributing to a broader rebalancing of global monetary reserves. This trend would later become a defining feature of the 2020s “Golden Decade” for gold.

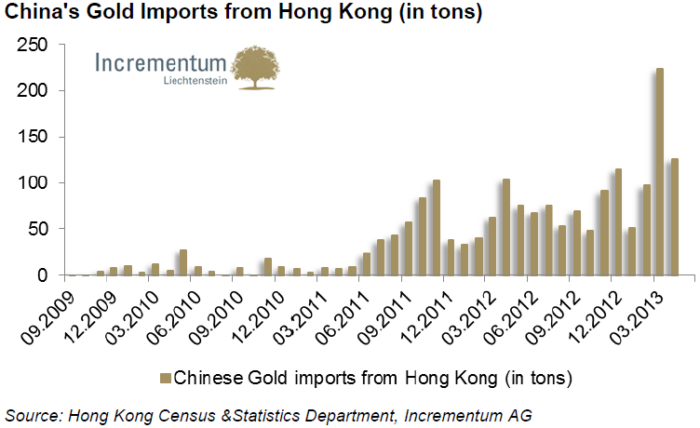

Another major structural shift highlighted in IGWT 2013 was the growing importance of emerging market demand. Indeed, demand for gold was increasingly driven by countries such as China, India and other rapidly growing emerging economies

Overall, gold purchases in these regions occurred through a combination of private investment, jewelry demand, and central bank accumulation.

Thus, the center of gravity in the gold market began shifting gradually from West to East, a development that continues to shape the market today.

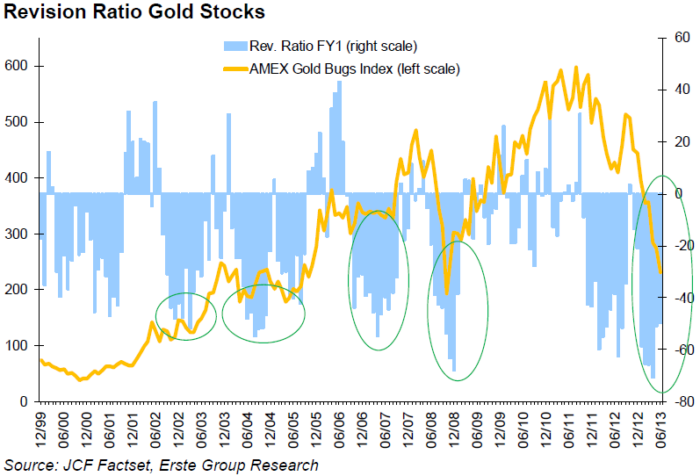

During this period, sentiment toward mining companies was extremely pessimistic. Against this backdrop, the report described gold mining equities as potentially “the ultimate contrarian play.”

The reasoning was that improved capital discipline combined with a future recovery in the gold price could eventually produce earnings surprises.

While the thesis ultimately proved correct in the long run, the recovery took far longer than anticipated, underscoring once again how timing can dominate investment outcomes.

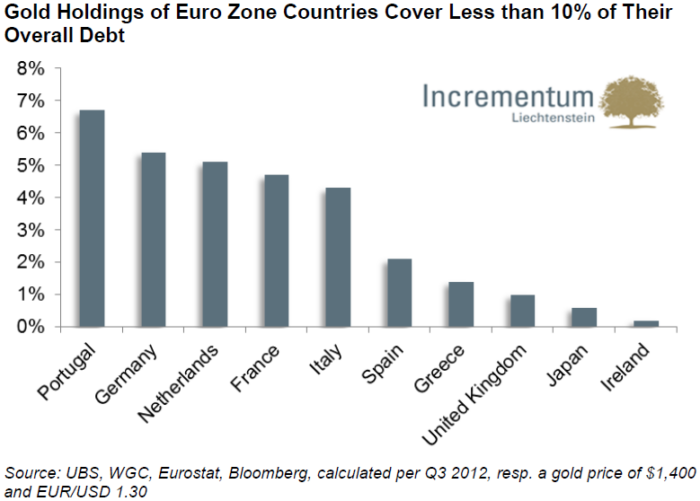

Not all predictions were challenged by the market. One call that proved particularly accurate concerned the possibility that crisis-stricken Southern European countries – anyone remembers the PIGS? – might sell their gold reserves to alleviate debt burdens.

At the time, we argued that such sales were highly unlikely for several reasons:

They would barely improve national debt ratios

They would signal weakness to financial markets

They could further undermine confidence

In fact, countries such as Portugal and Italy, which are both among the world’s largest official gold holders, never sold their gold reserves.

One quote from the report captured a fundamental truth about modern finance:

“Confidence is the most important and most volatile component of our monetary system.”

Definitely, gold reflects trust in money itself. When confidence in monetary systems erodes, investors often rediscover the appeal of hard assets with no counterparty risk.

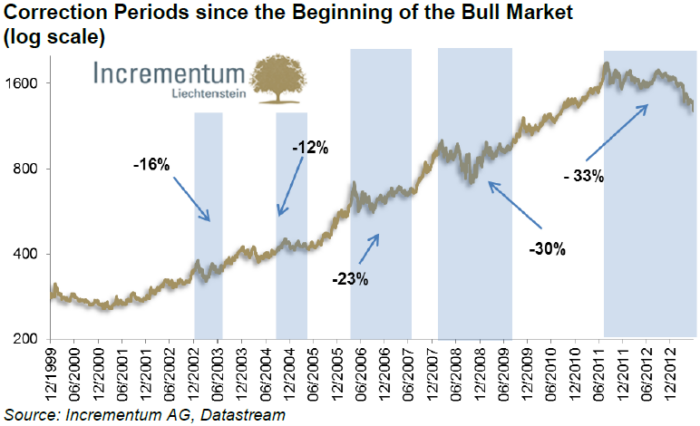

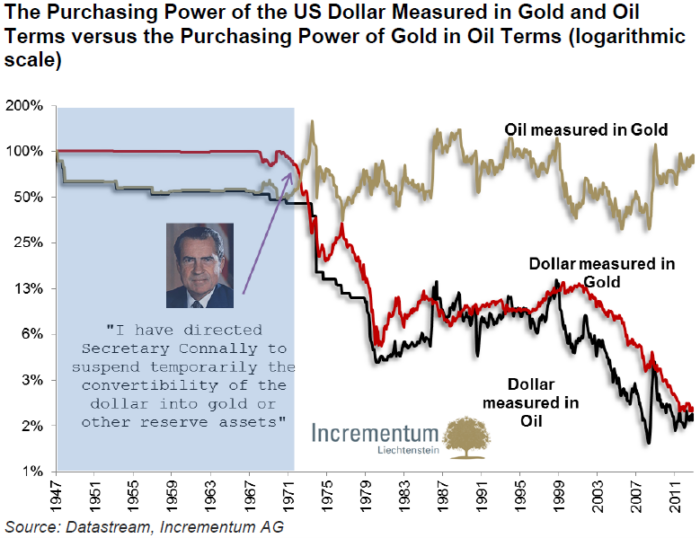

In 2013, we argued the climax of the 2000s bull market had not yet occurred.

Basically, our reasoning was the following:

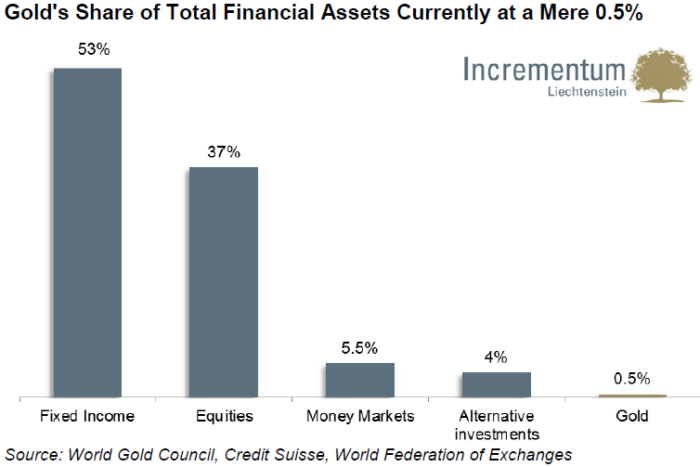

Gold demand was tiny vs allocations to other asset classes.

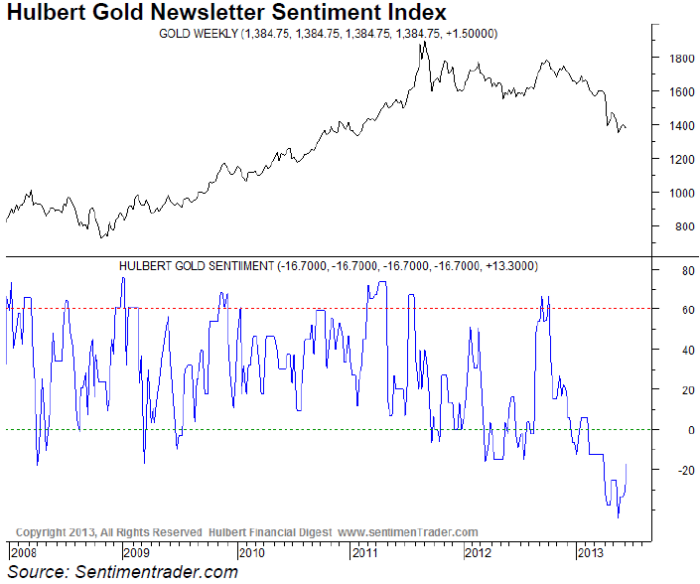

The rally paled vs the 1970s bull market.

No speculative mania yet.

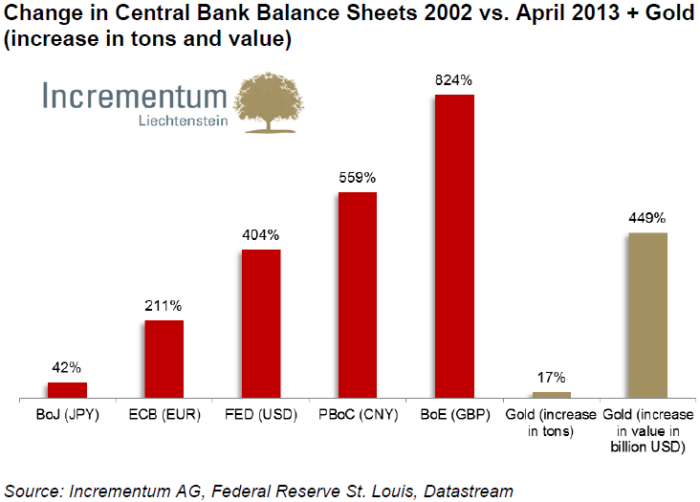

Monetary base expansion and government debt was exploding.

In hindsight, the “naysayers” turned out to be right. As we now know, that cycle had culminated a couple of years before, and had entered a long period of stagnant price action, despite ongoing central bank purchases and investment demand to protect from relentless monetary inflation.

Looking back, the 2013 edition of the In Gold We Trust report stands as an important lesson in market psychology and humility.

Even well-founded structural arguments can be overwhelmed by:

cyclical forces

investor sentiment

timing mismatches

Although the long-term thesis for gold remained intact, the cycle had already turned.

More than a decade later, the IGWT 2013 remains a fascinating snapshot of a pivotal moment in the gold market.

In a nutshell, our analysis captured:

the psychology of a post-peak environment

the growing importance of emerging market demand

the rise of central bank accumulation

and the fragile role of confidence in monetary systems

Above all, it reminds us of a simple truth: Markets reward patience and humility.

📘 If you would like to revisit the original report, you can read it in the IGWT Report Archive.

#InGoldWeTrust #20Years20Threads #IGWT13 #GoldReport #SoundMoney #GoldInvesting #PreciousMetals #GoldMining #MiningStocks #CentralBanks #MonetaryPolicy #MonetaryReserves #EmergingMarkets #DebtGrowth #DebtCrisis #MarketPsychology #ContrarianIndicators #InvestorSentiment #MacroTrends #InvestmentInsights #MarketAnalysis #FinancialResults #AustrianEconomics #MacroResearch #AnniversarySeries