The geopolitical environment has entered a new and dangerous phase, and the consequences are rapidly propagating through global commodity markets.

At the center of the disruption lies the Strait of Hormuz, which is indubitably the world’s most critical oil chokepoint. With conflict escalating in the Middle East, shipping traffic through the strait has been severely disrupted. Although some tanker transit has recently resumed, most shipping companies remain reluctant to send vessels through the corridor.

![]()

![]()

![]()

![]()

The reason is simple: the route is no longer considered safe.

To make long story short, insurance premiums have surged dramatically, and many tankers now face unacceptable risk from drones, missiles, and naval threats. Even when insurance coverage is technically available, the costs can make voyages uneconomic.

Compounding the problem is the damage to oil logistics infrastructure across the Persian Gulf, which has removed significant export capacity from the global market. Even if the conflict stabilizes, restoring this infrastructure and rebuilding logistical networks will take time. The result is a structural tightening of oil supply.

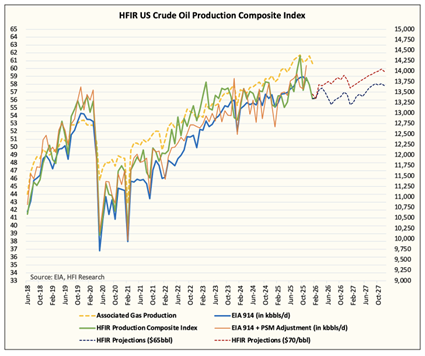

In theory, other producers such as the United States, Venezuela, or Russia could increase production to offset the decline in Middle Eastern supply. In practice, however, this is unlikely to happen quickly.

Above all, energy executives face a difficult dilemma: if they dramatically increase capital expenditures today to drill new wells, and the conflict suddenly cools down, oil prices could collapse and turn those investments into stranded capital. As a result, many companies are waiting rather than investing, which raises the probability that oil prices will remain elevated for longer than markets expect.

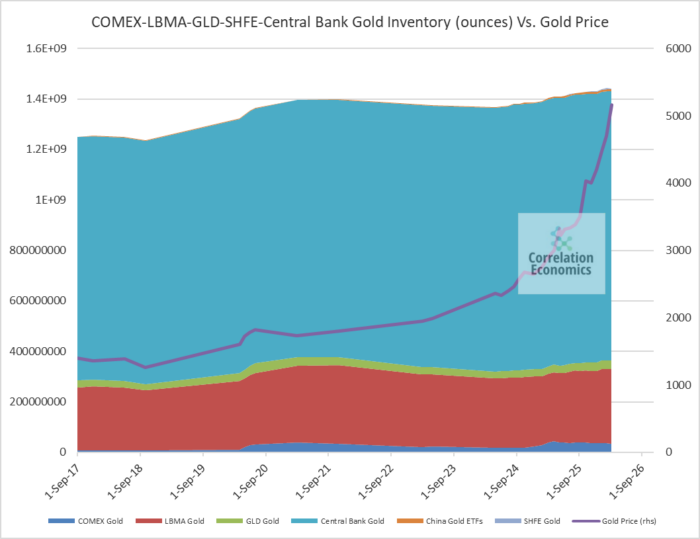

Unsurprisingly, periods of geopolitical instability consistently trigger a surge in demand for safe-haven assets, and gold remains the ultimate financial refuge.

The current environment combines several powerful drivers for gold:

Escalating geopolitical conflict

Rising energy-driven inflation

Global trade disruptions

Monetary uncertainty

When investors begin to price systemic risk into financial markets, capital tends to flow toward hard assets. Be that as it may, gold is not the only beneficiary of this dynamic.

Another scramble is emerging. Seemingly, the rush we witnessed last year was not a one-off, as the race to secure strategic and critical minerals proceeds.

If global trade routes become increasingly unstable, the transportation of many commodities could be disrupted. Therefore, governments and industries are accelerating efforts to secure supplies of essential materials.

Obviously, this is where silver becomes particularly important.

Silver sits at the intersection of monetary demand and industrial necessity.

It is essential for industries such as:

Solar energy

Electronics

Defense technology

Advanced manufacturing

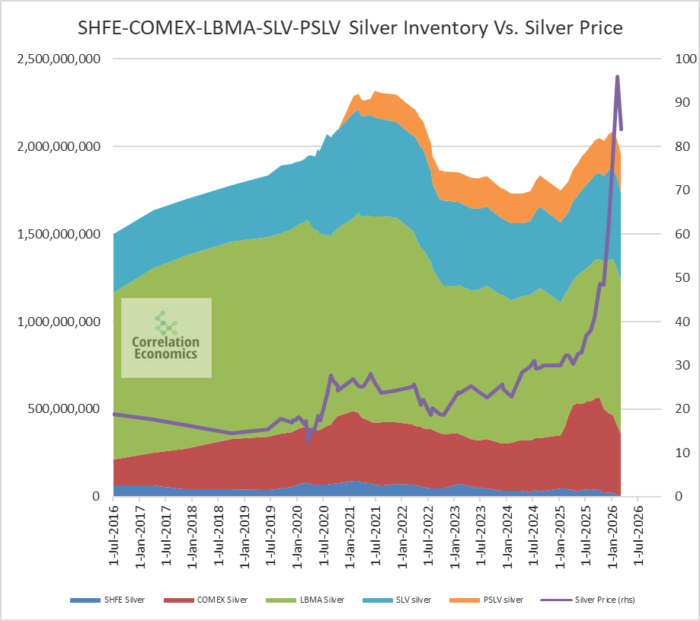

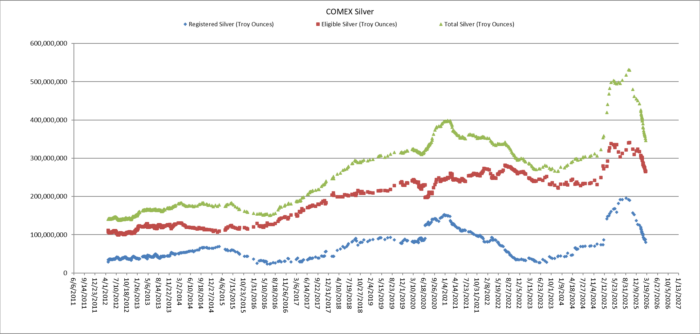

At the same time that industrial demand is growing, physical inventories of silver are shrinking.

We are already witnessing a continued drainage of silver stocks in major exchanges, either in the West or in the East.

The decline in registered and available silver inventories in the COMEX system highlights the tightening of the physical market. Meanwhile, similar trends are visible in Asia.

Inventories in the Shanghai silver hub have also been falling sharply while prices have begun to surge. Unmistakenly, this is a classic signal of tightening supply conditions.

When declining inventories collide with rising industrial demand and geopolitical uncertainty, silver markets can become extremely volatile.

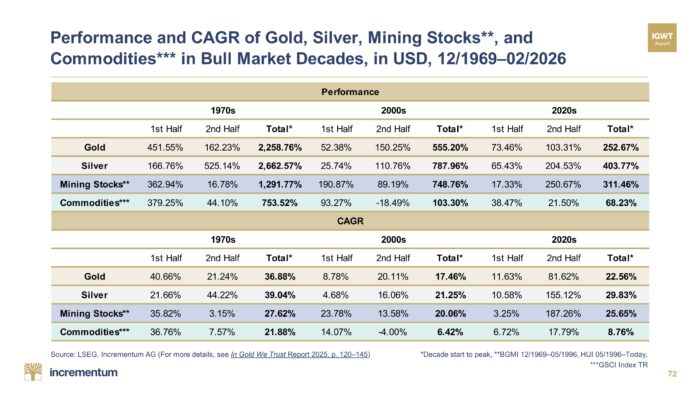

Historically, silver tends to outperform gold in the later stages of precious metals bull markets.

This dynamic brings us to a concept we introduced in the IGWT 2025 outlook: the distinction between safe haven gold and what we called performance gold.

Basically, safe haven gold refers to physical gold itself, which is the asset investors buy to preserve wealth during times of crisis. In contrast, performance gold refers to the assets that tend to outperform gold during powerful commodity bull markets, including:

Silver

Mining equities

Commodities

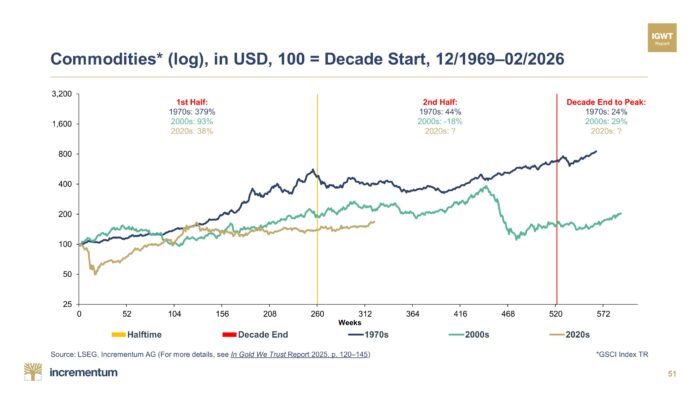

Our projection in IGWT 2025 was that during the second half of the Golden Decade — the 2020s bull market — performance gold would begin to outperform traditional safe haven gold.

Clearly, that forecast is now materializing in full. The ascent began in 2025, when silver and mining equities started to significantly outperform gold bullion. Today, we are witnessing the next phase: commodities themselves are beginning to join the rally.

This marks the transition from the defensive stage of the gold bull market to the performance stage, where leverage to commodities and resource production becomes increasingly valuable. Undoubtedly, this awakening of commodities has been a long time coming.

One of the most powerful beneficiaries of this environment is the gold mining sector. Notwithstanding, higher oil prices do raise the gold miners’ operating costs because energy represents a significant component of mining expenses.

The average gold miner currently operates with an all-in sustaining cost (AISC) of roughly USD 1,600 per ounce, with fuel representing about 13% of that cost structure, or approximately USD 208 per ounce.

Now consider a scenario where oil rises dramatically due to geopolitical disruptions. If oil moves from USD 65 to USD 200 per barrel, fuel costs would effectively triple:

Fuel cost rises from USD 208 → USD 624

Total AISC rises from USD 1,600 → approximately USD 2,024

Cost inflation equals roughly 26.5%

At first glance this appears negative for miners. However, the crucial variable is the price of gold. If gold trades near USD 5,100 per ounce, the economics for miners become extraordinary.

Revenue per ounce: USD 5,100

AISC: USD 2,024

Operating margin: USD 3,076 per ounce

Even with sharply higher energy costs, miners would still generate record margins.

This is precisely why mining equities tend to dramatically outperform gold during strong bull markets.

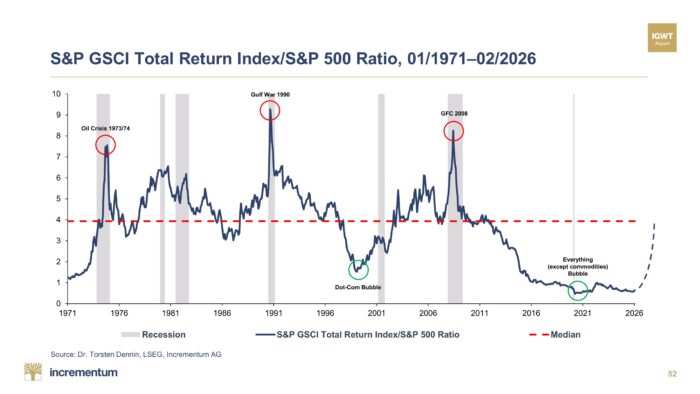

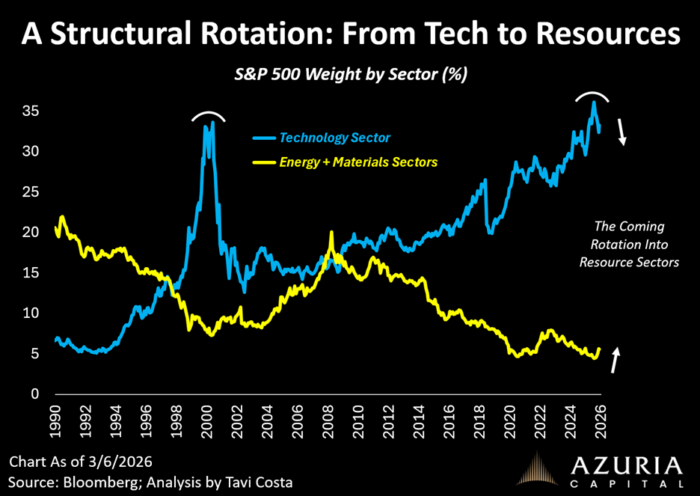

Furthermore, a broader structural shift is also unfolding in global capital markets. For decades, capital flowed overwhelmingly into technology and financial assets, while the resource sector suffered from chronic underinvestment. Nevertheless, that imbalance is now reversing.

As geopolitical fragmentation intensifies and supply chains become less reliable, investors are rediscovering the strategic importance of energy, materials, and mining companies. The world has certainly entered an era defined by:

Resource security

Energy scarcity

Resource nationalism

Supply chain resilience through re/near-shoring

In this environment, real assets are regaining importance within global portfolios.

The developments we are witnessing today suggest that the second half of the Golden Decade is now underway.

Geopolitical instability, energy disruptions, and tightening commodity markets are converging to create the conditions for a powerful revaluation of hard assets.

In truth, gold continues to benefit from safe haven demand. At any rate, the bigger opportunity lies in performance gold:

Silver

Mining companies

Commodities

These assets have already begun to outperform. Plainly, if the current macroeconomic and geopolitical trends persist, they may continue to lead the ultimate stage of the Golden Decade when commodities surge at last.

The transition is becoming increasingly visible. What began as a gold bull market is evolving into something much larger: a full-scale renaissance for the resource sector.

#GoldInvesting #SilverSqueeze #MiningStocks #PreciousMetals #Commodities #EnergyMarkets #GlobalTrade #GoldForecast #PhysicalGold #PhysicalSilver #InvestmentDemand #IndustrialDemand #OilShock #Geopolitics #Geoeconomics #CommoditySupercycle #SafeHaven #InflationHedge #BullMarket #GoldenDecades #MacroTrends #InvestmentInsights #MarketAnalysis #TheBigLong #IGWT25