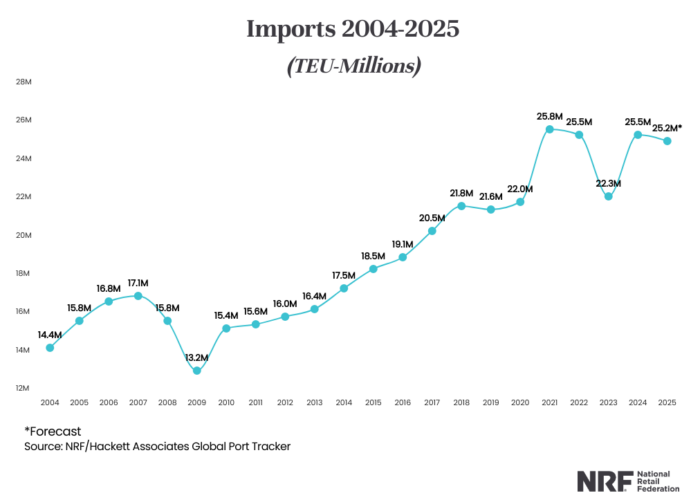

Few indicators capture the state of global commerce more cleanly than container throughput. In that light, the world economy is flashing unmistakable warning signals. The ports in American shores are expected to process 25.2 million TEU in 2025, a decline from 2024 and a vivid reflection of weakening import demand. Meanwhile, the trans-Pacific trade lanes, once the arteries of globalization, have slipped into a state of deep overcapacity. Carriers’ attempts to impose November rate hikes evaporated almost instantly. To this point, Freightos data show West Coast rates plunging by 32% in a single week at the end of last month.

Needless to say, this is not what a healthy, expanding global economy looks like. This is what happens when supply chains are rerouted, consumption cools, and geopolitical frictions become structural rather than episodic.

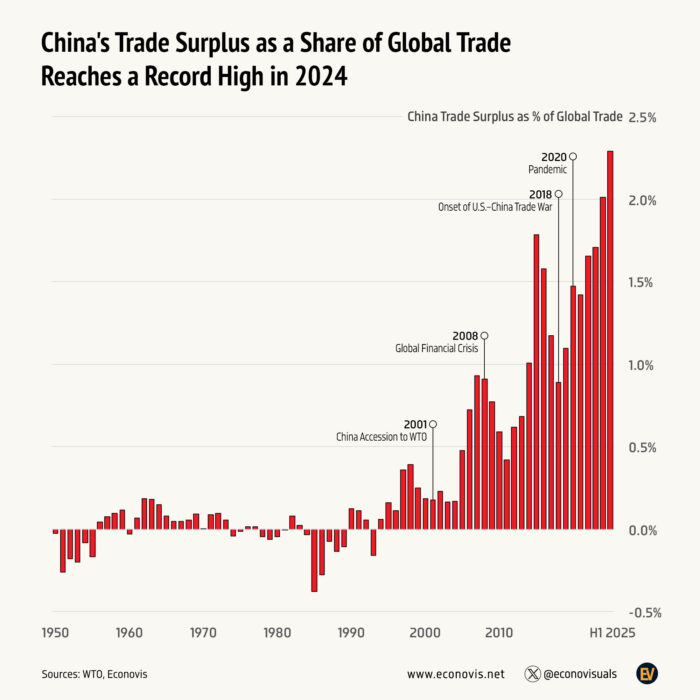

Amidst this global slowdown, notwithstanding, one bilateral relationship stands out: the U.S. trade deficit with China has begun to narrow. Years of trade barriers, reshoring incentives, diversification into Mexico and Southeast Asia, and the broader Mar-a-Lago Accord economic framework aligned with the America First grand macro strategy have borne fruit. Gradually, albeit decisively, American firms have recalibrated their supply chains.

In other words, even as global trade softens, China’s grip on the U.S. import market is slipping, and this represents a strategic victory for Washington. It is not a triumph of tariffs per se, but of the cumulative effect of political pressure, regulatory incentives, and corporate risk management.

Be that as it may, this improvement in the U.S. position is only half the story. To understand the shifting balance of power, we must confront China’s internal vulnerabilities.

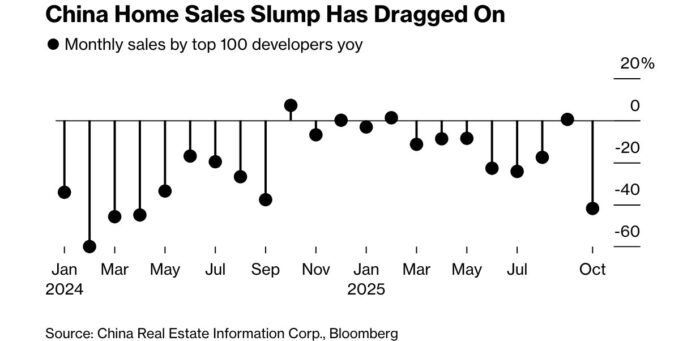

China’s property sector, which had been one of the marvels of its economic miracle, has entered a structural contraction. The property developer Vanke, once heralded as a paragon of stability, is now dependent on external liquidity infusions and pleading to defer bond repayments. Inspecting the causes, home prices have fallen for forty consecutive months, and used home prices in major cities have collapsed by a third from their peak.

In detail, October’s 41.9% drop in new-home sales among major developers was the worst in nearly two years. Looking ahead, UBS anticipates at least two more years of price declines, while Fitch foresees another 15–20% contraction in sales before any stabilization.

Most troubling of all, China abruptly instructed its largest private property data providers to stop releasing monthly sales figures to the public. Numbers that must be hidden are rarely numbers that inspire confidence.

Briefly, real estate is not just some sector for China. Demonstrably, it has become the backbone of household wealth, local government finance, and banking collateral. When that backbone buckles, everything from consumer sentiment to credit creation follows it downward.

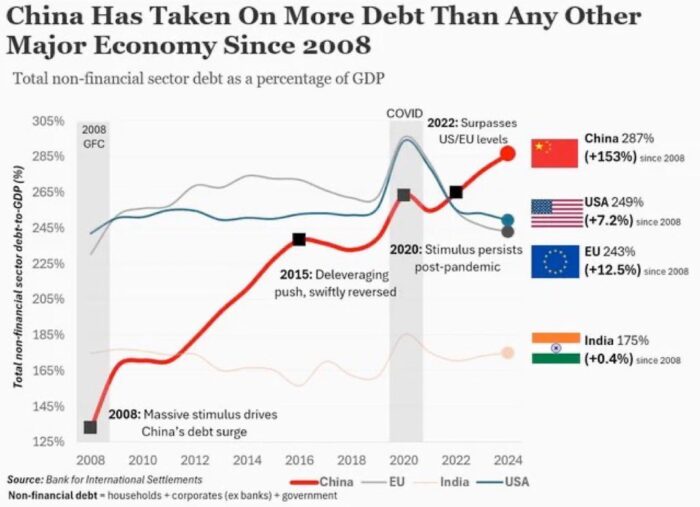

Undoubtedly, China’s total debt-to-GDP ratio — at 289% in the end of 2023 — is the highest among major economies and has grown at more than ten times the pace of U.S. debt since 2008. The country now embodies the classic arc of a debt-fueled boom turning into a debt-constrained stagnation.

The United States has debt problems of its own, but China’s leverage, distributed across opaque local governments, distressed developers, and shadow banking networks, represents a far more systemic strain. Certainly, economic development does not come from the velocity at which one adds debt, but from the productivity and resilience that debt enables. On that measure, China’s momentum has reversed.

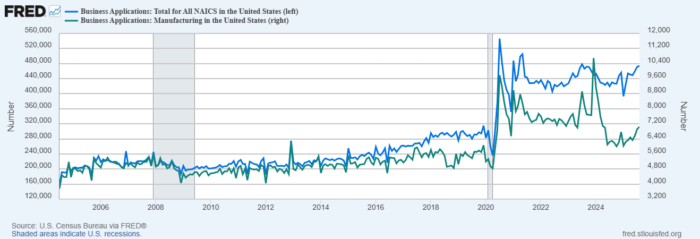

One of the most striking divergences between the two superpowers is the state of entrepreneurial activity. In the United States, business formation has surged to historic highs. Even manufacturing — long declared “lost” — has seen a renaissance in new business applications. The early contours of an industrial revival are taking shape, boosted by reshoring incentives and a political environment explicitly designed to rebuild supply chains at home.

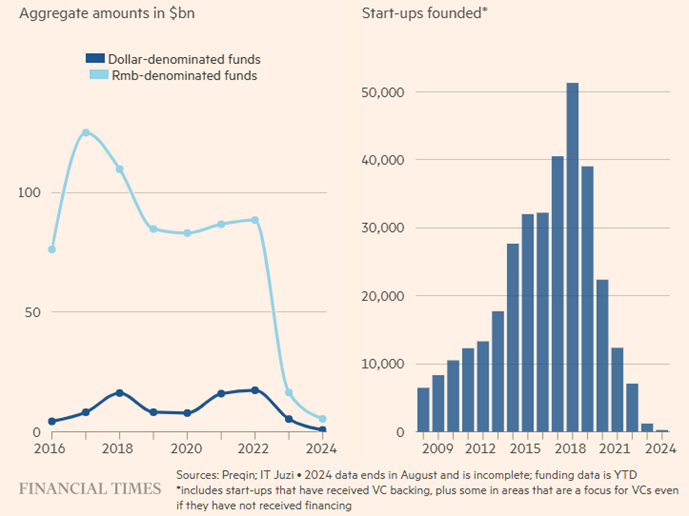

In contrast, China has witnessed the near-collapse of its venture capital ecosystem. Once second only to Silicon Valley, China’s startup landscape has been crippled by regulatory crackdowns, capital flight, and a pervasive fear among entrepreneurs. Many founders describe a business climate where risk-taking is punished and political conformity is rewarded.

Simply put, innovation thrives where freedom, capital, and optimism intersect. Today, that intersection lies in the United States, not China.

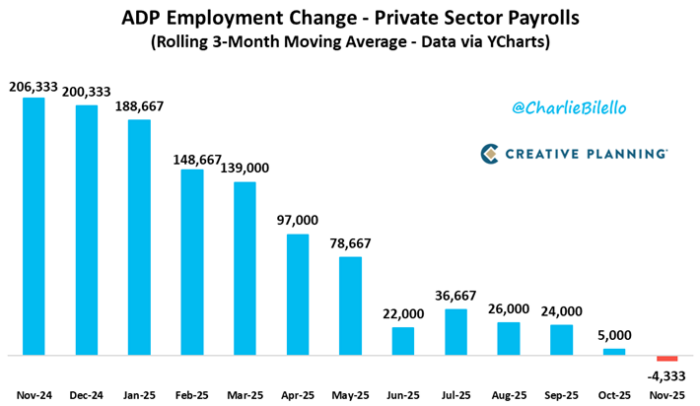

Not everything is rosy in America, as the U.S. labor market has begun to show signs of stress. November’s private-sector job losses, which were the worst since 2023, signal a slowdown in hiring momentum. Over the last three months, instead of adding over 200,000 jobs per month as we did a year ago, we have been losing jobs on average.

This is a reminder that while America enjoys structural advantages, it is not immune to the cyclical drag of tightening financial conditions, rising bankruptcies, or weakening consumer demand.

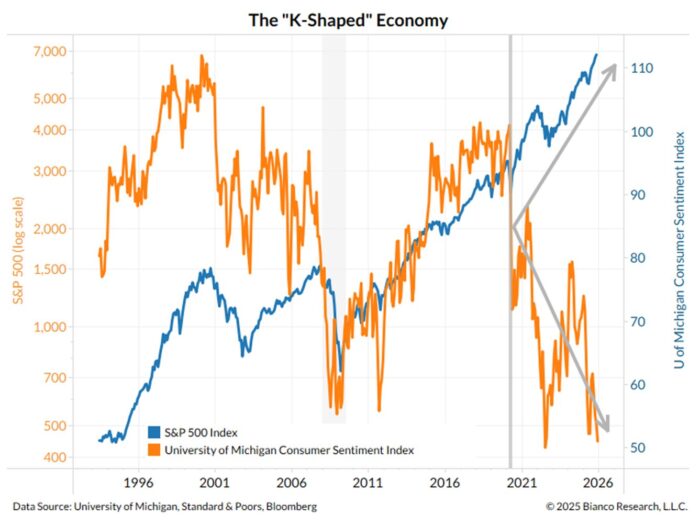

While corporate America, particularly the AI giants, surges ahead, U.S. consumers are experiencing a very different reality. The University of Michigan’s Consumer Sentiment Index recently plunged to 51, one of the lowest readings since the survey began in 1952. Not even the Cuban Missile Crisis, the stagflation of the 1970s, the Great Financial Crisis, or COVID lockdowns produced such a persistent collapse in sentiment.

The culprit is not unemployment, which remains low. As a result of all the inflation created by the government and the banking system over the last five years, the crisis of affordability has become impossible to ignore. While prices are up 26% over the past five years, wages only increased 21%. Everything from housing to groceries and to energy is more expensive. At any rate, the stock market is soaring, despite households feeling poorer.

This divergence between financial markets and the real economy — between asset owners and wage earners — is the social undercurrent of the Trade War era.

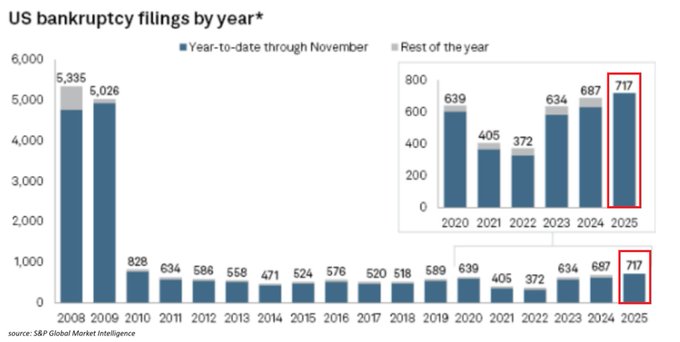

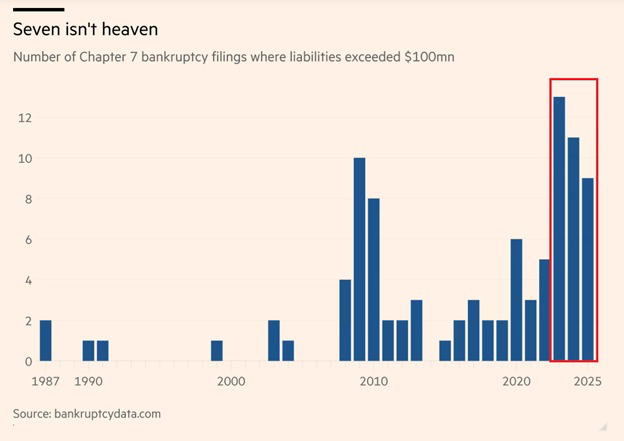

This stress is visible in the corporate landscape. 717 large U.S. companies have gone bankrupt this year. This is the highest number in fifteen years. Likewise, Chapter 7 liquidations, the most severe form of failure, are rising sharply. Apparently, the AI boom has concealed a painful reality: outside technology, many sectors are being squeezed by rising rates, fading pricing power, and heavy inventories.

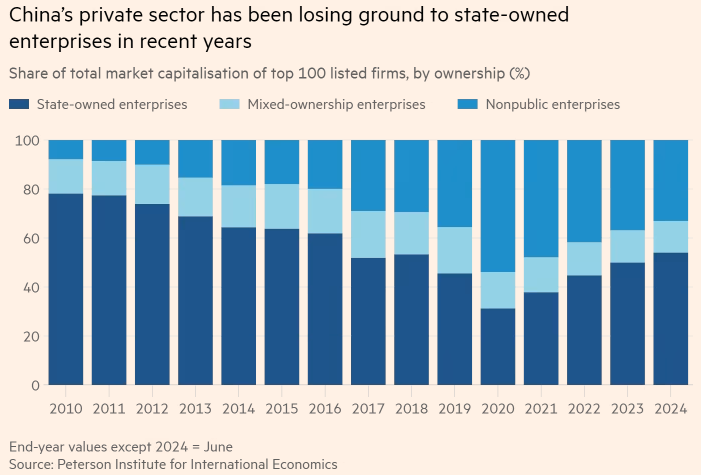

Yet, even here, the comparison with China is instructive. By going through the process of creative destruction, America is absorbing pain through corporate turnover. Conversely, China is experiencing destruction without the “creative” part. Insofar the Chinese private sector is not being renewed, it is being replaced by the State.

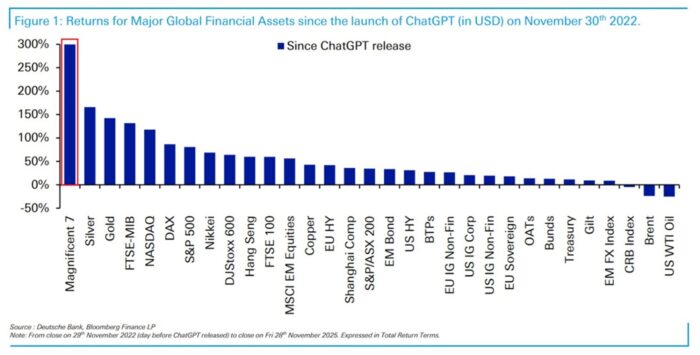

Despite the turbulence, global investors continue to vote decisively. Visibly, they are voting for America. The U.S. now makes up 65% of global equity market capitalization, while China is stuck at a mere 3%.

Since the launch of ChatGPT, three years ago:

Obviously, markets are not perfect, but they are forward-looking. They discount future cash flows, technological leadership, and institutional strength; and they overwhelmingly favor the United States.

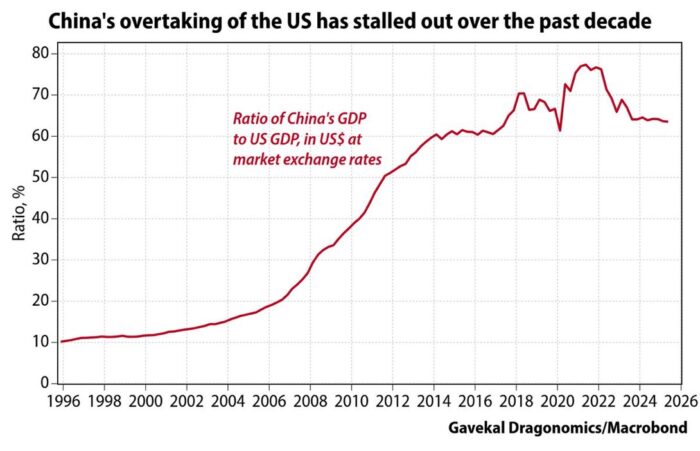

The ratio of China’s GDP to America’s once climbed rapidly. However, for the last several years, it has flatlined near 63%, refusing to inch closer to parity. The idea of China overtaking the U.S. — a dominant geopolitical narrative of the 2010s — has effectively faded.

In a nutshell, demographics, debt, slowing innovation, collapsing real estate, and capital flight have fundamentally altered China’s trajectory. The country remains powerful, but not ascendant.

Both nations are paying a price for protectionism. The world economy, too, has absorbed unnecessary strain. Far from an ideal solution to global imbalances, tariffs are a blunt, distortionary instrument.

Nevertheless, when we evaluate resilience, innovation, capital flows, entrepreneurship, market depth, and institutional adaptability, the answer becomes clear: the United States retains the advantage.

Still, China remains a formidable competitor, even though its structural headwinds are deepening. Evidently, its growth model is exhausted, and its policy decisions are constricting the private sector rather than empowering it.

Whereas the U.S., for all its challenges, continues to reinvent itself, economically, technologically, and strategically. Fundamentally, to become the world’s superpower there are certain aspects, besides the scale of production and trade dominance.

By staying true to its dynamism, the hegemonic status of the US remains unrivaled. In my opinion, the biggest menace to the American Exceptionalism lies not on some foreign adversary, but on subversive and “un-American” elements inside its borders that are exhausting its resources and, most importantly, its social fabric.