For much of the 2021–2024 period, ETF flows were reactive and often procyclical to the downside. That regime has shifted decisively.

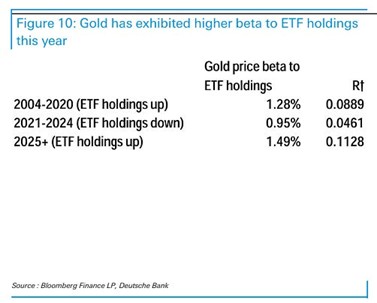

According to Deutsche Bank’s research, ETF demand in 2025 exerted a roughly 50% stronger influence on gold prices than during prior inflow cycles. The crucial nuance? While statistical models suggest gold prices “Granger-cause” ETF flows rather than the reverse, the intensity and persistence of these flows are now amplifying moves rather than merely tracking them.

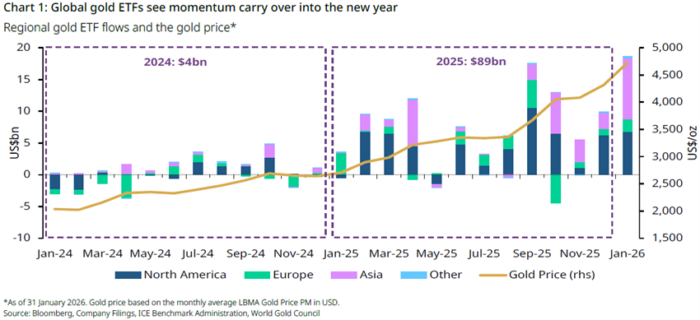

Examining the World Gold Council’s January 2026 Gold ETF Flows, global physically-backed gold ETFs attracted USD 19bn in January alone, which is the strongest month on record. Collective holdings rose by 120 tonnes to 4,145 tonnes, reaching a new all-time high, while total AUM climbed to USD 669bn.

Importantly, this acceleration did not emerge overnight. Since mid-2024, investor demand has been steadily rebuilding across regions. Over the course of 2025, global gold ETFs attracted USD 89bn in net inflows, marking a powerful re-engagement with the asset class.

The crucial nuance? Flows are no longer confined to one geography. All regions recorded net inflows over the last three months, as has occurred for most of the last couple of years. Visibly, North America and Asia led the charge, as Europe joined with its third consecutive month of inflows.

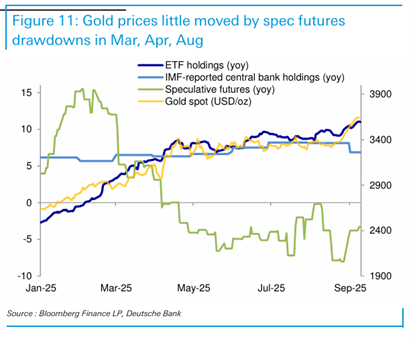

In previous cycles, ETFs tended to “puke” in downtrends. This time, they appear structurally stickier, as even during the late-January volatility investors kept buying the dips.

Why? Because the macro backdrop has changed. Our prior work on monetary transition and institutional stress – from the Fed Chair race and the broader policy narratives to the silver squeeze and industrial demand – has highlighted a critical shift: gold is no longer simply a hedge against inflation; it is increasingly a hedge against the system itself.

Naturally, in such an environment, ETF allocations may reflect strategic rebalancing rather than tactical trading. This behavior suggests something deeper than tactical speculation.

Zooming out reveals a critical distinction between 2025 and January 2026.

2025: North America Dominates

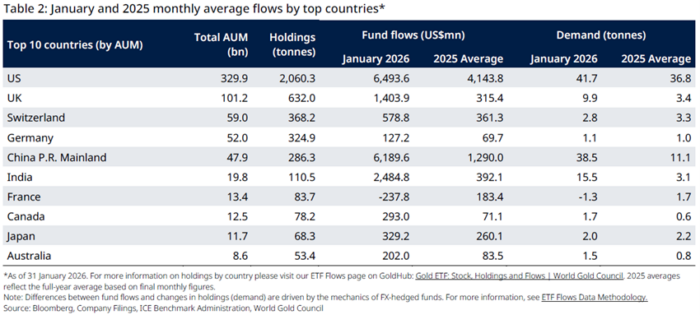

Over the full year 2025, North American funds attracted nearly double the net inflows of Asian funds on average. The US alone averaged USD 4.1bn in monthly inflows in 2025, compared to China’s USD 1.29bn monthly average.

In other words, the Western bid returned first.

January 2026: Asia Surges

January told a different story. Asian funds attracted USD 10bn, their strongest month on record, accounting for 51% of global net inflows. That is especially remarkable considering that Asian ETF holdings are only about one-fifth the size of North America’s.

Despite that, North America still posted substantial inflows, amounting to USD 6.8bn in January, as the US remained the single largest country-level contributor at USD 6.49bn. However, at the regional level, Asia was the dominant force, marking a clear shift in momentum.

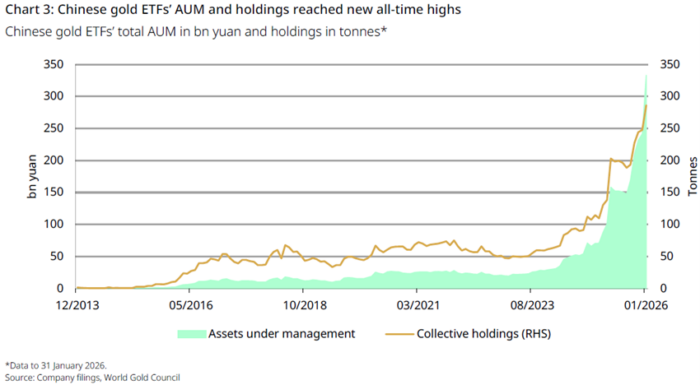

Nowhere has this shift been more visible than in China. The World Gold Council’s January 2026 update shows that Chinese gold ETFs added RMB 44bn (USD 6.2bn), equivalent to 38 tonnes, in a single month, which is also the strongest start to a year on record. As a result, assets under management jumped to RMB 333bn (USD 36bn), while holdings surged to 286 tonnes, leading both categories to all-time highs.

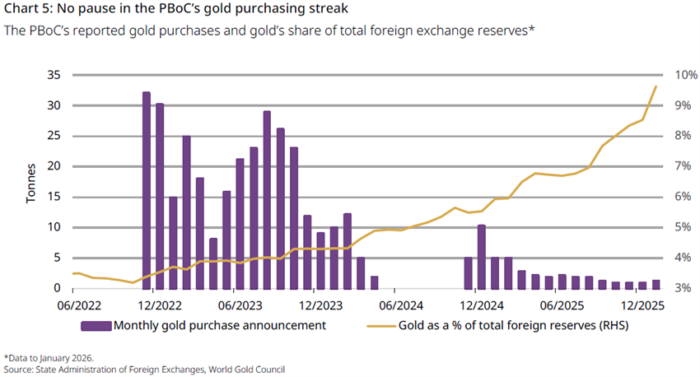

Meanwhile, the People’s Bank of China continued its steady accumulation, adding 1.2 tonnes and bringing official holdings to 2,308 tonnes, or 9.6% of total reserves.

Be that as it may, here is the key distinction: the incremental impact of ETFs dwarfed the incremental impact of official buying in January.

In a nutshell, while central banks are steady accumulators, ETFs are now accelerants. As the PBoC’s purchases reinforce the floor, ETF inflows raise the ceiling.

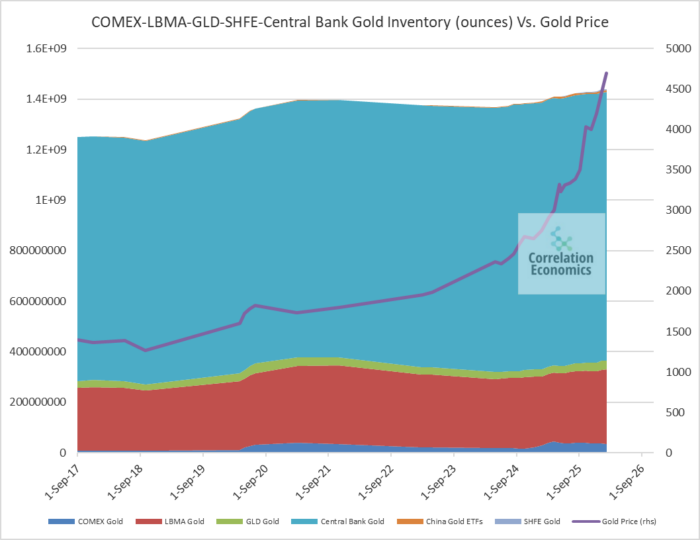

Although it is true that China’s total gold holdings – both official and ETF – remain small relative to Western inventory pools at the LBMA, COMEX, central banks and major global ETFs, as the chart below shows, that fact hardly tells the whole story. Basically, price is not set by stock, but by flow.

Even modest incremental demand from China can matter disproportionately when Western inventories are already tightly managed and structurally allocated. In a market where bullion banks are covering shorts and physical liquidity is thinner than headline numbers suggest, marginal buying power carries leverage.

In that sense, Chinese ETF growth represents a shift in the geography of price pressure. Despite physical demand being cleared through Western hubs, the strategic intent is progressively Eastern.

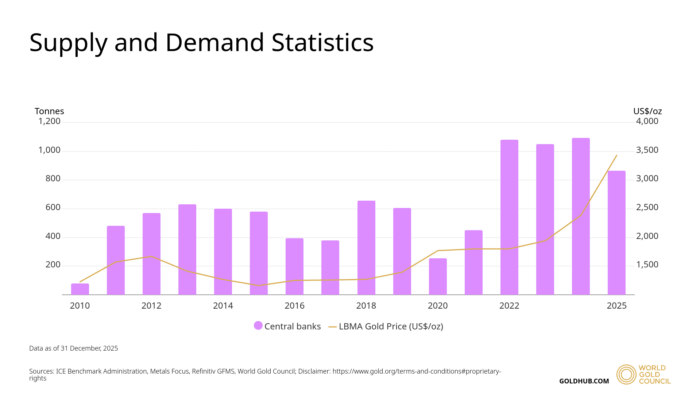

Since 2022, central banks have been adding roughly 1,000 tonnes annually, largely insensitive to price. This steady sovereign bid underpins the long-term thesis.

The PBoC’s 15th consecutive monthly purchase underscores that gold is no longer a residual reserve asset. Instead, it is being treated as strategic ballast in a fragmented monetary order.

In any event, central banks are not chasing momentum. In truth, they are accumulating deliberately.

The difference in tempo between official demand and ETF flows explains recent price acceleration. Whereas one is structural, the other is tactical, and increasingly aggressive.

Deutsche Bank’s analysis also reinforced something we have emphasized repeatedly: sovereign bond yields and inflation fears remain the dominant macro driver of gold, while the dollar’s explanatory power has faded. That finding aligns with our broader macro framework.

The uncertainty surrounding the future Federal Reserve leadership, the growing perception of fiscal dominance, and intensifying geopolitical fragmentation all contribute to structurally lower real yields and elevated inflation expectations. In short, declining local yields in China, rate-cut expectations globally, and heightened geopolitical risk have combined to create fertile conditions for gold allocations.

Essentially, ETF buyers are responding to a macro regime shift. Unquestionably, investors have taken a while to wake up to this new paradigm. At any rate, they’re now making up for lost time.

The crucial question is behavioral. Will ETF investors behave as they did in prior cycles by exiting aggressively during drawdowns? Or has gold’s rationale changed? Our thesis leans toward the latter.

The post-2022 environment has sensitized investors to sovereign debt trajectories, fiscal expansion, and institutional fragility. Clearly, gold is viewed increasingly as a vital portfolio insurance mechanism, not a simple alternative asset to raise diversification parameters.

In our opinion, if equity markets falter, ETF flows may prove more resilient than in prior tightening cycles. In this scenario, gold’s negative correlation profile may strengthen, precisely when traditional risk assets weaken.

Apparently, in spite of central banks having built the foundation, ETFs are erecting the superstructure of this bull market.

As January’s explosive growth in Chinese gold ETFs demonstrates, investor demand has become central to the price discovery of gold, along with silver. While official buying remains steady and price-insensitive, ETF flows are increasingly acting as price makers.

Furthermore, although China’s holdings remain small relative to Western inventory pools, marginal demand – particularly when synchronized with Western ETF inflows – is sufficient to push prices into uncharted territory.

In summary, gold’s secular bull run is a function of economic uncertainty, high inflation and geopolitical tensions. Zooming in, the barbarous relic is at the convergence of structural sovereign accumulation and tactical investor acceleration. On this account, we’ve entered the phase of this Golden Decade when investor demand takes the helm.

#GoldInvesting #GoldDemand #GoldETFs #PreciousMetals #Commodities #ChinaMarket #PhysicalGold #SpeculativeBehavior #FundFlows #CentralBanks #PBoC #MonetaryPolicy #InterestRates #DebtGrowth #FiscalProfligacy #WestVsEast #EmergingMarkets #HardAssets #SafeHaven #InflationHedge #MarketTrends #EconomicInsights #MacroResearch #InstitutionalCredibility #Geopolitics #PortfolioStrategy #AssetAllocation #RiskManagement #BullMarket #GoldenDecade #TheBigLong