Inflation and Investment

„No subject is so much discussed today – or so little understood – as inflation.“

Henry Hazlitt

The trend in price inflation has decisive effects on the performance of different asset classes and is one of the most important variables determining success or failure of an investment strategy. It nevertheless appears as though this parameter has been neglected in recent years. The reason for this is probably that the secular disinflationary trend – the “Great Moderation”- which has prevailed since the early 1980s is perceived as the normal state of affairs.

Only very few active investors still remember the devastating inflation, respectively stagflation, that developed nations experienced in the 1970s. Neither the inflationary period of the 1970s, nor the disinflationary era that followed were predicted, and it appears as though the tendency of inflation continues to play a subordinate role in the eyes of most market strategists, in spite of the fact that it was responsible for the worst performance of stocks and bonds in 80 years (1966 – 1981), followed by the best two decades these asset classes ever experienced.[1]

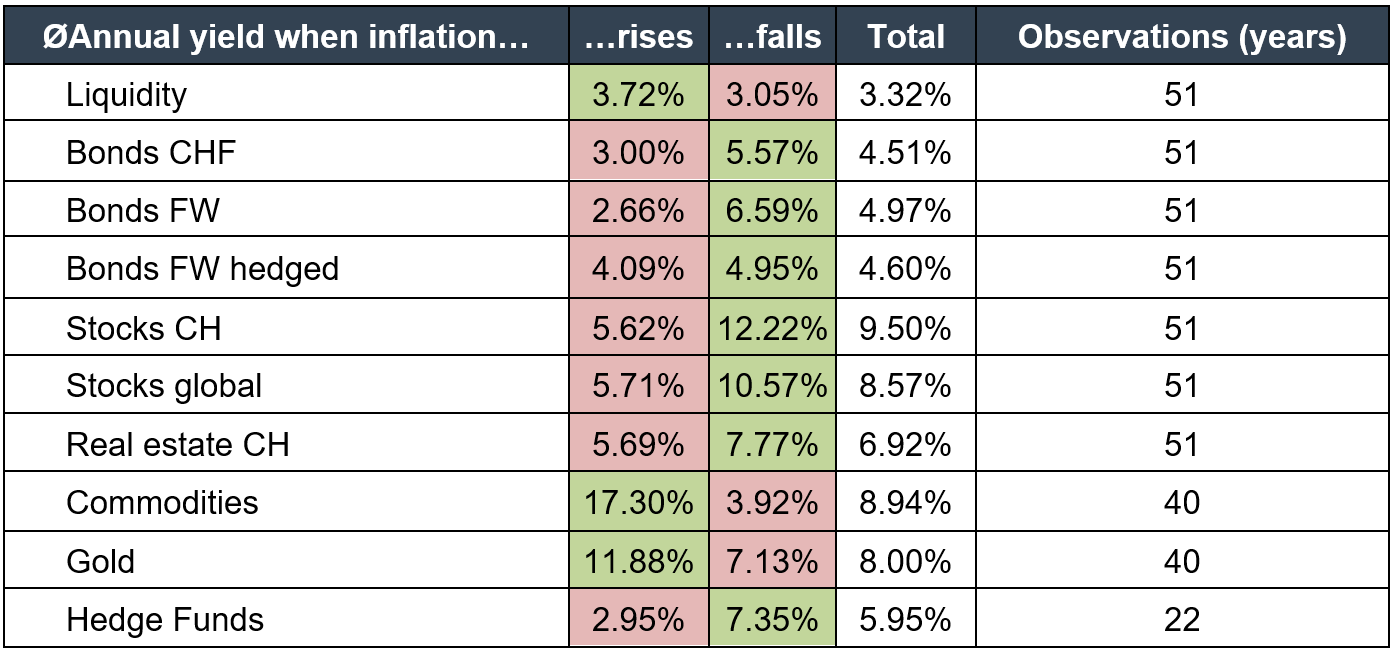

We have already discussed the inflation-sensitivity of different asset classes in 2014. At the time we considered their behavior from the perspective of US investors.[2] On the other side of the Atlantic the impact of inflation trends on different asset classes can be shown as well. An interesting study has been presented in a research paper by Swiss investment consultancy PPC Metrics.[3] The authors of the study analyze the consequences of accelerating and decelerating inflation rates on the annual returns of different asset classes. The result: In Switzerland most asset classes receive a tailwind from decelerating inflation rates (disinflation) as well. However, when inflation rates accelerate, it is primarily gold and commodities which exhibit a positive performance.

Source: PPC Metrics

In the following section, we will analyze various aspects concerning inflation and investment strategy.

a. Misunderstood inflation

“Inflation is a twisted magnifying lens through which everything is confused, distorted, and out of focus, so that few men are any longer able to see realities in their true proportions.”

Henry Hazlitt

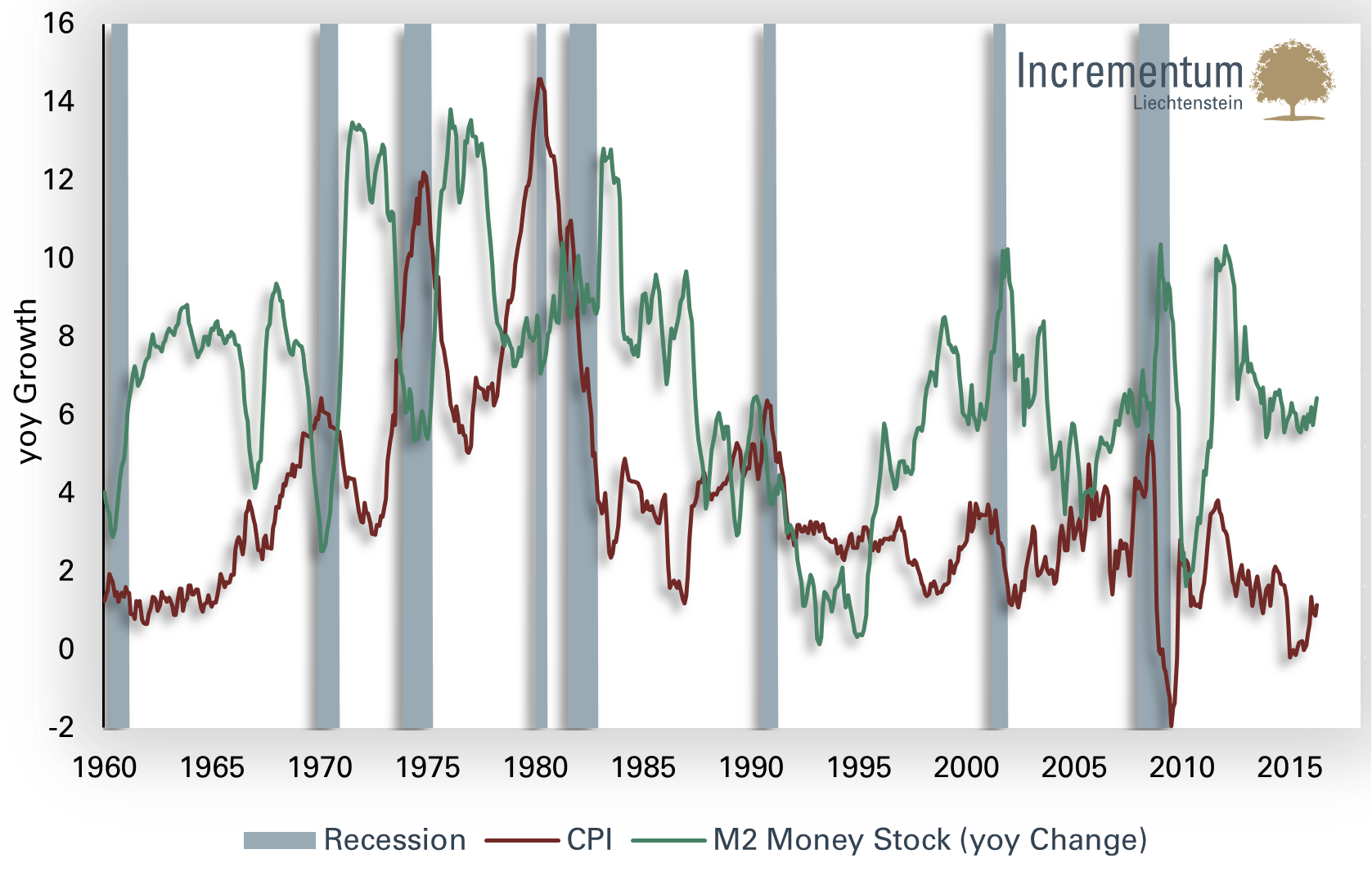

When we discuss inflation in our reports, we never tire of stressing the difference between monetary inflation and price inflation. Many readers may regard this as a pedantic exercise in hair-splitting, but we believe that this analysis is essential for a comprehensive understanding of the issue. Monetary inflation is the cause, price inflation is its consequence.

It is easy to understand that the “general level of prices” cannot permanently increase in a monetary system with a fixed money supply. While the price of a good that becomes scarcer would rise in such a monetary system, this would be balanced by the decline in the price of another good with a more plentiful supply. Prices would therefore only change relative to each other. An increase in the prices of all goods only becomes possible when either the overall level of production falls with a constant money supply, or if the money supply is not constant, but expands – or more correctly stated, when it expands at a faster pace than the supply of goods. Generally, the money supply therefore tends to rise faster than the “price level”.

Consumer price index vs. monetary aggregate M2, y/y rate of change

Source: Federal Reserve St. Louis, Incrementum AG

However, the situation is by no means trivial; it is not possible to derive the rate of price inflation directly from a comparison of the rate of money supply inflation and the growth rate of the supply of goods (and services). Several difficulties will arise.

A practical problem is already posed by the definition of the first variable, the money supply. In today’s monetary system the bulk of the money supply is created by commercial banks in the form of deposit money.

The creation of money is therefore partly in the hands of public and partly in the hands of private entities.[4] A number of different calculation methods exist in order to determine the total money supply.[5] An example are the different monetary aggregates calculated by central banks (M1, M2, etc.). In addition, there is a range of monetary substitutes in the realm of finance and so-called shadow banking complicating the matter even more.

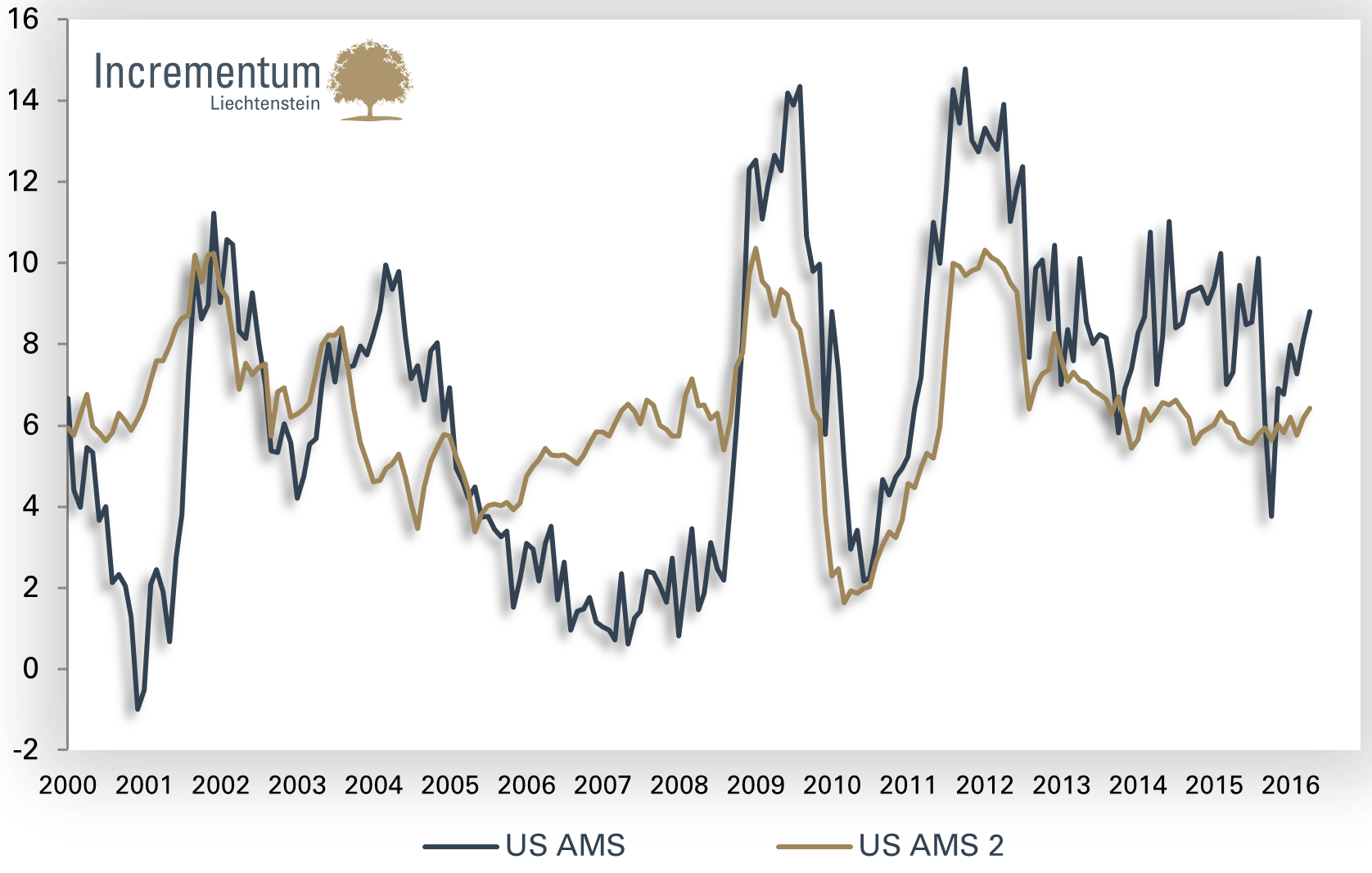

Interestingly, central banks are also not of one mind as to how these money supply aggregates should be correctly defined. Their calculation methods differ significantly. Apart from the monetary aggregates published by official bodies, there are also private sector analysts devoting themselves to the calculation of money supply growth. A leading analyst in this area is our advisory board member Dr. Frank Shostak, who is strongly focused on the calculation, comparison and effects of monetary inflation in research published by his economic and financial analysis firm “Applied Austrian School Economics” (AASE).[6]

US Austrian Money Supply (AMS) – % change yoy

Source: Applied Austrian School Economics, Dr. Frank Shostak

Apart from the problem that the money supply cannot be unambiguously quantified in today’s fractional reserve banking system, there are several more reasons why money supply inflation isn’t directly proportional to price inflation. Above all we want to emphasize the following reasons:

- Methodological problems associated with the measurement of consumer price inflation (composition of the basket of goods, decreasing quality of goods, “shrinkflation” [7], hedonics and imputed values to mention a few)

- Changes in preferences toward either hoarding money (i.e., an increase in the demand to hold money), or toward spending, which affects demand and has an effect on prices as well[8]

- The official inflation rate only takes the rate of change in consumer prices into account. Changes in asset prices are not considered (primarily investment assets and capital goods, but also art prices, etc.)

- Last, but not least, it is important for the reader to note that the general level of prices does not exist in real life. It is a mere academic exercise and obviously a very poor guiding light to direct monetary policy.

b. The Holy Grail of Monetary Policy

“Central banks’ exclusive focus on consumer prices could even be counter-productive. Such a monetary policy can undermine efficient capital allocation, promote malinvestment, distort the economic structures, hamper growth-stimulating creative destruction, increase risk appetites and lay the foundation for future monetary instability.”

Axel Weber

Since the 1990s, inflation targeting[9], i.e., the pursuit of price inflation objectives, has become a fundamental monetary policy strategy of central banks. Since price inflation rates only refer to a small and rather arbitrarily selected subset of all prices, which can only be controlled very imprecisely (if at all) and with large time lags by means of monetary policy, the strategy doesn’t appear to make much sense. Hayek time and again stressed that the targeting of macroeconomic variables is not a suitable means for achieving greater economic stability, but was more often likely to have the opposite effect.

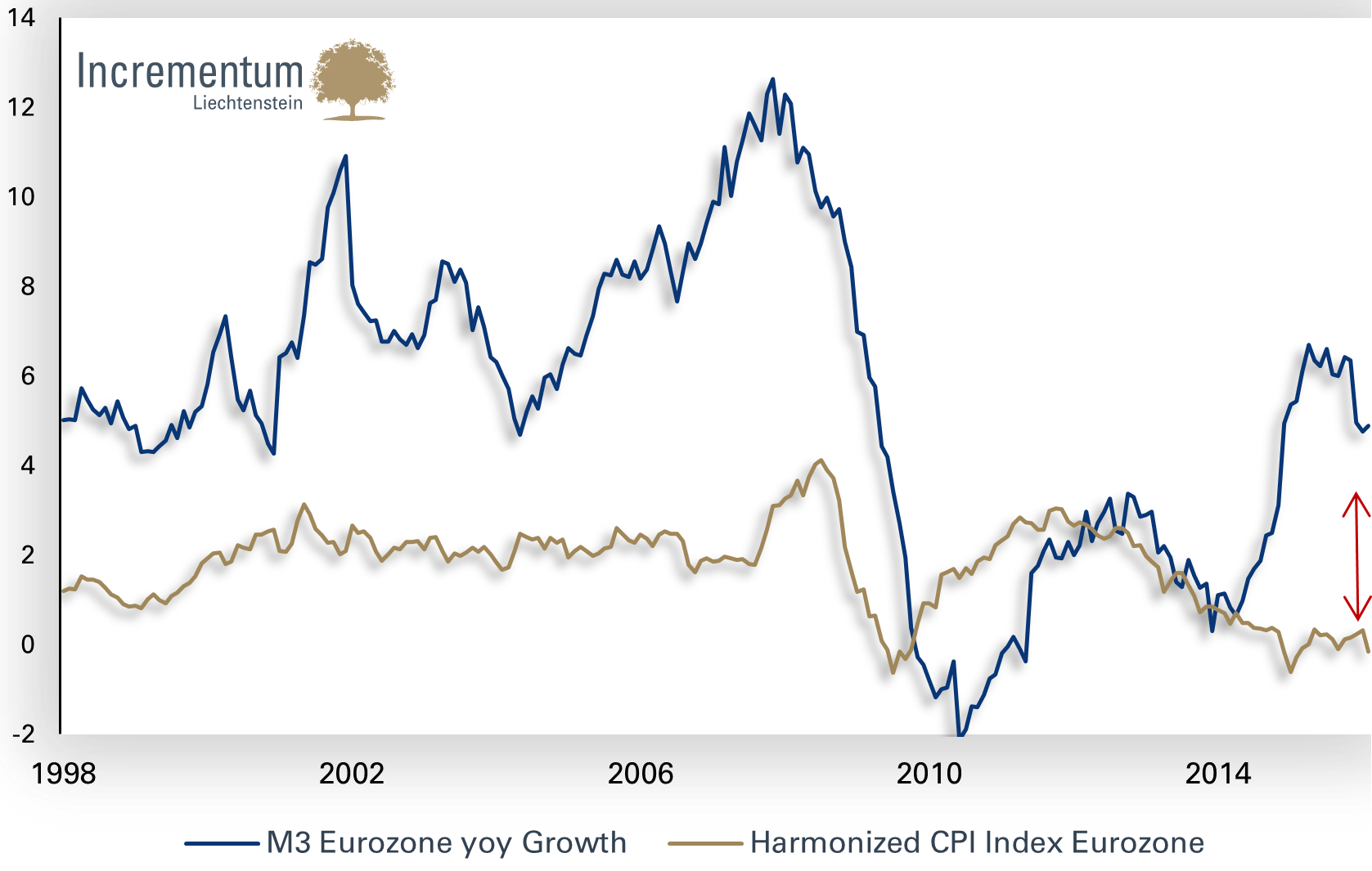

The European Central Bank is the most important central bank that has focused its monetary policy primarily on achieving an inflation target. As is well known, the ECB’s main goal is to generate consumer price inflation at, or just below, 2% per year. In line with the thought experiment presented above, the money supply will have to increase at a commensurately faster pace in order to ensure that the “price level” increases at this rate of change.

It is far less well-known that in addition to its price inflation target the ECB pursues a money supply growth target as well. When the ECB was established, the reference growth rate for the monetary aggregate M3 was set at 4.5% p.a. (at the insistence of the German Bundesbank).[10]

The idea behind this was:

4.5% money supply growth – 2.5% potential GDP growth = 2% price inflation = price stability according to the ECB’s definition

While the ECB was initially able to achieve a rate of consumer price inflation fairly close to its desired target, the volatility of price inflation has increased significantly since 2008. Moreover, prior to 2008, the growth rate of the money supply aggregate M3 stood noticeably above the reference value of 4.5% p.a.

Euro area: M3 and harmonized index of consumer prices (HICP), y/y

Source: Federal Reserve St. Louis, Incrementum AG

It is obvious from our perspective that the disproportionate growth rate of M3 in the time period before 2008 was the root cause of various bubbles and misallocations of capital. In fact, it seems to us that it represents a textbook example of Austrian business cycle theory (ABCT). Asset price inflation in the euro area until 2008 is well documented, one only needs to remember the legendary booms in property prices in e.g. Spain or Portugal.

At present the reference value of 4.5% growth for M3 is once again exceeded significantly, led by rapid growth in narrow indexes such as M1 and to a lesser extent M2, while consumer price inflation has missed its 2% target for several years running already – in recent years it has been stuck in a range from 0% to 1%. This suggests that the difference between strong money supply growth and relatively low consumer price inflation has primarily become manifest in the form of asset price inflation. Knowing M1 is growing faster than M3 substantiates our argument. This time the focus appears to be on real estate in the northern half of the euro zone, as well as bonds. Rental yields are following the general level of interest rates consistently, which have by now reached absurd levels.

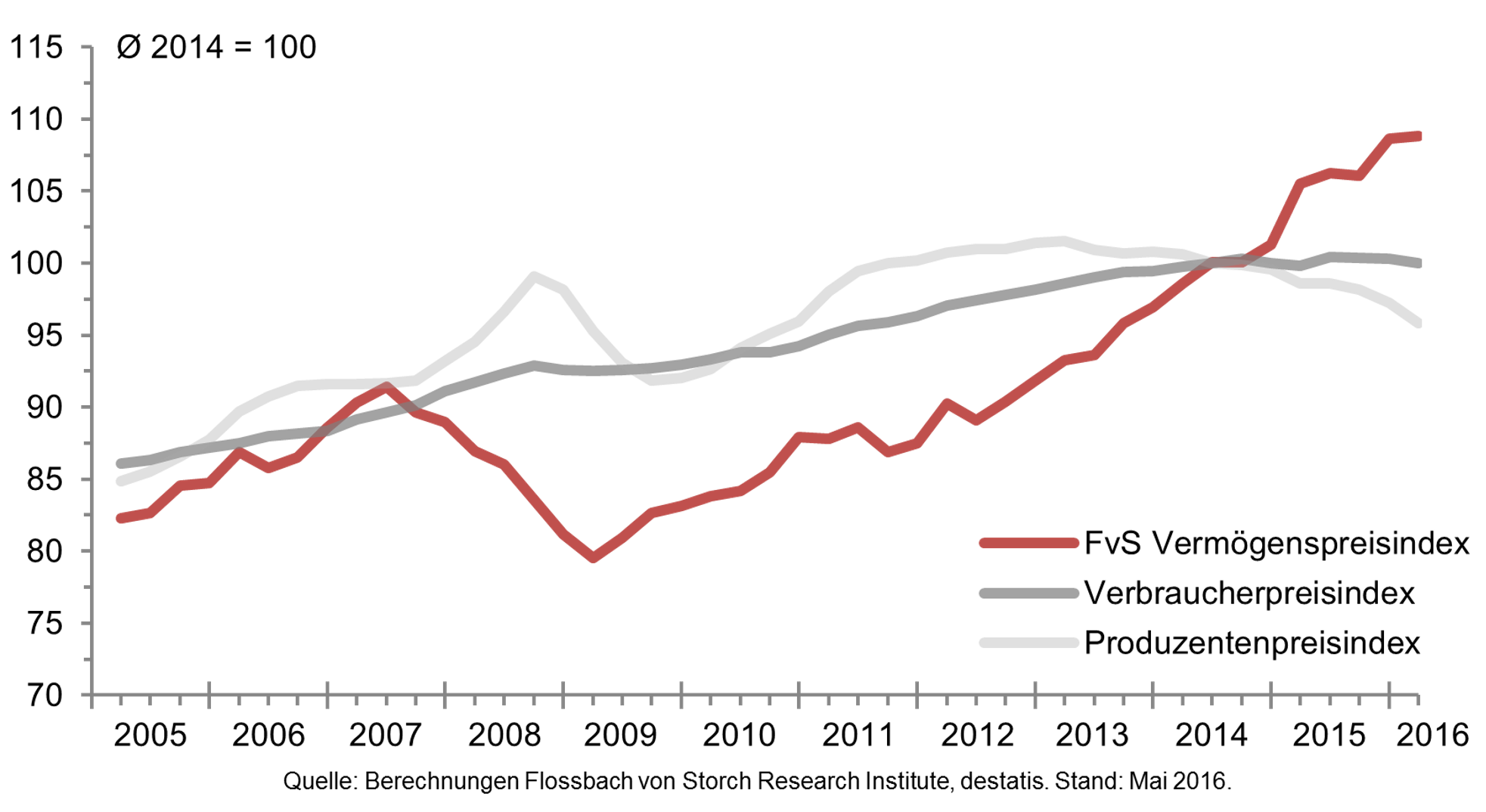

This is confirmed by numerous indexes as well. According to calculations by asset manager Flossbach von Storch (FvS)[11] asset price inflation amounted to 7.8% last year, the highest level since the statistics were first compiled. While the prices of financial assets practically stagnated (+0.7%), asset price inflation was driven to a record high by price increases in tangible assets (+9.5%). The main driver was real estate, which represents the largest part of German household wealth and rose in price at a never before seen pace. The prices of business assets (+24.5%), as well as collectibles and speculation goods (+15.4%) rose sharply as well. Stock prices rallied by 5.8% on average, while bonds lost 2.2% compared to the previous year.

The Cantillon effect is convincingly reflected by the FvS index as well. Thus rich households clearly benefited disproportionately from these price trends, as the value of their assets increased on average by 10.4%. The differential between asset price and consumer price inflation (+0.3%), resp. producer price inflation (-2.4%) reached a new record high as well. It is also interesting that young households are benefiting to a much smaller extent from asset price inflation than older ones. The reason for this is the relatively small share of their total wealth represented by real estate, as well as the relatively large share represented by savings deposits.

FvS asset price index (red line) vs. consumer price index (dark grey line) and producer price index (light grey line)

Source: Flossbach von Storch Research Institute

Why is it that central banks, instead of boosting consumer prices, have triggered an avalanche of asset price increases? One possible explanation for this phenomenon is that in previous economic cycles, reflation was achieved through conventional monetary policy and thus through credit expansion. The latter affects the real economy more quickly and soon leads to rising consumer prices. This time reflation was attempted directly by means of securities purchases, which primarily affected asset prices, but failed to sustainably boost consumer prices.

However, it appears now as though the ratio has turned. The baton could well be in the process of being passed from asset prices to consumer prices. We will discuss the associated consequences in the following chapters.

c. “The dollar is our currency, but it’s your problem”

“The problem we see (as do a growing amount of others) is failure in real terms. The mechanical solution above is currency dilution, which is another way of saying “devaluation”, which in turn is another way of saying “inflation”. We expect the post-Bretton Woods monetary regime to fail eventually in real terms, much as the Bretton Woods regime failed in 1971. Given the scale, breadth and depth of household, government and corporate leverage around the world, the necessary magnitude of central bank administered inflation would be significant.” [12]

Paul Brodsky

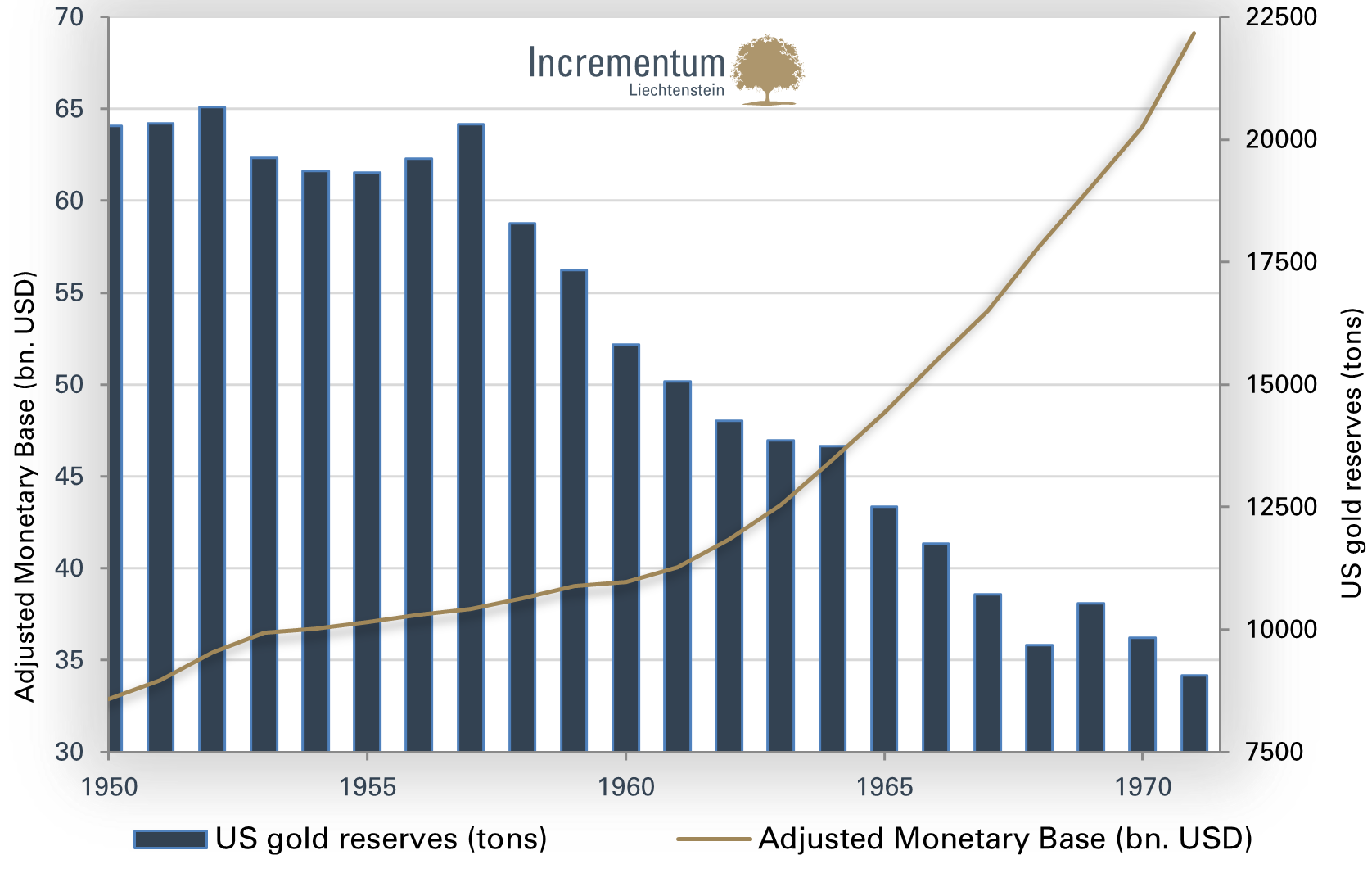

The current monetary architecture is an anomaly. In order to understand the current global monetary order and ultimately today’s situation with respect to the US dollar, commodities as well as inflation, it is worth taking a look at history. Due to the partial gold cover under the Bretton Woods system in the post war order until 1971, the precious metal remained the anchor of the global currency system and limited the ability of central banks to expand the money supply at will.

However, a partial debt money system like Bretton Woods, inherently requires steady money supply expansion as well. Governments moreover tend to expand their spending as a matter of course. Both processes conflicted with the gold cover clause. Specifically, the US balance of payments deteriorated at the time due to military expenditures in the context of the cold war in general and the Vietnam war specifically as well as rising welfare spending. This was the time of President Johnson’s Guns and Butter policy. US foreign liabilities exceeded the gold inventory stored with the Fed already in the 1960s – in the long term the Fed was unable to fulfil the US obligation to convert dollars into gold at the rate of USD 35 per troy ounce. Thus the de iure backing of the US dollar was undermined, while de facto the US dollar became exclusively dependent on the confidence of foreign governments. This confidence started to decline: in the 1960s foreign central banks decided to increasingly convert their dollar reserves into gold and the pressure on the Bretton Woods system increased steadily. Finally, what had to happen, happened, and – citing specious arguments – the US unilaterally abandoned the dollar’s gold convertibility.

US gold reserves and adjusted monetary base from 1950 to 1970

Source: World Gold Council, FRED, Incrementum AG

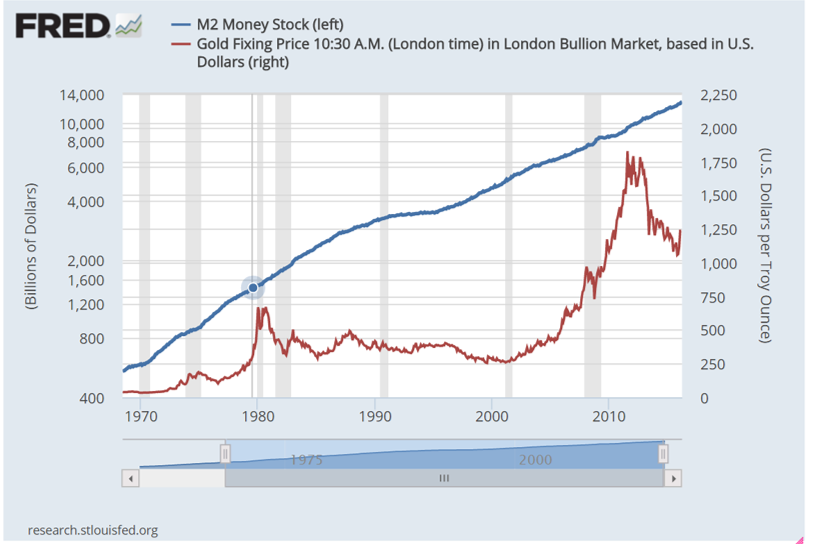

The end of the gold exchange standard had far-reaching consequences. Gold’s characteristics as an investment asset have essentially reversed following the severing of its tie to the dollar. Once the price of gold was no longer tied to the US dollar, it was suddenly transformed from a risk-free asset to an asset fluctuating in terms of the US dollar – and thus supposedly a risky one. Gold has therefore undergone a metamorphosis – from an anchor to a life preserver.

Gold price vs. US M2

Source: Federal Reserve St. Louis, Incrementum AG

Ever since, the gold price has been floating higher over the long term on the back of a continually swelling flood of money. However, this is happening amid the deafening roar of the volatile surf of inflationary tides, which can create short to medium term price risks for gold holders.[13] Apart from its function as a monetary anchor, during the time of the gold standard gold also provided a stable reference rate for all transactions due to the consistent size of the stock of available gold. In the framework of the Bretton Woods system gold served indirectly as the denominator and unit of account for international exchange transactions.

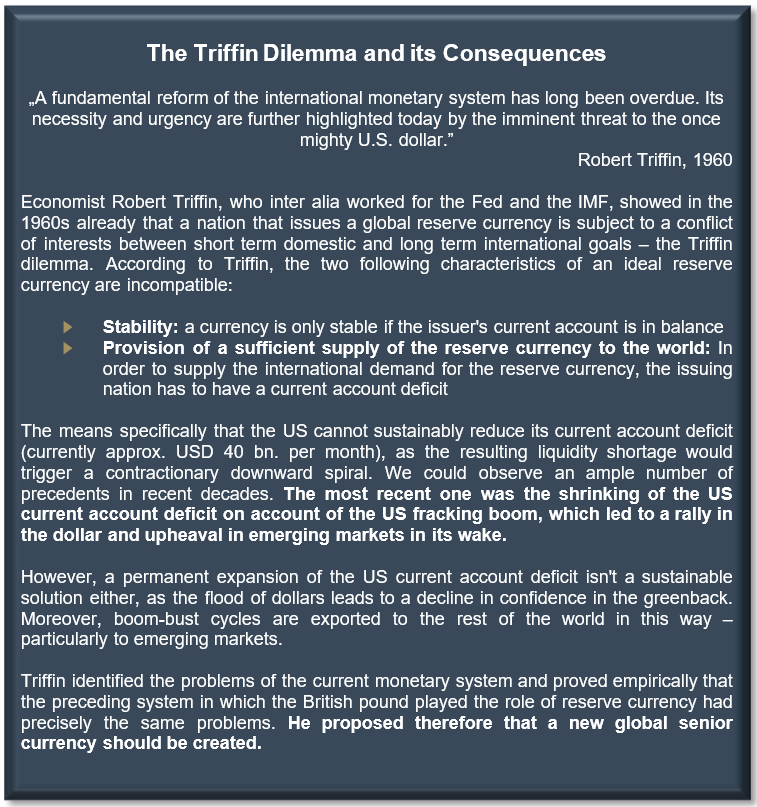

As a result of the abolition of the dollar’s gold convertibility, global monetary chaos reigned in the 1970s. The agreement between the US and Saudi Arabia regarding the settlement of oil transactions was decisive in calming the troubled waters. In particular, it promoted the continued role of the USD as the global reserve currency beyond the end of the Bretton Woods system. The previous partial gold cover was replaced by an implicit oil cover. This arrangement has since then often been referred to as the “petrodollar” system. This step, followed by the restrictive monetary policy implemented by the Fed under Paul Volcker, laid the foundation for the US dollar-centric monetary system, which, although tottering, remains with us to this day.

The US dollar’s status as the global reserve currency is highly advantageous for the US, as the country can earn a global seigniorage[14] via currency creation. As long as large parts of the world are willing to work in exchange for USD created ex nihilo, the US can purchase real goods and services by printing money.

By creating dollars out of thin air, the US dollar’s reserve currency status has decisively contributed to the greatest global macroeconomic imbalance in economic history. The privilege of being able to issue an international reserve currency was already subject to criticism in the 1960s.[15]

Nevertheless, the advantage imparted by the dollar’s reserve currency status is as a rule largely accepted as a given, and the associated systemic problems are simply shrugged off. US officials prefer to avoid the topic as well. In 2015 we witnessed two rare occasions on which the importance of the US dollar’s reserve currency status for the US was admitted at the highest levels, first by US secretary of state John Kerry[16] and then also in a speech delivered by US president Barack Obama[17]. It should definitely be assumed that maintaining the reserve currency status quo plays an important role in US geopolitical strategy.

d. Global inflation trends in a dollar-centric world

“I found myself doing extraordinary things that aren’t in the textbooks. Then the IMF asked the U.S. to please print money. The whole world is now practicing what they have been saying I should not. I decided that God had been on my side and had come to vindicate me.”

Gideon Gono, former governor of the Reserve Bank of Zimbabwe

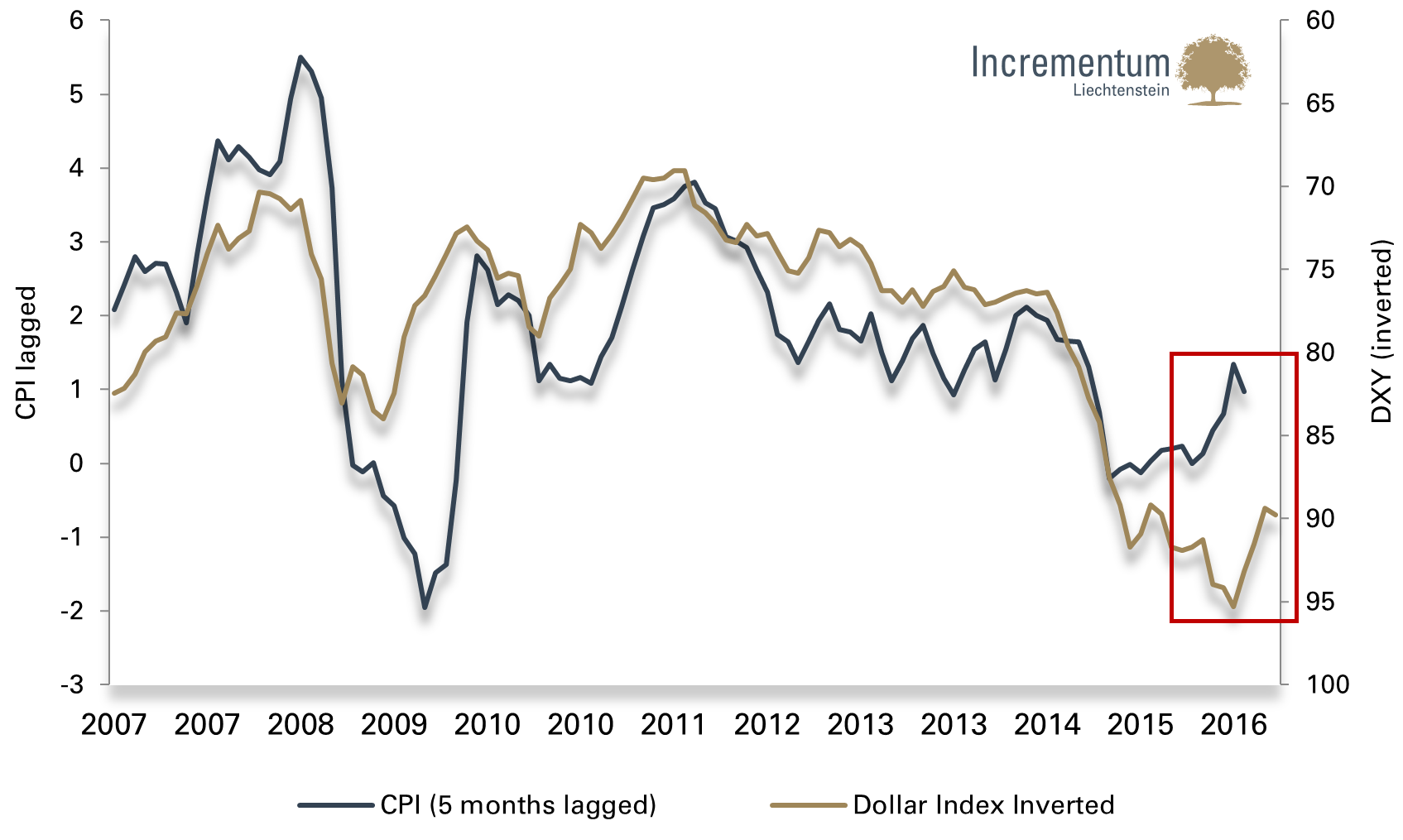

In what way is today’s monetary architecture relevant for investors? The dollar’s external value is naturally important for the trend in domestic US price inflation. As the chart below shows, there is a time lag of approximately five months before dollar appreciation or depreciation affects the trend in the US price inflation rate. Should the recent weakness in the US dollar persist, one should therefore expect US price inflation to exhibit a tendency to rise.

US CPI vs. US dollar index (lagged by 5 months, USD axis inverted)

Source: Federal Reserve St. Louis, Incrementum AG

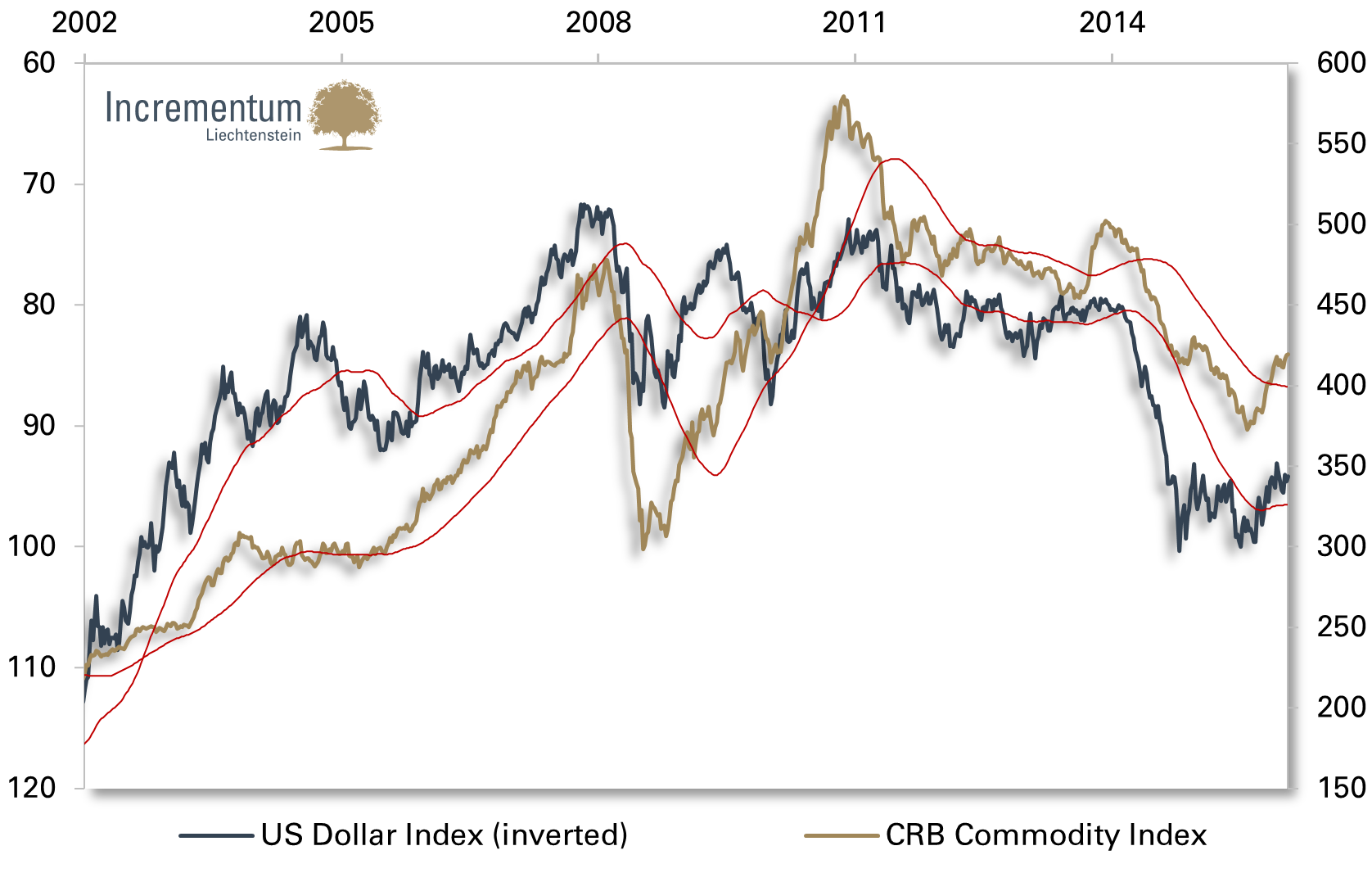

Why is the trend in the US dollar of decisive importance for international inflation trends as well? In recent years a textbook example of systemic instability could be observed. Thus, the price of crude oil declined by more than 50 percent within a mere seven months. Many analysts have attributed this exclusively to supply/demand factors, an explanation which we believe to be inadequate. All industrial commodities, as well as practically every fiat currency, have declined massively against the US dollar over the same time period. Such a simultaneous devaluation of all commodities is tantamount to a disinflationary earthquake in the current dollar-centric monetary system.

US Dollar Index (lhs, inverted) vs. CRB Index (rhs)

Source: Federal Reserve St. Louis, Incrementum AG

In our opinion commodities, as an asset class, are an antidote to the USD. There is reciprocity between the movements in commodity prices and the USD, with causality attributable to the USD to a greater extent than is generally assumed.

However, the US dollar is also a central reference value for all other currencies. While they used to be firmly anchored to gold in the previous gold-centric monetary system, they are nowadays tied to the US dollar, which is drifting like a buoy in a continually changing swell. In this role the dollar’s relative value vs. gold, respectively a broad basket of commodities plays a decisive role in global price inflation trends.

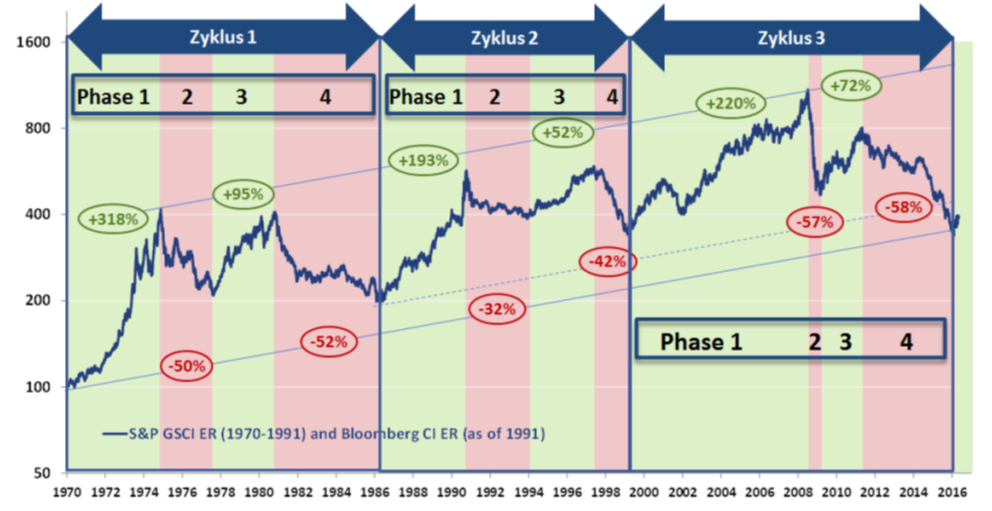

If the dollar depreciates against gold and commodities, all other currencies implicitly depreciate as well, and global price inflation will tend to rise. According to Tiberius Research, three large commodity cycles could be observed since 1971. What is interesting in this context is that the end of these cycles roughly coincided with temporary peaks in the US dollar.

Cycles in the commodity markets: the long view 1970-2016

Source: Tiberius Research, Dr. Torsten Dennin, Bloomberg

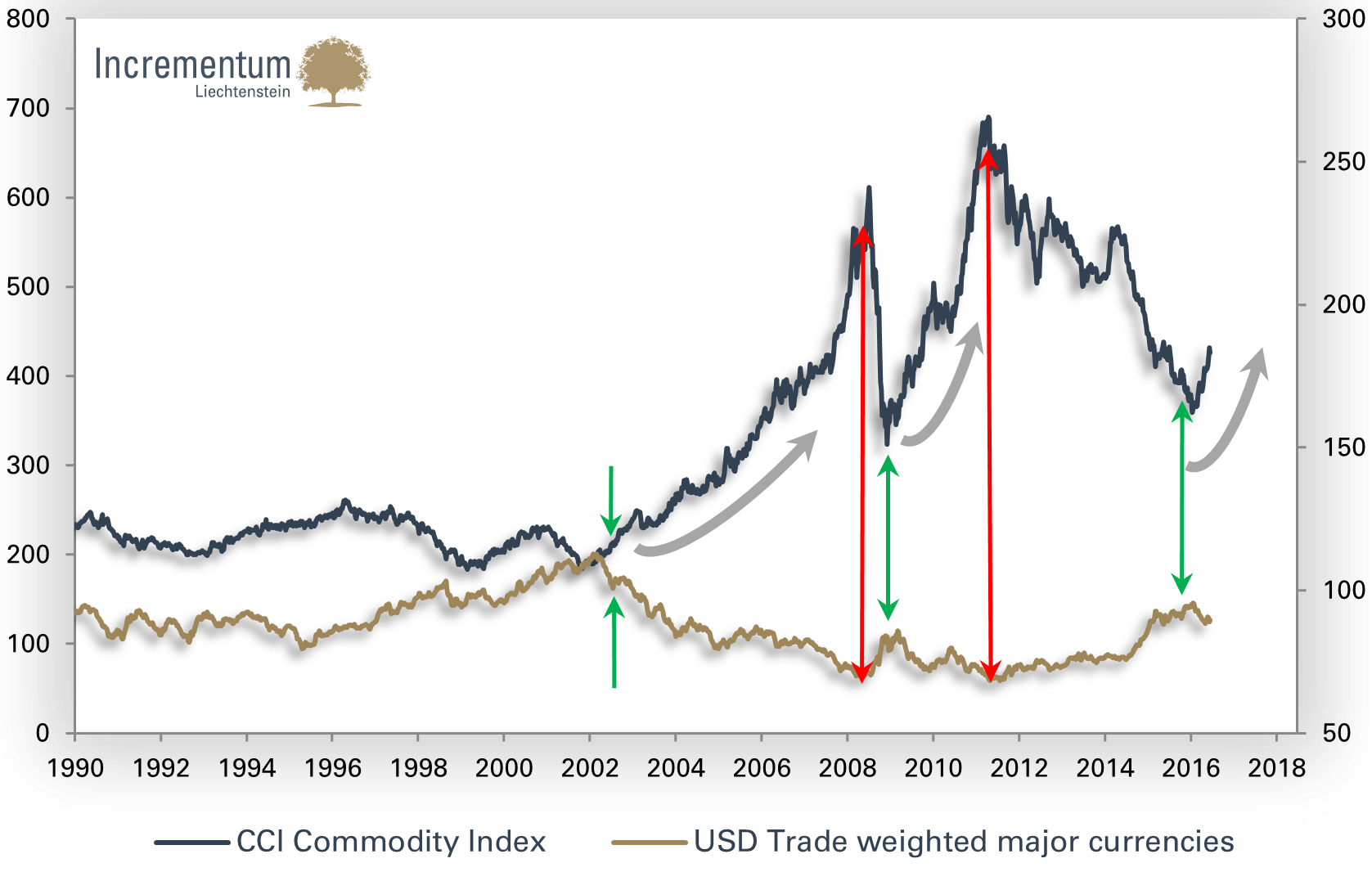

Since the 1990s, turning points in the trade-weighted US dollar index appear to coincide especially closely with turning points in commodity prices. It seems as though another such turning point has occurred in early 2016.

Trade weighted USD-Index vs. CCI Commodity Index

Source: Federal Reserve St. Louis, Incrementum AG

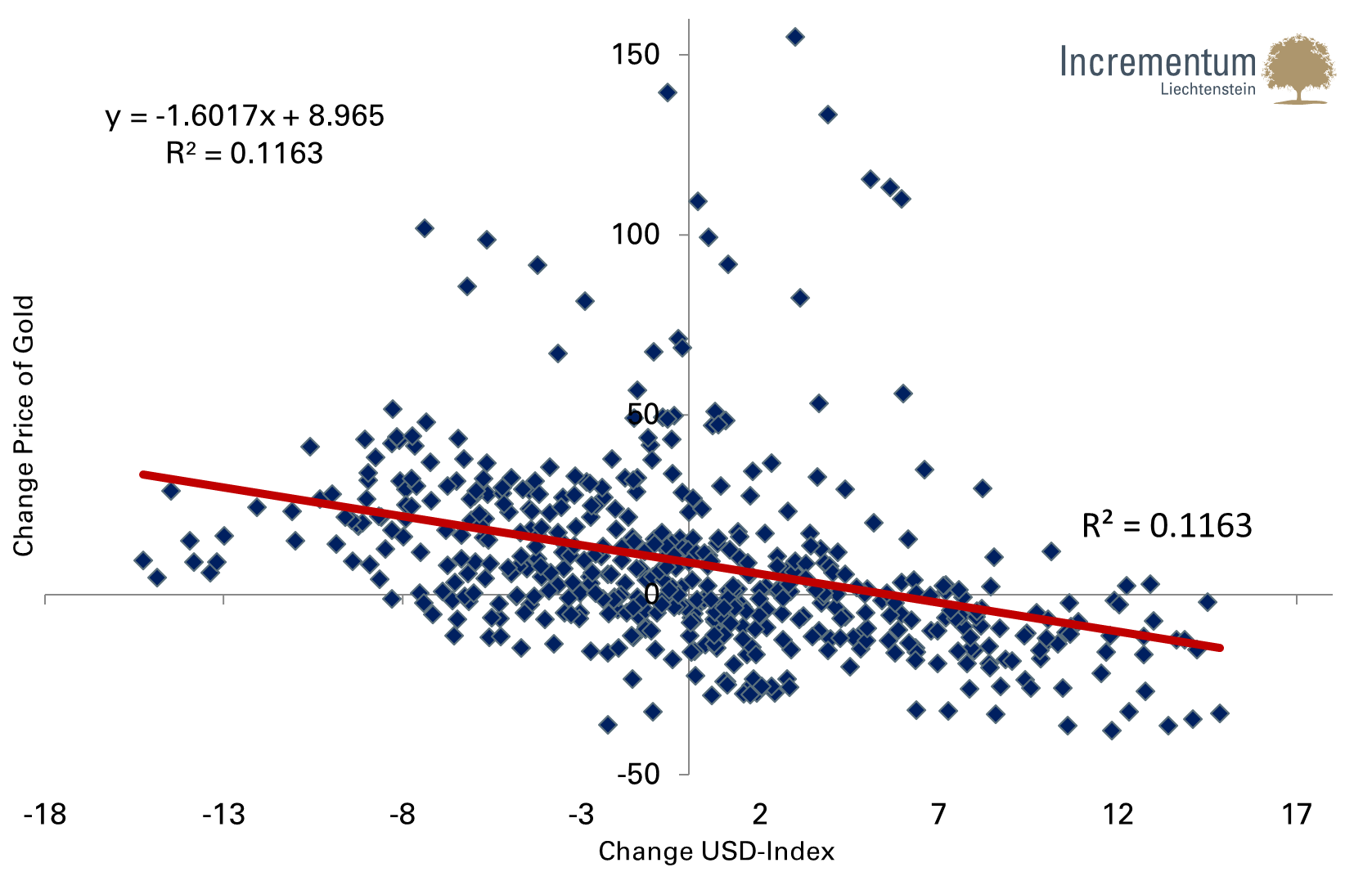

The dollar’s relationship to gold seems highly relevant as well. The following chart shows the monthly change in the gold price (vertical axis) as well as that of the trade-weighted US dollar (horizontal axis) since 1973. A negative correlation is evident, read, gold tended to do better when the dollar was weakening. The intersection of the regression line with the y-axis shows that in a dollar neutral environment, the gold price tended to increase by an average of approximately 9%. As the quadrant to the lower right illustrates, phases during which the dollar’s exchange rate was strong usually dampened gold’s performance.

The “alpha” of the gold price

Source: Incrementum AG, Fed. St. Louis

The following table shows the negative correlation between the dollar index (USDX) and the gold price quite clearly. It moreover shows that USDX and gold are not only overall negatively correlated (correlation coefficient: minus 0.63), but also that this inverse relationship is especially pronounced during bull and bear markets in the USDX.

Annual performance of the gold price, volatility, as well as correlations in different dollar regimes

Source: World Gold Council, Incrementum AG

e. Cycles of consumer price inflaton vs. asset price inflation

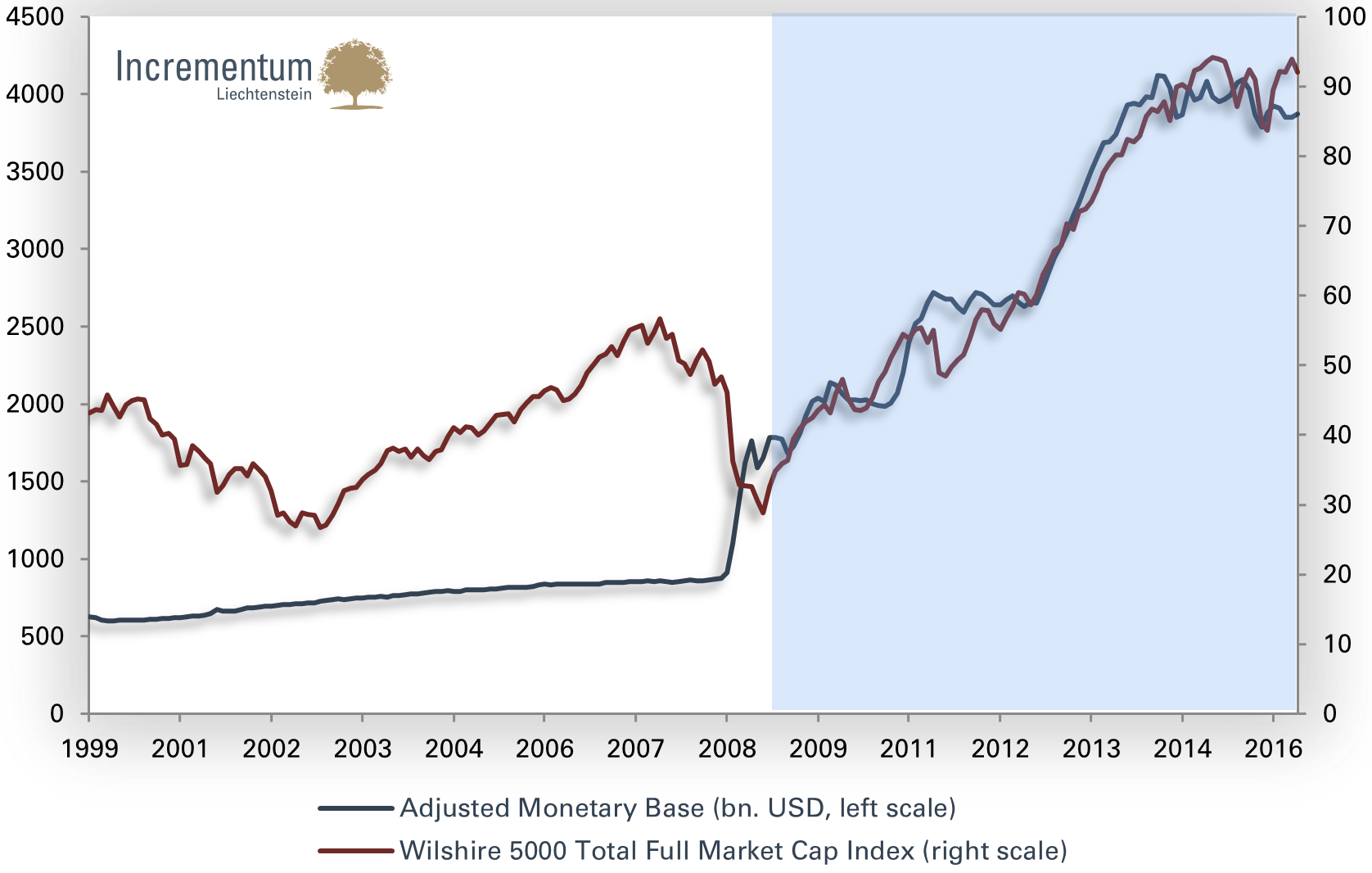

As already discussed, there are time periods during which monetary inflation has a greater effect on consumer prices, and phases during which monetary inflation is primarily affecting asset prices. The Fed’s QE programs have e.g. primarily led to asset price inflation. A debt saturated household sector does not express additional demand for credit, leaving all the central bank created money sloshing around financial markets instead of reaching the “real” economy; hence creating asset price inflation rather than consumer price inflation. The effect of monetary inflation on the trend in US stock prices is particularly conspicuous in this context. The strong correlation between the Fed’s balance sheet total and the US stock market has been in force for eight years now.

US monetary base vs. the Wilshire 5,000 Index

Source: Federal Reserve St. Louis, Incrementum AG

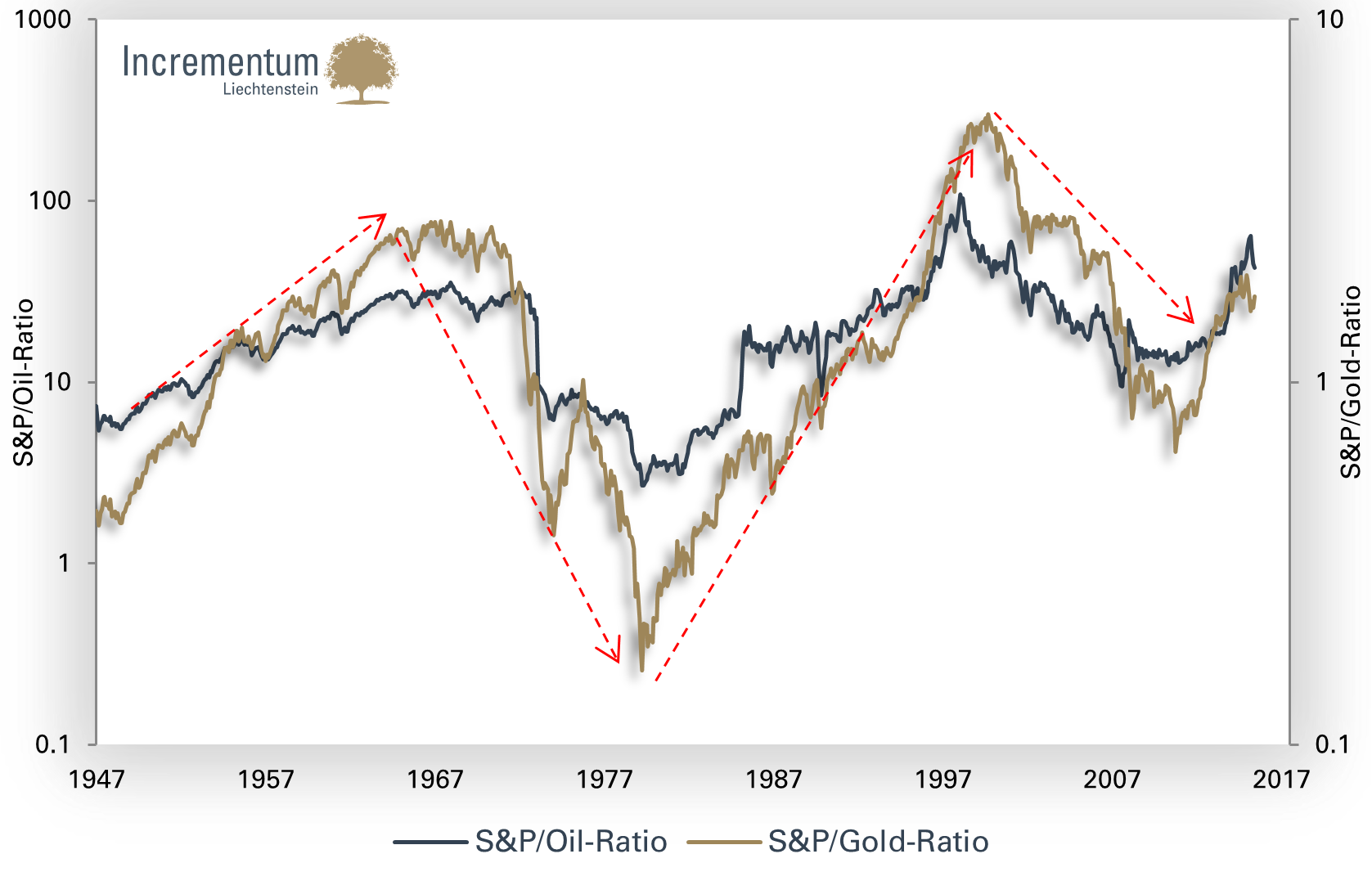

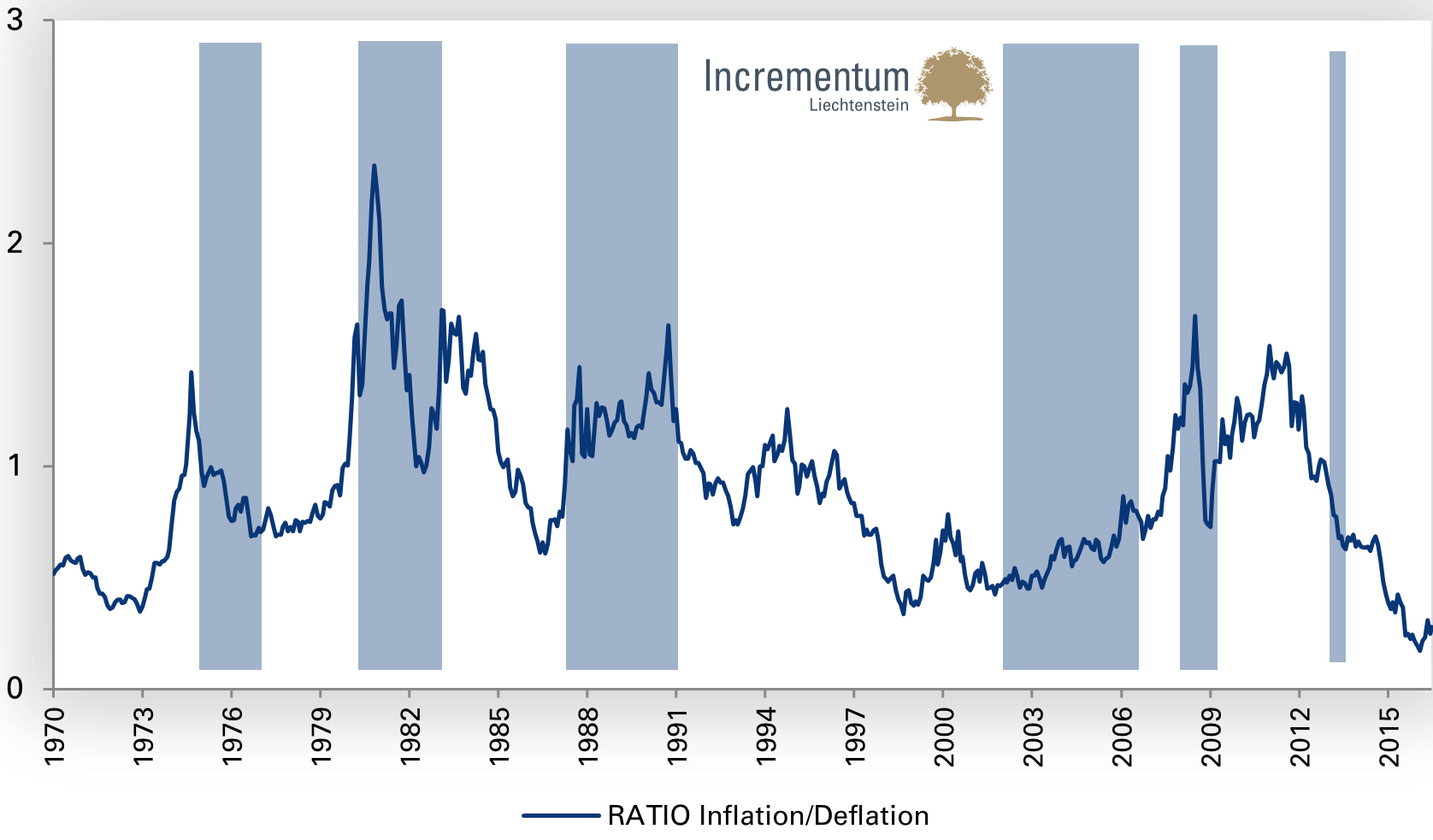

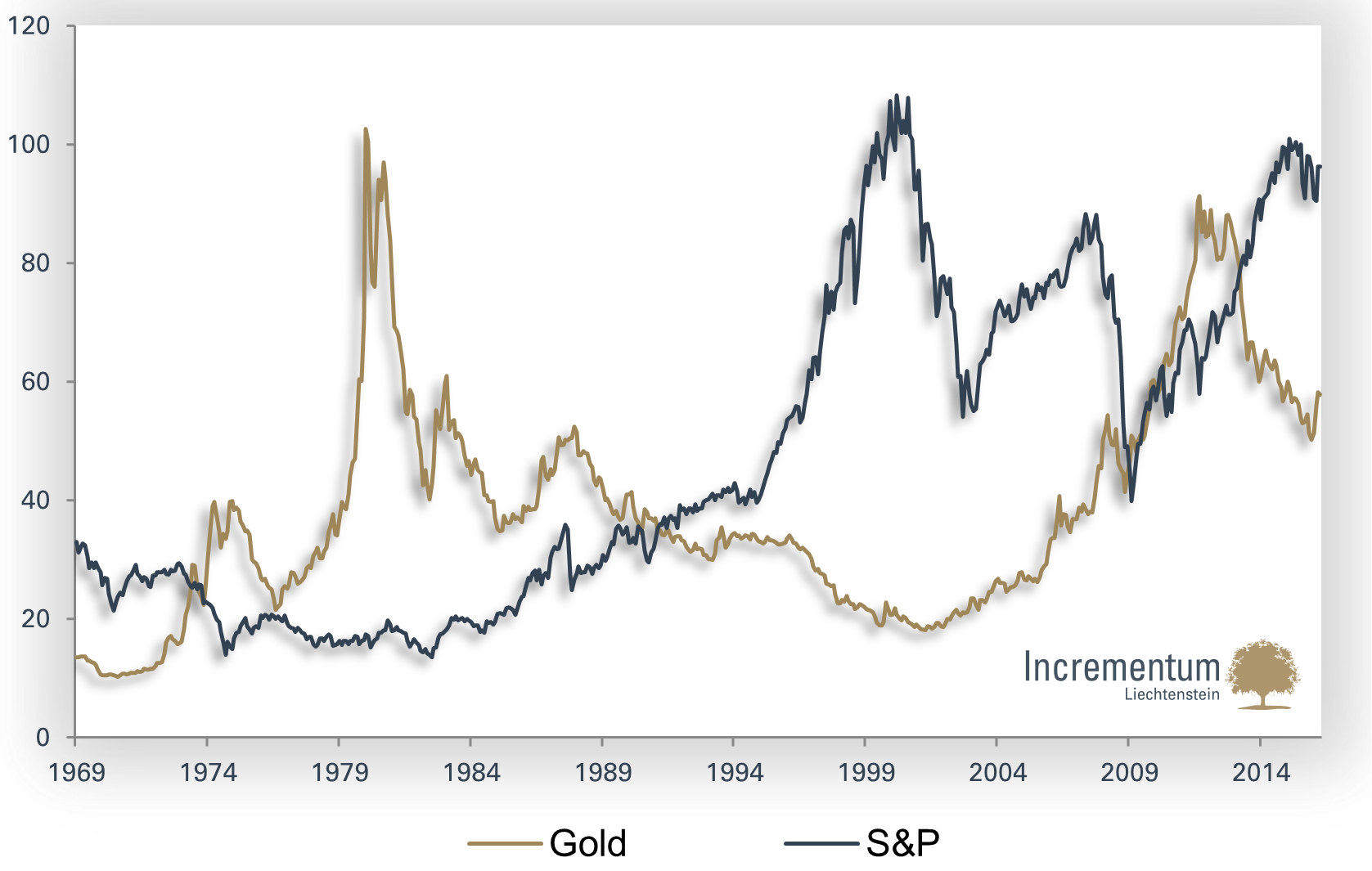

In order to examine the theory that there exist alternating long term cycles during which either consumer price inflation or asset price inflation predominates, we want to depict the two price trends relative to each other. Since we are sceptical with respect to the methodology used in the calculation of consumer prices, we are using a commodity price index as a proxy. A broad stock market index serves as the yardstick for asset prices.

S&P/Gold vs. S&P/Oil-Ratio

Source: Incrementum AG, Yahoo Finance

The insight provided by this ratio is that there have indeed been several price inflation cycles in recent years, which have manifested themselves alternately in asset prices and the prices of goods. Similar to what happened at the peaks in 1966 and 2000, another change in trend appears to have occurred at the end of 2015. This would argue in favor of the notion that inflation-sensitive assets will significantly outperform traditional asset classes such as stocks in coming years.

Many indicators are confirming this at present. Martin Pring, an iconic figure in the field of technical analysis, has developed a very interesting method of comparing different inflation phases. His Pring inflation and deflation indexes are replicating stock market sectors that are sensitive to changes in inflation. Deflation-sensitive stocks include banks, utilities and insurance companies, while inflation-sensitive stocks include mining and energy stocks. The highlighted periods show a rising ratio, which indicates that inflation-sensitive stocks are outperforming.

Ratio of inflation- /deflation-sensitive stocks

Source: Martin Pring, Incrementum AG

We believe that the radical reflation efforts of central banks are slowly beginning to succeed. As we have already noted in previous reports, this is however a dangerous game, as it is hardly possible to keep the momentum of inflation under control. The widespread belief that central banks can easily and at any time push the “inflation genie” back into the bottle is based on numerous erroneous assumptions. For instance, the time lags attending an inflationary process are greatly underestimated. As mentioned above, significant monetary inflation has already taken place, but has so far “only” affected asset prices. It is quite strange that rising food prices are usually regarded as a calamity, while rising house prices are considered a blessing. Both cases are simply a symptom of declining purchasing power – whether it finds expression in house prices or food prices is irrelevant in this context.

f. Criticism of the calculation of inflation

“Inflation makes it possible for some people to get rich by speculation and windfall instead of by hard work. It rewards gambling and penalizes thrift… It finally tends to demoralize the whole community. It promotes speculation, gambling, squandering, luxury, envy, resentment, discontent, corruption, crime, and increasing drift toward more intervention which may end in dictatorship.”

Henry Hazlitt

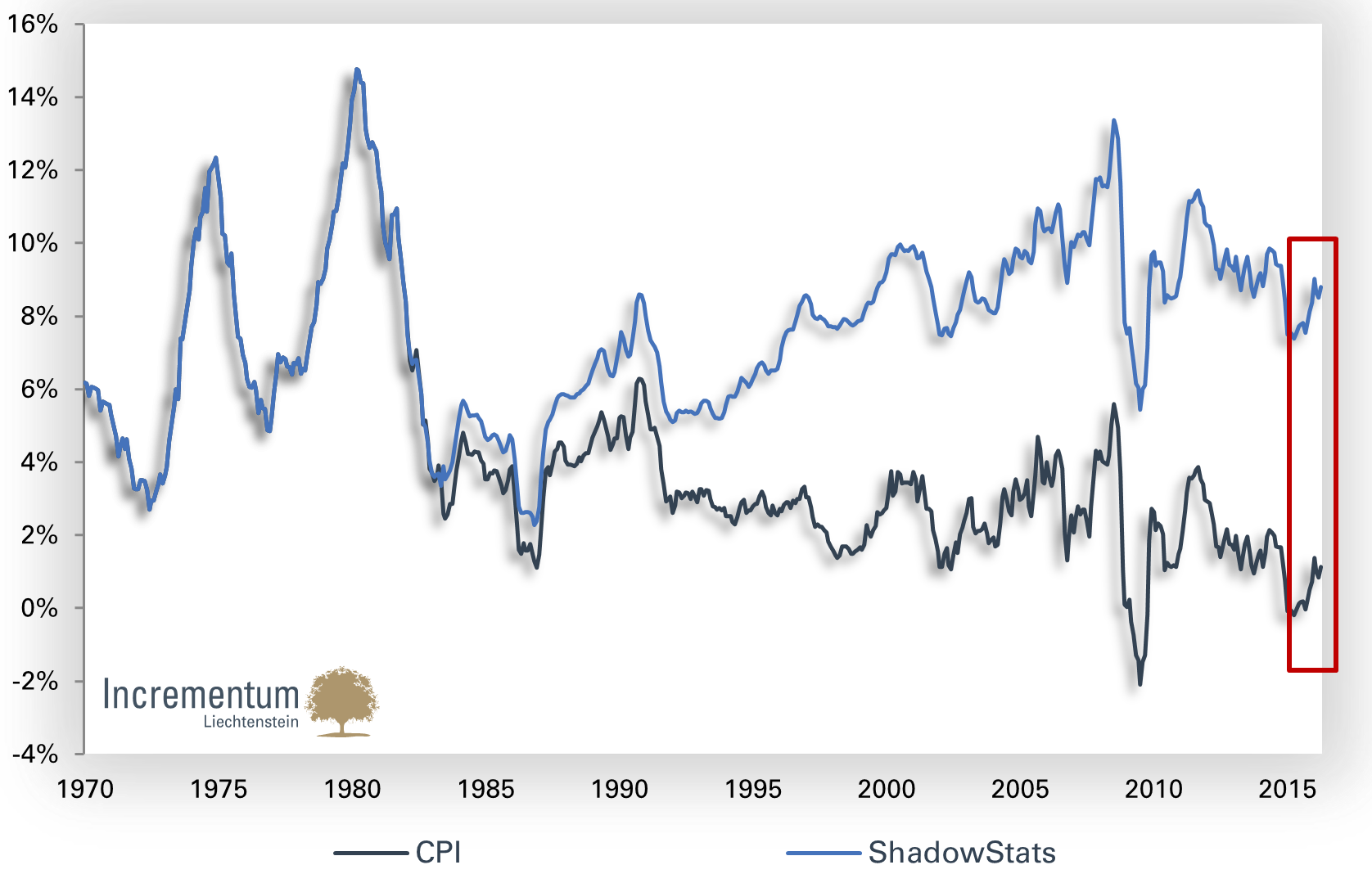

We have criticized the officially reported inflation data on several previous occasions already. The incentive for policymakers to report low inflation rates is obvious: Numerous types of welfare spending, transfer payments, salaries of civil servants, pension payments, etc. are tied to price indexes. Moreover, low inflation results in higher real GDP growth being reported, which is calculated by dividing nominal economic growth by a price index. The valuation, resp. demand for government bonds also depends strongly on current, and particularly expected price inflation rates.

Too low price inflation data furthermore distort the reactive function of monetary policy: It is suggested that we are close to the allegedly catastrophic threshold to deflation, and that audacious measures have to be taken as a result. In short, there is obviously great interest in keeping official inflation rates as low as possible.

Several different methods for the calculation of price inflation exist, some of which are probably superior to the official data. Shadow Stats for instance calculates the inflation rate according to the methodology employed in the 1980s, i.e., prior to the 24 different “adjustments” of the methodology implemented by the Bureau of Labor Statistics since then. The divergence between the inflation rate reported today and the inflation rate according to the old calculation method is shown in the following chart. While official price inflation according to the CPI averaged 2.7% per year, Shadow Stats calculates an average inflation rate of 7.6% p.a.

Official CPI inflation rate vs. Shadow Stats inflation rate (y/y)

Source: Shadow Stats, BMG Bullion, Incrementum AG

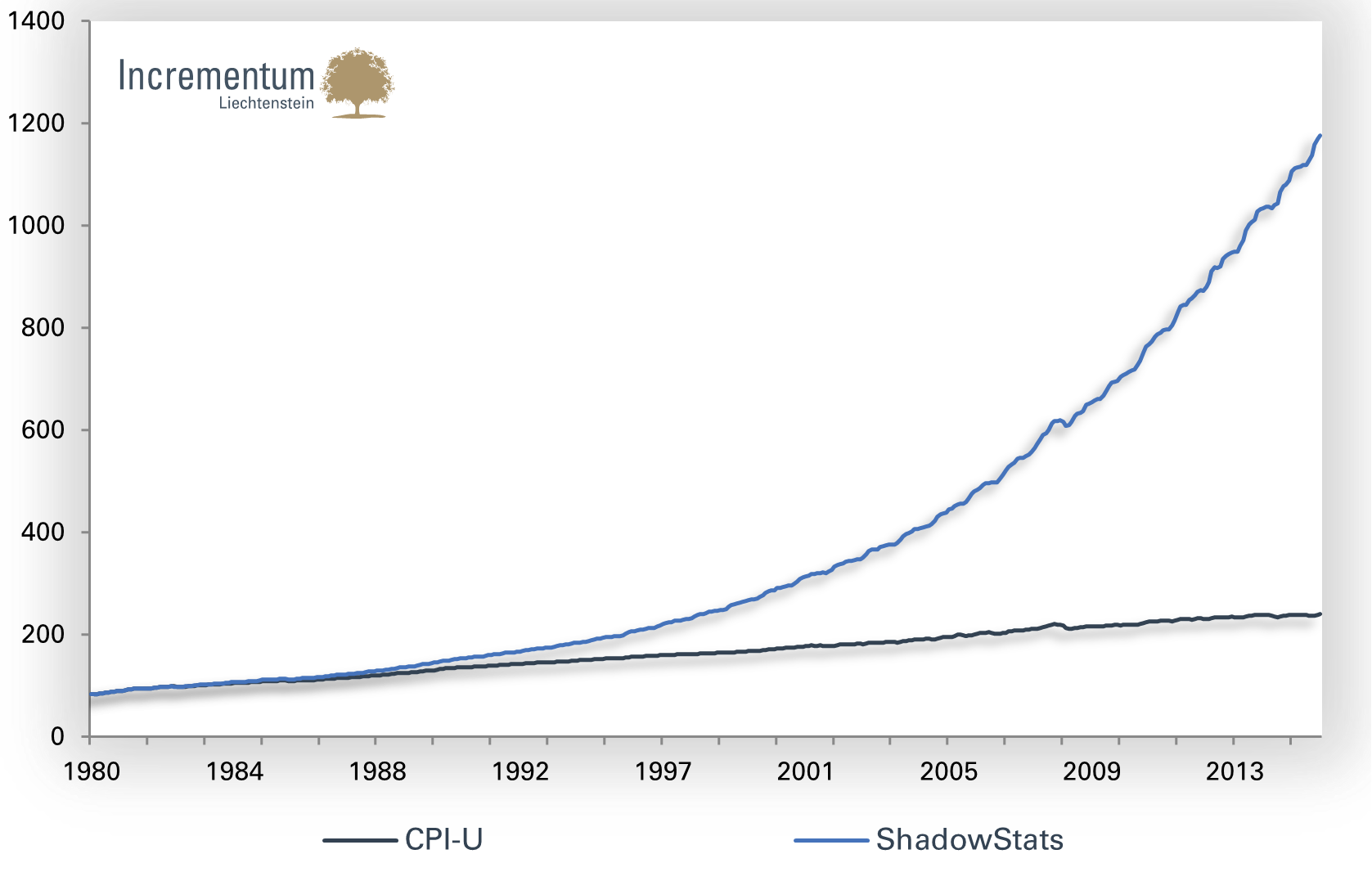

If one depicts the two time series as an index, one can see that according to the Shadow Stats data, the cost of living has risen more than 10-fold since 1980, while the official CPI data indicate only a 138% increase.

CPI and Shadow Stats Inflation Index since 1980

Source: Shadow Stats, BMG Bullion, Incrementum AG

Another method of calculating price inflation is a long term comparison of the purchasing power of fiat money and gold. This topic will be discussed in the next chapter.

g. Gold and the Illusion of Nominal Value

In his “scholions”, which are always well worth reading, Rahim Taghizadegan writes: “In a society based on the division of labor, most catallactic acts of exchange are settled via the mediation of a generally accepted medium of exchange: money. This medium also serves as a standard of comparison, enabling one to estimate the opportunity costs attending exchanges. Money is not only a medium for a value proposition, it is a value proposition in itself. Its purchasing power depends on the evaluation of its quality. In the case of money, quality primarily refers to its liquidity, this is to say the possibility to exchange it at any time and in any amount against other goods and services.” [18]

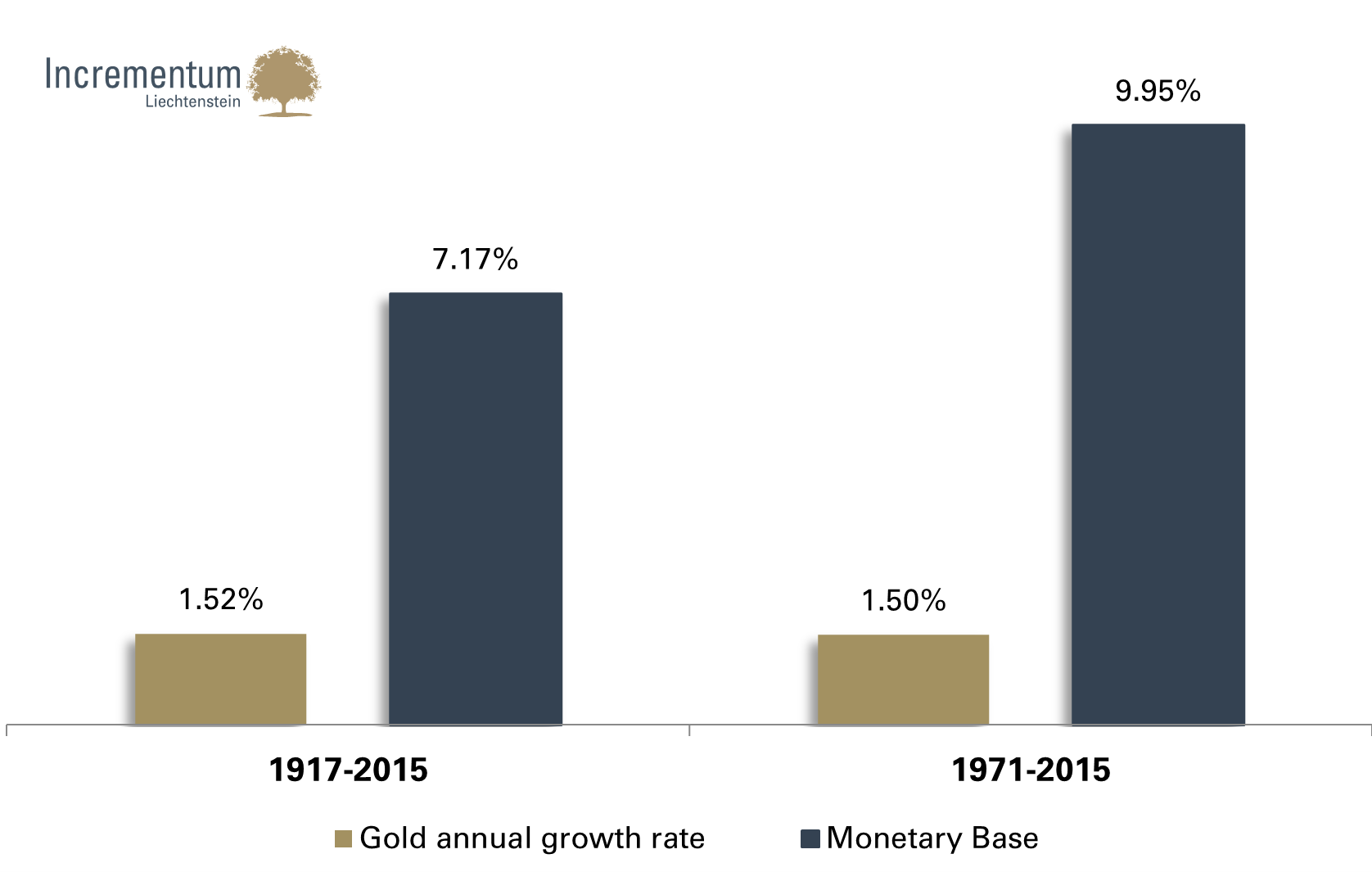

Historically the annual increase in the total stock of gold was consistently lower than the expansion of the money supply. Gold therefore protects investors in the long term against the loss of purchasing power caused by persistent money supply inflation in the fiat money system. Rather than looking at higher gold prices as a gain in the precious metal’s value, they should be seen as a consequence of monetary inflation.

Annual rate of change: gold vs. monetary base 1917 – 2015 and 1971 – 2015

Source: Incrementum AG, James Turk, World Gold Council

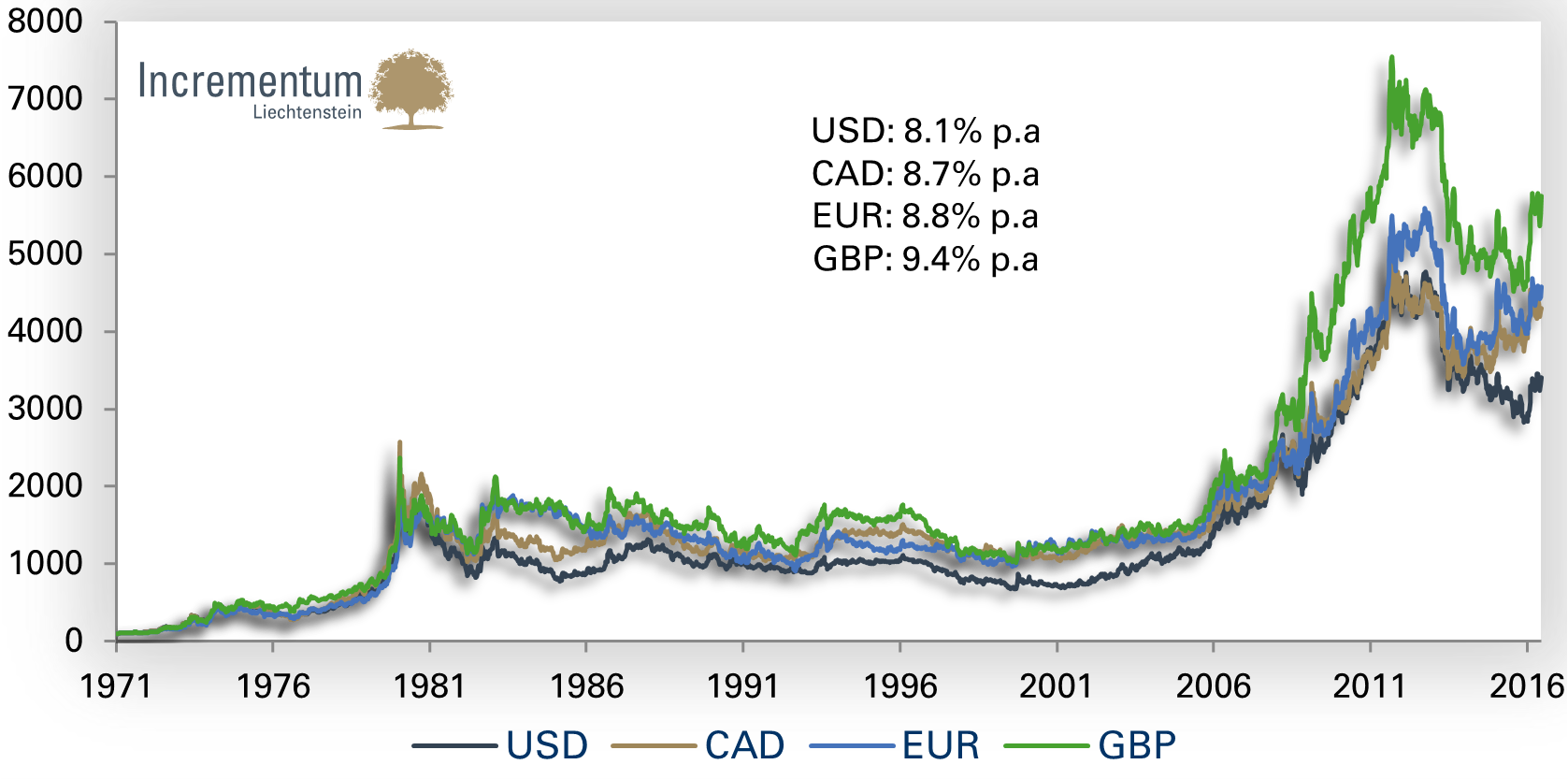

Even though the gold price in US dollar terms is currently not (yet) in the vicinity of its all-time high, the data are clear: the price of gold in terms of the dollar has increased by a factor of 34 since 1971. In the long term the gold price is rising against every paper currency.

Long term trend of the gold price in various currencies (indexed to 100)

Source: Fedearl Reserve St. Louis, Incrementum AG

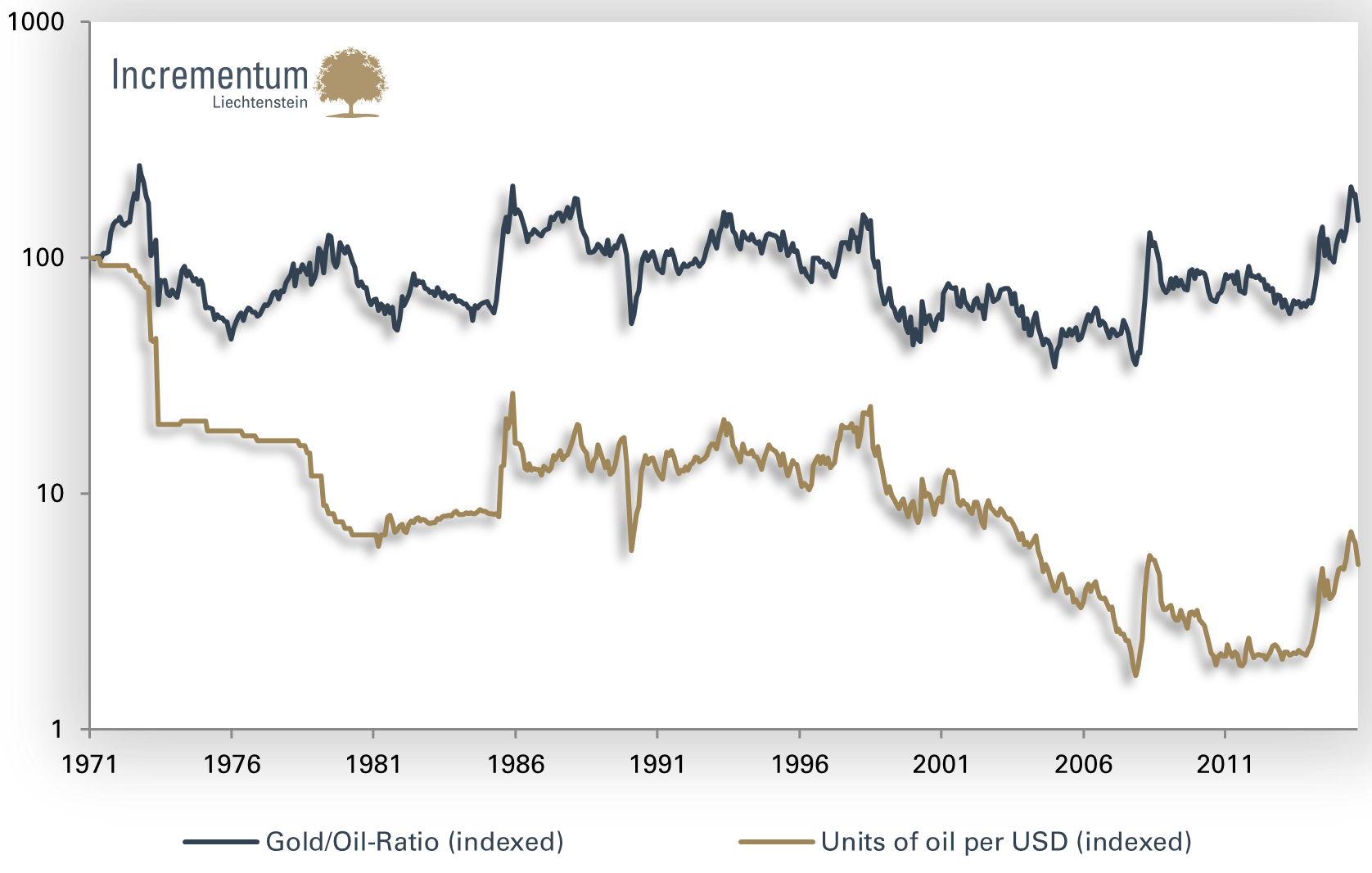

The gradual erosion of purchasing power since 1971 can also be discerned in the next chart. On the one hand it shows the gold/oil ratio (i.e., how many barrels of oil can be bought with one ounce of gold?), and on the other hand it shows the inverse of the oil price (i.e., how many units of oil can be bought with one US dollar?). One can see that while the price of oil in terms of gold tends to be relatively stable over time and gold’s purchasing power currently stands actually 40% above the level of 1971, the US dollar has lost has more than 95% of its purchasing power relative to oil over the same time period.

Gold/Oil-Ratio and Units of oil per USD (both indexed)

Source: Federal Reserve St. Louis, Incrementum AG

However, we have apparently become accustomed to continually rising prices. A simple example from everyday life: In the summer of 2016 all of Europe is focused on “King Soccer”. The European championship is underway and with it the peak season for Italian sticker manufacturer Panini. At the time of the 1992 championship, a packet containing five stickers could be bought for 50 German pfennigs (or 3.50 Austrian schillings). But at the time of the 2000 championship this had increased to 60 pfennigs and today the price is 60 euro cents. This is a price increase of 140 percent within 24 years.

However, the popular stickers made by Panini are by no means the only product which is getting ever more expensive when measured in terms of the real purchasing power of consumer incomes. Such historical comparisons become truly explosive if one looks at price developments in terms of gold. In the following we therefore want to show several historical comparisons that illustrate gold’s ability to preserve purchasing power in the long term.

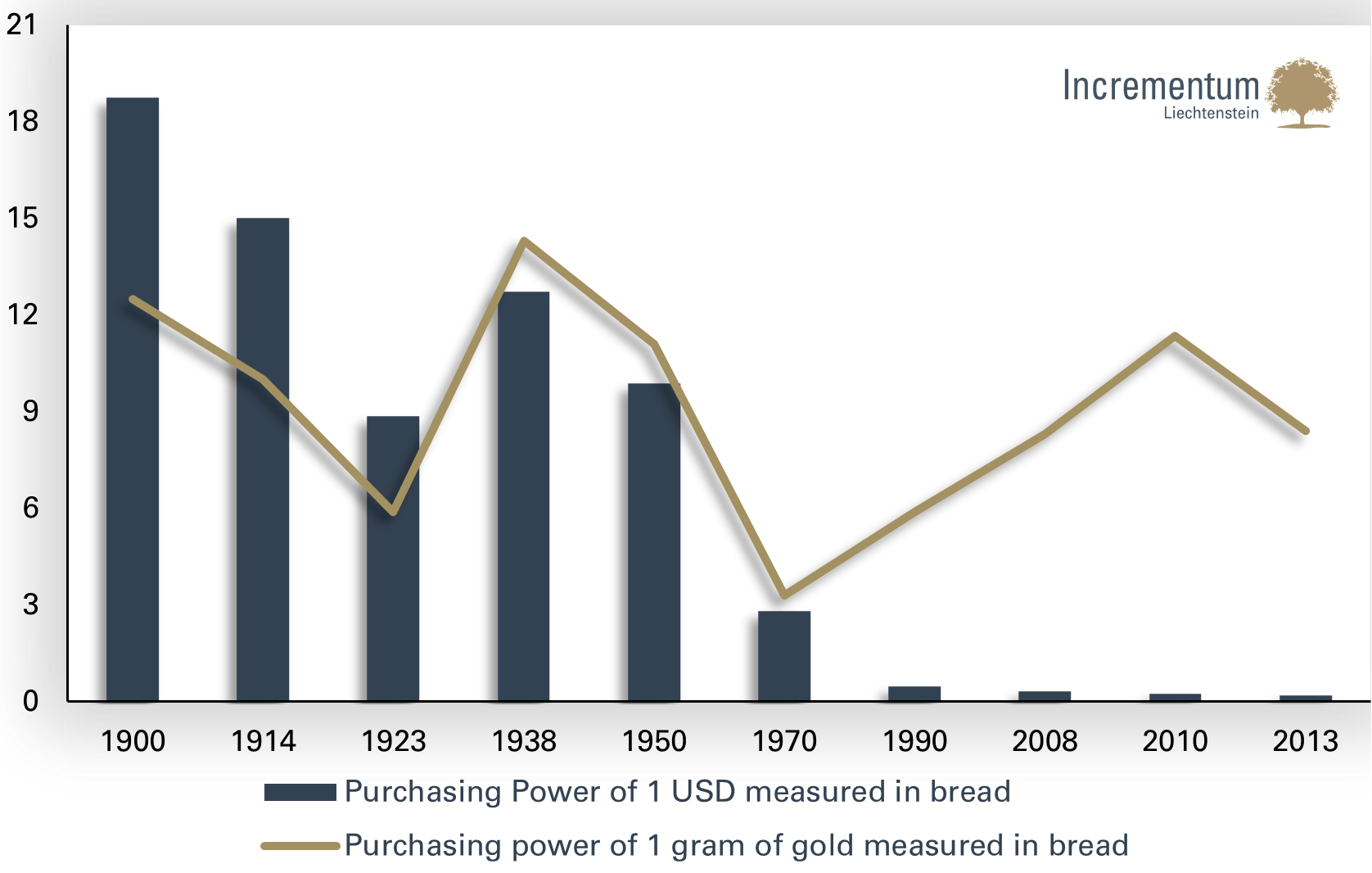

The value of gold and the USD relative to rye bread

Source: Wirtschaftswoche, Investor Verlag, Incrementum AG

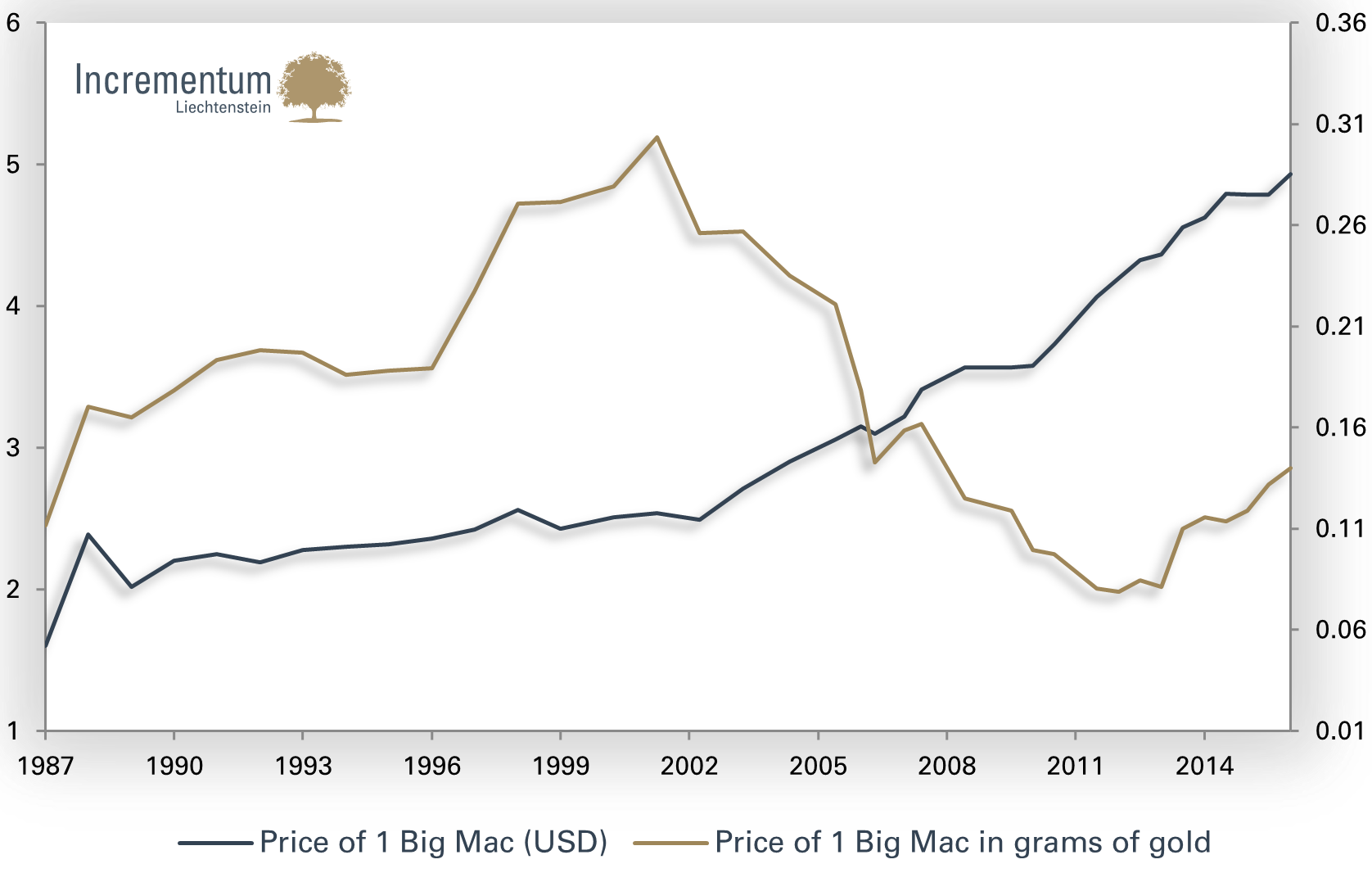

While bread is representative of staple foods, the Big Mac is representative of fast food. The Economist magazine developed the Big Mac index in 1986 as an indicator for differences in the purchasing power of various currencies. While it was originally merely intended as a striking example illustrating differences in purchasing power, the index has in the meantime become the world’s best-known indicator of purchasing power. Originally its purpose was to test the purchasing power parity theory empirically. According to this theory, exchange rates will tend to converge in the long term so as to offset differences in purchasing power. Thus the price of USD 4.93 for a Big Mac in the US compared to the price of USD 2.68 charged for a Big Mac in China would be considered evidence that the yuan is undervalued relative to the US dollar. Over the long term, the yuan should appreciate relative to the USD, until a Big Mac costs the same in both countries.

The following chart shows the historical price of a Big Mac measured in US dollars and in grams of gold. While gold’s purchasing power appears to be more volatile than that of the dollar in the short term, its value is clearly more stable in the long term. Between January of 1987[19] and January of 2016 the price of a Big Mac has more than tripled in dollar terms, rising from 1.60 to 4.93, while in gold terms it has only risen from approximately 0.11 to approximately 0.14 gram.

Price of a Big Mac measured in USD (lhs) and in grams of gold (rhs)

Source: The Economist, Incrementum AG

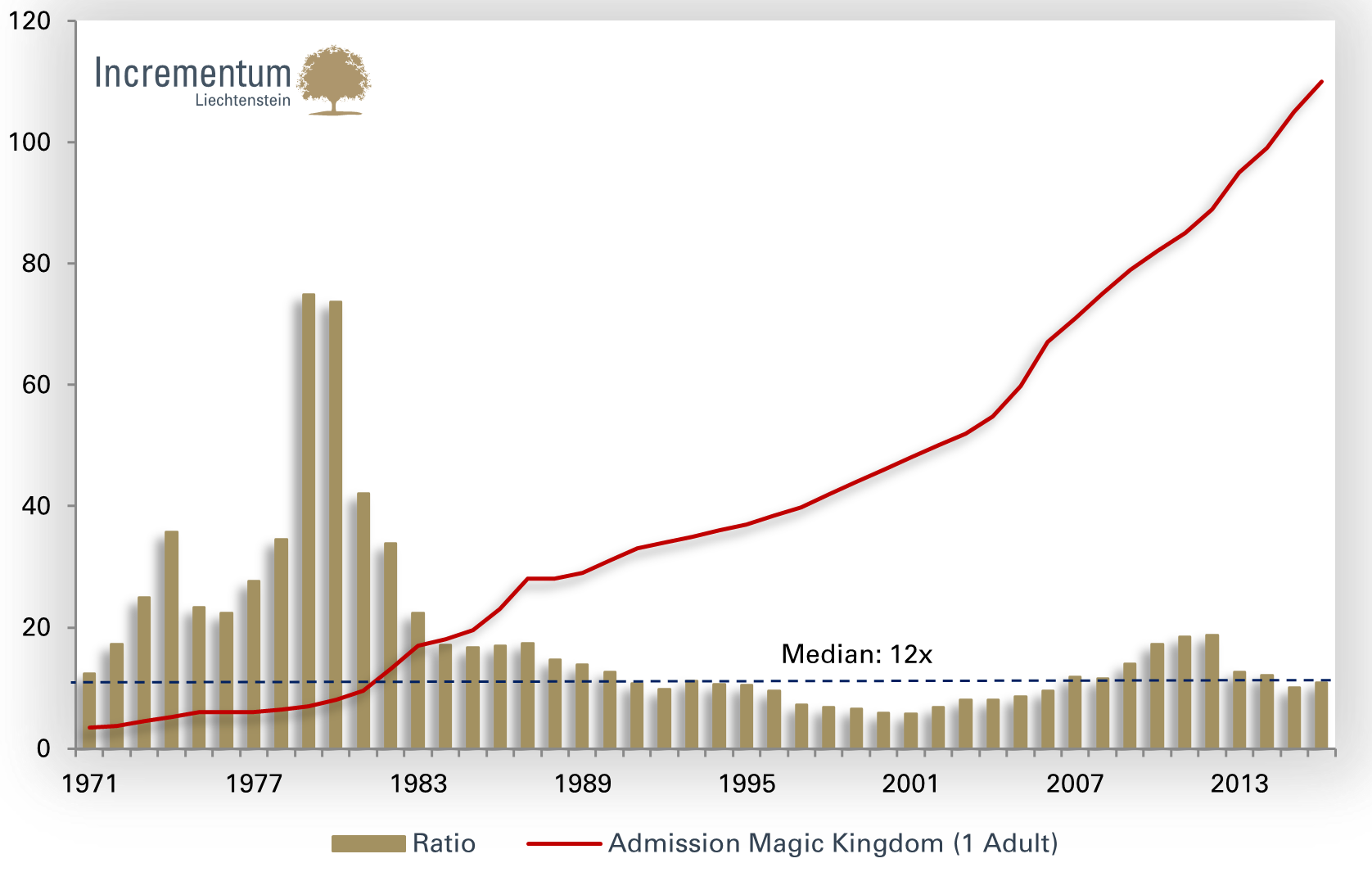

The contrast between the purchasing power of gold and paper money becomes especially obvious when looking at the prices of leisure attractions. The entrance fee for the Disney World Magic Kingdom in Florida is used as a proxy for leisure attractions in the US. At the time of its opening in 1971, the ticket price stood at USD 3.50 per day, today the entrance fee amounts to USD 110 per day. That equates to an average annualized price increase of 7.96%, twice the official inflation rate. If one looks at these ticket prices in gold terms, it can be seen that a median of 12 tickets could be purchased with an ounce of gold over time. Currently this figure stands at 10.9, which is quite close to the long-term average.[20]

Ticket price for Disney World vs. Gold/ Disney World ratio

Source: Incrementum AG, WDW Ticket Increase Guide

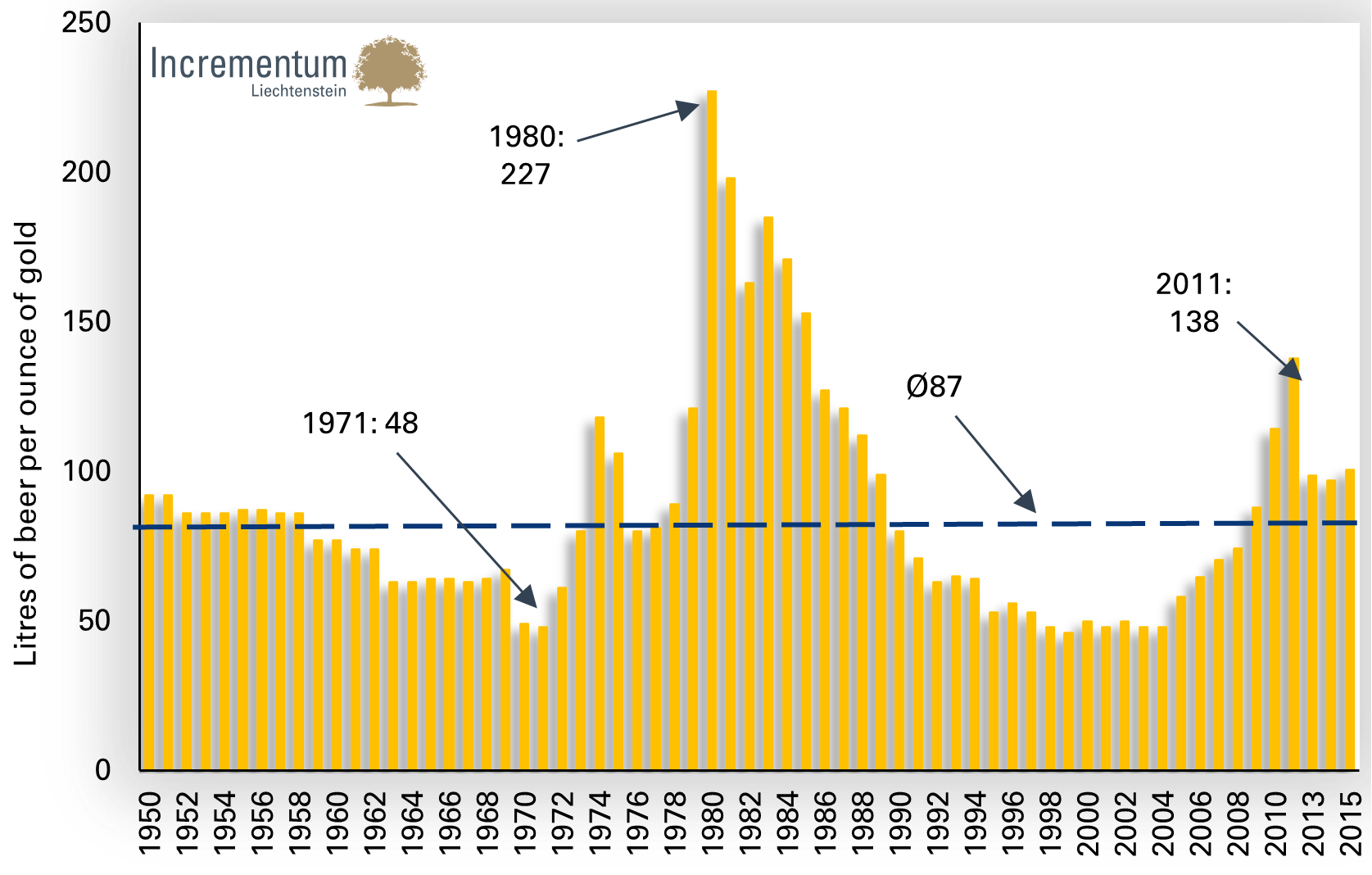

What Disneyland is for Americans, the Oktoberfest is for Bavarians. A regular feature of our chart collections is the “beer purchasing power” of gold. While a liter of beer (a “Maß” in German) at the Munich Oktoberfest in 1950 cost the equivalent of EUR 0.82, the average price in 2015 was EUR 10.25[21] The annual price inflation of beer since 1950 thus amounts to 4.2%. If one looks at the price of beer relative to the gold price, then one ounce of gold could buy 100 liters of beer in 2015. Historically the average is 87 liters – thus the “beer purchasing power” of gold is currently slightly above the long-term average. The peak was however reached in 1980 at 227 liters per ounce. We believe it is quite possible that this level will be reached again. Beer drinking friends of gold should therefore expect the metal’s beer purchasing power to increase.

Gold/Oktoberfest beer ratio

Source: www.HaaseEwert.de, Historisches Archiv Spaten-Löwenbräu, Incrementum AG

Looking at the significant erosion in the purchasing power of paper money relative to gold and other asset classes, such as stocks, is an interesting exercise as well. The average US employee must currently put in 55 hours of work in order to be able to buy one ounce of gold. In 1969 it took only 15 hours. In order to buy one unit of the S&P 500, 96 hours of work are currently required – back in 1969, only 35 hours of work were needed. Both asset classes show that wage earners have been impoverished in real terms, as they have to work significantly longer hours nowadays if they want to purchase investment assets.

Number of work hours needed to purchase an ounce of gold or one unit of the S&P 500 Index

Source: Federal Reserve St. Louis, IMF, BLS, Incrementum AG

Conclusion:

Men and machines are becoming more productive and are doing more efficient work. In a healthy, sound and fully-backed monetary system, prices would therefore steadily decline. Alas, the exact opposite is actually the case. What changes perpetually is the value of paper money. It declines year after year, while the working population is forced to struggle with stagnating or even falling real incomes.

Gold by contrast has a track record of successfully preserving value and purchasing power over thousands of years. In the course of human history, the market has chosen gold as the best money based on logical and rational reasons – such as its high liquidity, indestructibility, high value density, fungibility, divisibility, world-wide acceptance, etc. The slow and steady growth in its supply from mining (the global stock of gold is growing at approximately the same pace as the population) ensures stability and confidence. These unique characteristics are making gold one of the best hedges against excessive money supply expansion and Black Swan events.

h. Helicopter money: the reflation policy’s ace in the hole?

„We understand that in the past you have described the concept as ‘very interesting’, but that it is not something that the ECB is currently investigating. As members of the European Parliament, we call on you to investigate these different and alternative policies.” [22]

18 members of the European Parliament writing an open letter to Mario Draghi

Central banks are currently about as successful in generating rising prices in line with their inflation targets as the GDR’s politburo was in regularly supplying the population with bananas. For several years price inflation has come in way below plan, as a result of which the list of measures central bankers might need to implement next in order to finally boost inflation is getting longer and longer. One concept that is currently a topic of debate nearly everywhere, and which although it hasn’t been discussed by the ECB council yet, is “very interesting” according to Mario Draghi, is so-called helicopter money. Peter Praet, chief economist of the ECB, told the Italian newspaper La Repubblica that this “extreme instrument” would in principle be available as a last resort.[23] This seems a good enough reason to take a closer look at it.

What is helicopter money?

The metaphorical term “helicopter money” was coined by Milton Friedman, who used it as an illustration in the context of his monetary theory, describing money supply inflation as akin to a helicopter flying over a model community and dropping money that people would then pick up from the ground.[24] Nowadays it describes a targeted interest- and debt-free expansion of the money supply consisting of direct transfer payments to governments or households. The goal is to boost demand, and with it inflation. Thus money created by the central bank will no longer be injected into the economy by buying bonds from banks as has been the case hitherto, but possibly by one or more of the following four methods:

- QE combined with fiscal expansion: central banks purchase government bonds, temporarily increasing the money supply. This lowers the cost of government financing and creates leeway for fiscal stimulus or tax cuts.

- Cash transfer payments to governments: Very similar to point 1, but without governments having to redeem the debt – the central bank expands the money supply permanently. Rolling over outstanding debt in perpetuity would be one way to circumvent various legal aspects with this strategy. An implicit guarantee that central banks will do this for newly bought bonds also seems possible.

- Cancellation of outstanding debt securities, which central banks hold as assets on their balance sheets: this can be a one-off measure, but regular haircuts of a specific percentage size would also be thinkable. The purchase of negative yielding bonds de facto already represents such a measure.

- Cash transfer payments to private households: Central banks issue checks to individuals or simply credit a certain amount to their bank accounts.[25]

Hans-Werner Sinn points out that the QE programs of recent years – even though government bonds were only purchased in the secondary markets – essentially already represent helicopter money as described in point 1. Newly printed central bank money has reached government budgets indirectly through the debt channel, and has served to fund expenditures which otherwise would have required tax increases. Since the interest payments on these bonds are flowing back to governments via distribution of the central bank’s profits, this form of financing is ultimately interest-free as well.

“While democratic governments are nowadays determining the extent of their indebtedness, as well as who the recipients of transfer payments or the beneficiaries of tax cuts will be, in the case of helicopter money it is the ECB itself that will make these decisions.” [26]

Helicopter money is legally possible

The suspicion that central banks would exceed their mandates by issuing helicopter money has been frequently voiced. For instance, Bundesbank president Jens Weidmann remarked: “Central banks do not have a mandate for this policy, not least because massive wealth redistribution would be associated with it”. The legal mandate of ensuring price stability could no longer be safeguarded in the long term in the event of state financing through the printing press, as the momentum of price inflation could easily get out control. However, upon taking a closer look at the issue, many economists have come to the conclusion that the legal hurdles are much lower than is generally assumed.[27]

A study by Deutsche Bank shows that helicopter money – taken to mean monetary state financing – isn’t really a new concept, but has already been practiced several times in the past. The institutional framework conditions of central banks are very vague and leave a lot of scope for interpretation; specifically the quite unconventional variant of transfer payments to citizens seems legally unproblematic.[28] Political will is ultimately more important than technical and statutory framework conditions. On occasion of the next recession at the latest, helicopter money will likely appear on the agenda.

The limits of the debt money system

As mentioned above, the measures taken to date in the form of zero, respectively negative interest rates and QE have been quite unsuccessful. This was inter alia due to the fact that the efforts of central banks to persuade commercial banks to expand credit have been partially countered by government efforts to make banks safer by means of directives such as Basel III and also because there has been limited demand for new credit in the private sector. In addition, negative interest rates actually seem to hamper credit expansion: Banks are reluctant to pass them on to their depositors, who would likely flee into cash. As a result of this the net interest margins of banks are shrinking, which dampens rather than boosts credit expansion. Helicopter money would therefore represent a suitable means of circumventing the banking sector with respect to the money supply expansion process, as a result of which it is occasionally referred to by the moniker “QE for the people”.

A prominent and above all influential advocate of helicopter money is Adair Turner, the former chairman of the British financial market supervisory authority, who last October published a book entitled “Between Debt and the Devil”.[29]

He points out that bank lending mainly serves to finance consumption or the purchase of existing assets such as real estate rather than productive investment, which leads to price spirals and sooner or later to financial crises. Long-term nominal economic growth of around 4% per year in the developed nations prior to the 2008 financial crisis was supported by annual growth in private debt between 10% to 15%. Since then the latter has stagnated and governments have stepped into the breach – with the result that they are now also buried in debt up to their ears. These high debts are now dampening the effects of both conventional monetary and fiscal policy and are paralyzing growth. Turner moreover states that aggregate demand is too low and needs to be boosted.

In order to boost demand, Turner recommends the implementation of so-called “overt monetary finance” measures – a policy which according to Turner, is popularly referred to by the somewhat infelicitous term “helicopter money”. “Admittedly there would be a danger that this could lead to a rapid rise in inflation, even to hyper-inflation. One would have to act very carefully when implementing such a measure, and would have to be wary of overdoing it. The greatest risk of monetary state finance is posed by governments, which would quite possibly be tempted by this approach to take such steps over and over again”, Turner noted in an interview.[30]

The proponents of Modern Monetary Theory[31] also believe the weakness in aggregate demand to be the main problem and are therefore pleading for fiscal stimulus. They are of the opinion that the solvency of governments as issuers of fiat money, which is legal tender and has to be used for the payment of taxes, is unlimited. As long as there are idle resources in the economy, such as e.g. unemployed workers, government can put them to work by spending more money and creating additional demand.

What would the effect of helicopter money be?

Ideally helicopter money would boost both growth and inflation expectations. Apart from the direct increase in prosperity due to growth, there would be the following additional positive effects:

- Reduction of debt: A growing tax base would fill the coffers of governments and it would be come possible to pay back debts, the real value of which would moreover be be lower due to inflation as well. The same would apply if private households were the recipients of helicopter money. Thus, if a part of the helicopter cargo were always spent on paying down debt, it would be theoretically possible to eventually eliminate all debts of non-banks and replace them by central bank money (see also Irving’s “100% money regime”).[32] However, this would basically only be an accounting trick, in which one piece of paper with a claim to a country’s productive output would be substituted for another piece of paper with the exact same claim.

- Return to monetary policy normalcy: In the event of an economic expansion and rising inflation rates, interest rates could be gradually raised again. This would restore the ability to conduct conventional monetary policy to central banks and savers and pension funds would breathe a sigh of relief.

- Political chaos could be prevented: The growing rejection of current policies by the citizenry, which expresses itself in many regions in the form of growing support for nationalist and anti-establishment political movements, could be subdued (particularly in EU crisis countries, which have been subjected to austerity by EU institutions).

In the process, care would have to be taken to prevent inflation from getting out of hand. However, it would be difficult to keep this under control, as fine-tuning of inflation would be conditional on knowledge which central planners cannot possibly possess or obtain (e.g.: How much money is hoarded? How much is spent on assets? How will prices react if aggregate demand actually rises?). Central banks would therefore be forced to use trial and error in determining the size of the helicopter cargo – and on account of the non-linear nature of these processes, this would be akin to playing blind man’s bluff in a minefield:

„[I]t needs to be big enough for nominal growth expectations to shift higher and small enough to prevent an irreversible dis-anchoring of inflation expectations above the central bank’s target.“ [33]

With respect to the growth impetus triggered by helicopter money, this could turn out to be far lower than many people expect. As we have explained, the importance of consumer spending for economic activity is widely overestimated. Should helicopter money be used for government financing, it could hamper rather than foster structural reform, as policymakers would likely keep ailing, unsustainable and labor-intensive industries on artificial life support via injections of money, and undermine the process of creative destruction. Of course this doesn’t have to happen: Political leaders could also decide to invest in future-oriented infrastructure projects and allow painful cutbacks to occur in order to improve competitiveness. We believe a fatal spiral of subsidization and trough-feeding to be a more likely scenario over the medium term though, and helicopter money would likely be used to postpone structural reform for as long as possible.

When money is transferred directly to households

In anglophone countries helicopter money is primarily discussed in the context of monetary financing of government budgets. In the euro zone this variant would face greater problems as there exists no common fiscal policy. Direct transfer payments to citizens are therefore more likely in this currency area. However, what would people actually do if money were indeed falling from the skies like manna?

Oxford economist John Muellbauer has analyzed the 2001 and 2008 tax cuts in the US in a study. In both cases a significant portion of the additional disposable income was spent on consumption.[34] Agnieszka Gehringer and Tobias Schafföner examined the potential effects of negative interest rates and helicopter money on German savers in a study.[35] Their conclusion was that negative interest rates would be highly ineffective with respect to generating consumer price inflation. Helicopter money on the other hand could potentially have a strong inflationary effect: an average of 46.5% of a one-off payment of EUR 2,000 per household would be spent. In the event of regular payments, 30.5% of respondents said they would increase their consumption spending and 20.3% stated they would increase their savings. It can therefore be surmised that the inflationary effect would be strengthened if the helicopter were to be flying its rounds on a regular basis. Although the survey results are declarations of intent and as such have to be treated with caution, they nevertheless allow one to firmly conclude that helicopter money would provide a boost to inflation. We see behavioural factors at work as well: It is easier to squander an unexpected gift of money than a part of one’s regular income.

From debt money to “reputation money”

Does helicopter money create purchasing power without an expansion of outstanding credit or debt issuance by the government? Quite the contrary: As noted above, newly created central bank money could even gradually replace existing debt. Is helicopter money therefore a kind of perpetuum mobile of monetary policy?

As was to be expected, there is actually a catch. Central bank money injected into the economy is a line item on the liabilities side of a central bank’s balance sheet, similar to its equity capital, while on the asset side, there are assets such as gold or government bonds. Since no debt securities are purchased when helicopter money is issued, the money creation process will weigh on equity capital, which could eventually even become negative and jump over to the asset side of the balance sheet. While any other organization would go bankrupt under such circumstances, this can easily be done by a central bank, as it doesn’t need to pay its liabilities back. However, the population could lose confidence in the money issued by the central bank, as it would no longer be backed by any assets.

Thomas Mayer, former chief economist of Deutsche Bank and head of the Flossbach von Storch Research Institute believes it unlikely that inflation would get out of control as a result of this. In the study “From ZIRP, NIRP, QE and helicopter money to a better monetary system”, he points out that the character of money would fundamentally change in this “castling” of equity capital: Money would no longer be credit money, but “reputation money” backed by “the goodwill” of the population.[36]

Crypto-currencies, which have become popular since the financial crisis, are however also pure “reputation money”. Crypto-technology would be interesting for official state-issued money as well, as monetary policy could then wean itself entirely from the banking sector: The central bank would simply distribute helicopter money directly to households, and abandon the inefficient and cumbersome system of the private-public partnership in money creation.

This could moreover pave the way to a monetary system in which state-issued money is in competition with other crypto-currencies – inter alia with gold-backed crypto-currencies. Mayer regards crypto-technology as the decisive step toward making Hayek’s proposal of a monetary system in which different currencies compete freely a reality. Helicopter money could simplify the changeover to this new system. However, he also believes that the monetary system will still experience a severe crisis before this happens.

„… I cannot close my eyes to the fact that any hope for a voluntary abdication by governments of their present monopolies of the issues of circulating money is utopian.“

Friedrich August von Hayek, The Denationalization of Money

Conclusion:

Monetary policy is at the end of the line – no instrument from the toolbox of conventional and unconventional measures applied to date appears to be working anymore: Interest rates are at rock bottom and can only be lowered further if cash currency is banned; expanding central bank balance sheets further is becoming ever more dangerous as well – not to mention that it has never had the desired effect. Fiscal stimulus launched to counter the last recession has moreover raised government debt to such a dangerous level that it has become nigh impossible to revive the economy from this source. This debt burden also makes a return to monetary policy normalcy extremely unlikely, as governments would likely be bankrupted left and right as a result. If a recession were to strike, it would strike with full force, as neither monetary policy nor fiscal policy could be used to mitigate it. Only inflation and economic growth could solve this dilemma, but neither of them can be pushed beyond a pedestrian pace. The Gordian knot needs to be cut – but how?

Helicopter money could be the central bankers’ ace in the hole, as it would probably indeed boost inflation. Whether this inflation would evolve in an orderly manner or go off the charts in an uncontrollable burst, is difficult to predict. In either case helicopter money could well – whether this is the intention or not – ring in a new era of the monetary system, in which different crypto-currencies with “reputational backing” compete with each other.

It would also be the time for gold to shine. Should money indeed begin to drop from the skies, the reflation efforts of central banks would in all probability finally succeed and occasionally overshoot their targets – the kind of environment in which gold is traditionally doing well. Gold, which has been accorded great confidence for thousands of years, could furthermore play an important role in a possible monetary order based on reputation money.

i. Conclusion “Inflation and Investment”

In our book we write: The extent to which people underestimate this spiral of devaluation is quite astonishing. It is the biggest open secret in economic history. Open, because all historians are aware of it, because it is sufficiently well documented and astonishingly universal. In almost every culture, the guardians of the currency have abused their position. Since the modern monetary revolution, this abuse is however even less obvious, as currencies no longer have a real foundation and have become arbitrarily elastic. Thus the dilution and debasement of debt-based currencies, which is referred to as “inflation” by economists, is a secret for most people: they feel constant pressure as a result of the devaluation, but they are unaware of its causes and are looking in the wrong direction.[37]

As we will also show in the following chapter, the deliberate debasement of the currency is an old trick. By creating new money, the value of existing money is diluted and a permanent transfer of wealth is triggered. The fact that the expansion of the money supply has an effect on asset prices and consumer prices is obvious. Recent decades were characterized by asset prices benefiting from a strong monetary tailwind. The determined effort of the inflationary authorities to prevent consumer prices from falling is currently laying the foundation for a change in the trend of price inflation.

In our assessment, global price inflation will be boosted from July onward due to base effects related to the price of oil. This could be a critical turning point. If we should turn out to be correct with this assumption, inflation-sensitive asset classes like gold, commodities and particularly mining stocks will be among the best performing asset classes in coming years.

[1] See: “Inflation and Deflation”, Strategic Economic Decisions

[2] See: “In Gold we Trust Report 2014“; S. 28

[3] See: “PPC Metrics Research Paper Nr.1/2013: Anlagen in einem inflationären und deflationären Umfeld

[4] In his study “Can banks individually create money out of nothing? – The theories and the empirical evidence” Prof. Richard Werner has for the first time provided empirical evidence that banks’ lendings are not provided on the basis of existing savings, but that they are created as imaginary deposits for the borrower. Credit is hence created ex nihilo.

[5] See: Murphy, Robert P.: “Lost in a Maze of Monetary Aggregates?”, Mises.org, February 14, 2011

[7] https://en.wikipedia.org/wiki/Shrinkflation

[8] Monetarists speak in this context about the “velocity of money”. This concept is however problematic inter alia due to above-mentioned reasons.

[9] Hayek repeatedly pointed out that targeting a macroeconomic variable is not a suitable means to achieve higher macroeconomic stability. On the contrary, it is more likely to harm the system.

[10] See here for details: http://www.ecb.europa.eu/home/glossary/html/act4r.en.html#263

[11] The FvS Vermögenspreisindex measures the price development of the assets of German households. The index corresponds to the weighted price development of tangible and financial assets that are owned by German households. Tangible assets include real estate and business property as well as long-term consumer goods, collectibles and speculative assets.

[12] See: Brodsky, Paul: “The Fall of All we Know“, LinkedIn.com, May 6, 2016

[13] Also see: “Why the gold price rises at all”, “In Gold we Trust 2015”

[14] Investopedia.com on seigniorage: “Seigniorage is the difference between the value of money and the cost to produce it — in other words, it’s the economic cost of producing a currency within a given economy or country. If the seigniorage is positive, then the government will make an economic profit; a negative seigniorage will result in an economic loss.”

[15] Valery Giscard d’Estaing described that constellation as an “exorbitant privilege”.

[16] See: Strobel, Warren: “Dollar could suffer if U.S. walks away from Iran deal: John Kerry”, Reuters, August 12, 2015

[17] See: “Remarks by the President on the Iran Nuclear Deal”, The White House, Office of the Press Secretary, August 05, 2015

[18] See: Taghizadegan, Rahim: “Gewalt“ (“Violence”), Scholien 01/16, Scholarium.at

[19] Unfortunately, longer-term time series have not been available.

[20] See: “Shocking Disney World Price Inflation”, National Inflation Association

[21] Depending on the marque, a Maß cost between EUR 10.10 and EUR 10.40.

[22] See: “MEPS Want the ECB to look at Helicopter Money”, qe4people.eu

[23] See: Giugliano, Ferdinando and Tonia Mastrobuoni: “Peter Praet, capo economista all’Eurotower: La Bce potrà abbassare ancora I tassi”, La Repubblica, March 18, 2016

[24] See: Friedman, Milton: The Optimum Quantity of Money: And other Essays, AldineTransaction, 1969

[25] See: Saravelos, George, Daniel Brehon and Robin Winkler: “Helicopter 101: your guide to monetary financing”, Deutsche Bank Research, April 15, 2016

[26] See: Sinn, Hans-Werner: “Gefährliches Helikopter-Geld”, Frankfurter Allgemeine Zeitung (guest commentary), March 31, 2016

[27] For instance, Klaus Adam, who formerly worked in the research department of the ECB and now is professor at the University of Mannheim, notes it would not violate the central bank’s mandates if they acted on their own initiative and with respect to their inflation targets.

[28] See: Saravelos, George, Daniel Brehon and Robin Winkler: “Helicopter 101: your guide to monetary financing”, Deutsche Bank Research, April 15, 2016

[29] Turner is also chairman of the Governing Boards of the Institute for New Economic Thinking (INET), a think tank funded by George Soros that should explore new paradigms in economics.

[30] See: “Theorie & Praxis: Interview mit Adair Turner”, Institutional Money Magazin, 2/2016, p. 42

[31] Modern Monetary Theory addresses the implications resulting from the state’s currency monopoly to issue fiat money. Representatives of this theory regard traditional assets in central banks‘ balance sheets as unnecessary: fiat money could be issued without any limit.

[32] See: Mayer, Thomas: “From Zirp, Nirp, QE, and helicopter money to a better monetary system“, Economic Policy Note, Flossbach von Storch Research Institute, March 16, 2016

[33] See: Saravelos, George, Daniel Brehon and Robin Winkler: “Helicopter 101: your guide to monetary financing”, Deutsche Bank Research, April 15, 2016, p. 17

[34] See: Muellbauer, John: “Combatting Eurozone deflation: QE for the people”, VOXEU.org, December 23, 2014

[35] See: Gehringer, Agnieszka and Tobias Schafföner: “Wenn Negativzinsen und Helikoptergeld deutsche Sparer erreichen” (“When negative interest rates and helicopter money arrive to German savers”), Economic Policy Note, Flossbach von Storch Research Institute, May 09, 2016

[36] See: Mayer, Thomas: “From Zirp, Nirp, QE, and helicopter money to a better monetary system“, Economic Policy Note, Flossbach von Storch Research Institute, March 16, 2016

[37] See: Taghizadegan, Rahim, Ronald-Peter Stöferle, Mark Valek, and Heinz Blasnik: Austrian School for Investors – Austrian Investing between Inflation and deflation, mises.at, 2015