Essential features of gold

a) The Unusual Portfolio Characteristics of Gold[1]

Since August 15 1971 – the beginning of the new monetary era – the annualized return of the gold price amounts to 8.95%. The real appreciation of gold versus the dollar amounts to 4.7% per year on average. The attractive risk-return profile can also be discerned in the following illustration. What can also be gleaned is that productive assets – such as for example the S&P 500 Index[2] – exhibit a stronger return over the long term than gold. In our opinion, that is definitely to be expected over longer periods of time, due to the value-adding characteristics of companies. In the short to medium term however, the risk-return profile can easily turn in favor of gold – especially in times of monetary policy uncertainty.

Annual Return versus Annual Volatility[3]

![Annual Return versus Annual Volatility[3]](https://ingoldwetrust.report/wp-content/uploads/2024/09/essenzielle-spezifika-von-goldE1.png)

Source: Bloomberg, Ferdinand Regner, Incrementum AG

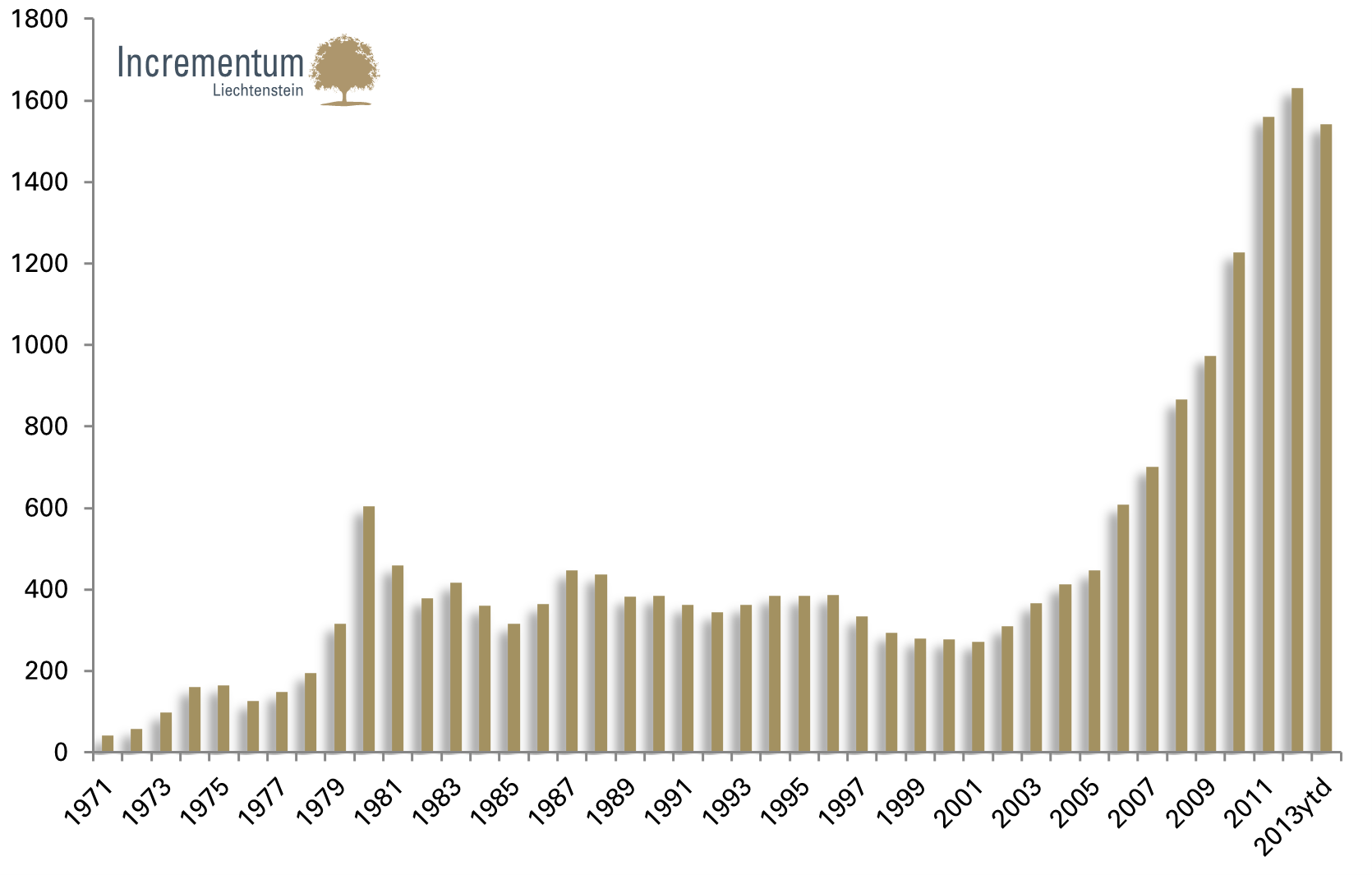

The fact that the current correction is rather insignificant in a long term context becomes clear when contemplating the following chart of annual average prices.

Average Annual Gold Price

Source: Incrementum AG, Datastream

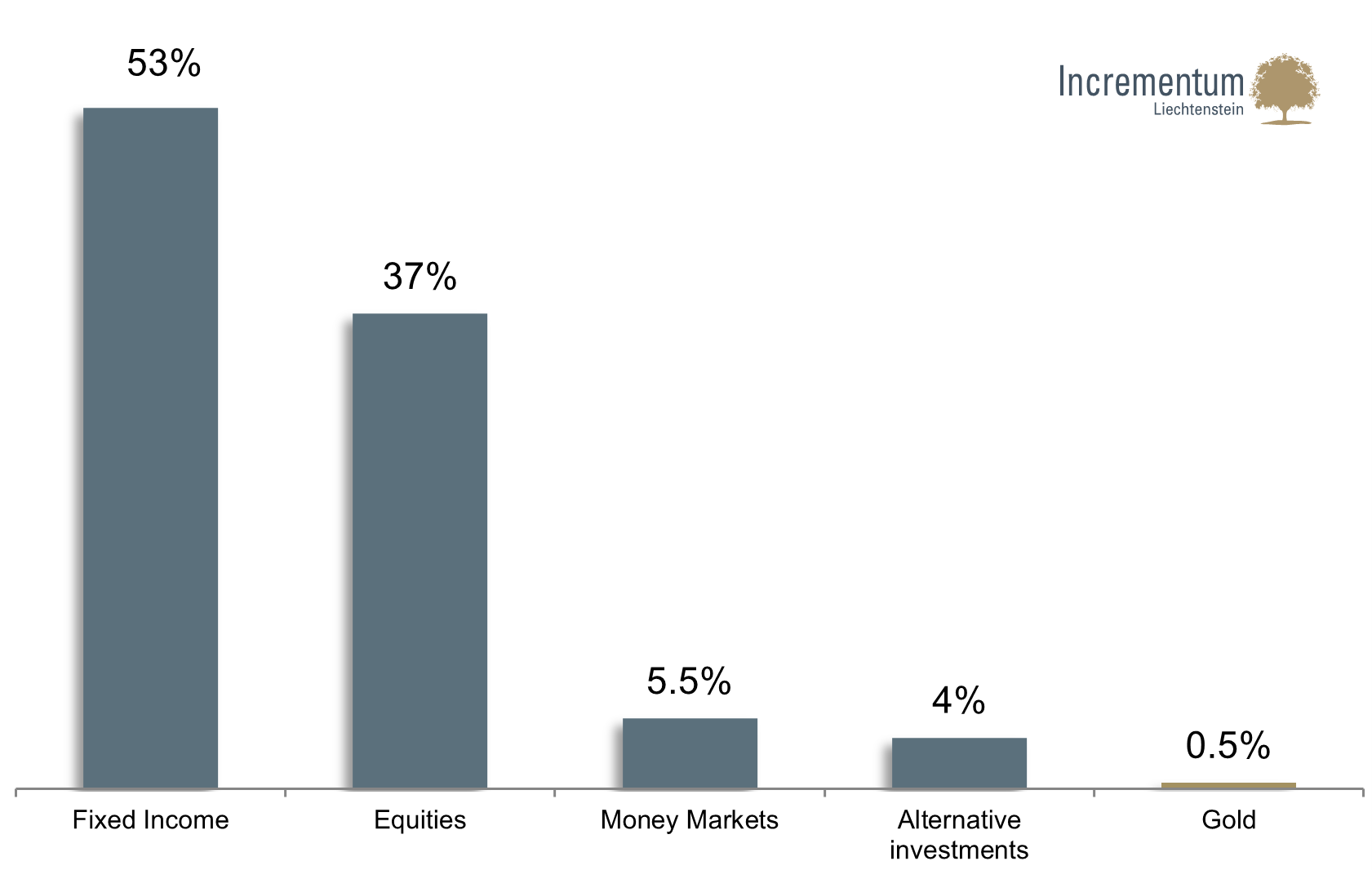

The value of global assets amounted to $223 trillion as of the end of 2012.[4] The share of investable gold currently amounts to $ 1.1 trillion, or only 0.5%.[5] We believe that this share is going to increase considerably in the future, since the notable characteristics of gold (global currency with a long term track record, no credit or counterparty risk, highly liquid and globally traded, very little inflation through mine production) are especially desirable in the current environment.

Gold’s Share of Total Financial Assets Currently at a Mere 0.5%

Source: World Gold Council, Credit Suisse, World Federation of Exchanges

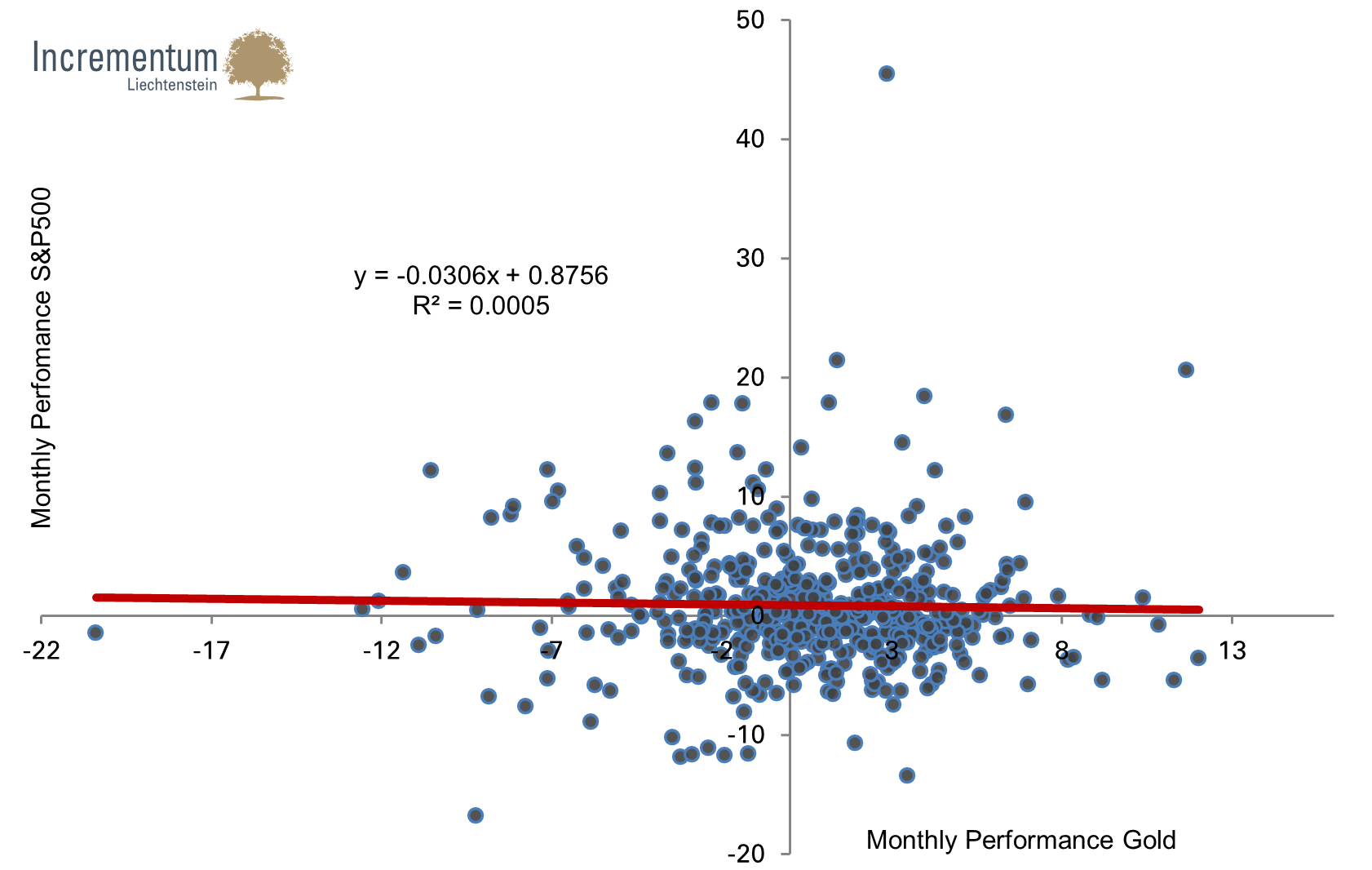

Countless studies confirm that gold as a portfolio addition lowers the volatility of a portfolio and thus improves the statistical portfolio characteristics. If one compares the monthly return of the S&P 500 with that of gold since 1971, one notices this diversification characteristic quite clearly. Apart from these quantitatively provable characteristics, gold has in addition the qualitative characteristic of being a debt-free investment asset that contrary to fixed income securities and bank deposits harbors no inherent counterparty risk.

Monthly Return, S&P 500 versus Gold since 1971

Source: Federal Reserve St. Louis, Incrementum AG

b) The Relative Scarcity of Gold versus Fiat Currencies

„If you can’t explain it to a six-year-old, you don’t understand it yourself.“

Albert Einstein

Gold’s supply curve only changes incrementally every year. First and foremost scrap supply is volatile, while mine production is extremely inelastic. This is one of the major virtues of gold in contrast to paper currencies which can be produced in unlimited quantity. Confidence in the future purchasing power of money depends crucially on how much money is currently available and how the money supply is expected to change in the future.

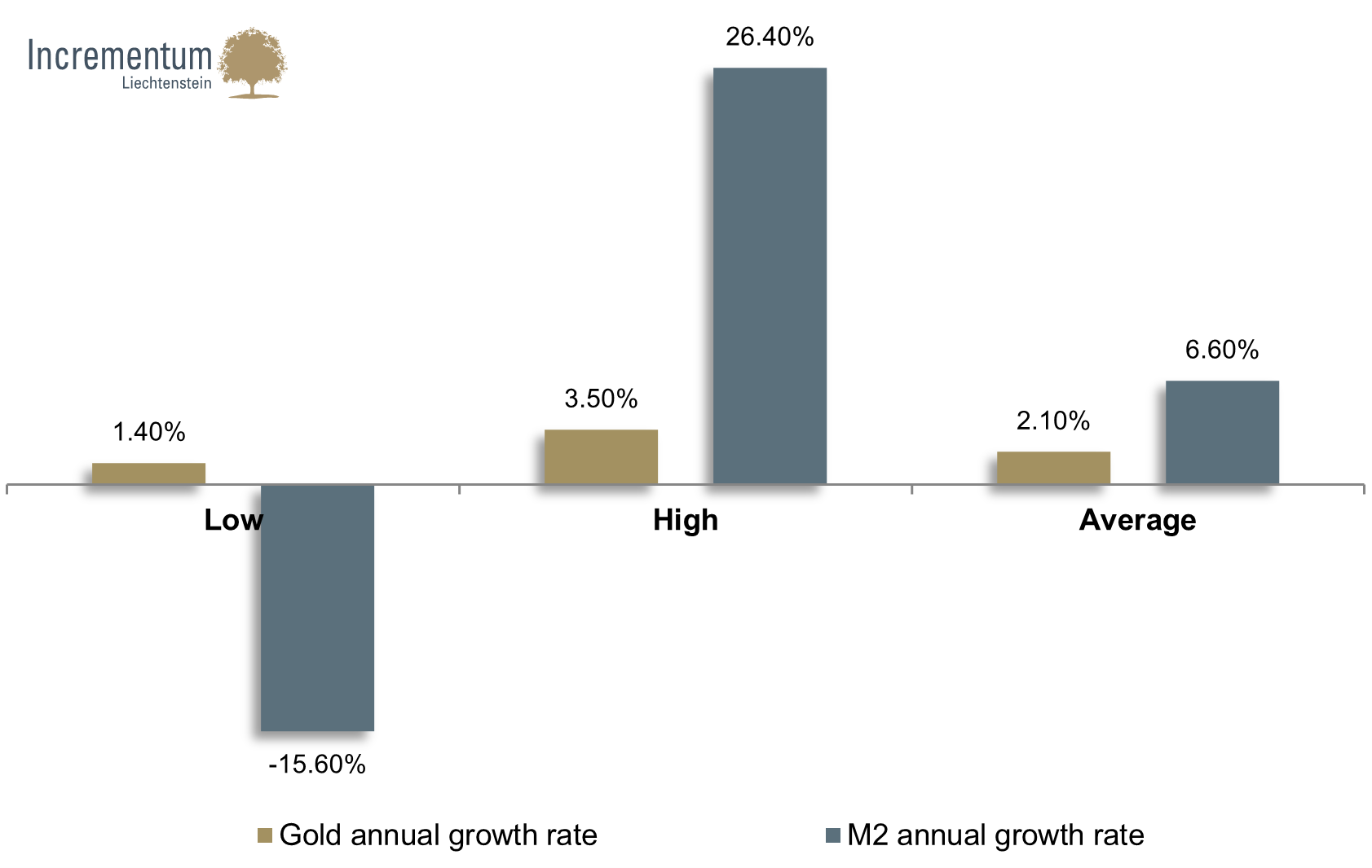

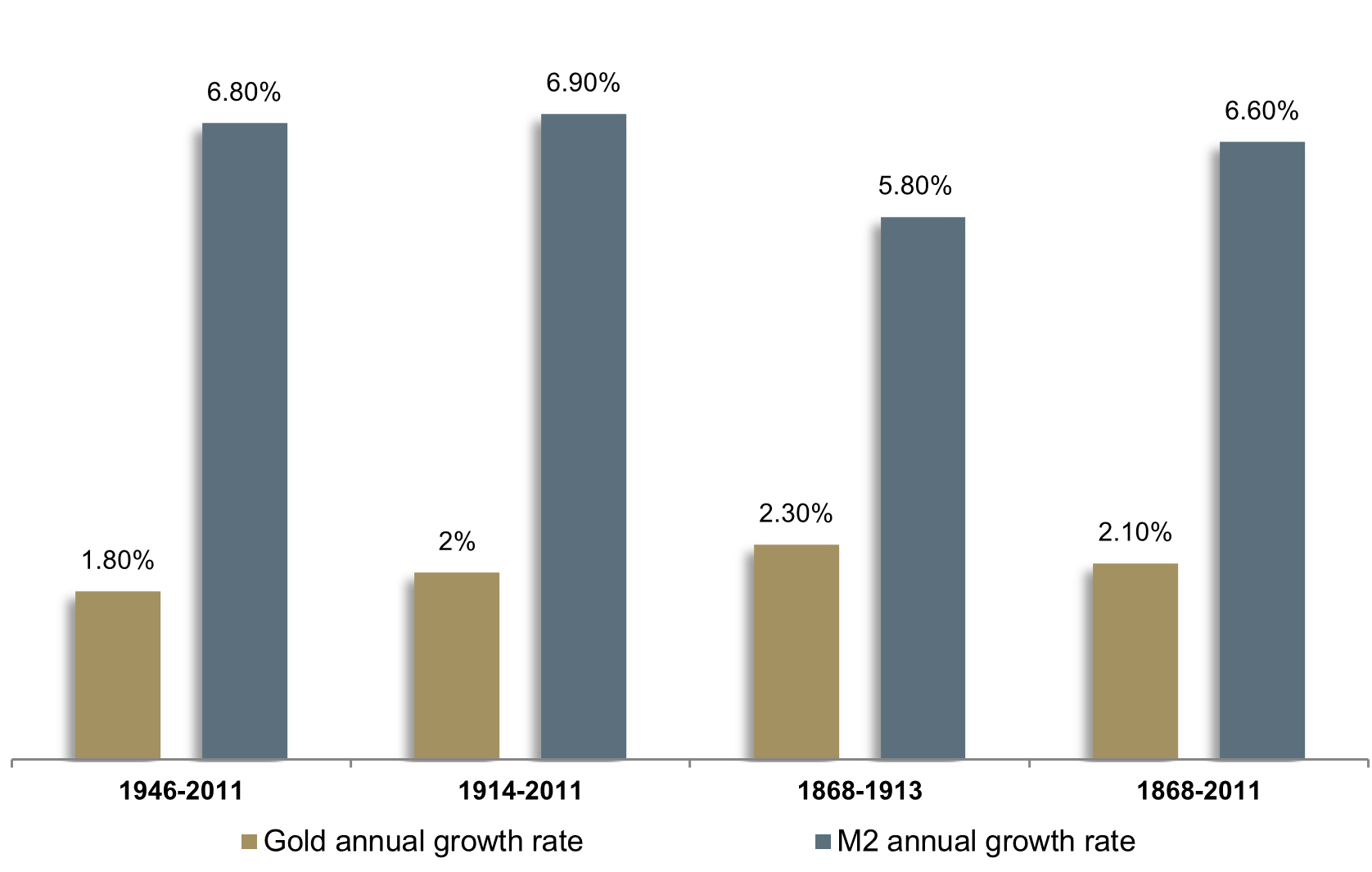

One can see this relative scarcity in the following illustrations. Between 1868 and 2011, the average growth rate of the monetary aggregate M2 was 6.6%, while the stock of gold grew only by 2.1%. M2’s historical volatility was also far higher, it ranged from minus 15.6% to plus 26%, while that of gold ranged only between 1.4% and a maximum of 3.5%.

Maximum, Minimum and Average Rate of Change of Gold versus Money Supply M2: 1868 to 2011

Source: GoldMoney Foundation, “The Aboveground Gold Stock: Its Importance and Its Size”, James Turk

If one analyzes the rates of change in different periods of time, one also notices the relative scarcity, the higher stability and lower volatility of the stock of gold. Since 1914, the year in which the Federal Reserve began to operate, the growth of M2 was 6.9% on average, while the stock of gold has only grown at 2% per annum.

Average Rate of Change Gold versus Money Supply M2 in Different Time Periods

Source: GoldMoney Foundation, “The Aboveground Gold Stock: Its Importance and Its Size”, James Turk

Despite technological progress and the associated increase in mine production, the stock of gold never grew by more than 3.5% in a year. This constant growth of the stock of gold results from the properties of natural deposits. Even if it takes ever more effort and becomes more expensive to mine gold, this is compensated by ever more efficient mining technology.[6]

What does this actually mean? Let us assume that the price of gold rises considerably in the future and mining adjusts accordingly, then mining of e.g. 3,500 tons per year would certainly be possible within 10 years time. If we assume further that annual mine production grows by 3% p.a. over the next ten years, cumulative mine production would amount to about 31,000 tons over the period. The total stock of gold would then amount to approximately 203,000 tons by 2023. If mine production were to amount to 3,500 tons at that point in time, this would still only represent an annualized inflation of the stock of gold of 1.7%.

c) Stock-to-Flow Ratio as the Most Important Reason for Gold’s Monetary Importance

Once again we return to the “greatest misunderstanding in the gold sector” [7] There is a clear difference between commodities, which can be explained by a consumption model (e.g. crude oil, copper, agricultural commodities) and goods that are bought in order to be held (gold, diamonds, works of art). While the economic utility of a consumable good is created when it is destroyed or used up, the utility of investment assets lies in their possession and later resale. Industrial commodities therefore have low stock-to-flow ratios, this is to say, inventories usually only cover consumption demand for a few months. If there were no inventories at all, supply would have to correspond exactly to production and demand exactly to consumption. However, if there are inventories, consumption can temporarily exceed production. Since inventories of consumable commodities are as a rule very low, prices will rise quickly in anticipation of a future supply shortage and bring consumption into balance with production.[8]

Unlike consumable commodities, gold and silver exhibit a large discrepancy between annual production and the total available supply (= high stock-to-flow ratio). As already discussed last year, it is our premise that the high stock-to-flow ratio represents the most important characteristic of gold (and silver). The entire amount of gold ever mined totals approximately 172,000 tons. That is the stock. Annual production was about 2,700 tons as of 2012. That is the flow. If one divides the two amounts, one arrives at the stock-to-flow ratio of currently 64 years.

We therefore proceed from the premise that gold isn’t as valuable because it is so rare, but quite the opposite: Gold is valued so highly because annual production relative to the existing stock is so small. Putting it differently: not only scarcity, but primarily the relative constancy of the available stock is what makes gold unique. The annual production of 2,700 tons is therefore not relevant to price determination. This characteristic was attained over centuries and can no longer be altered. This stability and security is a crucial precondition for creating confidence.

Apart from gold’s unique stock-to-flow ratio its high marketability is another important feature. The easier it is to exchange a commodity, the more pronounced its ‘moneyness‘ is. Carl Menger developed the theory of marketability in the 19th century. According to this theory, gold has established itself in a long term evolutionary process, because its marketability was higher than that of any other good. According to Menger, the marginal utility of gold therefore declines more slowly than that of other goods.[9] Gold and silver therefore enjoy their monetary status not due to their alleged scarcity, but rather due to their superior marketability.

In this respect there is a crucial difference between gold and other stores of value such as expensive real estate, diamonds or art objects. A Picasso painting, an expensive Bordeaux or a unique piece of real estate are all difficult to liquidate at an acceptable price in a liquidity emergency during a crisis situation. Furthermore, the specific features of art objects or real estate are only ascertainable after extensive due diligence. The fungibility of gold is therefore a crucial differentiation.[10] This seems to be an additional reason why central banks are hoarding gold and not real estate, art objects or commodities as their main currency reserve.[11]

The reason why individuals don’t spend all of their money today is their reservation demand[12] for money and the greater utility they expect it to command in the future. Reservation demand is therefore essential for price determination. The decisive factor is who values gold more highly: the new, incremental buyer, or the existing owner. The majority of gold analysts however focuses exclusively on ‘exchange demand’ and therefore assumes that price determination in gold can be forecast with the help of a simplistic consumption model.[13]

Closely related to this concept is the reservation price. Every gram of gold that is held for a variety of motives is for sale at a certain price. The motives for holding gold are diverse: as jewelry, as a currency reserve, in the form of objects of art, for technological applications, and so forth. Similarly diverse are therefore the associated time horizons, which range from the short term speculation of a trader to the generation-spanning insurance of an Indian bride. These decisions are not transparent, but depend on a range of competing opportunities in the course of time.

As a result, opportunity costs are essential for the gold price. How significant are the competing economic opportunities and risks that I am exposed to because I am holding gold? Real interest rates, growth rates of monetary aggregates, size and quality of debt, political risks, as well as the attraction of other investment classes are the most important determinants of opportunity costs. All market participants employ different filters, thoughts and time preferences in this context, which influence their price determination.

Everybody who owns gold is therefore part of the supply side. Gold owners and non-owners alike constitute the buy side because they are all capable of demanding additional units. There will always be a price, or a combination of price and circumstances that will induce market participants to sell their gold. For some this will be at a far higher price level, for some however also at a significantly lower price level (for instance as a consequence of a deflationary collapse). The decision not to sell gold at the prevailing price level is therefore just as important as the decision to buy gold.

d) The Ongoing (Re-)monetization of Gold in the International Financial and Monetary System

“As the international community attempts to take on these challenges, gold waits in the wings. For the first time in many years, gold stands well prepared to move once more towards the center-stage. This could be the start of an immensely important phase in the history of world money.”

OMFIF

The renaissance of gold in classical finance continues. OMFIF[14], a global think tank for central banks and sovereign wealth funds, in a sensational report[15] argues in favor of a remonetization of gold. In their view, gold should once again play a central role in the international currency framework. Due to its history, gold is said to be predestined to restore the structure and maintenance of trust and stability in international monetary relations.[16] Gold would be of mutual benefit for all countries as an anchor for currencies and could put an end to the currently escalating currency wars. OMFIF however doesn’t recommend a return to a classical gold standard. Gold should primarily settle balance of payments transactions. The report shows strikingly that fundamental changes to the currency system are already being discussed at the highest levels.[17]

OMFIF recommends the inclusion of gold in the IMF’s special drawing rights. This possibility was also mentioned by the governor of the People’s Bank of China. He regards SDRs as a “light in the tunnel of reform of the international currency system”.[18]SDRs are a currency unit introduced by the IMF, which isn’t traded on foreign exchange markets[19]. Currently the US dollar has a weight of 41.9%, the euro 37.4%, the Japanese yen 9.4% and the British pound 11.3%. Apart from gold, the ‘R-currencies’[20] are also supposed to receive a higher status in the international currency framework and are to be included in the SDR basket.

Due to its high liquidity and its unique characteristics, gold is increasingly used as collateral. Following Eurex, CME Group, the International Exchange and JP Morgan, LCH Clearnet, the largest clearing house in the world, now also accepts gold as collateral.[21] Clearnet functions as a clearing house for the largest international exchanges and trading platforms, as well as a number of OTC markets and derivatives. It appears as though there are worries about ‘event risk’, systemic and monetary risk.

Especially in the US, calls for gold backing, respectively the acceptance of gold as an official means of payment, are becoming ever louder. After the state of Utah already approved gold and silver as an official means of payment in 2011, similar plans are now considered in more than a dozen additional federal states.[22] The initiatives are among others receiving support from the Tea Party movement and the Gold Standard Institute. We interpret this development as an expression of increasing dissatisfaction with the financial and monetary policy of the United States. The symbolic effect of these initiatives is enormous, and we see a gradual continuation of this trend toward remonetization.

The growing number of initiatives that demand repatriation and a credible audit of state-owned gold reserves, also illustrates the growing importance of gold. In the case of the German Bundesbank (about 500 tons in eight years) this appears mainly designed to soften public pressure. However, many other countries are now also following the example of Charles de Gaulle.[23] Thus there are initiatives emerging in Mexico, Switzerland, the Netherlands, Azerbaijan and Romania that focus on demanding a repatriation of gold. We are convinced that this desire for transparency not only demonstrates the growing interest of populations in the gold reserves held by their governments, but is also an indication of growing distrust between central banks.

Last year no less a figure than German Bundesbank president Jens Weidmann drew attention with a speech in which he revealed himself as extremely critical of covert government financing with the help of uncovered paper currencies. Even if he did not argue directly in favor of a gold currency, he explicitly pointed to gold’s function as a medium of exchange, a means of payment and a store of value.[24]

The demands for gold-backed bonds are growing ever louder. There are a number of precedents for its use as collateral in crisis situations. In the 1970s Italy and Portugal for instance employed their gold reserves as collateral for loans from the German Bundesbank and the BIS. In 1991 India used its gold as collateral for a loan from the Bank of Japan.

In a study commissioned by the European parliament, author Ansgar Belke came to the conclusion that gold-backed bonds would be far more transparent, attractive and fair for investors than government bond purchasing programs.[25] According to the study, gold-backed bonds would alleviate the sovereign debt crisis at least in the short term. The World Gold Council is lobbying along similar lines and advises Italy to issue gold-backed bonds. A portion of its gold reserves of 2,400 tons should be used as collateral. That should lower financing costs and restore the damaged confidence in Italy’s creditworthiness.[26]

“Simply speaking, a gold-based solution would be less inflation-prone. Those arguing that the gold-backing solution would decouple the money supply and hard currency potentially leading to hyperinflation neglect the current non-role of gold for backing a currency. But above all, the use of gold as collateral avoids or lessens in importance, the reduction of incentives for reform of the beneficiary countries under the SMP and the OMT.” Ansgar Belke in a paper to the European parliament.[27]

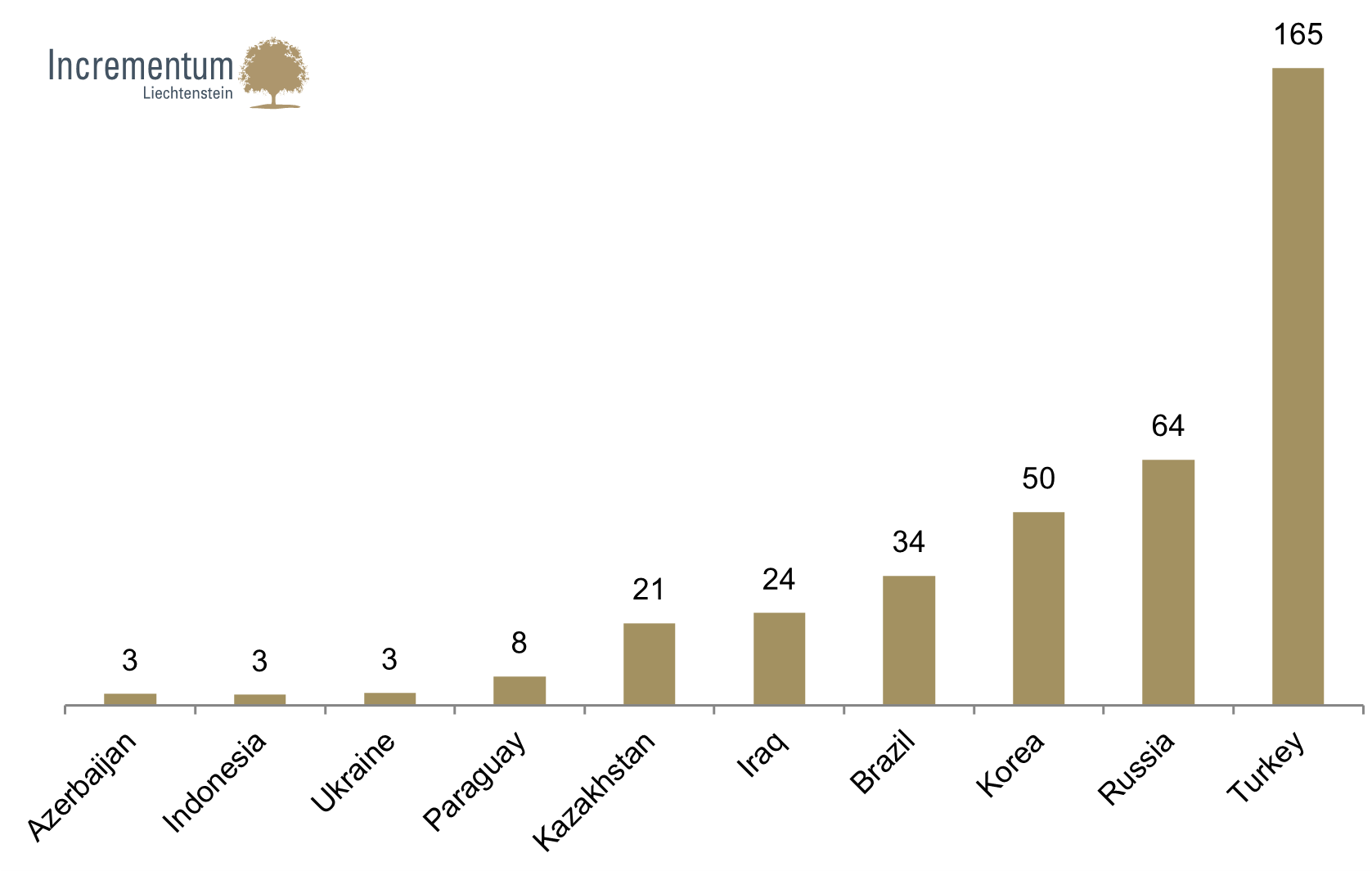

Central bank buying amounted to 534 tons last year. That is the largest quantity since 1964. In 2013, the IMF expects a net amount of 550 tons. Especially emerging countries show increasing confidence with respect to their own (economic-) political power, and on the other hand growing distrust toward established reserve currencies. This is demonstrated by the strong increase in gold purchases by the central banks concerned.

Central Bank Buying Since July 2012 in Tons

Source: World Gold Council

While France was the most important critic of the dollar’s currency hegemony in the 1960s (prior to the collapse of the Bretton Woods system), China appears to have taken on this role today. France at the time criticized the “exorbitant privilege” [28], stopped buying US treasuries, converted dollars to gold and repatriated gold. China is currently behaving in a similar manner, calling the dollar’s status a “product of the past”.[29] We assume that a speedy transformation of the renminbi into a reliable, stable and globally traded currency is one of the top priorities of China’s leadership.[30]

International acceptance of the Renminbi is proceeding apace. In the first half of 2012 the renminbi’s share of cross-border trade was already at 11% (vs. 7% in 2011 resp. 2% in 2010). China has recently taken a number of important steps in the direction of emancipation from a dollar-centric worldview. With the help of bilateral trade and clearing agreements, the economic integration and convertibility of the renminbi is gradually built up. The PBoC has thus negotiated 18 swap agreements with other central banks, among them those of Japan, South Korea, Hong Kong, Singapore, Argentina, Australia and most recently the United Kingdom[31]. More than 10 Asian central banks already hold renminbi reserves, and there are plans to expand this to South America, Africa, Europe and the Middle East. In September 2012 China announced that every country that wishes to trade crude oil can henceforth do so in Chinese currency as well. Shortly thereafter Russia publicized that it had entered into a trade agreement with China, in the context of which there will be unlimited oil sales to China. This trade will be billed exclusively in renminbi.

China wants to establish the renminbi as the dominant currency among emerging markets. That is reminiscent of the German Mark, which was a hard currency alternative to the US dollar in the 1970s and 1980s. This goal can however only be reached if its exchange value is strong and confidence in its future purchasing power is high. We believe that gold will be one of the pillars of China’s strategy. Specifically, we assume that China’s central bank continues to accumulate gold covertly, and believe that it is possible that gold-backing of the renminbi is planned. A gold-backed renminbi would increase its international acceptance in one fell swoop. The enormous gold reserves held by the United States[32] were for instance – aside from its military superiority – a major reason why the US dollar became the global reserve currency.

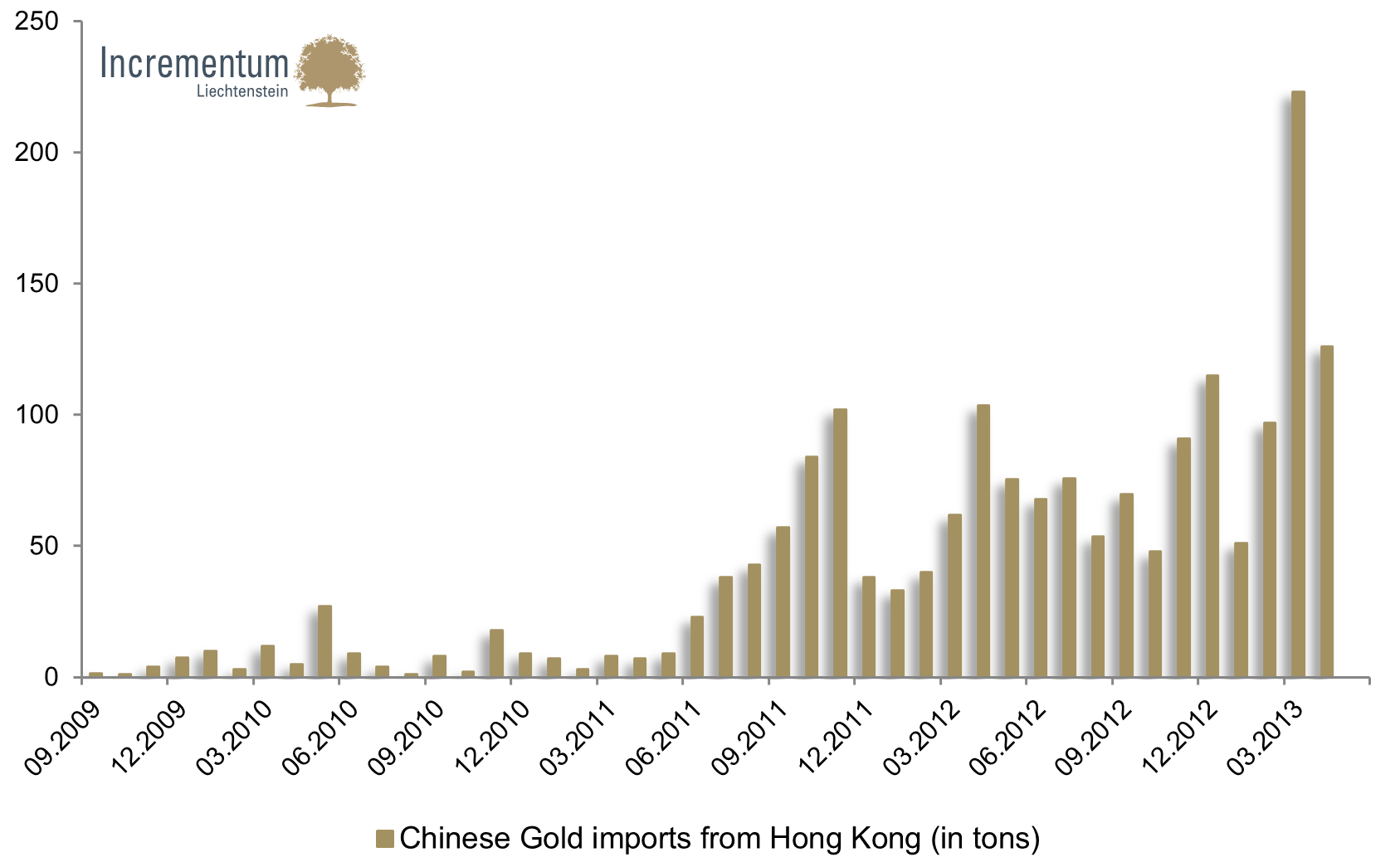

According to the World Gold Council, the central bank of China hasn’t bought any gold since 2009. The fact that there haven’t been any official announcements in four years clearly argues in favor of the notion that China will once again report surprisingly larger gold reserves. There is a lot of circumstantial evidence pointing in this direction. Last year, gold imports to the mainland from Hong Kong rose by 47% to nearly 560 tons. The momentum clearly appears to be increasing, as imports since the beginning of this year already amount to 498 tons.

China’s Gold Imports from Hong Kong (in tons)

Source: Hong Kong Census &Statistics Department, Incrementum AG

Our assumption is also confirmed by statements made by Chinese officials. In 2009 already, the newspaper China Youth Daily reported that there is a task force with a mandate to increase China’s gold reserves. The gold reserves are supposed to be increased to 6,000 tons within the coming 3 to 5 years and subsequently to 10,000 tons. This is also confirmed by a representative of China’s chamber of commerce. According to his statement, China is going to increase its gold reserves to up to 8,000 tons.[33] We therefore assume that the PBoC is currently massively expanding its gold reserves and holds far higher reserves than the officially reported 1,054 tons. We believe it is realistic that China has by now 4,000 – 6,000 tons, and with that the second largest gold reserves worldwide.

e) Excursion: Reasons for ‘Aurophobia’

It appears as though there are only two camps: people who love gold (a.k.a. ‘gold bugs’) or people who hate it. Between those two extremes there appear to be very few shades of gray, and people are only very slowly moving from one camp to the other. It appears as though there existed – especially in the financial sector – an ‘aurophobia’. In our opinion there are a number of phenomena of behavioral psychology (behavioral economics) that explain the extreme emotions attached to gold.

- Mental accounting: People always categorize financial transactions in terms of ‘mental accounts’ and evaluate them differently. Interest income is for instance booked in different accounts than price gains. Dividends are therefore regarded as a permanent addition to income, while capital gains are not booked as permanent, even though both have the exact same financial utility. That also explains why the phrase ‘gold pays no interest’ appears to be such a central counter-argument to owning gold.

- Normalcy bias: This describes the mental state of distorted perception people enter when facing a disaster.

- Cognitive dissonance[34]: it emerges if one’s stable and positive conception of oneself is endangered, if someone receives information that makes him look stupid, immoral or irrational. This appears to be the reason for the fact that the first ever purchase of gold costs many people an enormous mental effort.

- Availability heuristic and selective perception of information: Human beings tend to overestimate the importance of events of the recent past relative to events that have happened a long time ago. The recent past is therefore extrapolated into the future.

[1] we have already discussed the portfolio characteristics of gold in our previous gold reports in some detail, see “Gold as Portfolio Insurance” – Gold Report 2011 as well as “Gold as a Stabilizing Portfolio Component” – Gold Report 2012

[2] total return, i.e., including dividend payments

[3] all data CAGR. Periodicity from 1971, except emerging market stocks (from 1988), euro zone stocks (from 1987) and US treasuries (from 1974)

[4] see: “Global Wealth 2012: The Year in Review”, Credit Suisse

[5] the total stock of gold is much higher, however not liquid as it is either in the form of objects of art, central bank reserves, as jewelry not for sale, or in technological products.

[6] see: „The Above Ground Gold Stock: It’s Importance and Its Size“, Gold Money Foundation, James Turk and Juan Castaneda

[7] see: „What is key for the price formation of gold“, Robert Blumen, The Matterhorn Interview

[8] see “In Gold We Trust 2012” – “The Biggest Misunderstanding in the Gold Sector” as well as “Does Gold Mining Matter?” and “The Myth of the Gold Supply Deficit” by Robert Blumen

[9] see: “The Gold Problem Revisited”, Prof. Antal Fekete

[10] This fact is often on display in stress situations in the financial system. In such periods, it is never the offer that disappears, but always the bid. Due to its high liquidity and the low bid-ask spread, gold is therefore often quickly liquidated in stress situations in order to create liquidity.

[11] see: „Bitcoin: Money of the Future or Old Fashioned Bubble“, Mises Daily, Patrik Korda

[12] Reservation demand means that by holding on to something and making a conscious decision not to sell, one actually generates demand. Every good one holds and decides not to sell is subject to reservation demand.

[13] A remark: this is also why we believe that it is a mistake that gold is mainly analyzed in commodity research departments, as currency research departments appear to be to be far better suited to the task.

[14] Official Monetary and Financial Institutions Forum

[15] „Gold, the Renminbi and the multi-currency reserve system“, OMFIF, January 2013

[16] see: „Ein Schub für Renminbi und Gold“ (A push for renminbi and gold), Lars Schall

[17] see: „The Central Bank Revolution II“, Hinde Capital, 2013

[18] see: „China eyes SDR as global currency“, China daily

[19] Besides its normal functions, the IMF can also issue SDRs. This has – so far – not happened to any significant extent.

[20] Renminbi, Indian rupee, Russian ruble, Brazilian real and South African Rand

[21] http://www.zerohedge.com/news/lchclearnet-accepts-‘loco-london’-gold-collateral-next-tuesday

[22] http://www.bloomberg.com/news/2013-04-08/trust-in-gold-not-bernanke-as-u-s-states-promote-bullion.html

[23] Under the leadership of de Gaulle, France (on the advice of the legendary Jacques Rueff), converted the bulk of its dollar reserves according to the framework of the Bretton Woods agreement into gold, and thereafter shipped it to France “so that it wouldn’t be exposed to the grasp of a foreign power”.

[24]http://www.bundesbank.de/Redaktion/DE/Reden/2012/2012_09_18_weidmann_begruessungsrede.html

[25] SMP – Securities Markets Program

[26] “Italy considers gold as an alternative to austerity“, World Gold Council

[27] “A More Effective Euro Area Monetary Policy than OMTs – Gold-Backed Sovereign Debt”, European parliament, Ansgar Belke, DIW Berlin and University of Duisburg-Essen

[28] a designation by the former French finance minister Giscard d’Estaing, in the 1960s, which described the US privilege and the power of the global reserve currency.

[29] see: Inflationary Deflation“, Paul Mylchreest, Seymour Pierce

[30] Although one should clearly differentiate between a reserve currency and a trade currency

[31] “UK and China establish currency swap line”, Financial Times

[32] in 1952, the US gold reserves amounted to 29,663 tons

[33] “China should significantly boost gold in reserves“, Reuters

[34] Cognitive dissonance is a term in social psychology that explains an ” emotional state perceived as uncomfortable that comes from humans having several cognitions at once; perceptions, thoughts, opinions, attitudes, wishes or desires that are conflicting with each other, hence a kind of ‘feeling of disturbance’.