The 2011 report opened with a striking assessment of the macro environment:

“The (financial) world is currently long in questions but short in answers. We believe that gold is still one of the few right answers in times of chronic uncertainty.”

This was not rhetorical flourish. In 2011:

Sovereign debt levels were exploding

Central bank balance sheets had ballooned

Real interest rates were deeply negative

Political cohesion in the Eurozone was under severe strain

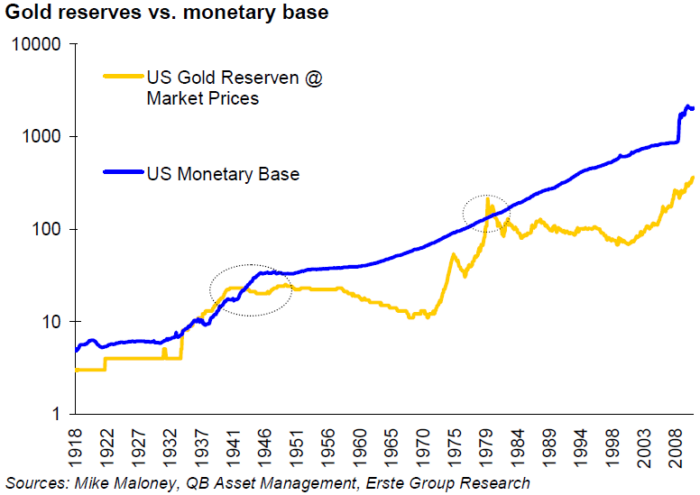

The monetary system stood at a crossroads. In lieu of being perceived as a mere commodity, gold was increasingly being viewed as money.

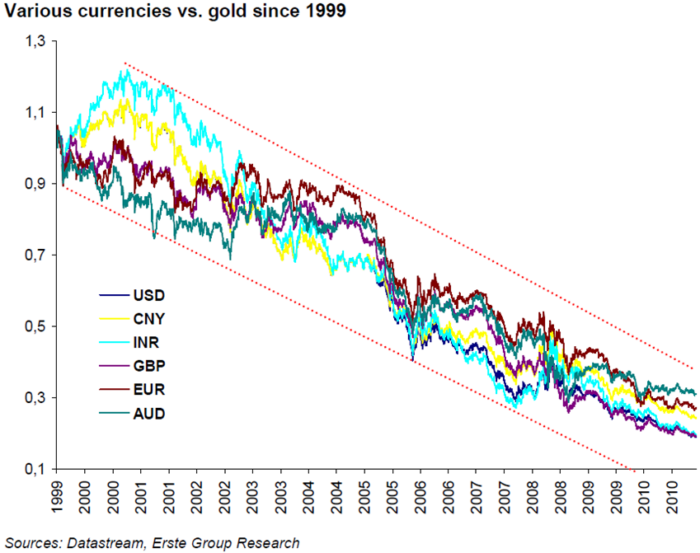

In our latest editions – especially IGWT 2025 – we described the 2000–2011 period as a Golden Decade, the second great secular bull market since the end of Bretton Woods.

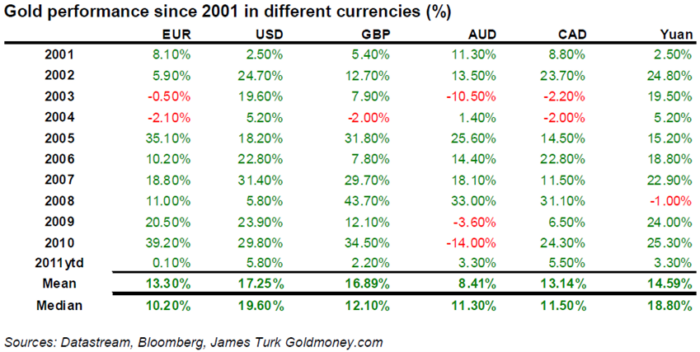

By 2011, the performance numbers were extraordinary:

“+25%, +140%, +460%, +4,322%. These are the performances since the previous Gold Report, since the first Gold Report, since the beginning of the bull market in 2000, and since 1970.”

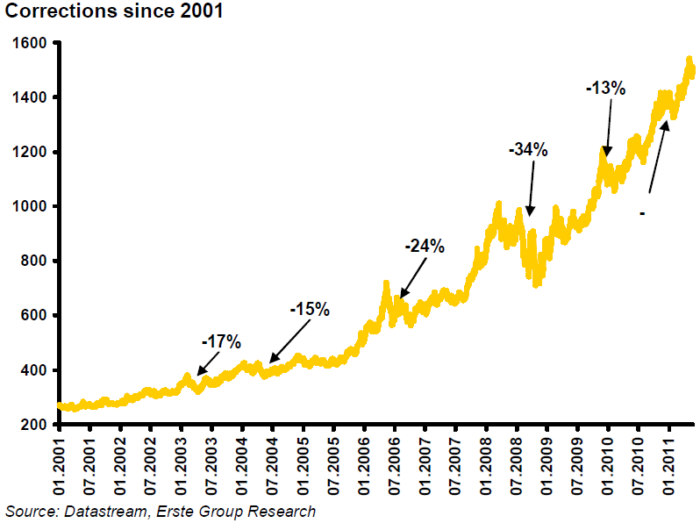

What began quietly in 2001 accelerated dramatically after 2008. Despite corrections – particularly during the financial crisis – the second half of the decade saw gold enter a powerful upward phase.

The climax came on September 6, 2011, when gold reached USD 1,921, just shy of the USD 2,000 mark. For most, such a level seemed bold only months earlier.

Even after a decade of gains, the 2011 report argued there was no reason for “aurophobia”: the irrational fear of gold. Despite strong performance, gold remained under-owned, underweighted, and widely misunderstood. The report emphasized that skepticism toward gold often reflects discomfort with what it represents. As Joseph Schumpeter famously observed:

“The modern mind dislikes gold because it blurts out unpleasant truths.”

Plainly, gold challenges monetary complacency by exposing the excess debt, the distortion of interest rates and the fragile confidence. This is precisely why it remains indispensable.

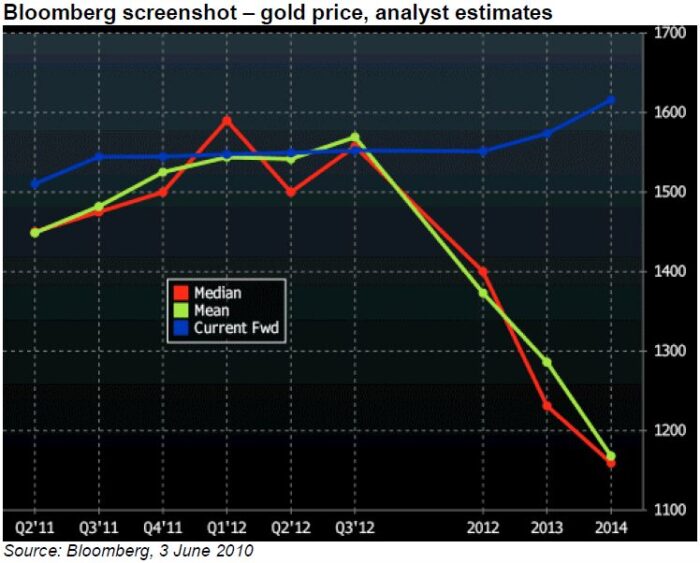

In the 2010 edition, we had set a target of USD 1,600. Meanwhile, mainstream analysts were projecting a median gold price of just USD 1,163 for 2011.

In any event, gold hit USD 1,600 on July 18, 2011, almost exactly when the IGWT 2011 was published.

This divergence from consensus thinking was not luck. In truth, it was rooted in a disciplined analysis of:

Monetary expansion

Structural debt dynamics

Real interest rate suppression

The Austrian School’s monetary theory

The 2011 edition did not stop there. It reaffirmed a higher objective:

“Next target price at USD 2,000. At the end of the parabolic trend phase we expect at least USD 2,300/ounce.”

The rationale was straightforward:

The inflation-adjusted 1980 high pointed toward USD 2,300

Structural over-indebtedness suggested prolonged monetary accommodation

Negative real rates provided the ideal tailwind

Gold ultimately peaked at USD 1,921 – just short of the symbolic USD 2,000 level – marking the high-water mark of the Golden Decade.

One of the most forward-looking aspects of the 2011 report was its discussion of a potential shift in the global monetary architecture.

The question posed was bold:

“The monetary system at the crossroads – on the way to a new gold standard?”

Already in late 2010, then–World Bank President Robert Zoellick had called for the development of a monetary system to succeed “Bretton Woods II”.

In hindsight, this discussion was remarkably prescient.

Following the freezing of Russian FX reserves in 2022, debates about de-dollarization and a potential new monetary order have intensified. In IGWT 2023, Zoltan Pozsar described this emerging framework as “Bretton Woods III” — a more commodity-anchored, multipolar system.

The seeds of that debate were clearly visible in 2011.

Another core message of IGWT 2011 was philosophical:

Gold is not a trade. Gold is not a momentum play. Gold is insurance.

As the report emphasized, gold carries no counterparty risk. In a system increasingly built on leverage, derivatives, and fiscal promises, that distinction matters.

Gold functions as:

A hedge against monetary debasement

Protection during recessions

A stabilizer during systemic stress

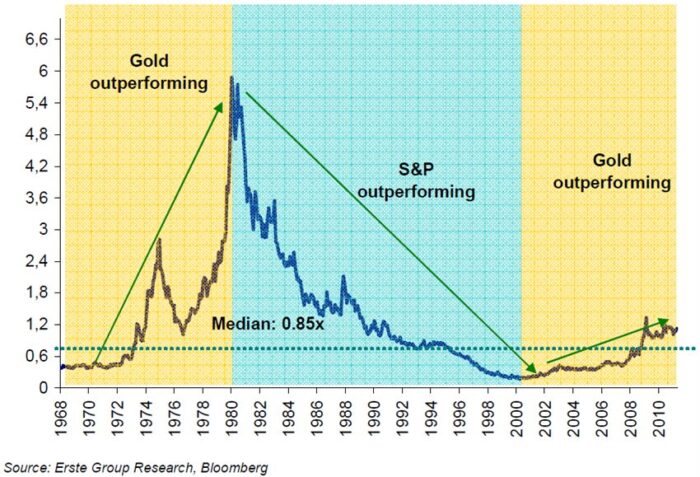

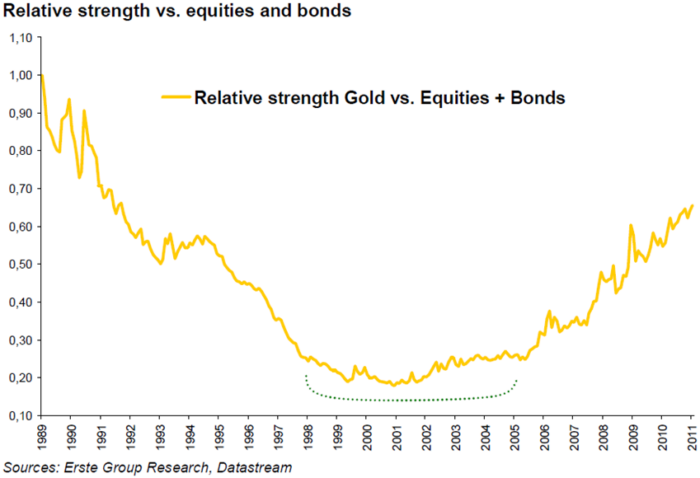

Evidently, history repeatedly confirms that during equity bear markets, gold often preserves or increases relative value.

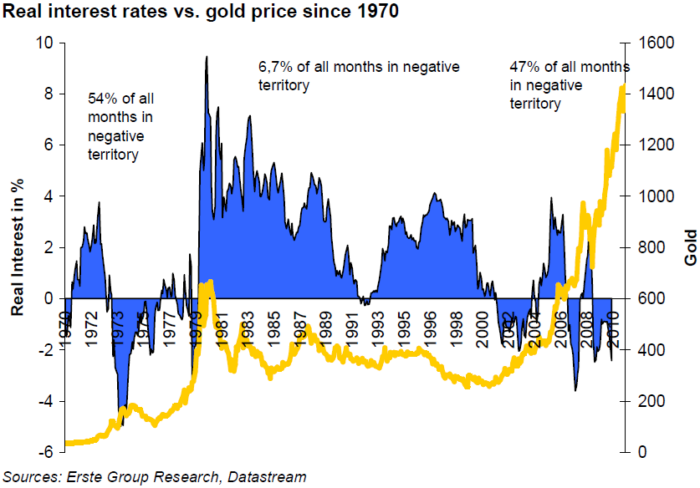

The 2011 report highlighted the importance of real interest rates:

When real yields fall below zero, the opportunity cost of holding gold collapses.

Between 2000 and 2011, real rates were negative nearly half the time. Undoubtedly, this formed a powerful structural backdrop for the secular bull market.

Curiously, as yields are pushed higher today due to relentless fiscal profligacy, this framework has ceased to be relevant.

Looking back, the IGWT 2011 captured:

The climax of a secular bull market

The consequences of excessive monetary expansion

The fragility of the fiat system

The re-monetization of gold

A price target that nearly materialized

Few analyses at the time were as aligned with unfolding reality as this one… if any.

The 2011 report stands as a landmark publication within the IGWT series. A snapshot of a turning point in monetary history.

🔗 We invite you to revisit this historic edition in full.

As we continue our 20 Years, 20 Threads journey, we look forward to revisiting further milestones that shaped the gold market, along with the global monetary landscape.

In times of uncertainty, one constant remains: In Gold We Trust.

#20Years20Threads #InGoldWeTrust #GoldReport #GoldSurge #GoldInvesting #GoldenDecade #PreciousMetals #ATH #MacroTrends #AssetPerformance #SafeHaven #InflationHedge #SoundMoney #MarketAnalysis #BullMarket #InvestmentInsights #MonetaryReserves #MonetaryReset #GoldStandard #Multipolarity #DeDollarization #GrowthExpectations #EconomicDepression #MonetaryPolicy #CentralBanking #DebtGrowth #QE #ZIRP #NIRP #PriceTarget #GoldForecast #RiskManagement #AssetAllocation #MarketDrawdowns #AlternativeAssets #AustrianEconomics #IGWT10 #IGWT11 #IGWT23 #IGWT25 #MacroResearch #AnniversarySeries