In Jackson Hole, Wyoming, Powell subtly, but decisively, changed his tone. As Ted Butler explained in his Sound Money Report article The Fed’s Prisoner’s Dilemma, Powell acknowledged on August 22 that interest rates appeared to be “in restrictive territory.”

That phrasing mattered. Demonstrably, it signaled that monetary policy was approaching a pivot: a more dovish stance and, eventually, rate cuts. Markets immediately understood the implication that lower rates mean looser financial conditions, a weaker dollar, and rising inflation expectations.

At first, gold responded, as expected. Immediately after, silver followed, though with far more torque.

From late August to September, silver’s advance was driven by investors and speculators positioning for a renewed easing cycle. With real yields set to fall, demand for hard assets intensified. Seeing that silver boasts a dual role as a monetary metal and an industrial input, it became especially attractive.

Anticipating the Fed’s policy change, the markets began to discount this new reality on the price of precious metals. Undoubtedly, this was not yet a frenzy and the surge was not restricted to silver, since gold, for the most part, mirrored its little brother’s advance.

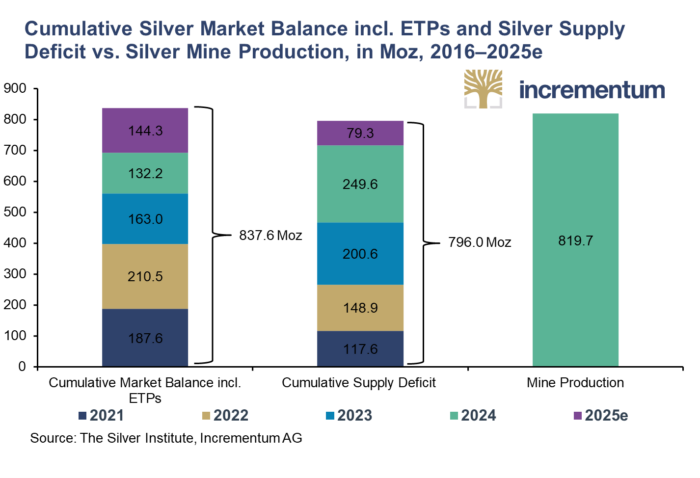

In October, the rally entered its first climax. Demand for physical silver became so intense that it triggered what we later dubbed The Great Silver Squeeze of October 2025. In our October 15 article, The Great Silver Shortage: How Bullion Banks Are Navigating a Perfect Storm, we argued that silver’s long-suppressed fundamentals were reasserting themselves.

Several forces converged. To wit:

Persistent systemic supply deficits

Record industrial demand

Declining mine output

Inventory shortages in key hubs such as London’s LBMA and New York’s COMEX

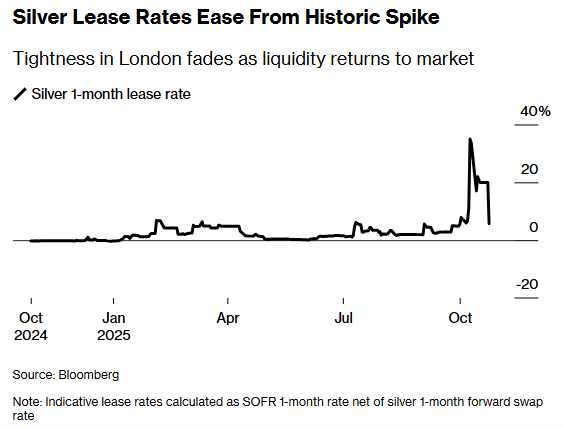

A broken leasing market, as the lease rate reached 39%, which exposed the fragility of the bullion banking model

As futures dominance weakened, the physical market began to dictate price action. This episode revealed how large synthetic positions were backed by surprisingly limited physical reserves.

Once emergency shipments of silver arrived in London, the acute shortage eased. Therefore, the squeeze subsided, marking the end of phase one. But as we wrote at the time, this was likely “the opening act of a longer bull market.”

In late November 2025, our article China’s Rising Influence on Gold and Silver Markets explored a crucial structural shift: physical demand is increasingly emanating from the East, while price discovery keeps on being executed in the West. Interestingly, the extreme shortage of silver in the Western hubs has flipped the usual direction of the flow of precious metals, particularly of silver.

All the same, China’s role in silver is anything but marginal. Evidently, it is a dominant industrial consumer, a major producer, and a strategic actor. The subsequent price action has validated our conclusion that China is quietly reshaping the precious metals landscape. In any event, the world is only beginning to grasp the implications of this development.

More recently, headlines around Chinese silver export restrictions proved overstated. Still, they highlighted the real driver behind today’s silver dynamics: the US–China Trade War.

Due to its unique characteristics and important uses, silver has been deemed a critical mineral. In a world of decoupling and supply-chain weaponization, industrial users are scrambling to secure long-term access to the metal. Unsurprisingly, governments are actively supporting this behavior as part of broader industrial and strategic agendas.

Within this framework, fiscal policy is taking precedence over monetary policy, which is a vision that aligns with the so-called Mar-a-Lago Accord. Seen through this lens, the subpoenas served on Powell a week ago, on January 9, make perfect sense. Obviously, they are not an isolated legal event, but part of a deeper institutional struggle.

Over the last couple of weeks, geopolitics has unmistakably taken the helm of price action in precious metals. Following the capture of Venezuela’s authoritarian president, Nicolás Maduro, on January 3, risk premiums across commodities initially expanded as markets reassessed political stability in Latin America. However, as the situation in Venezuela gradually faded from headlines, investors’ focus pivoted decisively toward the Middle East.

Very quickly, Iran has been gripped by widespread protests, which, according to multiple reports, have allegedly resulted in at least 2,400 casualties inflicted by the Iranian regime’s security forces. Against this backdrop, President Trump has repeatedly warned Tehran that any killing of peaceful protesters would trigger a U.S. military response. These statements were not isolated remarks, but part of a sustained escalation in rhetoric aimed directly at the Iranian leadership.

Two days ago, on Tuesday, President Trump went a step further, publicly telling protesting Iranians that “help is on its way.” Markets immediately interpreted this message as a credible signal of impending intervention. In response, investors rushed back into safe haven assets. Naturally, gold and silver surged sharply as geopolitical tail risks were repriced at speed.

However, the following day marked a sudden reversal. On Wednesday, reports emerged that U.S. aircraft carriers — critical assets for any large-scale military operation against Iran — were still days away from reaching the Persian Gulf. This clarification made it evident that no immediate military action was forthcoming. The market reaction was swift and brutal: risk premiums evaporated, safe-haven positioning was unwound, and the prices of gold and silver collapsed in dramatic fashion.

In an environment already strained by structural supply deficits, strategic competition, and fragile confidence in institutions, even shifts in rhetoric — let alone military movements — can trigger violent price swings. Plainly, such sensitivity has become a defining feature of the current silver market.

To fully understand the magnitude, and the true nature, of silver’s second-phase rally, it is essential to revisit the decisive catalyst identified by Ted Butler in his Sound Money Report Substack article, From $65 to $84 in 10 Days: Silver’s Christmas Cracker Explained.

As Butler demonstrated, the inflection point was October 26, 2025, when China’s Ministry of Commerce confirmed that it would enforce new export licensing restrictions on silver and other strategic metals, with the rules scheduled to take effect on January 1, 2026.

Unmistakenly, this announcement was the trigger. From the October 28 lows through year-end, silver embarked on a near-vertical ascent, rising approximately 60% in just over two months. By contrast, gold gained only around 12% over the same period. That divergence is telling and decisive.

On the one hand, gold was not subject to export restrictions. In addition, it was not directly entangled in trade-war dynamics, nor was it affected by industrial stockpiling or supply-chain weaponization. As such, gold’s comparatively modest advance reflects what one would normally expect from a classic mix of easing monetary policy expectations, geopolitical anxiety, and inflation hedging.

On the other hand, silver told a very different story. Succinctly, its explosive outperformance was not primarily driven by safe haven demand, nor by a sudden inflation scare. Instead, it was propelled by protectionist and industrial policy shocks, namely, the realization that a metal critical to electrification, defense, and advanced manufacturing could suddenly face state-controlled export bottlenecks from one of the world’s most important suppliers.

In short, silver was repriced as a strategic commodity, not merely a precious metal. This distinction matters enormously, as it explains why silver decoupled from gold so violently, why futures markets lost control to physical flows, and why price discovery became hypersensitive to trade policy, geopolitics, and industrial security rather than to monetary expansion and economic expectations.

Ultimately, the two-phased rally that began in August 2025 reveals how silver has evolved from a volatile brother of gold into a frontline asset in an era of great-power competition, geopolitical realignment, and resource nationalism. In that sense, silver’s surge was less about fear and far more about control.

#SilverRally #SilverSqueeze #PreciousMetals #Commodities #CriticalMinerals #GoldSurge #HardAssets #MarketStructure #SupplyDeficits #SoundMoney #SafeHaven #InflationHedge #MacroTrends #EconomicInsights #MarketAnalysis #PriceDiscovery #CentralBanks #FedPivot #Dedollarization #Geopolitics #TradeWar #Protectionism #EconomicStatecraft #WestVsEast