Past, present and future of the monetary order

“Auro loquente omnis oratio inanis est – When gold speaks, the world falls silent”

Gold has played a decisive role in monetary history since at least the times of King Croesus around 600 BC. Even today, when there is no longer any formal tie between gold and state-issued means of payment, the topics of gold and money remain inseparably interlinked. Currency systems have always changed. A glance at the history books reminds us that gold was needed time and again in order to create confidence in new currencies. Looking into the future suggests that this will likely sooner or later be the case again

a) Bismarck and the monetary system-related fall of civilizations[1]

The example of the fall of the Roman Empire provides an impressive account of how a growing bureaucracy and increasing misallocation of resources will lead to inflation and ultimately economic collapse.

An important study about the decline of major empires has been performed on behalf of former German chancellor Otto von Bismarck. He entrusted the historian, economist and agricultural politician Gustav Ruhland with the task of finding out why historical advanced civilizations and global empires collapsed. When the study was finalized, Bismarck was no longer in office, its insights were therefore not implemented. Ruhland’s insights should nevertheless be required reading for every citizen and politician.[2]

Ruhland came to the conclusion that the reasons for the decline of the ancient Greeks and Romans, as well as the Spanish and British empires were in all cases rooted in monetary policy. Ruhland noticed that peasants were always the first group that was no longer able to withstand growth pressures. It is impossible to endlessly exploit fields or milk cows. The peasants abandoned their fields and the government had to import food for the citizenry from ever more far-flung regions, which had to be conquered militarily.

According to Ruhland, in the downfall of the advanced civilizations he studied, this agrarian crisis was followed by a credit crisis related to land ownership, sovereign default, socialism and finally unrest.

Ruhland concluded:

“Different societies in different times and places all exhibited the same symptoms of ill health in their decline. This alone suggests that different people in history have experienced calamity due to the same economic malady. (…) And what should this genocidal malady be called? Economic science provides no reply to this question nowadays. As has already been stressed, modern-day macroeconomic specialization in its monographs regards every symptom as an isolated malady and treats it with reforms that fail to consider the big picture. Such a method (…) cannot be reconciled with the notion of the economy as an organism.”

Gustav Ruhland

With respect to the fall of Roman Empire, Ruhland formulated the following chain of causation:

- Growing impoverishment of the common people contrasted with an exorbitant increase in wealth/luxury of the few (Cantillon effect)

- Decline of tradesmen’s incomes due to cheap slave labor

- Increasing signs of decadence among the ruling classes (pomp, larceny, corruption, greed)

- Rising taxes, special levies; the government increasingly uses the military to collect taxes

- Government subsidizes the impoverished citizenry (keeping it calm with welfare statism, bread and circuses)

- Signs of decadence in the population, “barbarization” and a decline of morals

- External military conflicts to defend the status quo and/or as a distraction

- Bankers take over government

- Government intervenes in markets, national and monetary socialism

- Devaluation of money (e.g. by lowering the precious metals content of coins)

- Price inflation

- Uprisings, civil wars, external wars

- Chronic government insolvency

- Decline in population

- Barter trade replaces monetary economy

Parallels to the present are hardly deniable.

b) King dollar and the heirs to his throne

The current global monetary architecture is unique in the history of money. Following the Bretton Woods conference, the British pound had finally was replaced by the US dollar as the globally reigning currency. The United States emerged as the undisputed leading economic power in the post-war era. This was also reflected by the country’s gold reserves. With more than 20,000 tons of gold, the US was in possession of by far the largest gold reserves of all nations in the world.

During the second world war, US gold reserves increased rapidly, as the country’s large export surplus during the war was paid in gold at the time. Moreover, numerous rumors remain about the whereabouts of the gold held by the war’s losers, which possibly also found their way into the vaults of the victorious nations.

The gold exchange standard that was agreed upon in Bretton Woods in 1944 can be subsumed under the slogan “the dollar is as good as gold”. Due to an insufficient availability of gold, the finance ministers and central bank governors of 44 nations agreed to hold the dollar as a reserve currency[3]

in addition to their existing gold reserves. The Federal Reserve in turn committed itself to back at least 25% of the dollars in issue with gold and to convert dollars into gold if creditor central banks demanded it. The dollar’s exchange rate was fixed at 1/35th ounce of gold.

The International Monetary Fund was established as a “Bretton Woods institution”, inter alia in order to administer trade imbalances between countries by means of currency adjustments.

From this time onward, official foreign exchange reserves consisted partly of gold, but also of US dollars, resp. interest-paying treasury bonds. Central banks were able to obtain an interest income from holding treasury bonds, while the US was able to receive seignorage on a global level due to the demand for US debt securities.

The US started to abuse this “exorbitant privilege”, as French finance minister Valéry Giscard d’Estaing called it, in the 1960s at the latest, by monetizing its growing debt through the Federal Reserve. A number of countries were beginning to suspect that the gold reserves were no longer sufficient to back the amount of dollars in issue to the promised extent. After more and more countries, in the course of the so-called “gold drain”, demanded conversion of their dollar reserves into gold, Richard Nixon finally broke the convertibility promise on August 15, 1971.

After a very turbulent decade, the irredeemable dollar managed by the mid 1980s to regain its status as a global trade and reserve currency even without a formal gold backing. A major factor in obtaining this “King Dollar” status was the perception of disciplined monetary policy under Paul Volcker.

The international monetary system in force today is often called a “non-standard”. While the dollar is theoretically facing serious competition for the first time with the introduction of the euro, it nevertheless remains the undisputed number one currency in the world. This can be quantified by looking at its share of foreign exchange reserves (USD: 60.7% vs. EUR 24.2%), resp. its share of global currency trading (USD 87% vs. EUR 33.4%).[4]

Despite the US dollar’s continued dominance, there is ever more evidence that the dollar-centric worldview is slowly crumbling. We will discuss the most important indications of this trend in the following pages.

Today, the global financial system is dominated by the Bretton Woods’ institutions, IMF and World Bank. Voting rights in the two institutions no longer reflect the current economic balance of power, as a result of which emerging market nations (the BRIC countries in particular) increasingly feel they are underrepresented. For years they have argued in favor of reforms, which have already been agreed to on the level of the international organizations. However, the US Congress has to date refused to ratify these reforms, which would amount to a loss of power for the US.[5]

An additional trigger for the now openly waged conflict could be a paradigm change, which one only recognizes upon closer inspection of the relationship between the two largest powers. Historian Niall Ferguson has coined the term “Chimerica”, which describes the strong dependency between the two largest economies. The distribution of their roles is clear: while the Chinese consume little and save much, the exact opposite is the case with Americans. Americans buy Chinese products on credit, Beijing in turn uses its savings to extend credit to the US.[6] However, this community of interests may be about to change, which would have wide-ranging economic and political consequences.

.

c) Repatriation of gold reserves

A century ago, the idea of a currency without a fixed tie to gold, resp. without gold backing, would have been considered utterly absurd. Gold reserves represented the foundation of government sovereignty. Thus, it is not very surprising that the number of initiatives demanding a repatriation, resp. a proper audit of government gold reserves keeps growing. This desire for transparency illustrates the growing skepticism people feel towards the monetary experiments currently underway. However, they also express a strengthening desire for decentralized, sovereign and more individualistic policies.

While Germany continues to rather timidly remove its gold from Paris and New York[7], the Dutch central bank astonished the world by announcing (after the fact) the surprising repatriation of 122.5 tons from New York. In Austria, the National Bank (OeNB) announced its “new gold strategy”. A total of 110 tons of gold will be repatriated by 2020, in small tranches over the five-year period. Going forward, central bank governor Nowotny aims to have 50% of the country’s gold reserves stored in Vienna, 30% in London and 20% in Switzerland. The OeNB reacted to a critique by Austria’s court of auditors, which recommended a “rapid evaluation of all possibilities to achieve a better diversification of storage locations”.[8] After Germany and the Netherlands, Austria is the third European country to have decided to bring its gold back home. We are witnessing the biggest movement of international gold reserves in many years.[9]

Peter Boehringer, who started the German gold initiative, has made a remarkable statement. It is interesting that reports about Germany’s state-owned gold generate far more interest in the media than articles about the ESM, TARGET2 balances, and other guarantee cascades. According to Boehringer, this shows that people continue to perceive gold as real money. Physical tangibility, look and feel, are intuitive and indelibly etched in the part of the human mind that is responsible for the definition and perception of money, as Boehringer says in his highly interesting book “Holt unser Gold heim”. (“Bring our gold back home”).[10]

d) AIIB, NDB & Co.: The new challengers of Bretton Woods institutions?

October 24, 2014, could well go down in the history books as a turning point. On this day, the Asian Infrastructure Investment Bank, AIIB for short, was launched.

Why does this step send such a noteworthy signal? For the first time in the 21st century, an important international institution was established without the participation of the US. Especially peculiar is the fact that numerous close US allies, such as e.g. Great Britain, Australia, France and Germany are among the founding members – against an explicit US “recommendation” not to join.

Overview: Founding members of the AIIB

Source: The Telegraph

The AIIB will primarily provide financing for the rapid development of infrastructure projects (communication networks, railways, roads) and should finance projects worth several billion dollars within the coming few years.

The bulk of the financing volume will be directed towards the “new silk road” project. Many observers already call it the largest economic undertaking since the Marshall Plan. With this new version of the silk road, which once connected China to Central and South-East Asia, the Gulf states, Africa and Europe, Beijing hopes for an enormous economic boost, as well as the internationalization of its economy. Thus, Chinese companies are supposed to build airports, shipping ports, highways, railway lines and nuclear power stations on a grand scale in the nearly 65 countries connected by water and land.

Gold will also play a significant role in connection with the silk road. By means of a new gold fund with approx. USD 16 billion in AuM, stocking up on their gold reserves is to be made easier for member nations located along the silk road. Gold production in the likes of Afghanistan and Kazakhstan is also to be financed, according to state press agency Xinhua.[11]

In order to undermine the dollar’s dominance, emerging market countries have set a number of additional initiatives into motion: A milestone on the path to a multi-polar currency system was set in July last year. The BRICS nations, i.e., Brazil, Russia, India, China and South Africa, founded the New Development Bank (NDB). It is domiciled in Shanghai and supposed to develop into an alternative to the World Bank, the IMF and the Asian Development Bank[12] . With a population of three billion people (41% of the global population), 25% of global economic output and 42% of global foreign exchange reserves, the NDB combines an enormously important economic and growth area. In contrast to the World Bank, every member nation will have exactly one vote. Ironically enough, the establishment of the NDB was announced precisely on the 70th anniversary of the Bretton Woods agreement. The choice of this date is as subtle as a flying brick (so to speak).

The Shanghai Cooperation Organization (SCO)[13], will play an ever greater role as well in the future. The organization currently comprises China, Russia, Kazakhstan, Kyrgyzstan, Tajikistan, Uzbekistan as well as India, Pakistan, Mongolia and Iran in the role of observer nations. Turkey and Turkmenistan have also expressed interest in joining. Belarus, Afghanistan, the CIS and ASEAN are dialogue partners of the organization.

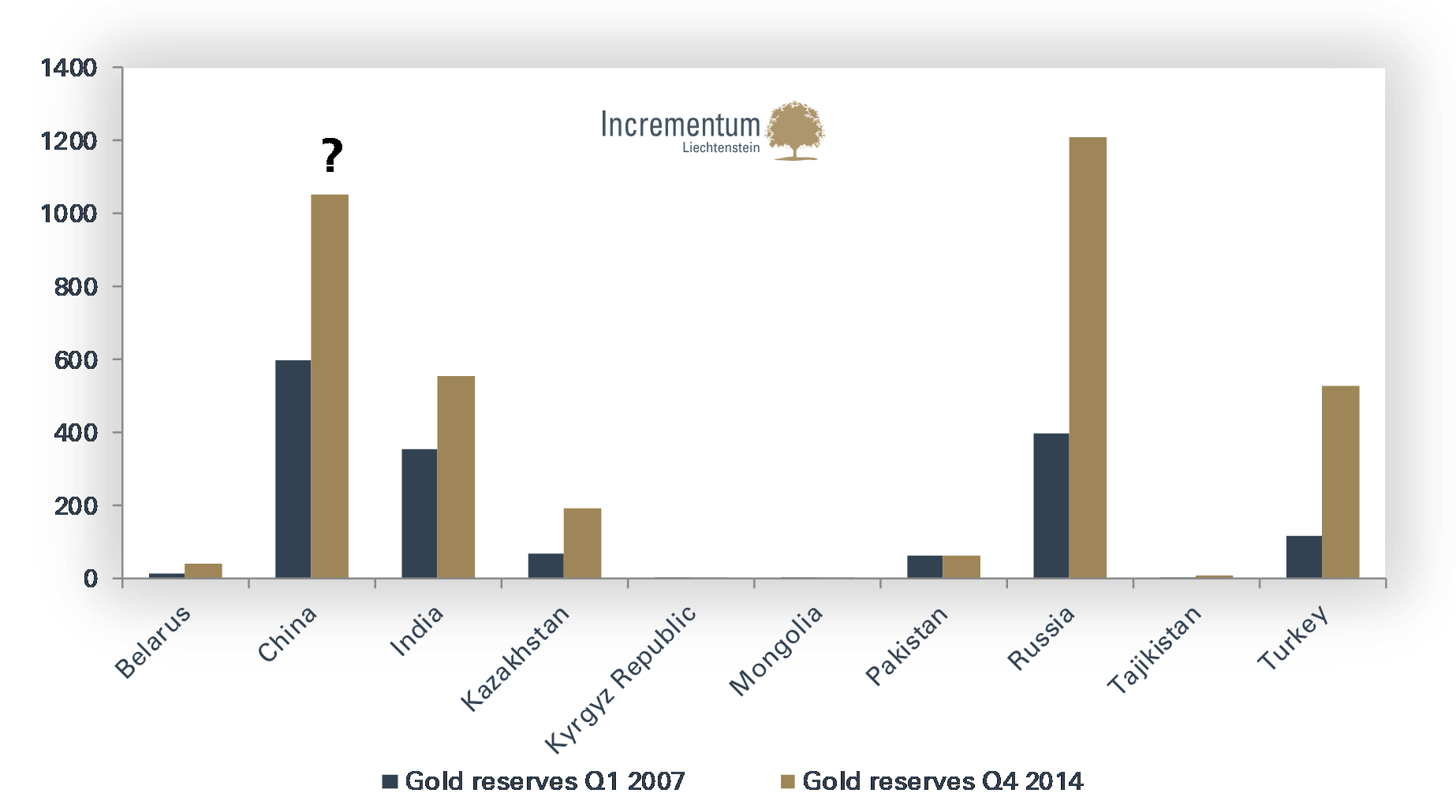

In our opinion, the importance of the SCO is vastly underestimated in the West. It is intended to unite the economic, as well as the military interests of Russia, China, and commodity-rich Asian nations in a single bloc. Should the current dialogue partners join the community, the SCO will comprise more than half of the world’s population. It would be naïve to believe that considerations with respect to currency policy aren’t going to play a role in this. We believe that gold is one of the pillars of the strategy. Interestingly, the region has a significant share of global gold production. Most of these countries have moreover significantly expanded the gold reserves of their central banks, as can be seen in the following chart.

SCO members: Gold reserves, Q1 2007 vs. Q4 2014

Sources: World Gold Council, Incrementum AG

The largely unknown Eurasian Economic Union should not be left unmentioned at this juncture either. Its current members are Russia, Kazakhstan, Belarus, Armenia and Kyrgyzstan. Apart from establishing a free trade zone, one of its goals is to launch a common currency. The so-called “Altyn” is supposed to be put into circulation within the coming five years. The currency’s name is originally from the Tatar language and actually means “gold”.

Conclusion:

The initiatives of emerging market nations, primarily those of China, express increasing impatience with the United States for blocking IMF reforms. Now Beijing is taking things into its own hands. It appears as though we are observing a big power struggle between China and the US, which is now no longer merely about influence in Asia, but globally.[14] Whether a sufficient renovation of the Western-dominated Bretton Woods Institutions succeeds, or whether the new institutions will become serious competition for the existing system, will be decided at the highest diplomatic levels. The main question is whether a multi-polar monetary architecture in the framework of competing institutions will be created, or whether a transition to one is only possible by means of fundamental reform of established structures (see also sections e, f).

e) Russland and China – gradual emancipation from the US dollar

“I believe in the Golden Rule – The Man with the Gold….Rules.”

Mr. T

For years, Vladimir Putin was known as a supporter of the euro. In 2010, he even mooted a currency union between the EU and Russia. This would have transformed the euro into a de facto petro-currency and would have put it on an equal footing with the US dollar.[15] However, in the wake of the imposition of sanctions, Moscow is increasingly turning towards Asia. The sanctions could prove a boomerang, as it appears as though they have strengthened the Beijing-Moscow axis further.[16]

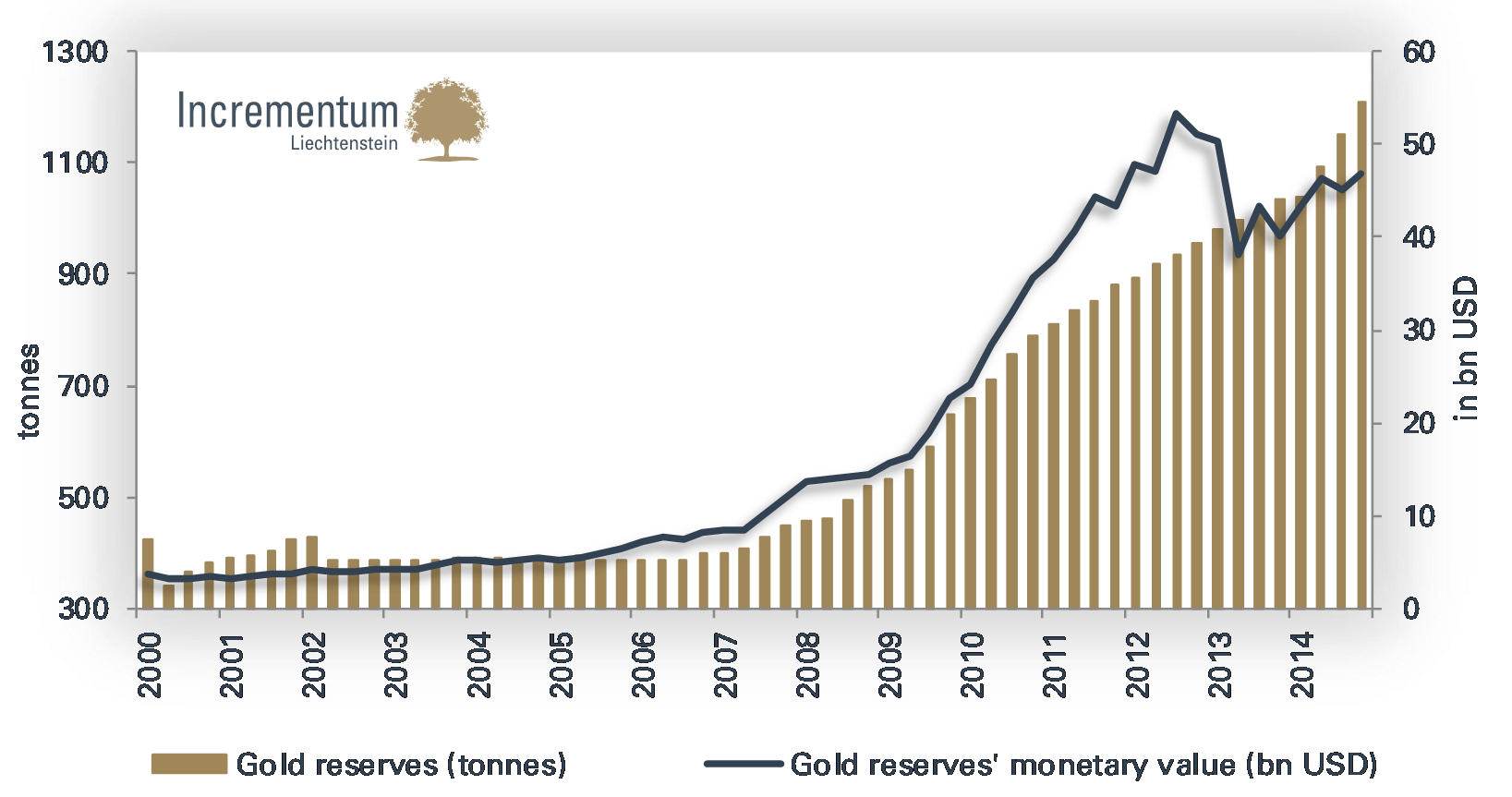

Gold is likely to play a very prominent role in this geopolitical power struggle. Russia has been gradually increasing its gold reserves for years. Since 2005 alone, its gold reserves have more than tripled, as a result of which Russia now holds the fifth largest (officially reported) gold reserves in the world, after the US, Germany, Italy and France. Since the beginning of the Ukraine conflict, Moscow has shifted into a higher gear and increased the momentum of gold purchases. These purchases are an unambiguous statement against the hegemony of the dollar, especially in combination with the fact that since January 2014, Russia has sold more than half of its US treasury holdings.

Russian gold reserves in tons (left scale) and value in USD bn (right scale)

Sources: World Gold Council, Incrementum AG

Does Moscow plan to introduce a gold-backed ruble? Economist Jude Wanninski had already recommended this in an attention-grabbing editorial in the Wall Street Journal back in 1998.[17] Only a gold-backed ruble would be able to lead Russia out of the debt crisis and provide the ruble with international acceptance. It appears as though Vladimir Putin has adopted this idea two decades later.[18]Putin’s quite pronounced aversion to the monopoly of the dollar is summarized trenchantly in the following quote:

“The Americans are living well beyond their means and are shifting a part of the weight of their problems to the global economy. They are living like parasites off the global economy and their monopoly of the dollar. If there is a systemic malfunction in the US, this will affect everyone. Countries like Russia and China hold a significant part of their reserves in US securities. There should be other reserve currencies.“[19]

However, critique of the dollar’s dominance is also becoming more widespread and frequent on the part of high-ranking institutions. Justin Yifu Lin, the former chief economist of the World Bank, proposed replacing the US dollar with a single global currency: “The dominance of the greenback is the root cause of global financial and economic crises. The solution to this is to replace the national currency with a global currency.“[20]

The fact that emancipation from the dollar is gaining momentum is confirmed by numerous other examples:

- At a conference in Krasnoyarsk in Siberia, Russia’s vice prime minister Dvorkovich remarked that Chinese companies would be permitted in the future to purchase stakes of more than 50% in state-owned Russian oil and gas fields. This would represent a milestone in the strategic economic partnership between these two nations. And the measure would not be limited to just the energy sector. Closer relations are also planned in other key sectors, such as the financial and the defense industries.

- The gas delivery agreement struck between Russia and China last year is a turning point in the strategic energy cooperation between the two countries. The exact size of the transaction is not yet known, some have reported up to USD 500bn. For the time being, payments will be made in USD. However, the contracts can be changed into yuan or ruble-based contracts at any time, upon which the US dollar would no longer be needed. Apart from this deal, 48 additional economic agreements were signed. The volume of trade between the two countries is set to double over the coming five years to an annual USD 200bn.

- The “China International Payment System” (CIPS) is designed to increase the renminbi’s importance in cross-border trade and associated international payment transactions. Russia is working on an alternative to SWIFT, after the British government threatened Russia with an exclusion from the financial messaging system.

- Russia and China have opened a USD 25bn (equivalent) currency swap line. Currently, some 75% of all trade between Russia and China is settled in US dollars. As a result of this agreement, the dollar can be circumvented from now on.[21]

- China has entered into a comprehensive foreign exchange htit.php&job_id=102agreement with Canada, traditionally one of the US’s closest allies. A further agreement was also struck with the ECB, in this case over EUR 50bn. Additional agreements were signed with Switzerland, Malaysia, Argentina, Ukraine and New Zealand. Companies in those countries can thus now completely circumvent the US dollar in trade and foreign exchange transactions.

- The liberalization of China’s bond market is moving forward rapidly. More than 20 foreign financial institutions have so far received licenses allowing them to enter China’s bond market. Currently the bond market has a volume of nearly USD 6 trillion, and thus appears to be – after the US and Japan – the third largest bond market in the world.[22] More than 50 central banks are by now holding RMB bonds as part of their foreign exchange reserves.

- London, Paris as well as Frankfurt harbor ambitions to establish themselves as the main trading hub for European renminbi trading. In London, the first RMB denominated bonds have been issued, which are held as a reserve by the Bank of England.

Conclusion:

We are currently in a transition period to a multi-polar currency system. The period of dollar dominance appears to be slowly but surely coming to an end. In the wake of Russia and China significantly strengthening their strategic alliance in recent months, it appears as though Western sanctions have heralded a new round in the struggle over the global monetary architecture.

f) Special drawing rights: monetary LSD as the currency of the future?

One possibility to postpone national currency problems is to move them to an international level. The next step in the monetary system’s road to perdition could be provided by special drawing rights[23], which former French president Valéry Giscard d’Estaing once referred to as “monetary LSD”.

Since the balance sheets of Western central banks have been strongly expanded already in the course of the 2008/09 crisis, our advisory board member Jim Rickards sees only limited possibilities for additional monetary rescue operations, without risking a fatal loss of confidence in paper currencies. According to Rickards, the next higher authority, i.e., the IMF, will therefore have to step into the breach in order to re-inflate the system:

“But the problem is, the Fed printed trillions of dollars without a liquidity crisis. What is going to happen when we do have a liquidity crisis, which I expect in the next couple of years, when there is a 2008-style panic starting again? What are they going to do? Print $6 trillion? $9 trillion? There is a limit to what they can do. And so at some point, it is going to get handed over to the IMF, and they are going to have to print SDRs (special drawing rights.“[24]

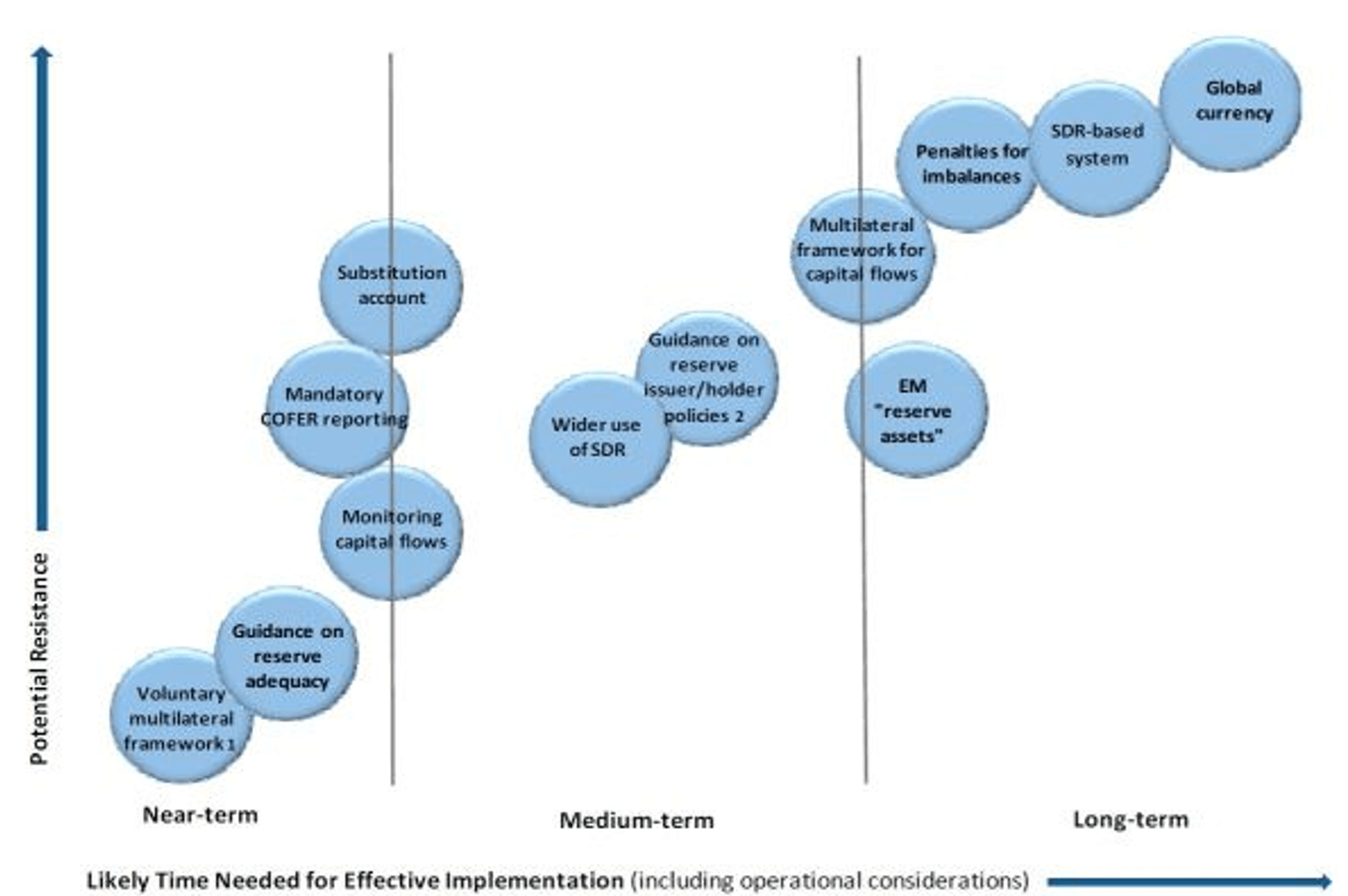

The IMF itself makes no bones about its ambition to establish special drawing rights as a global reserve currency. The following multi-step plan to position SDRs as a global reserve currency was presented in a study[25].

Step by step plan to transform SDRs into a “reserve currency”

Sources: IWF, Reserve Accumulation and International Monetary Stability

As they are currently constituted, special drawing rights are a pure fiat money; this is to say they are neither covered, nor redeemable. More and more often it is stated that a “grounding” with metals or even agricultural commodities should be introduced in order to create confidence in special drawing rights. From our perspective this makes little sense, while Jim Rickards refers to the idea of “paper gold” as “the greatest oxymoron of all times“.[26]

Nevertheless, such proposals, which are harking back to the origin of SDRs[27],find ever more prominent supporters. Meghnad Desai, chairman of the influential OMFIF council, recently pleaded publicly for the inclusion of gold in SDRs: “By moving counter-cyclically to the dollar, gold could improve the stabilizing properties of the SDR. Particularly if the threats to the dollar and the euro worsen, a large SDR issue improved by some gold content and the R-currencies may be urgently required.”[28]

China and the SDR

2015 could become the year that efforts to internationalize the Chinese renminbi are given direction: In October, the IMF will decide on altering the composition of special drawing rights, and it appears as though the Chinese currency has good cards. So far, only the US dollar (41.9%), the euro (37.4%), the British pound (11.3%) and the Japanese yen (9.4%) make up the currency basket.

Should the RMB become part of special drawing rights, this would on the one hand have symbolic, but on the other hand also real economic consequences. With the admission of the renminbi to the elite circle of currencies contained in the SDR, the IMF would acknowledge the ascendency of the second largest economy and concurrently decrease the dollar’s dominance. The classification as a reserve currency would make the yuan suddenly a lot more attractive for the central banks of emerging countries, which want to diversify their foreign exchange reserves away from the US dollar.

The conditions set by the IMF in 2010, especially with regard to the renminbi’s tradability, have largely been fulfilled. Capital movement regulations were changed, and access to China’s bond market has been eased for foreign investors. The classification as an “important export currency” has already been attained, as the share of China’s trade volume settled in yuan now stands at 20%. In the meantime, the RMB is the fifth-most traded currency in the world. From a purely formal perspective, Beijing appears to have done its homework, which is why IMF chief Lagarde already indicated that the admission of the renminbi was no longer a question of “if”, but of “when”.[29]

China has expressed interest in special drawing rights since the 1970s already.[30] Recently, its wishes have been expressed ever more strongly, e.g. by People’s Bank of China governor Zhou Xiaochuan. He demanded that the dollar should be replaced as the global reserve currency by SDRs:

“… the role of the SDR has not been put into full play due to limitations on its allocation and the scope of its uses. However, it serves as the light in the tunnel for the reform of the international monetary system…The basket of currencies forming the basis for SDR valuation should be expanded to include currencies of all major economies, and the GDP may also be included as a weight. The allocation of the SDR can be shifted from a purely calculation-based system to a system backed by real assets, such as a reserve pool, to further boost market confidence in its value.”[31]

We regard this largely as posturing. We assume that China doesn’t want to destroy the IMF and the dominant Western institutions, but that at the end of the day, it wants to become a member of the “big boys’ club”, as Jim Rickards has put it.[32] China’s leadership knows that the yuan is far from ready to overtake the dollar, despite the rapid progress of its efforts at internationalization.

Conclusion:

The admission of the renminbi into the SDR basket appears to be a purely political issue. The US have a veto and can block its admission. As a result, China will have to be flexible and offer some kind of quid pro quo. We believe that the US would only agree to the admission of the RMB into the SDR basket if it becomes fully convertible. Including it in the SDR currency basket would in our opinion make little sense unless the RMB’s managed peg to the dollar were removed. If it was to remain pegged to the USD, there would seem to be little point in including it, aside from the potential symbolic effect.

Last year, we already wrote the following regarding the future of special drawing rights: The next big crisis will lead to a reorientation of the international monetary architecture. Most proposals regarding an intensified use of special drawing rights appear to make little sense from an “Austrian” perspective, as a global institutionalized fiat money cannot circumvent the true problems inherent in the debt based monetary system. With prophetic foresight, Ludwig von Mises warned against a further centralization of the central banking system in 1912: “Once common principles for their circulation-credit policy are agreed to by the different credit-issuing banks, or once the multiplicity of credit issuing banks is replaced by a single World Bank, there will no longer be any limit to the issue of fiduciary media.“[33]

g) Gold-backed digital currencies

In the course of a competitive discovery process, people should be given the opportunity to learn which type of money is most sensible for them based on their individual situation and needs. Since obviously no one will want to use unsound money, healthy competitive pressure would incentivize both private and government money producers to issue money of better quality.[34]

To what extent precious metals-backed currencies would dominate in a free market monetary order is difficult to tell ex ante. However, a glance at monetary history suggests that humanity has always harbored a natural preference for gold and silver.

In the wake of Bitcoin, more and more new digital and crypto-currencies are being created. According to the web site mapsofcoins.com, more than 800 crypto-currencies based on Bitcoin’s technology currently exist – and the trend continues.[35] On the crypto-platform coinmarketcap.com, a total of 563 electronic currencies are listed. The sector has attained a market capitalization of USD 3.7bn, albeit the lion’s share thereof is attributable to Bitcoin (approx. USD 3.3 bn.).[36]

The rapid development phase, the ups and downs of individual digital currencies (esp. Bitcoin) and the competition over the possible money of the future of course does not steer clear of gold. Thus a new crypto-currency called HayekCoin was presented in the US only a short while ago.[37]

Named after Austrian Economic Nobel Prize winner Friedrich August von Hayek, it represents a gold-backed digital currency, with every virtual coin backed by one gram of physical gold. Physical gold can be transformed into the digital currency by paying it into an account. Thus every HayekCoin issued will not only be fully backed by gold, but will at all times exhibit the same value as one gram of gold.

This project and numerous other gold-covered crypto-currencies are an attempt to combine the advantages of a crypto-currency (easy and fast transfer over large distances, low transaction costs) with the advantages of gold. By tying them to gold, these crypto-currencies are supposed to be less susceptible to the vagaries of the market, in contrast to Bitcoin, which has experienced quite a roller-coaster ride since its introduction.

Another important provider is BitGold. The official goal of the Canadian enterprise is “(…) to make gold accessible and useful for digital payments and stable savings.“[38] In order to make this possible, BitGold intends to become a platform that works similar to PayPal. In the future, virtual, gold-backed BitGold is intended to be transferable via e-mail or smart phone to any desired recipient.

The payment network Ripple also appears to be developing well. Ripple is a digital standard for payments with which any currency can be traded. Thus, Ripple is similar to the e-mail standard for digital messages. Big names are among the investors in Ripple, such as Andreessen Horowitz, a venture capital firm with AUM of more than USD 2.7 bn., but also Google Ventures, Google’s internal venture capital company.[39] Two currency suppliers in the system have already switched their trading to gold.[40]

Conclusion:

A lot seems to be happening in the currency markets at the moment. Whether the highly innovative companies will ultimately be successful remains to be seen. They will first have to prove that they can overcome the difficult legacy of eGold, which hangs like the sword of Damocles over the entire sector of gold-backed digital currencies.

In principle, framework conditions are currently significantly better than they were just a few years ago. If new providers of gold-backed digital currencies can overcome the problems and the wind isn’t taken out of their sails politically, they could well be looking forward to a “golden future” – almost literally. However, until then, numerous obstacles will still have to be overcome.

[1] From the book: “Kredit verspielt – Warum Sie über (Ihr) Geld nachzudenken sollten, bevor es andere tun”, www.kredit-verspielt.de, Markus Weis (“Credit Lost – Why You Should Think About (Your) Money, Before Others Are Doing So”)

[2] The entire work “System der politischen Ökonomie“ (“System of Political Economy”) can be found here: http://www.vergessene-buecher.de/uebersicht.html#anfang

[3] https://en.wikipedia.org/wiki/Bretton_Woods_system

[4] Note: the sum of daily foreign exchange transactions sums up to 200%, as both currencies of each currency pair are counted. See: https://en.wikipedia.org/wiki/Foreign_exchange_market

[5] See: „China spaltet den Westen – und bringt die Finanzarchitektur ins Wanken“, Manager-Magazin.de („China splits the West – and shakes the financial architecture“)

[6] See: „Schulden ohne Sühne?”, Kai A. Konrad, Holger Zschäpitz (“Debts without punishment?”)

[7] The Bundesbank justified this by the signal effect during a time of crisis and with the complex logistics of providing security during transport and the creation of storage capacity.

[8] See: „Nationalbank denkt über Goldkonzept nach“, Der Standard (“National Bank thinks about gold concept”)

[9] See: „Bestätigt: Österreich holt 110 Tonnen Gold heim“, jilnik.com („Confirmed: Austria brings back 110 tons of gold“

[10] See: „Holt unser Gold heim – der Kampf um das deutsche Staatsgold“, Peter Boehringer

[11] See: „China Creates Gold Investment Fund For Central Banks“, Goldcore.com

[12] Although China is by now the by far largest economic power in Asia, the Asia Development Bank continues to be controlled by Japan. Thus Japan has twice as many votes in the ADB, and moreover the ADB’s president always comes from Japan.

[13] Shanghai Cooperation Organization

[14] „Amerika verliert Machtkampf mit China“, FAZ (“America loses power struggle with China”)

[15] See: „Chinas langer Währungsmarsch”, Nikolaus Jilch, Die Presse (‘China’s long currency march’)

[16] The participation of official representatives from China in the Victory Parade in Moscow, a giant military parade celebrating the victory over Nazi Germany, was hugely symbolic in our opinion. In the West the participation was barely noticed.

[17] See: “Fixing Russia with Gold”, Jude Wanniski

[18] See: “As the Sanctions War Heats Up, Will Putin Play His Gold Card?”, John Butler

[19] See: “Putin says U.S. is “parasite” on global economy”, Reuters

[20] See: „Replace dollar with super currency: economist”, China Daily USA

[21] See: “China prepares to bailout Russia“, Zerohedge.com

[22] See: „China widens foreign access to domestic bond market“, Financial Times, 4. Mai 2015

[23] The sesquipedalian term special drawing rights (SDR) designates an artificial currency unit introduced by the IMF that isn’t traded on foreign exchange markets. For a detailed analysis see also “In Gold We Trust 2014”.

[24] See: Jim Rickards, interview with Peak Prosperity, Sept. 21 2013

[25] “Enhancing International Monetary Stability – A role for the SDR?”, IMF, 2011

[26]See also our book “Oesterreichische Schule fuer Anleger”, p. 164-168, Taghizadegan, Stoeferle, Valek (an English version will become available later this year)

[27]Originally the value of an SDR was defined as 0.888671 grams of gold. Only after the breakdown of the Bretton Woods system was the SDR currency basket newly defined.

[28] See: “Emsiger WGC: Treffen am Rande von Weltbank und IWF” (“Busy WGC: Meeting on the sidelines of World Bank and IMF”) Foonds.com

[29] See: “IMF’s Lagarde says inclusion of China’s yuan in SDR basket a question of when”, Reuters

[30] See: “Wikileaks 1976: PBoC Focuses on Gold and SDRs”, Koos Jansen, Bullionstar Blog

[31] See: “Zhou Xiaochuan’s Statement on Reforming the International Monetary System”, cfr.org

[32] See: “China and the Gold Bugs”, Jim Rickards, www.acting-man.com

[33] See: “The Theory of Money and Credit”, Ludwig von Mises

[34] See: “Währungswettbewerb als Evolutionsverfahren”, Liberales Institut, Frank Schäffler und Norbert F. Tofall („Currency Competition as an Evolutionary Process“)

[35] http://mapofcoins.com/

[36] https://coinmarketcap.com/

[37] „Anthem Vault Joins Freedom Fest 2015: Featuring ‘The Hayek’”, AnthemVault News

[38] https://www.bitgold.com/about-bitgold

[39] https://www.ripplelabs.com/investors/

[40] Gold Bullion International as well as Ripple Singapore