When the first In Gold We Trust report was published in 2007, gold was far from a mainstream investment. Institutional interest was limited, gold allocations were marginal, and confidence in fiat currencies, while already eroding, had not yet reached crisis levels.

What began as a relatively compact analysis nevertheless laid the foundation for what would become one of the most widely read and cited annual gold reports worldwide. Looking back, the clarity of thought and the conviction displayed in that very first edition stand out.

As we highlighted in the 2025 edition of the In Gold We Trust, the year 2007 falls squarely into the second half of the 2000s secular gold bull market. This was a period we later dubbed Golden Decade, the second of its kind.

While gold had already bottomed out in 2001, it was during the mid-to-late 2000s that the price action began to accelerate meaningfully. By 2007, the bull market was no longer a hypothesis. Unquestionably, it had become evident.

This acceleration would ultimately culminate in the 2011 peak, though not without interruptions, corrections, and the defining stress test of the 2008 Global Financial Crisis.

One of the most important insights of the 2007 report was its emphasis on gold’s dual nature.

In essence, gold is not merely another commodity subject to industrial supply and demand dynamics. Due to being durable, liquid, indestructible, and globally trusted, gold is thereby a monetary asset.

This distinction proved crucial. Fundamentally, it allowed the report to frame gold not just as a cyclical trade, but as monetary insurance in a world of growing imbalances, rising debt, and declining confidence in fiat systems.

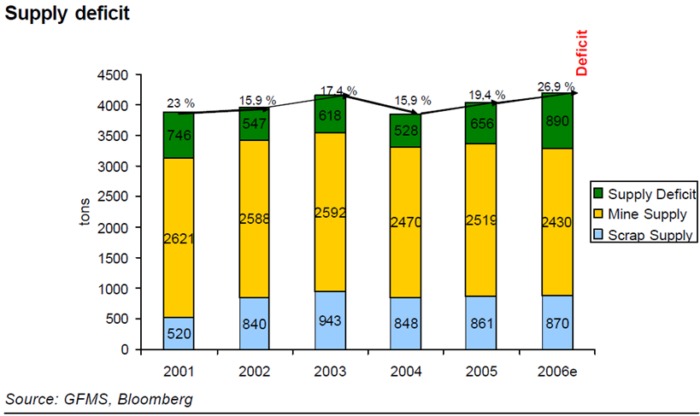

The debut edition also sounded an early warning on gold supply. Low gold prices throughout the 1990s had severely curtailed exploration and investment.

As a result, future mine supply was expected to stagnate at best. Moreover, rising energy and labor costs added further pressure.

The implication was straightforward: supply would struggle to respond quickly to rising demand. Naturally, this formed a structural setup that historically has led to higher prices.

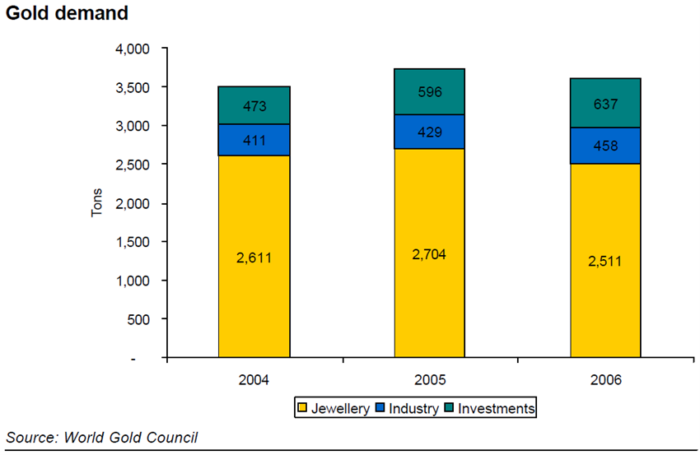

Even in 2007, global gold demand already exceeded annual mine production by a significant margin. The gap could only be bridged temporarily through recycling and central bank sales.

The report argued that such an imbalance was unsustainable over the long run unless prices adjusted upward. History would soon validate this assessment.

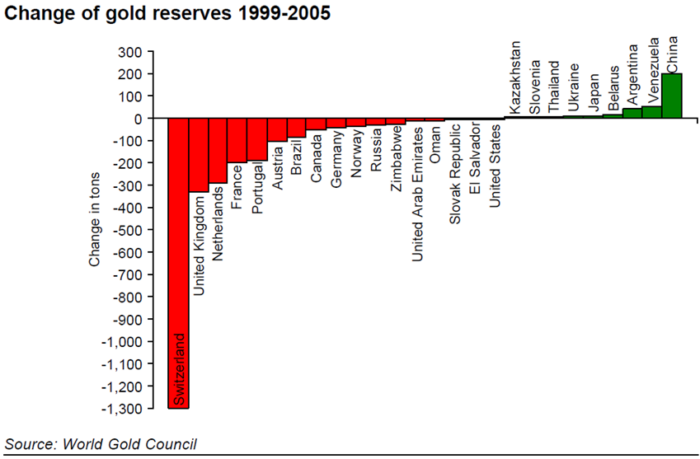

At the time, central banks were still net sellers of gold. However, the 2007 report anticipated a turning point.

Intuitively, it argued that large-scale official sales would eventually come to an end, and that central banks, particularly in emerging markets, would return as buyers. This shift, which later became one of the most powerful structural drivers of the gold market, was still far from consensus in 2007.

The debut report outlined initial price targets of USD 730 and, subsequently, a move above the prior all-time high of USD 875.

While these projections were viewed by some as overly optimistic at the time, reality soon overtook them. By late 2007 and early 2008, gold was already breaking new ground, setting the stage for what would become a multi-year rally.

The 2008 Global Financial Crisis introduced severe volatility across all asset classes, including gold. Temporary pullbacks tested investor conviction.

Be that as it may, gold proved resilient. What began as a mid-2000s bull market, ultimately extended well beyond the crisis, culminating in the historic highs of 2011.

With the benefit of hindsight, the 2007 In Gold We Trust report stands out for its prescience:

Structural supply constraints

Monetary and macroeconomic fragilities

The evolving role of gold as financial insurance

Clearly, many of the themes that still define today’s gold debate were already articulated in that very first edition.

From a modest debut in 2007 to a globally recognized annual publication, In Gold We Trust has now chronicled two decades of monetary evolution, market cycles, and shifting investor psychology.

The Golden Decade was only just beginning in 2007, and so was this journey.

For those interested in retracing the origins of the In Gold We Trust framework, we invite you to revisit the debut edition:

📘 Read the 2007 In Gold We Trust report: https://ingoldwetrust.report/reports-archive/in-gold-we-trust-report-2007/?lang=en

💛 Here’s to 20 years of analysis, and not forgetting the threads that connect them. Stay tuned for more.

#InGoldWeTrust #20Years20Threads #GoldSurge #GoldInvesting #PreciousMetals #Commodities #BullMarket #GoldenDecade #MacroTrends #InvestmentInsights #MarketAnalysis #MonetaryPolicy #SoundMoney #SafeHaven #InflationHedge #WealthPreservation #FinancialHistory #IGWT07