Gold as portfolio insurance

„It is a case of better having insurance and not needing it, than one day realizing that one needs it but doesn’t have it.“

Acting-man.com

As we have done in our previous studies[1], we want to analyze the advantages of gold in the context of portfolio diversification. Due to its unique characteristics, we are firmly convinced that gold – especially in the current environment – should be seen as an important portfolio component.

We believe that gold is not a replacement for investment in traditional securities such as stocks or bonds in a fiat money system, but is rather complementary to them. The correct way to look at a gold position in the framework of an investment portfolio is to regard it as a liquid, alternative cash position, which exhibits exchange rate risk relative to fiat money and possesses remarkable diversification characteristics. Numerous studies show that the addition of gold lowers a portfolio’s volatility and therefore improves statistical portfolio characteristics. The reason for this is that gold’s correlation with other asset classes is only 0.1 on average.[2]

In the following we want to discuss the so-called Permanent Portfolio, which represents an investment concept that can close a gap in conservative investment strategies in times of interest-free risk, as it tends to generate stable real returns. Gold plays a prominent role in this portfolio.

In addition, we want to examine gold in light of a desirable characteristic, which Nassim Taleb has made the world aware of: namely, anti-fragility. Does gold actually have this characteristic? Is it possible to construct an anti-fragile portfolio with the help of gold?

Lastly we will also look at gold’s opportunity costs, specifically with respect to real interest rates and the performance of equities.

a. A solution to the dilemma faced by investors: the Permanent Portfolio

“The portfolio’s safety is assured by the contrasting qualities of the four investments – which ensure that any event that damages one investment should be good for one or more of the others. And no investment, even at its worst, can devastate the portfolio — no matter what surprises lurk around the corner — because no investment has more than 25% of your capital.”

Harry Browne

After years of disinflation in consumer prices, most asset managers have significantly underweighted inflation-sensitive assets such as gold, commodities and mining stocks. In recent decades the credit and money supply expansion associated with the downtrend in interest rates has primarily affected asset prices. As discussed above, central banks continue to attempt to generate price inflation by any means necessary. Sooner or later, these reflation efforts are bound to succeed and asset price inflation will spill over into consumer price inflation. Since consumer price inflation cannot be fine-tuned at will by central banks (as inter alia their failure to achieve their inflation targets in recent years demonstrates), an extended price inflation cycle could be in the offing.

What to do though? Many investment strategies that have worked well in recent decades appear ill-equipped for an increasingly unstable and possibly even stagflationary environment. Flooding markets with fresh money leads to new “water levels” being established, in which former safe haven assets might well drown one day. A paradigm change is therefore needed for conservative investment strategies in order to attain the following goals:

- the chance to achieve capital gains with moderate risk

- generation of real returns

- avoidance of large drawdowns

Below we want to present a tried and tested concept that makes it possible to achieve attractive long-term returns independent of the market environment, while averting large drawdowns: the Permanent Portfolio. The strategy was developed in the early 1970s by US investment analyst Harry Browne, who was also strongly influenced by the Austrian School.

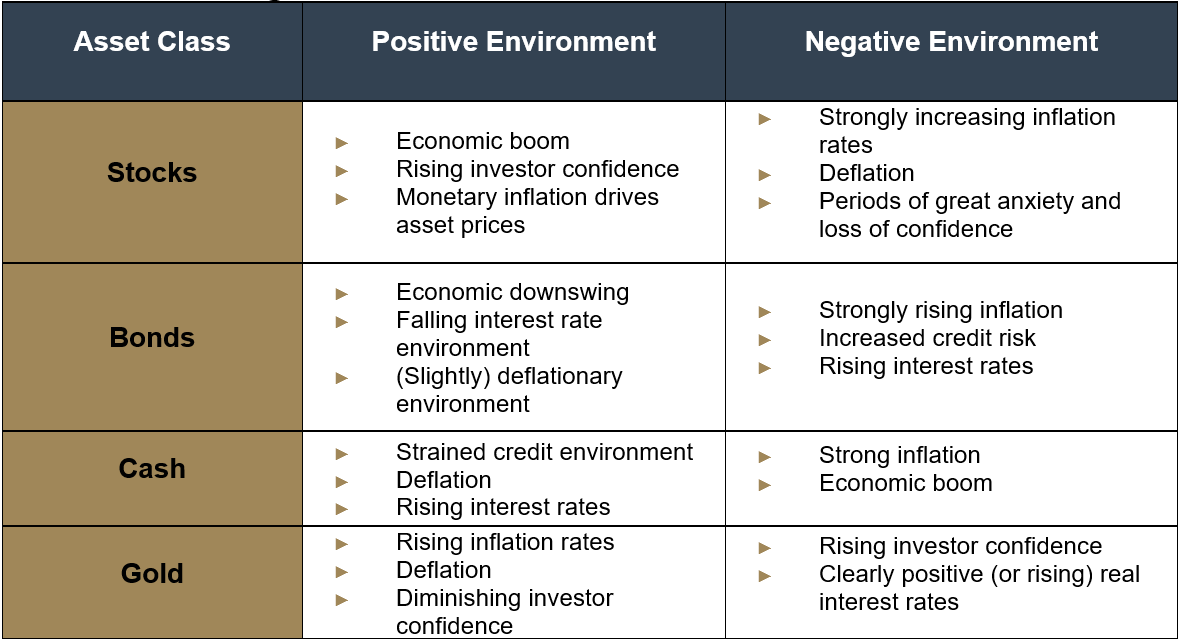

The basic idea is to construct a diversified portfolio that is invested in four different asset classes in equal parts. These tend to correlate negatively with each other in different economic scenarios, which reduces volatility and makes it possible to generate stable long-term returns. Shares of 25% each of the portfolio are allocated to gold, cash, stocks and bonds.

The four different economic scenarios which this method intends to provide for are:

- Inflationary growth (favorable for stocks and gold)

- Disinflationary growth (favorable for stocks and bonds)

- Deflationary stagnation (favorable for cash and bonds)

- Inflationary stagnation (favorable for gold)

The following table shows in greater detail which economic environments affect the asset classes under consideration in a positive or negative manner.

Source: Incrementum AG

The basic principle of the Permanent Portfolio approach is the humble – and very “Austrian” – insight that the future cannot be known. Investors should therefore diversify their capital in such a manner that they are equally well prepared for every possible economic environment (economic prosperity, recession, inflation, deflation).

The combination of the four components of the Permanent Portfolio not only generates stable long term returns. By making investors independent of forecasts, it also frees them of the prevailing “spiral of short-termism”. The latter refers to the pressure put on professional investors, who as a rule act as agents managing other people’s capital, to regularly report on their performance and have it measured against a benchmark. Reporting structures far too often tempt investors to simply join bandwagons in the markets in order to be able to consistently generate acceptable results relative to a benchmark, although plenty of evidence suggests that this is detrimental to long-term performance.[3]

By contrast, the Permanent Portfolio is constructed in a way that allows one to escape the pressures of the modern financial world to some extent. This is due to the strategy’s requirement that the portfolio must be regularly rebalanced in order to maintain the 25% allocation for each investment class, as the relative weighting of the components will over time shift due to differences in their performance. As soon as an asset class represents a weighting of more than 35% or less than 15% of the portfolio, it is rebalanced to the 25% level. Specifically, a component representing 35% of the portfolio would be reduced until its weighting is back at 25%, and a component representing less than 15% would be built up again toward the 25% threshold. The regular rebalancing of the portfolio ensures that one becomes immunized to a large extent against the influence of short-term fluctuations as well as the hysterical reactions of other market participants and the media.

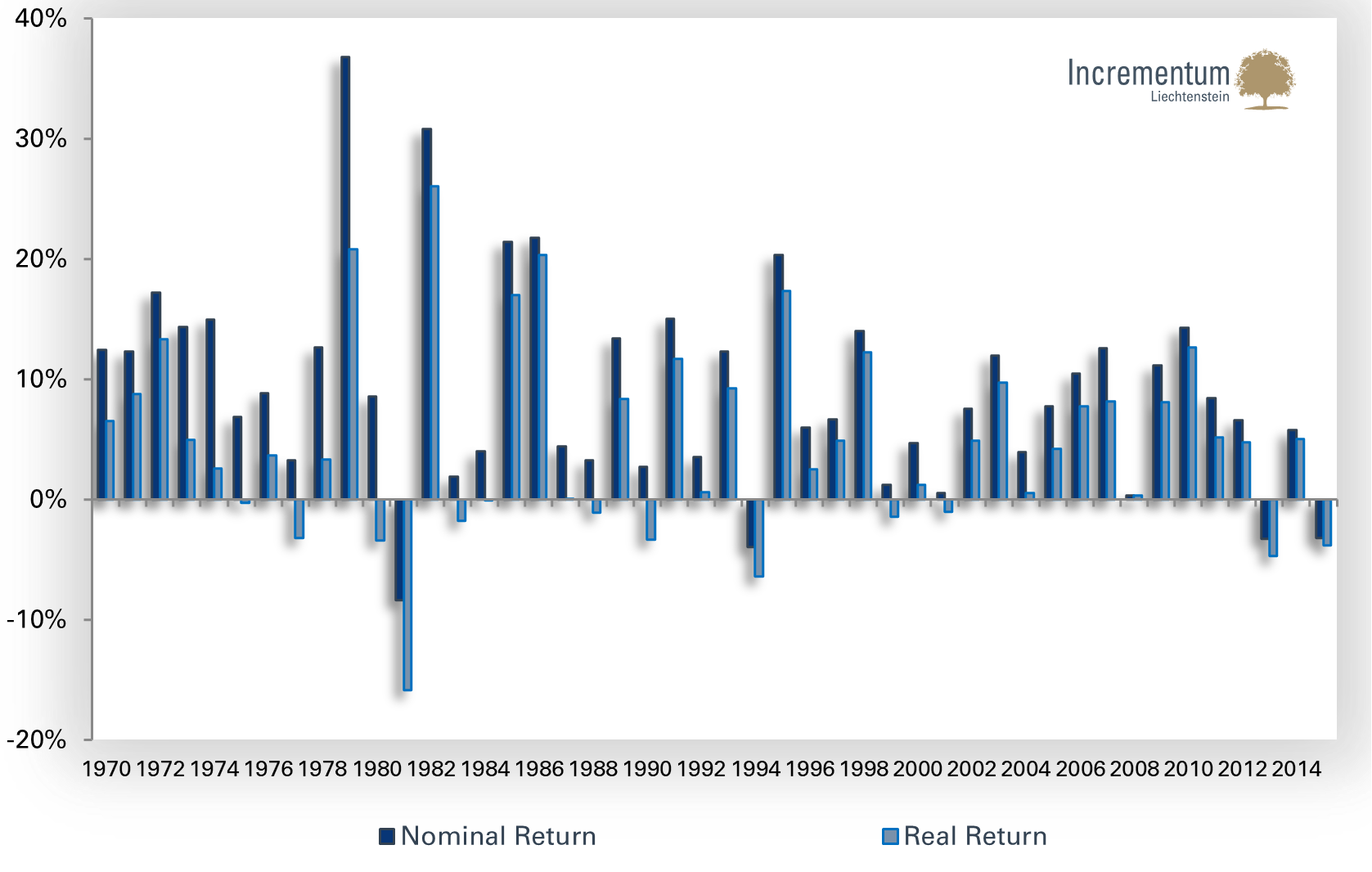

The strategy is well aligned with the anti-cyclical approach of Austrian Investing, whereas most market participants tend to buy when prices are rising and sell when they are falling.[4] The relatively rare rebalancing is moreover based on the philosophy that maintaining the portfolio should involve as little cost and effort as possible. There is no need to make specific timing decisions, and transaction costs, which are normally a significant drag on returns, are kept in check as well due to the low transaction frequency. The following chart shows the nominal and real returns achieved by the Permanent Portfolio from 1970 to 2015.

Annual performance of the Permanent Portfolio, 1970 – 2015, nominal and real return

Source: irrationalexuberance.com, Federal Reserve St.Louis; Incrementum AG

A close look reveals three characteristics that are particularly conspicuous:[5]

- The portfolio has generated respectable nominal returns. The average return of 9.1% per year is equivalent to that of investment portfolios which, as a rule, exhibit far greater volatility. As a matter of fact, the return is nearly identical to the 9.8% achieved by portfolios that are to 100% invested in equities – which achieve this return at the cost of far greater volatility.

- The portfolio has suffered no significant drawdowns. The number of losing years is small. In addition, the losses posted in those years have been small. In its worst year (1981) the portfolio posted a nominal loss of 8.3%. In comparison to pure equity portfolios this is a quite moderate loss. Moreover, the loss was more than compensated for by the gain recorded in the subsequent year.

- A positive real return has been achieved in most years within the time period under consideration. (Inflation-adjusted returns are extremely important in assessing and comparing investment strategies, a fact that is often overlooked.)

Conclusion:

In times when safe core investments are hard to find, the Permanent Portfolio stands out as a robust concept: It generates stable real returns in the long term without the risk of large drawdowns. Precisely because its individual components are fragile, the Permanent Portfolio is elastic and able to remain safely above the waterline in every market environment. A few months ago Incrementum launched the first European fund that invests according to the principles of the Permanent Portfolio. In the US, funds that implement the strategy very successfully have already been active since 1982.b. Anti-fragile investing with gold?

In 2012 Nassim Nicholas Taleb published “Antifragile: Things That Gain From Disorder”, a book in which he presents a kind of “theory of everything”. The German subtitle “Instruction manual for a world we don’t understand” is suggestive of the paradoxical Socratic motto “I know that I know nothing” – an insight in terms of which Taleb believes himself to be ahead of the crowd of top economists, central bankers, politicians and financial market actors who are obsessed with feasibility mania and blind faith in predictability.

However, Taleb wouldn’t be Taleb if he were humbly despairing in the face of this insight regarding his own ignorance; instead he wants to become a guru in how to best handle it. He shows how one can act successfully in light of this ignorance. To this end he has constructed a scheme that categorizes things either as “robust”, “fragile” or – and this is Taleb’s own ingredient – “anti-fragile”. It is clear what fragile and robust things are. The former break easily – they are vulnerable to exogenous shocks – while the latter are resilient and remain unchanged under the influence of different environments. Anti-fragility is a characteristic of things which benefit from volatility, randomness and certain kind of stresses.

Is gold anti-fragile?

The anti-fragility theory is of course very interesting for investors and particularly for short sellers – especially as Taleb has distinguished himself spectacularly in this special field. It seems natural to think of gold in this context: Gold is after all the classical crisis currency, which does well when all other asset prices are plummeting. Systemic stress – in the form of chaos, uncertainty, instability, unrest, volatility, etc. – is precisely the environment which gold needs to reach operating temperature. Is gold therefore an anti-fragile investment?

As obvious as this question seems to be, Taleb astonishingly avoids it completely in his book. At the Strategas Research Macro Conference in New York in March 2013 he was asked directly about gold and stated that he once believed in its ability to function as a portfolio stabilizer, but had come to change his opinion in the meantime: “It’s too neat a narrative, gold”.[6]Let us take this statement as the point of departure for a discussion of different aspects of gold:

Aspect 1: The value of gold rests on its “trust capital”

While Taleb’s statement indicates that this trust is partly blind faith, which mainly informs the attitude of slightly spaced-out gold aficionados and thus represents a shaky foundation, it should be noted that faith is a necessary precondition for every form of money. The value of “reputation money” even depends entirely on whether its users expect that it will be accepted by other users.

This not only applies to money though. In their book “Der fiktive Staat” (English: “The Fictional State”), Albrecht Korschorke and his colleagues argue that the entire State, and indeed every community and its institutions, are fictions. Nevertheless, they can be very real, stable and powerful entities:

“They are a complex of perceptions, which has functional character, as the entire reference frame of social addressing and authorization rests on it.” [7]

The authors analyze the meaning of narratives, which are fundamentally important for these institutions, as the trust of the reference group rests on them:

“Between the “soft” instruments of metaphors, narratives, and fictions on the one hand, and “hard” institutional arrangements on the other hand, exchanges in both directions are continually underway […] societal organization […] is metaphorical imagery that has attained functionality.” [8]

In short, gold’s narrative element, which Taleb takes exception to, is by no means a weakness. However, neither it is necessarily a strength, as narratives can lose their functional character or may not even be in possession of one in the first place. With respect to this first aspect, it remains however impossible to come to a firm conclusion on whether gold is fragile, robust or anti-fragile. A strong narrative is a precondition for trust and sound money. We therefore have to ask whether the narrative and the associated trust are strong. What is gold’s trust capital based on?

Aspect 2: In the past, gold was the most stable and enduring means of payment worldwide

The “narrative” of gold enthusiasts includes the statement that gold was universally accepted as a means of payment in the past and served as a safe haven currency in times of crisis. Speaking to Congress in 1999, even Alan Greenspan, who was chairman of the Fed in that time, remarked:

“Gold still represents the ultimate form of payment in the world. […] Fiat money, in extremis, is accepted by nobody. Gold is always accepted.” [9]

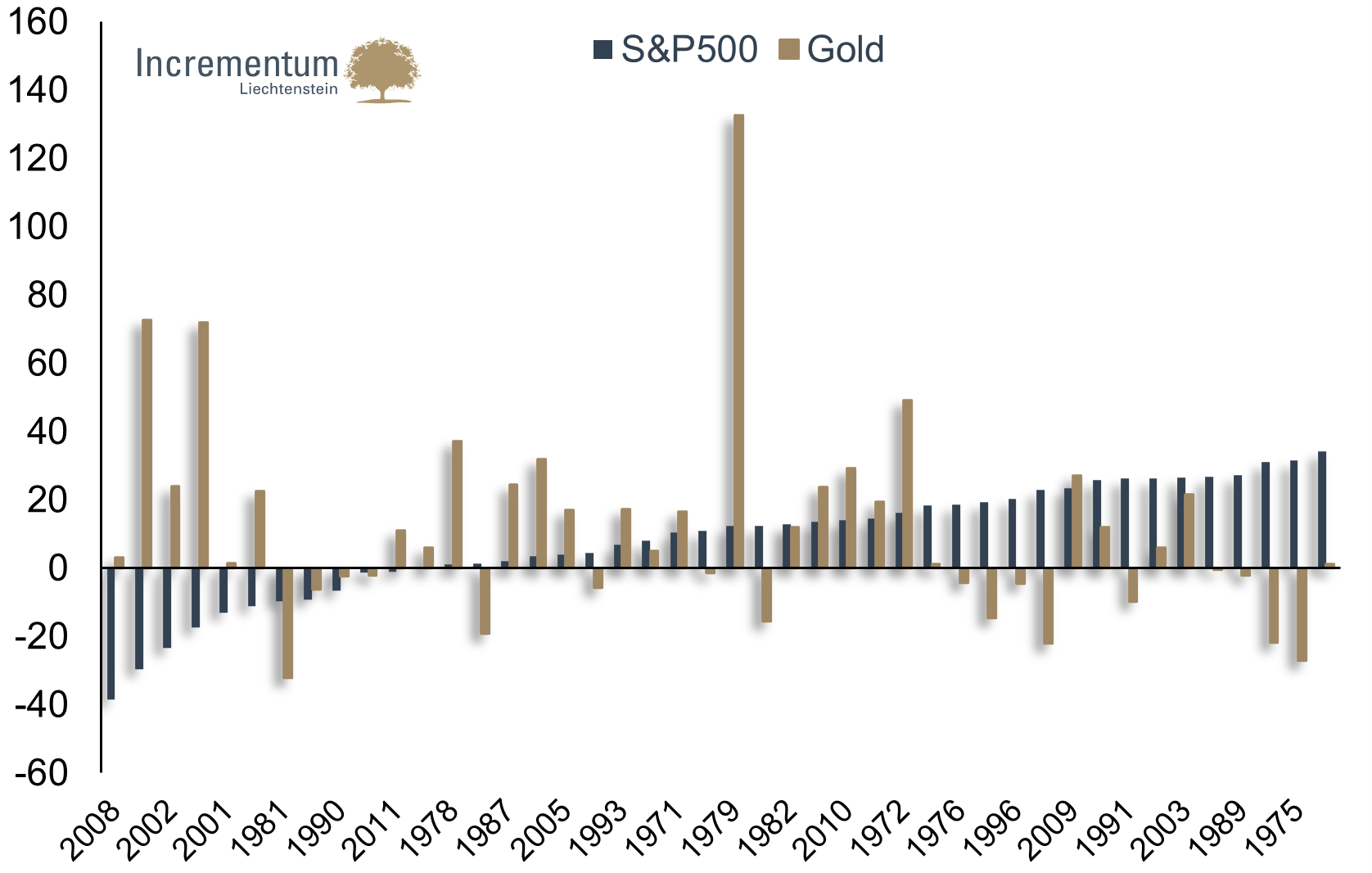

The following chart compares the annual performance data of gold and the S&P 500. An inverse relationship can be discerned. Moreover, in the six years in which the S&P’s biggest losses were recorded, gold posted not only an excellent performance in relative terms, but in absolute terms as well; bull markets in US stocks by contrast tended to weigh on gold’s price performance. However, it has to be pointed out that this inverse correlation is not perfect either: For instance, both gold and the S&P 500 Index rose between 2002 – 2007; occasionally there were also times when both declined concurrently. Gold recorded its biggest gain ever in 1979, a year in which the S&P 500 rose as well. The statement “Gold benefits from stress and suffers from stress withdrawal” is therefore not always applicable – thus gold cannot be a textbook example of anti-fragility. However, within the period under consideration, times of extreme stress (incl. “tail risk events”) were a sufficient condition for a rally in the gold price. This may be a hint that demand for gold becomes especially strong when the system is facing a fundamental threat – namely when doubts about the ability of counterparties to perform begin to arise.

Comparison of annual performance record, gold vs. S&P 500

Source: Federal Reserve St. Louis, Incrementum AG

However, Taleb would certainly not accept a mere reference to the past. Since the future is unpredictable, never before seen events could occur. So-called “black swans” can render forecasts which are based on historical patterns completely useless. However, one must also keep in mind that for the narrative of crisis-resistant gold, history is a factor that strengthens confidence in its monetary character. Empirically we can however conclude in connection with aspect 2: Gold is not a perfectly anti-fragile asset, but in severe times of crisis in the past, it has exhibited anti-fragile characteristics.

Aspect 3: Gold is intrinsically stable/ durable

Let us look at what the historical trust in gold is based on:

- Physical durability: Gold is resistant to air, humidity, most acids, caustic solutions, and solvents and as a result retains its physical attributes over time.

- Stable total stock: New gold can only be mined at great cost and effort and changes the size of the total stock only slightly, as gold isn’t used up and all the gold ever mined therefore remains available (high stock-to-flow ratio)

With respect to aspect 3 it can be stated: Gold is robust. The fact that gold is durable and stable creates trust. This trust has so far ensured that gold was always highly valued and accepted as a medium of exchange. Ultimately, this is precisely what is of greatest importance: namely, the value others attach to gold. It seems therefore appropriate to take a closer look at the gold demand as well.

Aspect 4: The valuation of gold is multi-dimensional and allows for price fluctuations

Industrial demand for gold barely plays a role, as a result of which price determination is mainly based on the metal’s monetary characteristics. In other words, gold is primarily money. However, as we have pointed out previously, the gold market is susceptible to manipulation as well.

The fact that central banks hold a large share of the global stock of gold as part of their strategic currency reserves, is on the one hand a positive signal for other gold holders: Even the upper echelons of the financial world have faith in gold as the ultimate insurance against risk (even if unofficially) and thus strengthen the narrative. On the other hand, this fact also politicizes the market to a notable extent. However, since central banks are holding gold as a strategic reserve inter alia in order to have greater negotiating power vis-à-vis other states in the event of a reorganization of the international monetary order, one shouldn’t expect them to undertake coordinated interventions in order to suppress the gold price in times of crisis. Moreover, central banks hold only around 30% of the total global stock of gold – the majority of gold holders comprises countless decentralized actors who are dispersed across the world.

In addition to this, speculation of course plays a role in the gold market as well. Gold serves as an inflation hedge or a safe haven currency, resp. is also amenable to technical analysis – the corresponding expectations and bets have an impact on the gold price as well. As a result, the gold market isn’t immune to exaggeration and the formation of bubbles. With the growing importance of automated trading systems, it should be expected that price spikes in both directions will become greater. An increase in short-term volatility seems inevitable in this context.

In summary one could state with respect to aspect 4 that the gold price tends to be fragile. It depends primarily on whether its “narrative” happens to be popular or not at a given time. After the Nixon shock the gold price rose by a factor of 50 until 2011, but lost 40% of its value again in the subsequent years. That’s quite degree of volatility. However, there exists a firm base of hardcore gold fans, resp. “people who understand gold”, who have faith in the narrative regardless of short-term fads, which tends to limit gold’s downside potential.

Aspect 5: Gold is liquid, even in stress situations

Gold is among the most liquid investment assets in the world. Its daily trading volume is only exceeded by that of three other currency pairs (USD/EUR, USD/JPY and USD/GBP). Due to its tight bid-ask spread, gold can be sold in stress situations without significant price discounts. In this respect gold is therefore robust.

Aspect 6: Gold is in a reciprocal relationship with the monetary system

Gold has neither maturity risk, nor commodity risk, and above all: Gold has no counterparty risk. The market in paper assets on the other hand is based on the promises of countless different counterparties. As long as confidence is high and the economy performs well, an asset without counterparty risk tends to be out of fashion; however, when concerns about potential defaults grow (deflationary environment), assets such as gold can rapidly regain importance. The attractiveness of gold is therefore an inverse function of the faith in the system.

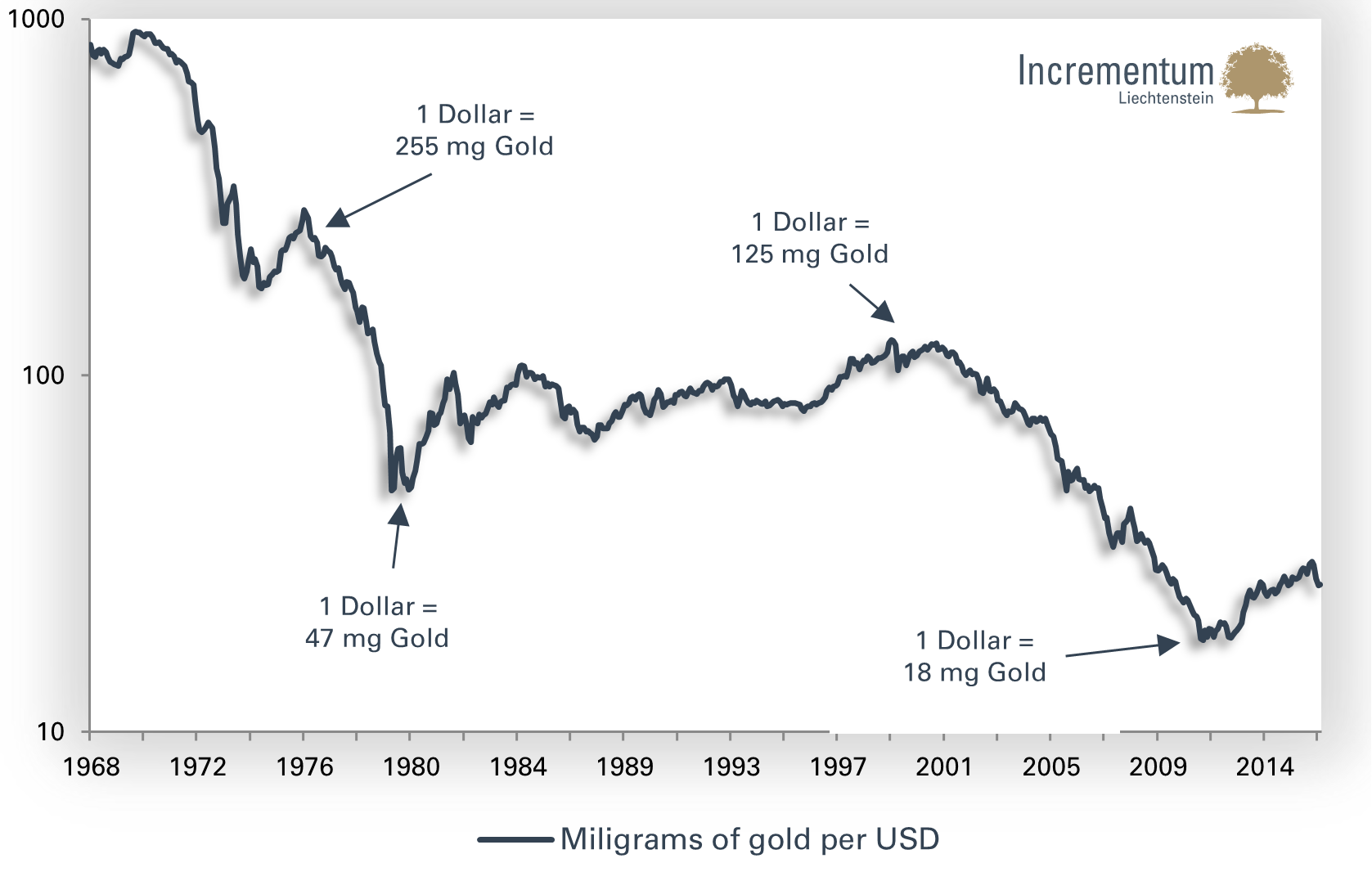

In this context it makes sense to look at gold as the measure of other things – after all, the global stock of gold has only grown by 1.5% annually over the past century, while the US dollar’s monetary base alone has been inflated by nearly 10% per year. We have frequently pointed out that over long time periods, the prices of numerous goods have barely changed relative to gold (resp. have even declined as a result of technological progress), whereas their dollar prices have vastly increased. The fluctuations of the monetary system also lead to fluctuations in the price of gold though, as it is measured in fiat currencies, primarily in terms of the US dollar. The next chart shows the exchange rate between gold and the US dollar inverted for a change: The US dollar has lost an enormous amount of value relative to the precious metal since 1971.

How many milligrams of gold can be purchased for one US dollar?

Source: Federal Reserve St. Louis, Incrementum AG

The “In Gold We Trust” report inter alia conveys the insight: The long-term trend in the gold price is not a gold story, but rather a story of the monetary system. The long-term uptrend in the gold price is the result of the system’s addiction to inflation. Moreover, periods during which the monetary system comes under pressure, lead to the gold price being pushed up. Periods during which the world seems to be doing fine – and these can last a long time – can result in gold and the associated narrative falling into oblivion. In short: With respect to aspect 6, gold is clearly anti-fragile.

Aspect 7: Black swans exist in gold’s universe as well, but we regard their destructive potential as limited

In order to assess the fragility or anti-fragility of an asset, Taleb recommends that one should ask what the largest possible loss could be, the so-called black swan. When securities markets are affected by black swan events, the environment tends to be especially beneficial for gold. However, are there also potential black swans for gold itself?

First, there is the threat of a gold ban, which we have devoted a separate chapter to. As we have pointed out, a comprehensive, effective gold ban appears highly unlikely, as controlling compliance would be ineffective, resp. too cost-intensive. Restrictions and taxation of gold trading, which would diminish the advantage of gold ownership considerably are however definitely possible.

Secondly, gold’s monopoly position in the area of alternative currencies could be challenged by emerging crypto-currencies, which are also regarded as a counter-concept to the current monetary system. Such competition for gold is a historical novelty. However, many crypto-currencies are gold-based as well; it appears highly unlikely that gold will be displaced by superior competition.

Thus, even in a worst case scenario, gold would continue to play a prominent role. Moreover, as Taleb remarks with respect to predictions: Things that have endured for a long time, in most cases tend to survive things which are newly emerging – the similarity between the future and the present tends to be far greater than one is inclined to assume. With respect to Aspect 7 we can therefore state that gold tends to be robust.

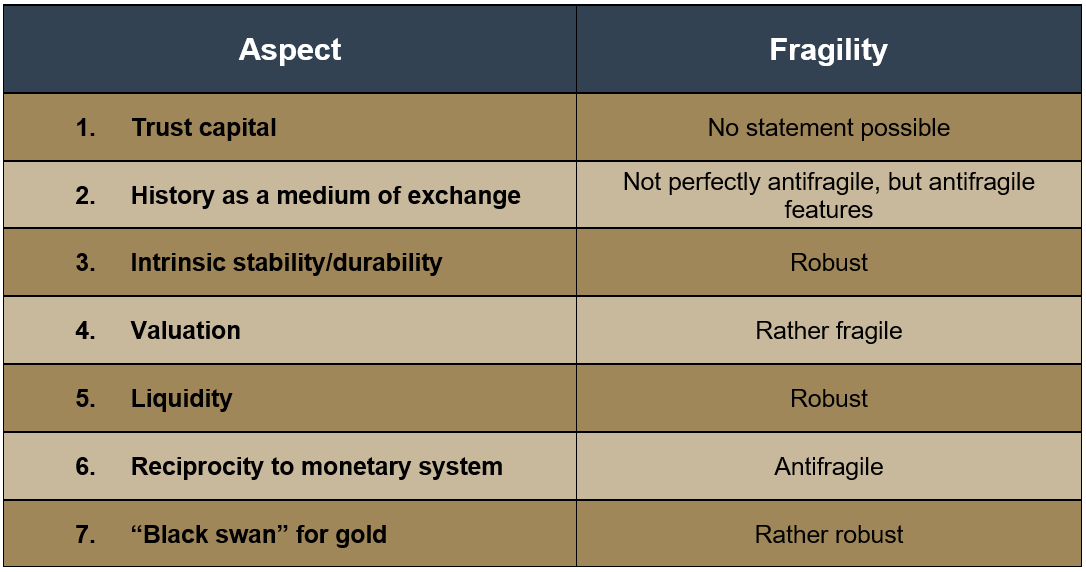

All in all, it can be said that the question whether gold is fragile, resp. anti-fragile is multi-dimensional. We have attempted to approach an answer and have addressed seven aspects of the precious metal, which are summarized in the following table:

Gold in the context of an anti-fragile portfolio

However, what is of greater interest to investors than the question of whether gold itself is anti-fragile, is whether it is possible to construct an anti-fragile portfolio with the help of gold. In answering this question, one has to take the fundamental principle of anti-fragile systems into account, which we have already discussed above – namely, that a number of elements within a system have to be fragile in order to render the system as a whole anti-fragile. In a portfolio context this means: An anti-fragile portfolio definitely has to contain individual components that are risky.

Taleb advises against constructing a portfolio solely out of components with medium risk. Instead he recommends a “barbell strategy”, i.e., a combination that consists of two sub-portfolios: an ultra-safe portfolio as well as a highly speculative portfolio, which contains extremely risky individual investments with an asymmetric risk/reward profile. We want to discuss gold in the context of these two sub-portfolios.

- Gold in the ultra-safe portfolio

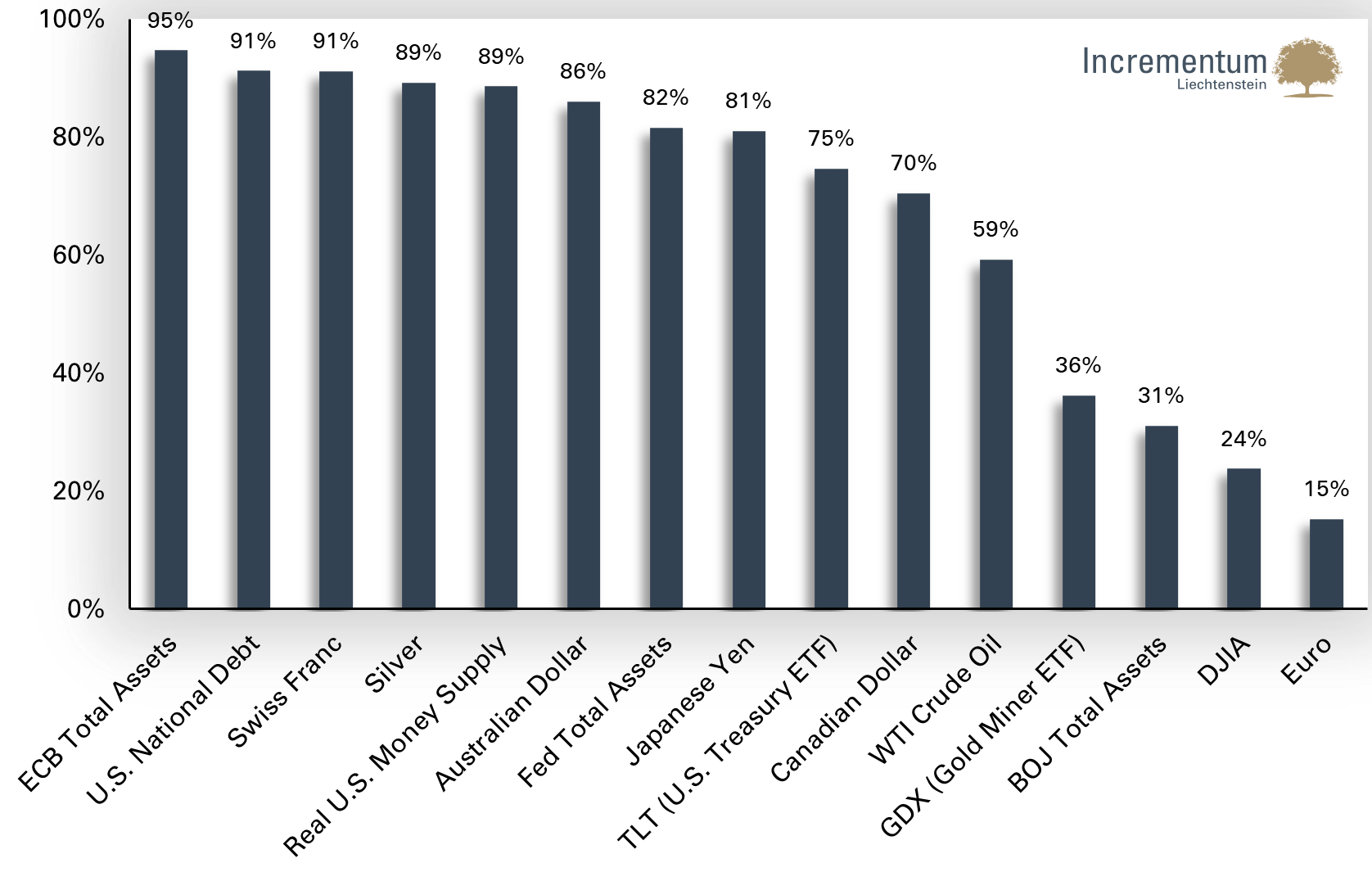

Numerous studies show that adding gold lowers the volatility of a portfolio and hence improves statistical portfolio characteristics. Since gold is barely, resp. even negatively correlated with most other asset classes as illustrated by the following chart, it can play an important role in portfolio diversification.

Long-Term Correlation Between Gold and Different Assets and Currencies

Source: National Inflation Association, Incrementum AG

We have discussed the Permanent Portfolio as an appropriately safe portfolio above. It is based on the principle of diversification, whereby four equal-weighted asset classes, which can experience strong volatility individually (and are therefore fragile), correlate negatively with each other and overall generate stable real returns without the risk of large drawdowns. Thus the Permanent Portfolio is not an anti-fragile, but a robust portfolio, and is therefore extremely suitable as a conservative core portfolio (resp. an ultra-safe sub-portfolio).

- Gold in the highly speculative sub-portfolio

The highly speculative sub-portfolio contains investment assets which can potentially generate very high returns, but are correspondingly risky. It is however important that the risk of loss is limited – therefore, investments with an asymmetric risk/reward profile such as options are suitable for inclusion. Gold itself can definitely play a role in such a portfolio as well, if it is actively managed and occasionally even leveraged.

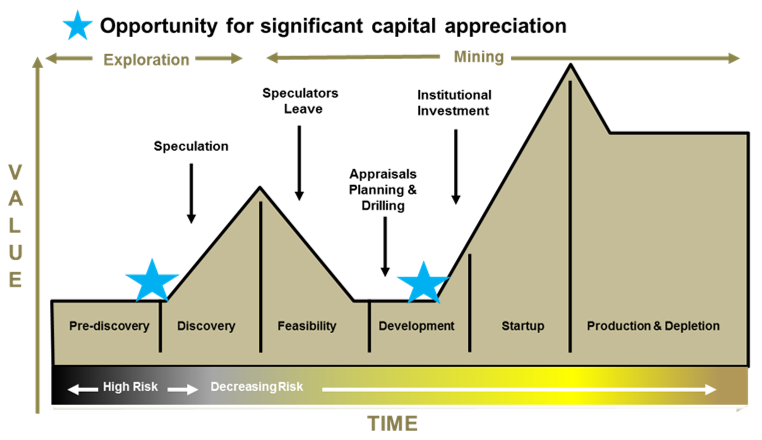

A clearly asymmetric risk/reward profile with option-like characteristics is inter alia provided by gold mining shares. The different characteristics and risk profiles of an investment in mining stocks are illustrated by the following chart. Funds investing in gold mining equities can occasionally be suitable for a highly speculative sub-portfolio as well.

Typical life cycle of a mining stock

Source: Brent Johnson, Santiago Capital

Conclusion

With anti-fragility Nassim Nicholas Taleb has presented an extremely interesting concept, which is quite useful for investors. Instead of performing necessarily incomplete and distorted calculations of specific risks and base portfolio allocations on those, he recommends constructing portfolios that are prepared for a variety of different scenarios. A number of scenarios would be devastating for fragile investments, while robust investments deliver stable returns regardless of the environment. An anti-fragile investment will post small losses in many scenarios, but benefits disproportionally in a stress scenario.

We have come to the conclusion that gold represents a multi-dimensional investment asset in this context. With respect to its physical durability, its high liquidity and its firm foundation of trust, it has to be assessed as robust. Worst-case scenarios in the form of a gold ban or competition from crypto-currencies would probably not have devastating effects. However, since the gold price can occasionally overheat, as well as decline strongly and remain at relatively low levels for extended time periods, gold is also fragile in this particular respect. With respect to gold’s most important characteristic as an asset that performs in a reciprocal manner relative to the monetary system, and its effectiveness as an inflation and crisis hedge, it is definitely anti-fragile though.

In a portfolio context gold can on the one hand provide stability, as it is an asset suitable for diversification purposes. If it is well managed it can generate returns in a speculative anti-fragile portfolio as well. This applies particularly to gold mining stocks, resp. gold mining funds.

c. The opportunity costs of gold

“’Time is Money’ is perhaps the simplest expression of the economic concept of opportunity cost: Forgoing one thing for something else. Interest rates represent nothing more than the “opportunity cost” of money, or of forgoing some amount of money today for the same at some future point in time. Assuming that cash in hand is normally used for consumption rather than savings, another way to look at interest rates is that they represent the opportunity cost of consumption today rather than at some point in the future: The higher the rate of interest, the higher the opportunity cost of consuming today, rather than tomorrow. This is the Iron Law of Money and Interest, available in all aspects.” [10]

John Butler

Opportunity costs are a crucial factor determining gold price trends. How great are the competing economic opportunities and risks which one has to accept if one decides to hold gold? Real interest rates, the growth of monetary aggregates, the volume and quality of outstanding debt, political risks, as well as the attractiveness of other asset classes (particularly equities) are in our opinion the most important factors affecting the trend in the gold price. Thus we want to focus on the most important opportunity costs impacting gold prices – particularly real interest rates and stock prices.

Real interest rates

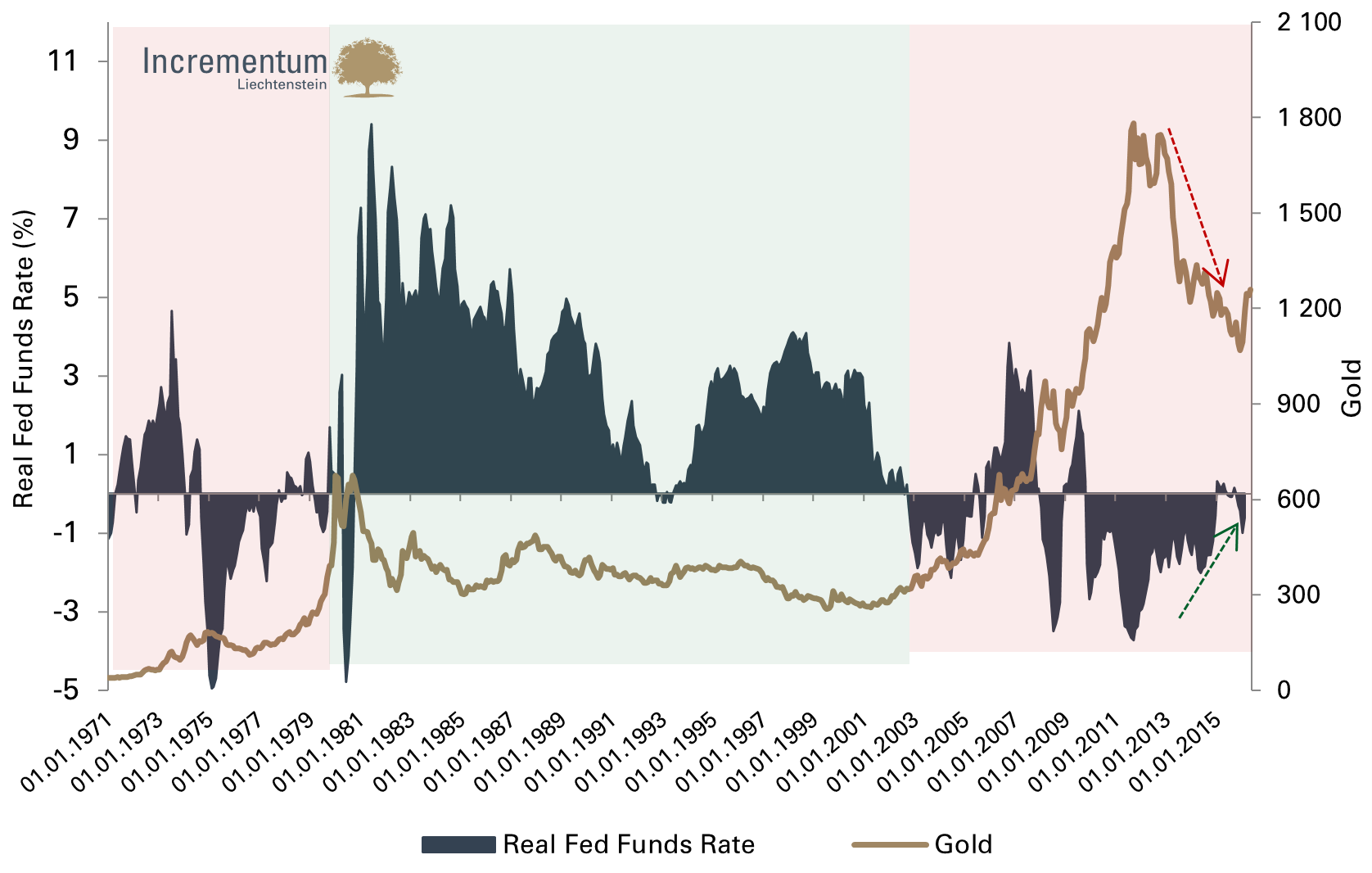

The following chart shows real interest rates compared to the gold price. There are two conspicuous time periods that were shaped by predominantly negative real interest rates: on the one hand the 1970s and on the other hand the time period from 2002 until today. Both phases clearly represented a positive environment for the gold price. However, one can also discern that the trend of real interest rates is relevant for the gold price. Thus real interest rates have been stuck in negative territory most of the time since 2011, but were in an upward trend. This increased the opportunity cost of holding gold, which created an unfavorable environment for the gold price.

Real interest rates vs. the gold price since 1971

Source: Federal Reserve St. Louis, Incrementum AG

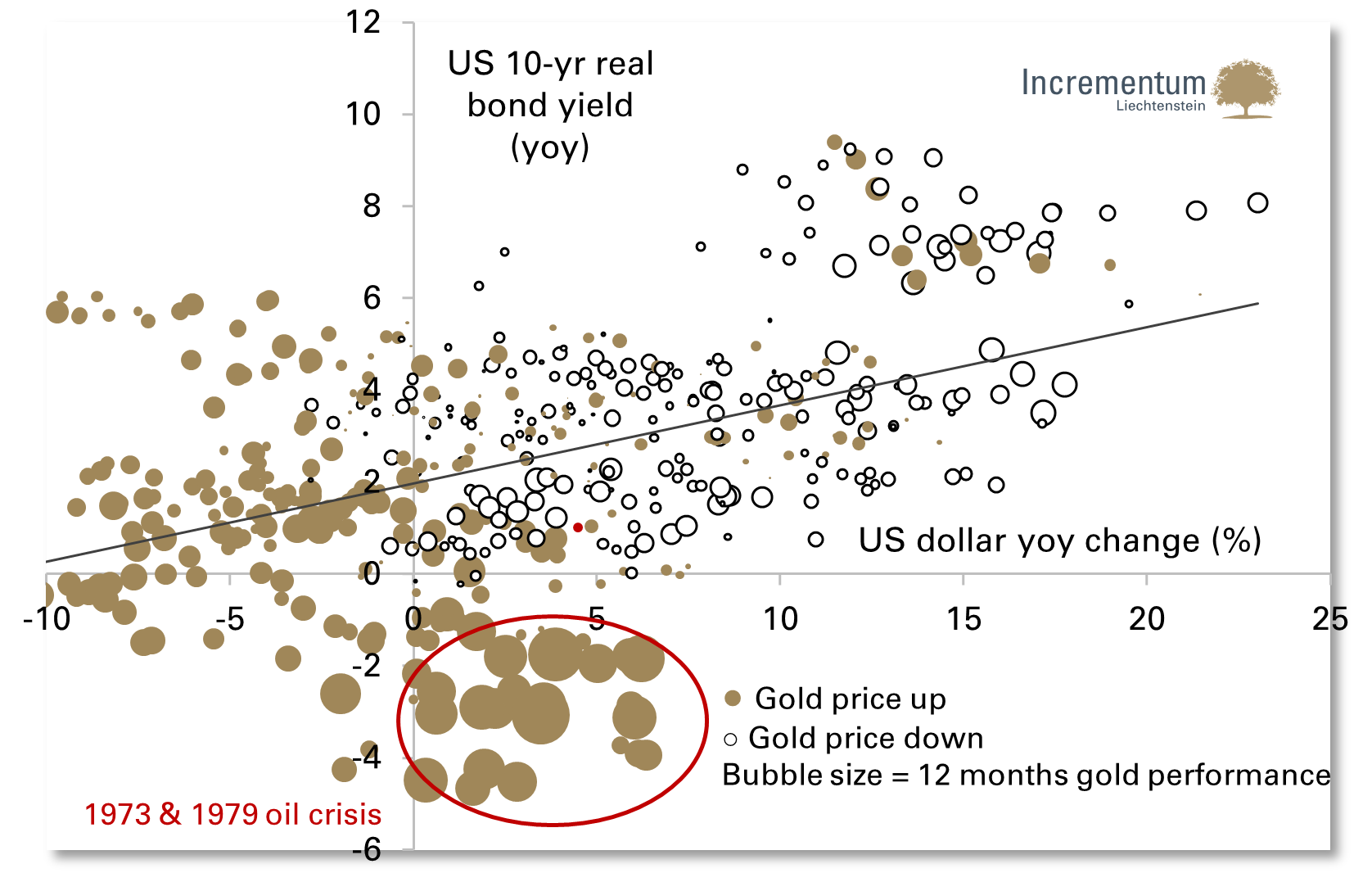

The following chart illustrates the annualized monthly performance of gold since 1973 compared to the trade-weighted dollar index as well as the real yields of 10 year US treasury notes. Golden circles stand for a rising gold price, white circles stand for a declining gold price; the larger the radius of the circles, the larger the price move. It can be seen that gold exhibited a stronger performance primarily in years in which the dollar weakened, while years in which the dollar appreciated and real interest rates increased were in most cases associated with a declining gold price. Gold posted its largest price gains during the oil crises of 1973 and 1979, while real interest rates were negative and the dollar’s performance was subdued. In our opinion such a scenario looks like an increasingly realistic possibility nowadays as well.

Gold vs. real interest rates and the trade-weighted US dollar index

Source: Société Générale, Federal Reserve St. Louis, Incrementum AG

Conclusion:

A long-term downtrend in the gold price would go hand in hand with rising or consistently positive real interest rates. Due to the amount of debt that has been amassed in the meantime – mainly on the government and corporate level, but also by private households – this is a hard to imagine scenario in our opinion, as central banks have long become hostage to these incautious debt policies.

Equities

Against the background of the above mentioned asset price inflation in a disinflationary environment, stocks as classical titles to capital were obviously among the greatest beneficiaries. The following chart illustrates that there exists a pronounced correlation between the trend in employment and the S&P 500 Index (scale inverted). The clear downtrend in initial jobless claims that has been in force since 2009 manifested itself in the form of increasing confidence and consequently rising stock prices. However, it appears now as though the trend in the labor market may be reversing. This could well signal the end of the bull market in equities.

S&P 500 (left scale) vs. initial jobless claims (right scale)

Source: Federal Reserve St. Louis, Incrementum AG

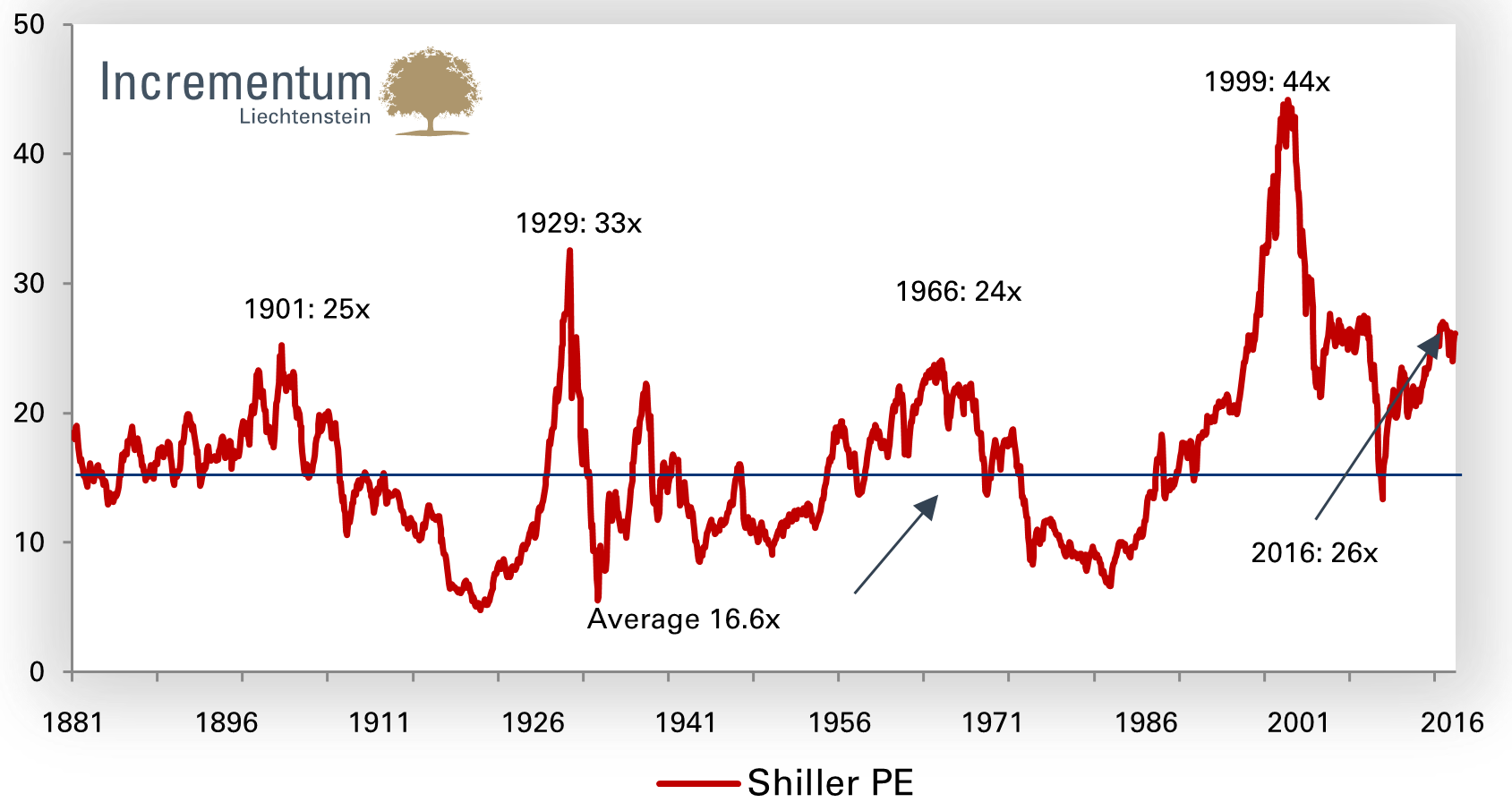

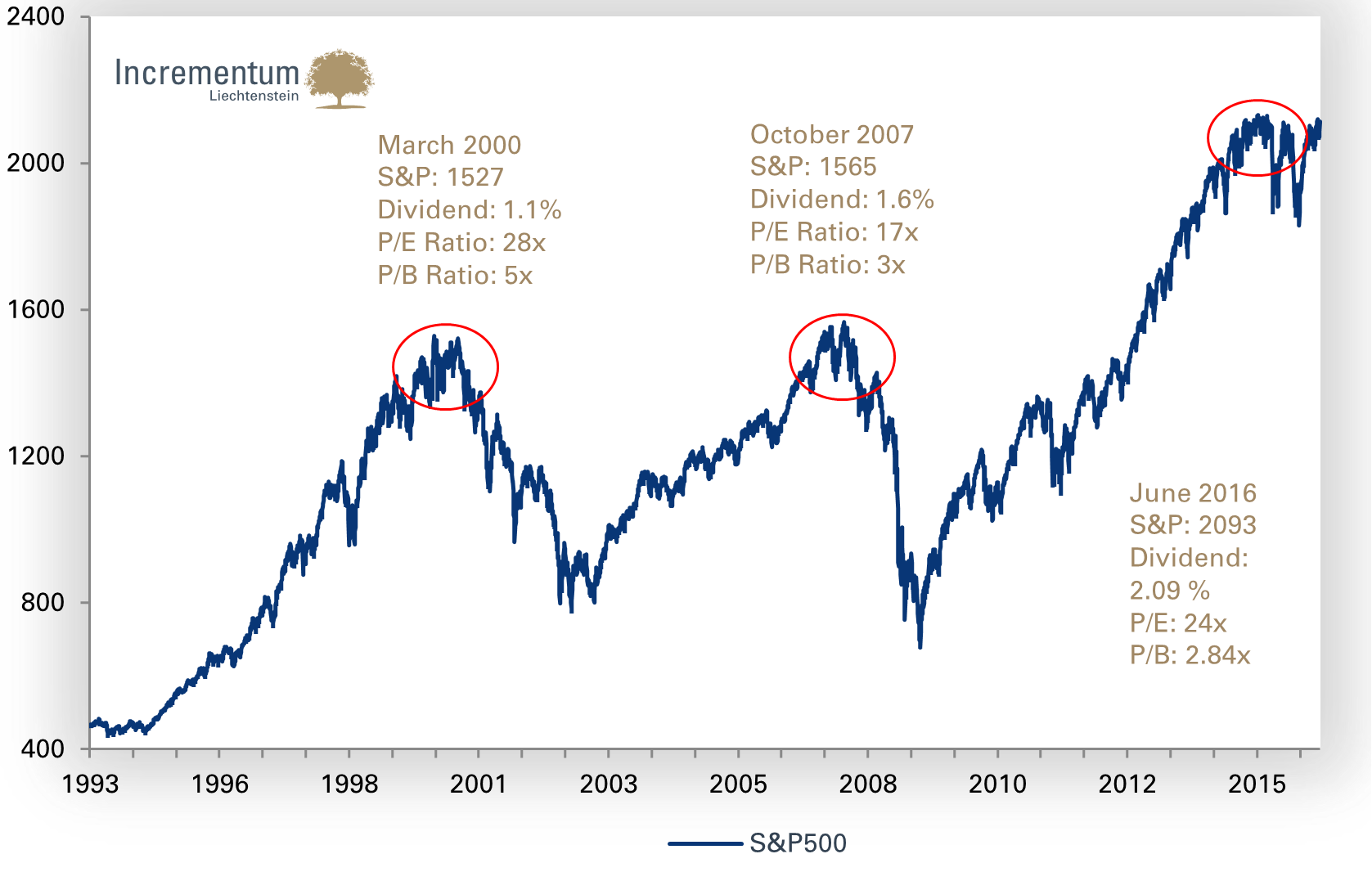

Naturally one should consider stock market valuations as well. The so-called Shiller P/E ratio (a.k.a. P/E 10 or CAPE) is suitable for assessing the long-term situation. According to this valuation measure, prospects for the US stock market do not appear very bright, as valuations are nowhere near bargain levels. The Shiller P/E ratio currently stands at 26, a level that has been exceeded on only two prior occasions over the past 134 years. The long-term average is 16.6, which is significantly below current levels.

Shiller P/E ratio since 1881

Source: Prof. Robert Shiller, Incrementum AG

If one looks at the last two major peaks in the S&P 500 Index in conjunction with the valuations prevailing at those times, a continuation of the bull market in stocks appears rather unlikely. The uptrend has been broken and the market has reached a plateau from which it has already suffered two short-term breakdowns over the past year.

S&P 500 Index and valuations at market peaks

Source: Yahoo Finance, Incrementum AG

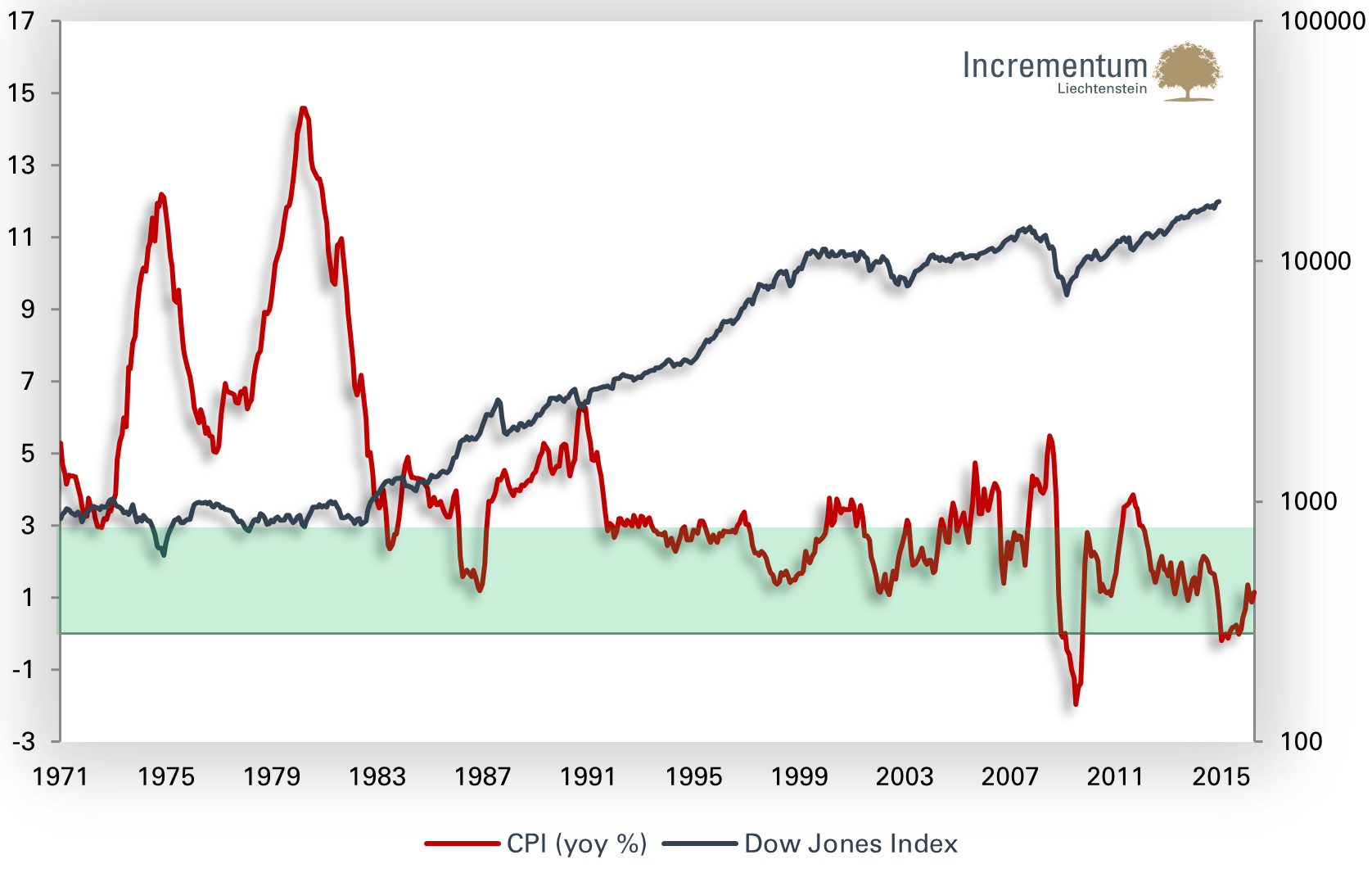

The inflation rate is not only of decisive importance for gold, but also for the stock market. Our analyses of price inflation show that the most favorable environment for equities is associated with inflation in a range of +1% to +3%. This “feel-good corridor” was continually violated in the 1970s, stocks moved sideways (in interesting ways) in nominal terms, but lost enormous ground in real terms. Other time periods with relatively high inflation rates such as e.g. 2000 – 2002, 2005 or 2007 to mid 2008, also tended to be negative for the stock market. Should inflation concerns – in line with our expectations – be gradually priced in, this would definitely represent a headwind for equities.

US inflation rate and the Dow Jones Industrial Average since 1971

Source: Incrementum AG, Wellenreiter Invest, Federal Reserve St. Louis

Conclusion:

The current valuation of US equities is quite ambitious compared to historical valuation levels. A reversion to the mean appears only a question of time, especially if inflation concerns should come to the fore. The bull market in US stocks seems to be sputtering lately. A preview of what the world could look like if the trends of recent years’ reverse, was provided early this year when stock markets plunged and gold entered a new bull market.

[1] See also: “Gold in the context of portfolio diversification”, “In Gold we Trust 2015”, and “The extraordinary portfolio characteristics of gold“, “In Gold we Trust 2014” and so forth

[2] See: “Gold: A commodity like no other”, World Gold Council, April 12, 2011

[3] See: Andreassen, Paul B.: “On the Social Psychology of the Stock Market: Aggregate Attributional Effects and the Regressiveness of Prediction“, Journal of Personality and Social Psychology, 1987 (53), pp. 490-496

[4] The concepts takes the pattern of “mean reversion” into account. As markets tend to exaggerate, they need to correct over time.

[5] See: Taghizadegan, Rahim, Ronald-Peter Stöferle, Mark Valek, and Heinz Blasnik: Austrian School for Investors – Austrian Investing between Inflation and deflation, mises.at, 2015

[6] See: Santoli, Michael: “Gold Not Antifragile Enough for Black Swan Author”, finance.yahoo.com, March 22, 2013

[7] See: Korschorke, Albrecht, Susanne Lüdemann, Thomas Frank und Ethel Matala de Mazza: Der fiktive Staat: Konstruktionen des politischen Körpers in der Geschichte Europas, Fischer Taschenbuch Verlag, Frankfurt am Main, 2007, p.11

[8] See: ibid. p.57

[9] Quoted in: Popescu, Dan: “The canary of the currency markets”, goldbroker.com, December 14, 2015

[10] Vgl. “The Iron Law of Money”, John Butler, GoldMoney Research