Following the structural revamp introduced in 2017, the 2018 edition reinforced what has since become the signature IGWT style.

The report featured:

A coherent macroeconomic narrative

Scenario-based analysis

Stronger visual storytelling

In essence, 2018 was the first edition where form and content aligned perfectly, setting the standard for all subsequent reports.

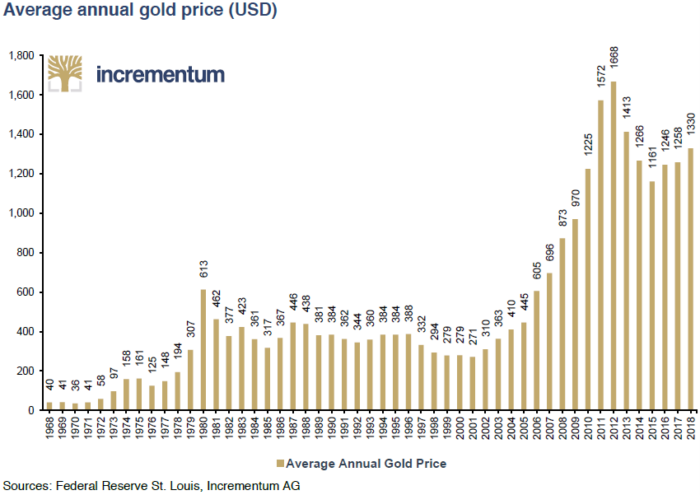

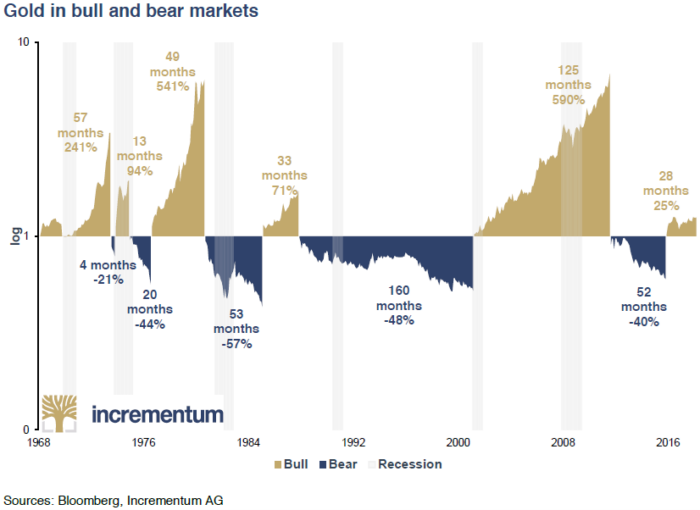

Seven years after the 2011 peak, gold remained in a prolonged consolidation phase.

In truth, prices had been moving sideways since 2013. Accordingly, we described this pattern as a “cha-cha-cha” on account of the frustrating sequence of advances and retreats with no clear trend.

Notwithstanding, this apparent stagnation masked a deeper process. Consolidation, as we argued, was not a sign of weakness, but of preparation.

The breakout, when it came in 2019, validated this view.

Building on the four-scenario framework introduced in the prior edition (IGWT 2017), we continued to map gold’s trajectory under different macroeconomic conditions up to early 2021, matching the period of President Donald Trump’s first term in office.

By 2018, gold prices were fluctuating within Scenarios B and C. Ergo, we maintained that Scenario C, which was characterized by rising inflation and solid growth, was the most likely outcome.

When Trump left office in January 2021, gold stood at USD 1,855.80, squarely within the projected range of USD 1,400 to USD 2,300. This outcome once again demonstrated the value of robust frameworks over precise timing, as well as how much we had improved with regards to forecasting the gold price.

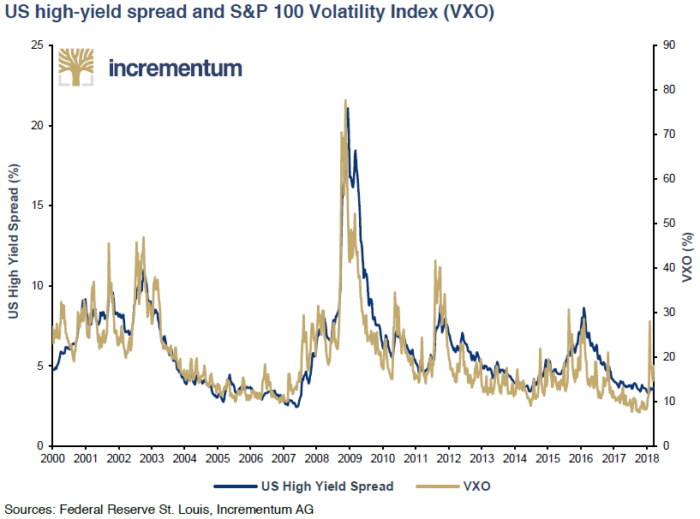

Interestingly, the illusion of stability began to fracture in early 2018. The volatility spike known as Volmageddon exposed the fragility of a system built on years of ultra-loose monetary policy.

Essentially, financial conditions tightened, leverage levels came into focus, and the risks embedded in the credit cycle became more visible. Despite markets recovering quickly, the message was clear: the foundation of the post-2008 expansion was far from solid.

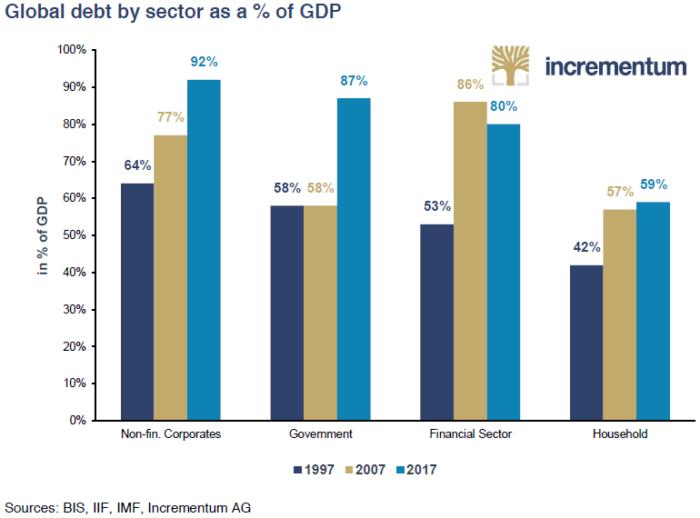

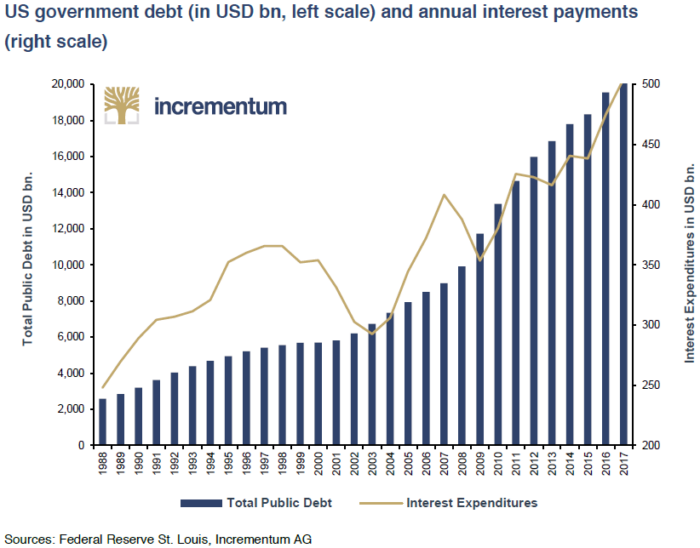

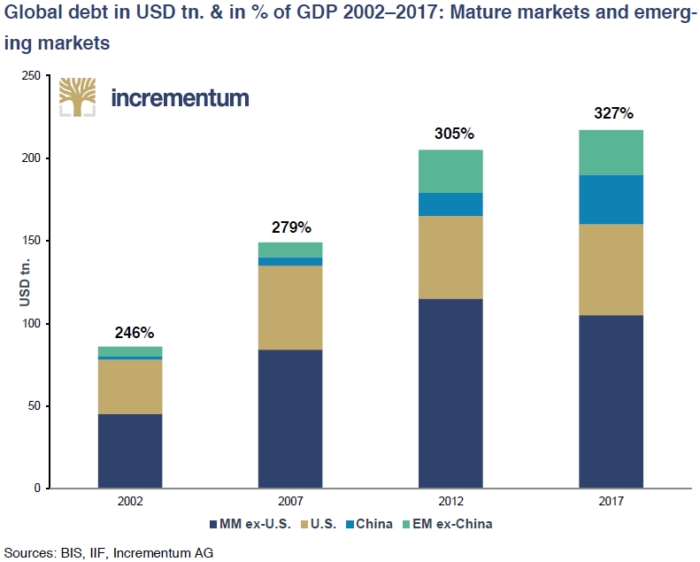

Evidently, the global recovery following the financial crisis had been driven primarily by expanding credit and rising government debt. This dynamic was not limited to developed markets. As a matter of fact, emerging economies also participated actively in the debt expansion, particularly through corporate borrowing and US dollar-denominated liabilities.

While this debt-fueled growth extended the cycle, it also introduced structural vulnerabilities:

Rising debt servicing costs

Increasing sensitivity to interest rates

Growing systemic fragility

The paradox was evident: the very mechanism sustaining growth was simultaneously undermining it. As the Austrian business cycle theory asserts, the boom lays down the seeds for its own bust.

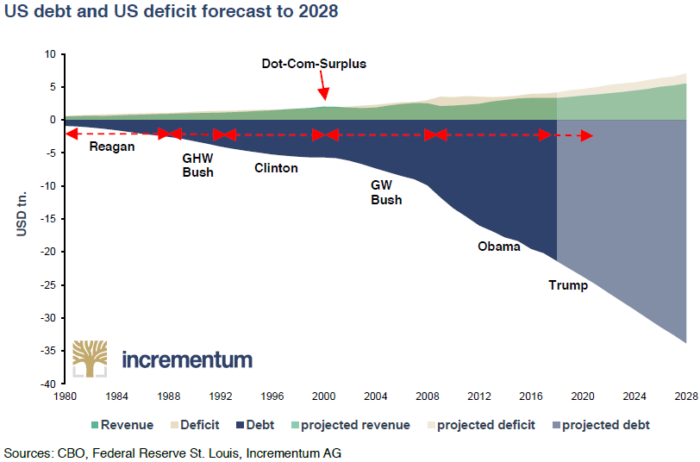

Another notable takeaway from the 2018 report is how quickly US debt projections became outdated. At that time, the CBO forecasted debt at USD 33.8 trillion by 2028.

Fast forwarding to today, debt levels have already reached USD 39 trillion. To call this an underestimation is an understatement.

This gap highlights a structural blind spot: the exponential nature of debt in a credit-driven system. The implications are clear:

Shrinking fiscal flexibility

Rising sensitivity to interest rates

Eroding confidence in sovereign balance sheets

In such an environment, gold’s role as a hedge against fiscal and monetary instability becomes increasingly critical.

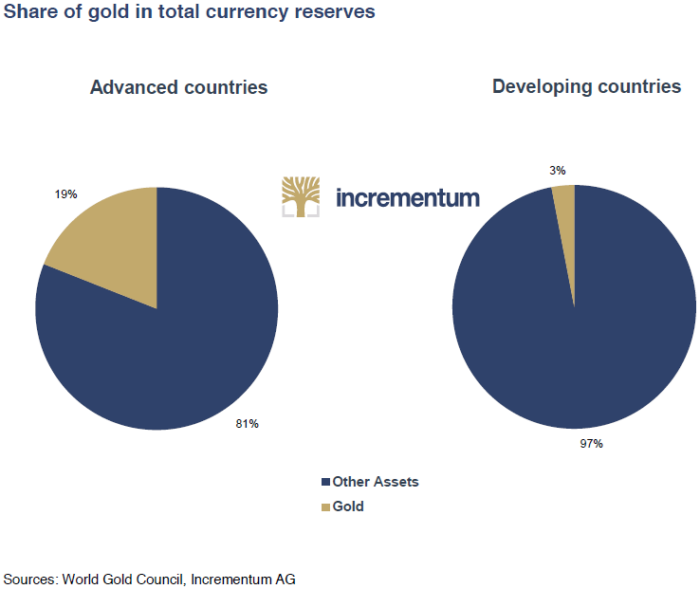

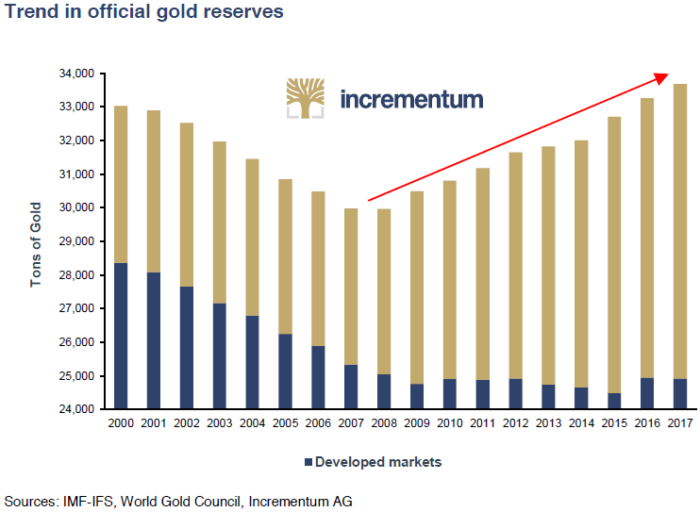

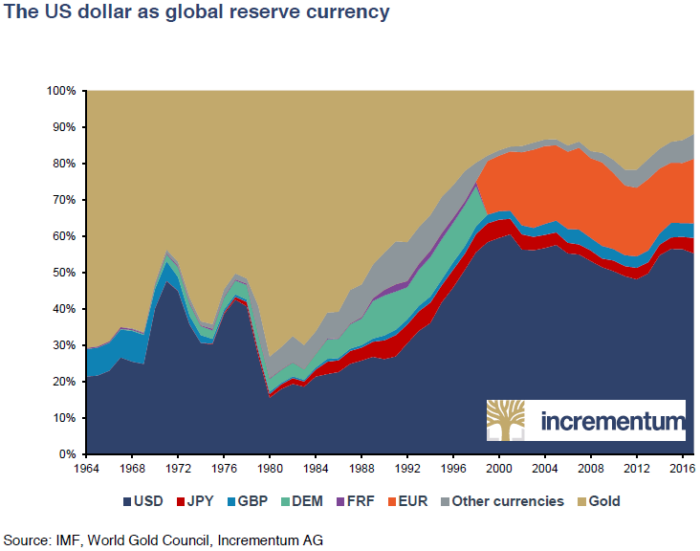

A distinct trend highlighted in the report was the steady accumulation of gold by central banks, particularly in emerging markets. Clearly, this development reflected a broader strategic shift:

Diversification away from the US dollar

Growing geopolitical considerations

Increasing demand for neutral reserve assets

As we noted in earlier editions, this trend was not purely economic. Obviously, there were some inescapable and intertwined considerations about power and sovereignty.

One of the most striking observations, which was reminiscent of a quote highlighted in the 2015 report, remains highly relevant:

“The increase in gold reserves should be seen as strong evidence of growing distrust in the dominance of the US dollar and the global monetary and credit system associated with it. Apart from economic interests, geopolitical interests and power aspirations play a very important part in this context as well.”

In 2018, this shift no longer seemed to live exclusively in the theoretical realm. Although it progressed in ebbs and flows, this trend was visibly unfolding.

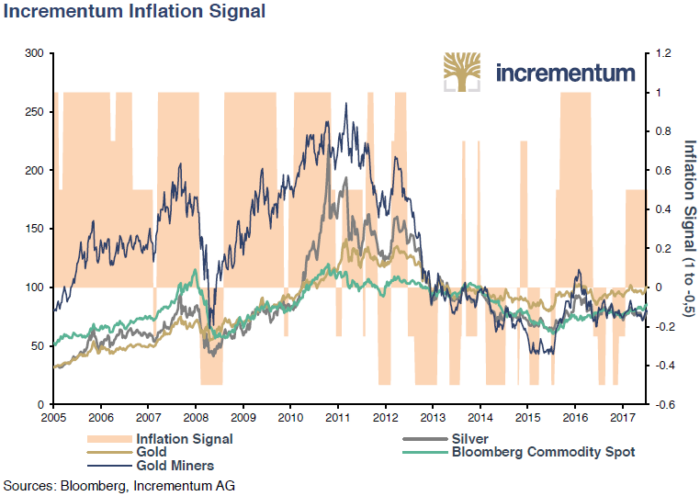

Our proprietary Incrementum Inflation Signal had been indicating a shift since 2016. The drivers were clear:

A weakening US dollar

Bottoming commodity prices

Persistently low interest rates

While inflation remained moderate in 2018, the underlying trend had turned. In hindsight, this marked the early stage of the inflationary wave that would fully materialize years later.

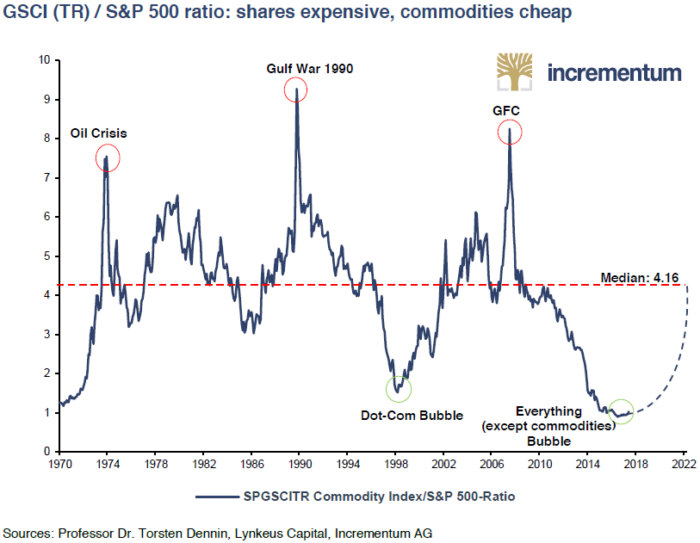

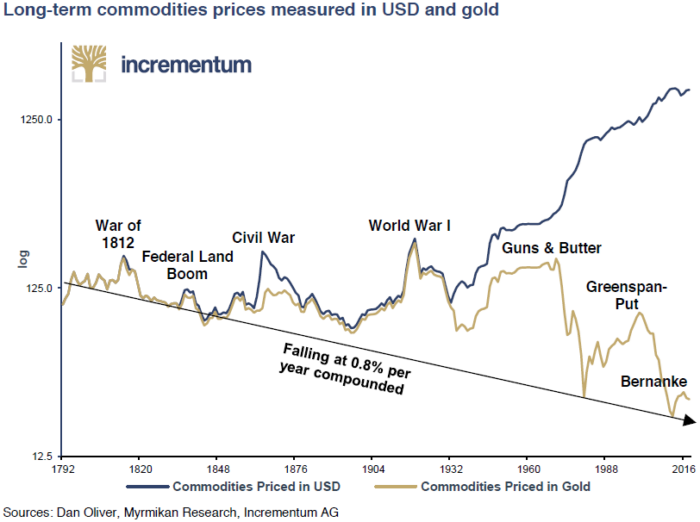

A fundamental insight of the report concerns the nature of price dynamics under different monetary regimes.

In a sound monetary system, productivity gains tend to result in falling prices. In contrast, a debt-based fiat system leads to structurally rising nominal prices.

Succintly, gold, in this context, serves as a measuring stick of purchasing power, revealing long-term trends that fiat currencies obscure.

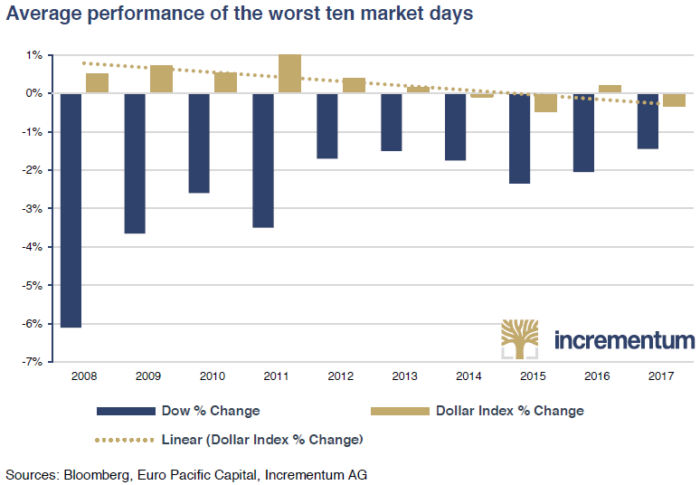

Traditionally, the US dollar strengthens during periods of financial stress. However, in 2018, we observed subtle, though important deviations from this pattern.

Demonstrably, the dollar’s behavior became increasingly dependent on policy credibility and macro conditions, rather than functioning as an unconditional safe haven. This shift hinted at deeper changes within the global monetary system, of course.

One of the central investment conclusions of the report was the growing importance of gold as a portfolio component. We emphasized its role as:

A diversifier

A hedge against systemic risk

A protector during periods of market stress

Of note, this thinking built on earlier concepts such as the Permanent Portfolio (2016) and foreshadowed the development of the “New 60/40 Portfolio” introduced some years later, in 2024. As confidence in traditional asset classes began to waver, gold’s strategic relevance increased.

Another key argument was that bonds, given their extreme valuations, might fail to provide protection in future downturns. If both equities and bonds were to decline simultaneously, investors would need an alternative safe haven.

Needless to say, we argued that gold was the most likely beneficiary in such a scenario. After all, gold has been the preserving its holders’ wealth for five millennia.

Despite multiple volatility episodes throughout 2018 and 2019, the anticipated recession did not immediately materialize. The reason was simply that credit continued to expand relentlessly.

Rather than allowing the cycle to reset, policymakers extended it further. However, this merely postponed the adjustment, increasing the scale of the eventual consequences.

The recession ultimately arrived, albeit not through the natural progression of the business cycle. Instead, it was triggered by the global lockdowns of 2020.

If you remember, the response was unprecedented:

Massive fiscal stimulus

Explosive growth in government debt

Rapid expansion of central bank balance sheets

Although these measures reignited growth, it also accelerated the structural trends identified in earlier IGWT reports. Be that as it may, we’re saving the throwback to the pandemic period for another day.

By 2018, it had become obvious that the debt expansion was global in nature.

Emerging markets, in particular, had significantly increased their exposure to debt, often denominated in foreign currencies. This development heightened their vulnerability to currency fluctuations, consequently tightening the financial conditions in these economies.

The debt cycle was certainly not confined to advanced economies. Indubitably, it had become systemic at the planetary scale.

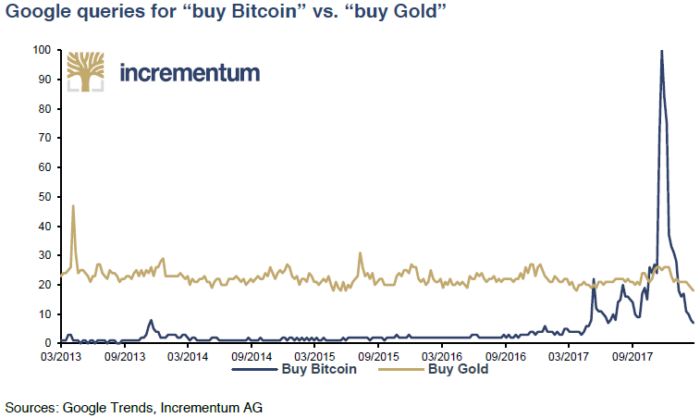

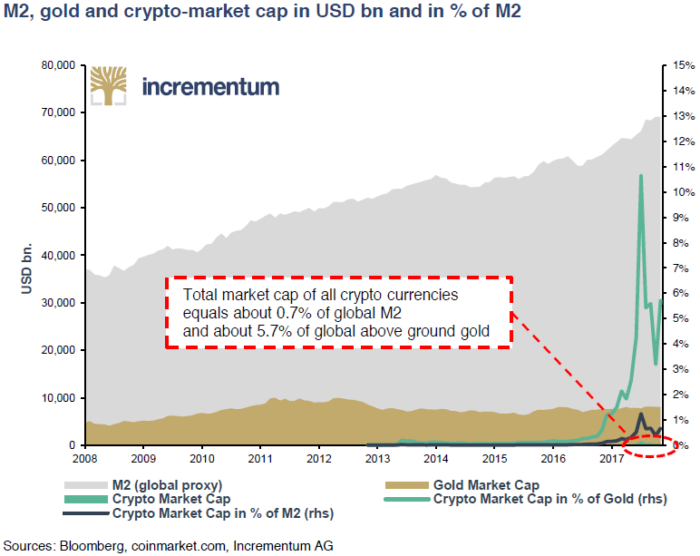

The rise of digital assets introduced a new dimension to the monetary debate. Rather than viewing Bitcoin as a competitor to gold, we proposed a more nuanced perspective.

On the one hand, gold represents a time-tested store of value. On the other hand, Bitcoin embodies a new form of monetary technology.

To sum up, in an evolving financial system, these assets can coexist and complement each other.

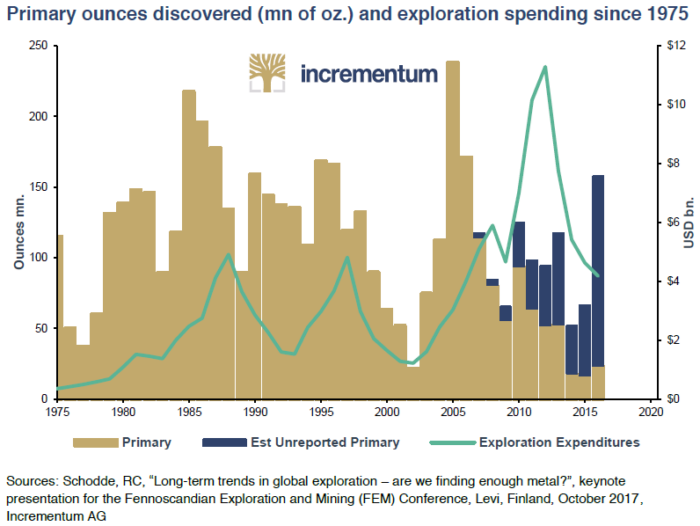

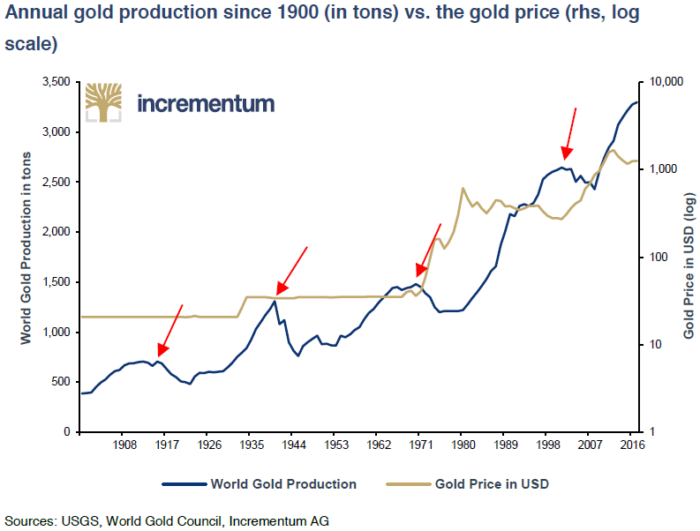

The report also explored the concept of peak gold – which was a topic already explored in the 2012 edition – examining whether production constraints might limit future supply. Naturally, this discussion led to a broader debate between:

Neo-Malthusians, who emphasize resource scarcity

Cornucopians, who highlight human innovation

Our conclusion was balanced: while geological constraints are real, technological progress continues to expand possibilities. In this tension lies a constructive, long-term case for gold.

The 2018 edition of the In Gold We Trust report did not coincide with a dramatic market event. Nevertheless, its significance lies in the timing, as well as the clarity of our findings.

To make long story short, it identified:

The growing fragility of a debt-driven system

The early signs of monetary regime change

The increasing relevance of gold in portfolio construction

The emergence of new monetary competitors

The structural shifts in global reserves and currency dynamics

Looking back, 2018 stands as a quiet but decisive inflection point. The tides were turning, although most investors had hardly noticed.

Go to the Archive of the IGWT Report and explore the 2018 edition in full.

#20Years20Threads #InGoldWeTrust #GoldReport #GoldInvesting #DebtCycle #CentralBanks #MonetaryPolicy #InflationHedge #SoundMoney #SafeHaven #AssetAllocation #PortfolioStrategy #Bitcoin #DigitalAssets #DeDollarization #GlobalDebt #EmergingMarkets #Commodities #ResourceEconomics #MacroTrends #InvestmentInsights #AustrianEconomics #IGWT18 #AnniversarySeries