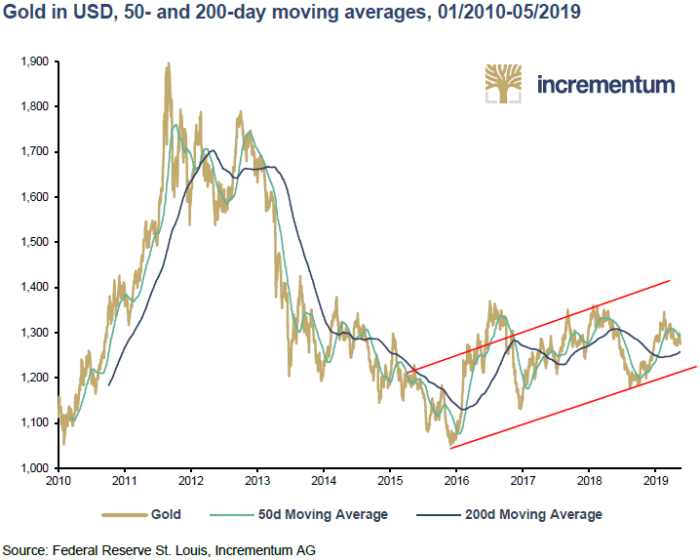

By 2019, we were eight years past the 2011 peak in gold.

Gold remained below its all-time high of USD 1,921, while silver had yet to reclaim its 1980 highs. The market appeared stuck in a prolonged consolidation phase.

In any event, beneath the surface, structural forces were quietly aligning. The next secular bull market was already forming, albeit unnoticed by most.

At the heart of the report lay a powerful observation:

“The Western world is to a large extent a high-trust society. Cooperation is no longer based on belonging to a small, tight-knit community such as a clan, but rather to a comparatively anonymous society in which people trust each other without necessarily knowing each other. Without this advance of trust, without this open approach to each other, there can be no mutually beneficial cooperation. However, there is growing evidence that this trust is increasingly eroding.”

Trust – arguably the most critical intangible pillar of modern economies – was deteriorating across multiple dimensions:

Political institutions

Monetary authorities

Media and societal cohesion

This erosion would prove to be one of the defining forces of the decade that followed.

The symptoms were already visible in 2019:

Rising populism

The Yellow Vest protests in France

Increasing youth disillusionment

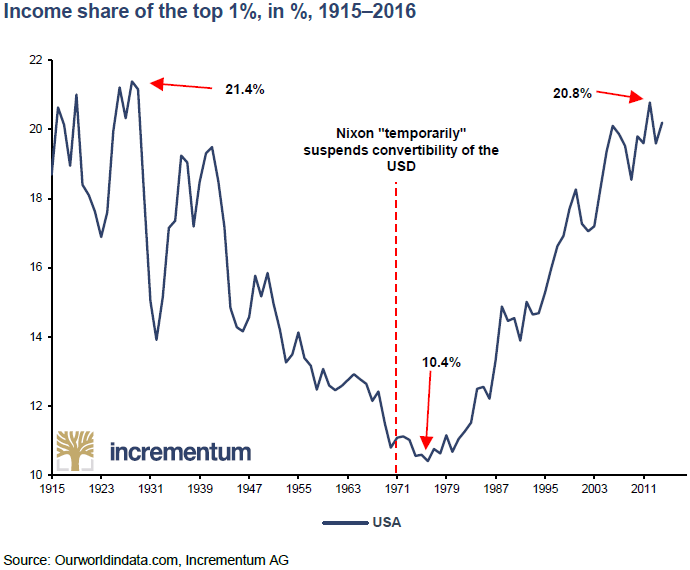

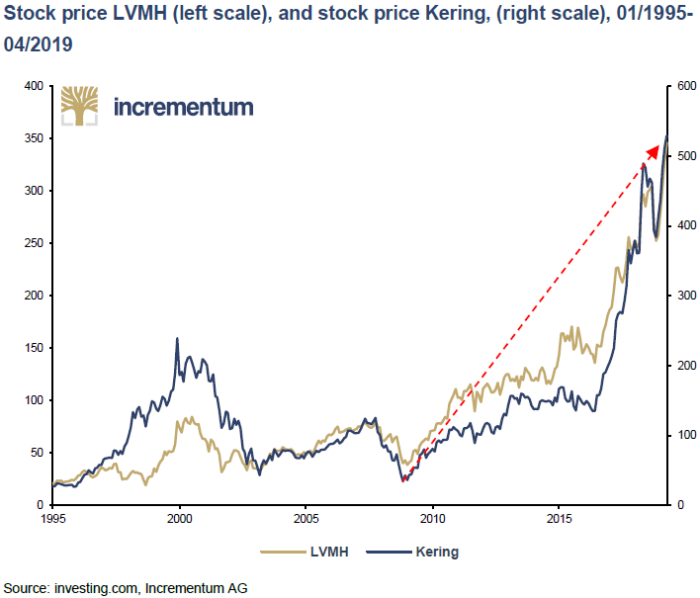

Since the Nixon Shock in 1971, inequality had been steadily rising, fueled by inflationary monetary policies. This dynamic led to a widening gap between asset owners and the broader population, fertilizing the ground for anti-establishment movements.

Inflationary policy did not affect everyone equally.

Asset prices surged

Luxury consumption flourished

Wage growth lagged behind

This phenomenon, often described as the Cantillon Effect, exacerbated social divides and intensified systemic tensions.

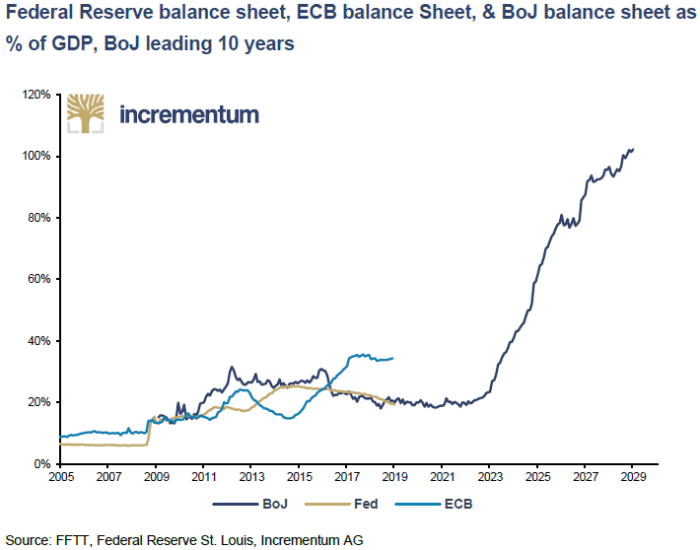

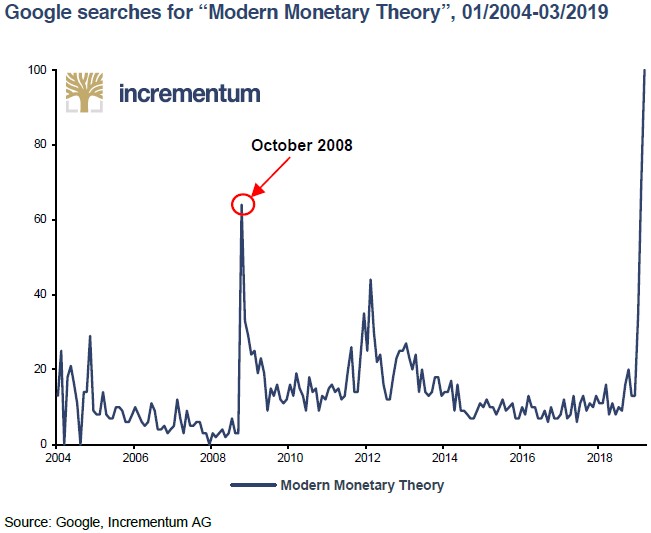

The events of late 2018 marked a turning point. After attempting monetary tightening, central banks were forced into a rapid reversal following a sharp market downturn.

This “monetary U-turn” included:

Renewed expectations of rate cuts

A return to quantitative easing

The growing popularity of Modern Monetary Theory (MMT)

Crucially, this episode marked the beginning of a decline in confidence in central banks’ perceived omnipotence.

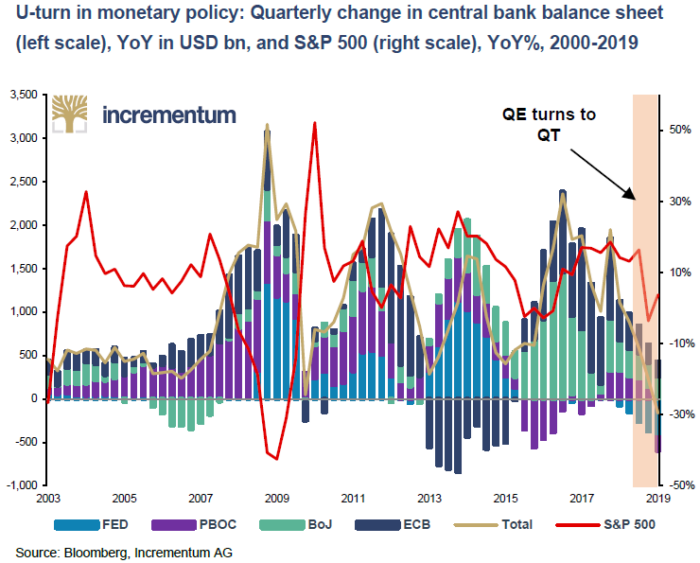

Quantitative tightening proved short-lived. Within less than a year, policymakers reverted to stimulus.

Ostensibly, the global financial system had become structurally dependent on liquidity injections. Notwithstanding, something had changed:

Confidence in central banks was no longer unquestioned.

Drawing on Hartmut Rosa’s acceleration theory, the monetary system can be understood as a system of dynamic stabilization. Essentially, it requires continuous expansion to remain stable:

The money supply must grow

Debt must expand

Economic activity must accelerate

This insight leads to a sobering conclusion. A lasting normalization of monetary policy is unlikely. Instead, so-called unconventional measures – QE, negative rates, and beyond – are destined to become standard tools, continuously expanded under systemic pressure.

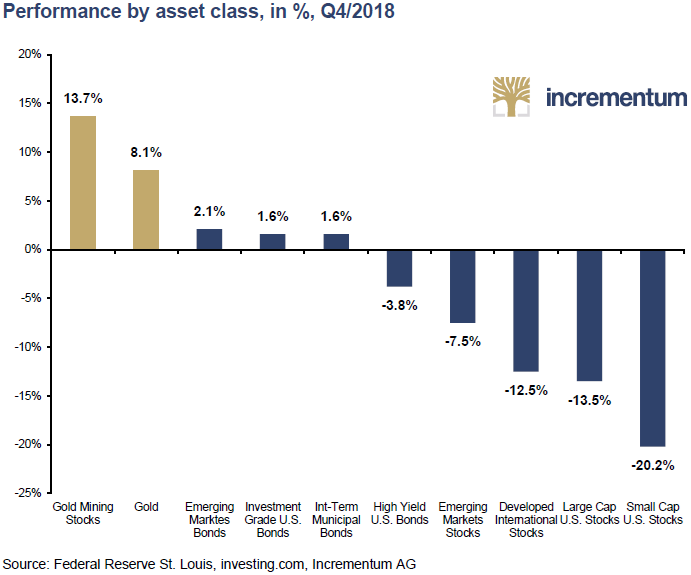

Against this backdrop, gold once again demonstrated its value. During the equity market turbulence of 2018:

Gold rose by 8.1%

Gold mining stocks surged by 13.7%

Evidently, this taught the lesson that gold thrives in periods of uncertainty and instability.

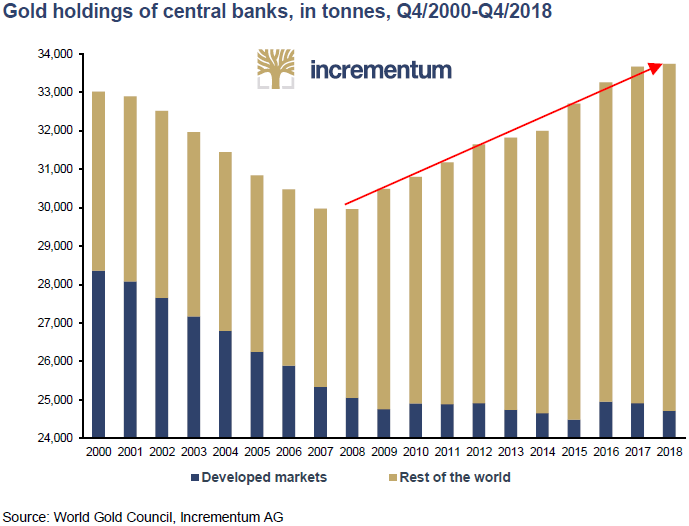

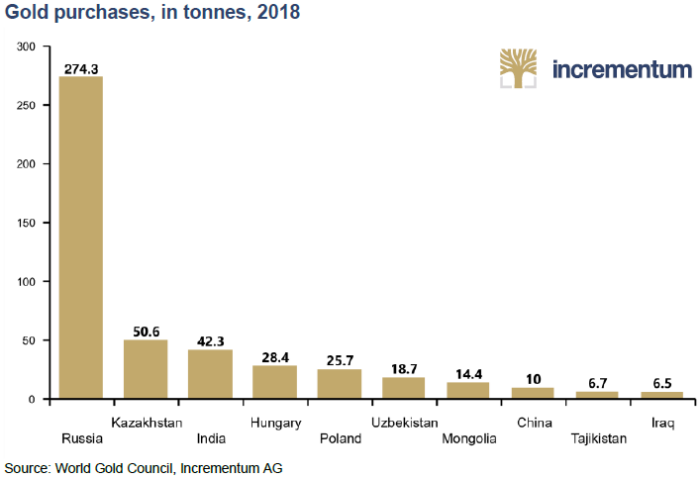

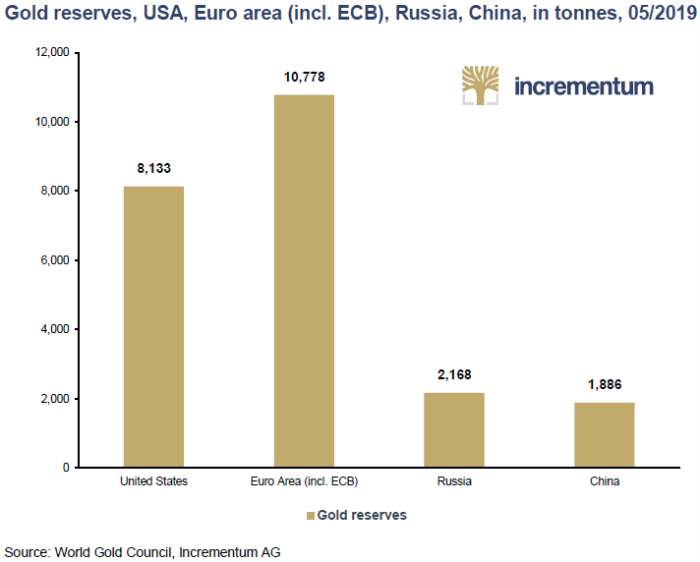

In 2018, central banks became net buyers of gold at the highest levels since 1971.

This trend reflected a growing unease with the US dollar-based monetary system and rising geopolitical tensions. In truth, gold was no longer just a shiny reserve asset, it was becoming a strategic monetary hedge.

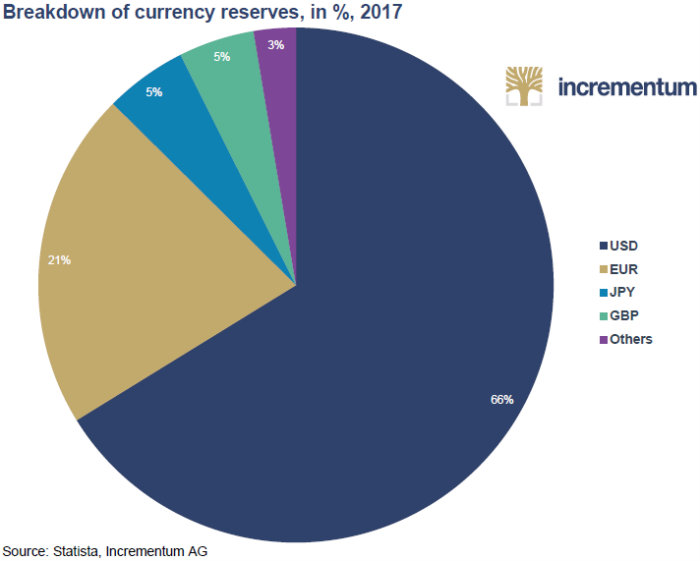

Emerging markets played an increasingly dominant role:

Representing ~50% of global GDP

Accounting for ~70% of gold demand

Ina nutshell, countries such as Russia, China, and Hungary significantly increased their gold reserves. This shift signaled a rebalancing of monetary power toward the East.

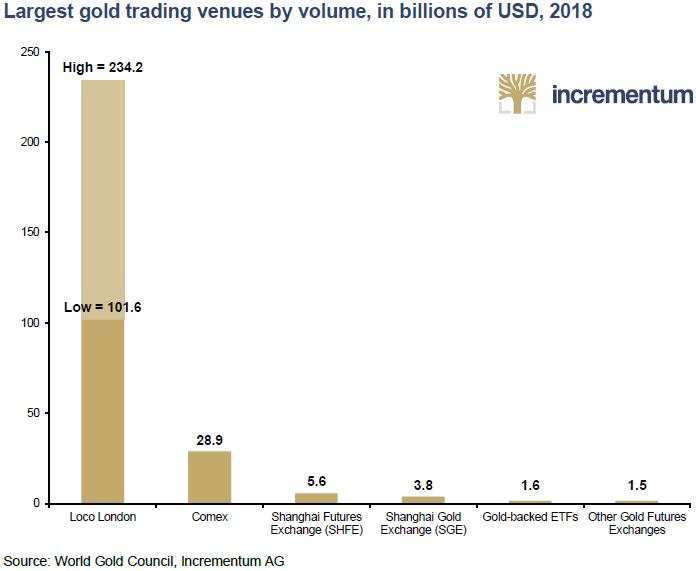

Of note, a striking structural imbalance persisted:

The East dominated physical demand

The West controlled price discovery

London and New York remained the epicenters of gold pricing, despite the growing importance of Asian markets.

The collapse of the Iran nuclear deal and subsequent sanctions highlighted a critical reality:

The US dollar had become a geopolitical weapon.

In response:

The EU explored alternatives to dollar dependence

China and Russia accelerated efforts to bypass the USD

Needless to say, this marked a decisive step toward the fragmentation of the global monetary order.

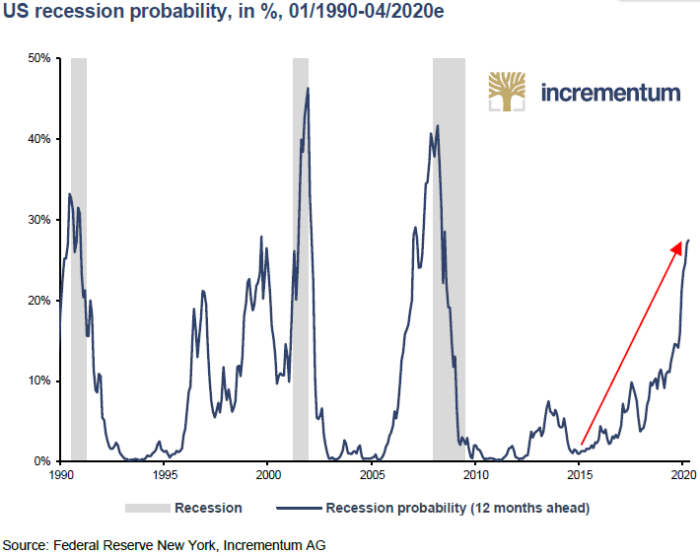

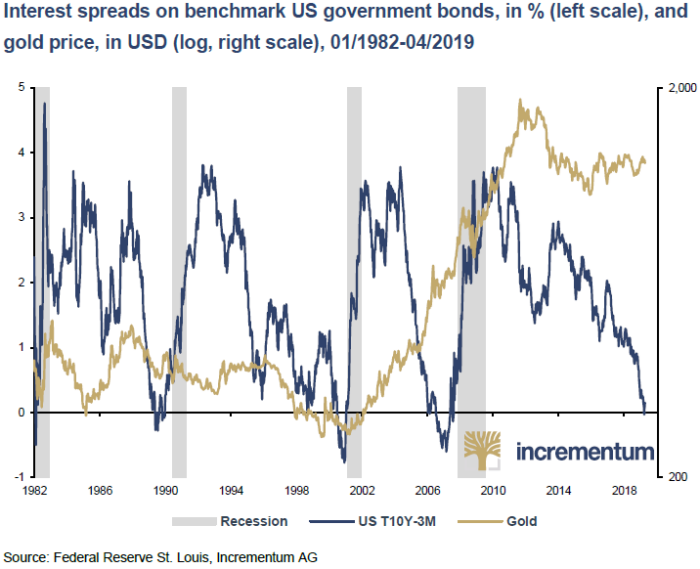

Despite strong equity markets in 2019, warning signs were evident:

Yield curve inversion

Rising debt levels

Slowing economic momentum

Thus, we anticipated:

Rate cuts

Renewed QE

Extreme policy measures

Not to sound cocky, but all of them were to materialize by the following year.

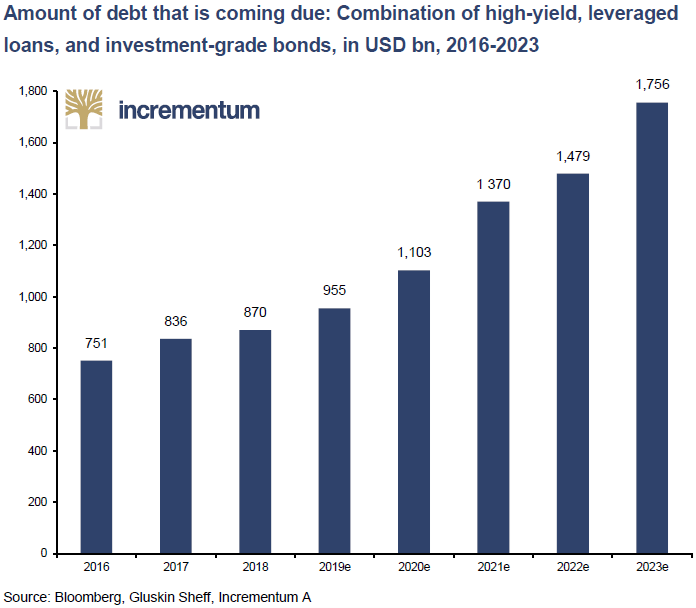

The US remained the “cleanest dirty shirt,” but underlying vulnerabilities were mounting:

Exploding public and private debt

Elevated asset valuations

Structural fragility

Unmistakenly, the system’s stability increasingly depended on continued monetary expansion.

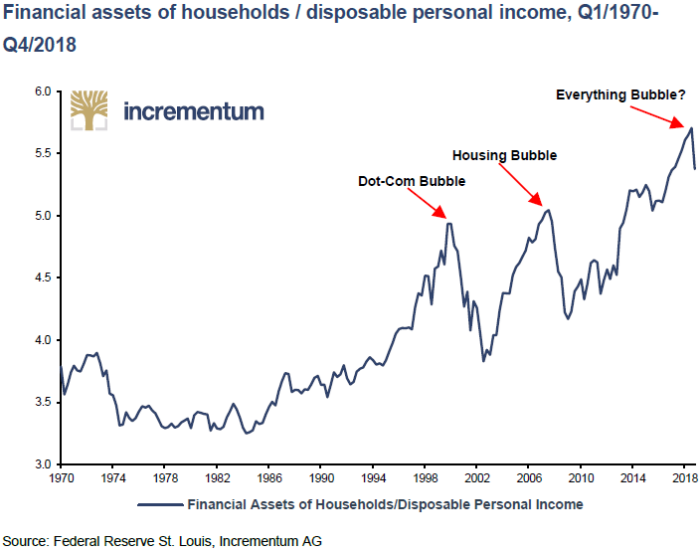

More than a decade after the Global Financial Crisis, the banking system remained structurally impaired.

Indeed, credit expansion was constrained. Therefore, systemic risks persisted, even though financial assets’ values rose progressively, and the official economic metrics indicated an unflagging recovery.

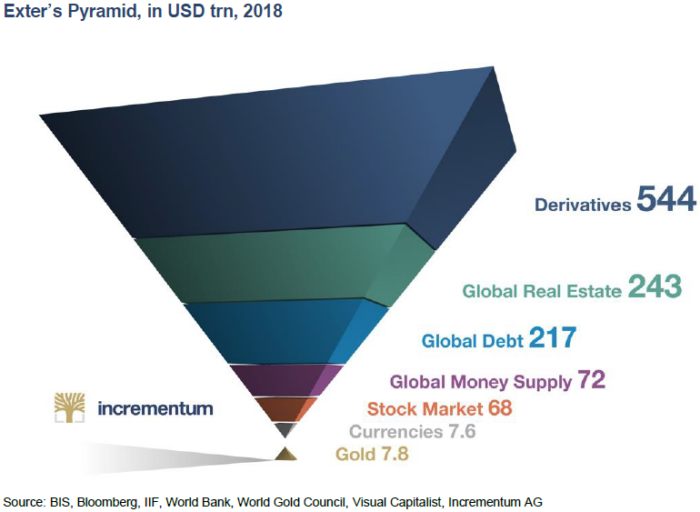

John Exter’s Pyramid provided a powerful framework. In short, as debt accumulates, financial assets become increasingly unstable.

At the top of the pyramid sits gold – or stands at the bottom holding everything together, depending on your perspective. In times when the inflated bubble financial system finally unravels, gold is proven to be the ultimate safe haven.

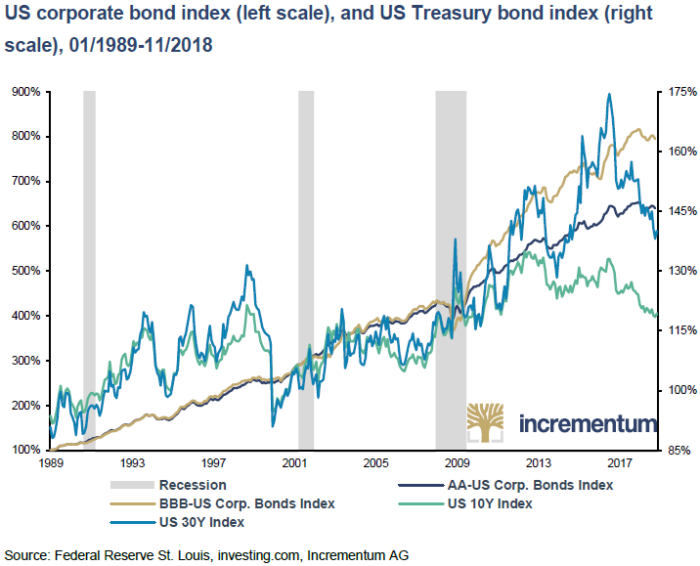

That being said, the surge in BBB-rated corporate debt posed a significant threat. Considering the level of indebtedness that corporations got themselves into, while the economy failed to recover to its estimated potential, a significant chunk of them could have faced a cascading series of defaults.

On this account, a wave of downgrades could ensue, triggering a credit market freeze. Believe it or not, this is precisely what occurred during the 2020 pandemic crisis, until monetary and government authorities came to the rescue.

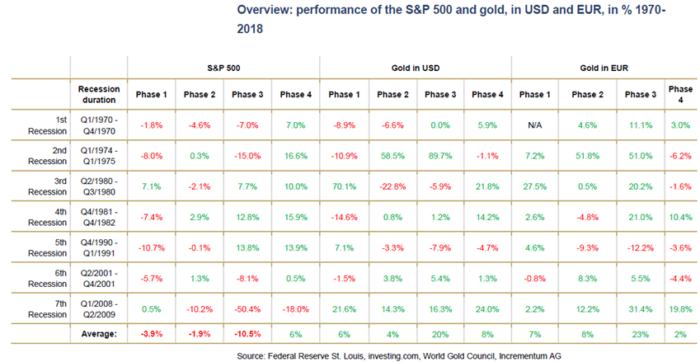

Our historical analysis showed that gold had delivered positive performance across all recession phases since 1970. At the same time, equities faltered, weighing down on investors portfolios right when they needed a wealth boost.

This has reinforced gold’s role as a portfolio stabilizer and hedge against equity drawdowns. In fact, due to being so relevant and insightful, we presented an updated version of this framework in all our subsequent IGWT reports since then.

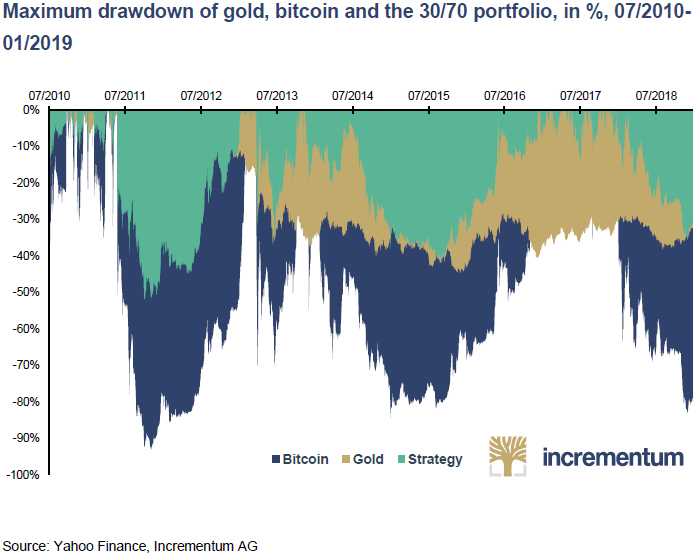

One of the most forward-looking ideas in the report was the combination of gold and Bitcoin. Basically, we devised a portfolio allocation of:

70% gold

30% Bitcoin

In the end, this strategy offered improved returns with comparable risk, benefiting from low correlation and rebalancing effects.

Keith Weiner (CEO of Monetary Metals) proposed an innovative concept:

Bonds denominated in gold

Interest paid in gold

This idea built on a theme that had been discussed for at least the previous two years. In the IGWT 2017, we showed there was a growing chorus in the US called for “dethroning” the US dollar as the global reserve currency.

Drawing on this precious metal’s stability, gold bonds could represent a step toward restoring gold’s role as a yielding monetary asset and potential anchor of a new system.

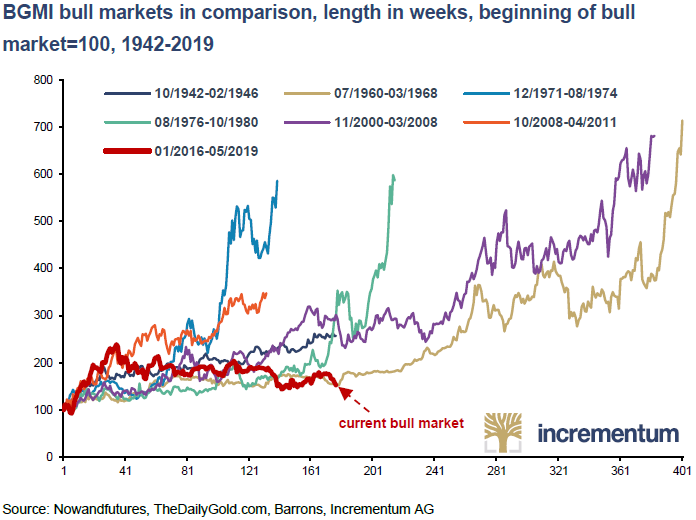

Despite improving fundamentals, gold mining equities lagged behind. Relative to previous rallies, gold miners were still incredibly dormant.

However, conditions pointed toward a significant revaluation and catch-up rally. As we would find out later on, this trend would unfold into a secular bull market. Nevertheless, gold discoveries would remain scant.

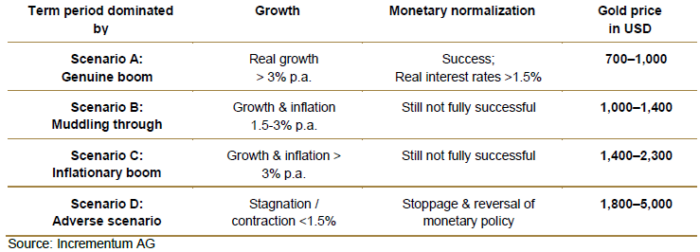

Similar to our calls made in our previous two reports, we identified an inflationary boom (Scenario C) as the most likely outcome.

📍 Target: approximately USD 1,800 by early 2021

Reality? Gold reached USD 1,855, validating our thesis with remarkable precision.

Notably, gold’s breakout from its long-standing consolidation phase began just weeks after the report’s release. Clearly, the groundwork was being prepared for the 2020s Golden Decade.

The IGWT 2019 report anticipated many of the defining trends of the current decade:

The erosion of trust across institutions

The return of aggressive monetary policy

The rise of de-dollarization

Increasing geopolitical fragmentation

Gold’s resurgence as a strategic asset

As this tough, though instructive decade for precious metals reached its end, a new rosier era would begin, not just for gold and silver investors, but for the global economy and the whole world order.

Dive back into this essential edition. Go to the Archive of the IGWT Report and explore the IGWT 2019 in full.

#20Years20Threads #InGoldWeTrust #GoldReport #GoldInvesting #GoldSurge #GoldReserves #PreciousMetals #SoundMoney #InflationHedge #DigitalAssets #ConsolidationPhase #CentralBanks #MonetaryPolicy #MonetarySystem #FinancialMarkets #MacroTrends #InvestmentInsights #MarketAnalysis #AustrianEconomics #20Years20Threads #IGWT26 #AnniversarySeries