The 2017 edition marked a clear departure from earlier formats. For the first time, the report combined:

A coherent macroeconomic framework

Scenario-based forecasting

Enhanced visual storytelling

This evolution elevated the IGWT report from a traditional research publication to a comprehensive macro framework, connecting monetary policy, financial markets, and gold in a systematic way.

![]()

![]()

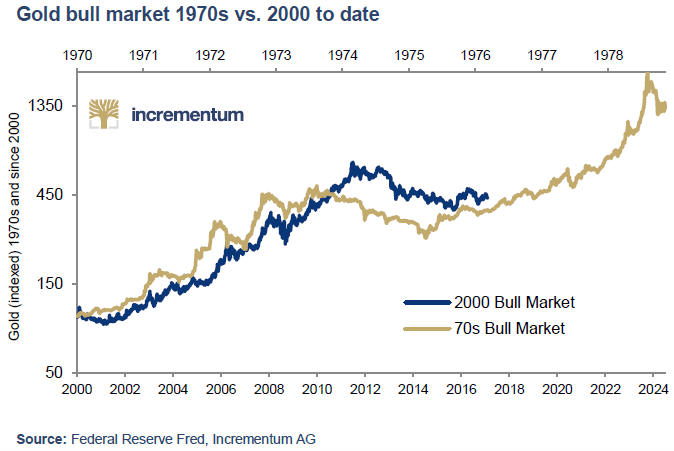

By 2017, the gold market was still dealing with the aftermath of the 2011 peak.

Gold had reached its all-time high of USD 1,921 in September 2011, while silver had peaked earlier that year, in April. What followed was a prolonged and psychologically taxing bear market that bottomed in late 2015.

Although prices had stabilized and partially recovered by 2016, the market entered a phase of consolidation. Therefore, the central question at the time was not whether gold would recover, but when.

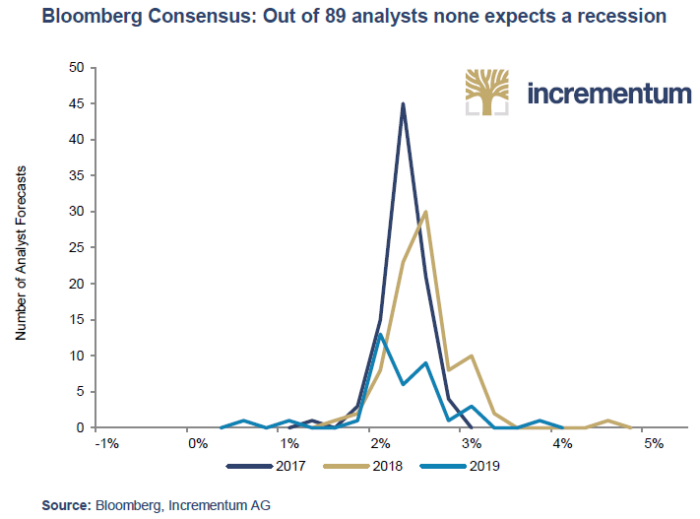

One of the most memorable insights of the report captured the prevailing sentiment:

“One almost gets the impression that the possibility of a recession is completely disregarded and treated as though it were a black swan.”

This observation reflected a broader complacency across financial markets. In spite of being hardly absent, of course, financial and economic risks were systematically underestimated.

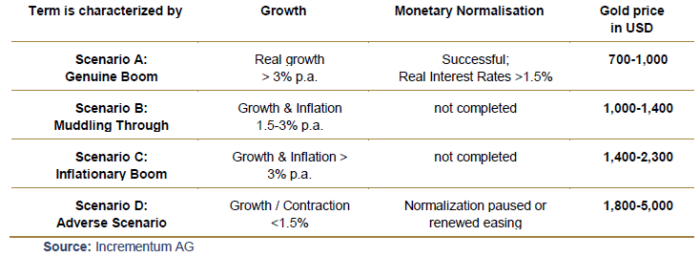

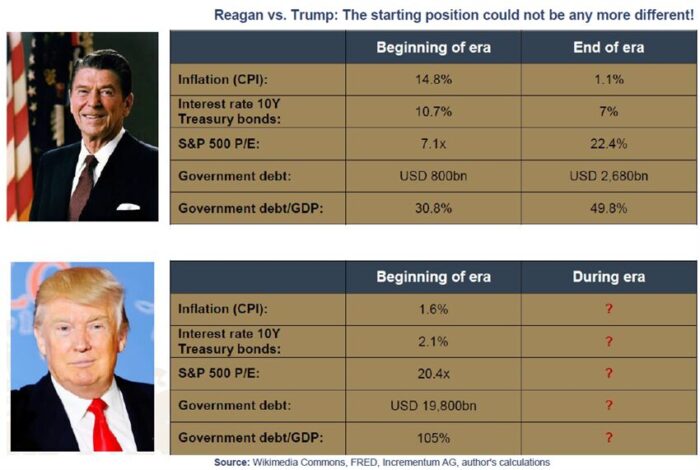

In contrast to earlier editions, the 2017 report placed greater emphasis on scenario analysis. Having said this, we developed four potential macroeconomic paths for the duration of Donald Trump’s presidential term. At any rate, we felt inclined to believe the bear would enter hibernation, making way for the bull to charge again soon.

Among the fancied path, Scenario C – characterized by strong growth and rising inflation – proved particularly relevant. Under this scenario, we projected a gold price range of USD 1,400 to USD 2,300 by early 2021.

In reality, gold ended Trump’s first term at USD 1,855.80, which was almost exactly in the middle of that range. This outcome highlights an important lesson: while precise timing is elusive, robust frameworks can remain highly effective.

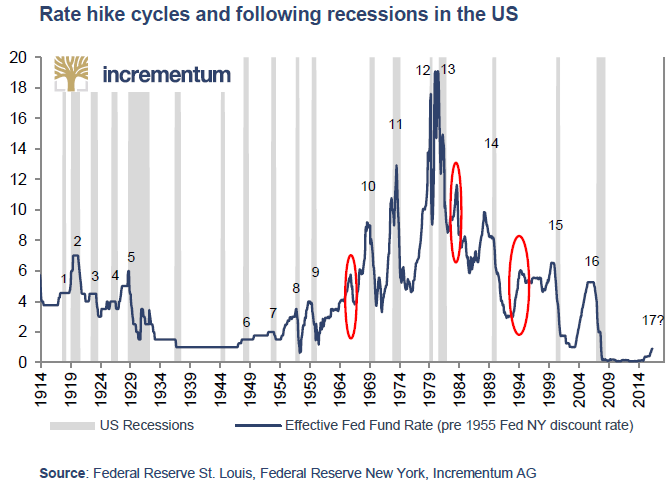

At first glance, the macroeconomic environment of 2017 appeared stable. However, a closer look revealed growing structural imbalances:

Central banks continued to dominate financial markets

Global debt levels expanded further

Real interest rates remained the key driver of gold

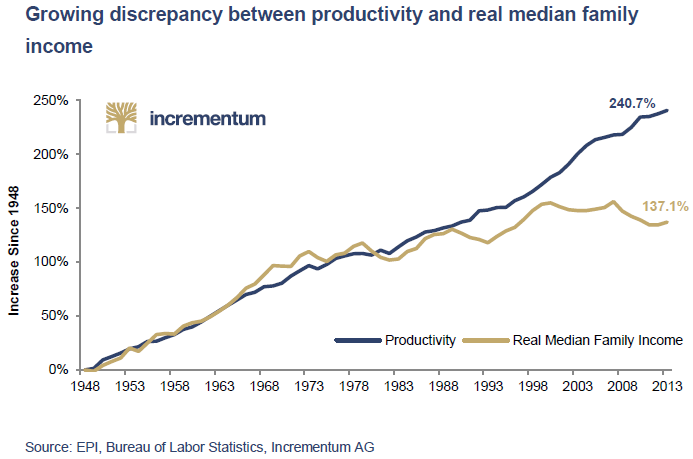

To make matters worse, the underlying economy showed clear signs of weakness:

Economic growth remained subdued

Productivity gains were limited

The system became increasingly dependent on continuous credit expansion

In essence, markets were pricing perfection, while fragility quietly intensified.

One of the most striking diagnoses of the 2017 report was the concept of the “zombie economy.”

Fundamentally, years of ultra-low and even negative interest rates had allowed unproductive firms to survive far longer than they otherwise would have.

In the end, this environment led to:

Capital misallocation

Suppressed productivity

Distorted price signals

Rather than resolving those structural weaknesses, monetary policy had effectively postponed them.

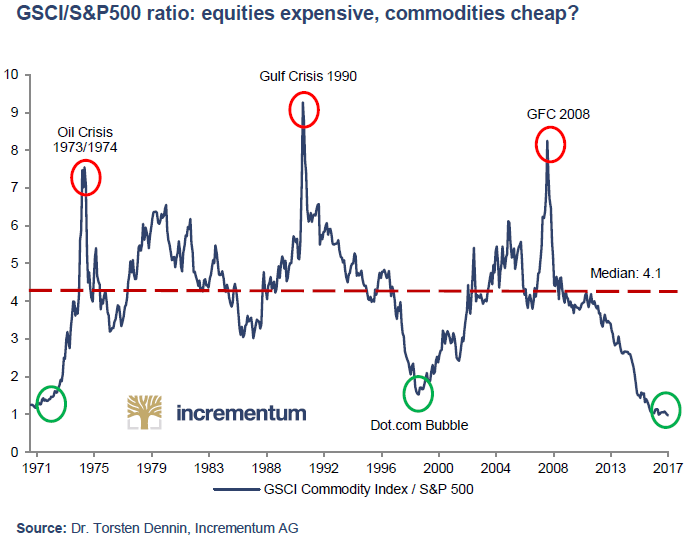

The unprecedented expansion of central bank liquidity had profound consequences for asset prices. Financial assets, particularly equities, benefited disproportionately from this liquidity surge, leading to what had been described as an “Everything Bubble.”

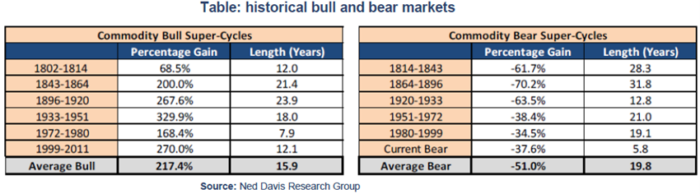

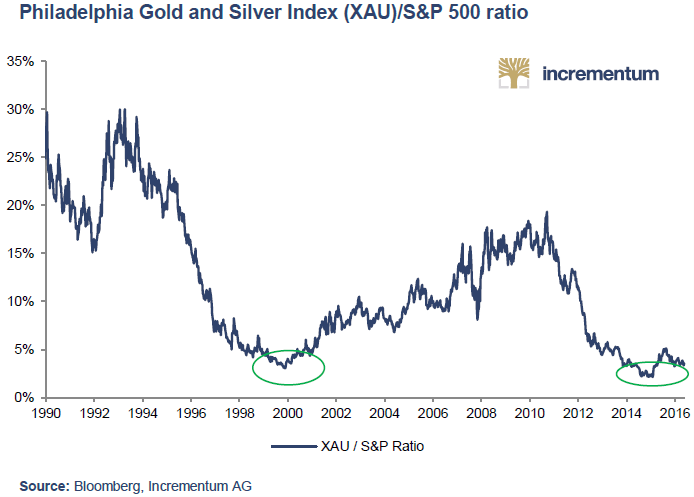

Be that as it may, this inflation of financial assets was not uniform. Unlike stocks and bonds, along with virtually all the real, physical asset segments, commodities, au contraire, remained deeply undervalued. Demonstrably, the GSCI/S&P 500 ratio reached multi-decade lows, highlighting a historically significant divergence between real assets and financial assets.

Needless to say, such divergences are rarely permanent. In truth, they often signal turning points in the broader market cycle.

The report also addressed the political consequences of this economic environment.

Catching every mainstream pundit and cosmopolitan liberal elitist by surprise, the election of Donald Trump as President of the US didn’t come out of the blue. As we argued in the report, this momentous development pertained to a broader trend that also included the victory of the Brexit vote a few months prior.

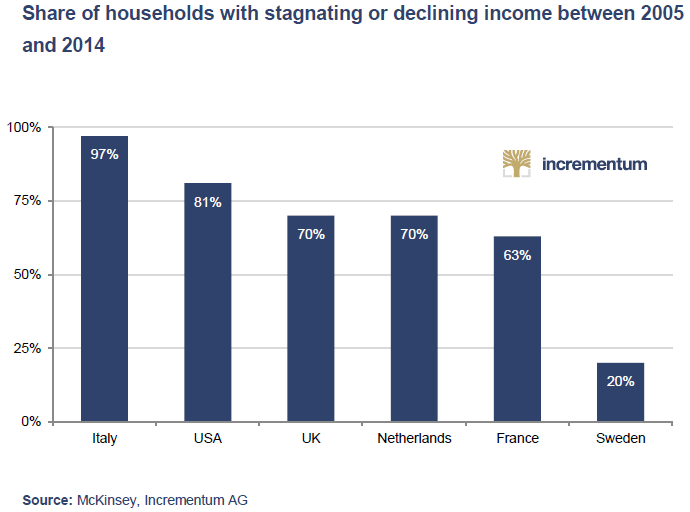

In short, across developed economies, large segments of the population had experienced stagnating or declining real incomes in the years following the Global Financial Crisis.

Undoubtedly, this lack of recovery fueled a growing backlash against established political and economic institutions. In this context, populism emerged not as a cause, but as a consequence of deeper structural imbalances.

The report also examined Donald Trump’s stance on monetary issues. Although he was not a traditional “gold advocate,” he viewed a strong US dollar as a symbol of economic strength, even if it reduced export competitiveness.

More importantly, the report identified an emerging global trend:

💱 A gradual move away from US dollar dominance.

In addition to being driven by emerging markets seeking greater monetary independence, some influential voices within the United States questioning the long-term costs of maintaining the dollar’s reserve currency status made it seem that the writing was on the wall that this macro phenomenon was going to be fulfilled sooner or later.

Apparently, it was much later, if at all, that the US dollar is going to cease to be the global hegemonic reserve and medium of exchange.

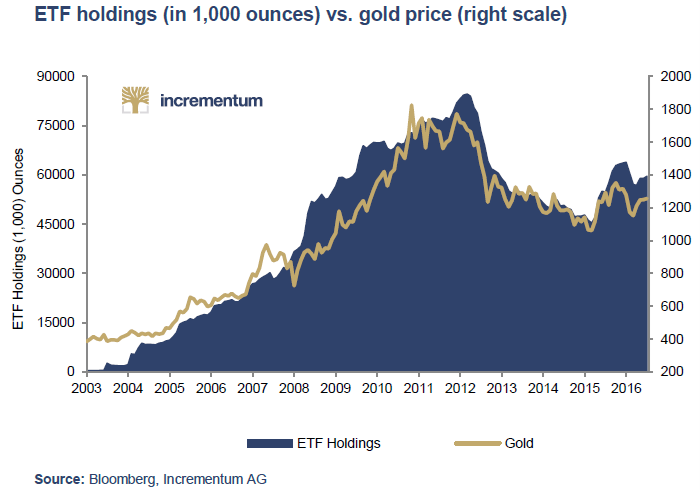

Despite the absence of dramatic price movements, underlying demand for gold began to strengthen. Indicators pointed to:

Rising ETF inflows

Improving sentiment

Renewed institutional and retail interest

Hence, these developments suggested that the foundation for the next bull market phase was already being laid, albeit quietly.

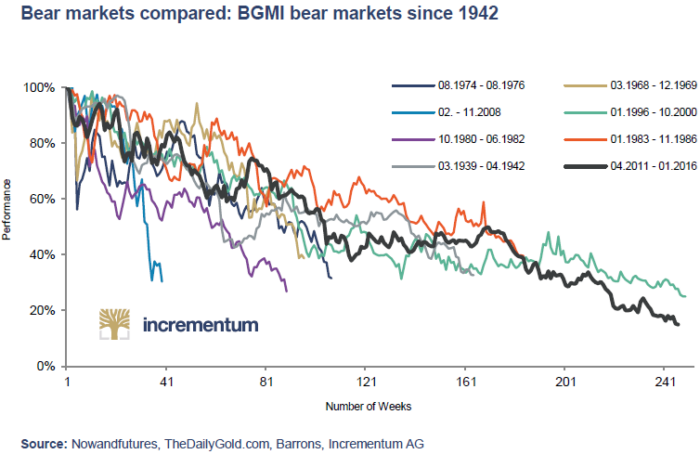

By the time the 2017 report was published, the bear market in gold mining equities had already ended in early 2016.

At any rate, the recovery phase proved to be prolonged:

Gold mining stocks only broke out decisively in 2020

Silver mining equities required even more time, achieving a breakout only in 2025

This lag underscores an important characteristic of mining equities: although they tend to respond with delay, they do so while amplifying the rally upwards once momentum builds.

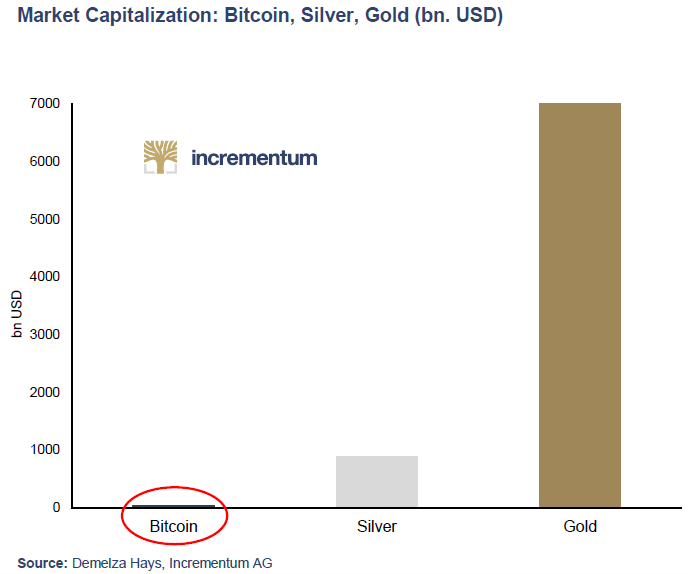

For the first time, the IGWT report included a dedicated discussion of Bitcoin. The central question was whether Bitcoin could be considered “digital gold” or whether it represented a speculative phenomenon better described as “fool’s gold.”

At the time, the answer was far from clear. Nevertheless, the inclusion of Bitcoin reflected an important development: the emergence of alternative monetary assets in a rapidly evolving financial landscape.

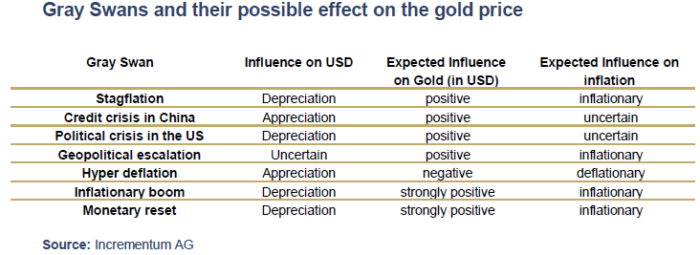

Another conceptual innovation of the report was the introduction of “gray swans.”

Contrary to black swans, which are defined as completely unpredictable events, gray swans are risks that are known but underestimated.

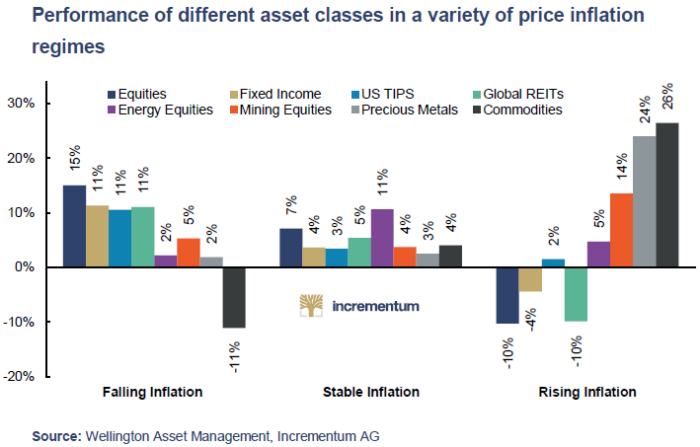

The report linked this concept directly to inflation regimes and asset performance:

In disinflationary or deflationary environments, bonds and equities tend to outperform

In moderate inflation regimes, equities typically dominate

In high inflation or stagflationary environments, commodities and gold outperform

Unsurprisingly, gold performs particularly well when inflation exceeds expectations. This is precisely the type of scenario often triggered by gray swan events.

A particularly noteworthy novelty included in the 2017 report was the introduction of the International Shadow Gold Price (ISGP).

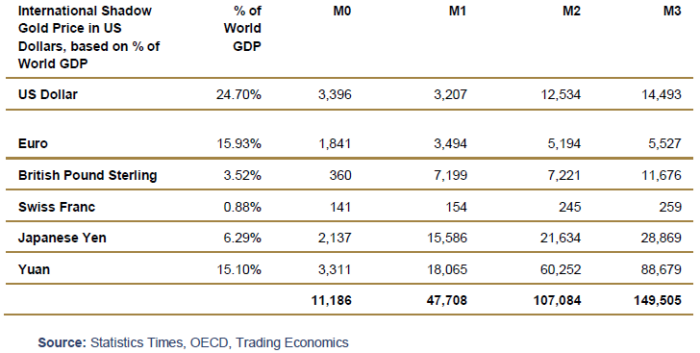

Based on six major currencies – the US dollar, euro, British pound, Swiss franc, Japanese yen, and Chinese yuan – the ISGP estimates the theoretical gold price required to fully back monetary aggregates.

Strikingly, the broader the monetary aggregate considered (from M0 to M3), the higher the implied gold price. Accordingly, this framework provided a powerful illustration of the extent of monetary expansion, along with the potential revaluation of gold in a fully backed system.

The 2017 edition of the In Gold We Trust report did not coincide with a dramatic market breakout. Instead, its importance lies in its clarity and foresight.

Notwithstanding, it identified:

The structural distortions caused by prolonged monetary easing

The emergence of a “zombie economy”

The growing divergence between financial assets and real assets

The early signs of renewed gold demand

The rise of new monetary competitors such as Bitcoin

The increasing relevance of underestimated systemic risks

Looking back today, it is evident that many of the defining themes of the 2020s were already present in 2017. Thus, this edition, in hindsight, feels less like a culmination and more like a beginning.

📘 Head over to the Archive to read the full report.

#20Years20Threads #InGoldWeTrust #GoldReport #GoldDemand #GoldInvesting #SilverMarket #MiningStocks #CentralBanks #DebtCycle #SystemicRisk #EverythingBubble #Commodities #HardAssets #SoundMoney #AustrianEconomics #Bitcoin #DigitalGold #DeDollarization #InflationHedge #WealthPreservation #MacroTrends #InvestmentInsights #IGWT17 #AnniversarySeries