The 2016 report represented a milestone, not just for its insights, but for its legacy.

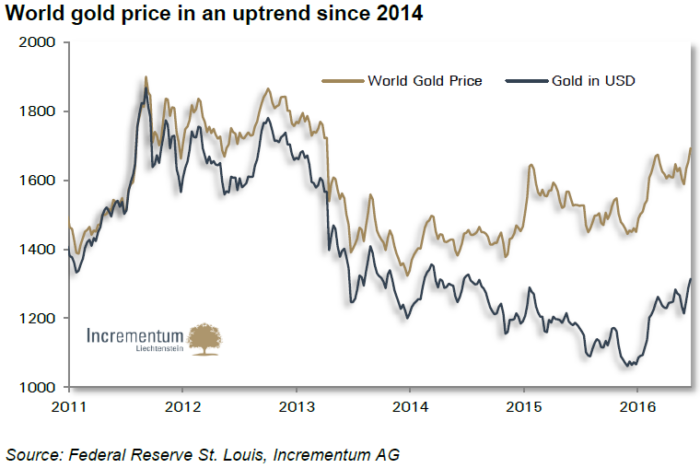

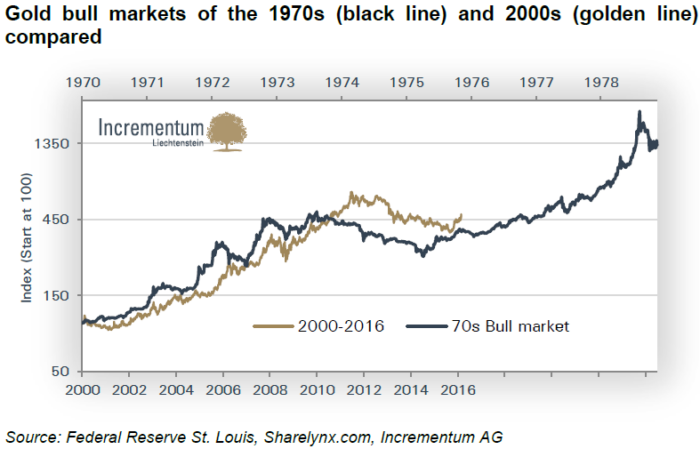

Five years after gold peaked at USD 1,921 in September 2011, the market was still recovering from a deep and psychologically draining bear phase. Be that as it may, beneath the surface, the foundations of a new cycle were already being laid.

What made this edition particularly powerful is that it recognized this transition in real time.

After years of declining prices, gold staged a remarkable comeback in the first quarter of 2016, recording its strongest quarterly performance in three decades.

This rebound was not random. Plainly, it was driven by two key forces:

Falling real interest rates

Growing doubts about global economic growth

As confidence in the effectiveness of post-crisis monetary policy waned, gold began to reassert itself as a strategic asset.

By 2016, it was becoming increasingly clear that:

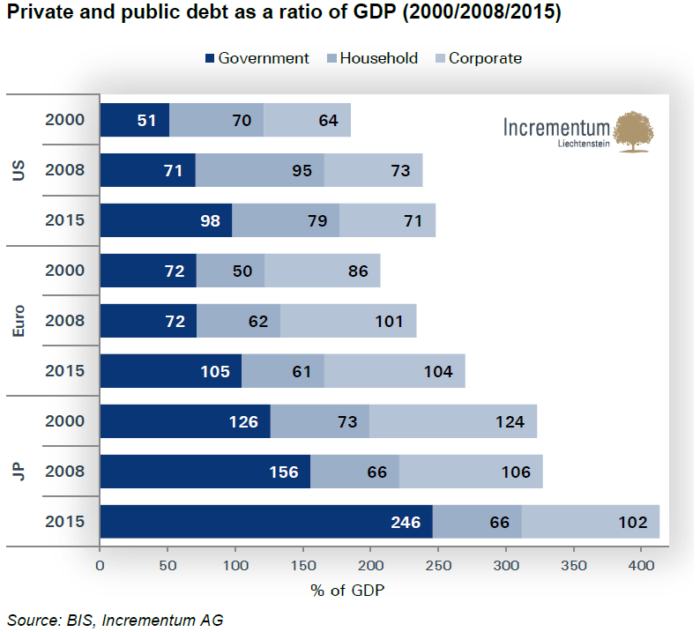

Post-Global Financial Crisis policies had failed to restore robust growth

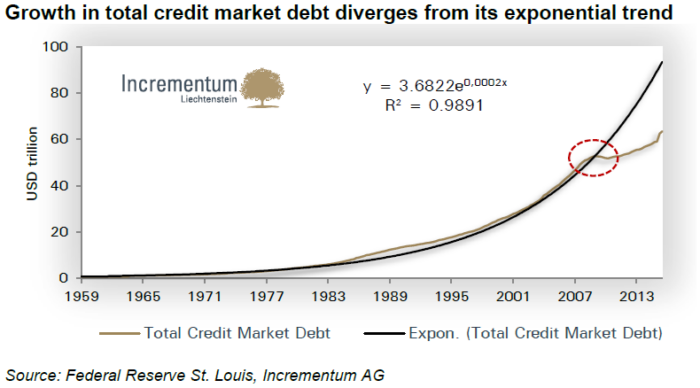

Global debt levels continued to expand relentlessly

Central banks were approaching the limits of their policy tools

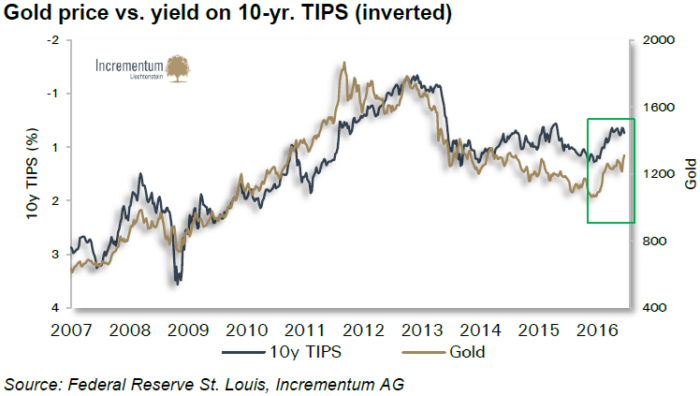

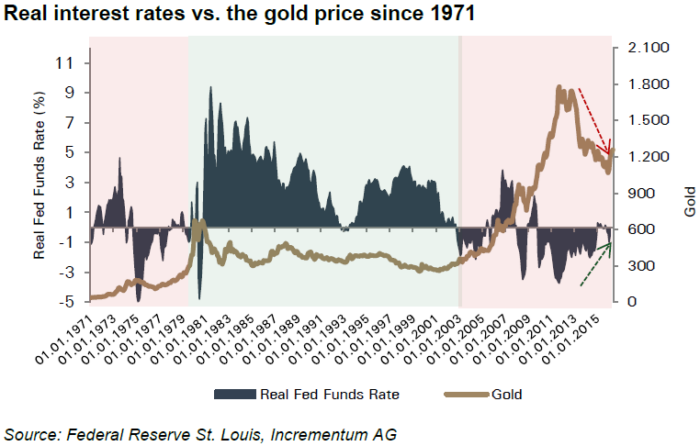

In this environment, gold once again demonstrated its sensitivity to real interest rates, moving inversely as expected.

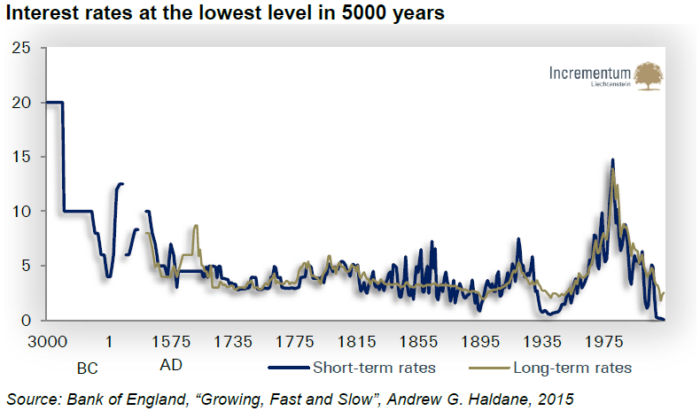

Perhaps the most defining feature of 2016 was the rise of negative interest rate policies (NIRP).

At one point, more than USD 8 trillion worth of bonds traded with negative yields, while interest rates reached levels not seen in millennia.

This led to one of the most memorable insights of the report:

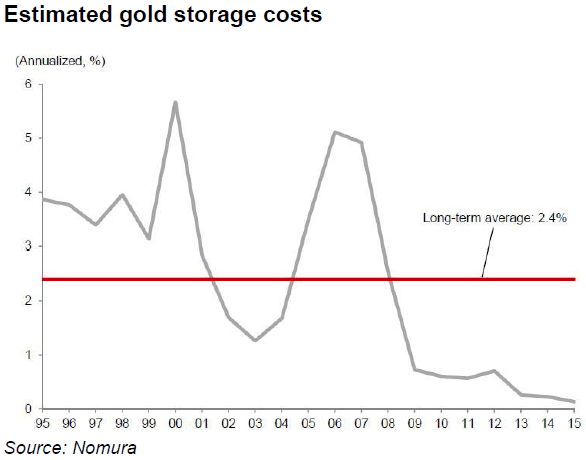

“It used to be said that gold doesn’t pay interest, now it can be said that it doesn’t cost interest.”

In a world where holding bonds guaranteed losses, gold’s opportunity cost effectively vanished.

The report described central banks as being caught in a structural dilemma:

Raising rates risked destabilizing an overleveraged system

Keeping rates low encouraged further distortions and asset bubbles

In practice, policymakers consistently chose the latter: prolonging the era of ultra-loose monetary policy.

Indeed, this dynamic would define the macro landscape for years to come.

With conventional tools losing effectiveness, previously radical ideas entered mainstream discussion. Among them, helicopter money, which stands for direct transfers from governments to consumers, was on top of the list.

While intended to stimulate demand, such policies carried significant risks, particularly the potential for uncontrolled inflation.

Needless to say, the seeds of future monetary experimentation were clearly visible.

Moreover, 2016 brought attention to structural issues within precious metals markets.

Notably, Deutsche Bank settled lawsuits related to gold and silver price manipulation, highlighting concerns about transparency and price discovery mechanisms.

For many investors, this reinforced the importance of understanding the market structure, besides analyzing the typical fundamentals.

Beyond economics, 2016 was a year of profound political change.

🇬🇧 The Brexit referendum signaled a rejection of European integration

🇺🇸 The rise of “Trumpmania” reflected growing dissatisfaction with the status quo

This populist wave challenged the prevailing neo-liberal, globalist framework and introduced a new layer of uncertainty into financial markets.

Historically, such periods of instability tend to strengthen gold’s appeal as a safe haven.

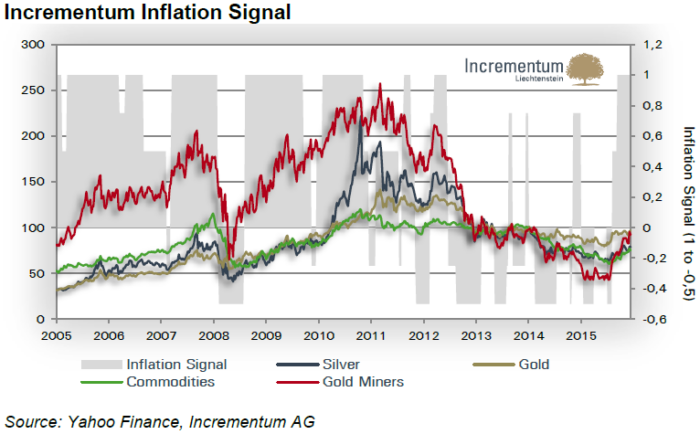

At any rate, the Incrementum Inflation Signal indicated that inflationary pressures were beginning to build.

Unquestionably, this raised major implications:

Hard assets were likely to outperform

Gold, silver, and mining equities were entering a favorable phase

In hindsight, these signals marked the early stages of a broader macro shift.

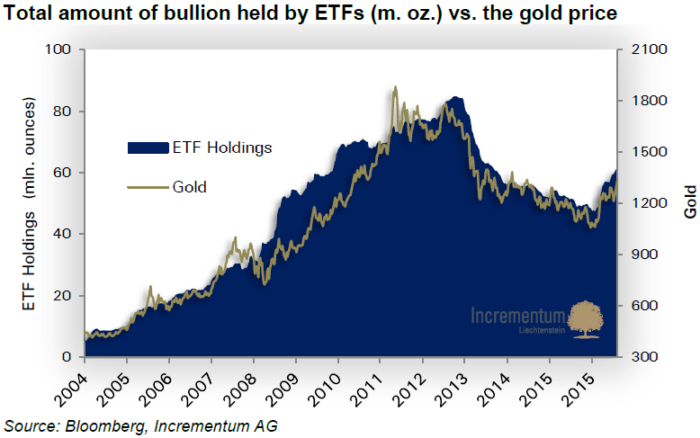

As gold prices began to rise, investor behavior followed:

ETF holdings increased

Long positions expanded

Capital rotated back into safe haven assets

These early inflows suggested that institutional investors were already positioning for a new cycle.

Looking back today, it is evident that many of the defining characteristics of the “Golden Decade” – a concept formalized years later – were already present in 2016:

Renewed investor interest

Strengthening price momentum

Supportive macroeconomic conditions, albeit at a more moderate level

Even if it was not yet widely recognized, the shift had begun.

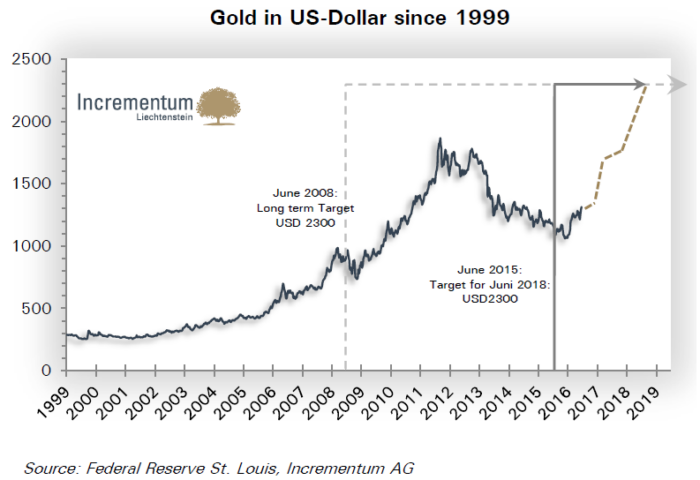

The report reiterated a long-term target of USD 2,300 per ounce for gold, originally expected by June 2018.

While the timing proved optimistic, the underlying thesis remained intact.

Ultimately, gold reached this level in 2024, validating the long-term perspective.

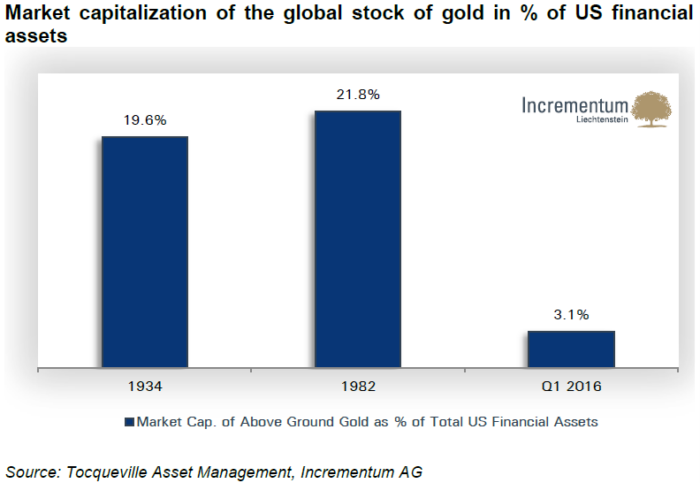

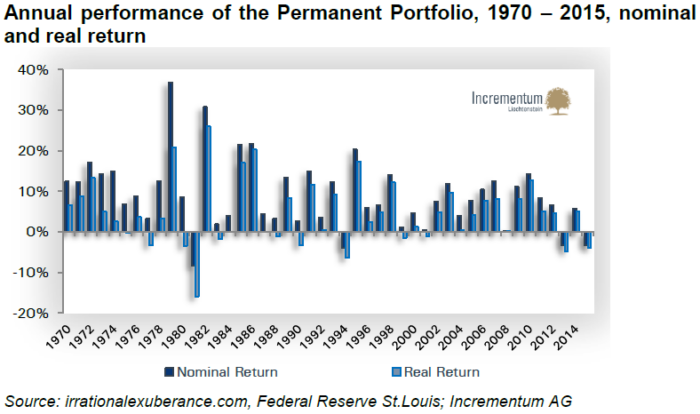

With trillions of dollars in negative-yielding bonds, gold’s role as a non-debt-based store of value became increasingly important.

In this context, the report revisited the concept of the Permanent Portfolio, developed by Harry Browne in the 1970s.

Designed to perform across all economic environments, this strategy emphasized resilience over prediction.

Interestingly, the ideas presented in 2016 would later influence the development of the “New 60/40 Portfolio”, introduced in the 2024 edition as part of the New Gold Playbook.

This evolution highlights a key theme of the IGWT series: adapting timeless principles to a changing macro environment.

The 2016 edition of the In Gold We Trust report captured a pivotal moment in financial history.

It marked the transition:

From bear market to recovery

From positive to negative rates

From policy confidence to systemic doubt

From globalization to rising populism and protectionism

Most importantly, it demonstrated that gold’s relevance is cyclical, although its importance is structural.

📘 Head over to our Content Vault to read the full report.

#20Years20Threads #InGoldWeTrust #GoldReport #GoldInvesting #SafeHaven #InflationHedge #BullMarket #BearMarket #RealRates #CentralBanks #MonetaryPolicy #DebtGrowth #NegativeRates #NIRP #FinancialRepression #HelicopterMoney #HardAssets #SilverRally #MiningStocks #GoldETF #FundFlows #PortfolioStrategy #AssetAllocation #PermanentPortfolio #NewGoldPlaybook #IGWT24 #Brexit #Trump2016 #Populism #Geopolitics #MarketManipulation #SoundMoney #EconomicHistory #MacroTrends #InvestmentInsights #MarketAnalysis #AustrianEconomics #IGWT16 #AnniversarySeries