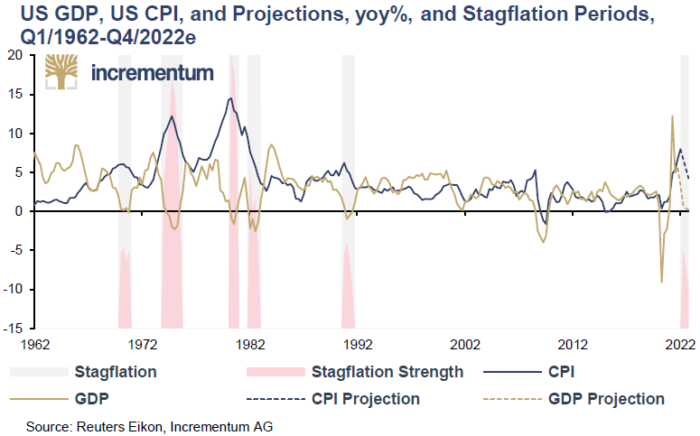

The report framed the macro environment through two dangerous forces:

🐺 Inflation

🐻 Recession

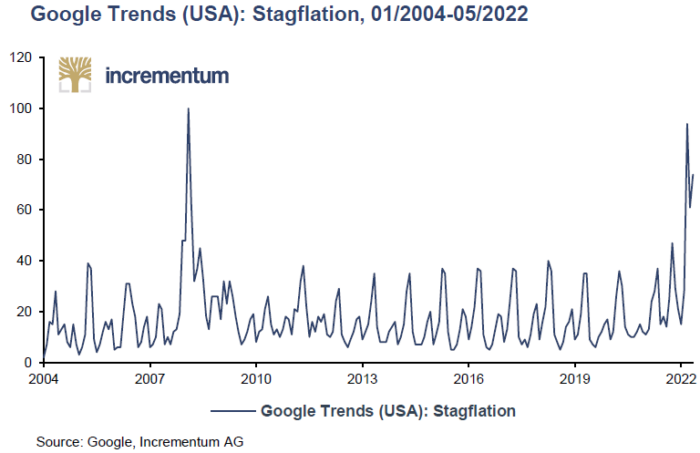

Together, they formed the defining monster of the decade: Stagflation 2.0

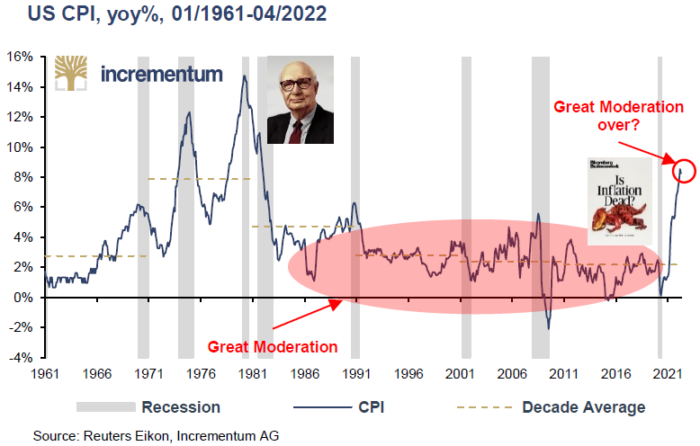

Unlike the temporary inflation scares of previous years, this inflationary wave was structural. Deglobalization, commodity shortages, years of monetary excess, and geopolitical fragmentation were fundamentally changing the economic environment.

Back then, most economists still expected inflation to fade quickly. We argued the opposite.

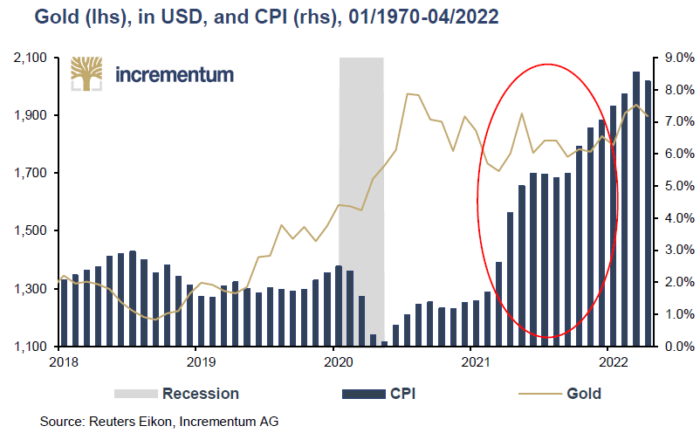

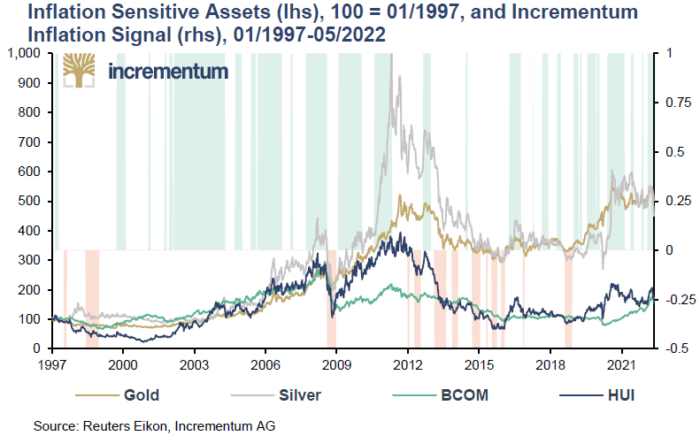

One of the biggest puzzles entering 2022 was gold’s surprisingly subdued performance during 2021.

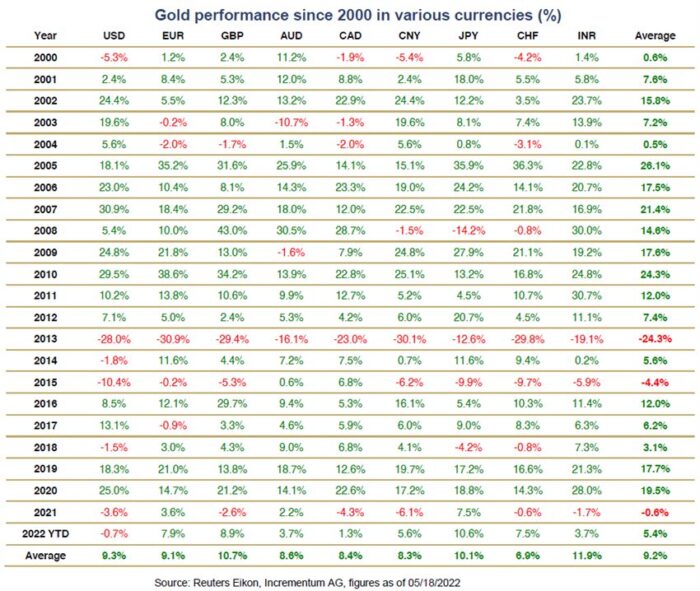

Despite rapidly rising inflation, gold failed to rally decisively. After extraordinary gains of +18.9% in 2019 and +24.6% in 2020, the gold market entered a consolidation phase. The strong US dollar, the speculative mania surrounding crypto assets, and widespread confidence in the “transitory inflation” narrative temporarily weakened investor enthusiasm for gold.

Understandably, many gold investors became deeply frustrated.

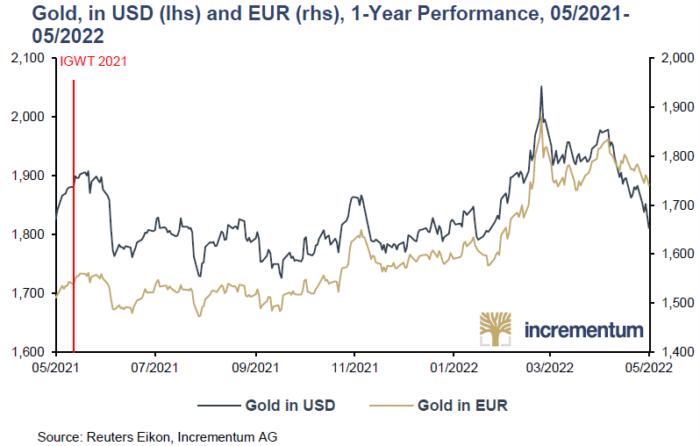

Notwithstanding, the secular bull market remained intact. Gold had already anticipated the inflation surge through its powerful rally between 2018 and 2020. By early 2022, momentum returned. On March 8, 2022, gold reached USD 2,070 – only slightly below the August 2020 all-time high of USD 2,075 – while posting its highest quarterly close ever during Q1 2022.

Importantly, the IGWT 2022 became only the second edition released after gold had definitively surpassed the 2011 peak, confirming the birth of a new secular bull market.

One quote from the report perfectly captured the atmosphere of 2022:

“A solidification of inflation has definitely taken place. Inflation is no longer an exotic, much less a “transitory”, topic but has arrived in the mainstream. This part of our last year’s forecast was therefore correct, but the gold price developed rather disappointingly in view of the strong increase in inflation. Towards the beginning of the year, frustration was still high among gold investors, with many gold bulls questioning their confidence in gold.”

Importantly, the report emphasized that wages were rising because inflation had already spread throughout the system, not the other way around.

Essentially, labor shortages, stimulus distortions, welfare programs introduced during the pandemic years, and rising living costs reinforced inflation persistence. Workers demanded higher wages to compensate for declining purchasing power, thereby broadening the inflationary spiral further.

Indubitably, inflation had become embedded socially, economically, and politically.

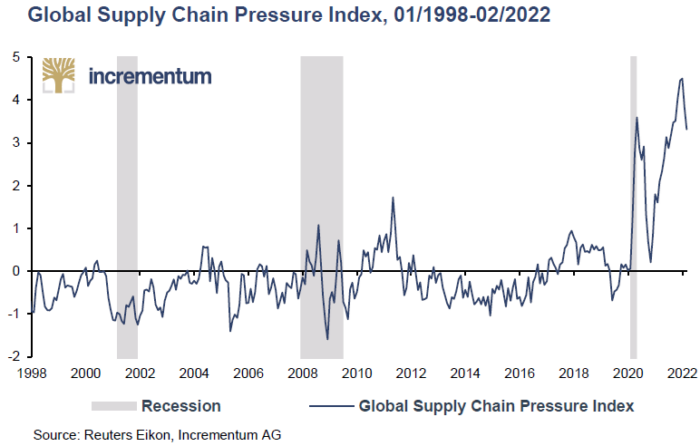

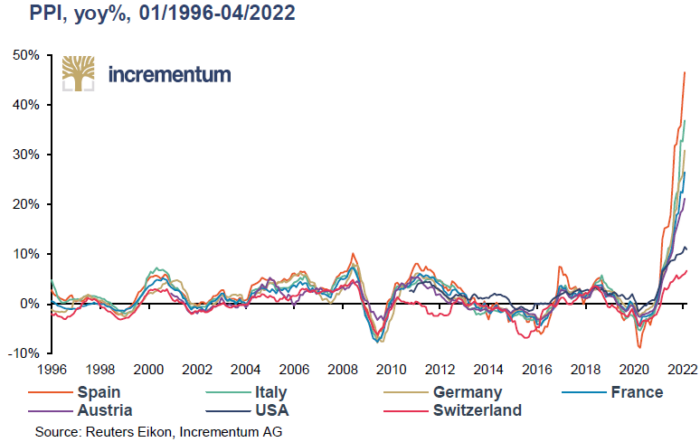

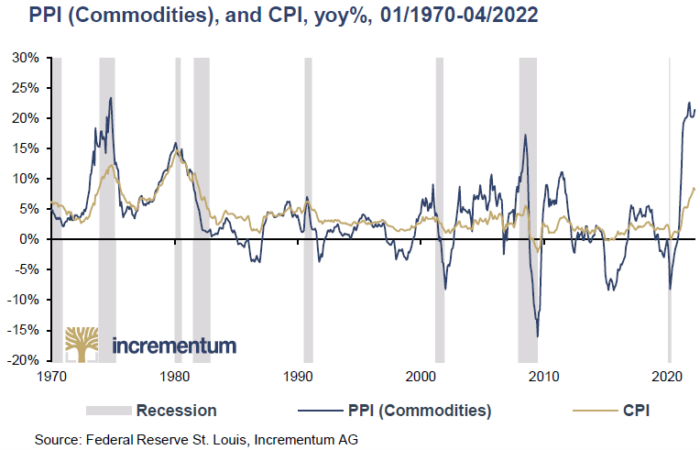

Even after lockdowns formally ended, global trade and supply chains remained heavily disrupted.

Shipping bottlenecks persisted. Manufacturing shortages lingered. Energy markets became increasingly unstable. The world was still suffering from the aftershocks of the pandemic-era shutdowns when the Russian invasion of Ukraine dramatically intensified the situation.

The war accelerated:

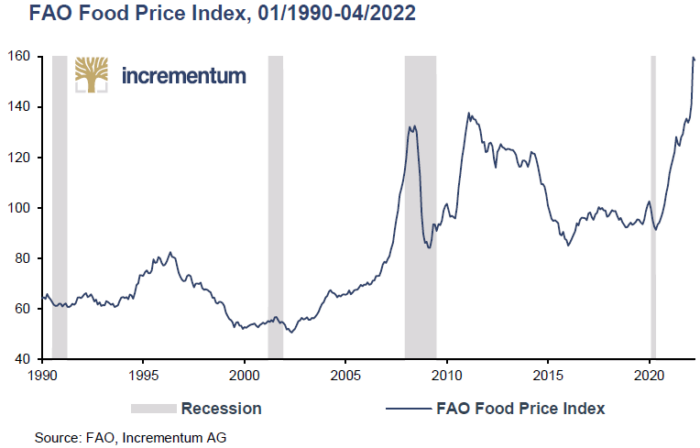

⚡ Energy shortages

🌾 Food insecurity

⛽ Commodity inflation

🌍 Geopolitical fragmentation

Markets suddenly rediscovered supply-side inflation. Intriguingly, this was something central banks were entirely unprepared for after decades dominated by demand-side concerns.

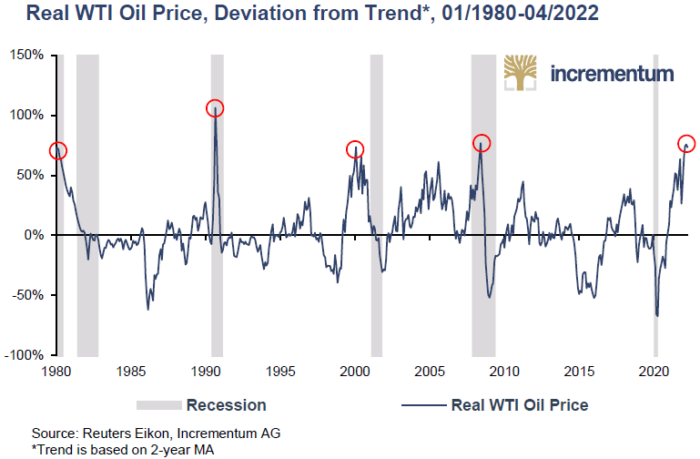

The report warned that years of underinvestment in oil and gas production had collided with sanctions, embargoes, and ESG-driven capex restraint.

In fact, JP Morgan even warned oil prices could potentially surge toward USD 185/barrel.

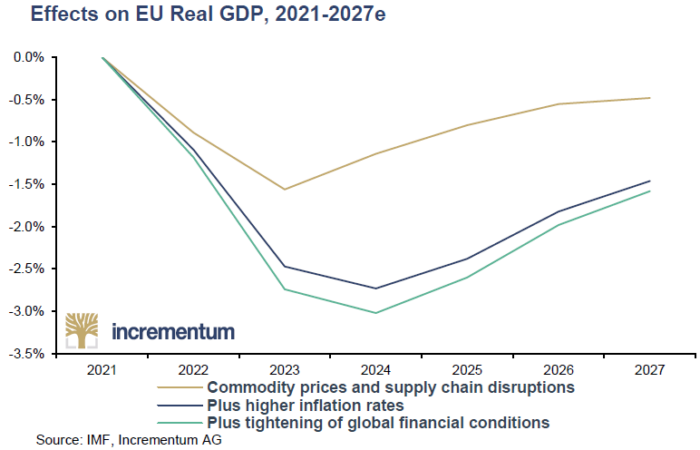

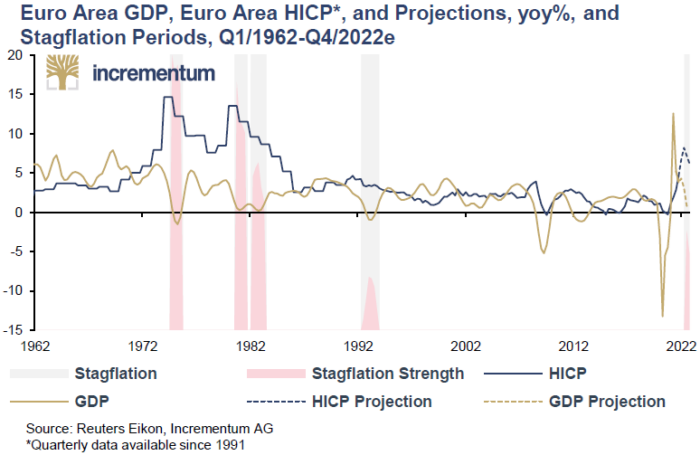

Meanwhile, Europe entered a stagflationary environment characterized by:

Weak growth

Sticky inflation

Chronic energy vulnerability

Looking back from 2026, that diagnosis proved largely correct.

However, the 2022 energy crisis also taught an important lesson: markets adapt. Supply chains gradually adjusted, energy production recovered, and oil prices normalized faster than many expected.

This remains highly relevant today as markets evaluate the economic consequences of the current Persian Gulf tensions.

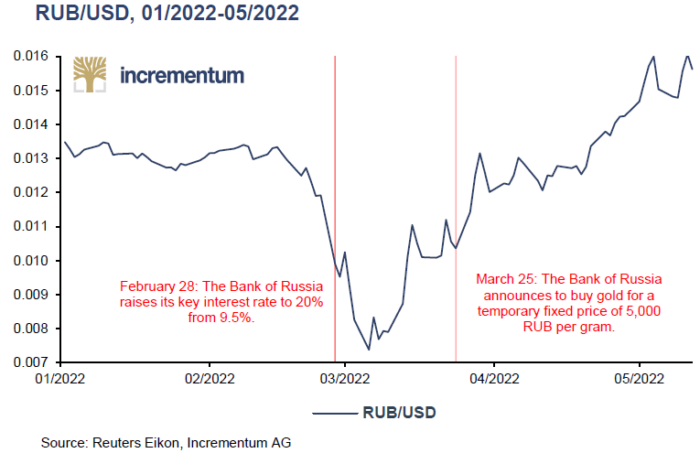

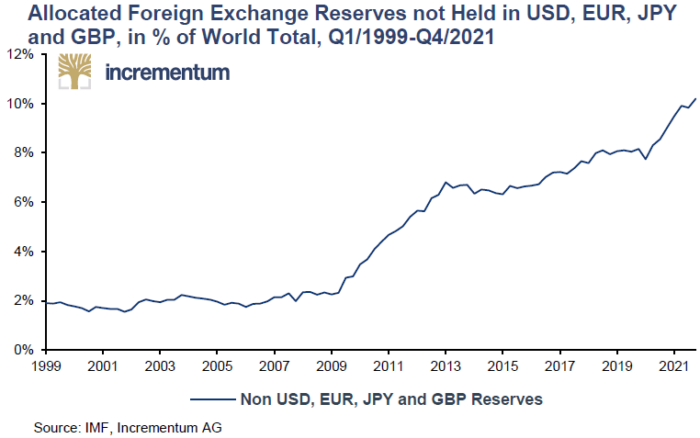

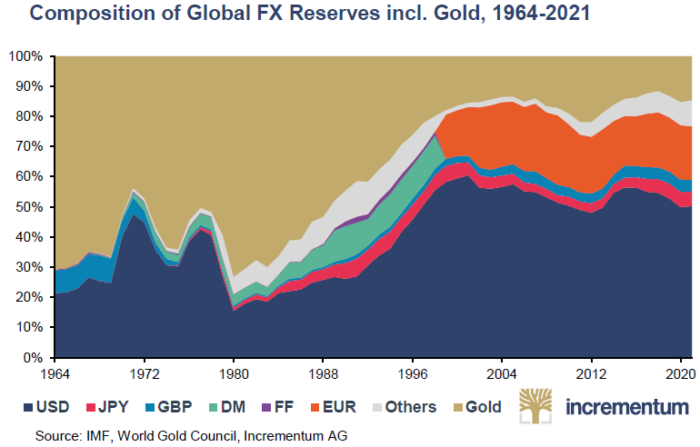

One of the most important geopolitical developments of the decade emerged after the freezing of Russia’s foreign exchange reserves.

Over USD 300 billion became effectively inaccessible overnight. That event shattered a foundational assumption of the post-Bretton Woods system: sovereign reserves were no longer politically neutral.

As a result, many countries, especially in the Global South, began reconsidering their dependence on US dollar-based reserves. Suddenly, gold looked very different.

The report emphasized that gold possesses several unique characteristics:

No counterparty risk

No default risk

No political liability

In an increasingly fragmented geopolitical environment, these properties became strategically important again.

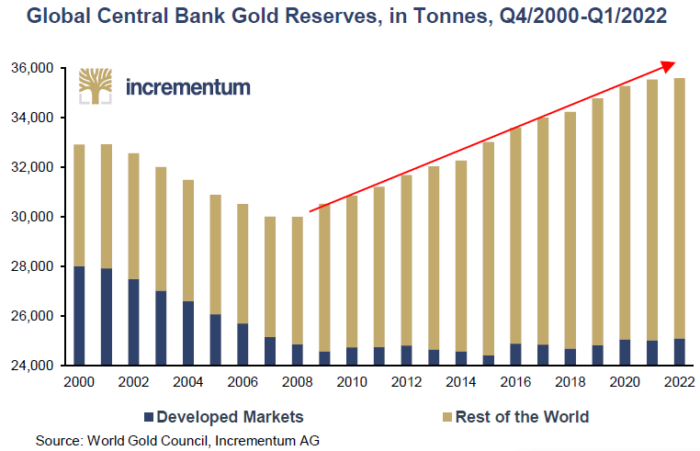

Central banks accelerated gold purchases after 2022, particularly across emerging markets such as China, India, and Russia.

Thus, gold was increasingly viewed not merely as a commodity, but as a neutral reserve asset and monetary anchor.

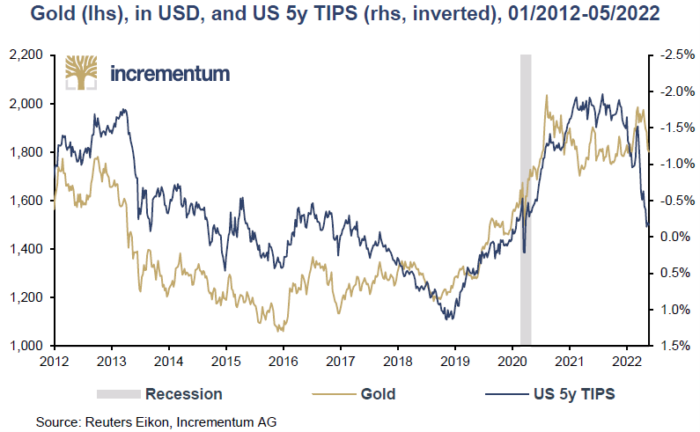

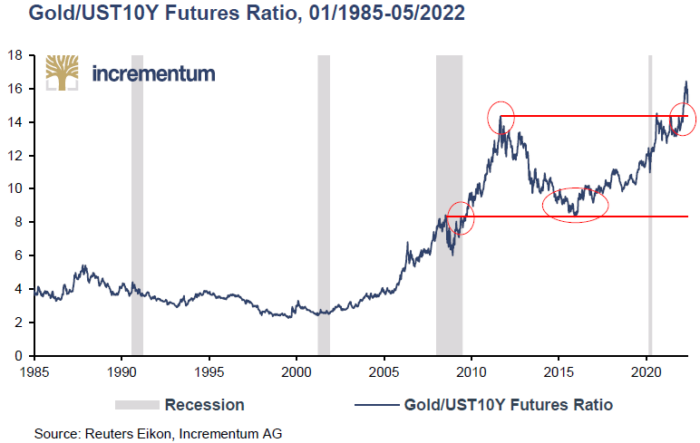

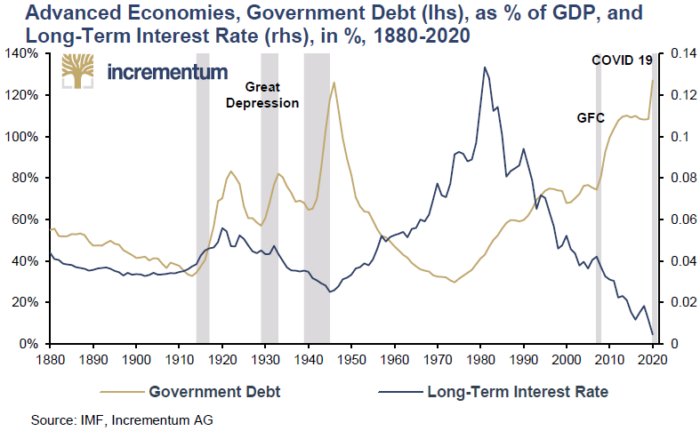

Historically, rising real interest rates tended to weaken gold prices. However, in 2022, that long-standing inverse relationship was obviously breaking down.

Despite sharply rising real yields, gold continued strengthening. This signaled that markets were beginning to reassess the credibility of sovereign debt itself.

Several forces contributed to this shift:

Exploding government debt levels

The weaponization of reserve assets

Rising skepticism toward sovereign bonds

Central bank diversification into gold

This was one of the clearest signs that the global monetary regime itself was changing. In truth, gold was increasingly being remonetized globally.

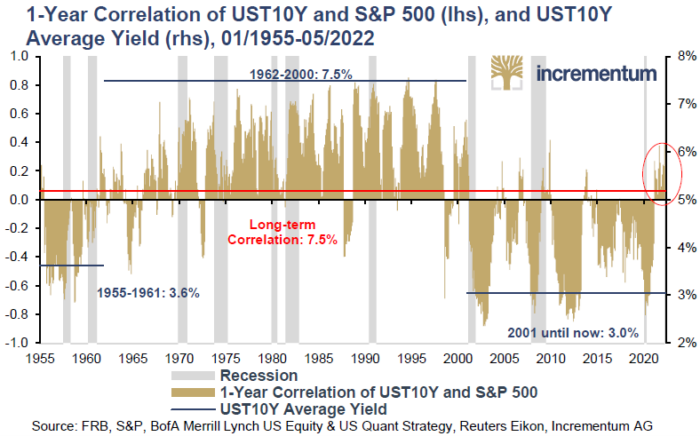

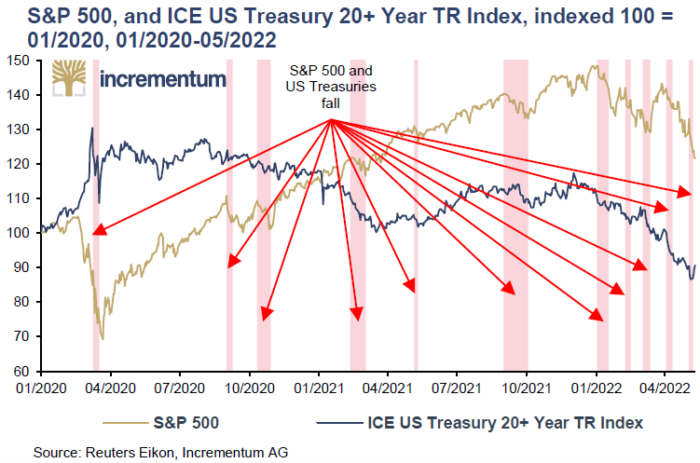

For decades, the traditional 60/40 portfolio relied on a negative correlation between stocks and bonds.

But in 2022, both asset classes fell simultaneously.

The report argued that positive stock-bond correlation could permanently damage the typical diversification model. Therefore, the traditional 60/40 portfolio model began failing as stocks and bonds declined simultaneously.

Patently, the old investment playbook was breaking down.

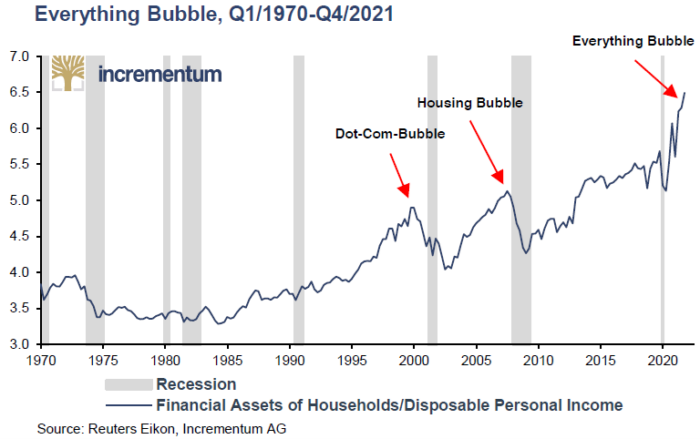

Furthermore, years of ultra-loose monetary policy had created extreme distortions across the financial system.

The report warned that Fed tightening would collide with:

Extreme valuations

Zombie companies

Excess leverage

Overfinancialization

The age of easy liquidity was ending.

As the Federal Reserve simultaneously pursued rate hikes, quantitative tightening, and the end of QE, the Everything Bubble entered a dangerous phase. Mean reversion was returning across the financial system.

Importantly, no asset class appeared immune. Equities, sovereign bonds, cryptocurrencies, and speculative growth assets all came under pressure.

Central banks suddenly confronted an impossible balancing act:

Fighting inflation

Supporting economic growth

Maintaining debt sustainability

They could not successfully achieve all three simultaneously.

This monetary policy trilemma became one of the defining themes of the report and remains highly relevant today. The longer inflation persisted, the more likely central banks would ultimately prioritize financial stability and debt sustainability over strict inflation control.

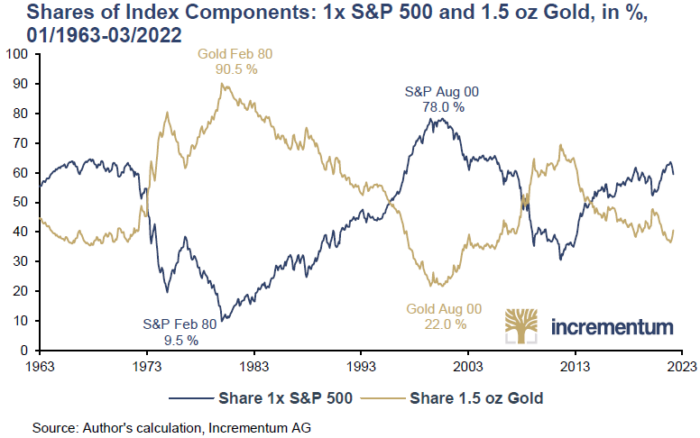

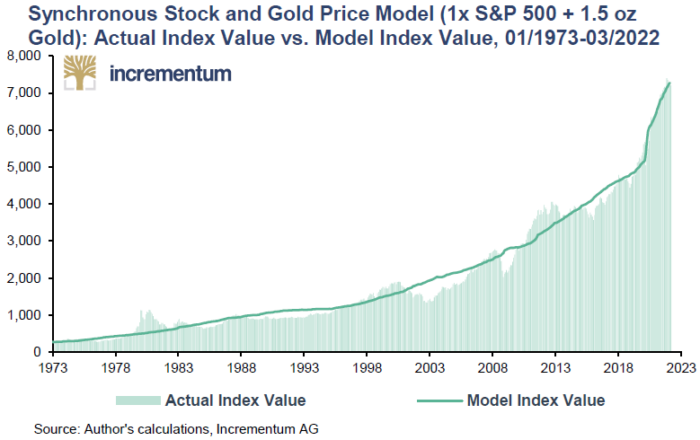

One of the most important conceptual frameworks introduced in IGWT 2022 was the:

📊 Synchronous Equity and Gold Price Model (SEGPM)

The core insight was simple, albeit profound. Ultimately, liquidity drives both equities and gold over time.

The report demonstrated that a combined index consisting of the S&P 500 plus 1.5 ounces of gold tracked US M2 money supply more closely than either asset individually.

Zooming in, investor confidence merely determined allocation preferences between the two. In other words, liquidity remained the master variable governing financial markets.

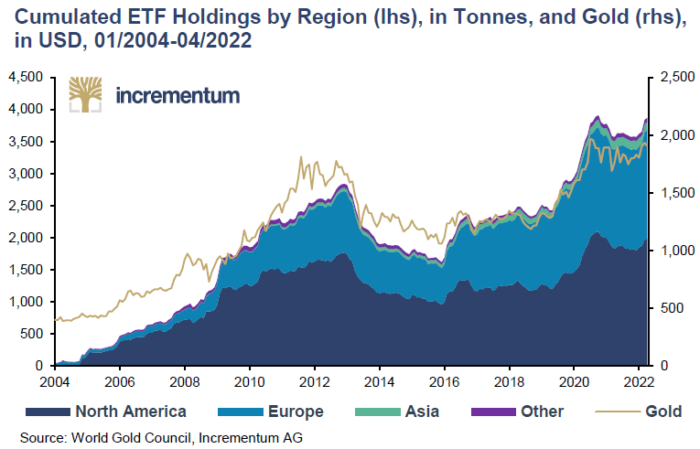

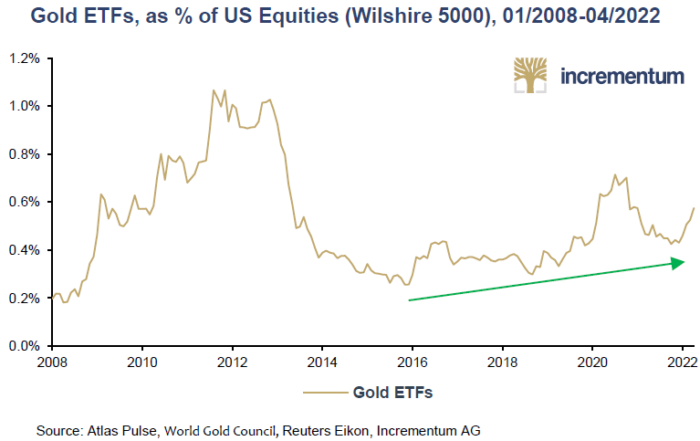

Investor sentiment toward gold had become deeply pessimistic after 2021.

Gold ETFs recorded outflows of 173 tonnes in 2021 after massive inflows of 874 tonnes during 2020. Visibly, total investor demand fell sharply.

In any event, by early 2022, the trend began reversing:

Gold ETF holdings began rising again

Inflation fears intensified

Investors returned to safe havens

The gold bull market was regaining momentum, even if skepticism still lingered.

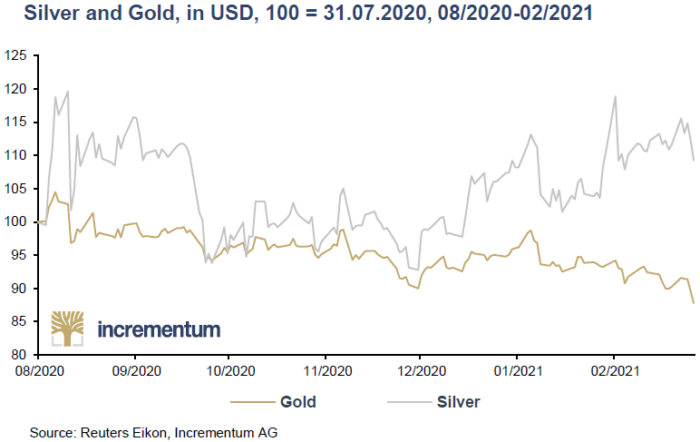

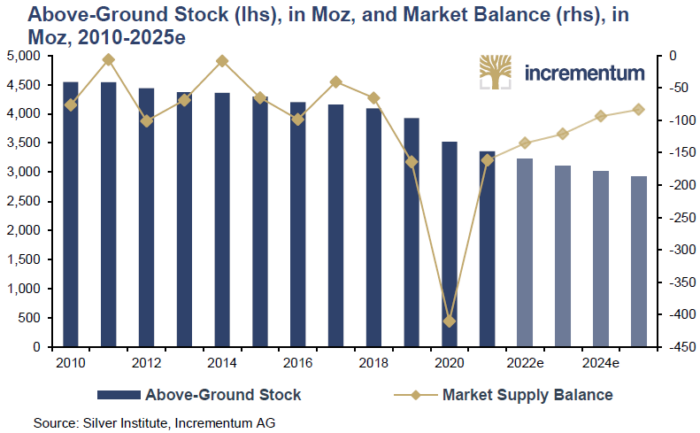

The report also highlighted the increasingly explosive fundamentals within the silver market.

Demand continued rising due to:

Solar energy

Electrification

Industrial applications

At the same time, silver supply remained constrained.

The report argued that substantially higher silver prices would eventually be required to resolve the imbalance between supply and demand. In hindsight, this thesis proved correct as silver eventually broke its long-standing secular highs a few years later.

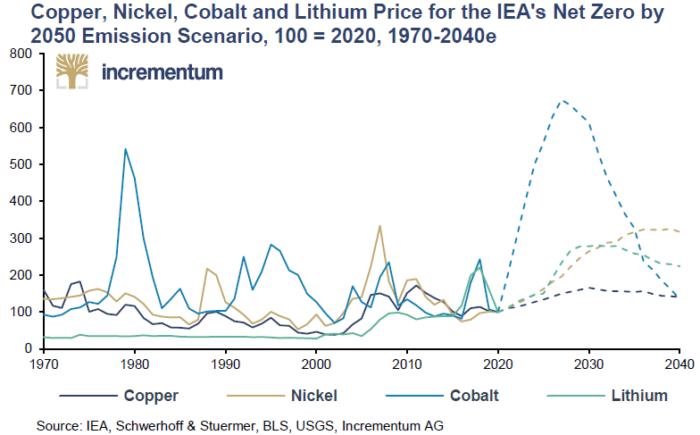

The IGWT 2022 explored how ESG policies themselves could unintentionally contribute to a commodity supercycle.

The contradiction was obvious:

The green transition required enormous quantities of raw materials

Yet, ESG policies discouraged investment in resource extraction and energy production

Unmistakenly, years of underinvestment in oil, gas, mining, and commodities collided with surging global demand.

For this reason, a structurally tighter commodity environment had emerged. Besides that, there was a growing realization that resource scarcity would become one of the defining macro themes of the decade.

The report rejected the simplistic “Bitcoin versus gold” narrative. Instead, both assets were presented as complementary alternatives to an increasingly fragile fiat-based monetary system.

• Gold represented the historical monetary anchor

• Bitcoin represented an emerging digital monetary challenger

Importantly, institutions such as the IMF opposed both gold-linked and Bitcoin-linked monetary systems for similar reasons: both constrain the flexibility of fiat currencies.

In turn, that flexibility – the ability to expand debt, monetize deficits, and intervene aggressively in financial markets – remains central to modern technocratic policymaking.

Therefore, gold and Bitcoin represented different forms of monetary discipline in an era increasingly defined by monetary excess.

One of the report’s most important takeaways was that gold behaves differently depending on the monetary environment.

In hyperinflationary countries such as Venezuela and Argentina, gold and local equities often rise together as investors flee collapsing fiat currencies for real assets.

Conversely, in countries with more stable monetary systems, gold often exhibits near-zero correlation with equities, making it a powerful diversification tool.

This duality explains why gold serves simultaneously as:

Financial insurance

Inflation hedge

Crisis lifeline

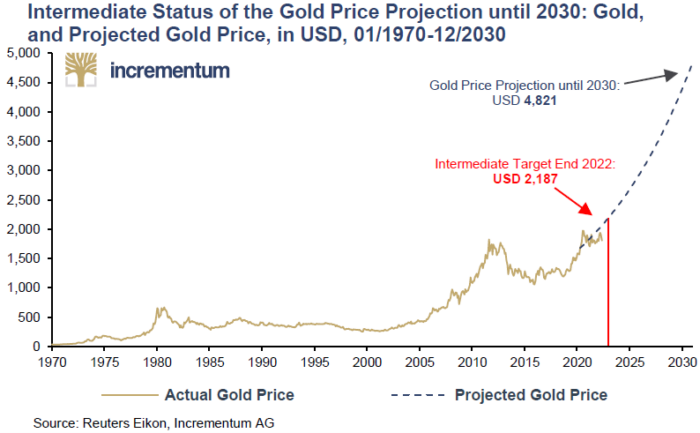

Once again, in this 2022 edition, we reaffirmed the long-term forecast first introduced in the IGWT 2020:

📌 Gold reaching USD 4,800 by the end of the decade.

At the time, many observers considered the projection extremely ambitious. At any rate, on January 21, 2026, gold already touched that level, years ahead of schedule.

With four years still remaining until 2030, the original target now appears increasingly conservative, further validating the secular bull market thesis outlined throughout the 2020s Golden Decade framework.

Looking back from 2026, the parallels between today’s environment and 2022 are striking.

We continue to face:

Geopolitical fragmentation

Persistent inflationary pressures

Debt sustainability concerns

Energy insecurity

Accelerating de-dollarization

The current tensions surrounding the Persian Gulf conflict echo many of the same fears markets experienced after the Russian invasion of Ukraine.

Importantly, the experience of 2022 demonstrated that while geopolitical shocks can initially produce severe inflationary pressure and economic panic, markets and supply chains eventually adapt.

That lesson remains highly relevant today.

Ultimately, Stagflation 2.0 was not merely a report about inflation. It documented the breakdown of the old macro regime, the remonetization of gold, the growing fragility of fiat systems, and the emergence of a completely new investment playbook for the 2020s Golden Decade.

Dive back into this essential edition. Go to the Archive of the IGWT Report and explore the IGWT 2022 in full.

#20Years20Threads #InGoldWeTrust #GoldInvesting #GoldReserves #SilverSupply #IndustrialDemand #PreciousMetals #Commodities #Bitcoin #HardAssets #SafeHaven #InflationHedge #InflationDynamics #InvestorDemand #CentralBanks #MonetaryPolicy #Dedollarization #SoundMoney #MoneySupply #DebtGrowth #GlobalEconomy #SupplyChains #EnergyCrisis #CommoditySupercycle #BullMarket #FinancialMarkets #MonetarySystem #AssetPerformance #PortfolioStrategy #GoldenDecade #MacroTrends #AustrianEconomics #Stagflation2.0 #IGWT22