The defining thesis of the 2020 report remains as relevant as ever:

“Covid-19 was the needle that popped the debt bubble. Since then, things have been happening at breathtaking speed. We do not know exactly where the path will take us. But thanks to the preparations of the past decades, we have an idea.”

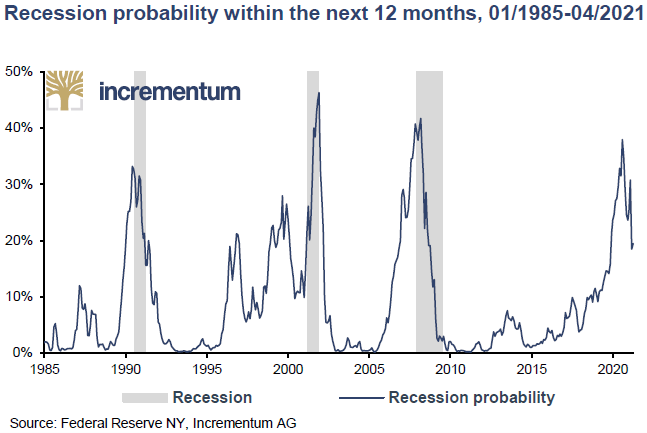

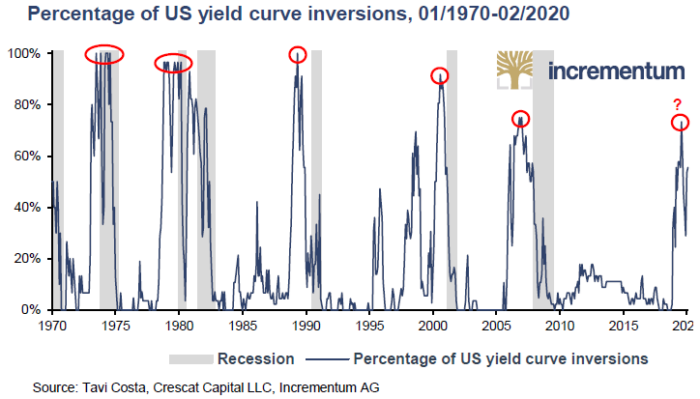

Although the pandemic was not the root cause of the crisis, it was the catalyst. By late 2019, the warning signs were unmistakable: yield curves had inverted, economic growth was slowing, and systemic fragilities were building beneath the surface.

In essence, the global economy was already heading toward recession. Covid-19 simply fast-forwarded the inevitable, exposing structural weaknesses that had accumulated over decades.

The response to the crisis was nothing short of extraordinary.

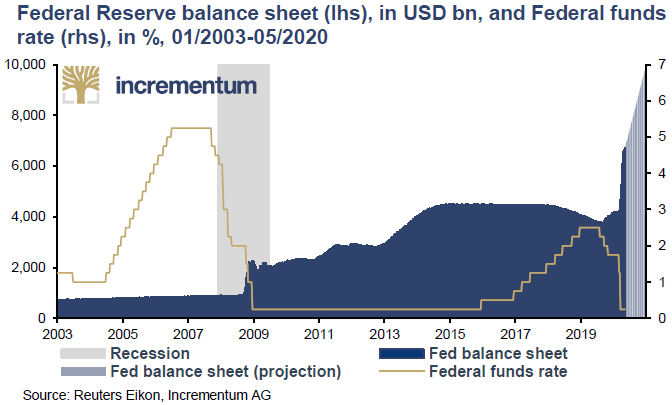

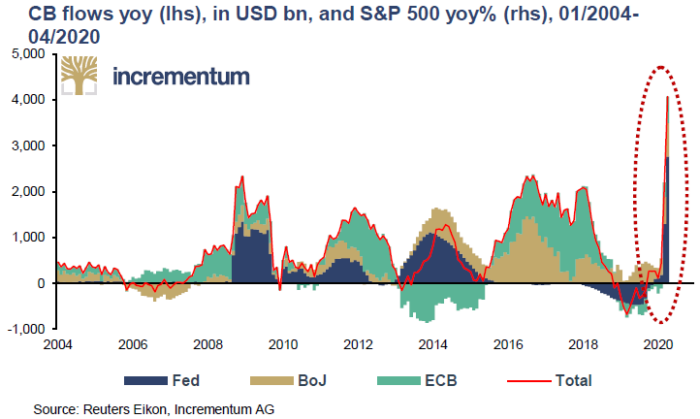

Attempts at monetary normalization collapsed almost instantly. The Federal Reserve’s tightening efforts proved short-lived, and the system reverted to aggressive easing. Quantitative easing returned, not as a temporary measure, but as a permanent fixture of monetary policy.

At the height of the panic, liquidity injections reached unprecedented levels, with the Fed effectively pumping USD 1 million per second into the financial system over a two-week period. What had once been dismissed as internet satire – “money printer go BRRR” – became reality.

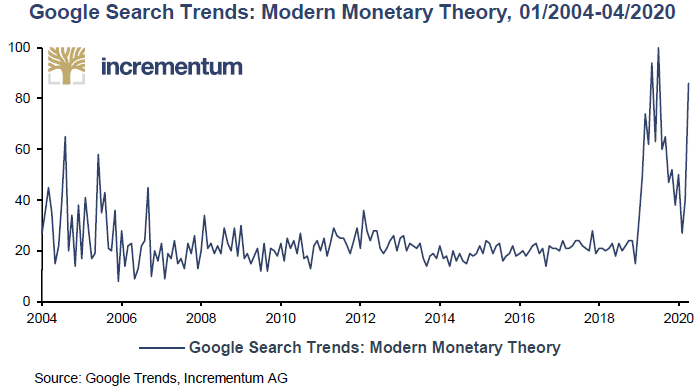

Simultaneously, governments unleashed massive fiscal stimulus programs. The result was a powerful and unprecedented combination: QE Infinity paired with direct fiscal transfers. The boundary between monetary and fiscal policy began to dissolve, giving rise to what can best be described as MMT by stealth. Apparently, such a dynamic hardly went unrecognized by market participants at the time.

The events of 2020 cannot be understood without placing them in a longer historical context.

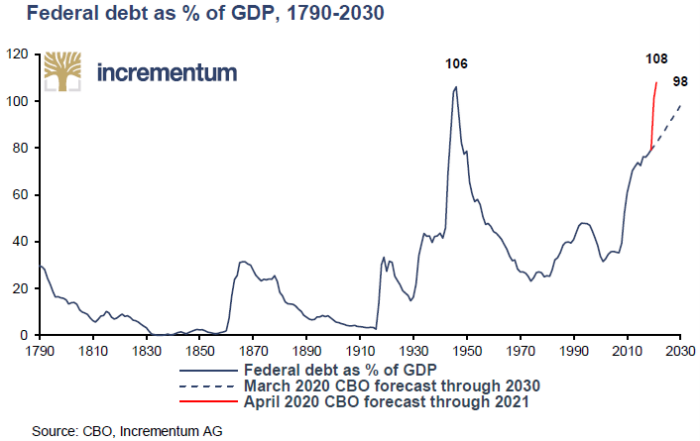

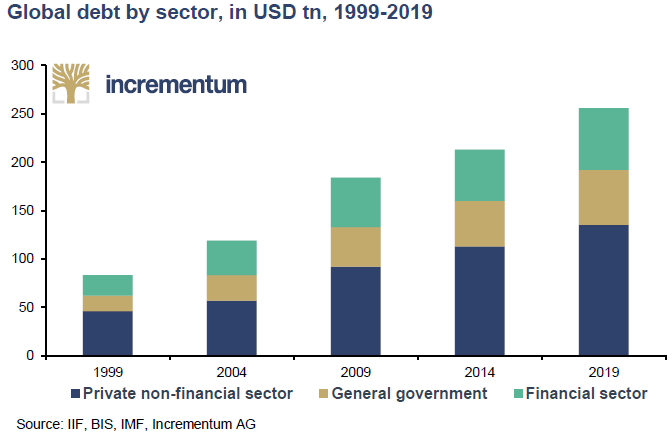

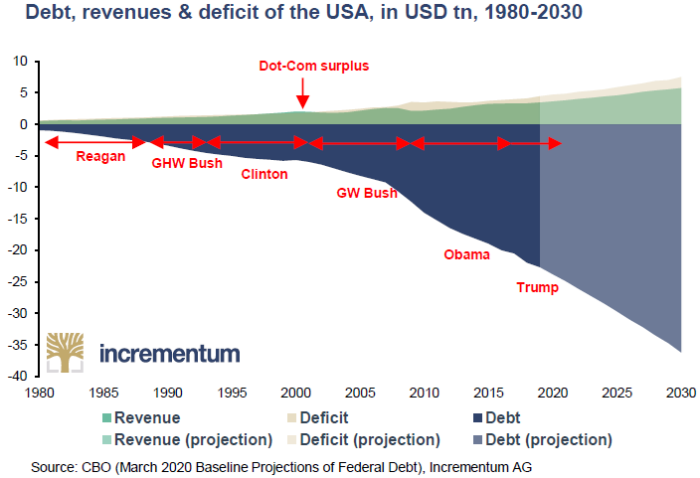

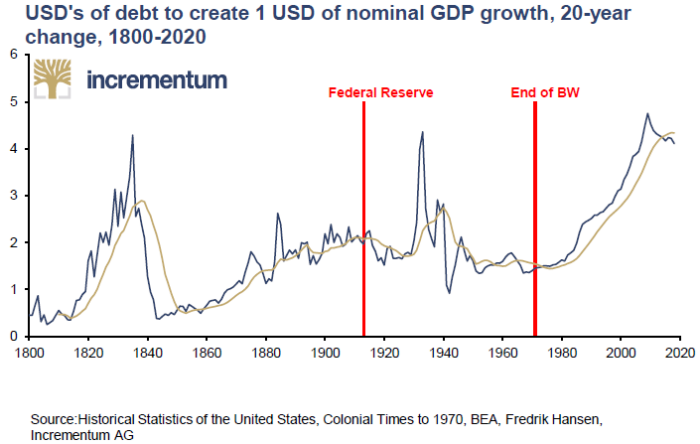

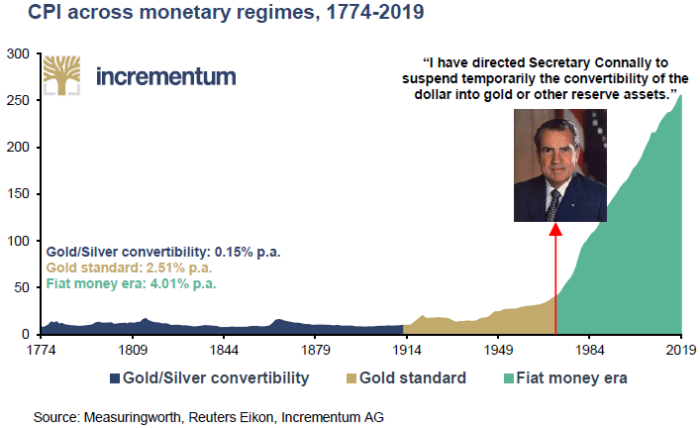

Since the collapse of the Bretton Woods system in 1971, the global monetary framework has been characterized by progressive debt expansion. Over time, the system became increasingly saturated with debt, with each additional unit of GDP requiring ever greater amounts of credit.

In other words, the marginal productivity of debt declined. There was simply less bang for each buck.

By 2020, this dynamic had reached critical levels. Public debt was exploding, corporate balance sheets were increasingly fragile, and private sector leverage was stretched. Worse than that, the system had become heavily dependent on continuous liquidity injections to sustain growth.

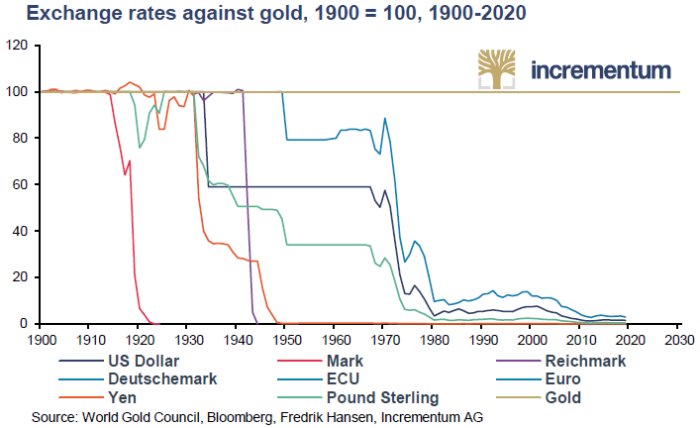

As a result, fiat currencies were engaged in what could be described as a race to the bottom. In a purely fiat regime, it is not about which currency appreciates, but which one depreciates more slowly. The long-term erosion of purchasing power had become structural.

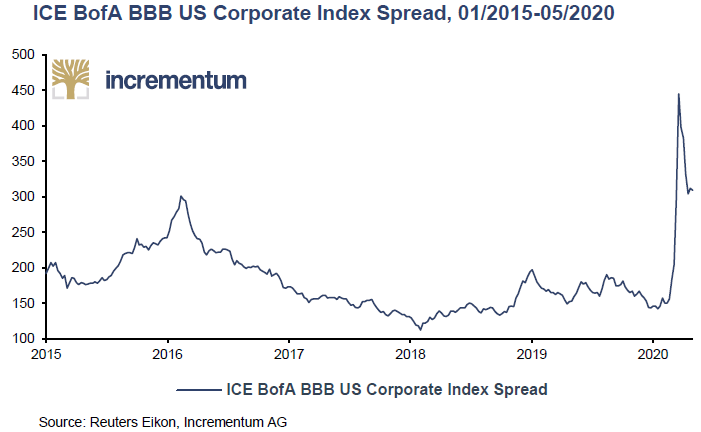

The fragility of the system became particularly evident in credit markets.

In March 2020, spreads on BBB-rated corporate bonds surged from approximately 150 basis points to 500 basis points within days, effectively freezing refinancing markets. The Federal Reserve intervened with a USD 500 billion program to stabilize the situation, preventing a cascade of defaults.

However, this intervention highlighted a deeper issue: the growing prevalence of “zombie companies.”

Roughly 17% of publicly listed companies globally were unable to generate sufficient cash flow to cover interest expenses for at least three years. These firms survived not because of economic viability, but due to artificially low borrowing costs.

One of the most astounding observations we came across at the time was the notion that “there is no money in monetary policy.” Despite years of ultra-loose conditions following the Global Financial Crisis, bank credit growth and real economic output remained subdued. Patently, the unconventional experiments carried out by the monetary wizards had failed to bring about the desired economic recovery.

The consequences were significant:

Persistent malinvestment

Stagnant productivity

Suppressed innovation and competitive dynamism

In short, the system had become not only fragile, but structurally inefficient.

The macroeconomic backdrop was equally dramatic.

According to IMF estimates, global GDP contracted by approximately 3% in 2020, marking the deepest recession in more than 80 years. The United States experienced an annualized GDP decline of 31% in Q2, while the Eurozone contracted by 7.5% for the year.

Such figures underscore the magnitude of the shock. Notwithstanding, they also explain the scale of the policy response, as well as the long-term consequences that followed.

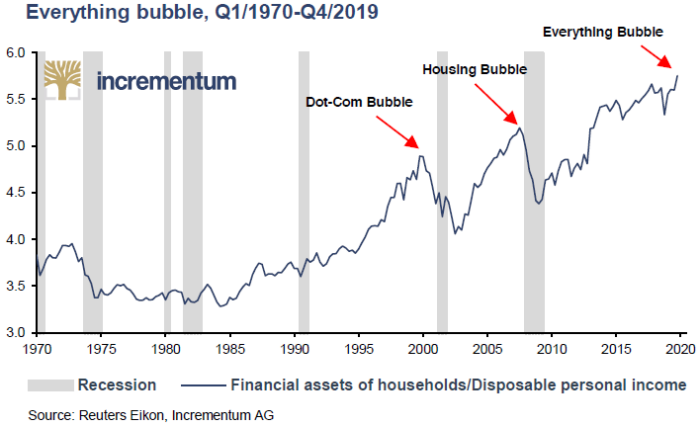

From the perspective of the Austrian School of Economics, the unfolding dynamics were entirely consistent with theory. Simply put, the inflationary process follows a recognizable pattern.

Initially, inflation manifests in asset prices like stocks, real estate, and financial instruments. Only later does it spill over into consumer prices.

This framework helps explain the emergence of the so-called “Everything Bubble” following the Global Financial Crisis. Years of ostensible ultra-loose monetary policy had inflated asset valuations across the board, setting the stage for broader inflationary wave that would follow.

By 2020, the conditions for a regime shift were firmly in place.

Against this backdrop, gold began to reassert its role.

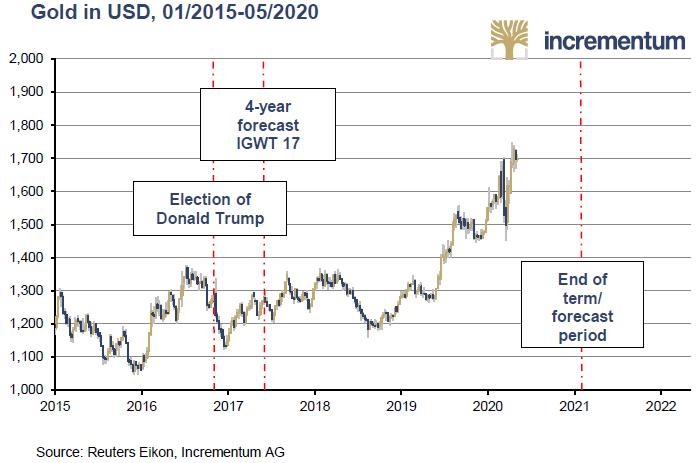

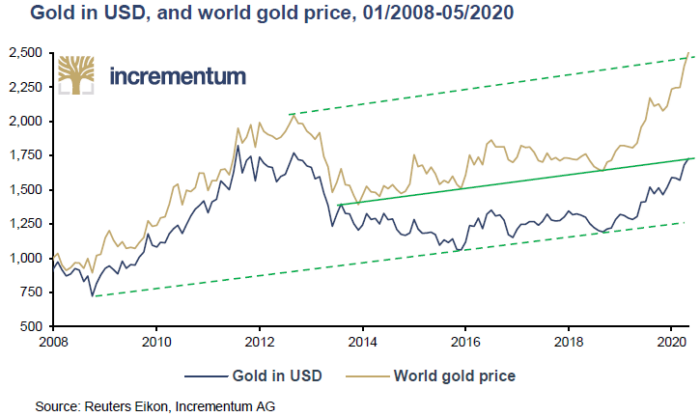

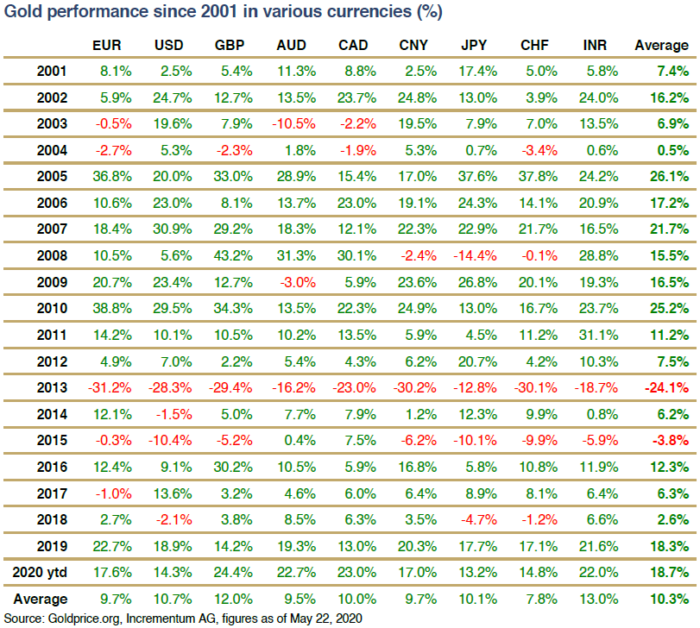

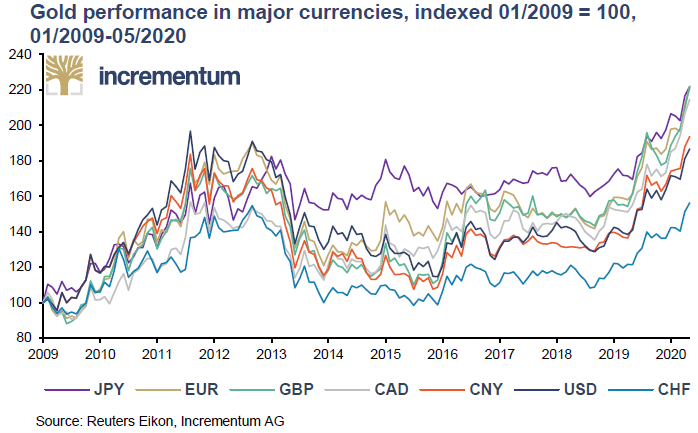

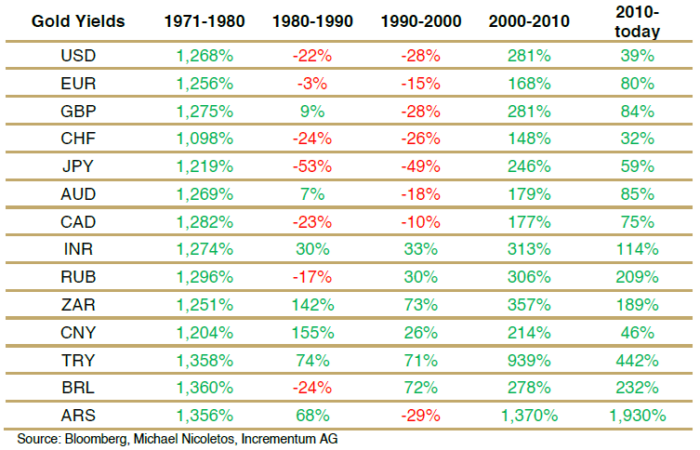

By mid-2020, gold had reached all-time highs in nearly every major currency, even if the strength of the US dollar temporarily masked this breakout in USD terms. From 2001 to 2020, gold delivered an average annual return of 10.3%, with particularly strong performance in 2019 and early 2020.

More importantly, the technical picture corresponded with the macro thesis. Remarkably, the fundamentals and the timing were perfectly aligned.

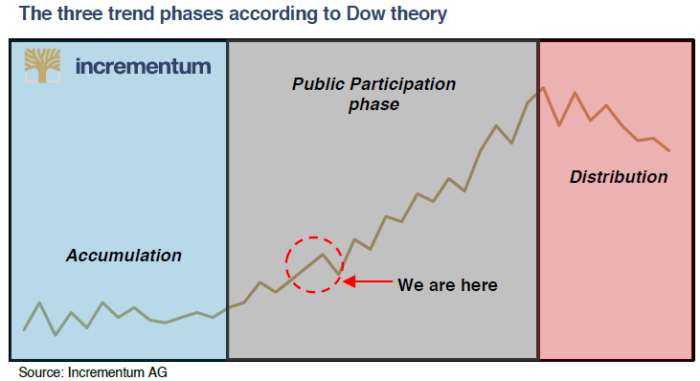

Building on our 2019 analysis based on the Dow Theory, we identified three phases of a bull market:

Accumulation

Participation

Mania

The breakout above long-standing resistance levels signaled the transition into the participation phase. By 2020, we assessed that gold was in the first third of this phase, suggesting that the most significant upside still lay ahead.

To put another way, the bull market was only just beginning.

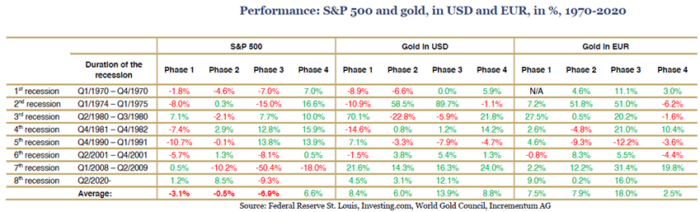

The events of March 2020 provided a powerful validation of gold’s role.

As global equity markets plunged, gold demonstrated resilience, reinforcing its status as a safe-haven asset. This was not surprising from a historical perspective, even if some commentators still dismissed gold as a “barbarous relic.”

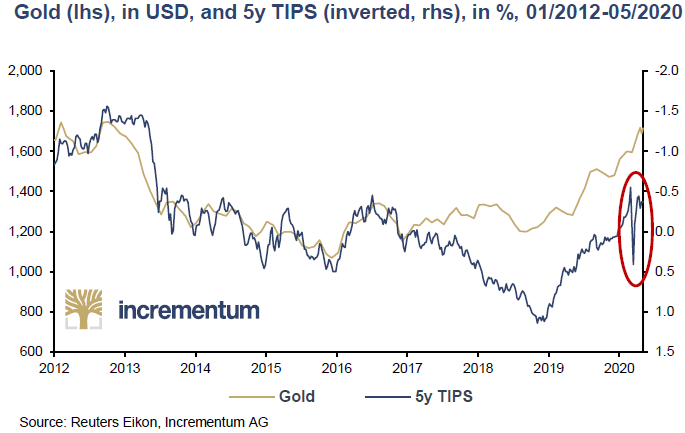

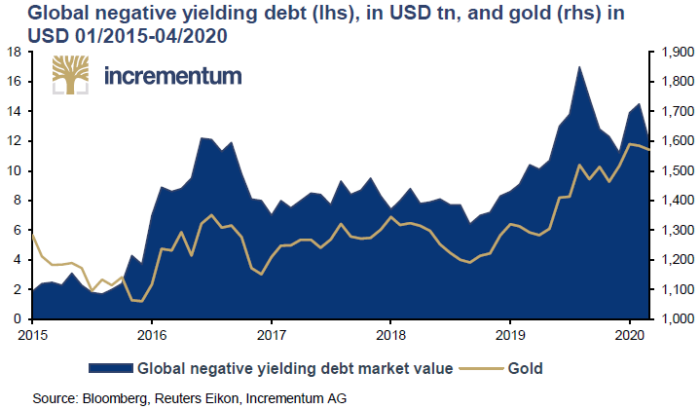

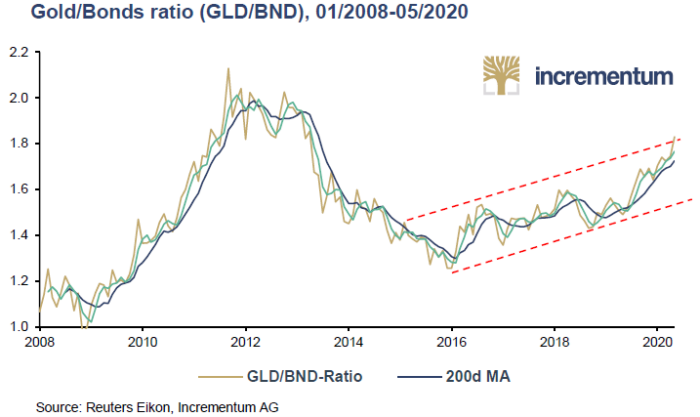

At the same time, real interest rates returned to negative territory, while the stock of negative-yielding debt remained elevated. Therefore, bonds, which were traditionally considered safe, were increasingly questioned as reliable stores of value.

Notably, an important development began to emerge: gold started to decouple from real yields. In fact, this development would grow in importance in the years that followed, signaling a transformation in the underlying drivers of the gold price.

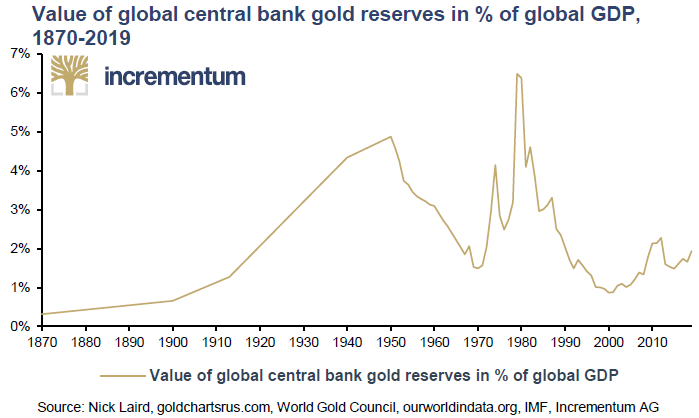

One of the most profound themes of the 2020 report was the emergence of a new monetary world order. Bear in mind that this had been a recurring theme over the last few reports.

Indubitably, this topic had always been relevant, offering some interesting updates every year. Having said that, the key trends we detected were:

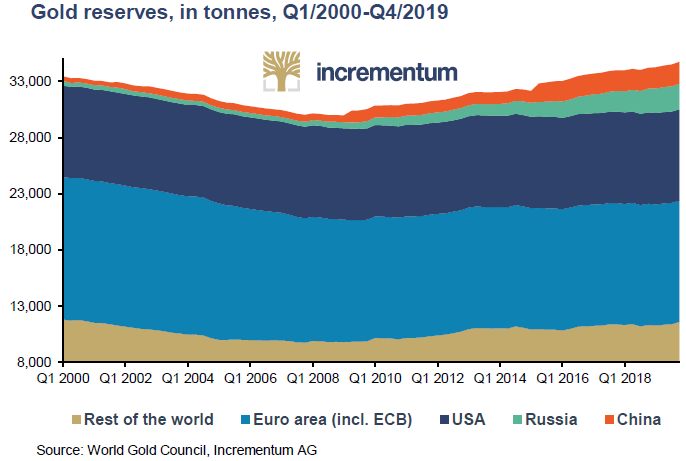

Accelerating central bank gold accumulation

A structural shift of gold demand toward emerging markets

Early signs of de-dollarization

Increasing recognition of gold as a neutral reserve asset

Unmistakenly, gold’s unique characteristic – its lack of counterparty risk and its universal acceptance – positioned it as a cornerstone asset in a changing geopolitical and monetary landscape.

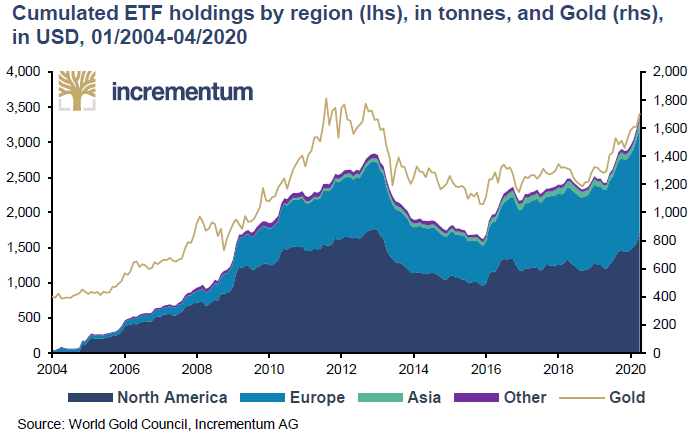

A notable shift began in mid-2019 when Western investors started to re-engage with gold. Visibly, ETF inflows surged, portfolio allocations increased, and gold demand turned more pro-cyclical than purely defensive.

This noted a departure from the traditional “crisis-only” demand pattern. Hence, it hinted at gold’s re-emergence as a mainstream portfolio component.

Yet, as later developments showed, this Western awakening remained incomplete, leaving room for the powerful East-driven demand dynamics analyzed in the In Gold We Trust reports.

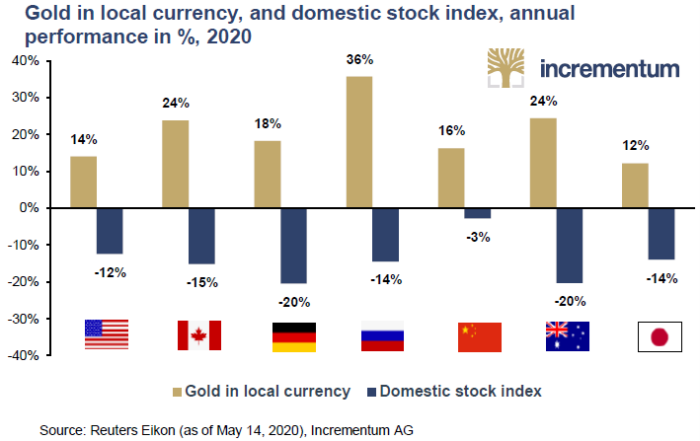

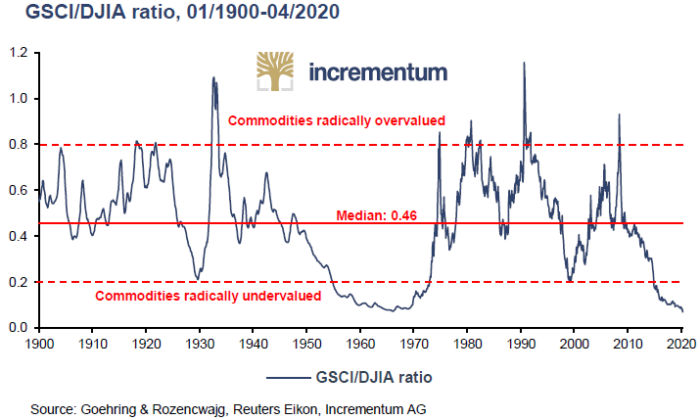

Beyond gold, we identified a broader opportunity in hard assets.

Essentially, commodities were trading at historically low levels relative to equities, suggesting the potential for a new commodity supercycle. Within this context, we anticipated:

Strong outperformance of commodities

Significant upside in mining equities

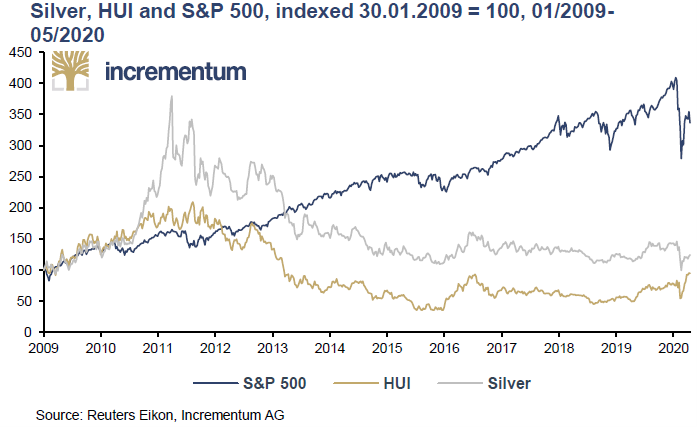

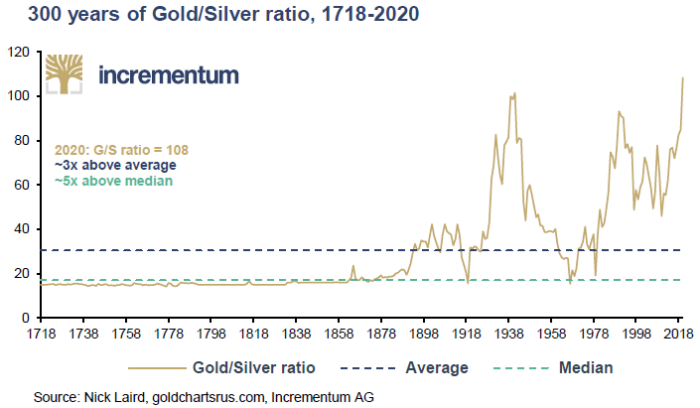

A particularly compelling case for silver

In particular, silver appeared historically undervalued relative to gold, with strong industrial demand prospects supporting its long-term outlook. As later developments confirmed, this thesis proved highly prescient.

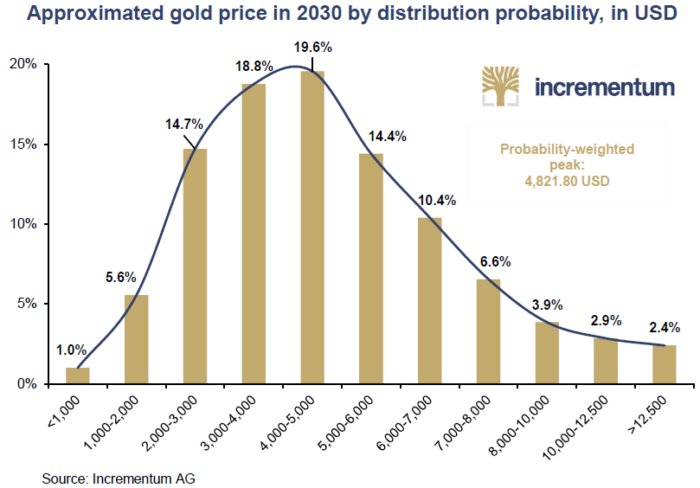

At the heart of the 2020 report was a bold forecast. We projected that gold would reach USD 4,800 by the end of the decade.

At the time, this target seemed ambitious; perhaps, even some would call us radical. Be that as it may, reality unfolded even faster than anticipated. As early as January of this year, gold reached that absurd level, demonstrating that the original projection had, if anything, been conservative.

Equally significant was the timing. The 2020 report was the eighth edition following the 2011 peak, and just two months later, on July 27, gold broke through its previous all-time high in USD terms.

This confirmed what the data, analysis, and theory had already suggested: A new bull market had begun.

The Dawning of a Golden Decade report distilled several critical themes:

Failure of monetary normalization

QE Infinity and fiscal dominance

Debt saturation and the rise of a zombie economy

A structural shift in inflation dynamics

Gold’s resurgence versus fiat currencies

The emergence of a new monetary order

A renaissance in commodities and hard assets

To sum up, 2020 might have been a year of crisis, but do you know what people say about crises? They also present opportunities.

Thus, this year was a turning point. It marked the beginning of a profound transformation in:

Money

Markets

Trust

What appeared chaotic in real time was, in hindsight, the early phase of a new regime. In plain terms, the role of gold was being redefined and the global financial system reshaped.

The blueprint was there all along.

Dive back into this essential edition. Go to the Archive of the IGWT Report and explore the IGWT 2020 in full.

#20Years20Threads #InGoldWeTrust #GoldenDecade #GoldInvesting #GoldSurge #SilverDemand #Commodities #MiningStocks #InflationExpectations #CantillonEffect #DebtCycle #DebtCrisis #CentralBanking #AssetPurchases #Stagflation #GlobalEconomy #CovidRecession #FinancialMarkets #EurodollarSystem #SoundMoney #HardAssets #MonetarySystem #DeDollarization #GoldReserves #SafeHaven #InflationHedge #InvestmentInsights #MarketAnalysis #MacroResearch #AustrianEconomics #IGWT20 #IGWT26 #AnniversarySeries