Over the weekend, negotiations between the United States and Iran collapsed, marking a decisive turning point in an already fragile situation. The U.S., under President Donald Trump, has since enforced a sweeping maritime blockade targeting Iranian ports and coastal infrastructure across the Persian Gulf, the Strait of Hormuz, and extending into the Gulf of Oman and Arabian Sea.

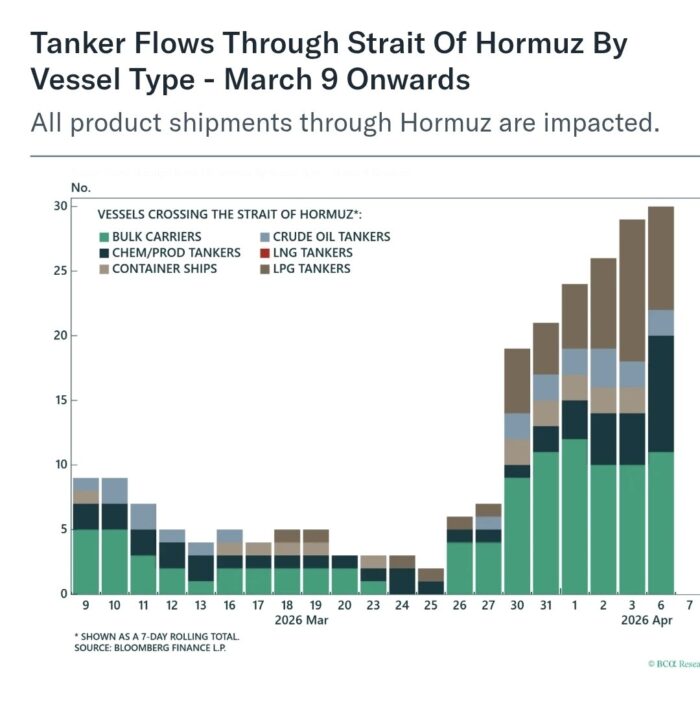

As of today, April 15, U.S. naval forces have been restricting vessels entering or leaving Iranian waters, while allowing non-Iran-bound traffic to transit. However, the impact has been immediate. At a time when the transit through the Strait of Hormuz had been slowly cropping up, trying to reach the average of 135 vessels per day in the pre-Iran war era, daily transits have collapsed to single digits once again this week. Needless to say, this represents a structural disruption to one of the most critical arteries of global trade.

Undoubtedly, the blockade is not the typical unserious rhetoric from President Trump of making unsubstantial threats, followed by an immediate softening or recantation. Plainly, this development has prompted an alarming outlook for the oil market.

![]()

![]()

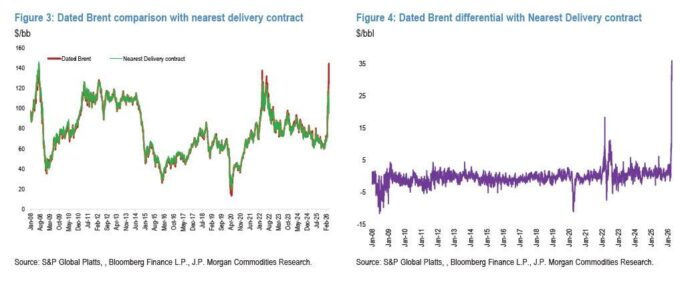

In essence, the physical crude market is experiencing extreme stress:

Dated Brent (spot physical oil) has surged above the 2008 peak

It reached USD 144.42 per barrel on April 7

Brent futures (June contract) hover in the neighborhood of USD 100 per barrel

The spot–futures spread has exploded to roughly USD 35 (vs. normal USD 1–2)

This unprecedented divergence reflects the simple reality that the world cannot source enough oil right now. Because approximately 13 million barrels per day remain missing from the market, refiners in Europe and Asia have been forced to compete aggressively for limited supply. Insofar as dated Brent reflects actual traded cargoes in the physical market, the intense pricing oscillation is the clearest signal of real-world scarcity, and definitely not mere speculative behavior.

With around 20% of global oil flows typically passing through the Strait of Hormuz, even a partial disruption would create outsized consequences. Unfortunately, the situations appear far from a disentanglement, as maritime shipping experts are warning that normalization of flows is unlikely in the near term.

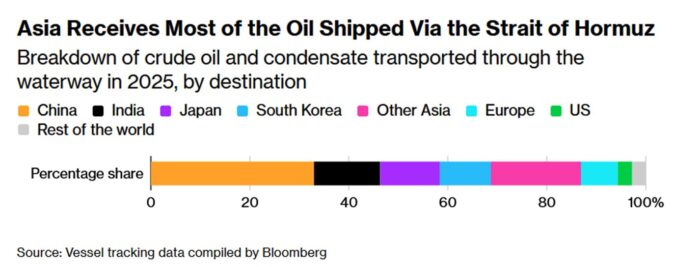

Unquestionably, Asia is absorbing the brunt of this disruption. More than 80% of oil flowing through the Strait of Hormuz is destined for Asian economies, including China, India, Japan, and South Korea. In fact, entire industrial chains, from fertilizers to plastics, are already feeling the strain.

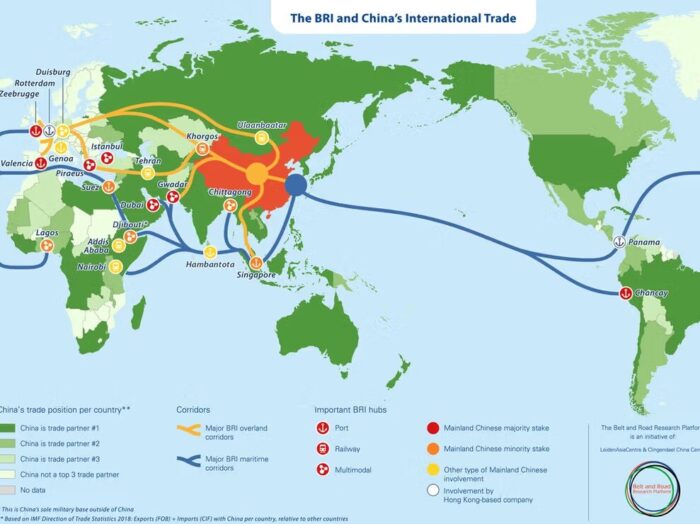

Importantly, China stands out as the most strategically exposed:

It is the largest global crude importer

A significant share of Iranian oil exports historically flowed to China

Iran is a key node in China’s Belt and Road Initiative (BRI)

Iran’s geography makes it a vital land and energy bridge connecting Asia, Europe, and the Middle East. Hence, disruptions here, in addition to affecting oil markets, they challenge China’s long-term strategy to bypass maritime routes influenced by U.S. power.

In short, if disruptions persist, China faces a dual threat: energy shortages; and a strategic setback to its global trade ambitions.

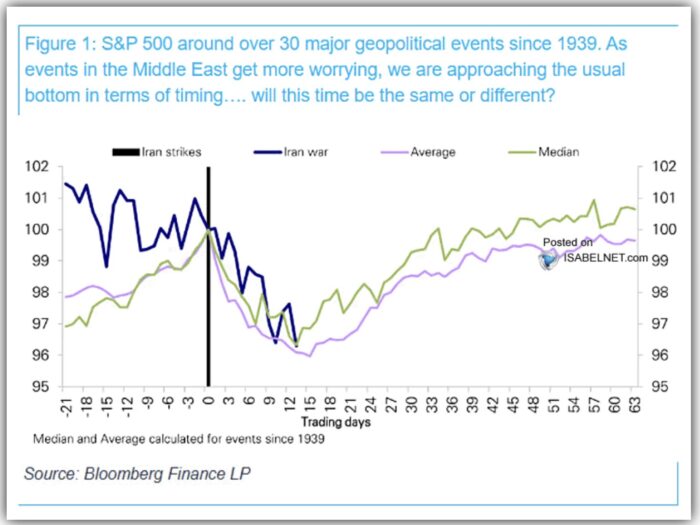

Moreover, the oil shock is already rippling through financial markets.

Crude oil prices jumped +7% at the start of the week

Notwithstanding, equity markets remain relatively resilient

Historically, markets take about 3 weeks to bottom after geopolitical shocks

Visibly, current market behavior appears to be aligning with the historical record, as stocks and other financial assets have been surging since last week. However, another way of interpreting this bounce in the markets is that the worst has already passed or is discounted in prices, as the global economy adapts to the new paradigm of a less fluid flow of oil through the traditional sea lanes.

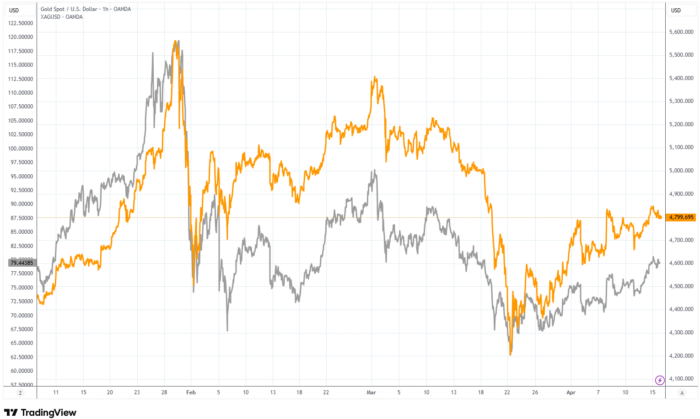

The behavior of gold and silver during this crisis may appear counterintuitive, but ultimately it was textbook. Their initial decline was hardly a failure of their role as safe havens. Instead, it was a liquidity-driven selloff, as investors raised cash amid rising oil prices and tighter financial conditions. As outlined in our recent article titled Spring Cleaning in Gold, this phase flushed out leverage and reset positioning.

What followed has been a powerful recovery. From the bottom on March 23 up to today:

🟡 Gold has risen around 17%

⚪ Silver has surged 30%, approximately

This marks a transition from liquidity stress to structural repricing. The drivers are unambiguous:

Energy inflation is rising

Geopolitical risks are intensifying

Confidence in global systems is weakening

Historically, while oil shocks are temporary, gold repricing is lasting. As inflation pressures build and monetary policy eventually adapts, demand for hard assets strengthens.

Specifically, silver’s outsized move reflects its dual role as both a monetary and industrial metal, making it more volatile. Nevertheless, this critical metal is, consequently, highly responsive during recoveries.

In short, the selloff was a sort of reset. This rebound may be the beginning of a larger move higher.

Although China is not the only actor watching closely, it may be the most consequential.

The U.S. is simultaneously expanding its strategic footprint in Southeast Asia. A newly signed defense partnership with Indonesia enhances U.S. surveillance over the Strait of Malacca, the world’s busiest shipping lane:

Handles 24% of global trade

Carries ~80% of China’s oil imports

This raises a critical question: could the current crisis spill into other chokepoints?

For Beijing, this is the “Malacca Dilemma” on steroids. Basically, the Chinese authorities have a mortal fear that this key maritime route could be constrained. Restricting both straits simultaneously would be the coup de grâce for the Middle Kingdom.

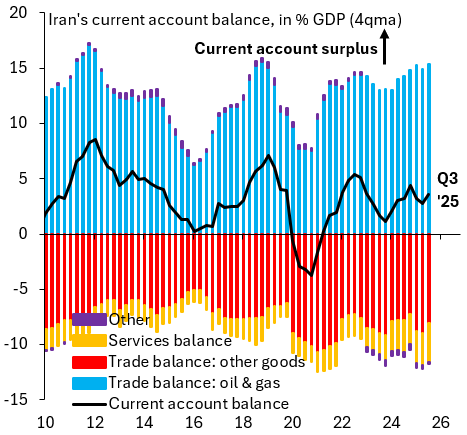

For Iran, the economic consequences could be severe and immediate. In truth, a sustained collapse in oil exports would trigger:

A sharp drop in foreign currency inflows

Currency devaluation

Rising import costs

Inflationary pressures

The likely policy response, borrowing and money printing, introduces a high probability of: hyperinflation; financial instability; and, of course, long-term economic damage.

Indubitably, this is a well-documented pattern in commodity-dependent economies under sanctions and trade isolation. Therefore, this scenario does not live solely in the theoretical realm.

What began as a localized conflict is rapidly evolving into a broader geopolitical confrontation. At stake:

Global energy security

Trade routes and maritime control

Strategic influence between major powers

The Strait of Hormuz has turned from a regional chokepoint, into a global pressure point now.

With the ceasefire window set to expire on April 22, the coming days will be decisive. Either diplomacy returns, or escalation deepens across multiple fronts.

To conclude, the current crisis exposes how critical dependence on narrow maritime chokepoints forms a fundamental vulnerability in the global economy. When those arteries are disrupted, the consequences cascade rapidly, from oil markets to inflation, and from geopolitics to financial markets too.

Seemingly, the global economy and international financial system is going through a massive stress test. Clearly, the results, so far, suggest that the system is far more fragile than many assumed.

#OilShock #EnergyMarkets #StraitOfHormuz #EnergyCrisis #GlobalEconomy #ChinaEconomy #ForeignPolicy #SupplyChains #NavalChokepoints #Commodities #GoldInvesting #SilverRally #SafeHaven #InflationHedge #FinancialSystem #MarketRisks #EconomicInsights #MacroTrends #AffordabilityCrisis #Stagflation #Geopolitics #BullMarket #GoldenDecade #TheBigLong #IGWT25