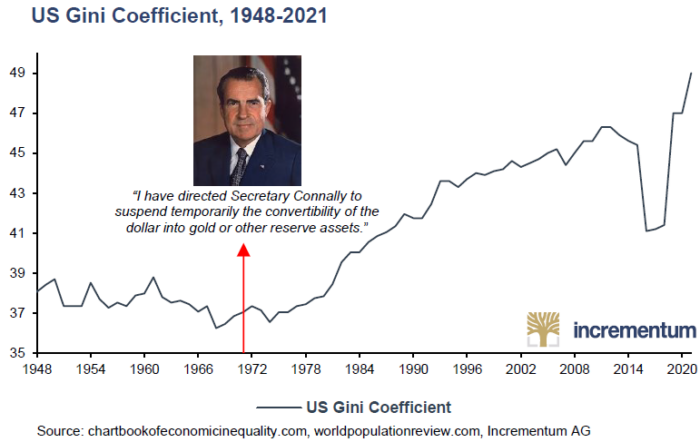

The report began by revisiting one of the defining turning points in modern monetary history: the Nixon Shock of 1971.

Fifty years after the US severed the final link between the dollar and gold, the consequences of fully untethered fiat currencies had become increasingly difficult to ignore. Debt levels had exploded, central banks had become the dominant force in financial markets, and the global economy had grown dependent on permanent monetary intervention.

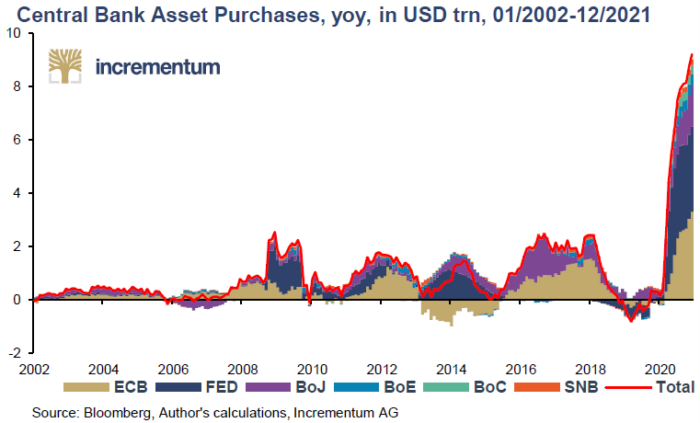

Simply put, the eurodollar system – the vast offshore dollar-based banking network that had fueled decades of global growth – effectively fractured during the Global Financial Crisis on August 9, 2007. Since then, private bank balance sheets stagnated, credit growth weakened, and central banks attempted to replace private credit creation with ever larger interventions.

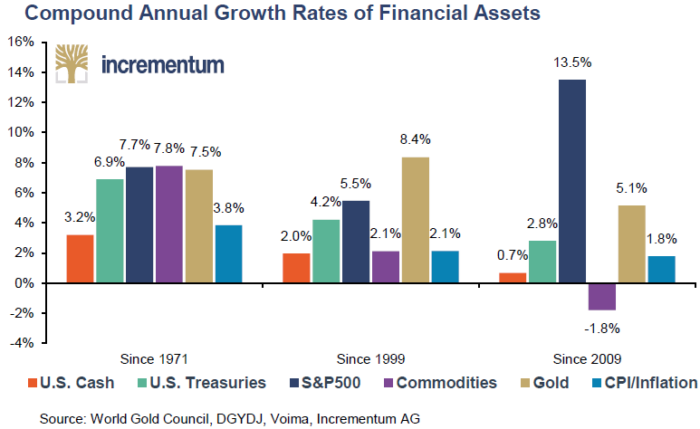

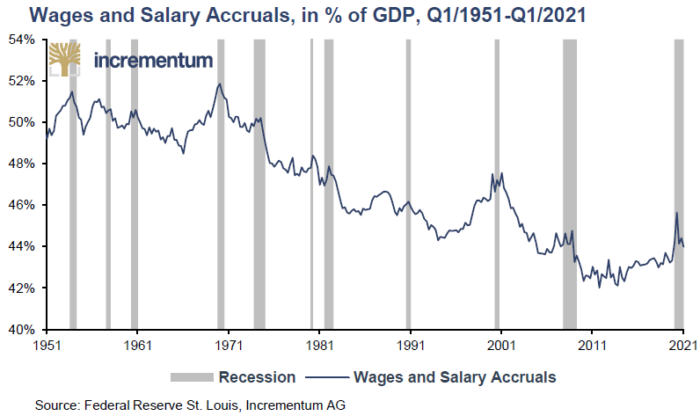

The result was what the report described as a Silent Depression. Basically, a paradigm emerged where the real economy remained sluggish while financial assets soared to historic valuations.

To wit, housing markets surged, equity markets boomed, bond prices inflated, and speculative assets multiplied. However, underneath the apparent prosperity, productivity growth weakened, debt burdens expanded, and the financialization of the global economy accelerated dramatically.

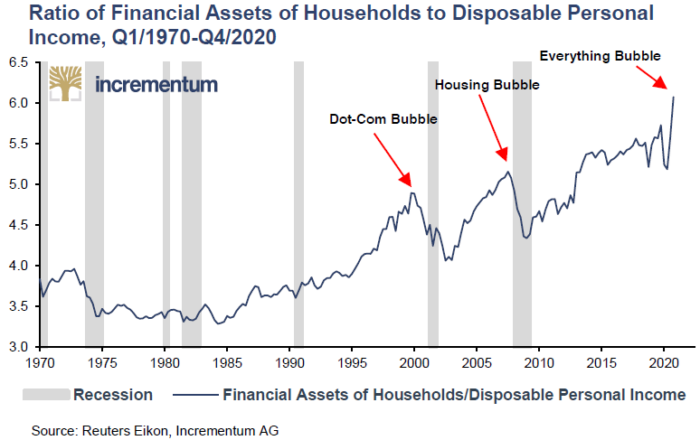

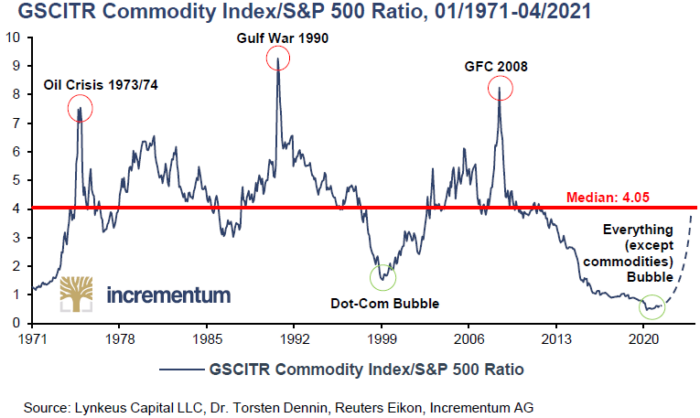

Patently, the Everything bubble was not a theory. In spite of this topic being constantly shrugged off, it had become the defining feature of the post-2008 world.

By 2021, nearly every major financial market had reached historically stretched valuations. The drivers were clear:

Zero and negative interest rates

Quantitative easing on an unprecedented scale

Massive pandemic stimulus

Fiscal deficits financed indirectly by central banks

In a nutshell, liquidity flooded into virtually every corner of the financial system. Asset prices detached from underlying economic fundamentals, while investors increasingly embraced speculation as a substitute for productive capital allocation. All the same, commodities had not caught the bid… yet.

One of the most important conceptual contributions of the IGWT 2021 was its explanation of modern money creation.

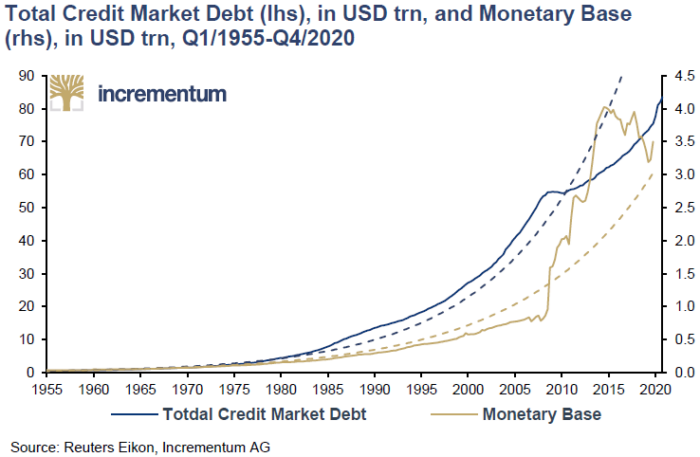

Contrary to popular belief, most money is not created directly by governments or central banks. Since the 1950s, commercial banks have created the overwhelming majority of money through credit expansion. Modern money is fundamentally composed of bank ledger entries.

This distinction matters enormously.

Because once economic growth became increasingly dependent on credit creation, the entire system also became increasingly dependent on permanently low interest rates and expanding debt levels. The eurodollar fracture after 2007 exposed the fragility of this arrangement. Central banks could print reserves, but they struggled to restore organic private credit growth.

Thus emerged the paradox of the post-GFC era where massive liquidity creation coexists alongside structurally weak economic growth.

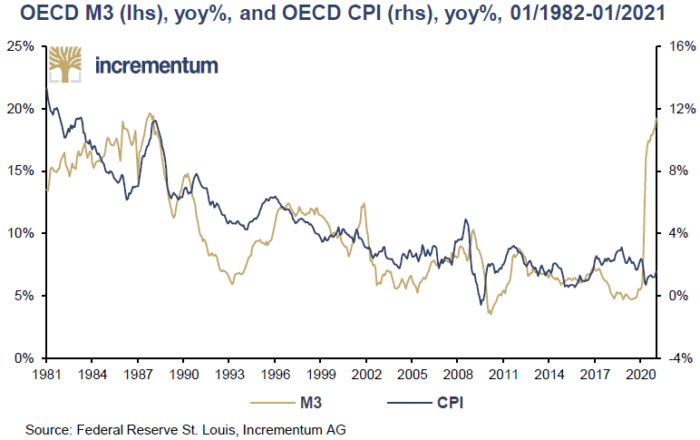

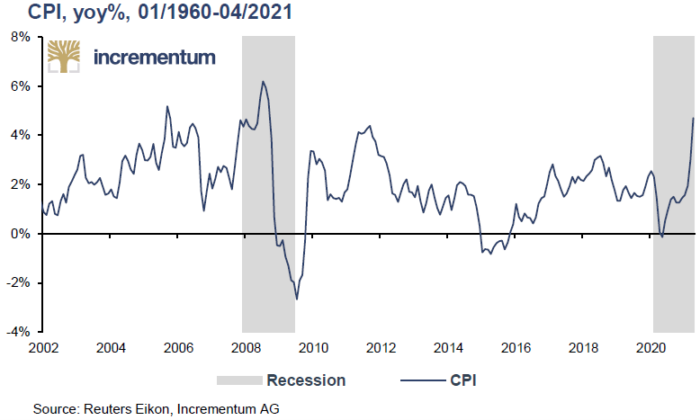

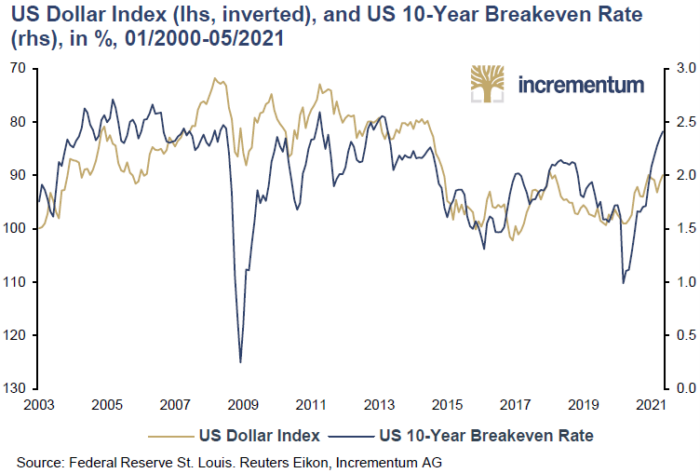

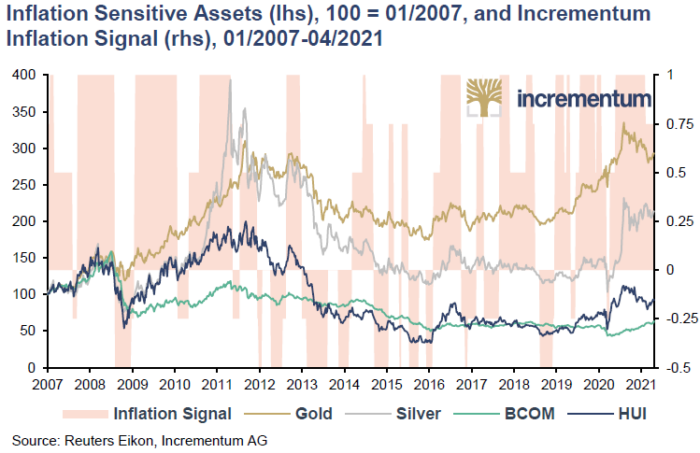

For years after the Global Financial Crisis, inflation largely remained confined to financial assets, as mentioned above.

Importantly, in the IGWT 2021 we argued that the inflationary process was evolving inasmuch as it was no longer restricted to Wall Street. Unmistakenly, it was migrating toward consumer prices.

In essence, food, energy, housing, automobiles, and consumer goods all began experiencing visible price pressures. At last, Main Street was feeling the consequences of years of monetary expansion.

Accordingly, the report asserted that the balance between inflationary and deflationary forces had decisively shifted. The pendulum had finally swung back toward the former state.

This stood in direct opposition to the dominant consensus of the time, which insisted inflationary pressures would remain temporary.

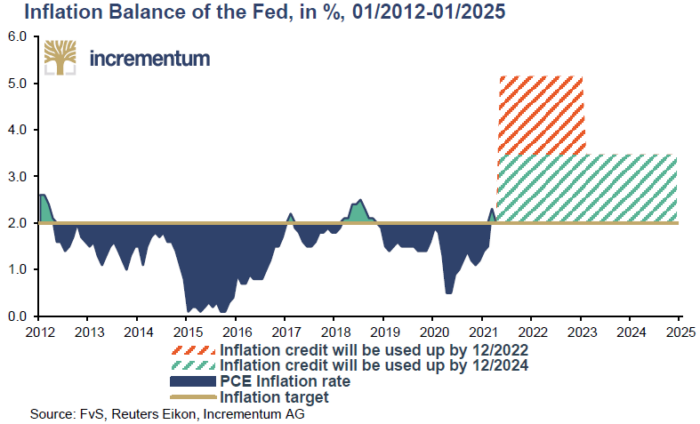

One of the most underappreciated developments highlighted in the IGWT 2021 was the Federal Reserve’s quiet, albeit profound policy shift toward Average Inflation Targeting.

Under the old framework, inflation above 2% would normally prompt monetary tightening. Under the new regime, however, the Fed openly signaled that it would tolerate inflation running above target for extended periods in order to compensate for the subdued inflation of the previous decade.

In practice, this amounted to a structural commitment to looser monetary policy for longer. The report interpreted this shift as confirmation that central banks had become trapped by excessive debt levels and financial market dependence on cheap liquidity.

Seemingly, policymakers could no longer normalize interest rates without threatening economic stability, asset prices, and government financing conditions. Ergo, the money spigots would remain open far longer than most investors anticipated.

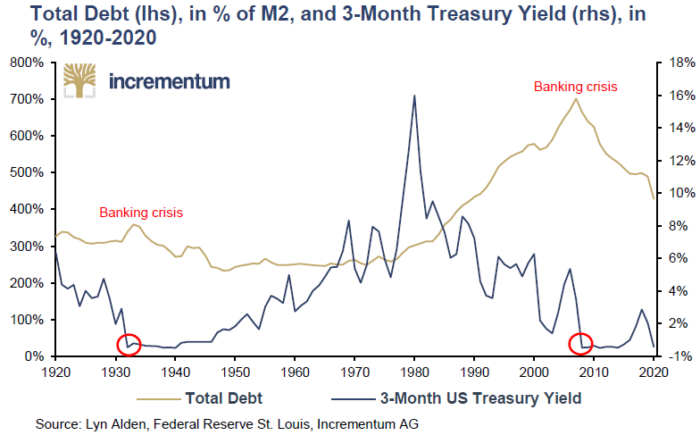

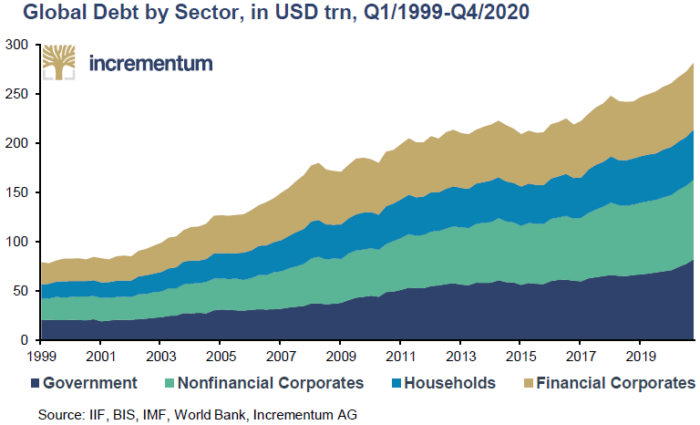

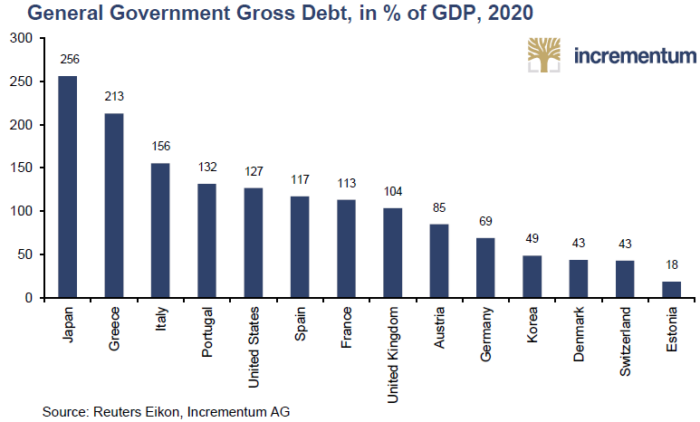

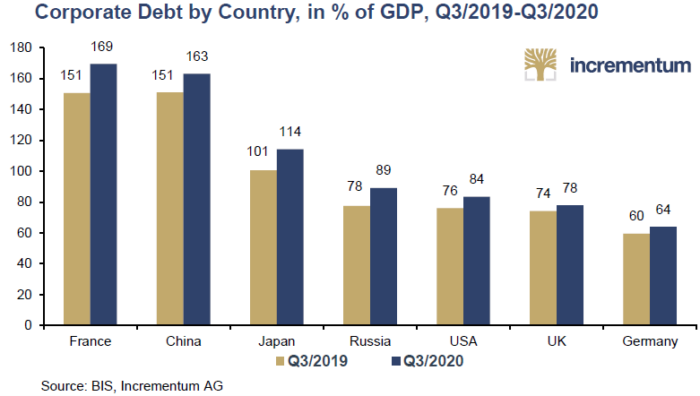

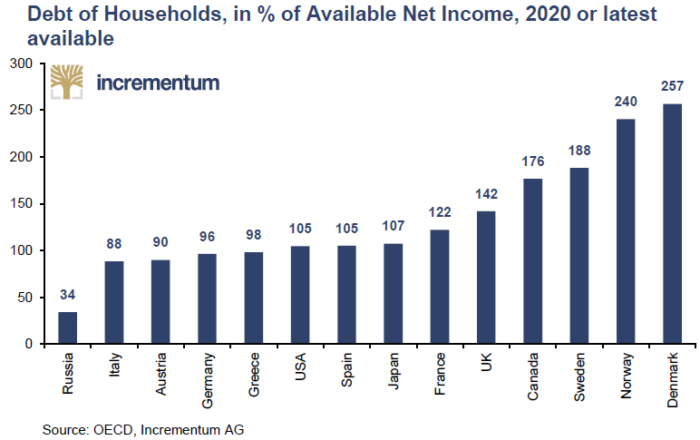

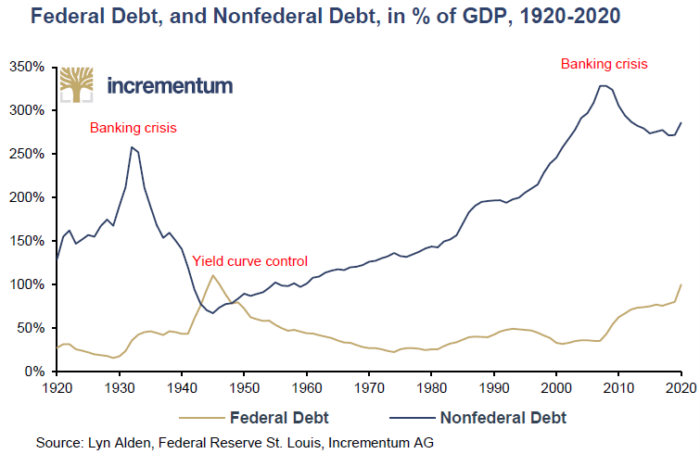

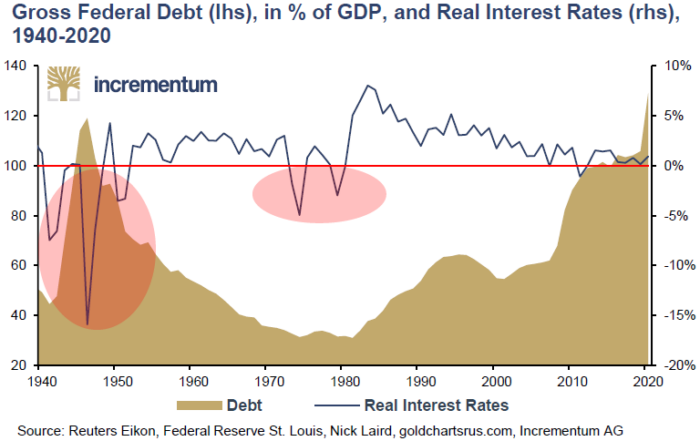

The debt dynamics discussed in this edition were among the most alarming aspects of the report.

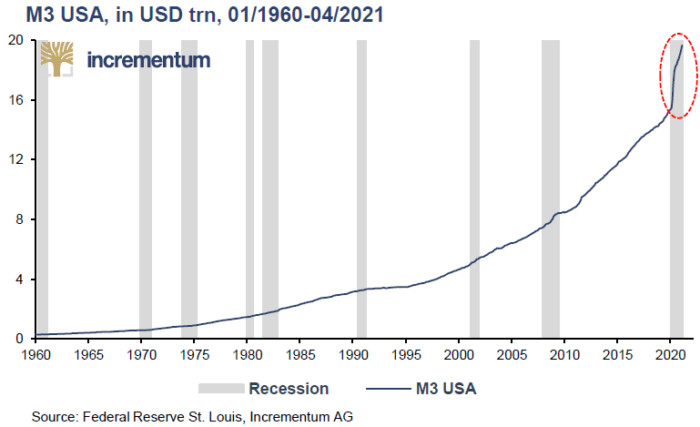

Following the pandemic response, governments, corporations, and households simultaneously embarked on one of the largest debt expansions in modern history. By the end of 2020, global debt-to-GDP had exceeded 355%, reaching unprecedented levels.

Governments financed enormous fiscal deficits through stimulus programs, transfer payments, bailouts, and emergency spending measures. Corporations aggressively borrowed at ultra-low interest rates, often using debt not for productive investment, but for financial engineering, acquisitions, and share buybacks. Meanwhile, households also increased leverage substantially in order to navigate lockdown-induced economic disruptions.

The report argued that this debt surge fundamentally changed the policy landscape. Once debt levels become sufficiently extreme, higher interest rates become politically and economically intolerable. Any meaningful normalization risks triggering defaults, recessions, or financial instability.

This reality forcibly locked policymakers into a regime of financial repression:

Negative real interest rates

Ongoing monetary accommodation

Yield suppression

Persistent inflationary pressures

In other words, the debt trap became the defining structural constraint of the global financial order. As we emphasized above, this is a feature of the eurodollar system, not a bug.

As debt burdens exploded following the pandemic response, we alerted that governments would ultimately become unable to tolerate materially higher interest rates.

The report projected that Yield Curve Control (YCC) – the deliberate suppression of government bond yields below inflation – would likely become mainstream policy. The historical parallel was explicitly the post-World War II period of financial repression.

Essentially, authorities would cap interest rates, inflate away the debt and suppress real yields. A combination of these options, in various degrees, was what awaited consumers, investors and business worldwide, but especially in developed economies.

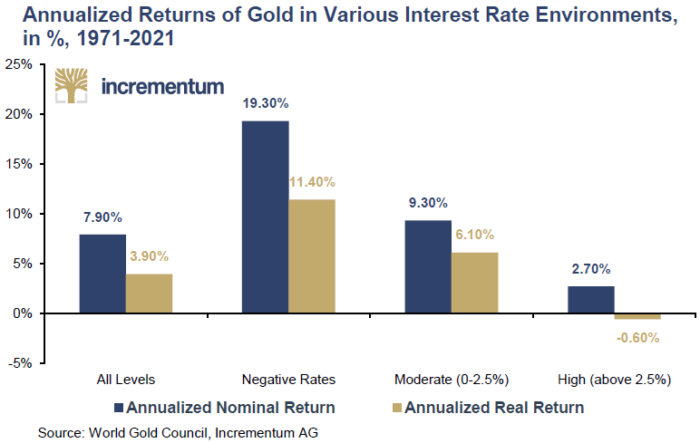

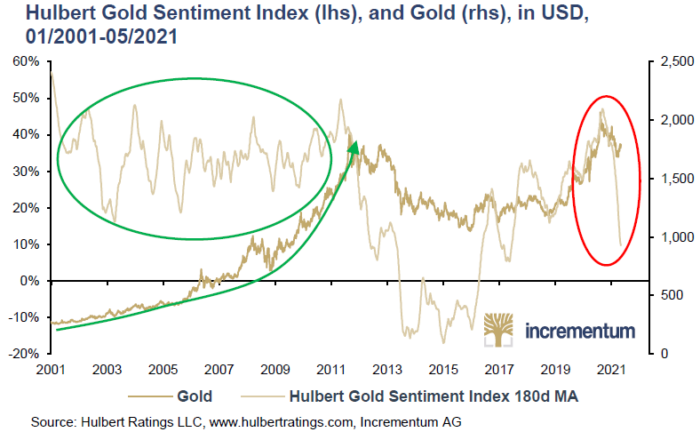

Curiously, the report noted that deeply negative real interest rates had historically created one of the most bullish environments imaginable for gold. Nevertheless, investors remained dramatically underallocated to precious metals.

This disconnect would later become one of the defining features of the new gold bull market.

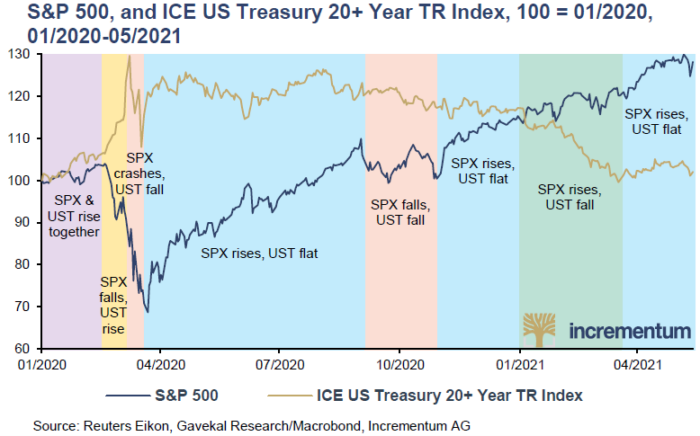

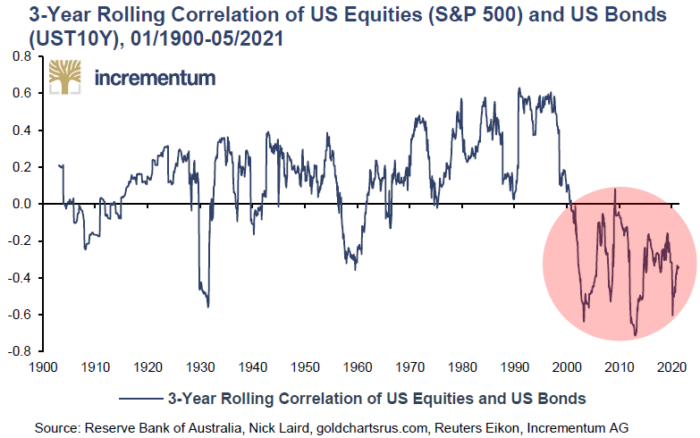

For decades, the classic 60/40 portfolio model, composed by 60% equities and 40% bonds, represented the cornerstone of institutional investing.

Be that as it may, this view was gradually changing. In truth, we contended that this framework was becoming increasingly fragile.

The logic behind the traditional portfolio rested on the assumption that bonds would offset equity market weakness during periods of stress. However, in an inflationary environment, both asset classes could decline simultaneously.

If inflation rose persistently:

Bond prices would suffer from rising yields

Equities would struggle under tightening financial conditions

Correlations between stocks and bonds could shift materially

In that world, diversification itself would likely begin to fail. Therefore, we maintained that gold and hard assets could increasingly replace sovereign bonds as the true portfolio stabilizers of the coming decade.

Another major theme of the IGWT 2021 was the accelerating transformation of the global monetary order.

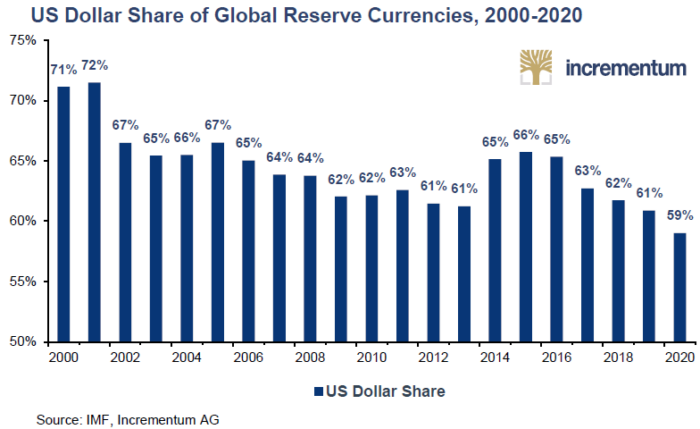

For decades, the US dollar stood at the unquestioned center of the international financial system. Yet, the report showed that confidence in the dollar-centric system was beginning to erode, particularly after years of aggressive monetary expansion, financial sanctions, and growing geopolitical fragmentation.

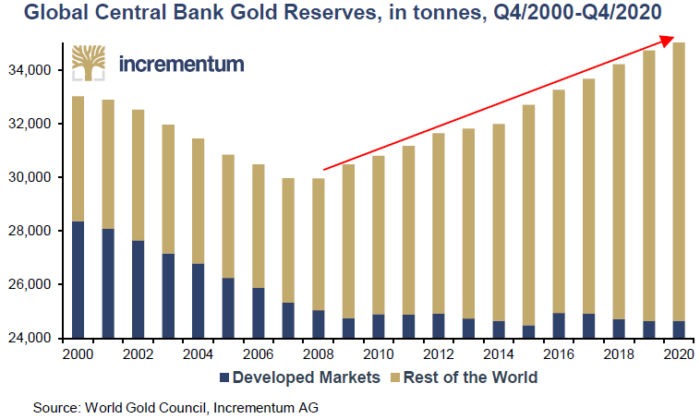

Evidently, China, Russia, Europe, and numerous emerging economies increasingly sought to reduce their dependence on the dollar, while simultaneously expanding their gold reserves. The process of de-dollarization was still gradual, but the direction was unmistakable. Central banks, especially in emerging markets, accelerated gold accumulation as they searched for politically neutral reserve assets.

Of relevance, the report framed gold as one of the few universally accepted monetary assets without counterparty risk. In a world characterized by geopolitical rivalries and financial weaponization, this characteristic became increasingly valuable.

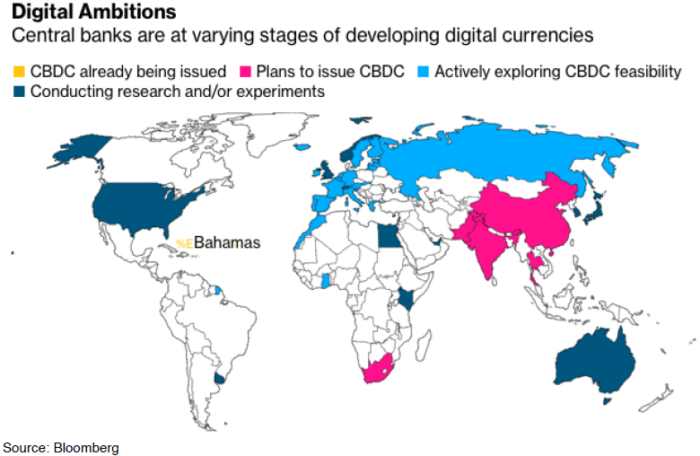

Related to the de-dollarization efforts, Central Bank Digital Currencies (CBDCs) became all the rage. However, due to their characteristics, we issued early warnings about them.

At the time, the topic was entering mainstream discussion. Hence, we inspected this matter thoroughly. Undoubtedly, as we found out, CBDCs should not be confused with decentralized cryptocurrencies like Bitcoin. Instead, they represented digitized fiat systems, potentially capable of enabling:

Greater financial surveillance

Programmable money

Direct policy transmission

Negative interest rate enforcement

Increased monetary control

The report therefore described CBDCs as “digitized fiat,” not freedom money.

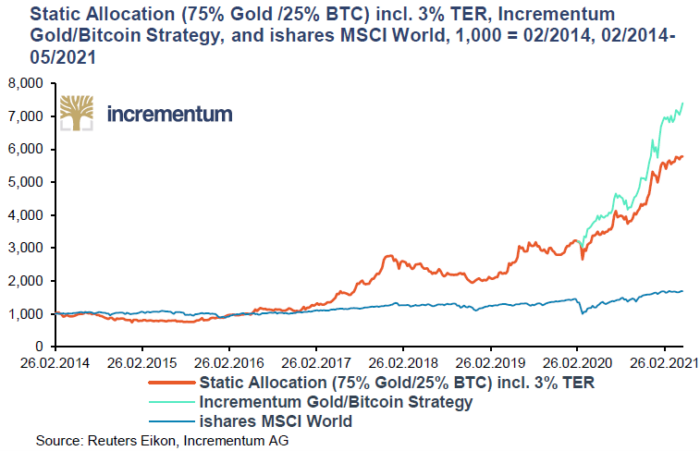

On the flip side, the report adopted a nuanced stance toward Bitcoin itself. Rather than framing Bitcoin and gold as rivals, the IGWT 2021 reinforced that both could coexist within a changing monetary landscape:

Gold as the time-tested monetary anchor

Bitcoin as an emerging digital hard asset

Inevitably, this framework would become one of the defining intellectual pillars of Incrementum’s investment thesis for the decade ahead.

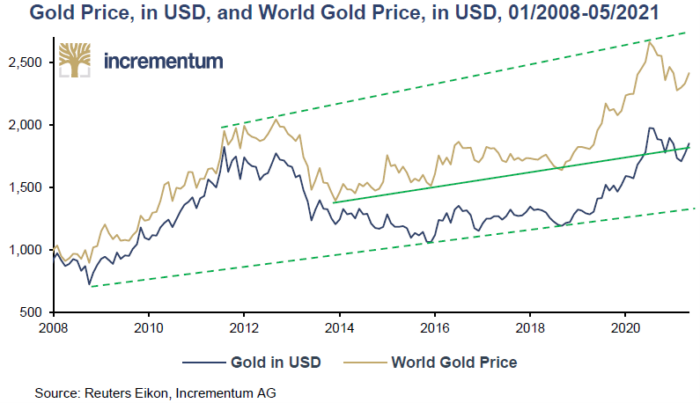

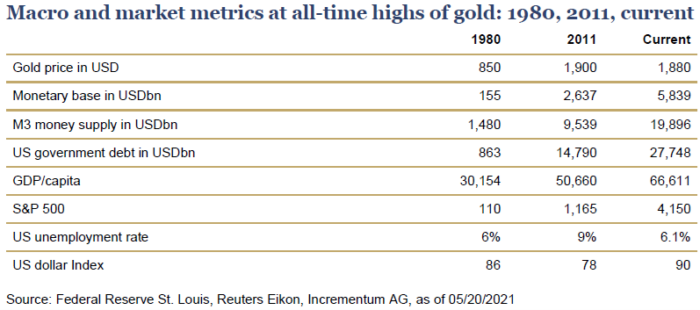

This edition was historically significant for another reason. It was the first IGWT report published after gold had finally broken above its 2011 highs.

For nearly a decade, the USD 1,921 level had represented one of the most important resistance zones in financial markets. When gold decisively exceeded that ceiling in 2020, the report interpreted it not as a short-term anomaly, but as confirmation that a new secular bull market had begun.

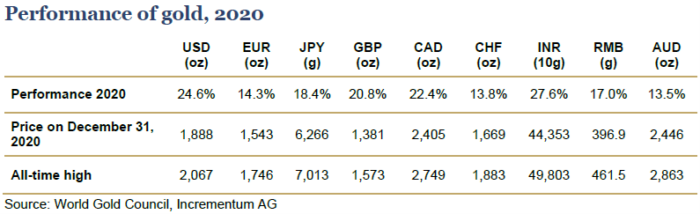

Overall, gold reached all-time highs in nearly every major currency:

+24.6% in USD

+14.3% in EUR

+27.6% in INR

This broad-based breakout reflected far more than currency weakness. Plainly, it signaled a profound change in the monetary environment itself.

Even though rising nominal yields, Bitcoin mania, and ETF outflows temporarily weakened sentiment toward gold in early 2021, IGWT strongly averred not to mistake consolidation for the end of the bull market.

Obviously, once new all-time highs were fully established in US dollar terms, a powerful new participation phase in the secular gold bull market would likely unfold.

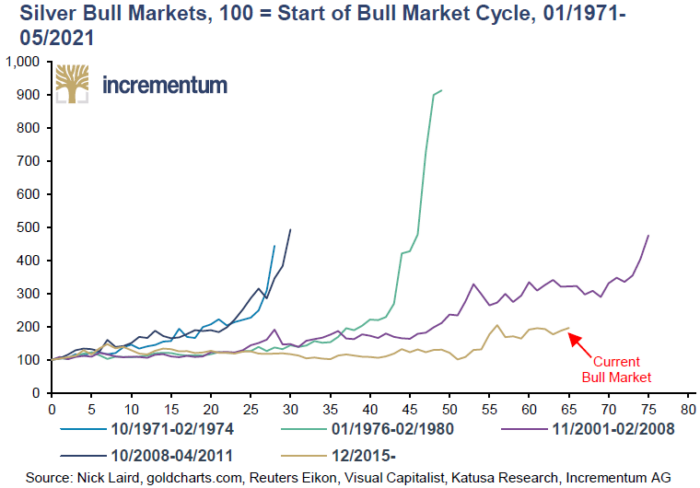

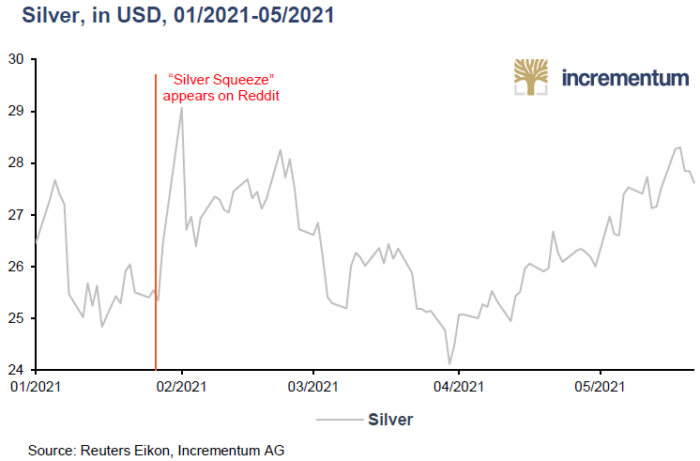

While gold had already broken decisively above its prior highs, silver still lagged behind in 2021. In any event, we regarded this divergence not as weakness, but as opportunity.

Historically, silver tends to underperform during the early stages of precious metals bull markets before eventually accelerating dramatically later in the cycle. Given its dual role as both a monetary and industrial metal, silver was deeply undervalued relative to gold. The growing importance of electrification, solar energy, and industrial demand further strengthened the long-term thesis for silver.

As later developments confirmed, silver would eventually break above both its 2011 highs and later even achieving all-time highs, surpassing the legendary 1980 peak during the ongoing Golden Decade.

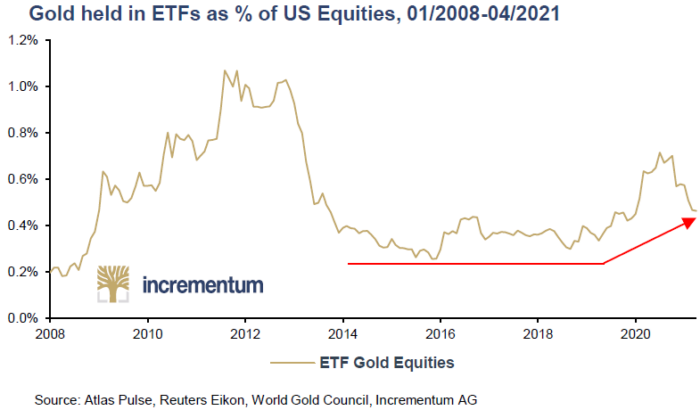

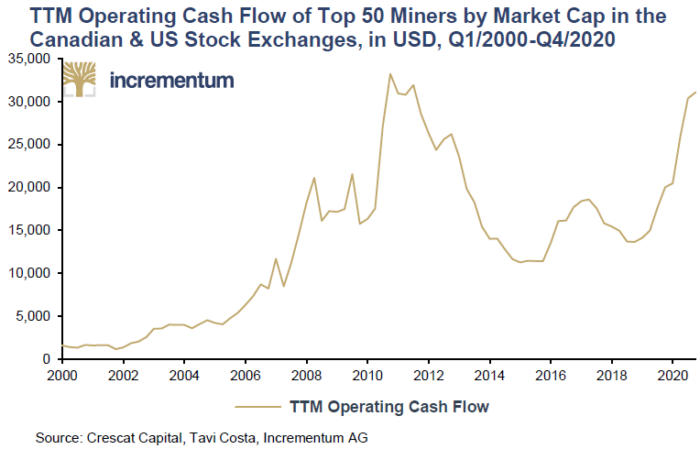

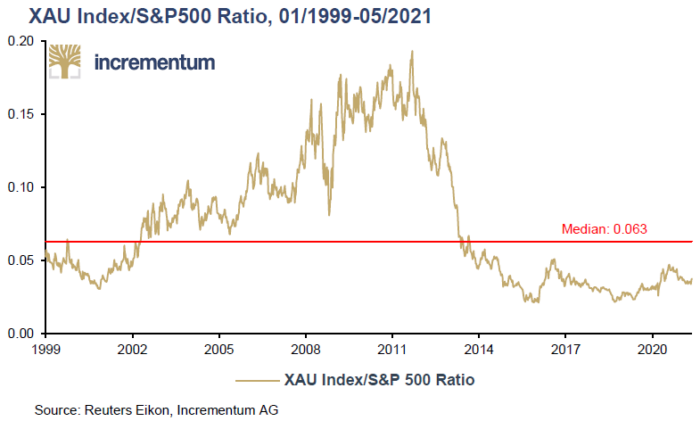

Despite rising precious metals prices, gold mining equities remained remarkably unloved in 2021.

This disconnect was one of the report’s most important investment observations. Mining companies had spent years improving operational discipline after the painful bear market of the previous decade. Balance sheets strengthened, free cash flow improved, margins expanded, and capital allocation became more shareholder friendly.

Despite that, investor sentiment toward the sector remained extremely depressed.

For these reasons, we claimed that mining equities offered asymmetric upside potential precisely because they remained so underowned and misunderstood. If gold continued rising within a structurally inflationary environment, miners could eventually become one of the strongest-performing segments within the financial markets.

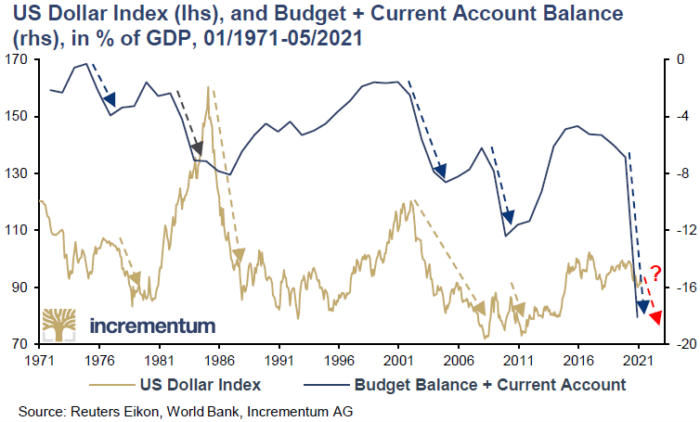

Another major macro theme explored was the sharp deterioration of America’s twin deficits:

The fiscal deficit

The current account deficit

In short, massive stimulus programs, emergency spending, and ultra-loose monetary policy unleashed one of the largest fiscal expansions in US history. At the same time, consumption surged while imports soared, further widening the current account imbalance.

Supposedly, such twin-deficit dynamics would normally place severe downward pressure on a currency.

However, one of the great paradoxes of the present era has been that the US dollar has demonstrated unbelievable resilience. Unquestionably, this is proof that confidence in the dollar system has hardly broken (completely), even though the underlying imbalances have become increasingly difficult to sustain.

At its core, the IGWT 2021 ultimately reaffirmed the timeless principle that gold is far more than an inflation hedge. Once again, the report examined gold’s unique ability to protect against the myriad of financial and economic risks and pitfalls.

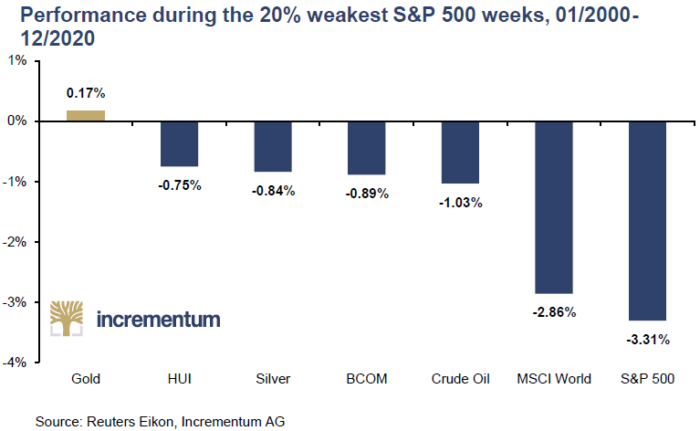

Strikingly, we analyzed the performance of several major asset classes during the 20% weakest weeks for the S&P 500 between 2000 and 2020. The findings were revealing.

While the S&P 500 itself fell by an average of 3.31% during these periods, global equities dropped 2.86%, crude oil declined 1.03%, the broader commodities complex lost 0.89%, silver fell 0.84%, and even gold mining stocks declined 0.75%. Conversely, gold posted a slightly positive return of 0.17%.

At first glance, such a figure may appear rather unremarkable. But compared to virtually every major asset class, gold has demonstrated why it is indispensable in long-term portfolio construction.

IGWT 2021 also explored one of the great contradictions of the decade:

The green transition itself depended on ultra-loose monetary policy, cheap energy, and massive debt creation.

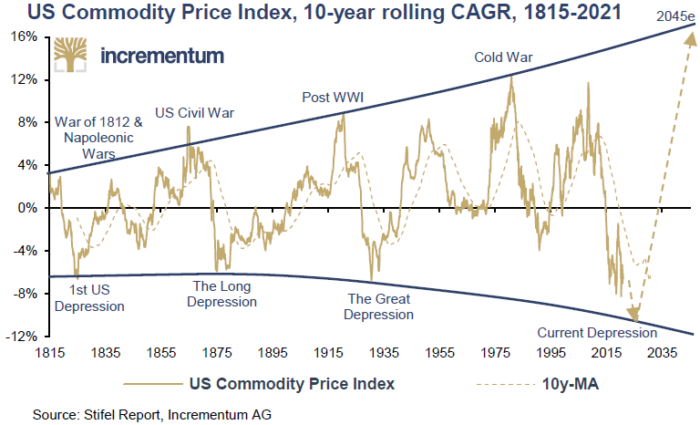

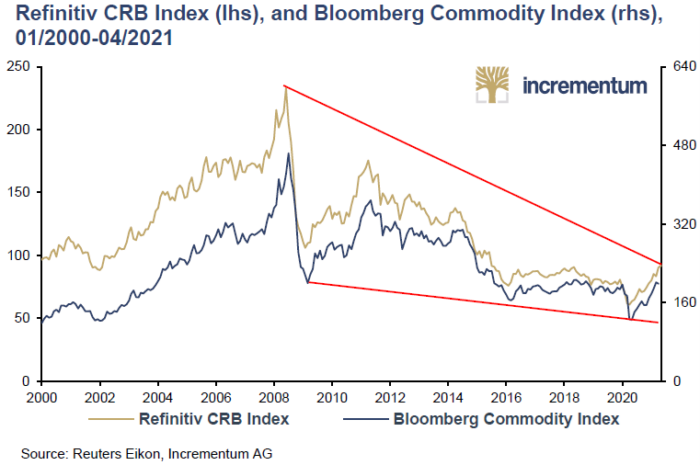

At the same time, commodity markets were beginning to awaken after years of underinvestment. Gold, silver, copper, and oil all strengthened, reinforcing the report’s thesis that the 2020s could resemble the inflationary commodity boom of the 1970s.

The report repeatedly emphasized that hard assets would become increasingly important in a world characterized by:

Higher inflation

Financial repression

Rising geopolitical fragmentation

Declining fiat credibility

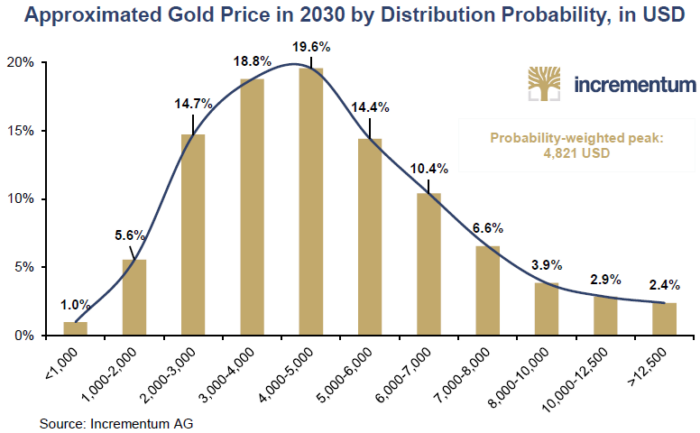

Perhaps the boldest aspect of IGWT 2021 was its unwavering confidence in the long-term outlook for gold.

The report reiterated the ambitious forecast first presented in the IGWT 2020, where w predicted that gold would reach USD 4,800 by the end of the decade.

Needless to say, many considered the projection unrealistic. Yet, by early 2026, gold managed to achieve this target years ahead of schedule.

Evidently, the thesis behind the forecast proved remarkably accurate. In many ways, the IGWT 2021 recognized earlier than most that the monetary regime itself was changing.

And once monetary regimes change, everything changes with them.

Looking back today, this edition stands as a comprehensive framework for understanding the structural transition unfolding across the global monetary system.

The report identified, well before the mainstream consensus:

The return of persistent inflation

The rise of financial repression

The fragility of debt-dependent economies

The limitations of central banking

The growing role of gold and hard assets in a changing world order

Most importantly, it recognized that the post-2008 regime of endless liquidity and financial engineering could not continue indefinitely without consequences.

The “Monetary Climate Change” described in 2021 was never simply about inflation statistics or market cycles. Indeed, it was about the gradual erosion of trust in the foundations of the fiat monetary system itself.

As history repeatedly demonstrates, whenever monetary trust begins to weaken, gold inevitably returns to the center of the conversation.

Dive back into this essential edition. Go to the Archive of the IGWT Report and explore the IGWT 2021 in full.

#20Years20Threads #InGoldWeTrust #GoldReport #GoldenDecade #GoldInvesting #GoldSurge #SilverSqueeze #SilverDemand #MiningStocks #PreciousMetals #Commodities #BullMarket #FundFlows #MonetarySystem #SafeHaven #InflationHedge #FinancialRepression #DeDollarization #CentralBanks #GoldReserves #HardAssets #CommoditySupercycle #SustainabilityReporting #EnergyTransition #YieldCurve #CBDC #Bitcoin #SoundMoney #FinancialMarkets #GlobalEconomy #PortfolioStrategy #AssetAllocation #MarketAnalysis #MacroResearch #AustrianEconomics #IGWT21 #IGWT26 #AnniversarySeries