The report argued that the world was no longer dealing with cyclical instability alone. Instead, multiple structural fault lines were converging at the same time.

The post-2008 financial order had been sustained by:

Ultra-low interest rates

Massive liquidity injections

Quantitative easing

Expanding public debt

Faith in central bank omnipotence

Seemingly, by 2023, that framework was beginning to crack.

Years of monetary excess collided with the inflationary consequences of pandemic stimulus, deglobalization, supply-side disruptions, and geopolitical fragmentation. The report described this moment as a decisive confrontation between the old financial regime and a new emerging reality.

In the end, the fundamental driver for a gold rally were all there:

“Is gold now already too expensive? We hear this question frequently, from customers, journalists and private investors. Given the current turbulent mixed situation, it is hard for us to imagine that we are at the end of a gold bull market. A comparison of various macro and market metricsat the time of the last two secular all-time highs in 1980 and 2011 with the currentsituation reinforces this view. The gold price definitely still has a lot of room tomove up.”

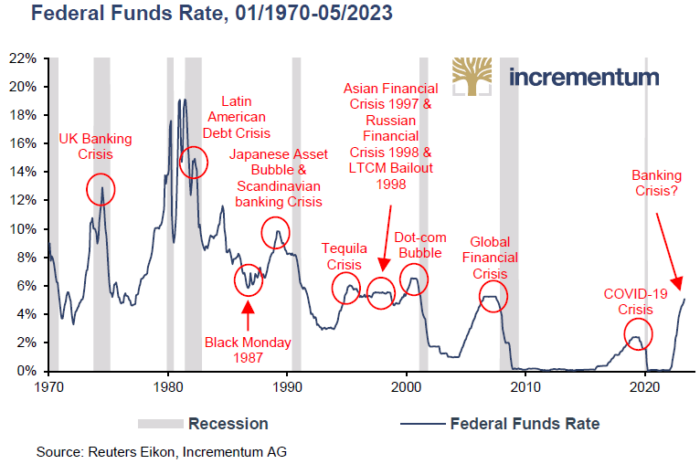

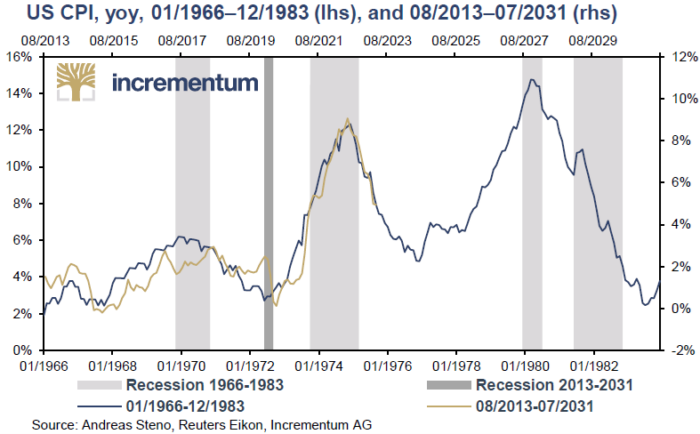

One of the report’s core arguments was that central banks had waited far too long to react to inflation.

For years, policymakers insisted that inflation was merely “transitory.” Jerome Powell repeatedly downplayed the persistence of inflationary pressures, while Christine Lagarde referred to the inflation surge as a temporary “hump.”

Reality turned out very differently. By 2023, inflation had become entrenched across much of the developed world, forcing central banks into the most aggressive tightening cycle in decades.

The Federal Reserve suddenly shifted from extreme monetary accommodation to historically rapid rate hikes. Demonstrably, Powell raised rates roughly twice as much in less than a third of the time Janet Yellen had required during the previous tightening cycle.

Unsurprisingly, this abrupt reversal exposed the painful truth that the global economy had become deeply dependent on cheap money.

In the IGWT 2023, we argued that central banks were trapped inside a monetary policy trilemma:

Price stability

Financial market stability

Economic support

Basically, pursuing one objective increasingly destabilized the other two. Ergo the cracks started appearing soon.

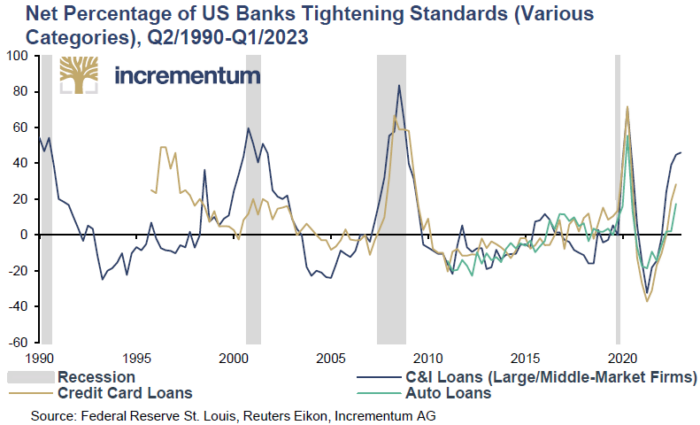

The report highlighted how the fastest tightening cycle in decades quickly triggered financial accidents.

The UK pension crisis, the collapse of FTX, liquidity stress in commercial real estate, and most importantly, the failures of Silicon Valley Bank, Signature Bank, and First Republic all revealed how fragile the financial system had become.

Three of the four largest bank failures in US history occurred within weeks of each other.

The report rejected the comforting narrative that these were isolated management failures. Instead, we framed them as symptoms of a system addicted to liquidity and structurally dependent on low interest rates.

Once again, the Austrian Business Cycle Theory featured prominently throughout the report.

In case you’re not on the know, artificial booms fueled by excessive monetary stimulus inevitably lead to painful busts once liquidity conditions tighten.

As Warren Buffett famously said:

“Only when the tide goes out do you discover who’s been swimming naked.”

By 2023, the tide was clearly going out.

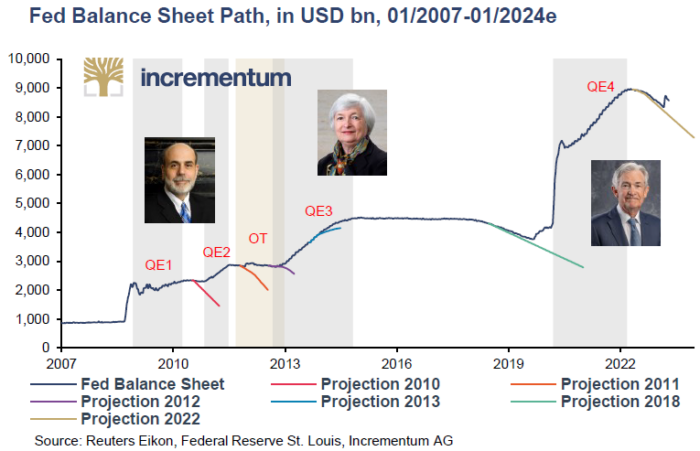

A particularly important insight from the IGWT 2023 was the idea that central banks could never truly normalize monetary policy without destabilizing the system.

The Federal Reserve was officially pursuing quantitative tightening, reducing its balance sheet while maintaining restrictive policy.

But when banking stress emerged in March 2023, the Fed quickly injected roughly USD 400bn back into the system.

Unquestionably, this revealed that whenever systemic stress appears, central banks ultimately revert to liquidity creation. Every attempt at meaningful balance sheet normalization since 2008 had either failed outright or been reversed during crises.

Therefore, we questioned whether that attempt at restrictive monetary policy was ultimately a bluff.

Would central banks truly tolerate a deep recession and widespread financial instability in order to defeat inflation? Or would they eventually pivot back toward stimulus, thereby reigniting inflationary pressures?

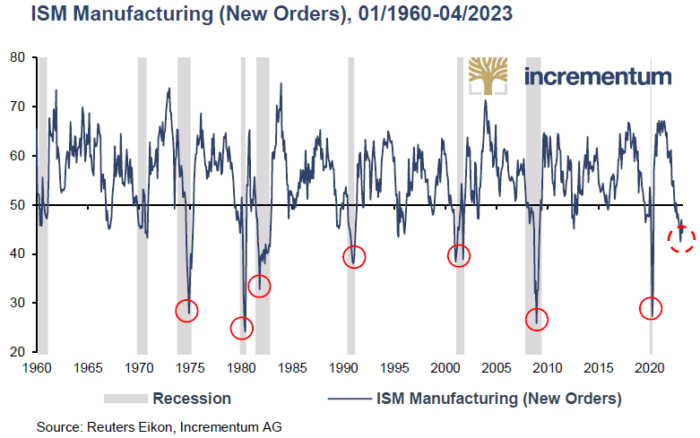

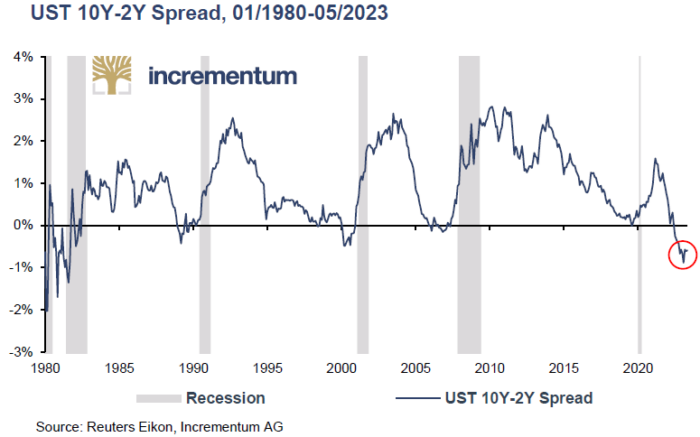

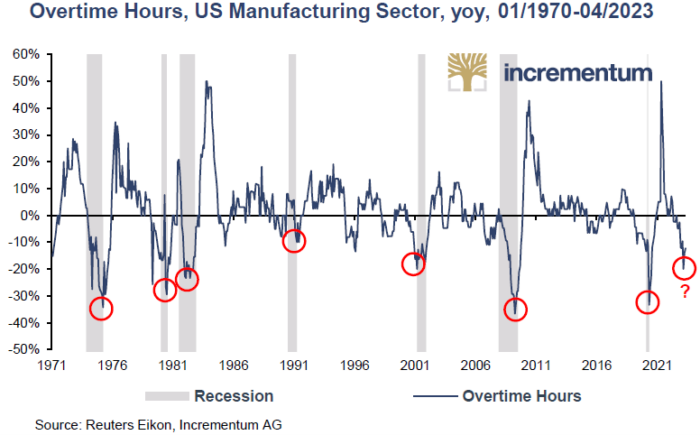

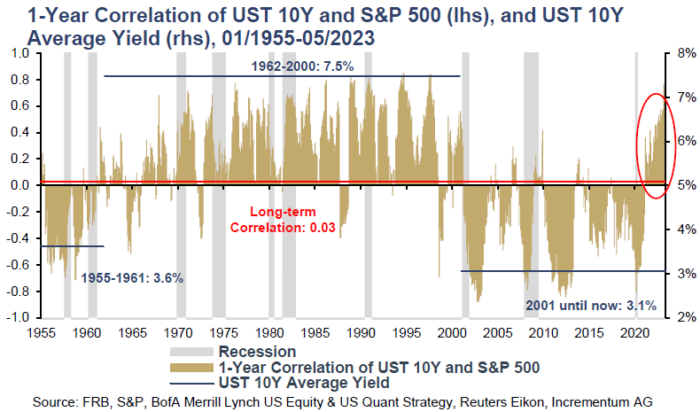

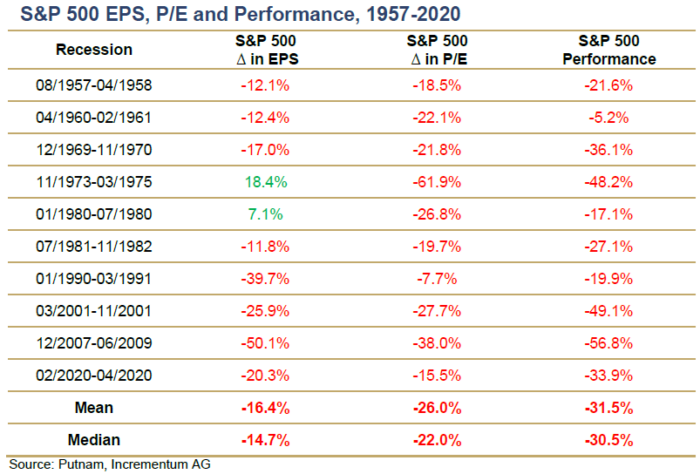

Another major theme explored in the report was the growing probability of recession. Insofar as the yield curve had inverted sharply and other leading indicators had been weakening, the odds of a recession in the US being called were rather high.

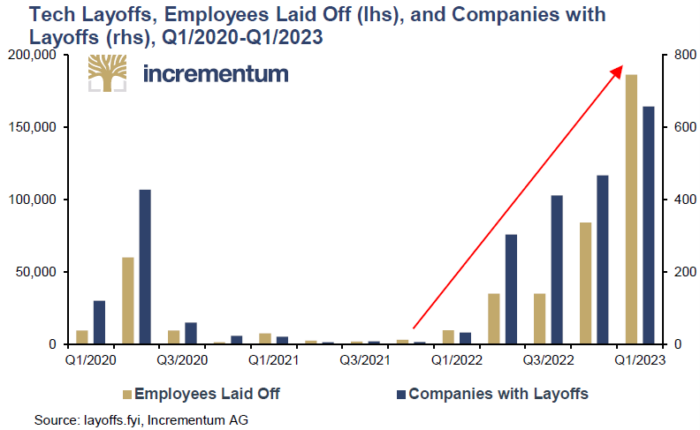

Furthermore, the labor market was softening. A growing number of companies were reducing their payrolls. Curiously, the tech industry was leading the charge with colossal layoff numbers.

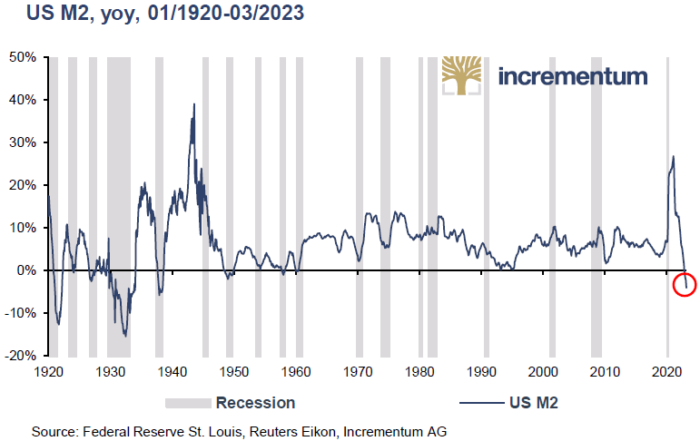

Perhaps most importantly, the US M2 money supply growth turned negative year-over-year for the first time since the Great Depression. Plainly, this development was historically unusual.

According to the Austrian perspective explored throughout the IGWT 2023, shrinking money and credit supply are powerful warning signals of economic dislocation. The report alerted that:

The longer recession was delayed, the more severe it could become

Asset bubbles inflated during the cheap-money era would eventually deflate

Policymakers would likely respond to future crises with even larger stimulus programs

In a nutshell, deflationary shocks would eventually trigger inflationary policy responses down the road.

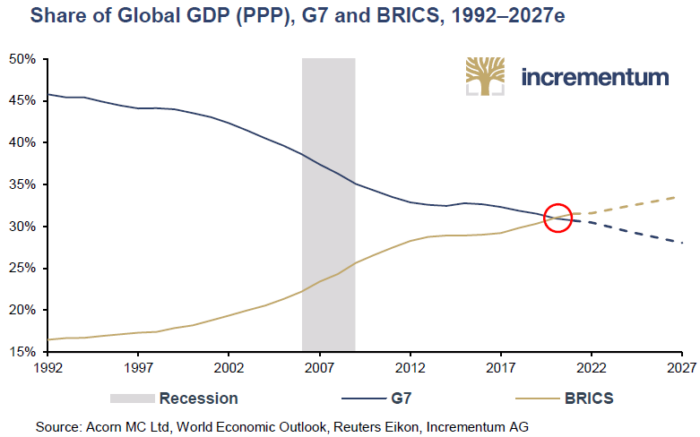

One of the defining themes of this edition was the growing geopolitical confrontation between the Western-led order and the emerging BRICS bloc.

The report argued that the world was moving away from the unipolar order dominated by the United States and toward an increasingly fragmented multipolar system.

At the center of this transformation stood China. Emphatically, the strategic rise of the BRICS nations and the accelerating shift in economic gravity away from the G7 economies.

The report framed this transition through the lens of the Thucydides Trap. In essence, this theory asserts that the rise of a new power inevitably creates tensions with the existing hegemon.

In this case:

The BRICS bloc increasingly challenged the Western-led financial order

China expanded its geopolitical influence across Asia, Africa, the Middle East, and Latin America

The US and its allies attempted to preserve the existing monetary architecture

Global trade, commodities, and reserve assets became geopolitical weapons

Evidently, this geopolitical fragmentation was no longer theoretical. As a matter of fact, it was already reshaping:

Trade flows

Currency arrangements

Commodity markets

Reserve management strategies

Capital allocation

In addition, China’s mediation between Saudi Arabia and Iran, the rapid expansion of BRICS+, and the growing use of yuan-based trade settlements were all interpreted as signs that a new geopolitical era was emerging.

On this account, the geopolitical showdown and the monetary showdown had become inseparable.

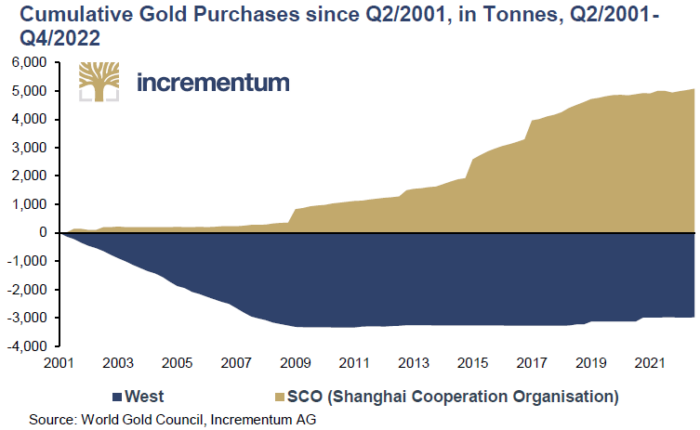

One of the most influential sections of the IGWT 2023 explored the accelerating process of de-dollarization.

For years, this phenomenon had been viewed as a fringe topic discussed mainly by macro specialists. By 2023, however, the trend had become impossible to dismiss.

Importantly, we hardly claimed that the US dollar would collapse overnight. Simply put, we described the process as tectonic plates slowly shifting beneath the global monetary system.

One of the report’s most fascinating intellectual frameworks came from Zoltan Pozsar (a.k.a., the repo guru) and his concept of Bretton Woods III.

According to Pozsar, the world was gradually transitioning away from the post-1971 fiat-dollar system toward a new order increasingly influenced by commodities, strategic resources, and neutral reserve assets.

In our featured interview, Pozsar’s thesis was highlighted:

Bretton Woods I was anchored by gold

Bretton Woods II was anchored by dollar-based financial assets

Bretton Woods III could become increasingly anchored by commodities and gold

This shift accelerated after the sanctions against Russia demonstrated that Western reserve assets and currencies could be weaponized geopolitically. As a result, many emerging-market countries increasingly viewed gold as politically neutral money.

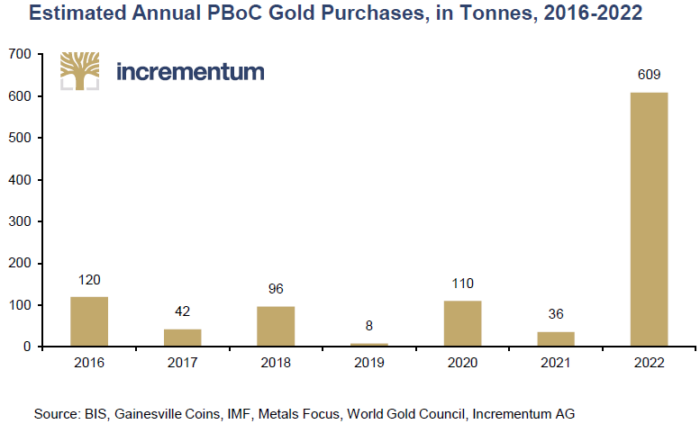

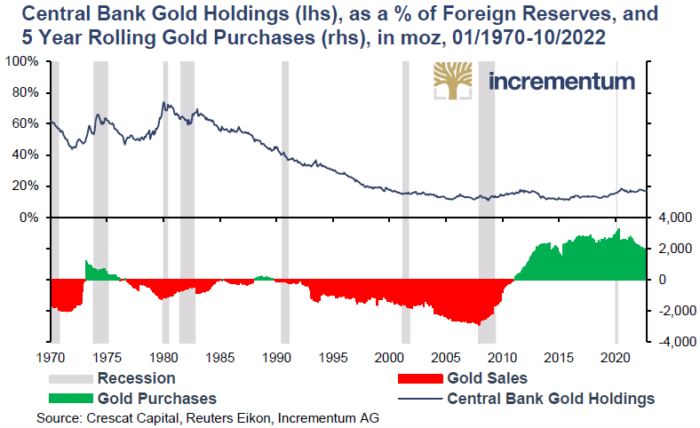

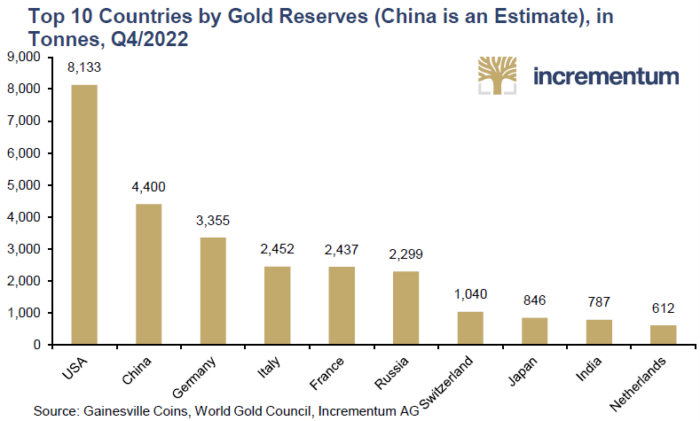

Indubtably, the relentless accumulation of gold by central banks represented one of the clearest signs that the global monetary order was evolving.

Thus, rather than disappearing, gold was quietly being remonetized.

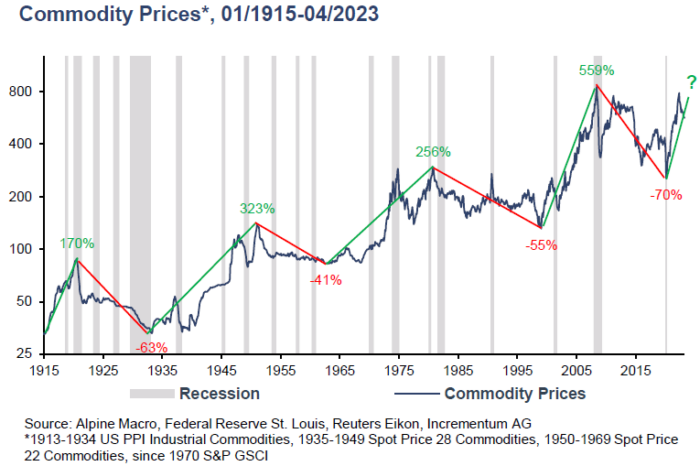

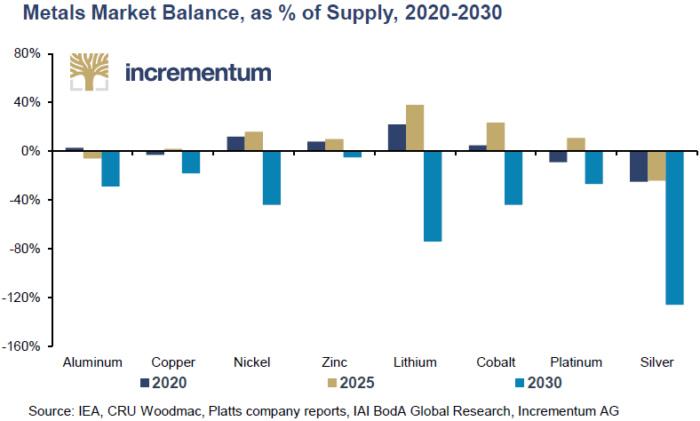

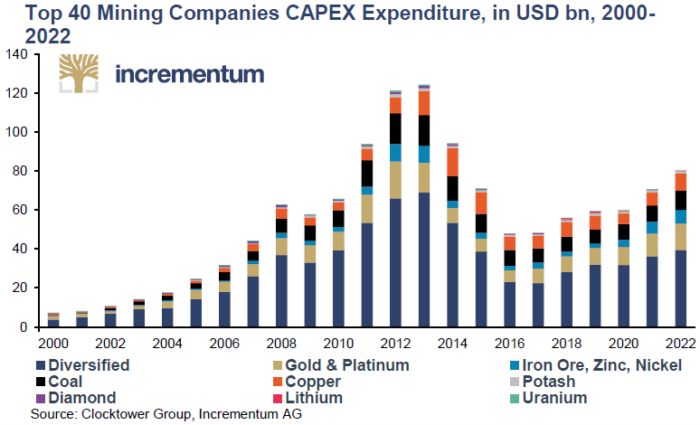

Another major theme explored in the report was the growing relevance of resource nationalism and energy scarcity.

Fundamentally, globalization was steadily giving way to strategic competition over commodities, energy supplies, and industrial metals. In fact, countries rich in natural resources increasingly sought to secure domestic supply chains and limit foreign dependence.

Examples cited throughout the report included:

Chile moving toward greater state control over lithium production

Indonesia restricting exports of key industrial metals

Governments prioritizing strategic commodity security

Growing geopolitical competition for energy and raw materials

Interestingly, the world was simultaneously facing:

Fossilflation — rising energy prices caused by underinvestment in traditional energy production

Greenflation — rising demand for metals and minerals required for the energy transition

Due to years of ESG-driven underinvestment, production and available stock across large parts of the commodity complex had grown immensely constrained.

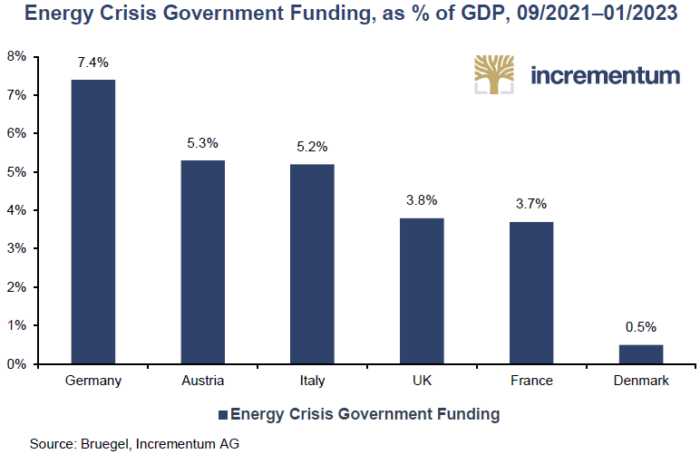

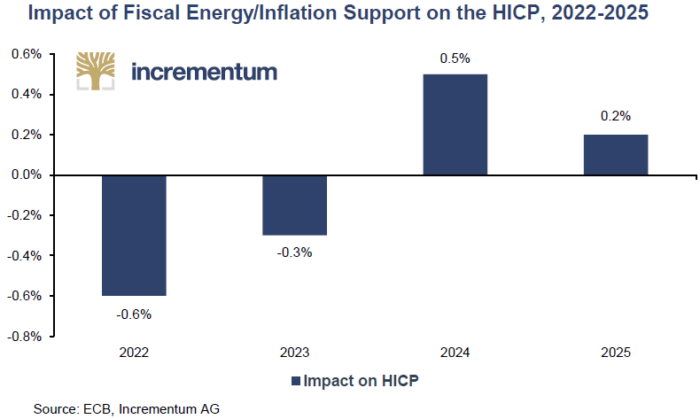

Discernibly, governments across Europe and other regions were forced to intervene aggressively to cushion households and corporations from soaring energy prices. Without surprise, these interventions were accompanied by great costs.

At the same time, the green energy transition required enormous quantities of copper, silver, lithium, nickel, uranium, and rare earth metals.

In hindsight, this became one of the report’s most important structural themes.

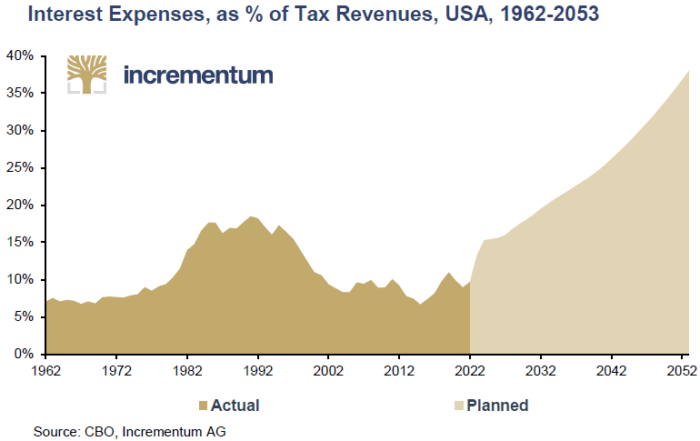

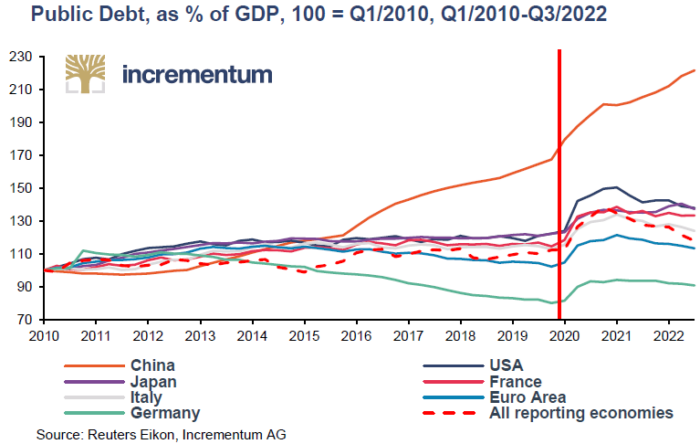

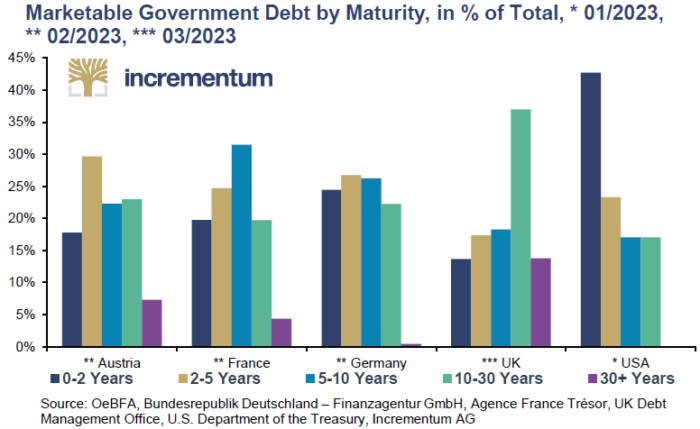

The deteriorating fiscal position of governments across the developed world was also inspected. Many years of deficit spending, pandemic stimulus, military expenditures, entitlement expansion, and rising refinancing costs had pushed sovereign debt burdens to historic extremes.

The report warned that public debt dynamics were becoming increasingly unsustainable.

In reality, government bonds were gradually losing their traditional perception as risk-free assets. Several factors contributed to this shift:

Persistently high inflation

Rising sovereign debt burdens

Declining confidence in fiscal discipline

Negative real yields

The weaponization of reserve currencies and sovereign assets

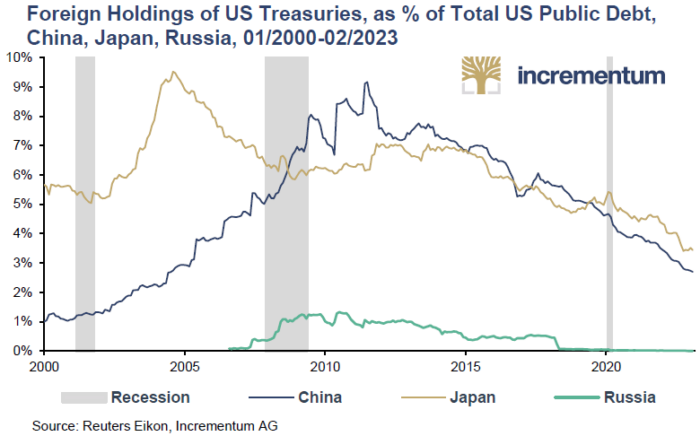

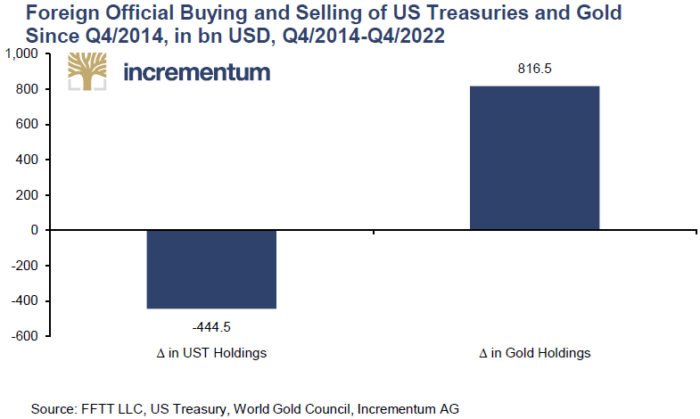

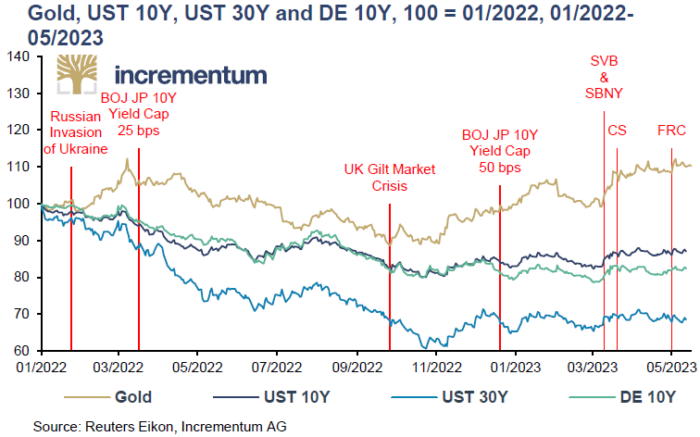

The freezing of Russian reserves after the Ukraine conflict profoundly altered how many countries viewed Western reserve assets.

Patently, US Treasuries and other sovereign bonds appeared to have lost the “risk-free” status that had put them at the basis of the whole monetary system.

Taking advantage of the situation, gold increasingly filled this vacuum. Unlike sovereign bonds, gold:

Carries no counterparty risk

Cannot be printed

Cannot easily be sanctioned

Is globally liquid

Functions outside the fiat system

That being said, gold was re-emerging as the ultimate safe haven asset in a world where traditional notions of monetary neutrality were eroding.

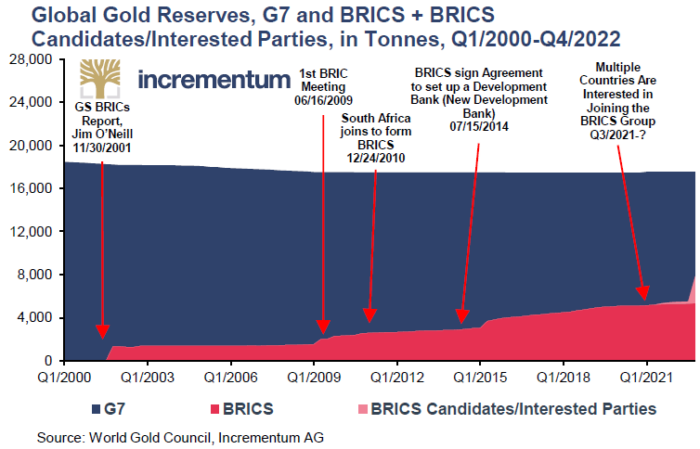

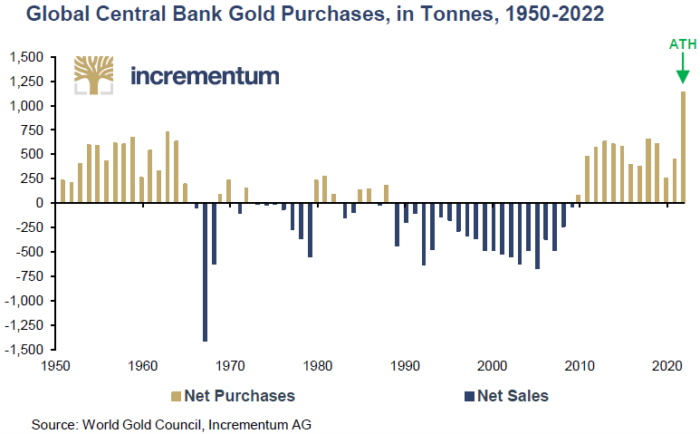

Perhaps the most important conclusion of the report was that gold was quietly regaining strategic importance inside the international monetary system.

Over the last couple of years, central bank gold purchases surged dramatically. Driving this trend were emerging market countries. For them, gold was viewed as:

A neutral reserve asset

A hedge against geopolitical fragmentation

Protection against sanctions risk

Insurance against fiat debasement

When the weaponization of the US dollar began at full steam the year before, gold began to effectively function as a neutral means of exchange and a true store of value.

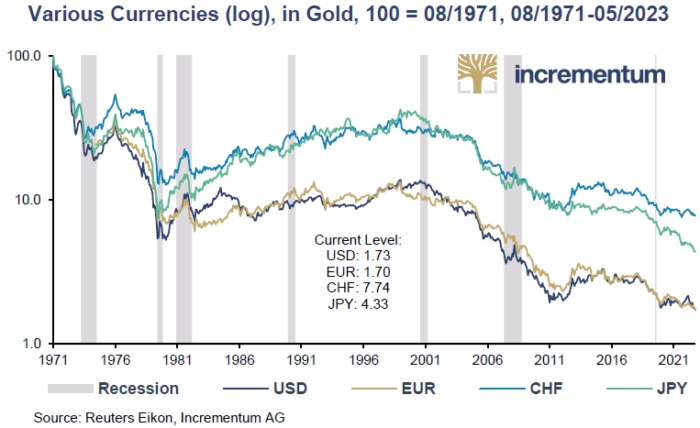

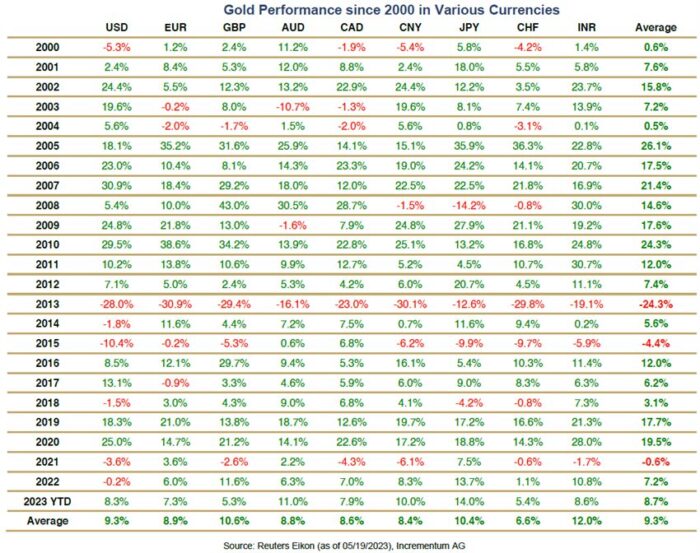

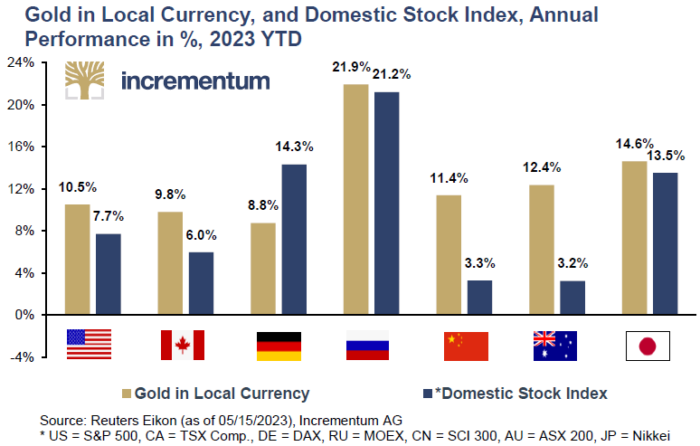

One of the report’s most compelling observations was that gold had already reached all-time highs in nearly every major currency, with the US dollar being the primary exception.

Crucially, this reflected that in lieu of gold becoming more expensive, fiat currencies were gradually losing purchasing power relative to gold.

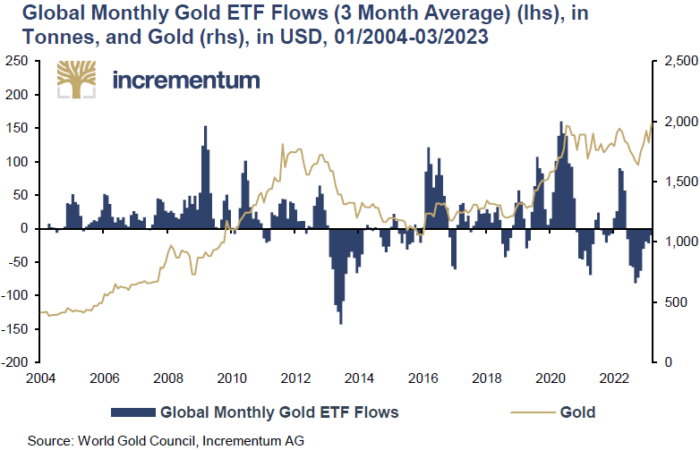

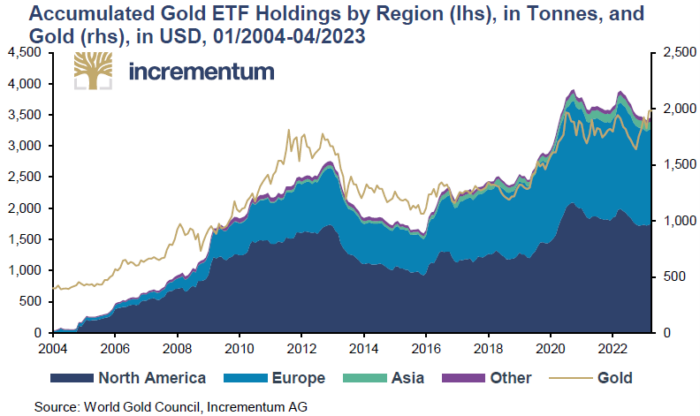

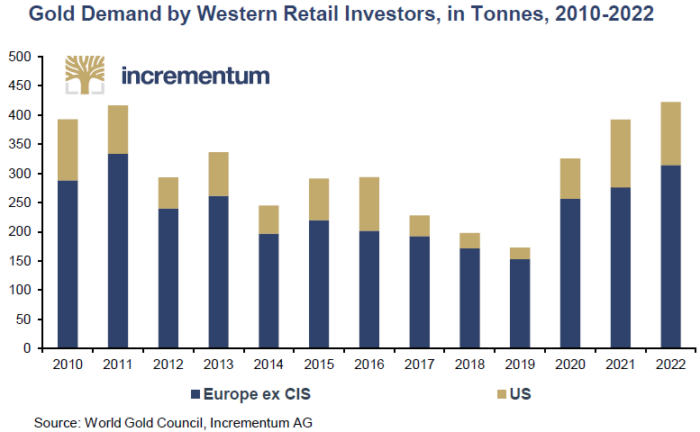

Furthermore, Western financial investors largely remained on the sidelines. During much of 2022 and early 2023, gold ETFs experienced extended outflows, reflecting skepticism toward the precious metals sector.

However, while ETF demand remained subdued, demand for physical gold was turning even more robust. The report emphasized that:

Wealthy investors increasingly preferred physical bullion over paper claims

Banking instability revived interest in tangible monetary assets

Unmistakenly, Western investors had not yet fully re-entered the market. Still, once gold decisively broke into new all-time highs, we expected FOMO-driven capital inflows to return rapidly to ETFs and institutional portfolios.

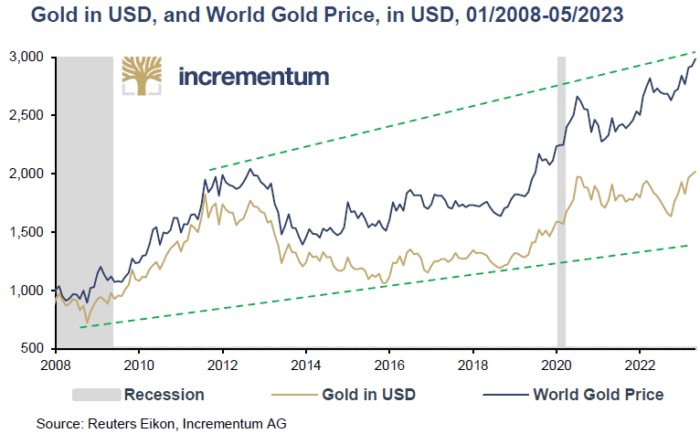

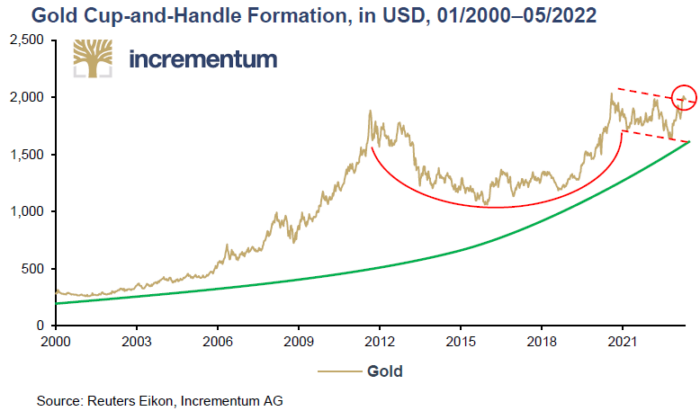

By 2023, gold had spent several frustrating years consolidating beneath the USD 2,075 resistance level.

The report analyzed how sentiment toward gold had weakened despite:

Persistent inflation

Banking instability

Massive debt burdens

Rising geopolitical risk

Record central bank buying

Nevertheless, from a technical perspective, the chart structure looked increasingly constructive.

The development of a giant cup-and-handle formation, stretching back more than two decades, suggested an imminent and powerful rally. As soon as gold decisively broke above resistance, a major new phase of the secular bull market would begin.

As we now know, that breakout finally arrived a few months later in 2023. What followed turned out to be one of the strongest advances in modern gold market history. Hence, the report identified the transition point remarkably well.

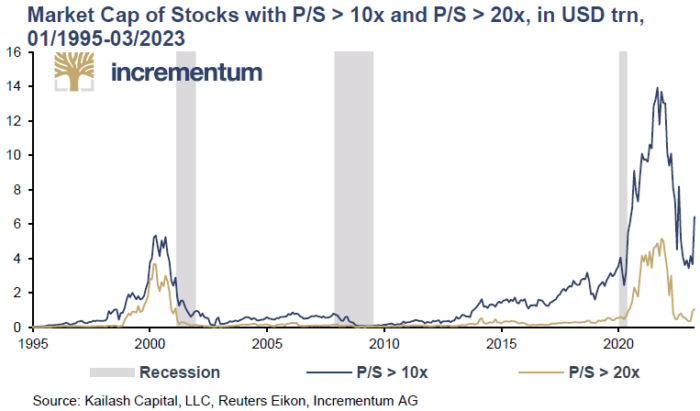

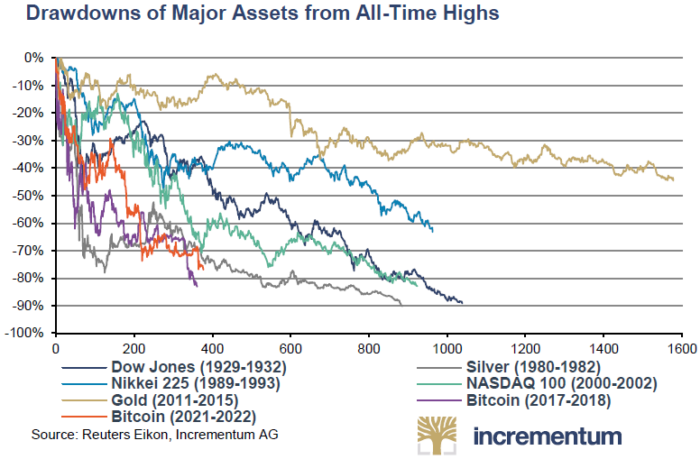

Another major theme throughout the IGWT 2023 was the ostensible bursting of the Everything Bubble, which was inflated during the era of zero interest rates, and its transition into the Everything Crash.

Bear in mind that more than a decade of artificially suppressed rates had inflated valuations across:

Equities

Bonds

Real estate

Venture capital

Technology stocks

Private markets

Cryptocurrencies

As central banks tightened policy aggressively, these distortions increasingly came under pressure. Once liquidity conditions tightened because of the hawkish stance:

Misallocations would be exposed

Valuation excesses would compress

Leverage would become destabilizing

Financial accidents would multiply

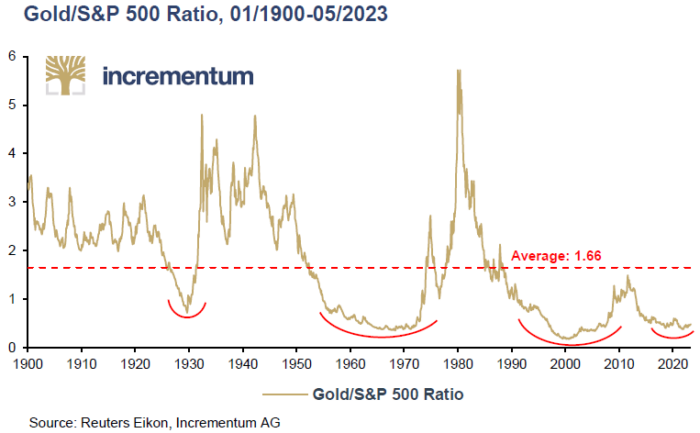

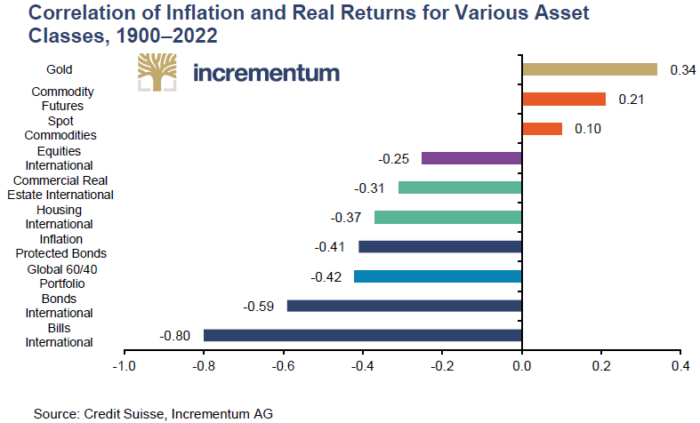

The report also highlighted that equities still appeared historically expensive relative to gold despite the 2022 bear market.

Considering historical episodes of financial panics and bear markets, besides the one that was unfolding, gold always managed to beat equities. Regarding the widespread corrections that had been unfolding across financial markets at that moment, gold continued to outperform many global equity markets.

For this reason, the secular revaluation of hard assets versus financial assets was still in its early stages.

Another fascinating aspect of this edition was its nuanced treatment of Bitcoin. Rather than framing gold and Bitcoin as enemies, we contended that both assets represented alternative responses to growing distrust in the fiat system.

The report explored:

Bitcoin as digital monetary challenger

Gold as timeless monetary ballast

The coexistence of both assets within portfolios

The growing demand for scarce, non-inflationary assets

Importantly, the IGWT 2023 maintained a balanced perspective. While acknowledging Bitcoin’s potential, we also emphasized:

Its volatility

Its speculative nature

Its comparatively short track record

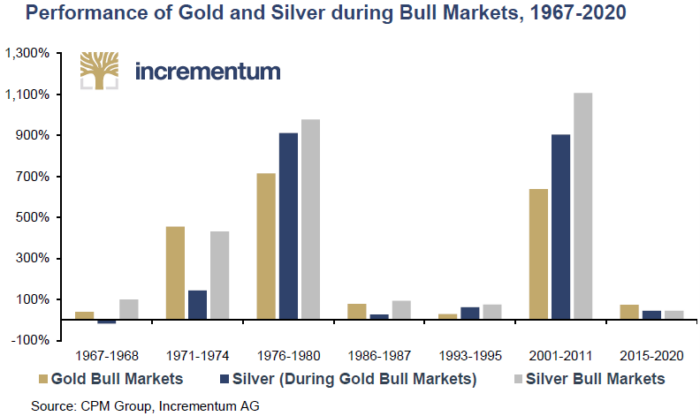

In any event, not that long ago, silver was deemed an extremely unstable and risky asset. Now, however, it has solidified its role as a long term inflation hedge.

Speaking of silver, this metal took a more prominent position in the IGWT 2023 compared to previous years.

Essentially, silver’s long-term outlook was improving significantly due to a rare convergence of monetary and industrial demand drivers. The white metal was no longer viewed solely as a speculative monetary metal. It was increasingly perceived as a strategic industrial resource as well.

Unlike gold, silver benefits from:

Monetary demand during periods of currency debasement

Industrial demand linked to electrification and solar energy

Tightening physical supply dynamics

Historically depressed relative valuation versus gold

Distinctly, silver’s role in the energy transition was becoming increasingly important. Solar panels, electrification infrastructure, semiconductors, and green technologies all required substantial quantities of silver.

In addition, years of underinvestment constrained mine supply growth.

All things considered, silver could eventually outperform gold during the later stages of the precious metals bull market.

Fast forward to 2026 and silver has done just that.

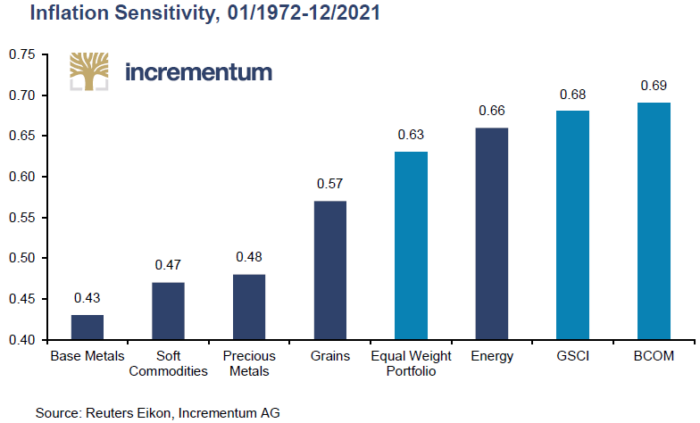

The long-term commodity supercycle thesis was also revisited.

In short:

Years of underinvestment had constrained supply

ESG policies discouraged mining investment

Geopolitical fragmentation increased resource nationalism

The energy transition would require enormous quantities of raw materials

As a result, commodity markets could enter a prolonged structural bull market.

Specifically, we highlighted the undervaluation of precious metals mining stocks. Despite improving fundamentals, many mining companies continued trading at historically depressed valuations.

Undoubtedly, the secular hard asset bull market was quietly rebuilding beneath the surface, even if most investors remained focused on technology and growth equities.

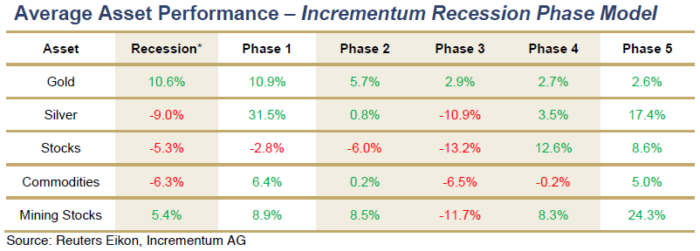

The most important analytical framework introduced in this edition was the Incrementum Recession Phase Model.

Basically, the model examined how different asset classes have historically behaved throughout the various phases of past recessions.

Its conclusions strongly reinforced gold’s role as a portfolio diversifier and recession hedge. On the flip side, the traditional 60/40 portfolio framework faced significant structural challenges in the emerging macro regime.

Finally, the IGWT 2023 also reaffirmed the long-term bullish outlook established in previous editions of the report.

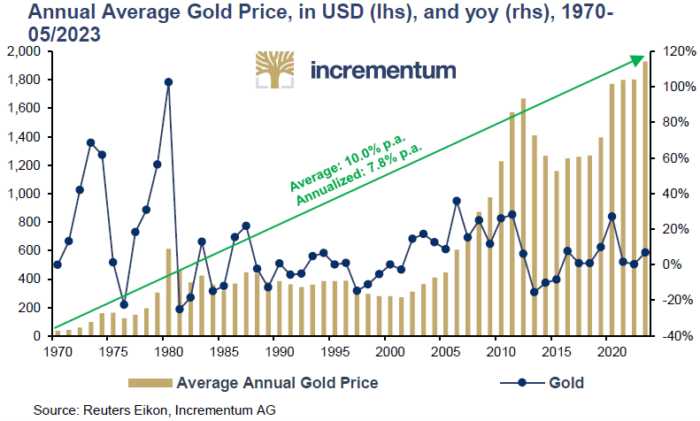

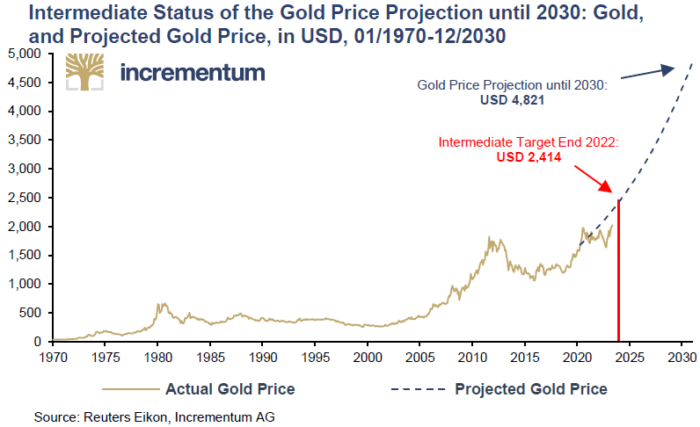

Back in the IGWT 2020, we had introduced the now familiar 2030 gold price target of roughly USD 4,800.

At the time, many observers viewed the forecast as highly ambitious. Yet, by early 2026, gold had already reached that level.

Therefore, the projection that once seemed radical, has ultimately proved to be too conservative.

More than anything else, this edition captured the emergence of a new macroeconomic era.

Manifestly , the world was moving away from:

The era of endless monetary accommodation

Unquestioned faith in central banks

Stable globalization

Low inflation

Financial repression hidden beneath cheap money

And toward a new regime defined by:

Geopolitical fragmentation

Resource competition

Debt saturation

Fiscal dominance

Persistent inflationary pressures

Renewed interest in hard assets and monetary neutrality

In hindsight, the “Showdown” thesis was highly prescient, with the report being published a few months before gold’s decisive breakout into terra incognita.

All in all, the structural forces identified throughout its pages continue shaping markets today.

More than a report about gold, the IGWT 2023 expounded about the transformation of the global monetary order.

Moreover, it explored the fragility of debt-saturated financial systems, the limits of central banking, the resurgence of geopolitical rivalry, the re-monetization of gold, and the growing skepticism toward fiat currencies.

Most importantly, it argued that the world had entered an era where multiple systemic showdowns were unfolding simultaneously.

Surely, that assessment now appears more relevant than ever.

Dive back into this essential edition. Go to the Archive of the IGWT Report and explore the IGWT 2023 in full.

#20Years20Threads #InGoldWeTrust #GoldReport #GoldInvesting #GoldDemand #SilverSqueeze #SilverDemand #PreciousMetals #SoundMoney #MiningStocks #Bitcoin #HardAssets #BullMarket #ConsolidationPhase #InflationDynamics #SafeHaven #InflationHedge #CentralBanks #MonetaryPolicy #ReserveAssets #DeDollarization #MonetarySystem #GoldReserves #BRICS #EmergingMarkets #MultipolarWorld #InvestorDemand #CommoditySupercycle #DebtGrowth #FinancialMarkets #AssetPerformance #PortfolioStrategy #WealthManagement #GoldenDecade #GlobalEconomy #Geopolitics #AustrianEconomics #MarketAnalysis #MacroResearch #IGWT23