The Six Vectors of Gold Remonetization

“Topics such as de-dollarization, the remonetization of gold, and the use of digital central bank currencies to build a new financial system are on the agenda.”

Zoltan Pozsar

- No return to the gold standard – but gold is returning. Not by decree, but by function. Not by revolution, but by evolution. Six vectors are driving this process – each observable on its own, yet collectively selfreinforcing.

- Vector I – Reserves: Since the freezing of Russian FX reserves in 2022, the rule has been: Reserves that are not physically controlled are not reserves in an emergency. The wave of repatriation is proof of this.

- Vector II – Private: The largest institutional demand gap in monetary history. Pension funds hold less than 2% gold.

- Vector III – Balance Sheet: Silent recapitalization is already underway. Bundesbank: EUR 387bn; Eurosystem: EUR 1,274bn. In February 2025, Treasury Secretary Scott Bessent publicly signaled the monetization of the asset side – the market interpreted this as a harbinger of a gold revaluation.

- Vector IV – Anchoring: The Trump-Bessent-Shelton trio. Judy Shelton’s Treasury Trust Bonds – 50-year, gold-convertible, planned launch on July 4, 2026 – are the concrete instrument for a politically viable reanchoring.

- Vector V – Accumulation: The West is still asleep. Since 2010, central banks have accumulated 9,700 t of gold – almost exclusively in the East. A moderate rebalancing by the Western “gold-light” group would release 2,000–3,000 t.

- Vector VI – Digitalization: Tokenized gold beats CBDCs. While CBDCs are programmable and monitorable, tokenized gold remains currency – neutral and censorship-resistant.

A look at monetary history reveals that the question of “sound money” was never purely academic in nature but has always been of central importance for economic stability and social order. The past five decades of the pure fiat experiment are, measured against 5,000 years of monetary history, a brief anomaly. And anomalies tend to be corrected.

Our thesis of a remonetization of gold may seem bold at first glance, which makes a clear conceptual framework all the more important. Those waiting for the reintroduction of a classical gold standard will be disappointed: Governments have no incentive to voluntarily relinquish the fiscal and monetary flexibility that the fiat regime offers them. Rather, what is meant is a process in which gold regains monetary relevance. Not necessarily as money in the strict sense, but certainly as the ultimate reference asset for value, trust, and settlement.

This remonetization does not occur by decree, but through function; not through revolution, but through evolution; not a sudden fanfare, but a steadily rising crescendo. Paradigm shifts often creep in through customs, certainties, and economic necessities. Gold is not moving to the center of the system. Rather, driven by fiscal exhaustion, geopolitical fragmentation, and dwindling institutional trust, the system is moving toward gold.

What connects the following six vectors is a shared underlying structure: At each of these junctures, gold regains a key role as a store of value and a safe haven. Not all vectors will become reality simultaneously or in their entirety, but several parallel channels should suffice to sustainably strengthen gold’s monetary relevance.

Vector I: Reserve Function and Store of Value: Gold as a Sanction – Resistant Reserve Asset

In the transition from a hegemonic to a multipolar world, the question of the resilience of government reserves is taking on new significance. Since the freezing of Russian central bank reserves in February 2022, it has become clear that in the event of a crisis, fiat currency reserves carry not only a market risk but also a political risk of default. Reserves are thus no longer merely liquidity buffers; they are part of the political power architecture.

For countries outside the Western sphere of influence, this raises a fundamental question: How can trade surpluses be stored in such a way that they do not fall under foreign control in the event of a conflict? In this context, gold possesses a characteristic that no fiat reserve asset can offer: It is a reserve asset without issuer risk or counterparty risk. These characteristics are not new. What is new is that gold has once again become politically relevant.

From a game-theoretical perspective, the argument is stronger than it initially appears. This is not just about Russia. The mere possibility of freezing assets has redefined the concept of “risk-free reserves” for all nations. Even with a low probability of occurrence, the expected loss in a binary, all-or-nothing risk event is so high that diversification becomes rational. The logic of insurance applies: One does not insure against the probable, but against the intolerable.

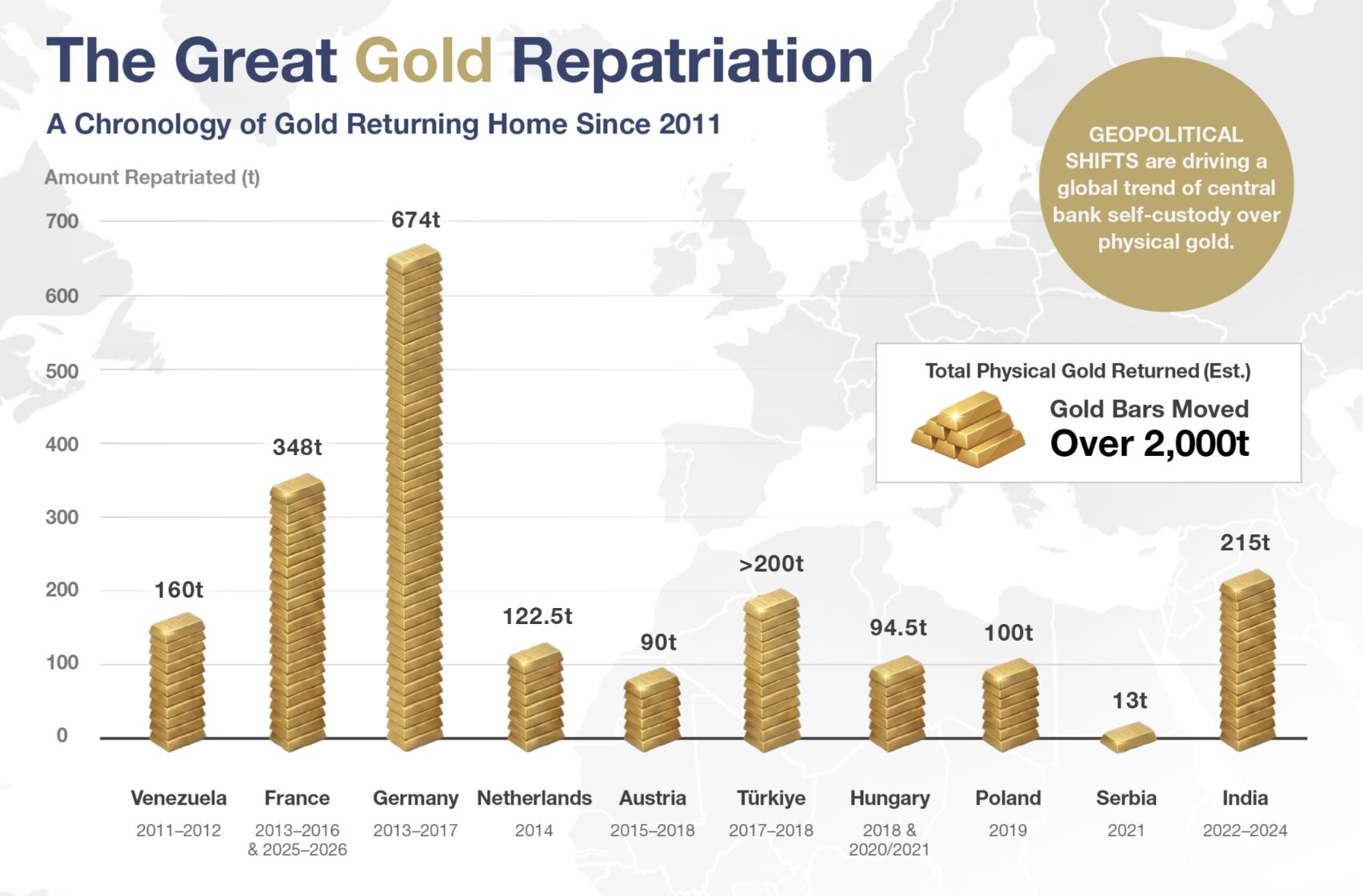

We view the ongoing trend toward the repatriation of gold reserves as empirical evidence of this thesis:[1]

- Between 2013 and 2017, Germany repatriated a total of 674 t from New York and Paris.

- The Netherlands brought back 122 t in 2014.

- Poland is systematically transferring gold to Warsaw.

- Between July 2025 and January 2026, France moved its last 129 t from New York – through sales and repurchases in Europe – realizing a book profit of around 13bn euros in the process.

In this regard, gold should primarily be understood as a store of value. It is not yet a dominant international means of payment. But it is regaining importance as a reserve asset that cannot be frozen, devalued, or denied access to at the push of a button in extreme situations. In a world of increasing bloc formation, that is precisely the decisive advantage.

At the same time, alternative settlement architectures are emerging: Russia and China are conducting parts of their trade in yuan and rubles; the Shanghai Gold Exchange is gaining importance. At the 2024 BRICS summit in Kazan, a joint settlement platform was discussed in which gold could serve as neutral collateral. For years, we have viewed the ongoing de-dollarization and its implications for gold as one of the defining trends of this decade.

From the petrodollar to petrogold

In a multipolar world, a historical connection is taking on new significance: that between commodity trade and gold. The petrodollar system – the tacit agreement in place since 1974 to invoice oil in US dollars and recycle the surpluses into US Treasuries – is losing its binding power. Jeff Currie, longtime head of commodities research at Goldman Sachs, sums up the shift: US dollar recycling is increasingly becoming gold recycling. Oil surpluses no longer flow into US Treasuries, but into gold.

Saudi Arabia is increasingly accepting yuan for oil deliveries to China; the Shanghai Gold Exchange offers a direct conversion mechanism for this: Yuan proceeds can be converted directly into physical gold via SGE contracts, without the detour through the US dollar. Luke Gromen views the pricing of oil in gold equivalents as “inevitable” and points to the gold-to-oil ratio as a barometer for the health of the petrodollar system.

Source: In Gold We Trust Report 2025, National Central Banks, Of cial Publications, BOE, MiningVisuals, Incrementum AG

Should this pattern solidify – oil for yuan for gold – a de facto petrogold cycle would emerge. While in the classic petrodollar system energy revenues flow back into the US financial system as demand for US Treasuries and finance the US current account deficit, this backflow does not exist in the petrogold system. The revenues go into vaults instead of bonds. This undermines both global demand for the US dollar and the US’s ability to refinance its deficits on favorable terms.

The petrogold cycle does not replace the petrodollar, but creates a parallel framework. The implication for remonetization: Gold would not only gain importance as a reserve asset and balance sheet instrument, but would also function as a settlement medium in commodity trading for the first time since the end of Bretton Woods. This would directly link the reserve function, settlement, and digitization.

Vector II: Private Remonetization – When Institutions Rediscover Gold

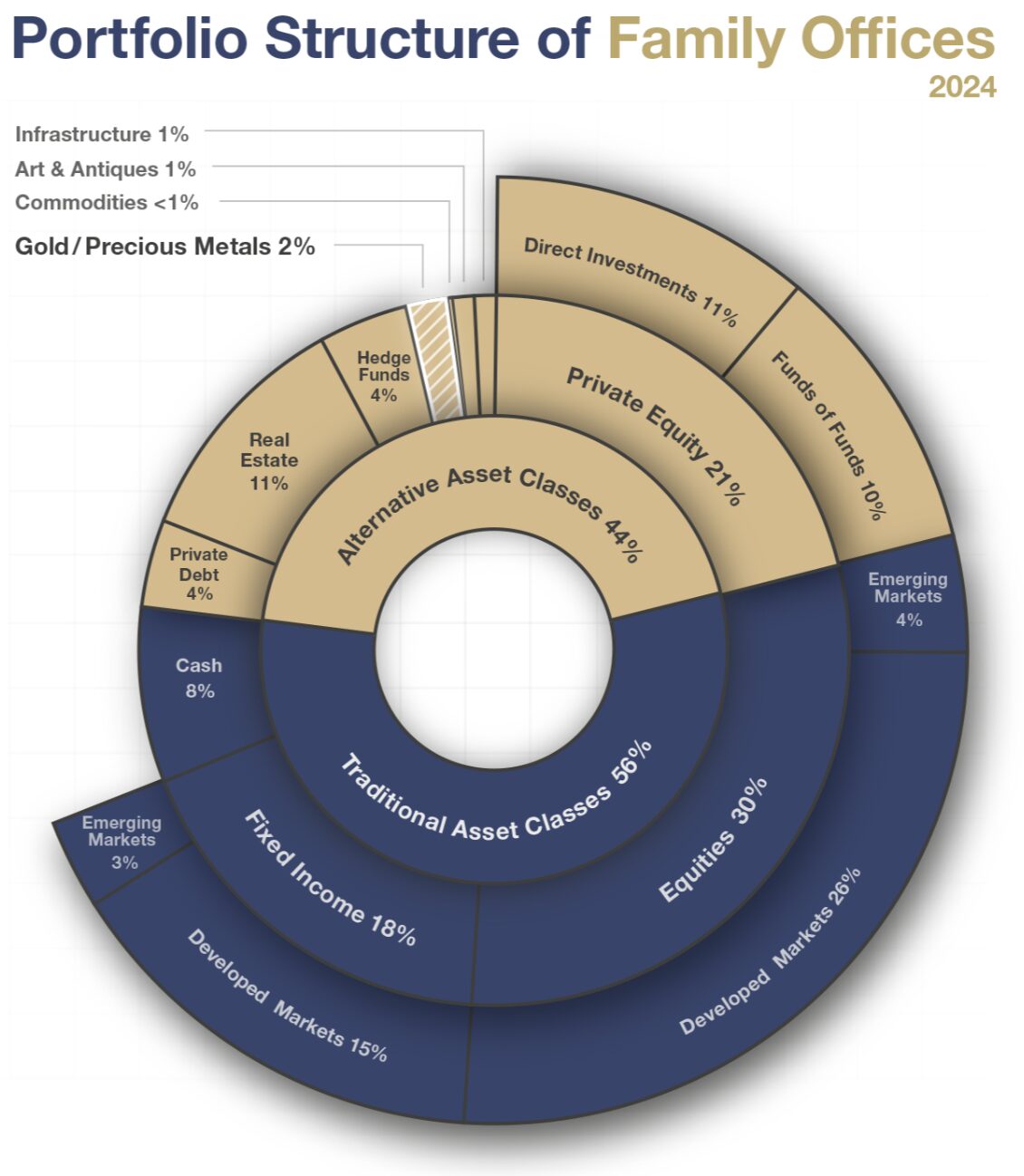

The debate to date on the remonetization of gold has focused almost exclusively on central banks and governments. In doing so, it overlooks a crucial feedback loop: private remonetization. When institutional investors such as pension funds, sovereign wealth funds, family offices, or insurance companies once again treat gold as a primary liquidity reserve, this fundamentally changes the market structure and increases pressure on policymakers to follow suit.

The starting point is remarkable: Despite the historic gold price rally of recent years, institutional allocation remains marginal. According to a WGC/OMFIF survey , over 70% of the pension funds and insurance companies surveyed hold less than 2% in gold. For most large asset managers, gold remains a tactical, not a strategic, allocation; the average gold allocation in a traditional 60/40 portfolio is estimated at 0.5–1%.

At the same time, several developments point to a turning of the tide. Net inflows into physically backed gold ETFs reached record levels in 2024 and 2025. The holdings of the world’s largest gold ETFs stood at over 3,200 metric tonnes at the end of 2025, exceeding the gold reserves of individual G7 countries. In Europe, the assets under management of the largest physically backed gold security, Xetra–Gold, climbed to a record EUR 20.8bn with 172.8 t of gold holdings. This is a remarkable signal for demand in German-speaking countries.

What these figures obscure: There is a massive discrepancy between verbal endorsement and actual allocation. Over 80% of institutional investors surveyed describe gold as a sensible portfolio component. In practice, this is hardly reflected in the allocation data. The reasons are structural: regulatory hurdles, benchmark-driven thinking – most asset managers are measured against bond or stock indices that do not include gold – and that peer-risk logic that John Maynard Keynes recognized as early as 1936: “It is better for reputation to fail conventionally than to succeed unconventionally.”[2] Those who hold gold and underperform in the short term lose their mandate, whereas those who hold the benchmark do not.

The fiscal and geopolitical stress factors of the other vectors also affect the private sector. In a world of rising government debt, negative real returns, and geopolitical fragmentation, when pension funds seek a hedge without issuer risk, they inevitably turn to gold. The first signs are visible: In the Netherlands, a pension fund was mentioned in public debates in 2024 due to its strategic 5% gold allocation; in Switzerland, a major pension fund has integrated gold into its overlay strategy.

The relevance of this vector lies in its feedback effect: Private remonetization increases demand, drives up the price, and thereby improves central banks’ balance sheets (see Vector III). It increases political pressure on regulators to treat gold as recognized collateral, and it creates a market infrastructure that in turn facilitates digitization (see Vector VI). Private remonetization is thus not a byproduct of government remonetization; it is its catalyst.

Source: UBS, MiningVisuals, Incrementum AG

Vector III: Valuation, Accounting & Recapitalization – Gold as a Balance Sheet Lever

Central to gold’s role as a store of value are key issues of valuation, accounting, and ultimately recapitalization. These have two dimensions: an accounting one and a functional one.

1. The accounting dimension

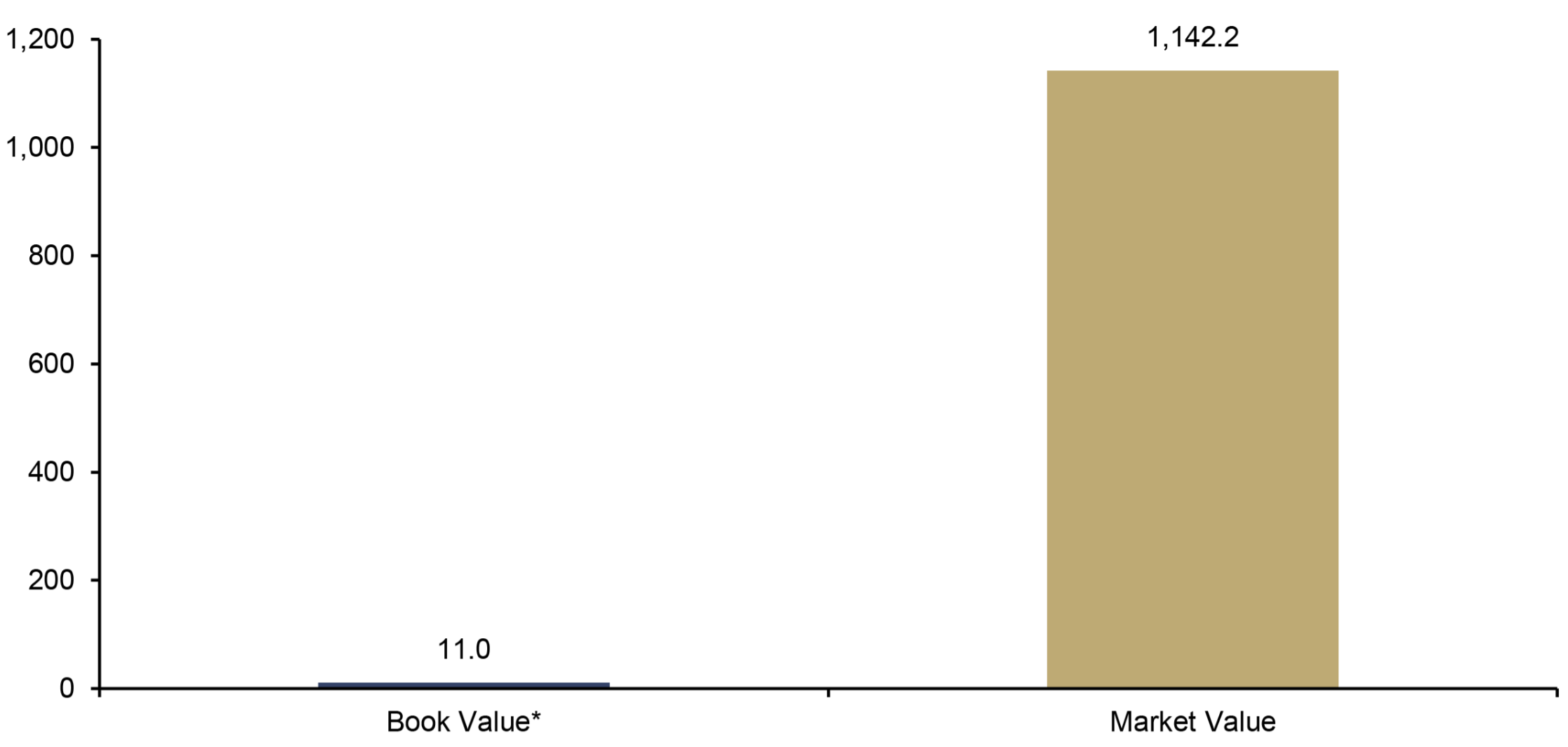

The most spectacular case of accounting undervaluation is found in the US. US gold reserves are recorded in the books at a price of USD 42.22 per ounce, which has been fixed by law and unchanged since 1973. At current market prices of around USD 4,600, this amounts to less than one hundredth of the actual value; the revaluation gap for the 261.5moz thus totals approximately USD 1.2trn. The gold is not owned by the Federal Reserve but by the Treasury; the Federal Reserve merely holds gold certificates at the statutory price.

The Eurosystem has gone a step further. Since the ECB’s founding in 1999, the central banks of the euro area have valued their gold reserves quarterly at market prices. The resulting unrealized gains are recorded in the revaluation account and effectively function as equity without the need to sell physical gold.

Deutsche Bundesbank: The revaluation reserve for gold reached a historic high of EUR 387bn at the end of 2025. The Bundesbank’s gold is thus valued at roughly 45 times the 2025 net loss of EUR 8.6bn and more than 14 times the cumulative balance sheet loss of EUR 27.8bn. The gold position itself climbed to EUR 395bn, with acquisition costs of just EUR 8bn. As early as 2023, Executive Board member Joachim Wuermeling explicitly referred to the balancing item as part of “own funds”, a remarkable departure from the traditional view.

ECB/Eurosystem: The value of gold reserves rose to EUR 1,274bn in 2025, a sharp increase compared to EUR 872bn in 2024.

Swiss National Bank: The SNB holds approximately 1,040 t of gold at market prices. With the gold price rising by 45.9% to CHF 110,919 per kilogram in 2025, the unchanged holdings resulted in a valuation gain of CHF 36.3bn, following CHF 21.2bn the previous year. In the case of the SNB, it is particularly revealing that the massive SNB equity portfolio incurred the largest loss in the SNB’s history in 2022, amounting to CHF 132bn. But it was the gold reserves that stabilized the balance sheet.

2. The functional dimension

Gold no longer functions merely as a reserve but as an instrument of silent recapitalization. In a system with global debt exceeding 350% of GDP, this creates room for maneuvering on the asset side of government balance sheets without incurring new debt.

Historical experience, as systematically documented in the study “Official Reserve Revaluations: The International Experience,” shows that the fiscal use of such revaluation gains is not merely a theoretical construct. Three precedents are particularly relevant:

- Germany in 1997: Chancellor Helmut Kohl and Finance Minister Theo Waigel attempted to use DM 20bn from the revaluation of the Deutsche Bundesbank’s gold reserves to meet the Maastricht criteria. Bundesbank President Hans Tietmeyer blocked this move, viewing it as an attack on the Bundesbank’s independence. What was politically untenable at the time is increasingly seen as an option today in the context of rising government debt.

- Italy 2002: The Banca d’Italia transferred EUR 13bn from its adjustment account to cover losses from the conversion of nonmarketable government bonds. This set a precedent for practical applicability within the Eurosystem.

- South Africa 2024: The central bank and the Ministry of Finance agreed to transfer 150bn ZAR (approx. 2% of GDP) from revaluation gains between 2024 and 2027 to reduce debt.

In the US, too, the boundaries of what is said and thought are shifting. Treasury Secretary Scott Bessent stated in February 2025: “We’re going to monetize the asset side of the US balance sheet for the American people.” At the same time, the Federal Reserve published its aforementioned study on international gold revaluations, and Senator Lummis’s bill called for a revaluation of gold certificates at market price.

The central question is thus less whether a revaluation will take place but rather how the gold will be functionally utilized: as collateral, as a balance sheet stabilizer, or as fiscal leeway. This reveals a regulatory inconsistency: Capital rules treat gold with a 0% risk weighting, yet gold is denied HQLA status. The system implicitly recognizes the monetary quality of gold – the offsetting entries are the balance sheet evidence – but denies explicit institutional recognition.

In this context, the “Freegold” thesis gains relevance. It’s a concept attributed to the pseudonymous analyst FOFOA (“Friend of a Friend of Another”):[3] Gold exerts its monetary effect most strongly when it is not tied to a fixed exchange rate but is freely valued on the market, as the Eurosystem has effectively anticipated with its quarterly mark-to-market valuation since 1999.

In addition, Bitcoin is establishing itself as a parallel, nonsovereign reserve asset – not as a substitute for gold but as a complementary option: Gold stabilizes government balance sheets through physical substance; Bitcoin expands strategic flexibility in the digital realm. Together, they could serve as outlets for the recapitalization of an overindebted system.[4]

US Gold Reserves, in USD bn, 12/2025

Source: Federal Reserve St. Louis, World Gold Council, Incrementum AG *USD 42.22 per troy ounce

Vector IV: Gold-Backed Bonds as an Anchor of Credibility

Dr. Judy Shelton – described by the Financial Times as “Trump’s favorite economist,” nominated twice by Trump to the Federal Reserve Board of Governors in 2019 and 2020, and narrowly defeated in the US Senate (47–50) – proposed a mechanism for repegging the US dollar to gold in her 2024 book Good as Gold: How to Unleash the Power of Sound Money. She proposes the issuance of 50-year, gold-convertible, zero-coupon bonds, which she calls Treasury Trust Bonds (TTBs). Symbolically, she hopes for a launch on July 4, 2026, the 250th anniversary of the Declaration of Independence.

Shelton’s political credibility is remarkable: She was a member of Trump’s 2016 Treasury Landing Team and co-author of the Federal Reserve chapter of Project 2025. She has publicly praised Treasury Secretary Scott Bessent as “a proud economic historian”. (He refers to himself tongue-in-cheek as a “gold bug”.) The Trump-Bessent-Shelton constellation thus forms the most ideologically cohesive pro-gold trio at the helm of a US administration in at least a generation. In our exclusive interview in this In Gold We Trust report, Shelton argues that TTBs would strengthen confidence in fiscal discipline without restricting monetary flexibility.[5]

The fiscal incentive for policymakers is considerable: With a gold-backed bond, the coupon rate decreases because the gold backing partially offsets the default risk for the investor. For policymakers seeking ways to lower the interest burden without austerity programs, this is a compelling argument.

The difference between a gold-backed bond and a conventional government bond is akin to the difference between a promise and a pledge.

The urgency grows with every budget cycle. The creeping loss of confidence ultimately forces issuers to regain trust through real collateral. Not a gold standard, but a credibility standard.

The precedents exist: The US issued gold-clause bonds until 1933; the Joint Resolution of 1933 invalidated these and was only amended by the Act of October 28, 1977, so that gold clauses are enforceable again for contracts entered into on or after that date. France issued gold-indexed bonds in 1936; Italy discussed using its gold reserves as collateral in 2011-12.

We see a promising testing ground in emerging markets with their own gold production. Uzbekistan, Kazakhstan, and Ghana would have a dual incentive: lower borrowing costs and the monetization of their own gold production. Zimbabwe took the lead in April 2024 with Zimbabwe Gold (ZiG) and launched a gold-backed currency, albeit with questionable success so far.

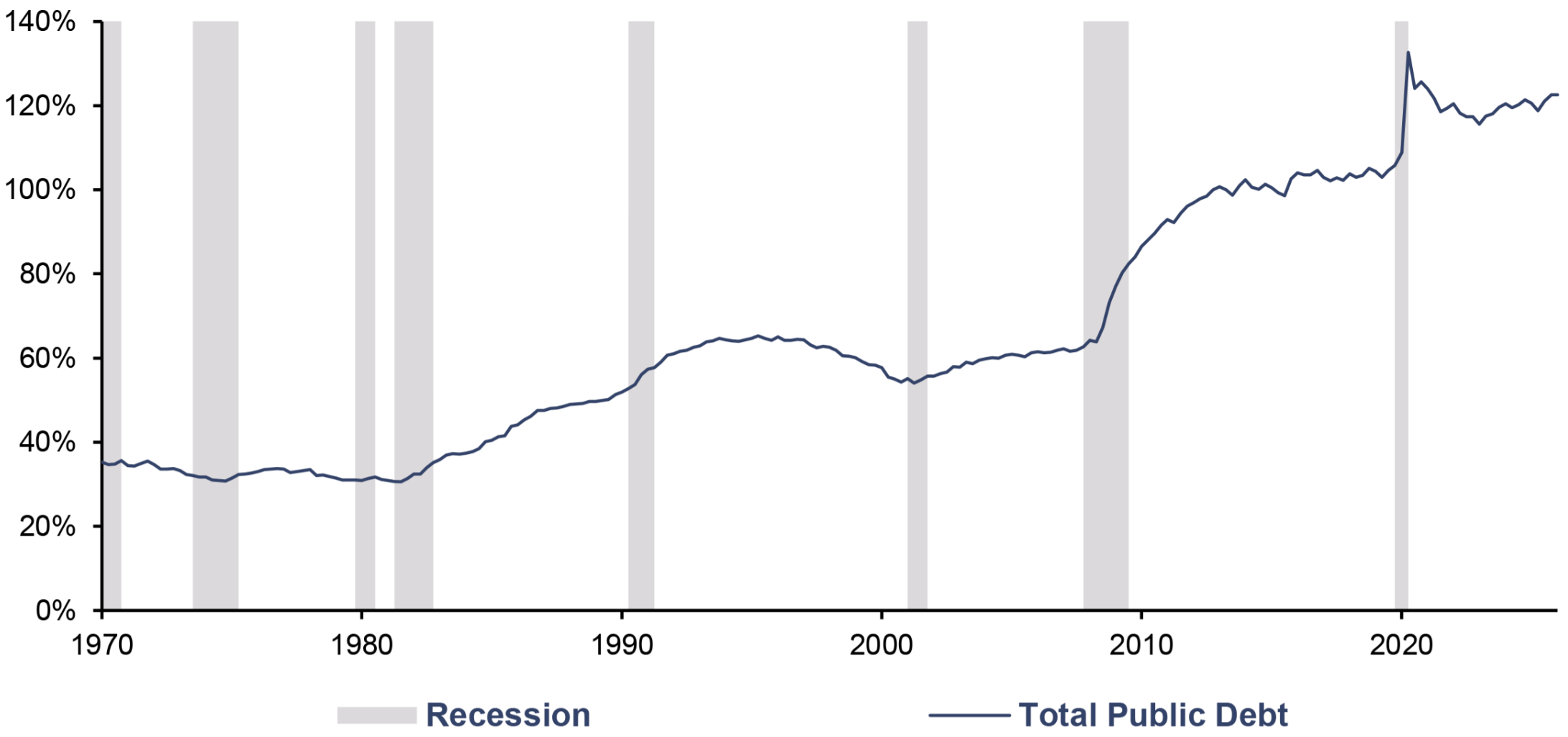

US Total Public Debt, as a % of US GDP, Q1/1970–Q1/2026

Source: LSEG, Incrementum AG

Vector V: Western Central Banks Are Becoming Gold Buyers

Since 2010, central banks worldwide have accumulated a net total of approximately 9,700 t of gold, with almost 4,000 t of that coming in the years 2022–2025 alone. However, these purchases were made almost exclusively by emerging economies. Western central banks have stood by and watched, and in some cases even sold off their reserves. The next phase will begin when the West follows suit.

Why have Western central banks bought so little gold to date? The psychological hurdle is high: An open increase in gold reserves would be an implicit admission that the fiat system is reaching its limits. Poland deserves special attention: NBP President Adam Glapinski is the pioneer in this regard within the EU. His argument: “Gold symbolizes the strength of the country.” This is a statement that is likely to increasingly resonate with European conservatives as well.

The symmetry of sanctions

The freezing of Russian currency reserves in 2022 has brought an uncomfortable truth to light: Reserves that one does not physically control are not reserves in a crisis. This lesson is often cited as an impetus for the East to diversify away from the US dollar. Yet the lever works both ways.

China’s rare earth export controls starting in 2025, and the export bans on germanium, gallium, and antimony since December 2024 are, in effect, the mirror image of the freezing of currency reserves on the real-economy side. With nearly 90% of the world’s rare earth refining capacity, Beijing controls materials that are indispensable for defense, semiconductors, and the energy transition.

The logic is symmetrical: One side controls the financial infrastructure, the other the physical. Both sides are learning the same lesson: Dependence is vulnerability. And the only form of reserve that is subject to neither financial nor physical vulnerability is gold in one’s own vaults.

The blind spot in Western reserve portfolios

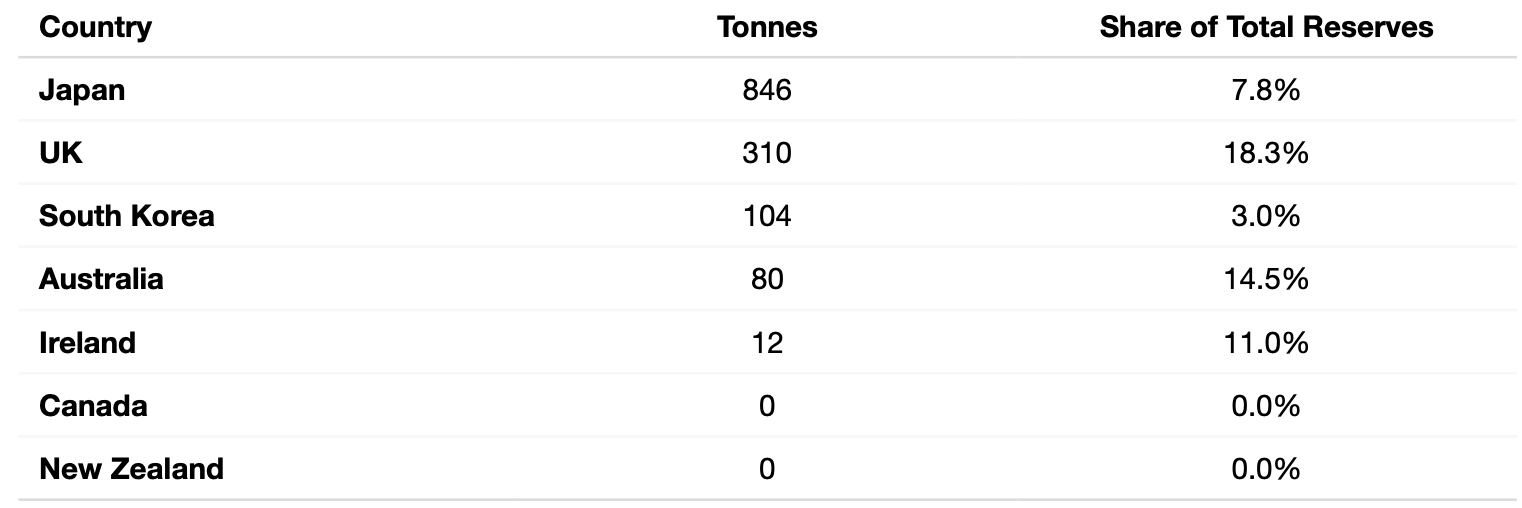

The legacy holders such as the US, Germany, Italy, and France hold between 65% and 75% of their currency reserves in gold. A second group of Western economies, however, falls well below that.

Gold Reserves, Q3/2025

Source: World Gold Council, Incrementum AG

Canada is perhaps the most striking case of monetary self-neglect: a G7 nation, one of the world’s five largest gold producers – and zero tonnes in the vaults of the Bank of Canada. The last holdings were sold in 2016 at average prices of around USD 1,200/ oz. Converted to today’s terms that is monetary collateral damage of historic proportions.

The movement in the opposite direction, however, has already begun. Singapore significantly increased its gold holdings in 2023/24. The Czech Republic has increased its gold reserves ninefold since 2022, from eight to nearly 72 t by the end of 2025, with the stated goal of further increasing them to 100 t by 2028.

The paradox of producer nations

The situation becomes particularly noteworthy when considering the gold reserves of the major gold-producing countries. Canada, Australia, and the US, accounting for about one-fifth of global mine production, are among the world’s most significant gold producers. However, the mined gold generally leaves the country and flows through the global market into private vaults, ETFs, and increasingly the balance sheets of Asian central banks.

Here, one could venture a hypothesis that would have been considered exotic ten years ago but now falls on fertile geopolitical ground: Why shouldn’t Western gold producers sell their mine output primarily to their own central banks? The model would by no means be new. Kazakhstan and Uzbekistan have been practicing this for years with considerable success. The Central Bank of Uzbekistan even has a statutory right of first refusal on domestic gold production and has used this to build up its reserves to 390 t. This represents 85% of its total foreign exchange reserves.

From the perspective of Western gold-producing countries, such a “domestic-first” model would have several advantages: It would diversify currency reserves without having to participate in the global market, and it would hedge against strategic vulnerabilities, mirroring on the precious metals side what China has imposed with rare earths.

Four drivers of Western gold purchases

- QE losses as a balance sheet crisis. Numerous central banks are sitting on unrealized losses from their bond purchases during the QE era. The longer interest rates remain high, the more attractive gold becomes as a balance sheet stabilizer. The Bundesbank’s revaluation reserve reached a historic high of EUR 387bn at the end of 2025. The gold buffer has become a functional substitute for equity capital (see Vector III).

- Erosion of confidence in US Treasury bonds. The US fiscal position is unsustainable in the long run. If US Treasury bonds lose their status as a risk-free investment, they also lose their reserve currency status. The USD’s share of global foreign exchange reserves has fallen to its lowest level since 1994; the share of gold rose to its highest since 1991.

- Portfolio logic. While continental legacy holders hold 60–75% of their reserves in gold, the UK, Canada, Japan, and Australia are well below that level. The portfolio-theoretical appeal of increasing gold holdings grows in proportion to every new crisis of confidence.

- Fiscal dominance. When central banks lose their monetary independence under pressure from their governments, gold becomes the institution’s insurance against its own government.

The leverage of numbers

What happens if Western central banks with low gold allocations increase their holdings? Doubling Japan’s gold reserve ratio to just 15% would require the purchase of more than 800 t. That amounts to more than one-fifth of annual global gold production. If Canada and Australia were to reallocate just 10% of their currency reserves into gold, they would need to acquire 400 t, which could easily be covered by domestic production over several years.

For the Western “gold-light” group alone, and assuming moderate target ratios, this results in a potential cumulative demand of 2,000 to 3,000 t. This would correspond to slightly less than a full year’s mine production – as a one-time rebalancing impulse, not as an ongoing flow.

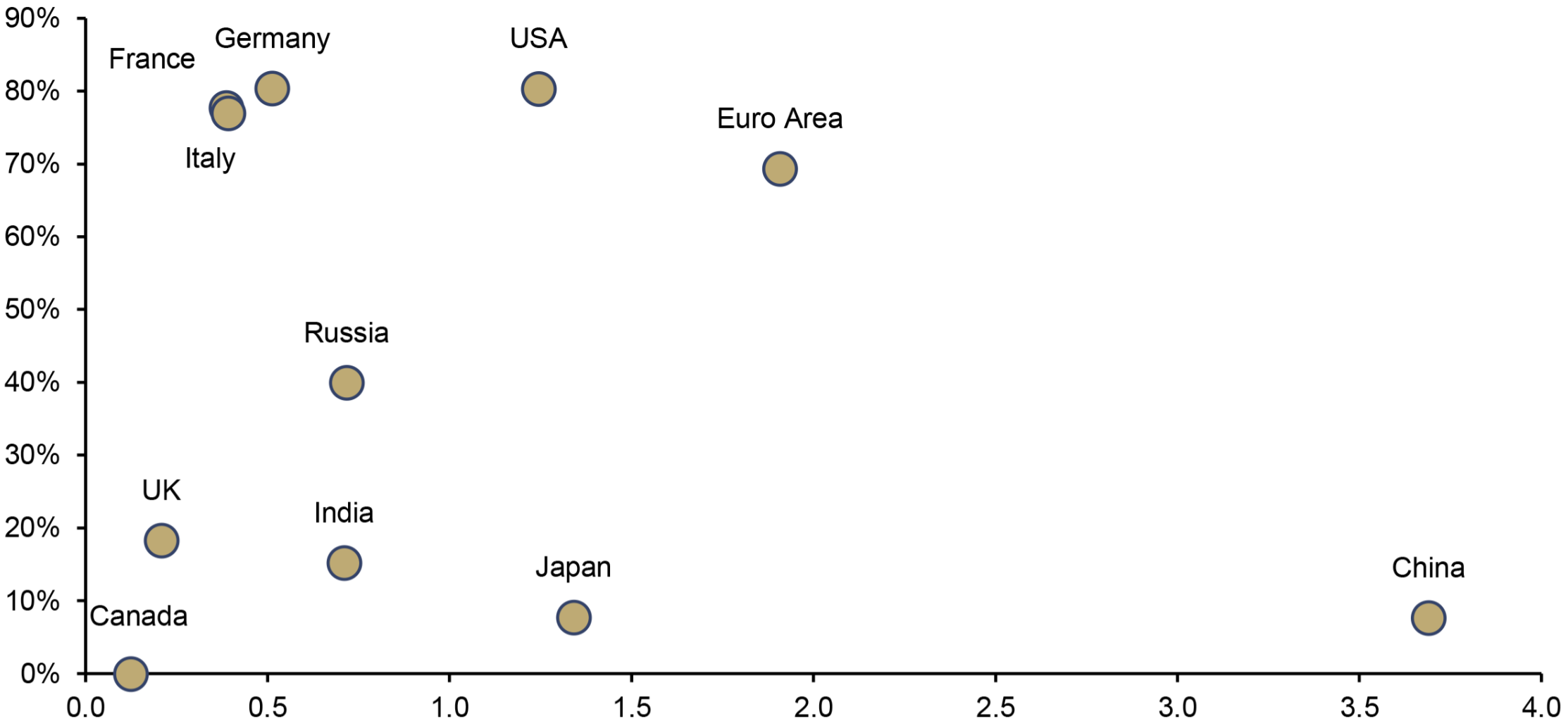

Total Reserves of Top 10 Economies + Euro Area, USD trn (x-axis), and Share of Gold Reserves (y-axis), 09/2025

Source: World Bank, World Gold Council, Incrementum AG

Vector VI: Digitalization – Gold-Backed Tokens Mobilize Gold

The final vector is technological in nature. Historically, gold has been an excellent store of value but cumbersome to transact. Tokenization promises to address precisely this weakness.[6] Fully backed, transparently auditable gold tokens – with Tether Gold (XAUT) and Pax Gold (PAXG) as market leaders and the HSBC Gold Token representing the established banking sector – have put the concept into practice: Physical scarcity meets digital settlement speed.

What began as a niche is growing explosively. The market capitalization of gold tokens has quintupled within 24 months, surpassing the USD 6bn mark in February 2026. XAUT and PAXG account for approximately 97% of the segment; more than 1.2 Moz of physical gold serve as backing for the tokens in circulation. Trading volume in 2025 reached USD 178bn, surpassing all major US gold ETFs with the exception of GLD. The HSBC Gold Token, on the market since March 2024, exceeded USD 1bn in trading volume in November 2025 and is now the third-largest gold token worldwide.

Tokenization begins to resolve an age-old dilemma: If gold becomes as easily transferable as a US dollar, its disadvantage relative to fiat currency diminishes.

Regulatory developments paint a mixed picture. In the EU, MiCA has explicitly regulated gold–backed tokens as “asset-referenced tokens” (ARTs) since June 30, 2024. This is a harmonized framework that enables institutional adoption but could crowd out smaller issuers and favor market concentration due to compliance costs such as reserve requirements and audit obligations. In the US, the division of jurisdiction between the SEC and the CFTC remains unclear. This creates a regulatory vacuum that is both a risk and an opportunity.

Tokenized gold is in direct competition with CBDCs. The fundamental difference is political in nature. CBDCs are programmable, monitorable, and can be assigned negative interest rates or expiration dates. Gold tokens offer currency neutrality, no central authority, and no issuer access to transaction data. For users who value monetary sovereignty, this is a decisive advantage. The further the CBDC agenda advances, the more attractive the gold–backed alternative becomes.

Digitalization does not replace gold, but it does change how gold is used. The real test is not whether gold can be tokenized, but how: whether ownership rights, backing, verifiability, and insolvency resilience can be structured robustly enough so that, in a crisis, digital forms of gold are more than just elegant user interfaces built on top of an old counterparty risk.

What Connects the Six Vectors: Feedback Loops

As different as these six vectors may seem, they share a common underlying structure. In every case, gold regains monetary significance precisely where the existing system relies on trust, the quality of collateral, or political neutrality. Gold is not becoming more relevant because it has been modernized. It is becoming more relevant because the weaknesses of the alternatives are becoming apparent.

Feedback instead of addition

The key point is that the vectors do not act in isolation but reinforce one another. The cycle reads like a self-reinforcing engine:

- Accumulation (Vector V) and private demand (Vector II) drive the gold price.

- A rising gold price improves central banks’ balance sheets (Vector III).

- Improved balance sheets reduce political resistance to gold-backed bonds (Vector IV).

- Gold-backed bonds legitimize gold as a reserve asset (Vector I).

- A higher, legitimized gold price makes tokenized gold products more attractive (Vector VI).

- Tokenization, in turn, increases demand – and closes the loop.

This positive feedback loop is the actual catalyst. Once a critical mass is reached, the process accelerates on its own. Remonetization is thus not a binary event but a gradual phase transition. It can begin with reserves, gain traction through private portfolios, become politically relevant through balance sheet logic, and open up new areas of application through technological innovations. Those waiting for one big bang will overlook the crucial point: Systemic turning points are not heralded by decrees but by changing practices.

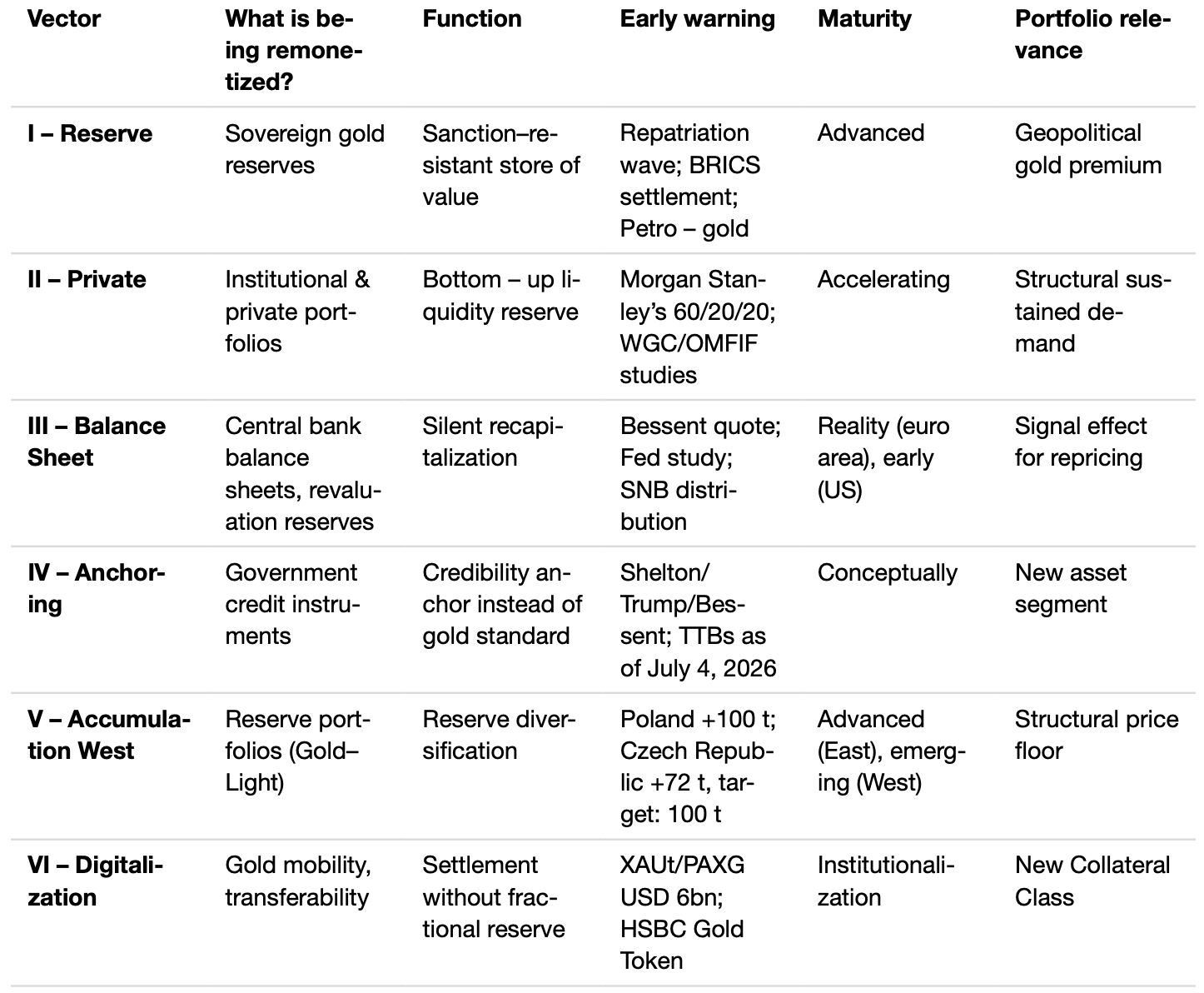

An Overview of the Vectors

Source: In Gold We Trust

Arguments against the concept – and why we remain convinced

However, there are also factors that argue against the remonetization of gold. The following structural objections deserve serious consideration:

- The cash flow argument: Gold generates no current income. As long as government bonds are considered risk-free, the institutional incentive remains limited. Counterargument: It is precisely this status that is eroding – see Vector III.

- The systemic risk argument: An erratic rise in the price of gold would destabilize the debt-based monetary system. Political resistance to this stems not from a conspiracy but from rational politics of interest. Counterargument: An orderly process like the Eurosystem model is in any case more attractive to policymakers than market chaos – the question is not whether a transition occurs, but whether it occurs in an orderly or chaotic manner.

- The substitution argument: Gold could lose its collateral function to other assets, such as Bitcoin or tokenized commodities. Counterargument: Complementarity is more likely than substitution (see the Bitcoin discussion in Vector III).

What would have to happen for the remonetization thesis to fail? Three scenarios are conceivable:

- Significant debt reduction through real economic growth or fiscal consolidation

- Substantial geopolitical détente with the lifting of all sanctions and a return to multilateral cooperation

- A technological breakthrough in CBDCs that renders gold obsolete as an anchor of trust

Each of these scenarios is possible on its own. However, it is extremely unlikely that they would occur in combination. Remonetization would fail only if several secular trends were to reverse simultaneously.

The burden of proof has shifted

The real flaw in the current debate lies in what is considered normal. Over half a century of fiat regimes has clouded historical memory: The unbacked paper money system is now regarded as the norm, while gold is seen as a relic. Historically speaking, it is exactly the opposite. The past 54 years are the anomaly, and 5,000 years of monetary history are the proper frame of reference.

The burden of proof therefore does not lie with those who consider a gradual remonetization plausible. It lies with those who claim that a historically unique fiat regime will be able to function permanently without resorting to monetary anchors.

Back to the Monetary Future– this is not a nostalgic throwback. It is the sober realization that the history of money is longer and more cyclical than a single political cycle. Gold is not returning because it romanticizes the present. It is returning because the present can no longer keep its promises.

[1] See “Bringing it Home: Central Bank Gold Repatriation,” In Gold We Trust report 2025

[2] See the chapter “The Psychology Behind Gold’s Underallocation” in this In Gold We Trust report

[3] See “20 Years later – a Freegold Project: Interview with FOFOA,” In Gold We Trust report 2019

[4] See “The New Playbook for Bitcoin,” In Gold We Trust report 2024

[5] See the chapter “Back to the Founders: Dr. Shelton on the Constitution, Gold, and the Future of the US Dollar” in this In Gold We Trust report

[6] See the chapters “A Golden “Stabilization” Op in Plain Sight” and “Gold Goes Digital: Tokenization, Financial Infrastructure & Trust” in this In Gold We Trust report