The Corporate Gold Standard: Why Gold and Silver Miners Should Hold Their Own Metal

“Any business that is a price taker does not deserve a good multiple.”

Chris Ritchie

- Closing the Big Short. Mining companies are the only industry on earth that systematically converts the very asset their investors bought them for into the currency that asset is meant to hedge against. Since 1971, the US dollar has lost ~98% against gold.

- The Corporate Gold Standard: practice what you preach. We propose miners retain 5–10% of output as bullion on the balance sheet – the same allocation the industry has long recommended to its own investors. What is prudent for a portfolio is prudent for a treasury.

- Gold is the natural hedge against a miner’s cost inflation. With an R² of 0.97 between the gold price and AISC, gold-denominated mining costs have barely moved for decades. Compounding today’s USD 1,605 AISC at its historical 8% CAGR over a 15-year project cycle yields ~USD 5,090 – already above today’s gold price.

- From price taker to price maker. Every ounce retained delivers pure metal-price leverage, free of operational risk – the same exposure that earns royalty companies 25–30x EV/EBITDA versus 7–10x for producers. In a market priced at the margin, even moderate supply discipline would have disproportionate price effects.

For twenty years, the In Gold We Trust report has argued that every investor should hold at least 5%–10% of their portfolio in gold, as a hedge against monetary debasement, a discipline against fiat excess, and an anchor in Austrian capital theory. The Corporate Gold Standard applies that same logic to the balance sheets of the companies that produce the metal in the first place. If gold earns its place in every rational portfolio precisely because fiat cannot be trusted, then gold miners run the world’s most peculiar business model: they dig up the antidote – and promptly exchange it for the poison.

The Irony of Gold Producers

It is one of the most remarkable contradictions in the financial world: The companies that extract gold from the earth – the very asset that has served as humanity’s ultimate store of value for millennia – generally tend to sell it promptly, only to hold the very currency whose debasement they tell their investors to avoid. In a manner of speaking, though previously “long gold”, they have now gone “long currency”.

Now, with metals prices near recent highs, producers are rapidly accumulating more of that currency. That is a champagne problem, but one for which a solution is required. The industry markets gold as an inflation hedge while industry standard dictates that feasibility studies are run with an implicit inflation rate of zero percent. As our friend Chris Ritchie, former president of SilverCrest Metals and architect of its bold treasury strategy, puts it: Good governance would suggest that miners evaluate the total costs and risks over the entire capital allocation life cycle.

This cognitive dissonance is not a peripheral issue. It lies at the heart of the mining sector’s chronic undervaluation and its inability to attract capital beyond a narrow niche of precious metals enthusiasts. With a CAGR of 9% since 1971, gold is one of the best-performing assets in history – yet the mining industry remains uninvestable for most of the market. The industry has chronically underperformed, and malinvestment of retained profits is among the most frequently cited causes. It is a particular irony that a mining company should overcome the considerable technical, regulatory, and financial hurdles required to generate a return on capital, only to reinvest and destroy it. The way out may start with simply embracing the core functionality of the product itself.

Our proposal is, in essence, a Corporate Gold Standard – a framework in which gold producers cease to operate as mere throughput machines, converting the asset of highest monetary integrity into the asset of lowest as rapidly as the conveyor belt allows. Most gold producers function like refineries in reverse: They extract the one substance that has best preserved purchasing power for 5,000 years, then immediately exchange it for a currency that has lost 98% of its value against gold since 1971 – and rush to do so precisely when their product is appreciating. In effect, they run a permanent short position against the very asset their investors bought shares to gain exposure to.

The Corporate Gold Standard proposes a simple corrective: Gold producers ought to retain a meaningful portion of output, at least 5–10%, as a hard-currency war chest on the balance sheet. Portfolio theory has long advocated that investors hold 5–10% of their personal balance sheets in gold. Why should corporates – who are legal “persons” of another construct – differ in practice? Taking their own advice would build industry credibility and credit alike. Robust balance sheets attract capital; maintaining them mitigates malinvestment and capital destruction.

The Replacement Cost Trap

From our point of view, the industry’s standard metric, all-in sustaining costs (AISC), systematically obscures the true cost of gold production. AISC captures the ongoing operating costs and sustaining capital of an existing (read: successful) mine. It does not capture that mine’s sunk costs of exploration, the capital expenditure of mine construction, the costs allocated to projects that never make it to production, the G&A during the time leading up to production, and the time value of deployed capital. It also critically fails to recognize, much less measure, the improbability of repeated future success(es).

The numbers are sobering: Out of 750 exploration projects, on average only one reaches production (Colorado School of Mines). Successful mines are statistical outliers, not the norm. Once all upstream costs are accounted for – exploration, development, construction, failed projects, cost of capital, and a realistic inflation rate – the true total cost per ounce of silver, by Ritchie’s calculation at SilverCrest, was approximately USD 22 at a time when silver was trading at USD 18. For the industry as a whole, the true total cost today likely exceeds USD 40 by a considerable margin. This is not a dire issue when silver is at USD 75 but, given the highly cyclical nature of the business, having the flexibility to choose when to sell one’s product is imperative, especially when total cost may be higher than its value at many times throughout the cycle, let alone a much greater future replacement cost. A successful mine is a dying mine from day one.

The Compounding Effect of Rising Costs

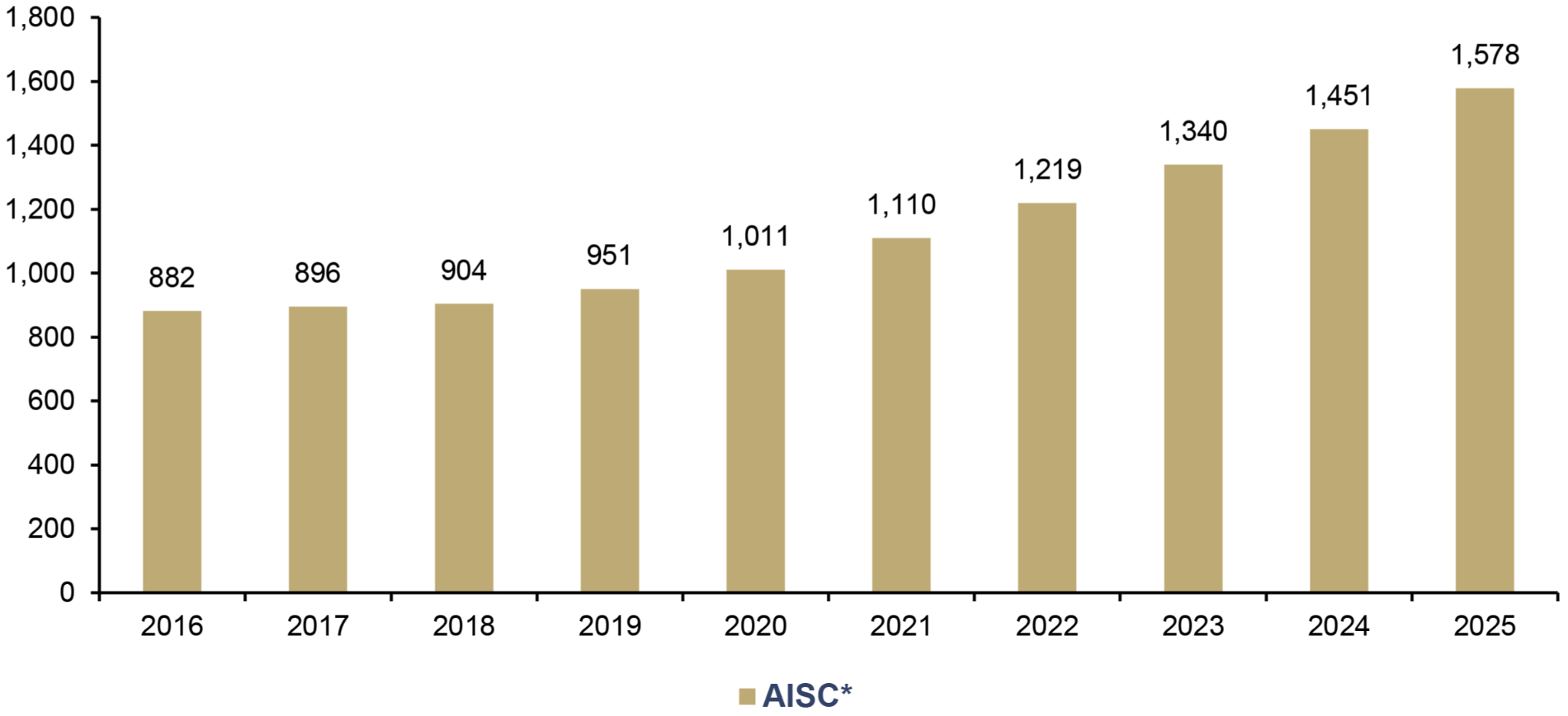

Particularly revealing is the empirical analysis of AISC trends: Over the period from 1990 to 2022, based on data from 400 producers, AISC grew at a compound annual growth rate (CAGR) of approximately 8%. That trajectory has continued through the current cycle: Industry-average AISC rose 9% y/y in Q3/2025 to USD 1,605, the highest on record, driven by higher sustaining capex, input costs, and royalty payments tied to the elevated gold price.

All-in Sustaining Cost (AISC)* for Major Producers**, in USD, 2016–2025

Source: FactSet, Incrementum AG

*Output weighted, **NEM, AEM, ABX, AU, GFI, K, NST, HAR, EDV, BTO

Simultaneously, the fiat currency received upon sale loses roughly 10% of its real purchasing power per year – measured by actual cost-of-living increases, not official inflation statistics. Short-term pricing and costs will vary; but when considered over the same time horizon within which mining companies allocate, gold has moved in virtual symmetry with costs. The mining industry allocates large sums of money over very long periods of time. Knowing that the industry’s product can be functionally used to offset the risks it faces is transformative.

The implication can be illustrated with a straightforward calculation: Take today’s median AISC of USD 1,605 and compound it at 8% annually over 15 years, the typical discovery-to-production cycle. That implies a future AISC of ~USD 5,090, already above today’s gold price of ~USD 4,600. The cost of a future ounce already exceeds what today’s ounce sells for.

In other words: selling an ounce today and holding the proceeds in dollars means (i) exchanging an asset with limited supply for one with unlimited supply, (ii) exposing investors to more reinvestment and mining-related risk, and (iii) decreasing their leverage to the metal exposure they chose. When deciding how to allocate capital, it is worth considering that the cheapest ounces a producer can find may well be the ones already in their hand.

The 0.97 R²: Gold as a Functional Inflation Hedge

One of the strongest arguments for holding gold on the balance sheet is also the least appreciated: the near-perfect correlation between the gold price and the industry’s production costs. With an R² of 0.97, the gold price moves in near-lockstep with AISC over the capital allocation life cycle.

This correlation reflects three distinct mechanisms. First, the same inflationary forces – energy costs, wages, materials, regulatory burden – drive both production costs and the gold price. Second, the gold price must ultimately cover the marginal cost of the highest-cost producer still operating. Third, and often overlooked: The correlation is partly endogenous. When gold prices rise, producers extend mine life by processing lower-grade ore that would be uneconomic at lower prices, a practice known as “low-grading”. This mechanically raises reported AISC, as more tonnes must be moved per ounce recovered. Conversely, in bear markets, producers “high-grade” their deposits, selectively mining only the richest ore to compress costs. The R² of 0.97 thus captures both exogenous inflation and endogenous grade management.

The implication remains intact: Whether the correlation arises from shared inflationary drivers or price-responsive mining behavior, gold-denominated costs are far more stable than fiat-denominated costs. This insight can be expressed mathematically:

C(real) = C(fiat) / P(Au)

where C(fiat) is the total cost of production in fiat currency and P(Au) is the gold price. The fiat-denominated cost fluctuates wildly; the gold-denominated cost barely moves. The producer who retains gold holds the most stable unit of account for their own cost structure.

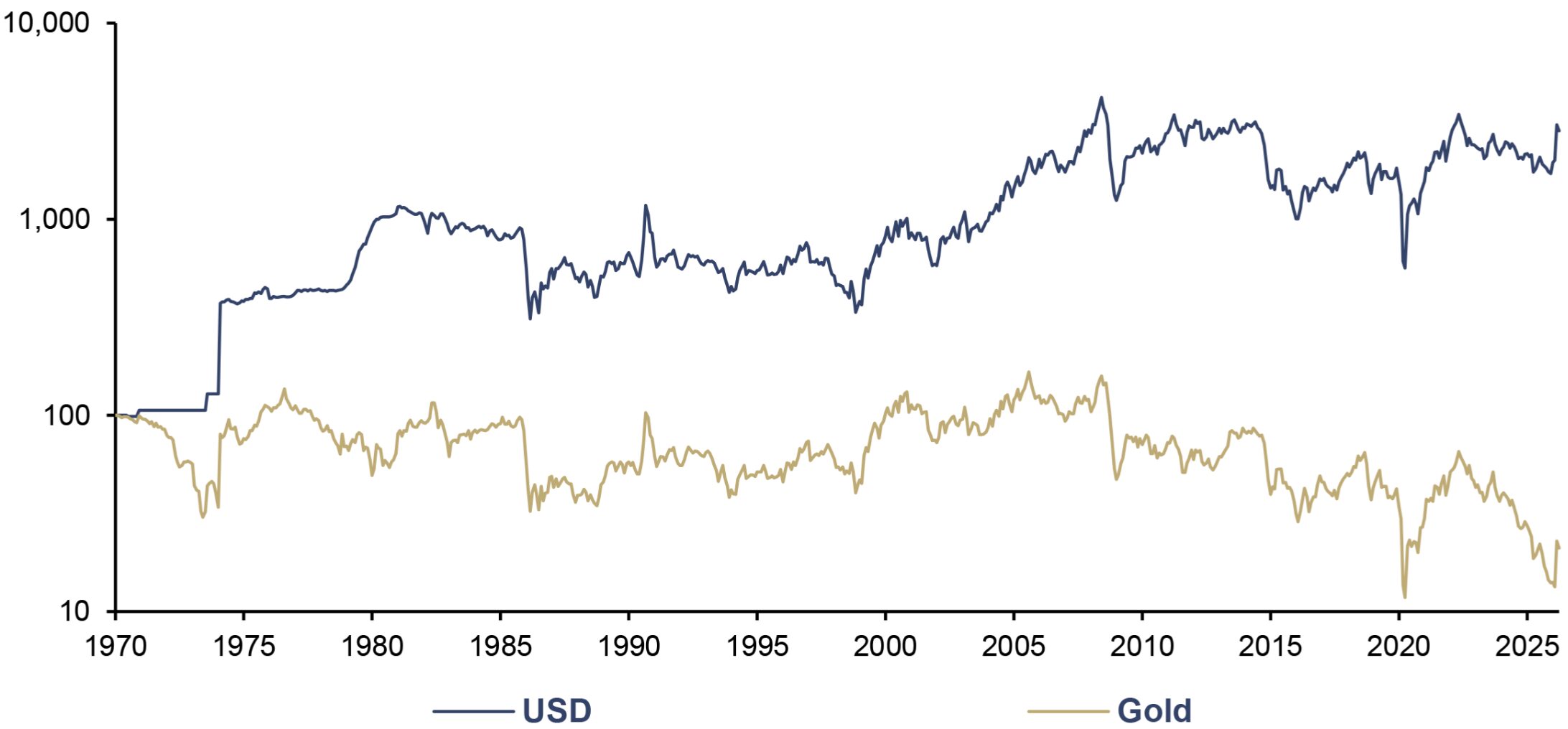

The energy dimension makes this point especially vivid. Energy typically accounts for 25–30% of cash costs in gold mining: diesel for haul trucks, electricity for crushing and grinding, gas for heating and processing. A producer that sells gold at USD 4,600 and parks the proceeds in dollars is betting that those dollars will purchase the same energy next quarter. Given that oil has lost roughly 80% of its US dollar value against gold since 1971, this has consistently been a losing bet. A producer retaining a portion of output as a hard-currency war chest insures operational continuity precisely when it matters most.

Oil (WTI) (log), in USD, and in Gold, 100 = 01/1970, 01/1970–04/2026

Source: Nick Laird, LSEG, Incrementum AG

For a mining company, gold is the natural hedge against its own cost inflation. A company investing in 15-year project cycles, whose greatest risk is cost escalation, holds the perfect hedge literally in its hands. One strategy: Hold enough gold to offset anticipated annual sustaining costs. Another: Increase holdings ahead of major capex endeavors.

The current cycle illustrates the point. With AISC at ~USD 1,600 and gold around USD 4,600, margins are at record levels – yet the industry converts virtually 100% of output into fiat. Had producers retained just 5% of production during 2013–2019 – when gold averaged USD 1,250 – those ounces would today be worth nearly 4x their original value, without a single drill hole required. These “post-production margins” carry no additional capital investment and far less risk than “next-production margins.” Selling is also a risk: Price upside opportunity is permanently forgone.

Healthier Leverage: The Royalty Logic for Producers

The valuation discount at which gold producers trade relative to royalty and streaming companies is one of the most persistent anomalies in the mining sector. While a Franco-Nevada or Wheaton Precious Metals commands EV/EBITDA multiples of 25–30x, even high-quality producers languish at 7–10x. The explanation lies not solely in the operational risks of mining but in the nature of the exposure: Royalty companies offer pure metal price leverage with significantly reduced operational risk. Every ounce a producer holds on its balance sheet offers similar “post-production” leverage. If investors prefer gold and silver to fiat, then every ounce held can support the company’s multiple. When sold, that multiple must then trend back toward that of an entity whose reserves are composed of instruments losing 10% annually in value.

To emphasize: An ounce of gold stored above ground is no longer exposed to the risks of mining – no geological risk, no operational risk, no political risk, no environmental risk. It offers pure, undiluted exposure to the metal price. It offers zero exposure to monetary debasement. Or, framed in the language of the Austrian School: The time preference shifts in favor of the future: The producer trades immediate but depreciating consumption (fiat proceeds) for the accumulation of a non-inflatable asset which can more likely support greater future consumption. Every metal ounce held offers the investor healthier leverage, and purer exposure, to the future itself.

Supply Discipline: From Price Taker to Price Maker

The supply-side implication is equally striking. What if major gold producers withheld 5–10% of annual output? And why should the logic stop there – why shouldn’t every company seeking to preserve its balance sheet’s purchasing power treat gold as a treasury currency? The empirical answer is unambiguous: backtests show that including gold among managed treasury currencies would have added meaningful value over decades.

Annual gold mine production currently stands at 3,672 t, or approximately 118moz. Withholding just 5% amounts to some 180 t – a figure that may seem modest in the context of central bank purchases, exceeding 1,000 t in each of 2022, 2023, and 2024, before easing to 863 t in 2025, but price discovery always happens at the margin.

The mechanism is mechanically trivial: Producers simply do not ship a fraction of monthly doré or refined output to the bullion bank. The metal moves from processing plant to corporate vault rather than from vault to market. No fiat round-trip is required, no tax event is triggered, and the full economic exposure remains with the producer until it chooses to realize it. For those concerned about liquidity, physical gold serves as first-class collateral against revolving credit facilities – a mechanism private investors, central banks, and even some sovereign funds already exploit. Producers need not worry about Basel III risk-weightings; unlike deposit-taking institutions, they face no regulatory constraint on holding their own product.

The Network Effects of an Industry Strategy

When a single producer pursues this path, the market impact is marginal. But if major gold mining companies were to follow, a self-reinforcing cycle would emerge: Withheld supply supports the price. A rising price improves margins. Better margins require fewer sales to cover actual costs and enable further withholding. And the combination of increasing metal price exposure and decreasing dependence on operational output leads to higher valuation multiples. Adjusting the weightings of this strategy when prices are at different stages of the cycle can allow for better capital allocation decision making and multiple options for cost-effective downside protection on metal held.

To put the numbers in perspective: Annual global silver mine production of roughly 820moz at a recent silver price around USD 75 equates to a market value of approximately USD 61.5 bn, still a rounding error in global financial markets. Put differently, a single day’s trading volume in a mega-cap such as Nvidia can exceed the entire annual output value of the silver mining industry. Precious metals markets, measured against global capital flows, remain tiny. Even moderate supply discipline at the producer level would have disproportionate price effects.

From Theory to Practice: The SilverCrest Experiment

Consider one example: The SilverCrest Metals team completed construction with excess capital, low costs, and at a unique time in the cycle. In hindsight, it’s easy to say that it was wise to hold onto metal when the selling price at the time of around USD 18 for silver and around USD 1,800 for gold was below their fully loaded total costs and well below the industry average AISC. With gold and silver at much higher levels now, the industry is at a very different part of the cycle with different capital allocation options in front of it.

The market ultimately validated this discipline: In February 2025, Coeur Mining completed its acquisition of SilverCrest in an all-stock transaction valued at approximately USD 1.7 bn. The bullion treasury was not a deal-breaker but a dealmaker – it was priced into the acquisition multiple, not discounted out of it. The corporate-gold-standard thesis earned an exit premium, not a conglomerate discount.

To forestall the inevitable objection: Michael Saylor’s (Micro)Strategy has pursued a parallel thesis with Bitcoin since 2020, turning a software company into a digital-asset treasury vehicle. The difference is one of capital structure, not of strategy. Gold producers have the advantage Saylor never had: They produce the asset they would accumulate. The treasury strategy need not be funded by convertible-bond issuance; it can be funded simply by not selling a fraction of what is mined. It is the cheapest treasury strategy in the world – the capital outlay is an opportunity cost of deferred revenue recognition, not a capital raise.

It’s reasonable to expect that congestion and cost inflation can increase as more projects rush towards production. While margins are high, the balance sheets of producers have never been healthier. Holding onto gold and silver now might seem to be a higher-risk capital allocation decision, but selling all of your gold and silver to hold dollars also poses a significant and rarely discussed risk.

If holding 10% is seen as risky, then the risk of holding 90% of the balance sheet in an instrument that producers tell their investors to avoid like the plague deserves equal scrutiny. Increased dividends and buybacks are welcome and investor-friendly decisions. Allocating capital to holding bullion (or simply withholding bullion from current sale) should also be included in the conversation and would also likely be welcomed by a large group of investors. Companies can give investors more of the exposure that they want, lead the industry in supply discipline, and retain balance sheet flexibility.

Retail Enthusiasm, Institutional Skepticism

The shareholder reception to the bullion strategy at SilverCrest was notably bifurcated. Retail investors – many of whom buy mining shares precisely because they believe in gold as money – responded enthusiastically. SilverCrest’s approach aligned with their core conviction: Here, finally, was a company that practiced what the sector preached. The bullion strategy became a branding asset in itself, generating loyalty and advocacy that transcended conventional equity analysis.

As companies battle for superior cost of capital, adjusting the narrative to more effectively communicate with the enormous amount of capital that cares about inflation (but doesn’t know much or care about mining) will be core to a successful marketing strategy. The current marketing system is not set up to access this audience, though doing so offers a true opportunity to differentiate.

This divergence is revealing. It suggests that the bullion thesis resonates most powerfully with the very investors the mining sector most needs to attract and retain: long-term, conviction-driven holders who understand gold’s monetary properties. As Marty Neumeier writes in The Brand Flip: “Customers no longer buy brands. They join brands.” The retail investors who rallied behind SilverCrest were not passive shareholders; they were members of a tribe that shared a common monetary worldview, and their support built upon itself. Tesla is the textbook case. Owners who bought the car for its environmental credentials became members of a tribe; that tribe then extended its conviction from the car to the stock, turning shareholders into the brand’s most effective marketing arm.

The Austrian Perspective: Time Preference and Capital Theory

From the perspective of Austrian capital theory, the behavior of the mining industry can be characterized as pathological time preference. Producers act as though an ounce of gold will be worth less tomorrow than today – even though the opposite is true when measured in fiat purchasing power. They discount the future at a rate that would only be rational if the fiat money received in exchange were to preserve its value.

The rational capital allocation for a gold producer in an inflationary environment – and the current environment of fiscal dominance, shrinking tax bases, and structurally elevated inflation is precisely such an environment – consists in retaining a portion of production in the hardest available currency: its own product.

The Next Decade: Massive Cost Escalation

Data and experience would suggest that a decade of massive cost increases in mining is a risk that needs to be managed. This assessment aligns with several structural trends:

- Declining ore grades: Average gold grades at producing mines have been falling for decades. Lower grades mean more tonnes of rock, more energy, more water, and more chemicals per ounce – and consequently, higher costs per ounce.

- Increasing depth and complexity of development: The easy-to-reach deposits have been exhausted. New projects require deeper shafts, more remote locations, and more complex processing methods.

- Regulatory thickening: Permitting timelines for new mines have doubled or tripled in many jurisdictions. Longer permitting processes mean higher capital risk and higher financing costs.

- Energy cost volatility: Mining is energy-intensive. In an environment of geopolitical fragmentation and energy transition, stable and affordable energy supply chains and prices can no longer be taken for granted.

- Labor market tightness: The mining sector increasingly competes with other industries for skilled workers, particularly in remote regions.

- Resource nationalism and geopolitical fragmentation: Royalty hikes, windfall taxes, and outright shutdowns have become base case in many countries.

- Social license and ESG cost loading: Community consent and new disclosure rules have moved from reputational concerns to line items on the cost sheet.

- Tailings and legacy liability: Tougher tailings standards continue to drive up AISC. As of November 2025, only 67% of 836 ICMM member facilities were in full conformance with the Global Industry Standard, leaving one-third still investing toward compliance.

All these factors point in the same direction: the cost or risk of replacing an ounce sold today is rising faster than the general price level. This replacement cost logic tightens with every passing year.

The CFO’s Dilemma: Practical Obstacles

Intellectual elegance notwithstanding, the bullion retention thesis faces real-world obstacles that explain why adoption has remained limited. Any CFO considering this path will confront several challenges that deserve honest acknowledgment.

- Accounting ambiguity: Under IFRS, gold fits no standard classification – not financial instrument (IFRS 9), not investment property (IAS 40), and inventory treatment (IAS 2) requires intent to sell. Producers retaining gold enter an accounting grey zone requiring bespoke policies. The World Gold Council has long advocated for a common framework, but progress remains slow.

- Metric distortion: Sell-side analysts evaluate producers on standardized metrics – AISC, free cash flow yield, production growth. Gold on the balance sheet disrupts these models. A producer withholding 5 or 10% of output shows lower revenue, lower reported FCF, and potentially higher AISC per sold ounce – mechanically translating into lower target prices. Early adopters may pay a “complexity discount” until analytical frameworks evolve to treat bullion retention as value-accretive.

- Earnings volatility: Mark-to-market holdings introduce unrealized gains and losses unrelated to operations. For CFOs answering to quarterly-focused analysts, this can trigger covenant breaches and credit downgrades. Put options on treasury holdings offer one solution – insuring downside while preserving upside.

- Asymmetric perception risk: Treasury strategies carry asymmetric reputational exposure – when they work, investors shrug; when they fail, management faces intense scrutiny. This asymmetry biases risk-averse boards toward the status quo.

- Cash flow timing: Mining operations have relentless cash needs – payroll, energy, consumables, royalties, taxes. Retaining metal requires sufficient cash reserves or the discipline to time retention to periods of excess cash generation. For junior producers without SilverCrest’s enviable position – debt-free, high-margin – the liquidity calculus is less forgiving. A position must be established over time.

- The “buy it yourself” objection: If shareholders wanted pure gold exposure, they simply could buy it themselves. This objection has surface logic but misses the point. Shareholders cannot replicate the producer’s unique advantage of acquiring gold at production cost rather than market price, nor the supply-side impact of coordinated withholding.

These are real obstacles, not theoretical ones. But they are obstacles to execution, not to the fundamental principle. Every one of them admits a solution: bespoke accounting policies, investor education, phased implementation, cycle-aware retention strategies. The question is whether management teams – and boards – have the conviction to accept short-term friction in pursuit of a structurally superior capital management proposition.

However, this again presents an opportunity for differentiation, branding and community building. If industry players become advocates to fix this system to allow for better risk mitigation, then they can tap into the believers in gold who in turn become passionate brand advocates and champions of the strategy. As William Pollard states, “Those who initiate the change will have the better opportunity to manage the change that is inevitable.”

The Brand Flip: From Price Taker to Tribe Builder

The challenges outlined above are real but they miss a deeper strategic dimension. As Marty Neumeier argues in The Brand Flip: “A brand is not owned by the company, but by the customers who draw meaning from it.“ The mining industry has historically struggled to create a strong brand. It has commodities. It has ticker symbols. But it has failed to create meaning for its investors – the very investors who believe, more fervently than almost any other investor class, in the product they are financing. To be fair, this has much to do with the near irrelevance to which gold has been relegated since the 1970s in a “dollarized” economy. Now that this trend is clearly reversing, it requires consideration from corporate leaders who wish to be industry leaders.

Peter Drucker wrote that a business has only one valid purpose: to create a customer. And only two basic functions: innovation and marketing. The gold mining sector invests heavily in generating tangible value, but has allocated far fewer resources to improving intangible value – and thereby its cost of capital. The industry is investor-relations heavy but has made limited inroads in forming a narrative attractive to the 98% of the investing world that does not typically invest in mining. The bullion retention thesis is, at its core, a marketing innovation. It tells the investor: We believe in our product as much as you do. We are not just extractors; we are custodians of sound money.

Neumeier identifies a crucial shift: “Today’s customers want more than products, more than features, more than benefits, even more than experiences. They want meaning.” The gold investor tribe is driven by meaning – monetary sovereignty, protection against institutional failure, preservation of purchasing power across generations. Yet the companies that serve this tribe operate as though they were selling wheat or copper: undifferentiated, generic, competing solely on cost metrics.

The loyalty economics are compelling. Neumeier cites research showing that loyal customers spend 33% more than new customers, that a 5% increase in retention can mean a 30% increase in profits, and that emotionally connected customers are four times as likely to do business with a company. In the mining context, this translates directly to cost of capital: A producer with a loyal, conviction-driven shareholder base can issue equity at tighter discounts, weather volatility with less panic selling, and maintain higher trading multiples through cycles. As Peter Drucker noted: “The aim of marketing is to make selling superfluous.” For miners, the aim of holding bullion is to make the perpetual discount to NAV superfluous.

If the industry wants to put customers first, it must give them more of what they want – exposure to gold and silver – and less of what they do not want: pure mining risk returned in the form of depreciating fiat. Very few people invest in gold mining because they love the process of mining. They want the product, or as near as they can get to it. The company that internalizes this insight, and acts on it, does not merely improve its capital allocation. It flips its brand.

Conclusion: Dear Mining Industry, Take Your Own Product Seriously

The irony is exquisite: the innovation the gold mining sector most urgently needs is not better extraction technology or more efficient processing – it is to believe in its own product.

The arguments for retaining a portion of production on the balance sheet are multi-layered and mutually reinforcing: Across most cycles, true total costs can exceed the selling price for extended periods. Replacement costs are rising faster than inflation. Gold is the natural hedge against a miner’s own cost inflation. Ounces held above ground offer pure metal price leverage without operational risk. Supply discipline supports the price and thereby the margins of the entire industry. Holding fiat on your balance sheet is a short position on gold, a drag on valuation, and – so long as you believe central banks will continue printing – a material capital allocation risk in and of itself.

Naturally, there are practical objections: cash flow requirements, tax implications, accounting provisions, and analyst expectations for consistent sales volumes. But these objections concern the “how”, not the “whether” or the “why”. No reasonable observer would argue that a producer should withhold its entire production – yet the same logic should apply in reverse to holding 100% of treasury in fiat. 5–10% is not a radical proposition. It is the same allocation prudent investors have been advised to hold for decades, applied to the balance sheets of the companies that produce the asset in the first place.

The question is not whether gold producers should hold their metal. The question is why, for so long, they have not done so. The industry’s own product has functional utility across all aspects of its business, from improving the overall cost of capital to hedging fiat-currency treasury risks, to more effective marketing. The industry tells its investors to hold 5–10% of their net worth in gold and silver. If it truly means it, it should start by doing so itself.

Or, to borrow SilverCrest’s own motto: The product is the solution.