Introduction: Back to the Monetary Future

“The future looks like a past that feels very far gone…”

Bridgewater Associates

- The In Gold We Trust report celebrates its 20th edition this year. When the first report was published in 2007 – at that time still under the auspices of Erste Group – gold traded at around USD 670. Since then, the price of gold has increased almost sevenfold – and our core theses have been confirmed.

- The theme “Back to the Monetary Future” encapsulates the essence of twenty years of gold market analysis: The future of money lies in its past. The monetary and fiscal policy decisions of 1971, 2008, and 2020 continue to shape today’s market dynamics.

- The Pax Americana – the political, military, economic, and above all monetary order that has shaped the global system since 1945 – is drawing to a close.

- The bull market of recent years was driven by gold-friendly emerging markets and by dwindling confidence in the international order. Renewed waves of inflation in the West could unleash further substantial demand for gold.

- Bull market (not yet) a bubble: The “Golden Decade” proclaimed in the In Gold We Trust report 2020 is in full swing. Since then, the price of gold has risen by 165% in US dollars. According to Dow Theory, we are in the midst of the public participation phase – the most dynamic phase of the secular bull market.

When we published the first edition of the In Gold We Trust report in May 2007 – it was just 22 pages long – the world was a different place: George W. Bush was in the White House; Italy was the reigning soccer world champion; Netflix mailed DVDs; and the iPhone, which Steve Jobs had just unveiled, was not yet on the market. An ounce of gold traded at around USD 670, and the US national debt stood just under 9trn USD, or about 60% of GDP.

Outside of a few hedge fund offices in Connecticut, virtually no one had heard the term subprime, and the Federal Reserve under Ben Bernanke was regarded as the infallible guardian of price stability. The idea that central banks would one day create trillions out of thin air, push interest rates below zero, and buy government bonds would have been dismissed as monetary science fiction. And the idea that an anonymous author would create a digital counterpart to gold with a nine-page white paper was simply beyond anyone’s imagination.

And when we referred to the Austrian School of Economics in our early In Gold We Trust reports, we were often met with polite incomprehension, as if we were describing an obscure Alpine sect. Two decades and several credit cycles later, terms like the Cantillon effect, malinvestments, and time preference have long since entered the mainstream. Much of the credit for this surely goes to Satoshi Nakamoto: Thanks to Bitcoin, more 20-year-olds today understand the nature of fiat money better than many central bankers would like.

Twenty issues, more than 5,000 pages, and a rise in the price of gold of almost 600% later, we find ourselves in a reality that Doc Brown, the scatterbrained yet likable scientist from the famous film trilogy Back to the Future, would describe as an “alternative timeline.” The Pax Americana – that political, military, and above all monetary order that has shaped the global system since 1945 – is drawing to a close. The collapse of institutional trust – in governments, central banks, and the fiat money system itself – has become the central driving force behind the price of gold.

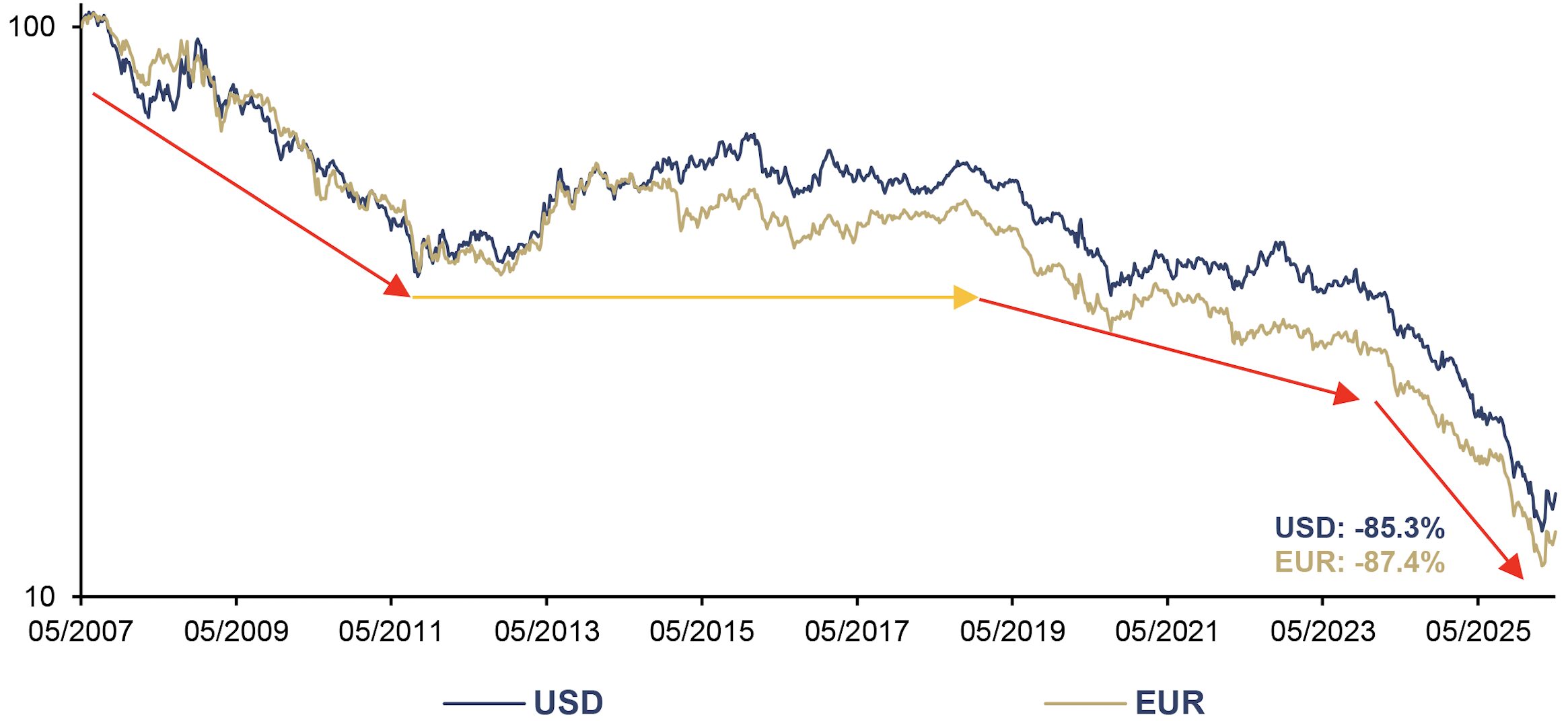

USD and EUR (log), in Gold, 100 = 05/2007, 05/2007–05/2026

Source: LSEG, Incrementum AG

The theme of our 20th-anniversary issue, “Back to the Monetary Future,” is more than a cinematic nod to a cult film from our childhood: It is a thesis. Just as Marty McFly in Back to the Future had to realize that one must understand the past to fix the present, so monetary history teaches us that the future of money lies in its past.

Back to the Future of Trust: Trust as a Monetary Foundation

At the heart of the process we have been documenting since 2007 lies the central importance of trust. It is the intangible glue that holds societies together, enables cooperation, and makes the future seem predictable. Tony Deden, one of the most astute thinkers of our time, calls it the “invisible lever” – a form of capital more valuable than any balance sheet item. Without trust, there are no relationships, no credit, no economy, no money.

It was therefore no coincidence that we explicitly included the word trust in the title of the In Gold We Trust report 2019, “Gold in the Age of Eroding Trust.” It merely echoed what has been emblazoned in the headline since the very first report in 2007: In Gold We Trust. The erosion of trust has not slowed since then, but rather has accelerated. Trust can be built up over decades – only to be squandered in seconds. This asymmetry is the real risk. Trust erodes insidiously, in homeopathic doses, until a tipping point is reached and it is suddenly lost. “Gradually, then suddenly” – Hemingway could hardly have described the dynamic more aptly.

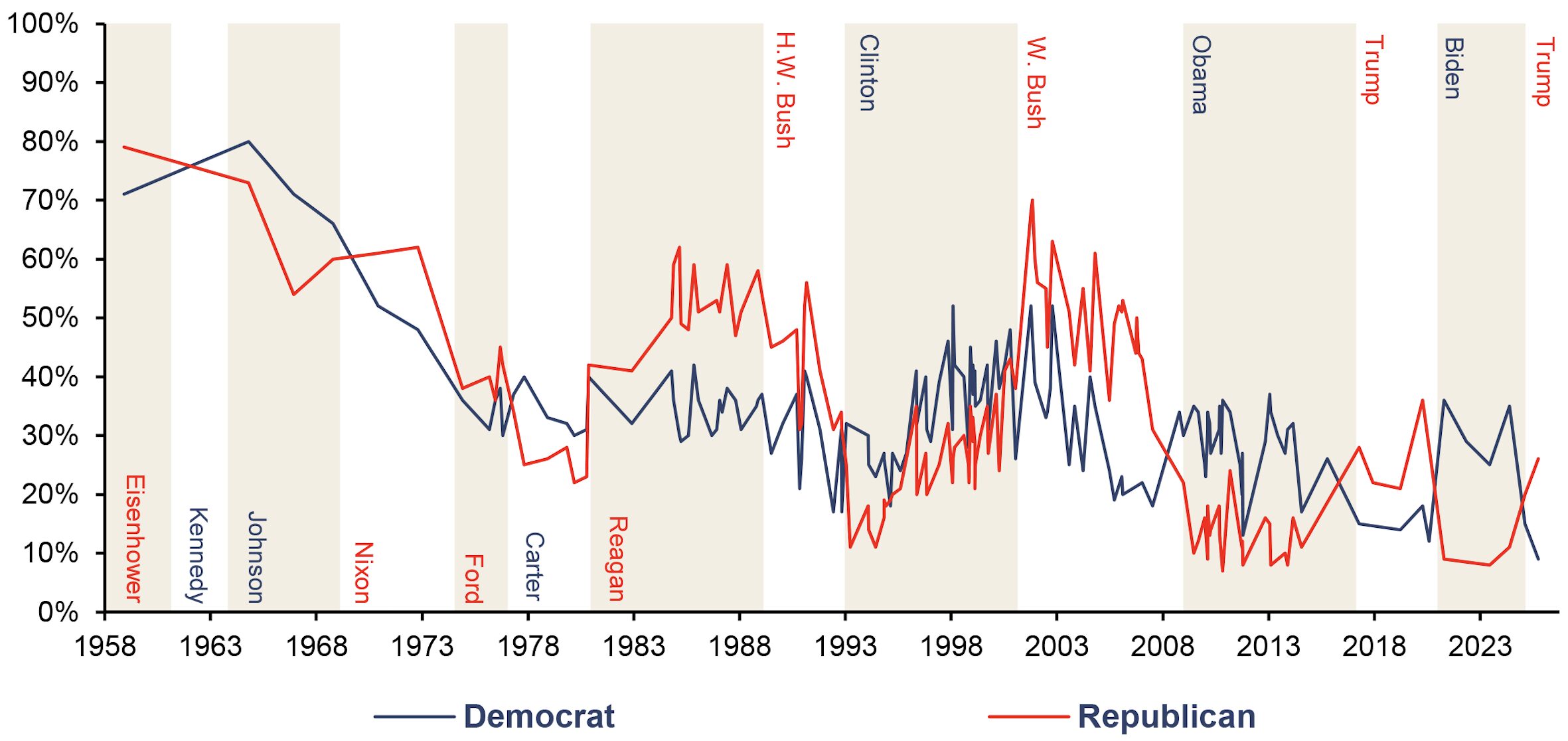

The political polarization in the US illustrates just how much social consensus is eroding. Donald Trump’s election victory was followed, just one year later, by an equally decisive mayoral victory in New York by Zohran Mamdani, a candidate from the left wing of the Democratic Party. Affordability was the defining issue in both cases, yet the political solutions proposed by the respective winners could hardly be more different. The struggle over distribution is no longer an abstract theory; it is a central issue in current politics. Historical parallels to the Gilded Age of the late 19th century are striking: Such peaks in inequality have usually preceded major political upheavals or deep market corrections.

Trust in Government, 01/1958–12/2025

Source: Pew Research Center, National Election Studies, Gallup, ABC/Washington Post, CBS/New York Times, CNN, Incrementum AG

Yet trust is not only the currency of politics but also the foundation of every monetary system. The current loss of trust is more than a social observation. As Ludwig von Mises recognized, trust is the invisible infrastructure of every monetary system. If citizens no longer consider the state’s promises – including the stability of money’s value – to be credible, the velocity of money increases: People hold paper money for shorter periods, flee to tangible assets, and demand higher risk premiums. Trust, in our view, is currently being repriced – and the market is rendering its verdict in ounces.

The Geopolitical Showdown and Gold’s Margin Call

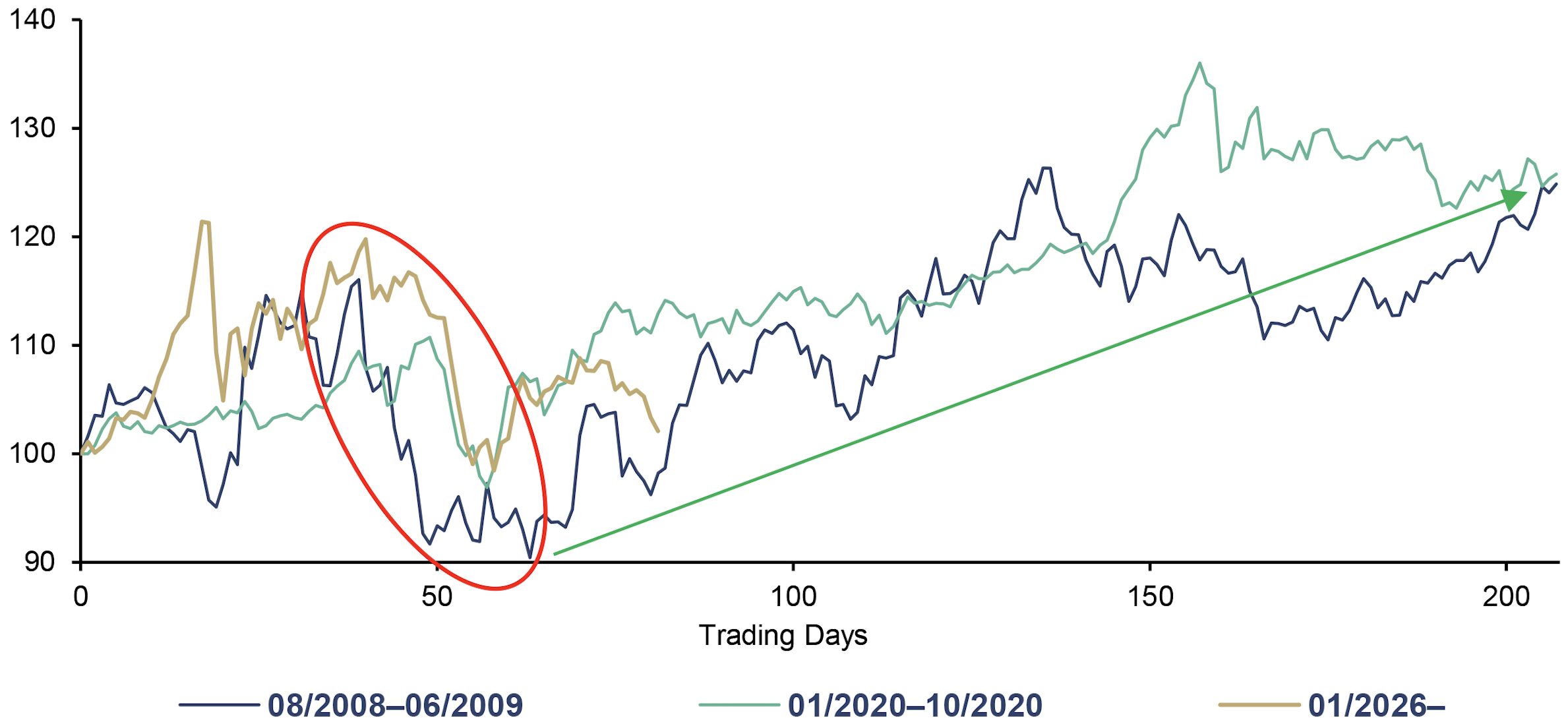

Following gold’s spectacular rally of the preceding quarters, a consolidation phase was not only likely but, from a technical perspective, overdue. The impetus came from the very event that, by the textbook, should have had the opposite effect: the Iran crisis. While a large portion of market participants speculated on another price jump, the market swung in the opposite direction – the war did not become a catalyst but rather the trigger for a healthy correction. No upward trend is linear; even structural bull markets require phases of correction, position adjustment, and sentiment unwinding. Since the release of last year’s In Gold We Trust report “The Big Long”, gold has traded nearly 40% higher despite this correction.

In March 2026, the gold price fell by USD 611 in a single month – the largest absolute monthly decline ever. By the end of the correction, gold had fallen 27% from its January all-time high. As expected, the mainstream declared the safe-haven a failure. But those who understand the mechanism recognize a familiar pattern: During periods of acute financial stress, gold is sold not in spite of, but because of its high liquidity. We saw exactly the same pattern in October 2008, with a 29% drop, when the Lehman bankruptcy triggered margin calls across all asset classes, and in March 2020, when a wave of liquidation swept through the market in the early stages of the Covid-19 pandemic and gold fell by 12%.

Gold, in USD, 100 = 08/2008, 01/2020, and 01/2026, 08/2008–04/2026

Source: LSEG, Incrementum AG

The simultaneity of two mechanisms makes the recent slump unique: First, the closure of the Strait of Hormuz cut off cash flows to oil producers in the Gulf region, who for years had been recycling their US dollar surpluses into gold. Second, the escalation forced a wave of deleveraging because rising yields, increasing interest rate expectations, and a stronger US dollar triggered margin calls.

But this is precisely the crux of the matter: The central banks’ response to this very sequence of stress events is the real catalyst for gold. The two drawdowns in 2008 and 2020 did not mark the end of the gold rally, but rather the starting point of the next upswing. A good omen for 2026?

The Lehman shock was followed by QE1 through QE3 and a tripling of the gold price. The Covid-19 crash was followed by unprecedented fiscal and monetary expansion and a rise in the gold price of over 70%. The transmission sequence – energy shock → inflation shock → government bond stress → credit revaluation → forced liquidation → central bank intervention – is a self-reinforcing cycle. And gold benefits at every stage: as a hedge against inflation, as a safe haven, and ultimately as a neutral store of value outside the spiral of devaluation.

The liquidity-driven pullbacks in gold do not refute the thesis; they are buying opportunities generated by the thesis itself. March 2026 was a monetary stress test. Gold passed it with flying colors.

Source: MiningVisuals, Incrementum AG

The Iliad of Our Time: A World Order in Turmoil

“RIP. Pax Americana, 1945–2025.” – so reads Alexander Chartres’s succinct epitaph. What the coming world order will look like remains to be seen. What is clearly discernible for now is the nature of the transitional phase: We find ourselves in an interregnum in which the old order is losing its cohesion, while the new one has not yet been defined. This interim phase is marked by heightened volatility, a multipolar distribution of power, and unabashed imperialism. After decades of increasing division of labor and steady capital optimization, hard power is becoming the decisive currency: energy, metals, semiconductors, and military hardware.

Halford Mackinder already articulated in his Heartland theory that space, resources, and centers of power shape the world order: Whoever controls the Eurasian landmass shapes the global order.[1] The war between Russia and Ukraine, which has been ongoing since 2022, has abruptly brought this old geopolitical logic back into the present. At the same time, it is becoming clear that conflicts are no longer confined to specific regions but are affecting energy prices, supply chains, capital flows, and monetary architectures worldwide.

Now Iran, too, is coming into focus amid these tectonic shifts. Niall Ferguson provides the historical context. His central thesis: Time is not on the side of an overstretched hegemon, because the economic costs of a war rise faster than its strategic gains. Ferguson draws a parallel to the 1956 Suez Crisis: It was not the Soviet threat that forced Prime Minister Anthony Eden to back down, but economic constraints.

An escalating Iran crisis could therefore become a second Suez moment for the US – and mark that monetary Rubicon at which the petrodollar system gradually shifts toward the petroyuan or even petrogold. If Tehran accepts only the renminbi for oil exports in the future, the cornerstone of US dollar hegemony established in 1973 will be permanently undermined; regional powers would turn to an Iran-China-Russia axis, and the Strait of Hormuz would thus shift from a geopolitical chokepoint to a geoeconomic turning point. The United Arab Emirates’ surprising withdrawal from OPEC at the beginning of May has shaken another long-established institution – with unclear consequences.

What began as a series of isolated shocks – sanctions, frozen reserves, tariff wars – is coalescing into a structural repricing of the entire currency framework. Beijing, according to Ferguson, will use every crisis to expand its parallel financial and payment infrastructure to the Middle East via petroyuan trade and central bank digital currency bridges. The shift away from the US dollar is not happening as a cliff but as a slope – and every crisis increases the incline.

For decades, the international order was based on free trade, the free movement of capital, and globally integrated supply chains, framed by US hegemony and the hegemony of the US dollar. This web of trust, contracts, and tacit agreements has developed deep cracks. Markets are entering a new regime, defined by geopolitics and a realignment of global trade relations. Stefan Zweig’s The World of Yesterday – that order whose permanence its inhabitants took for granted until it vanished overnight – is, as a metaphor, unfortunately more relevant than ever.

When (Geo-)Politics Becomes Inflationary

The market consequences of the Iran crisis are already visible – and structurally stagflationary. Brent crude oil has temporarily broken through the USD 110/barrel mark. The IEA speaks of the largest supply disruption in the history of the global oil market: Around 20% of global seaborne oil trade, as well as significant LNG volume, is affected.

This is precisely the stagflationary cocktail we warned about in the In Gold We Trust report 2022, “Stagflation 2.0”: a supply-side energy shock hitting an economy that is already chronically drained. Even if the acute Middle East conflict is de-escalated in the short term or even resolved permanently, we foresee a structurally higher price level for energy – a “higher structural floor” that will persist even after the conflict ends.

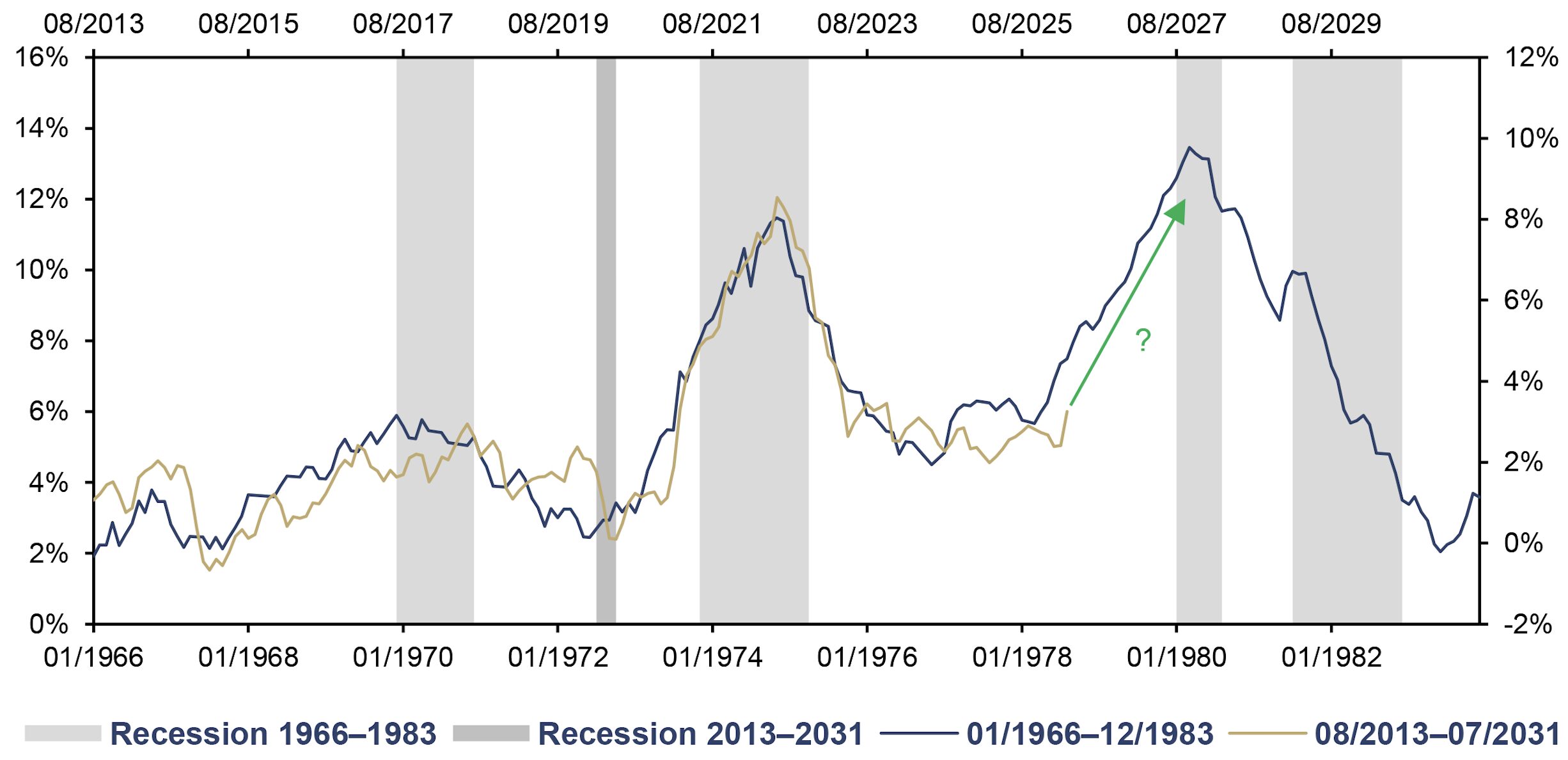

Furthermore, we do not rule out the possibility that, as in the 1970s, a second wave of inflation is looming. The course of inflation in the 1970s may offer a good indication of the future. The parallels between the developments are, in any case, striking.

US CPI, yoy, 01/1966–12/1983 (lhs), and 08/2013–07/2031 (rhs)

Source: Andreas Steno, LSEG, Incrementum AG

But inflationary forces are at work not only geopolitically but also domestically. Henry Maxey, CIO of Ruffer, outlines this dimension in his brilliant essay “Let Them Have Cake – and Circuses.” At the center: a US president with his back against the wall. As his popularity erodes and the November congressional elections threaten to turn into a trial of his presidency, Donald Trump is reaching into the toolbox of populism: an administrative cap on interest rates for credit card debt, the purchase of USD 200bn in mortgage-backed securities, stimulus checks – financed by tariff revenues. An economic perpetual motion machine.

Maxey picks up on a fascinating idea from Fre d Hirsch, which he expounded in The Political Economy of Inflation (1978): Inflation most often goes hand in hand with the breakdown of the social status order:

It is then no accident that inflation has been most entrenched in societies and periods in which the underlying ideological struggle has been most intense… Put another way, containment of the latent distributional struggle without financial instability requires either sufficient authority or sufficient consensus, on the values or principles underlying the distribution of income and other aspects of welfare. If established authority weakens before a sufficient consensus or a new authority emerges, inflation results.

The point is as elegant as it is uncomfortable: If societies cannot agree on who should lose out, inflation makes that decision – for everyone.

The ultimate consequence, according to Ruffer, is “DINOsty – Democracy In Name Only.” What Friedrich A. von Hayek described in The Road to Serfdom as the creeping erosion of the liberal order is taking place today not through tanks but through legal provisions: The legal campaign against the Chairman of the Federal Reserve is the harbinger of a systematic politicization of money. When the central bank’s independence becomes a bargaining chip in politics, domestic and foreign policy, fiscal and monetary policy merge into a single fiscal amalgam – with gold as one of the few assets that cannot be elected or dismissed.

The Remonetization of Gold

The erosion of institutional trust is often followed by a search for new – or proven – monetary anchors. It is precisely in this context that a development long considered unthinkable is gaining significance: the remonetization of gold.

On July 4, 2026, the US will celebrate its 250th anniversary. The symbolic significance of this date is considerable: The semiquincentennial could provide the historical occasion that has repeatedly triggered fundamental upheavals in the monetary order. Gold-backed bonds, a formal revaluation of gold reserves, or even a partial debt writeoff – such options are increasingly being discussed. A revaluation of the US gold reserves is no longer a far-fetched speculation, but a political possibility that is quietly gaining plausibility.

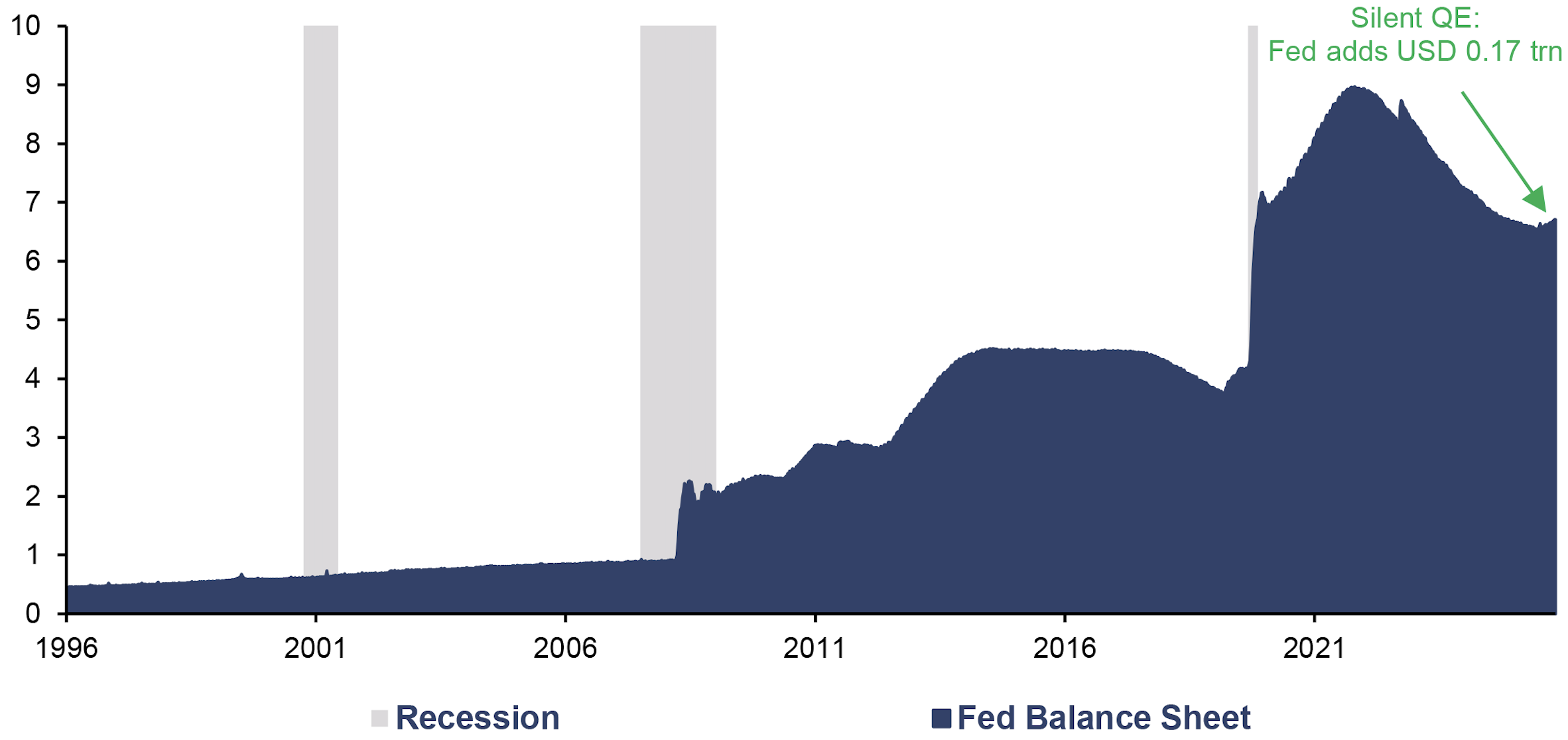

Kevin Warsh faces a dilemma: He wants to shrink the balance sheet and, in particular, divest long-term Treasuries and MBS. However, the official end of quantitative tightening on December 1, 2025, has shown that liquidity was simply too tight for that. Since then, the balance sheet of the Federal Reserve has risen by around USD 175bn to USD 6.7trn. Officially, this balance sheet expansion is labeled as reserve management, but economically it acts like “quiet QE”.

Fed Balance Sheet, in USD trn, 01/1996–04/2026

Source: LSEG, Incrementum AG

Of the USD 4.8trn in balance sheet expansion during the pandemic, only about half has been unwound to date. Should the next recession or financial market shock break the US fiscal straitjacket – rising deficits coupled with weakening foreign demand for US Treasuries – “quiet QE” could quickly give way to “The Big Print”, the inflationary endgame that our friend Larry Lepard has been warning about for years.

In such a challenging environment, unconventional options are needed, such as revaluing US gold reserves at market prices. The US holds exactly 261,498,926 troy ounces of gold, or roughly 8,133 t. This is the world’s largest government gold reserve. However, these holdings are still in the books at the price of USD 42.22 per troy ounce, which has been fixed by law since 1973. The reported book value thus amounts to just USD 11.04bn. A revaluation at the current market price of around USD 4,600 per ounce would multiply this value to approximately USD 1.2trn. This corresponds to about 3% of the total US national debt. This book profit in the trillion US dollar range would be available to the US Treasury as fiscal leeway.

Two pieces of evidence suggest that the idea has already emerged from the realm of theory. First, US Treasury Secretary Scott Bessent stated: “We’re going to monetize the asset side of the US balance sheet.” Second – and even more remarkable – in August 2025, the Federal Reserve published a paper with the programmatic title “Official Reserve Revaluations: The International Experience”.

History provides a precedent – and a remarkably instructive one: With the Gold Reserve Act of January 30, 1934, Franklin D. Roosevelt raised the official price of gold from USD 20.67 to USD 35 per ounce. This corresponded to an effective devaluation of the US dollar against gold of 41%. The one-time seigniorage gain of approximately USD 2.8bn flowed into the newly created Exchange Stabilization Fund (ESF) and thus into the Treasury vehicle that still exists today, allowing the Secretary of the Treasury to intervene in foreign exchange markets without congressional approval. Further US dollar devaluations followed in 1972 and 1973, first to USD 38, then to the current rate of USD 42.22.

For the US, not only is a one-time revaluation conceivable, but also a shift to market-valued gold reserves, similar to the situation in the eurozone. This would make hidden reserves visible and ensure that future increases in the gold price are continuously reflected on the balance sheet. In addition to the one-time effect, the investment perspective from the government’s standpoint is equally revealing in this context: What economic dynamics arise when central banks value gold at market prices?

Market-valued gold reserves create an asymmetric exposure to rising gold prices. If the gold price rises, the value of the reserves increases immediately and can enable higher distributions, stronger capital buffers, or additional room for maneuver. If the gold price falls, negative effects are absorbed through revaluation accounts, reduced retained earnings, or the forgoing of distributions. The resulting profile resembles a historically embedded call option: substantial upside potential with limited immediate burden on the owner. In times of high debt and fiscal constraints, gold thus transforms from a passive reserve asset into strategic optionality – in short: Free Gold.

Emerging economies are also eagerly driving forward the remonetization of gold. Under the project name “The Unit,” Russian researchers are working on a gold-backed settlement instrument for intra-BRICS trade: 40% physical gold, 60% currency basket of the five founding members. It is still a research project, not an official BRICS program. Yet the concept itself is a signal: In any serious post-US dollar architecture, gold will play a pivotal role.

In this context, Bernhard Matthes has pointed out a fascinating parallel: The gold purchases by central banks in Asia and the Middle East are not mere diversification; they resemble a strategic positioning race. Should gold indeed become the monetary anchor of a BRICS settlement system, every participating nation will face the same question as the euro accession candidates of the 1990s: At what exchange rate will my currency be incorporated into the new system?

Those who hold substantial gold reserves at this point will enter the new order from a stronger starting position. Viewed in this light, the conspicuous buildup of gold reserves by China, India, Türkiye, and a growing number of other central banks follows a sober logic: It is about securing monetary leverage for an architectural framework that has not yet been established, but for which they are already positioning themselves. Or, to put it more colloquially, following the example of the German vacationer in Mallorca who lays his towel on the beach chair at six in the morning, whoever reserves first gets the best spot.

At the same time, the Shanghai Gold Exchange (SGE) is systematically expanding its infrastructure. Gold is thus transforming from a safe-haven asset into a settlement instrument: repo-eligible collateral, a component of coverage, and a potentially neutral unit of account. What is quietly taking shape here is the beginning of a parallel financial system with Asia as its center of gravity.

The following metaphor suggests itself: China is playing Go – patiently, strategically, focused on encirclement – while the US is playing poker, relying on short-term bluffs and maximum leverage. And Europe? Sitting at the table, having translated the rules into twenty-four languages, having commissioned an impact assessment and convened an ethics advisory board, while the others have long since begun their respective games.

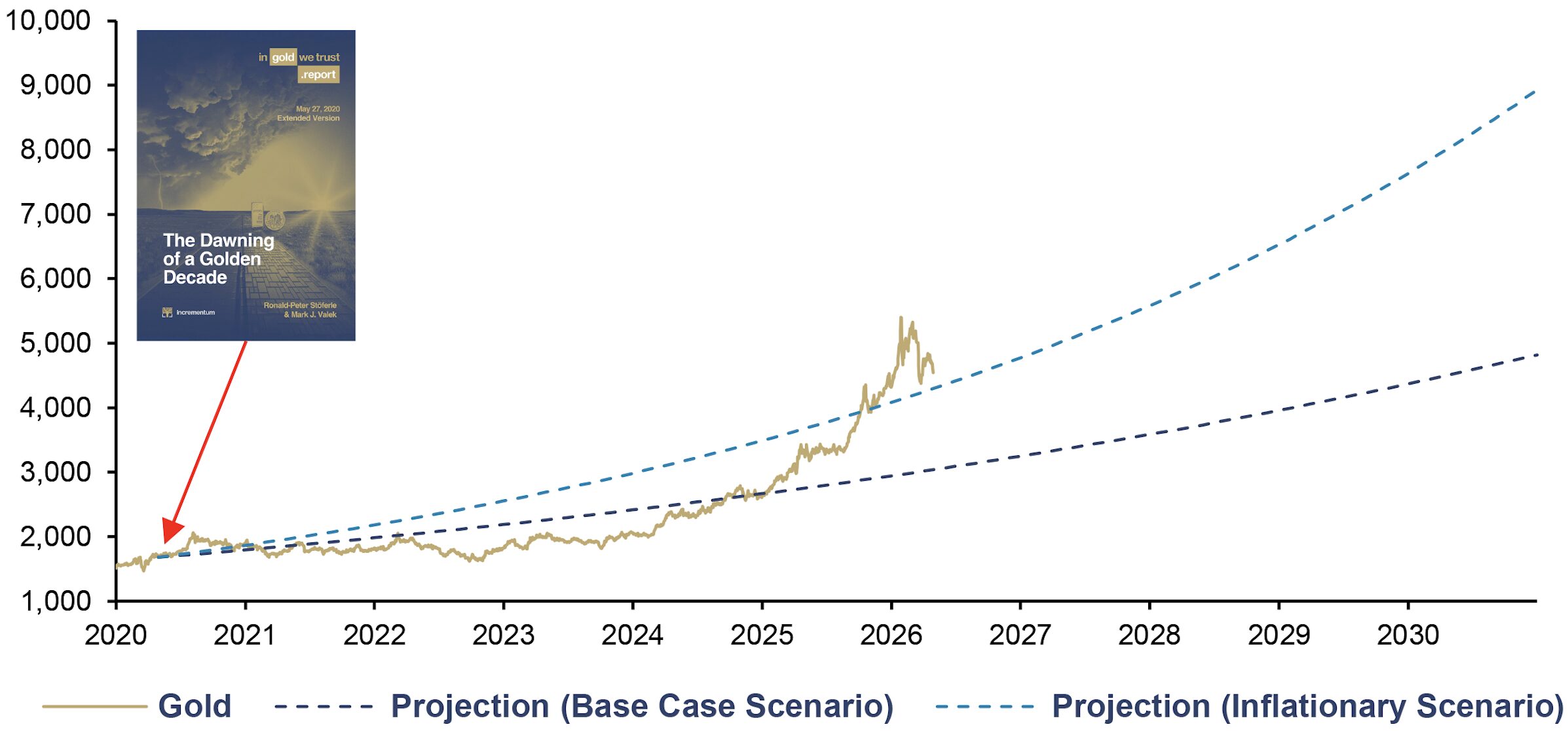

The Golden Decade Is in Full Swing

At the heart of our analysis lies a single thesis: The gold bull market of recent years is the manifestation of a long-term upward trend that we announced in the In Gold We Trust report 2020, titled “The Dawning of a Golden Decade.” We were met with skepticism from the mainstream for this. But the numbers speak for themselves. Since we proclaimed the golden decade, the price of gold in US dollars has risen by 165%, or, to put it differently, the US dollar has depreciated against gold by almost two-thirds.

Gold, in USD, 01/2020–12/2030

Source: LSEG, Incrementum AG

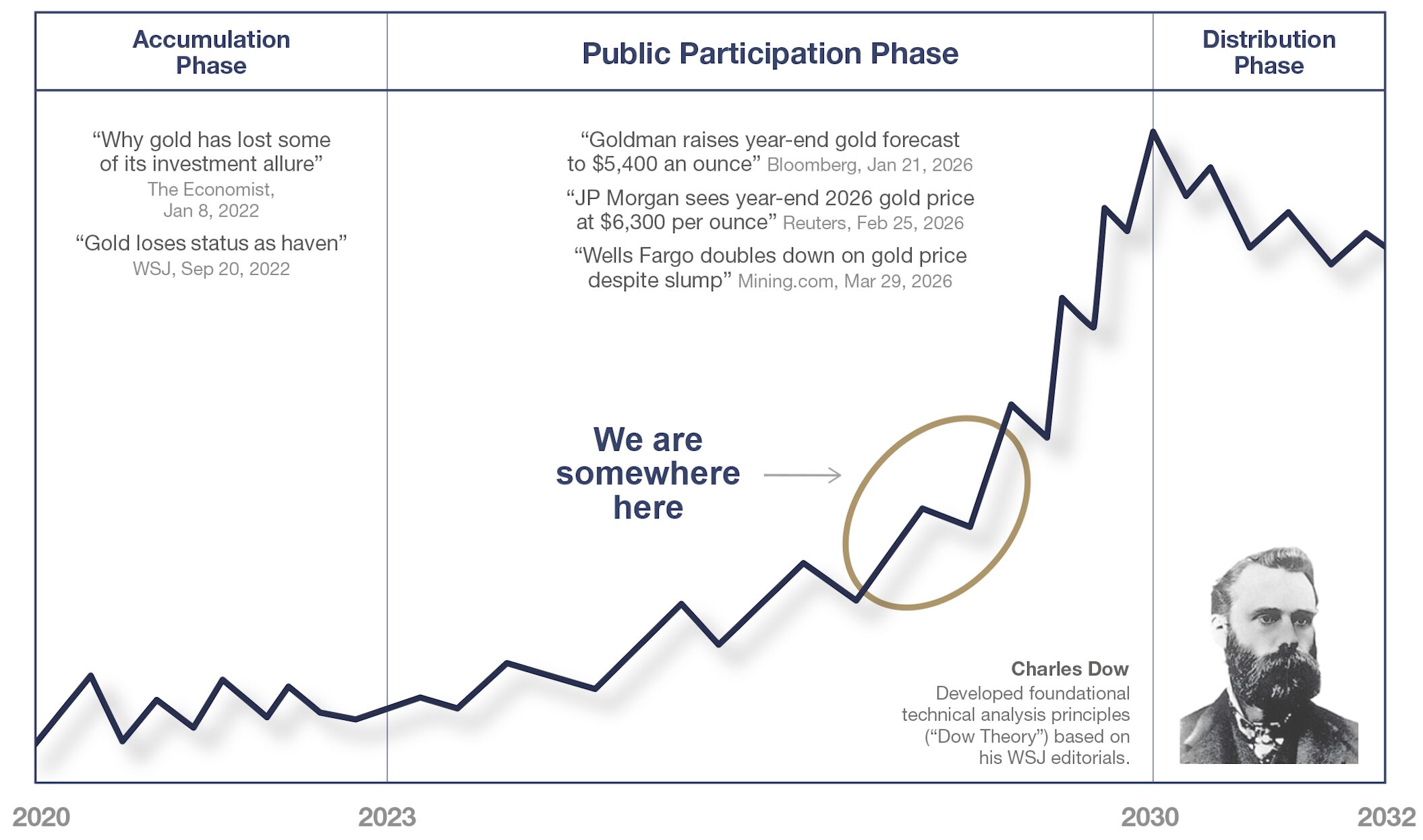

According to Dow Theory, we are currently in the middle of the public participation phase, the longest and most dynamic stage of a bull market. This phase is characterized by increasingly optimistic media coverage. At the same time, speculative interest and trading volumes are rising, new financial products are being launched, and analysts who have viewed gold with skepticism for years are suddenly and aggressively revising their price targets upward. In our assessment, we are roughly in the middle of this phase, which will ultimately culminate in a mania phase.

Where We Think We Are in the Bull Market (Dow Theory)

Source: MiningVisuals, Incrementum AG

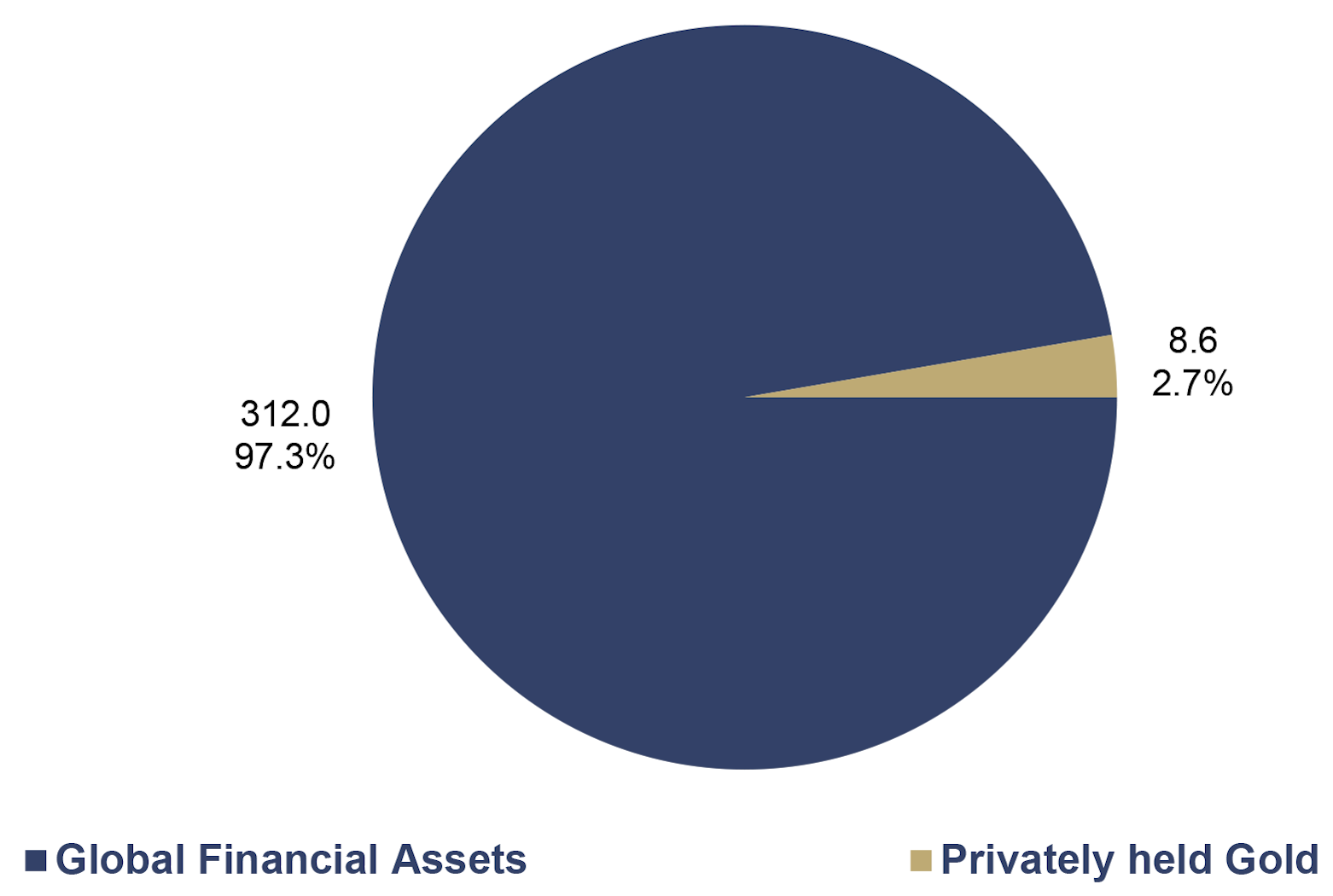

The scale of the market makes it unmistakably clear that we are still far from a mania phase: Global financial assets of USD 312trn contrast with privately held gold holdings of USD 8.6trn – 2.7% of the total volume. Gold is anything but a crowded trade – on the contrary, it is a party where the first guests are just starting to arrive.

Market Capitalization of Global Financial Assets and Privately held Gold, in USD trn, 2025

Source: BIS, ICE, Metals Focus, Preqin, SIFMA, WFE, World Gold Council, Incrementum AG

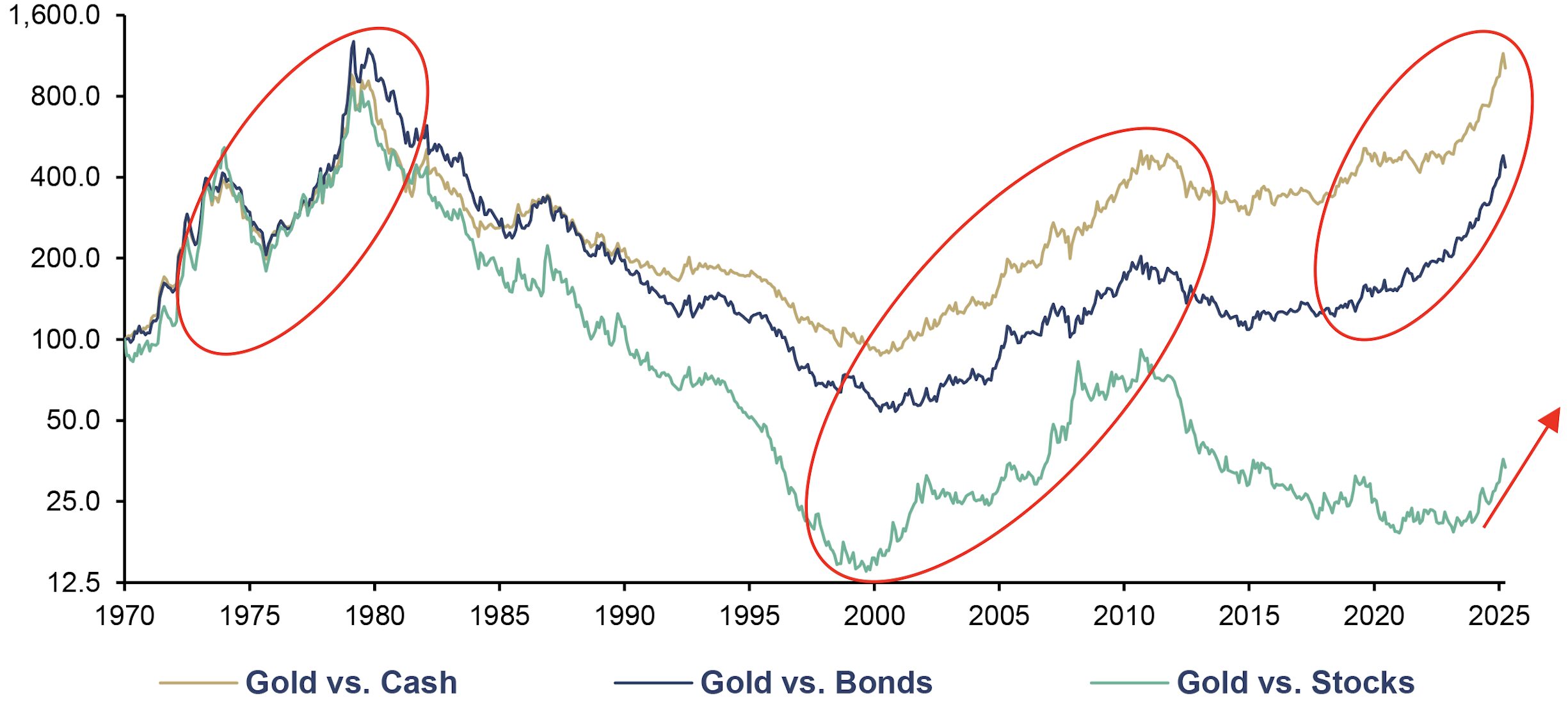

Gold is also showing technical breakouts on a relative basis. Compared to cash and government bonds, the precious metal has already reached new cycle highs – but compared to US stocks, the catch-up rally is only just beginning. The chart below illustrates this impressively: While the gold-to-cash and gold-to-bond ratios have surpassed the secular highs of the early 1980s, the gold-to-stocks ratio is still well below the cycle highs of 1980 and 2011.

Gold vs. Cash (US 3M TR), Bonds (US 10Y TR), and Stocks (S&P 500 TR) (log), 100 = 31/12/1970, 12/1970–03/2026

Source: Topdown Charts, Robert J. Shiller, LSEG, Incrementum AG

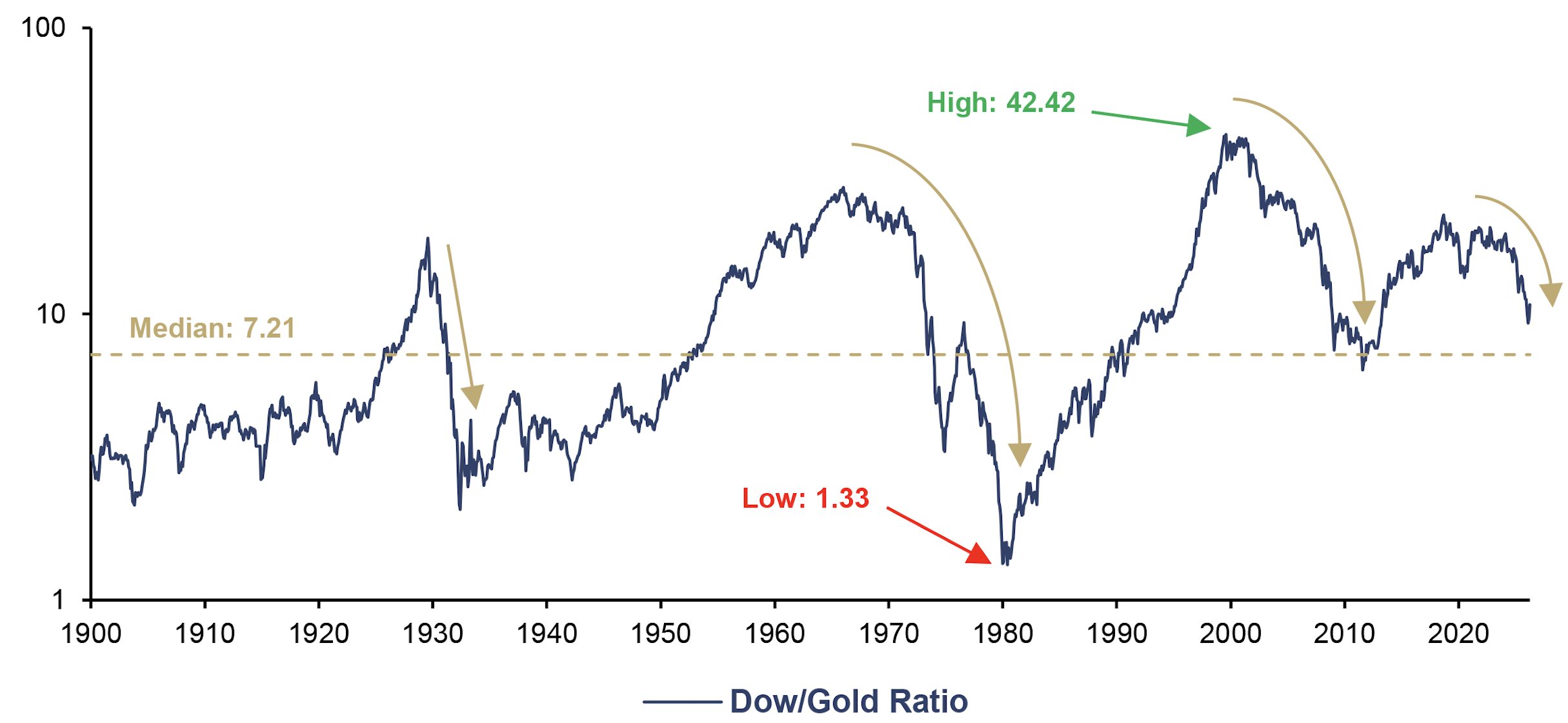

Given that gold has recently gained ground against stocks, it is worth taking a long-term look at the Dow/gold ratio. During the past three major downtrends in this ratio – the 1930s, 1970s, and 2000s – the trend was consistently accompanied by a significant rise in the price of gold and stagnant US stock markets. Currently, the Dow/gold ratio stands at 10.74, well above the historical median of 7.21. Gold remains attractively valued relative to US stocks.

Dow/Gold Ratio (log), 01/1900–04/2026

Source: Nick Laird, LSEG, Incrementum AG

The baton is passing: From central banks to investors

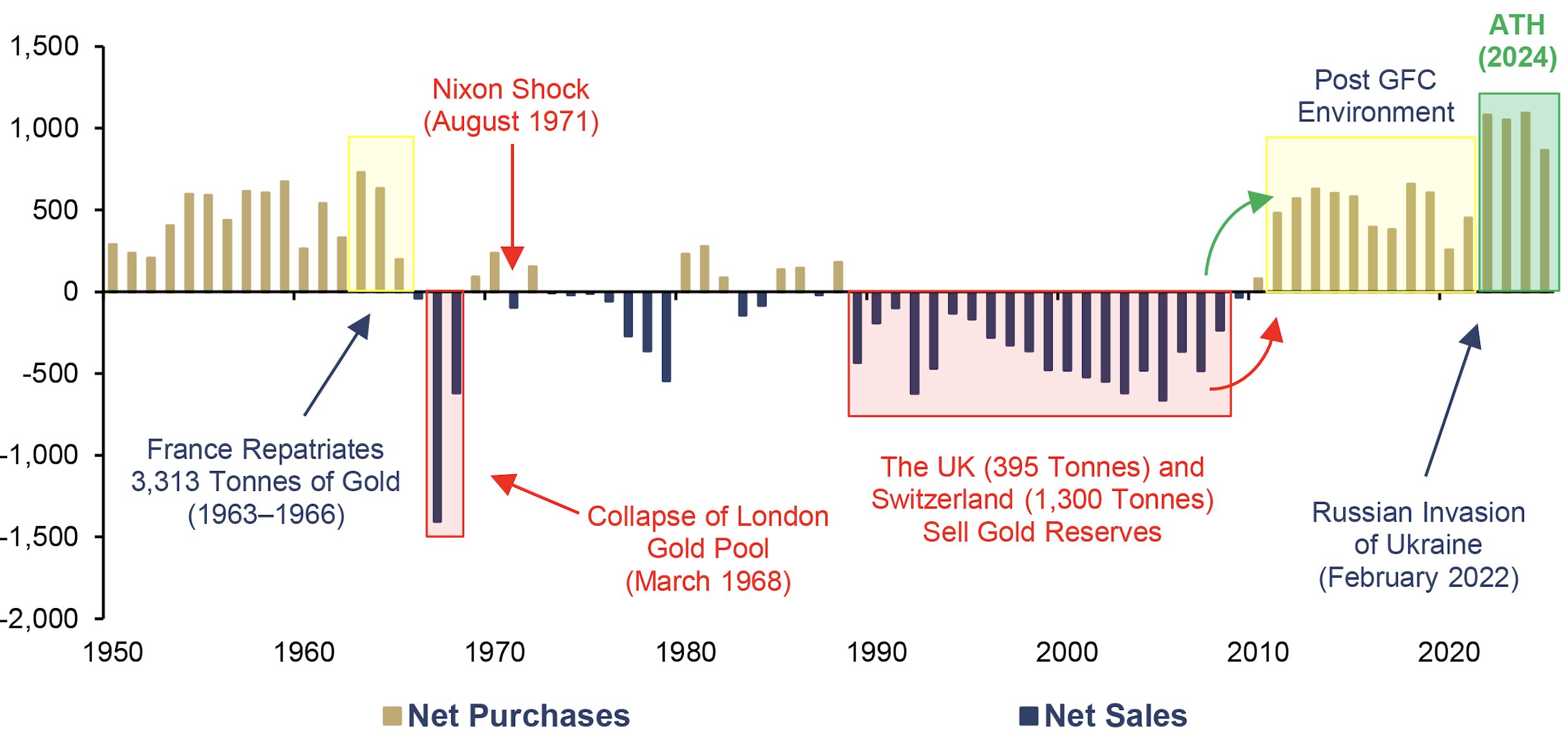

The demand structure of the gold market has shifted in recent quarters. Central banks have bought over 1,000 t in three of the last four years (2022, 2023, 2024), with 863 t added in 2025. In terms of value, this amounts to USD 60–85 bn per year. To put this in perspective: With global mine production at around 3,600 t per year, central banks alone are absorbing nearly a quarter of annual output.

Global Central Bank Gold Purchases, in Tonnes, 1950–2025

Source: ICE Benchmark Administration, Metals Focus, Refinitiv GFMS, World Gold Council, Incrementum AG

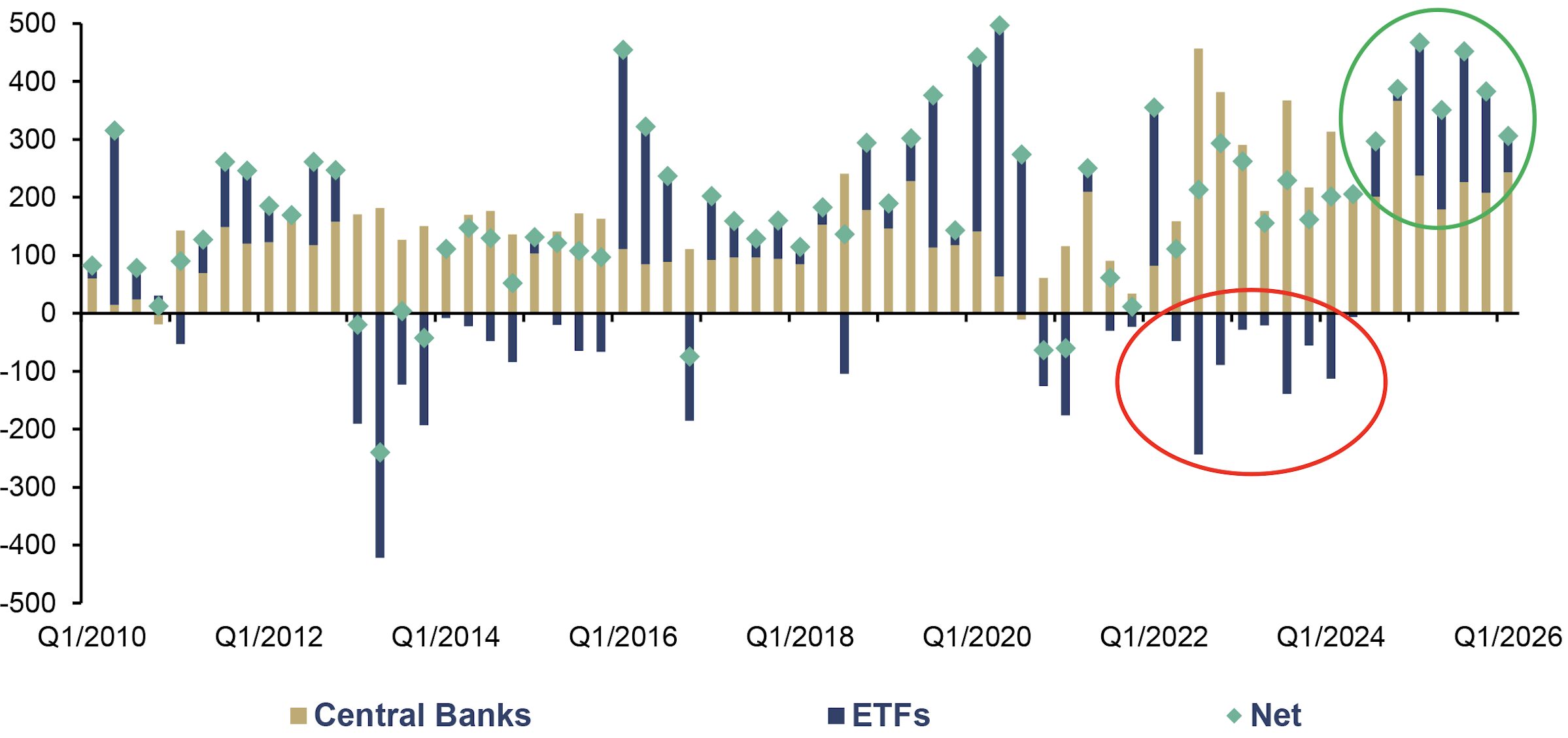

For several quarters now, we have observed a shift: Retail investors, institutional buyers, and ETF inflows have taken the baton from central banks. This is the handoff that, in Dow Theory, is considered a hallmark of a fully developed public participation phase: The bull market, still supported by central banks during the accumulation phase, is now being shouldered aside by a broader investor base. The bull market has entered the mainstream.

Central Bank, ETF, and Net Gold Flows, in Tonnes, Q1/2010–Q1/2026

Source: World Gold Council, Incrementum AG

But with this shift, the risks are changing. Central banks are price-inelastic demanders. They accumulate driven by strategic considerations, not by expectations of returns. Investors, on the other hand, react to sentiment, margin calls, and opportunity costs. March 2026 abruptly laid bare this dynamic: According to the World Gold Council, gold ETFs recorded the largest monthly outflow on record at USD 11.8bn, or 84.8 t. The sell-off was concentrated almost exclusively in the West, while Asia, led by China, remained a net buyer. The pattern is revealing: Western ETF investors sell procyclically into the pullback, while Asian buyers use precisely these price declines to build positions. The question every investor ought to ask: Into whose vaults is Western gold quietly flowing?

Our assessment remains nuanced: The secular bull market is intact, but the shift in the demand structure calls for vigilance. Corrections of 20–30% were not the exception but the rule in past gold bull markets. At current levels, absolute pullbacks of USD 800–1,000 are quickly labeled a crash – even though, until recently, that represented the entire gold price.

It is therefore crucial to distinguish between safe-haven gold – the strategic physical core holding, which is held independently of market events – and performance gold, the tactical component that specifically bets on price increases and must be actively managed accordingly. Those who hold performance gold need not only conviction but also nerves of steel – and consistent risk management.

Providing precisely this perspective – sober, fact-based, with a touch of humor, independent of market euphoria or doomsday prophecies – has been our mission for twenty years.

Thank You Very Much!

Year after year, the In Gold We Trust report strives to live up to its reputation as the “gold standard of gold studies.” Our goal is to produce the world’s most widely read and comprehensive analysis of gold. The gallery of 20 years of In Gold We Trust reports reflects this commitment.

This year’s leitmotif, “Back to the Monetary Future,” was carefully chosen. The monetary policy decisions of past decades – from the abandonment of the gold standard in 1971 to the era of zero interest rates after 2008 – are key to understanding what is happening in the markets today. In Back to the Future, Doc Brown warns Marty McFly emphatically: “We must not interfere with the timeline!” Yet that is precisely what central banks have done: With their monetary policy, they have fundamentally distorted the natural monetary order. We are now experiencing the consequences in real time – persistently elevated inflation rates, asset price bubbles, and an increasing flight to real assets like gold.

If our analyses are correct – and the data since 2007 gives us reason for confidence – then the current gold bull market still has considerable potential ahead of it. For while Marty McFly needed a DeLorean to travel through time, a glance at monetary history is enough for us to foresee the monetary future.

In the 20th edition of the In Gold We Trust report, we remain committed to the philosophy of kaizen, the Japanese art of continuous, incremental improvement: Twenty years of publication are not a reason for us to rest on our laurels, but rather an incentive. This year, the report features a completely revamped design and a redesigned webpage. We have also brought creative reinforcements on board with Mining Visuals, a Swedish specialist in the graphical presentation of mining sector data. Our core team has also grown significantly. As in 2025, the short version is available in German, English, Spanish, and Japanese. And once again, the In Gold We Trust report is available as a printed edition on Amazon – because some things, like gold and good research reports, you just want to hold in your hands.

We thank our more than 20 wonderful colleagues across four continents for their tireless efforts spanning over 20,000 hours and countless time zones.

Special thanks go to our Premium Partners.[2] Without their support, it would not be possible to make the In Gold We Trust report available free of charge and to expand our range of services year after year. In addition to the annual publication in five languages, we provide our Monthly Gold Compass as well as ongoing information on our In Gold We Trust website at ingoldwetrust.report.

To prepare for the future of money, one must first return to its past. That is why we are convinced that the current gold bull market still has considerable room to run. We would like to present the reasons behind our assessment to you, our valued readers, as a reliable guide to the topic of gold across the more than 460 pages of the In Gold We Trust report 2026.

We now invite you to join us on our annual journey and hope that reading our 20th In Gold We Trust report brings you as much joy as writing it has brought us.

With warm regards from Liechtenstein,

Ronald-Peter Stöferle and Mark J. Valek

[1] See chapter “Gold and the Monetary Analogue of Mackinder’s Foundational ‘Heartland Theory’” in this In Gold We Trust report

[2] At the end of the In Gold We Trust report, you will find an overview of our premium partners, including a brief description of each company.