Dollar Milkshake Meets Mar-a-Lago

“A strong nation, like a strong person, can afford to be gentle, firm, thoughtful, and restrained. It can afford to extend a helping hand to others. It is a weak nation, like a weak person, that must behave with bluster and boasting and rashness and other signs of insecurity.”

Jimmy Carter

- The global monetary system has split into competing blocs (US, EU, BRICS+), with middle powers pivoting. All increasingly anchor their systems to gold and hard assets as universal trust mechanisms.

- The Trump administration is crafting a “Mar-a-Lago Accord”, a bold economic and security pact featuring aggressive tariffs, binding defense commitments, and gold-backed bonds designed to overhaul the global monetary order. The goal? To resolve the Triffin dilemma, which Washington claims has long distorted trade and eroded US dominance.

- A strategic trifecta emerges: tariffs as leverage, a Plaza-style currency reset, and gold bonds as a credibility anchor.

- Beyond policy efforts, market forces may trigger a 20–30% dollar decline as capital shifts from US assets, ending the long-standing premium on American exceptionalism.

- Geopolitical fragmentation gives gold dual upside: direct holdings hedge instability, while select miners gain as gold rises and costs stabilize. Gold now offers both defense and offense.

- The Big Long unfolds: a macro bet on a future system anchored not in credit but in scarce, unprintable collateral.

Introduction

The new administration appears to grasp what previous ones missed: trade imbalances persist in today’s financial system because massive capital flows overwhelm traditional trade relationships.

The US runs persistent deficits not because it consumes too much or produces too little, but because it absorbs too much of the world’s excess savings.

Policy success will require addressing this root cause. Either through negotiated adjustment – a Mar-a-Lago Accord – or unilateral capital flow restrictions, the goal is to reduce foreign purchases of US financial assets and increase their purchases of US goods and services.

Michael McNair

De-dollarization is a process.[1] Yet, this process is neither linear nor one-dimensional. While BRICS+ nations and their allies implement alternative payment systems and currency swap arrangements and accelerate central bank gold purchases to reduce their reliance on Western financial markets, opposing forces fight to reinforce the greenback’s dominance. As each network increasingly relies on gold and other hard assets as anchors of stability, The Big Long emerges – an asymmetric macro bet that the future monetary system will be anchored in collateral you can’t print.

Like the environment preceding Federal Reserve Chair Paul Volcker’s monetary “shock” in the 1980s, today’s Western financial system requires a fundamental recalibration to restore lost credibility. However, unlike the Volcker era, contemporary debt levels prevent the Federal Reserve from raising rates high enough to produce a similar outcome to what Volcker achieved, necessitating a pivot to hard assets.

This chapter examines the fracturing global economic order through various theoretical lenses, assessing their relevance and applicability in practice. We start by shedding light on the rising tensions between the America-First-driven policies of the United States and the BRICS+ nations – most notably China’s pursuit of greater monetary autonomy. This dynamic signals a broader shift in international relations, moving from multilateral cooperation to more bilateral engagements.

Building on this, we critically examine the possibility of a significant realignment in the global monetary and trading system, mirroring historic agreements such as the Plaza and Louvre Accords. Since the publication of Stephen Miran’s blueprint “A User’s Guide to Restructuring the Global Trading System”,[2] the term Mar-a-Lago Accord, named after Donald Trump’s resort in Florida, has become the common appellation for this potential fundamental realignment. We will explore various efforts to bring about this recalibration, including mechanisms such as gold-backed bonds and financial repression.

De-Westernization: The Fracturing Global Economic Order

What began as de-dollarization has evolved into a broader movement toward de-Westernization, with gold emerging as a primary beneficiary. Two forces are driving this transformation: the East and Global South pivoting to alternative economic frameworks, and internal fracturing within the Western alliance following President Donald Trump’s return to the Oval Office.

As contrarian investors positioned themselves against prevailing narratives in 2007, forward-thinking investors are now reassessing their core assumptions about currency dynamics, trade relationships, and global power structures. This shift will manifest in abrupt changes to asset allocation and international capital flows. The foundation of trust in the international system is gradually, but now also suddenly, eroding.

What was once East versus West is now US vs. EU vs. BRICS+, with certain nations in the Middle East and Global South positioning themselves as neutral or semi-allied middle powers. As the G7 faces unprecedented disunity, the expanded BRICS+ bloc (Brazil, Russia, India, China, and South Africa, plus Egypt, Iran, UAE, Ethiopia, and Indonesia) is forging ahead into the new multipolar system, increasingly underpinned by gold to establish universal trust.

America First: Bilateral vs. Multilateral

President Trump’s America First approach to economic policy rejects the notion that the US must stabilize global trade. By prioritizing bilateral deals over multilateral frameworks, Trump is delivering on his campaign pledge to overturn what he sees as decades of US negotiations from weakness. This strategy marks a clean break with past administrations, favoring immediate national gain over long-term global system stability.

The retreat from multilateralism impacts US monetary mechanisms. “Swap lines won’t be free anymore. They’ll come with strings, or maybe chains,” writes Brent Johnson. Trump could transform the Federal Reserve’s dollar swap lines (which provided USD 500bn to foreign central banks in 2020 to help prevent a liquidity crisis) from cooperative infrastructure into negotiating leverage. The underlying message is clear: Access to dollar liquidity is no longer automatic but conditional on meeting specific policy requirements.

Further, the Trump administration’s withdrawals from multilateral institutions like the WHO, the Paris Climate Agreement, and the UN Human Rights Council signal a retreat from global cooperation. This weakening of Western cohesion has pushed European partners toward more euro-centric strategies, including Germany’s military spending increases and the ECB’s development of a digital euro that would reduce reliance on US financial infrastructure.

The US Dollar Milkshake in Action

The Dollar Milkshake Theory provides a framework for understanding current market dynamics.[3] It originates from our friend Brent Johnson, who kindly agreed to describe the essence of the theory in his own words.

The Milkshake Theory is a realpolitik framework for understanding the global monetary system – a model grounded not in how we might wish the world to operate, but in how capital actually moves through it. It focuses on the hard constraints of liquidity, credit, and sovereign debt – forces that override political idealism and economic theory in moments of crisis. Far from only offering a forecast of specific outcomes, it provides investors with a pragmatic lens for interpreting market behavior when the realities of global debt burdens collide with the structural demand for US dollars. In a world shaped by self-interest, scarcity, and competition for capital, this is not about what we want to happen – it’s about what the mechanics say will happen when stress emerges.

The theory explains why the US dollar usually strengthens during systemic shocks. Even though – or precisely because – the global financial system is based on the US dollar, it benefits during severe turbulence, as international capital flows toward America’s liquid markets, robust financial system, and established rule of law.

We saw this in action through Panama’s BRI-xit in February 2025 when Panama formally withdrew from China’s Belt and Road Initiative (BRI) under pressure from the Trump administration, prioritizing bilateral trade with the United States instead. This illustrates how the Dollar Milkshake works: By shaking up established trade relationships, the US successfully redirected financial flows back toward dollar-denominated commerce.

This pattern extends beyond Panama. Since Trump’s inauguration, an escalating tariff war has forced even G7 members to confront the US economic might in bilateral trade negotiations. Even Canada and Mexico – America’s closest trading partners and neighbors – have not been exempt from Trump’s hardline position. The early evidence supports the Milkshake effect, as major multinationals from Asia, Europe, and the Middle East committed hundreds of billions in new US investments post-2025:

- The UAE agrees to USD 1.4trn in US economy investments over 10 years.

- Taiwan Semiconductor (TSMC) pledges USD 100bn for US-based chip manufacturing.

- Apple commits USD 500bn to US-based AI and manufacturing initiatives.

Trump’s tariffs threaten trade flows that have historically generated dollar revenues, creating an even greater dependence on American capital markets for access to dollars. The question is not whether the Milkshake effect exists but how it might be deployed as a tool of economic statecraft.

However, Trump’s dual pursuit of a weaker dollar to boost exports creates tension with his insistence on US dollar dominance in global trade. This inconsistency destabilizes the dollar’s ability to serve as an economic anchor, elevating gold’s role amidst currency volatility and policy unpredictability.

Economic Statecraft Leading to De-Dollarization?

The evolution of economic warfare

Besides the tariffs that have shocked markets and dealt severe blows to the world economy, the freezing of Russian assets and the weaponization of the financial system through the US-controlled SWIFT system have demonstrated that every country is vulnerable to Western financial power. These actions can be characterized as economic statecraft, where nations deliberately leverage their economic resources as instruments of power projection rather than solely for wealth creation. For this reason, countries that may seem antagonistic to US hegemony have sought alternative means to transact and save, accelerating de-dollarization that had been gradually advancing since the Global Financial Crisis.

The economic statecraft concept was explored in an excellent report by Michael Every at Rabobank. When analyzing its key characteristics, one recognizes it is at odds with the precepts of economic policy. This is protectionism rebranded – a case of old wine in a new bottle.

While economic policy uses fiscal, monetary, and trade tools to achieve financial goals, such as inflation or budget-deficit targeting, economic statecraft employs economic means – sanctions, export controls, tariffs, investment restrictions, and price caps – to advance foreign policy and national security goals. Thus, understanding a state’s national interests, one might surmise how it would use economic statecraft to achieve its goals.

Despite Trump’s post on his Truth Social that any BRICS+ country moving away from the US dollar system, or even attempting to create a BRICS+ currency, would “face 100% Tariffs, and should expect to say goodbye to selling into the wonderful US Economy”, there was no need to make such a threat. Given Indian External Affairs Minister Subrahmanyam Jaishankar affirming that “we have absolutely no interest in undermining the dollar at all”, after declaring in mid-November that “India has never been for de-dollarization”, the US would appear to have nothing to worry about. Without sanctions, there would not have been such serious attempts at ditching the US dollar.

China’s Strategic Autonomy

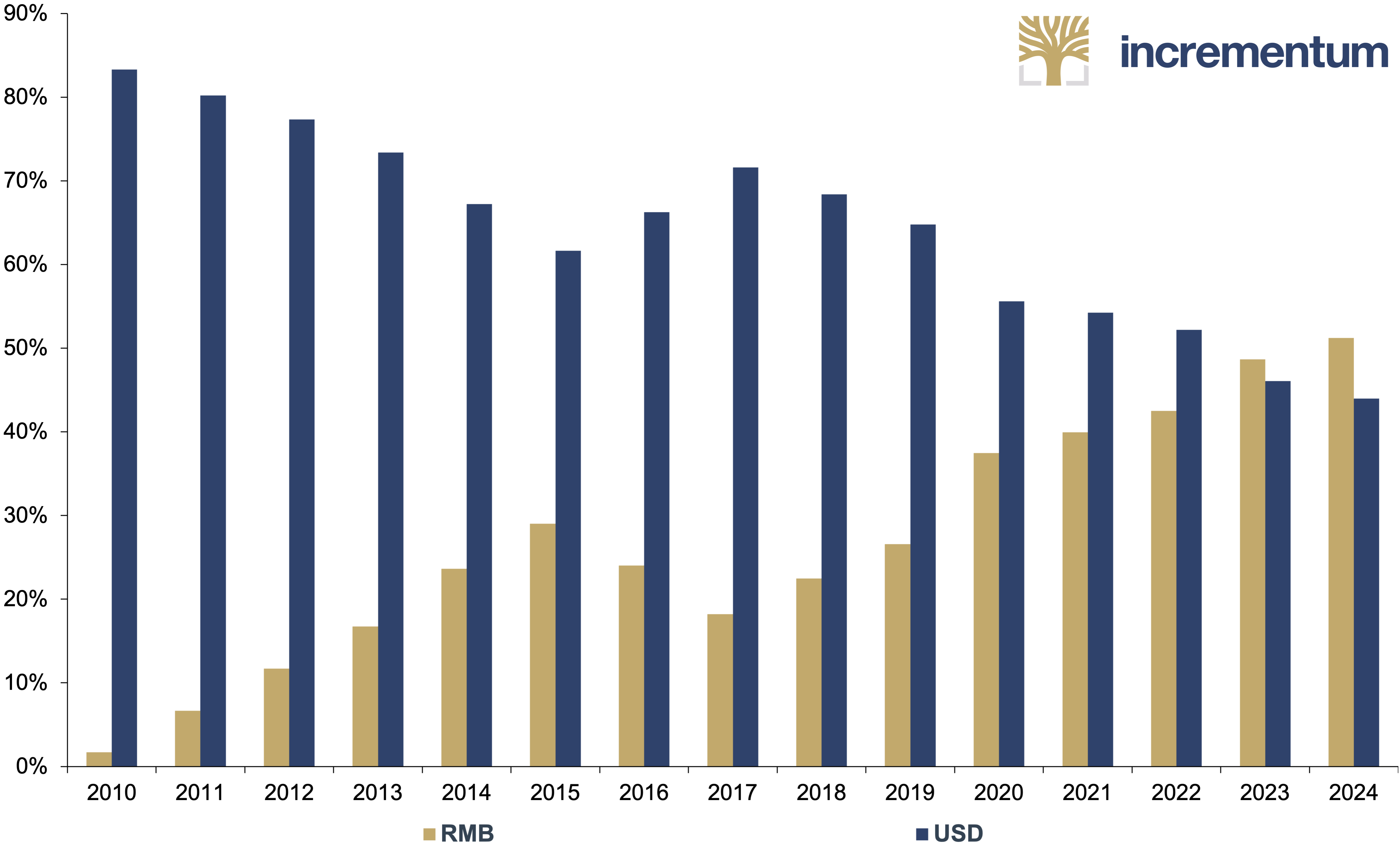

Meanwhile, China methodically cements its autonomy from Western finance. By March 2023, the renminbi accounted for 53% of China’s cross-border payments, overtaking the US dollar’s 43% – down from 83% in 2010. “China is not seeking to topple the dollar’s global dominance. That comes with much responsibility and accepting certain vulnerabilities. China’s motives here are primarily about autonomy and resilience,” writes Syracuse University professor and Atlantic Council senior fellow Daniel McDowell.

Share of China’s Cross Border Payments and Receipts, 2010–2024

Source: Chinese State Administration of Foreign Exchanges (SAFE), Incrementum AG

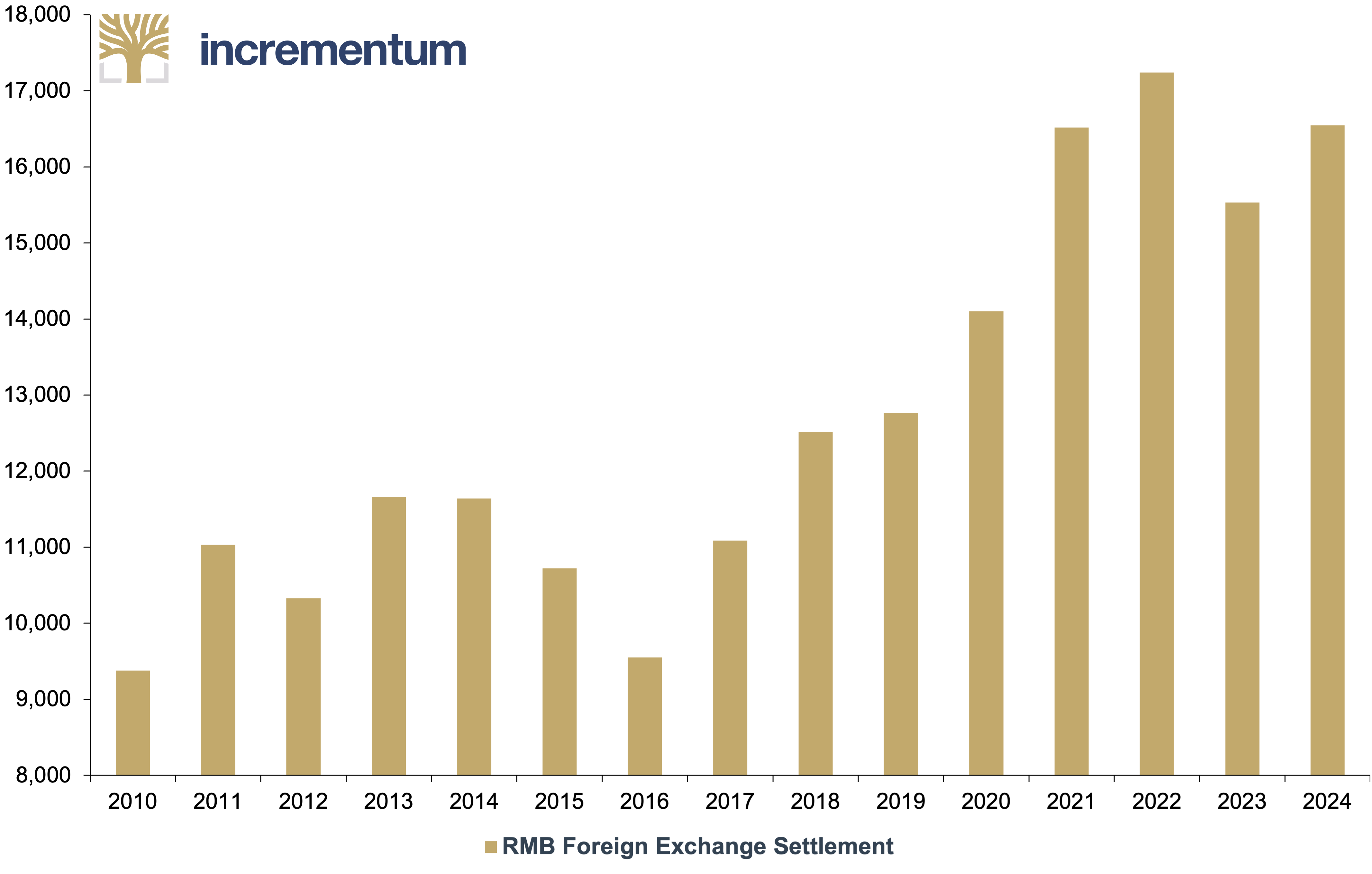

The People’s Bank of China reported that this shift was led by 12,400 new market entities in Shanghai choosing the RMB for cross-border settlements in 2024. The city’s cross-border RMB settlement under trade in goods increased by 30% yearly, while the settlement of commodities such as precious metals, iron ore, and grain doubled during the same period.

By September 2023, China had signed bilateral local currency swap agreements with 30 Belt and Road Initiative (BRI) participating countries and established RMB clearing arrangements in 17 BRI countries.[4] The Cross-border Interbank Payment System (CIPS), launched in 2019, now reaches over 3,000 banking institutions across 167 countries and regions, creating an alternative to the Western-dominated SWIFT system.

RMB Foreign Exchange Settlement, in RMB bn, 2010–2024

Source: Chinese State Administration of Foreign Exchanges (SAFE), Incrementum AG

The Energy and Commodity Nexus

Energy and commodity trading are leading the shift toward alternative payment systems. According to the Russian ambassador to China, 92% of Russia-China trade settlements in 2024 were conducted in local currencies (rubles and yuan).

Saudi Arabia’s 2024 decision to join the Bank for International Settlements (BIS) and Project mBridge – a collaborative effort led by BIS and China to settle trades using multiple central bank digital currencies – marked another significant development. Josh Lipsky, who runs a global CBDC tracker at the Atlantic Council, observed:

The most advanced cross-border CBDC project just added a major G20 economy and the largest oil exporter in the world… This means in the coming year you can expect to see a scaling up of commodity settlement on the platform outside of dollars.

Project mBridge represents one of the most advanced alternatives to dollar-dominated payment systems. By mid-2024, the project reached the minimum viable product (MVP) stage, with participating central banks deploying validating nodes and commercial banks conducting real-value transactions. Saudi Arabia’s 2024 entry has coincided with the Kingdom’s growing interest in reducing dollar dependence, including its USD 6.93bn currency swap agreement with China in late 2023. The platform’s growing observer membership now includes 31 entities, ranging from the European Central Bank to the Reserve Bank of India and the Bank of Brazil. This reveals the seriousness with which monetary authorities are exploring dollar alternatives. This development provides oil exporters with infrastructure to support petrodollar alternatives and bypass Western payment rails.

Stablecoins: A Counterforce to De-Dollarization?

As BRICS countries push forward with de-dollarization efforts and explore alternatives to the US dollar, stablecoins have emerged as a noteworthy counterbalance – particularly in the Global South. As a digital technology solution, they offer an entry point into US dollar-based liquidity, strengthening the demand for the world’s reserve currency in emerging markets.

With a market capitalization of roughly USD 230bn and settling of over USD 10trn of transactions (cross-border remittances, exchange trading, on-/off-ramping into other cryptocurrencies, and payments) annually, stablecoins already act as a crucial dollarizing force. Federal Reserve Governor Christopher Waller recognized the dollarizing aspect of stablecoins in early 2024, noting that

…most trading in decentralized finance (DeFi) involve trades using stablecoins, which link their value one-for-one to the US dollar. About 99 percent of stablecoin market capitalization is linked to the US dollar, meaning that crypto-assets are de facto traded in US dollars. So it is likely that any expansion of trading in the DeFi world will simply strengthen the dominant role of the dollar.

The Trump administration has recognized this opportunity, with Treasury Secretary Scott Bessent explicitly stating at the 2025 White House Digital Asset Summit: “As President Trump has directed, we are going to keep the US the dominant reserve currency in the world, and we will use stablecoins to do that.”

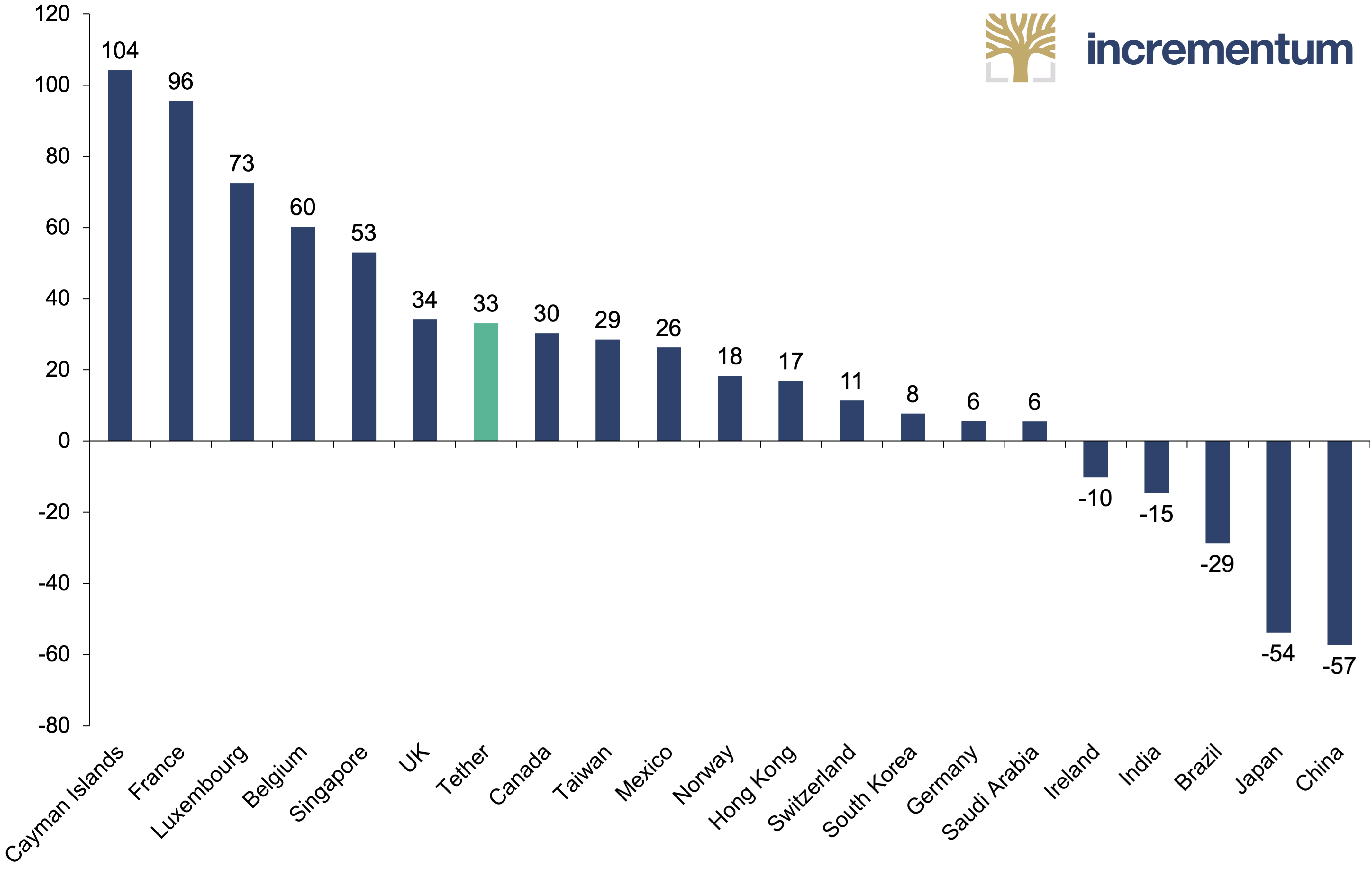

Change in US Treasury Holdings, in USD bn, 2024

Source: U.S. Department of the Treasury, Coindesk, Incrementum AG

What makes stablecoins noteworthy in the de-dollarization context is their reserve composition. Tether, the largest stablecoin issuer, with nearly USD 100bn in circulation, emerged as the seventh-largest buyer of US Treasury securities in 2024. Yet its reserves include approximately 82% in cash and cash equivalents, 3.7% in precious metals, 5.5% in Bitcoin, and the remainder in other investments.

Gold-backed stablecoins have also begun to emerge. Tether launched USD₮ in 2024, a stablecoin backed by another Tether token, XAUt, which is directly backed by – and can be redeemed for – physical gold bars. Though market share for gold-backed stablecoins remains modest compared to USD-pegged stablecoins such as USDT, as former VanEck executive Gabor Gurbacs notes: “Tether Gold is what the dollar used to be before 1971.”

History Repeats Itself? The Plaza Accord and Louvre Accord

Understanding the 1980s currency interventions

In contrast to an externally driven demand shift in the US dollar’s role as the global reserve currency, a realignment could also be embedded in a strategic repositioning of the new US administration. Chatter referring to a “Mar-a-Lago Accord” is gaining momentum as the overvalued dollar impedes Trump’s trade and economic policy. In June 2024, Scott Bessent suggested that a “grand economic reordering” could occur in the upcoming years. Before exploring this subject further, we should examine the Plaza Accord of September 22, 1985, and the Louvre Accord, adopted on February 22, 1987.[5]

The context behind the Plaza Accord

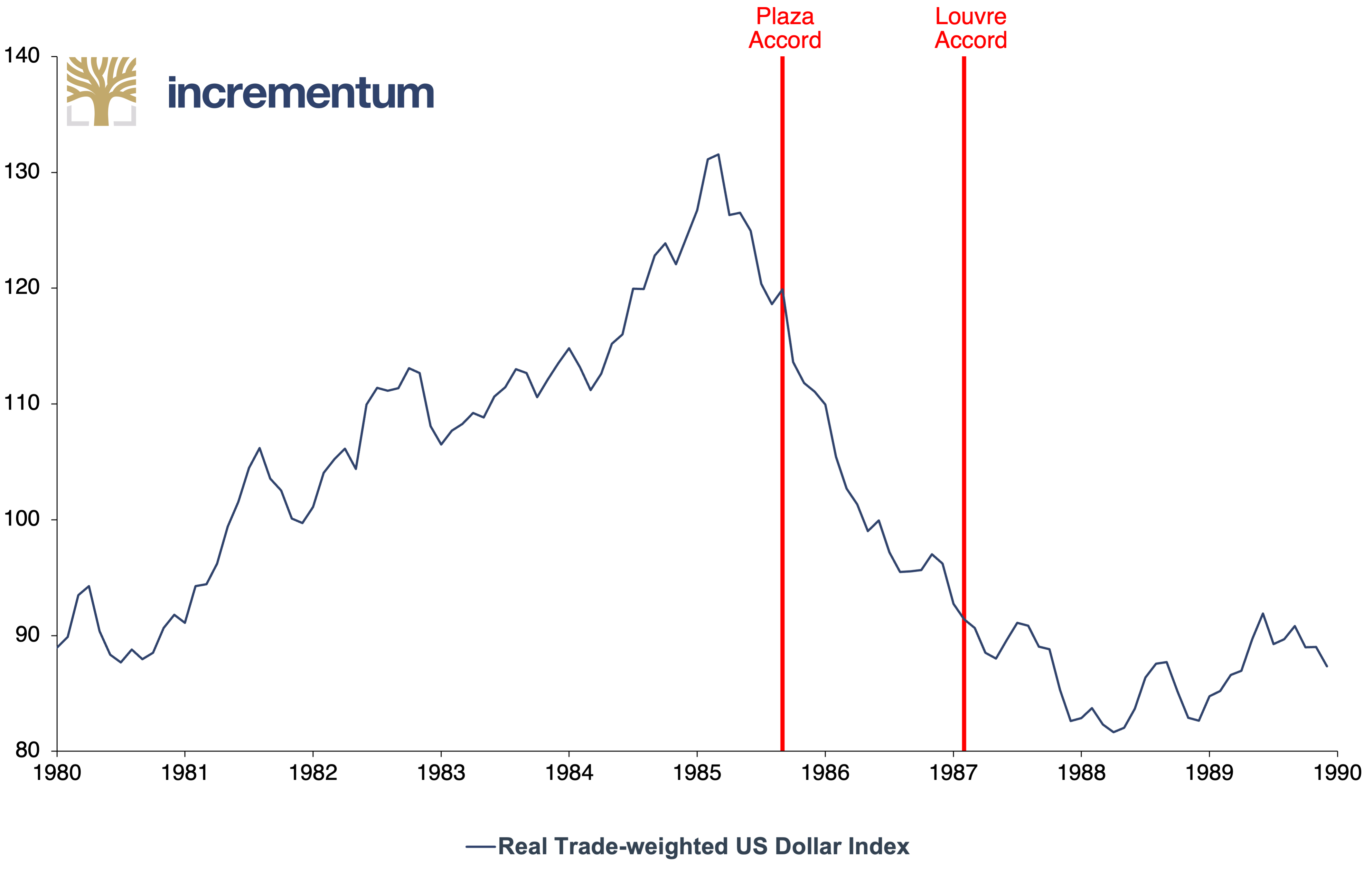

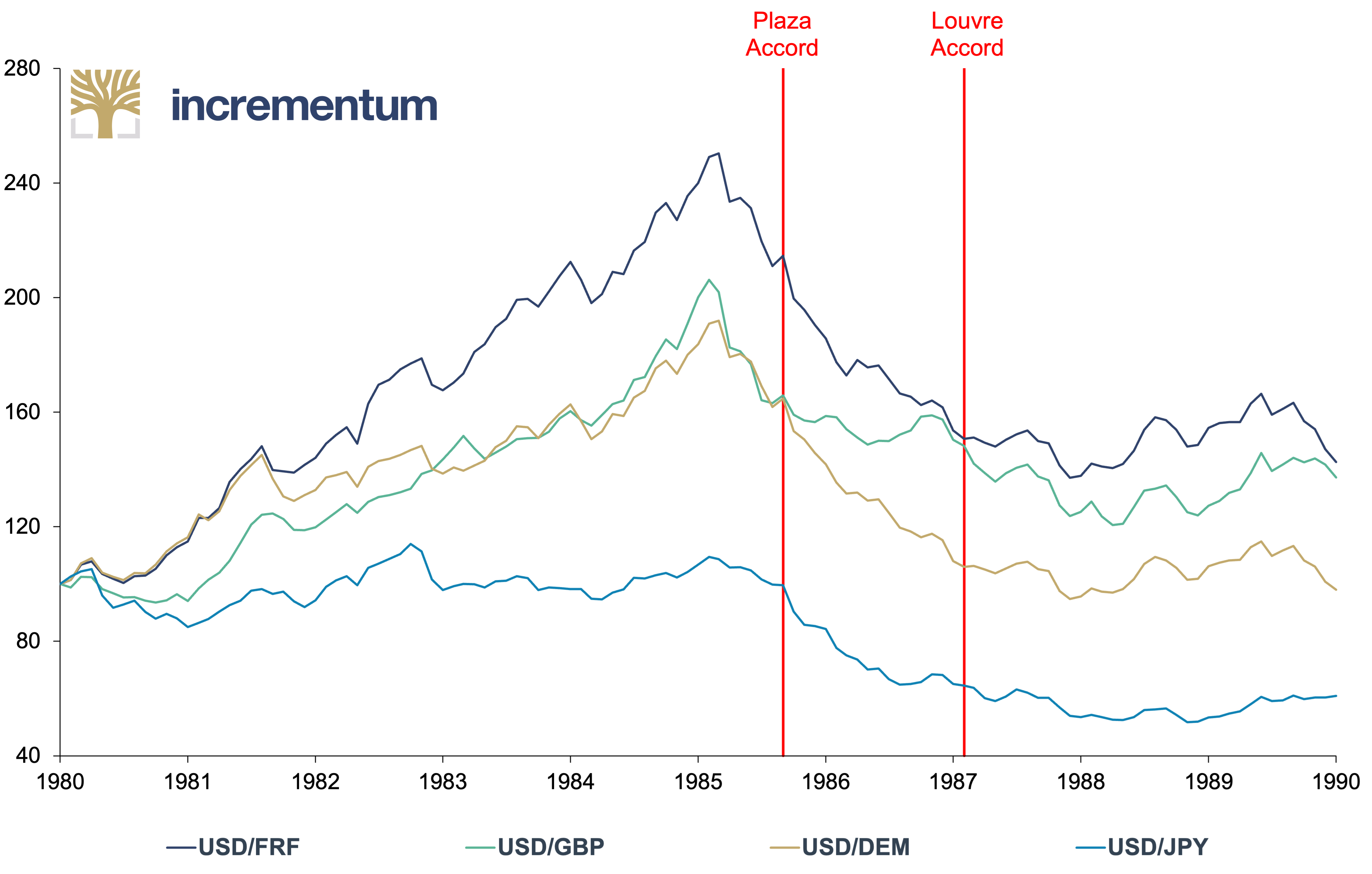

The Plaza Accord of 1985 marked a pivotal moment in post-Bretton Woods monetary relations. After Nixon decided to close the gold window in early 1971, currencies began to float freely. However, the absence of an external anchor introduced volatility and encouraged competitive devaluations. By the early 1980s, under the influence of tight US monetary policy and high real interest rates, the US dollar appreciated dramatically, by as much as 150% against the French franc and nearly 100% against the Deutschmark over five years. The real trade-weighted US Dollar Index reached a historical peak in early 1985, reflecting a significant overvaluation of the US dollar relative to the currencies of its major trading partners. This surge made US exports uncompetitive, led to a deterioration of the US current account balance, and mirrored a reverse trend in surplus nations like Germany and Japan, which saw their current account balances improve.

Real Trade-weighted US Dollar Index, 01/1980–01/1990

Source: Federal Reserve St. Louis, Incrementum AG

Outcomes and limitations of the Louvre Accord

Recognizing the unsustainable nature of these imbalances, the G5 nations (United States, Japan, Germany, France, and the United Kingdom) met at New York’s Plaza Hotel on September 22, 1985, to coordinate a strategic response. Under the leadership of US Treasury Secretary James Baker, they agreed that exchange rates should reflect underlying economic fundamentals and that a concerted devaluation of the US dollar was desirable. The Plaza Accord thus marked an unprecedented level of coordination among leading economies, engendering the zeitgeist of multilateral approaches to solving international economic stability issues. The effects were immediate: The US dollar fell sharply, and currencies like the yen and the Deutschmark surged. Yet markets had already begun adjusting months before the agreement, and the pace of depreciation continued even after the targeted range had been achieved.

USD Exchange Rate Against FRF, GBP, DEM and JPY, 01/1980 = 100, 01/1980–01/1990

Source: fxtop.com, Incrementum AG

This prompted renewed concern about disorderly currency movements, leading to the Louvre Accord in February 1987, signed by the same group of nations. The objective this time was to halt the US dollar’s excessive slide and stabilize exchange rates.

Despite commitments to align fiscal and monetary policies, currencies like the yen and pound continued to appreciate well beyond these bands. Both agreements highlighted the challenges of managing exchange rates in a world of capital mobility and sovereign economic policies. Ultimately, exchange rates are driven by fundamentals – real interest rate differentials, trade balances, investment climates, and fiscal positions. The inherent spontaneity of markets prevents them from being steered to a desired result.

Gold prices, inversely tied to the US dollar, managed a trend reversal within the challenging environment of positive real interest rates in the 1980s and rallied after each accord, reinforcing gold’s status as a hedge against dollar uncertainty and monetary instability.

Time for a Mar-a-Lago Accord?

The current situation shares striking parallels with the situation preceding the Plaza Accord: a persistently overvalued US dollar, widening trade and current account deficits, and mounting economic tensions between the US and key partners. However, unlike the coordinated efforts of allies in the 1980s, today’s emerging currency realignment will likely unfold amid heightened geopolitical tensions and a more fragmented international landscape.

Stephan Miran’s framework and the Triffin dilemma

The Trump administration has made it clear that trade and financial policy will now be guided by a single principle: America First. To dismiss this departure from cosmopolitanism as mere haphazard tribalism would be reductive. Beneath the veneer of the outdated mercantilist theory lies a calculated strategy, as outlined in “A User’s Guide to Restructuring the Global Trading System”, by one of the leading architects of Trump 2.0’s economic stance, the chairman of the Council of Economic Advisers, Stephen Miran.

Miran centers his analysis around the Triffin dilemma, which we have written about on several occasions.[6] He points out that possessing the global reserve currency can be both a blessing and a curse. While issuing the reserve currency entails the privilege to borrow extensively without significantly raising yields, as global demand for the issuer’s debt remains relentless, the strong currency causes chronic twin deficits and an unsustainable debt accumulation, gradually eroding trustworthiness and reserve status.

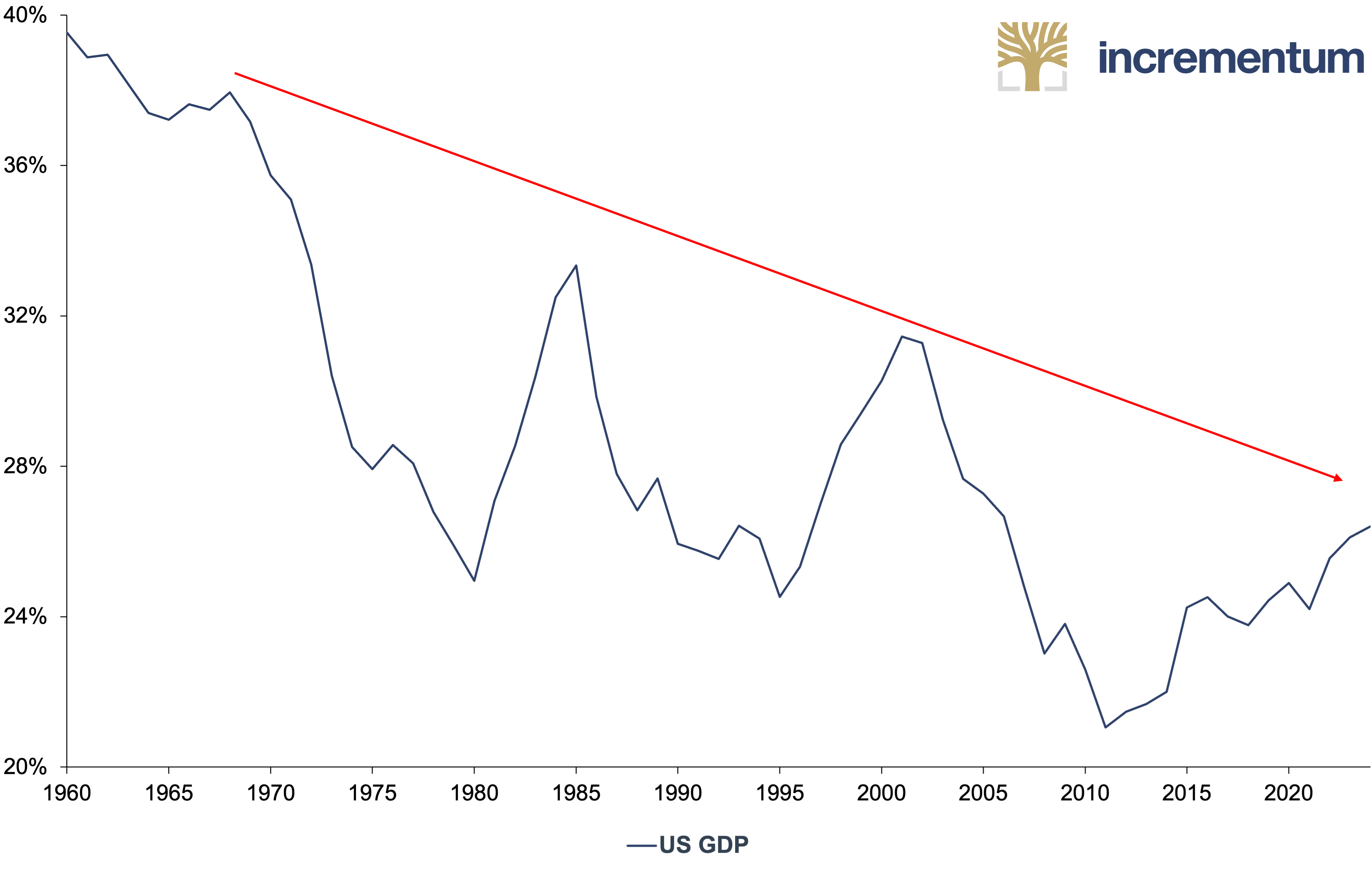

The dollar’s dual mandate, serving simultaneously as the world’s reserve asset and sustaining America’s trade balance, has become an impossible paradox. As the global economy outpaces US growth, this contradiction intensifies: Foreign demand for dollar-denominated reserves forces perpetual dollar appreciation, skewing trade flows toward imports and accelerating the erosion of domestic industrial capacity.

US GDP, as % of Global GDP, 1960–2024

Source: LSEG, Incrementum AG

As global growth eclipsed US expansion, the world’s hunger for dollar reserves created a vicious dynamic: Demand for Treasury securities and dollar-denominated assets ballooned beyond any rational alignment with America’s economic footprint. This structural imbalance exerted inexorable upward pressure on the dollar’s exchange rate – artificially cheapening imports while pricing US exports out of competitiveness. The inevitable consequence? A slow-motion unraveling of domestic productive capacity, as manufacturing atrophied under the weight of financialized distortions.

US Dollar Index, in USD, 01/2010–04/2025

Source: LSEG, Incrementum AG

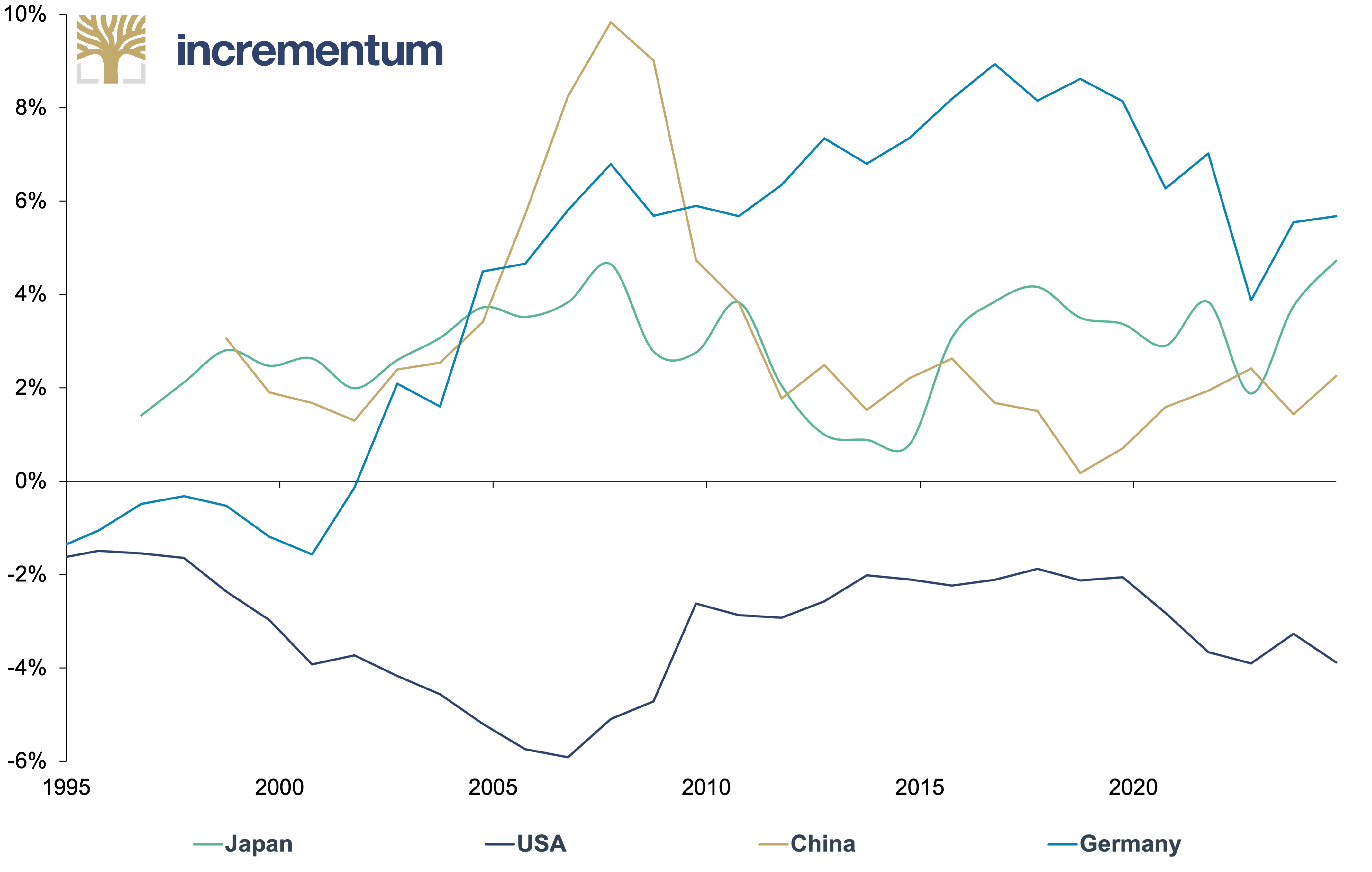

Just as thirty years ago, the US today has a significant and persistent current account deficit, while Germany, Japan, and China have substantial surpluses.

Current Account Balance, as % of GDP, 1995–2024

Source: LSEG, Incrementum AG

The “tipping point”, as described by Triffin – where unchecked twin deficits ultimately destroy the reserve currency’s hegemonic status – has yet to be reached, and the Global Financial Crisis alleviated some of the system’s inherent imbalances and temporarily stabilized the US share of global GDP. Yet, these underlying dynamics persist today, and the current administration is neither willing to risk a sudden de-dollarization tipping point nor to shoulder the burden of sustaining the system, as the US had done so far.

Current imbalances

A Mar-a-Lago Accord may offer a solution “to improve America’s position within the system without destroying the system”, as Miran stated. The attempt is to merge US trade and security policy effectively. Miran enumerates three key pillars:

- Countries under the US security umbrella would be required to purchase US government bonds to maintain the security zone as a global public good.

- These countries would be expected to exchange short-term bonds for ultra-long-term century bonds, not short-term bills.

- Noncompliance would trigger tariffs.

This approach divides the world into friends and foes, with no room for nuance. Nations must either align with the new economic and security order (gaining privileged market access) or face marginalization through aggressive tariffs, capital controls, and financial isolation. Such tactics wouldn’t merely contradict the spirit of the Plaza and Louvre Accords; they would actively dismantle their multilateral foundations.

Even with a concerted effort, it remains uncertain whether the scale of financing required for effective implementation could realistically be mobilized. Since the Plaza Accord was signed in 1985, global foreign exchange trading volumes have surged more than tenfold and now exceed USD 5trn daily. As both 1980s accords demonstrate, there is limited ability to resist the underlying fundamental forces that ultimately drive the markets.

Not everyone is a fan of Miran’s plan. Beyond the practical implementation challenges, fundamental doubts persist about whether this restructuring of global financial relations can unfold orderly. Barry Eichengreen highlights Miran’s controversial proposal for a “usage fee” on foreign holders of US Treasuries, effectively confiscating a portion of interest payments. Such a measure would violate the principle of equal treatment for investors and mark a radical departure from established financial norms. Eichengreen warns of a dangerous domino effect: Attempts to restrict foreign bond purchases could backfire, accelerating de-dollarization rather than managing it as intended.

Tools for Global Economic Restructuring

A broader strategy — anchored in swift, complementary measures rather than isolated policies — will be essential to reshape global economic relations while advancing domestic objectives. A recent piece by Michael McNair compellingly outlines how additional policy tools could execute the Miran Plan, reinforcing that trade and capital flows structurally compel the US to run massive deficits. These imbalances are driven not only by the dollar’s reserve currency status and resulting appreciation but also by the unique position of the US as the only country with unrestricted capital mobility and a financial system large enough to absorb global inflows.

McNair elaborates on reinstating the 30% foreign withholding tax, abolished in 1984, which could “kill […] two birds with one stone”, as he describes it. With estimated foreign holdings of USD 30trn in US securities, such a tax could generate approximately USD 360bn annually, or USD 3.6trn over a decade, offsetting the projected cost of extending the Trump tax cuts and discouraging excessive foreign reserve accumulation. Since most countries already impose similar taxes, the risk of retaliation or large-scale capital reallocation would remain limited.

The legal foundation for implementing this “user fee” on foreign holders of US Treasuries already exists in the International Emergency Economic Powers Act (IEEPA), which provides the President with authority over international transactions in response to foreign-origin threats to US national security, foreign policy, or the economy.

Miran’s proposal to accumulate foreign reserves as a unilateral tool for trade rebalancing could play an even more critical role. This approach reveals the strategic logic behind the Trump administration’s creation of a US Sovereign Wealth Fund (SWF). By selling dollars to purchase foreign currencies or assets, the US government could increase demand for those currencies, raising their value and reducing the trade imbalance.

McNair substantiates this possibility as follows: “The White House’s own fact sheet on the SWF explicitly states that its purpose is to pursue President Trump’s economic policies — including the pursuit of fair and balanced trade”. This direct connection to trade policy alignment strongly suggests the SWF is meant to serve as a tool for addressing trade imbalances through capital flows, as outlined in Miran’s framework.

While the Treasury’s Exchange Stabilization Fund (ESF) already provides a legal mechanism for currency operations, its limited size – under USD 40bn – necessitates creative expansion. Additionally, the merger of the SWF and the US International Development Finance Corp., which is even being considered to absorb key USAID functions that have been radically restructured by the Department of Government Efficiency (DOGE), could create a unified vehicle that scales the capability to execute financial operations to unprecedented heights.

Imagine capitalizing this consolidated fund using US Treasury gold reserves, currently valued at approximately USD 800bn. Given the DFC’s ability to operate with bank-like leverage ratios of 10 to 20 times its equity capital, such capitalization could support between USD 8.4trn and USD 16.8trn in lending and reserve accumulation capacity – without requiring a formal revaluation of Treasury’s gold, which remains recorded at USD 42.22 per ounce. This approach would provide an extraordinary tool to align trade and capital flows and implement Miran’s plan to rebalance global economic relations. McNair explains the mechanism as follows:

The US SWF operates through a different mechanism [than traditional SWF’s]: instead of recycling trade-earned dollars, it would create new dollar reserves to purchase foreign assets. However, from a balance of payments perspective, the economic impact is identical to traditional reserve accumulation or sovereign wealth funds. Whether through a central bank converting trade-earned dollars into reserves, a commodity-based SWF reinvesting oil revenues, or the US creating new dollars to purchase foreign assets, all these activities represent capital outflows that must be matched by corresponding trade flows.

Recent unprecedented activity in the physical gold market – record COMEX deliveries, rising US vault holdings, depleted London inventories, and the US shifting to net gold imports – has raised speculation that the Treasury may be quietly accumulating gold to capitalize this merged DFC/SWF. Such purchases would be legally permitted under 31 USC 5116, despite the Treasury not having bought gold since 1968.

While the consistency of this broader strategy is striking, it should not obscure the significant risks associated with its implementation. A carefully balanced combination of tools may prove essential to its success. In the following section, we will explore some of the more unconventional approaches currently under consideration.

Gold-Backed Bonds

Against debt-soaked sovereigns pushing the world toward a genuine monetary paradigm shift, Judy Shelton, a longtime advocate of gold’s monetary role, has resuscitated a proposal for gold-convertible Treasury securities. While once viewed as aspirational, this approach appears feasible as trust in hard assets rises and could reintroduce a golden anchor to the formal monetary architecture.

Historical context of gold-backed bonds

During the classical gold standard era, government bonds functioned within a monetary system where currencies maintained fixed conversions to gold. While these bonds were not typically redeemable directly in gold, they functioned within a system where currency stability was guaranteed through gold convertibility. With Britain leading this system as the world’s financial center, consolidated annuities, aka consols, represented the benchmark for sovereign debt. These bonds’ purchasing power remained stable due to the pound sterling’s gold backing.

The predictability of this arrangement allowed governments to borrow at historically low interest rates. The British government could issue perpetual consols at around 2.5–3% during much of the 19th century, while US long-term bonds typically yielded 3–4%.

The Carter bonds emergency

Fast-forward to more recent times. Between 1971 and 1981, the M2 money supply more than doubled. Monetary expansion led to stagflation – the previously “unthinkable” combination of high inflation and economic stagnation that Keynesian economists struggled to explain. Americans faced the worst of both worlds: double-digit inflation alongside rising unemployment. Consumer price inflation, which had averaged just over 2% annually in the 1960s, surged, reaching over 14% by 1980. As inflation accelerated, the US Treasury faced a genuine crisis of confidence. Foreign central banks and investors increasingly questioned the wisdom of holding dollar-denominated assets.

In this context, the Carter administration issued government bonds denominated in foreign currencies – specifically Swiss francs and German Deutsche Marks. These Carter bonds represented an admission of the dollar’s diminished standing and the Treasury’s difficulty financing deficits in domestic markets at favorable interest rates.

In 1978 and 1979, the Treasury issued almost USD 10bn in German mark- and Swiss franc-denominated securities. The world’s reserve currency issuer was effectively acknowledging it could no longer reliably finance itself in its currency – a move typically associated with banana republics, not the global financial superpower. Market participants recognized the issuance for what it was: an emergency measure reflecting severe distress in America’s financial position.

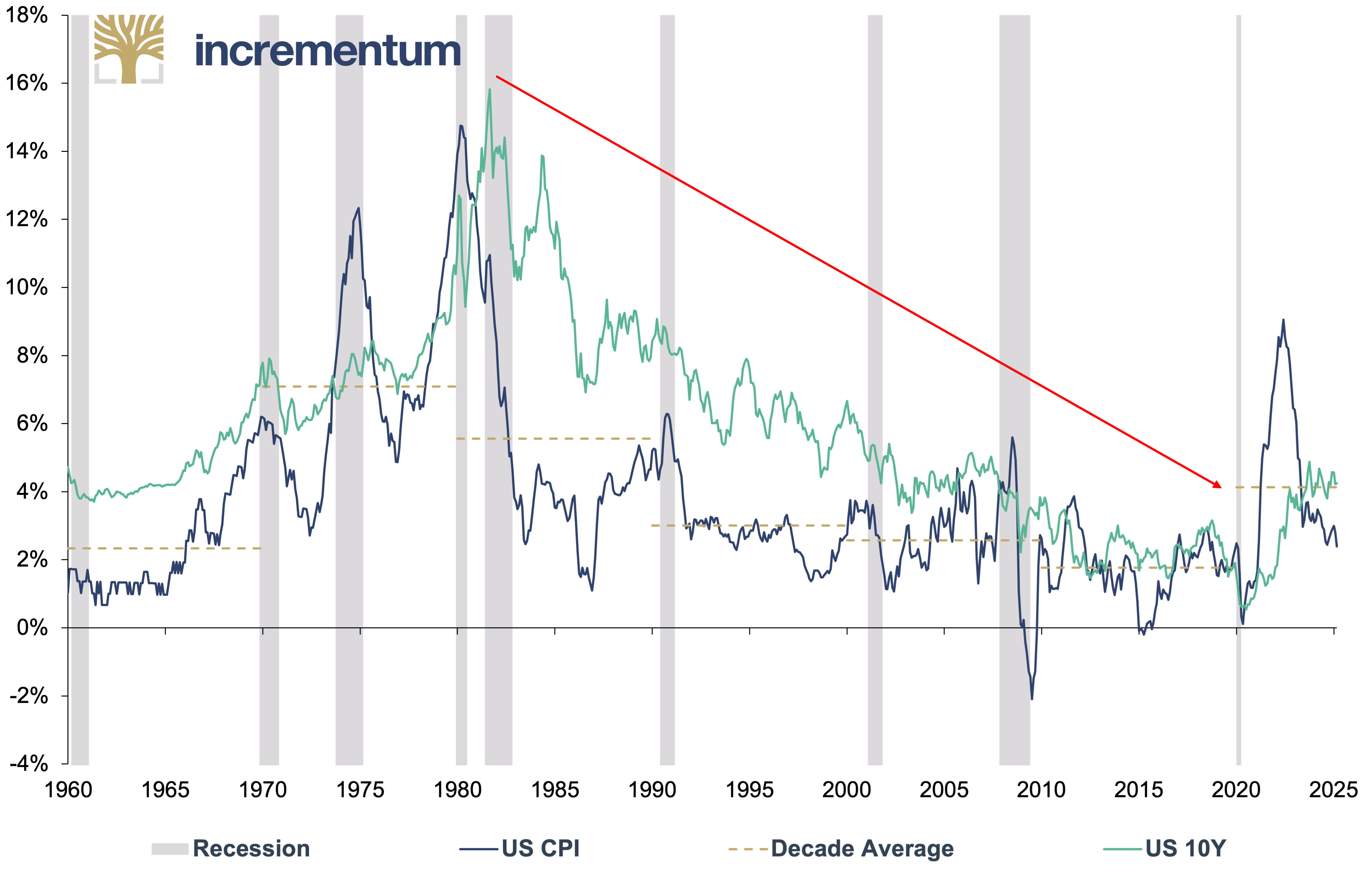

Aftermath and “The Great Moderation”

The appointment of Paul Volcker as Federal Reserve Chairman in August 1979 marked the beginning of a painful but effective restoration of monetary credibility. Volcker’s vigorous interest rate hikes – pushing the federal funds rate above 20% in 1981 – precipitated a severe recession but broke inflation’s back. Consumer price inflation fell from 13.5% in 1980 to 3.2% by 1983. As inflation expectations recalibrated, bond yields began a secular decline. The 10-year Treasury yield peaked at 15.8% in September 1981 and entered a four-decade-long bond bull market, known as The Great Moderation.

US CPI, yoy, and US 10Y, 01/1960–03/2025

Source: LSEG, Incrementum AG

Similarities to the 1970s

Recent developments in global financial markets bear resemblances to the 1970s experience of monetary uncertainty, inflation, and international questioning of dollar primacy. The credibility of central banks has suffered significant damage. Structurally, US fiscal deficits have become entrenched at levels that would have been unimaginable in previous decades. In a non-recessionary period, the 2023 federal deficit reached USD 1.7trn or 6.3% of GDP. Interest costs on federal debt in the US now surpass military spending.

Differences from the 1970s

Despite the parallels, today’s situation differs fundamentally from the 1970s in several critical aspects. Most notably, the United States now operates with debt levels previously associated with wartime emergencies. Total public debt exceeded 120% as of Q4/2024, compared to hovering in the low 30% range throughout the 1970s. This constrains monetary policy.

Moreover, the US now faces a deficit of more than 6% of GDP vs. 2–3% in 1980, a net international investment position of -79% of GDP vs. +10–15% under Reagan, and a true interest expense totaling 108% of fiscal year-to-date receipts.[7] In this context, the Trump administration is left with a singular policy path: drastic and rapid debt-to-GDP devaluation through profoundly negative real rates over a short period, a reality that both policymakers and investors appear to be navigating somewhere between denial, anger, and bargaining.

Perhaps most significantly, the international monetary system has evolved from the relatively simple bipolar Cold War structure to a multipolar arrangement with multiple currency blocs and regional financial systems. China’s emergence as an ambitious yet passive-aggressive economic superpower marks a stark departure from the 1970s. Meanwhile, innovations like central bank digital currencies, stablecoins, and Bitcoin further complicate matters by offering technological alternatives that did not exist in previous crises.

Flashback to 2017

When we interviewed Judy Shelton in the In Gold We Trust report 2017,[8] she emphasized that today’s post-1971 “non-system”, with currencies floating in a “do your own thing” style, lacks a reliable anchor. Shelton lamented that this “incoherent architecture” inevitably led to currency manipulation by big players like China, compromising the real economy in advanced nations – especially the US manufacturing base. Already in 2017, she advanced the concept of a gold-linked bond:

I was recently at a conference […] I presented a proposal for a gold-linked Treasury bond […] That would be a vitally important signal that the US intended to move toward a stable dollar. It would suggest an inclination to establish new currency arrangements – and would represent a first step toward building a new international monetary system.

Shelton stressed that it needn’t be a pure gold standard from day one; however, issuing a portion of government debt convertible into gold restricts dollar overissuance. If the government inflates away the bond’s face value, it risks losing gold from its national coffers.

In those 2017 remarks, Shelton also mentioned the possibility of a new “Bretton Woods-style” conference where the US dollar’s gold linkage might be partially restored. Little did we realize that 2025 might see the reemergence of these exact ideas, with President Trump and his cabinet pursuing a reset of the global monetary system, with Shelton being mentioned as a potential successor to Jerome Powell as Chair of the Federal Reserve.

Core elements of gold-backed bonds

Shelton’s plan is straightforward and includes two primary components: gold convertibility and revaluing the United States’ current gold reserves. Selected Treasury issuances – for example, 50-year maturities – would include an option for the bondholder to redeem in gold at a pre-specified ounce allotment per USD 1,000 face value.

The US holds 261.5 million ounces (Moz) of gold. These official reserves look small on Treasury accounts at the book price of USD 42.22/oz. However, at current market prices and an official gold hoard of 8,133 t, the revaluation profit would amount to roughly USD 800bn, effectively an underutilized national treasure. Shelton proposes using that advantage to anchor debt issuance to new gold T-bonds.

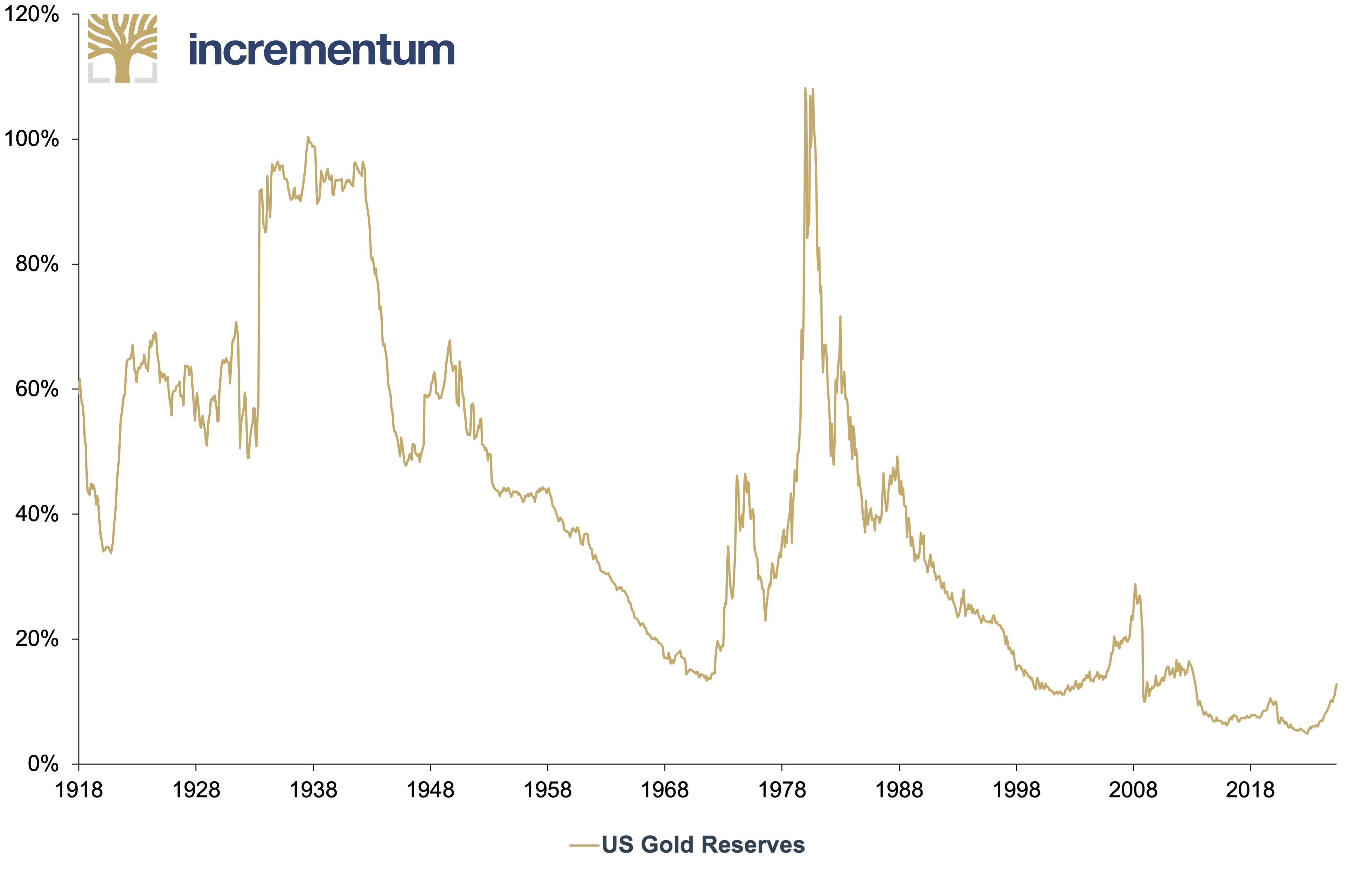

Astute commentators from Luke Gromen to Myrmikan’s Dan Oliver argue that gold remains cheap relative to the Fed’s balance sheet. As a share of the Federal Reserve’s assets, the official gold stock is at historic lows, even lower than in 1969, months before the US dollar’s final Bretton Woods crisis.

US Gold Reserves, as % of Fed Balance Sheet, 01/1918–04/2025

Source: Nick Laird, Federal Reserve St. Louis, LSEG, Incrementum AG

Further, gold-backed Treasuries would fit within the vision of the above-mentioned Mar-a-Lago Accord as an ideal vehicle for locking allies into long-duration UST holdings, since they offer a reallocation incentive that operates without coercion.

Gold-Backed bond mechanics

A modern gold-backed Treasury bond would carry a face value of, say, USD 1,000, and a built-in redemption option at maturity of, say, 50 years. Holders might choose either the nominal payout or a specified amount of gold. Because this gold redemption clause protects against inflation, the Treasury can offer a lower coupon, potentially saving billions in interest expenses. Even issuing a small fraction, e.g. 5–10%, of total debt in gold-linked form could anchor perceptions of the dollar’s stability and influence the entire yield curve.

This possibility of a gold revaluation recently gained attention after government officials publicly acknowledged that the measure is being considered. For instance, Cynthia Lummis, chair of the Senate Banking Subcommittee on Digital Assets, proposed utilizing revaluation gains to fund a Strategic Bitcoin Stockpile: “We have reserves at our 12 Federal Reserve Banks, including gold certificates that could be converted to current fair market value. They are held at their 1970s value on the books.”

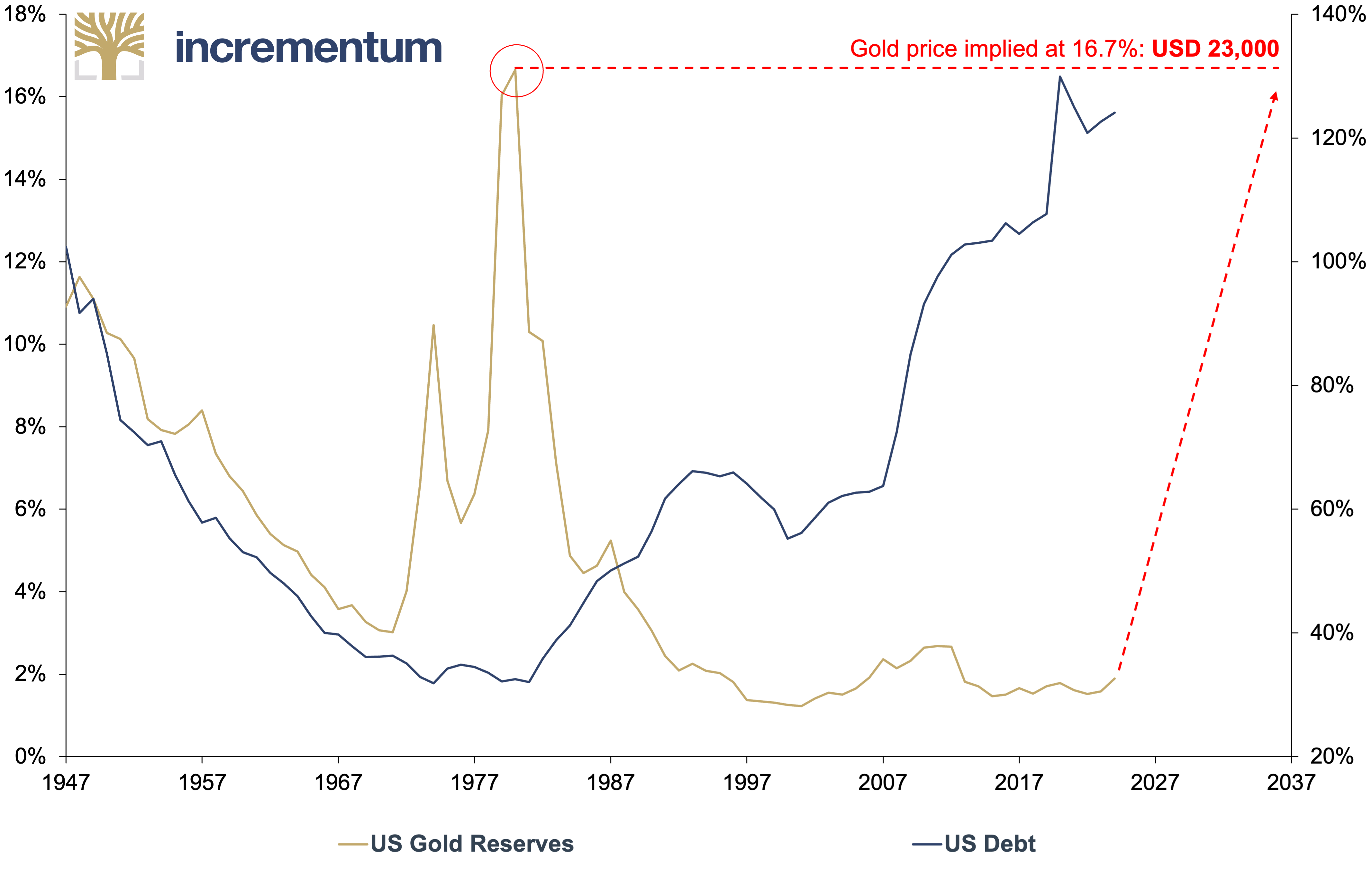

Still, as our friend Tavi Costa recently revealed, even at the mark-to-market adjustment, the US Treasury gold reserves currently account to a mere 2% of total outstanding government debt. This is one of the lowest levels in history.

US Gold Reserves (lhs), as % of US Debt, and US Debt (rhs), as % of GDP, 1947–2024

Source: Tavi Costa, Nick Laird, LSEG, Incrementum AG

Why this time might be different

A Mar-a-Lago Accord might combine trade alliances, defense commitments, and partial gold exchangeability, reminiscent of discussions around Bretton Woods III. President Trump has repeatedly stressed that US allies should share more of the burden for their defense. 50–100-year gold-backed bonds can encourage allies to hold US debt, locking in defense and trade benefits. If a handful of allies, such as Japan and EU nations, buy gold-backed bonds, a new system could emerge – not a proper gold standard, but with a gold reference at least, enhancing discipline.

“What could better symbolize America’s vision for a new Golden Age than issuing gold-backed bonds on July 4, 2026 — America’s 250th birthday — to mature 50 years later on our country’s 300th birthday?,” Shelton writes for the New York Sun. With his reelection and a strong mandate for “fair trade”, President Trump may push more aggressively for fiscal and monetary realignment.

Tariffs, currency negotiations, and gold-backed bonds form a trifecta. Tariffs provide negotiation leverage; currency deals (like a new Plaza Accord) might be hammered out in the process; and the gold bond is the hard anchor, ensuring any new arrangement is credible.

Put differently, gold-backed bonds could be a key part of a carrot-and-stick approach with regard to the US leveraging its balance sheet and military to nudge countries to roll their short-term debt into long-term bonds. The Treasury’s current debt profile skews toward short-term maturities, which creates rollover risk and makes it vulnerable to interest rate fluctuations. Without triggering market disruption, the debt maturity profile could be transformed by incentivizing allied central banks and sovereign wealth funds to exchange their short-term holdings for a long-duration gold-backed instrument.

Such a move would provide the US with breathing room while giving foreign creditors an increased sense of security in an era of monetary uncertainty. For allies concerned about dollar devaluation, these instruments provide protection. And, for the Treasury, the gold-backed bonds offer a mechanism to extend debt maturities at potentially lower interest costs than conventional long-dated bonds.

In this sense, Judy Shelton’s plan co-opts gold to reverse the decline of the West’s debt-based system. It thus represents a repeal of much of the anti-gold 20th and 21st century “wisdom” that has led to such widespread strife. What might have sounded fringe (as elites often call things they don’t have good counterarguments against) when we interviewed Shelton in 2017 feels almost inevitable in 2025.

Conclusion

Nation-states have realized that their currencies could one day play the role of a global reserve, which could undermine their objective of shaping stable and resilient economies. Indeed, everyone has understood that solving the Triffin dilemma is an ordeal too great and burdensome to pursue.

Therefore, a global economic reconfiguration is in the cards. Whether it will be characterized by the emergent BRICS+ group calling the shots or a revived American dominance leading the way remains to be seen. At any rate, we can expect that gold’s monetary role will stage a remarkable comeback, like Liverpool’s Miracle of Istanbul in 2005.

Practical considerations for investors

“We may be on the cusp of generational change in the international trade and financial systems,” Stephen Miran bluntly states. Going big and long on gold positions investors to front-run other market participants into the new world we are entering, as the dollar’s dual role as trade and reserve currency has created an unsustainable tension that must be resolved.

Any Mar-a-Lago Accord, using America’s carrot-and-stick approach to influence exchange rates, would likely trigger significant volatility in currency markets. It is foreseeable that central banks and sovereign wealth funds will accelerate their reallocation into tangible assets if the US devalues its currency and attempts to pressure foreign states into shifting into longer-duration US dollar-denominated securities, especially if those are partially backed by gold. Measures such as the recent announcement by Poland’s central bank to raise its gold reserves to 20% are likely to become the norm, particularly outside the Western world.

More specifically, geopolitical fragmentation has created a two-track opportunity in gold: Direct ownership benefits from currency debasement and systemic instability. At the same time, select mining equities will experience substantial earnings expansion as gold prices rise while input costs stabilize. Gold has now entered a rare window where it provides both portfolio defense and offense.

Beyond gold, equity sectors positioned for reshoring and domestic manufacturing should do well. President Trump’s March 2025 executive order to increase American mineral production adds gold, copper, uranium, and potash to the list of defined minerals while expediting permitting on federal lands, in addition to those already included in 30 USC. 1606(a)(3), and any other as determined by the chair of the National Energy Dominance Council (NEDC).

China’s immediate response – authorizing additional state spending for mineral production – and Canada’s call for accelerated pipeline construction and mineral extraction signal a global race for resource dominance. Tech-forward defense firms, infrastructure developers, and commodity producers will benefit from this competitive dynamic. Meanwhile, multinationals dependent on global supply chains face significant margin compression as trade barriers rise.

For bonds, the Treasury yield curve will transform. If Miran’s vision materializes, forced purchases of ultra-long century bonds by allies will create demand at the long end of the curve. At the same time, short-term rates remain elevated – potentially inverting the curve for an extended period. According to Miran, an agreement whereby US trading partners term out their reserve holdings into ultra-long-duration UST securities will:

- alleviate funding pressure on the Treasury and reduce the amount of duration it needs to sell into the market;

- improve debt sustainability by reducing the amount of debt that will need to be rolled over at higher rates as the budget deteriorates over time; and

- solidify that providing a defense umbrella and reserve assets is intertwined.

Emerging markets will either align with the Western bloc and accept unfavorable terms or accelerate de-dollarization and face short-term economic pain. This binary creates trading opportunities in EM currencies and sovereign debt, particularly for the middle powers with resource endowments that can pivot between blocs.

The path forward in a multipolar world

From the perspective of Main Street, the outlook appears challenging. Implementing such a plan could run counter to fundamental economic laws. It remains to be seen whether Trump might recognize that policies potentially undermining citizens’ purchasing power and relying heavily on centralized planning might not effectively address the imbalances within the US economy. Under these conditions, pursuing the America First agenda could risk exacerbating existing stagflationary pressures.

Ultimately, intertwined trade and security policy and higher economic uncertainty create a feedback loop benefiting gold and other hard assets. Noticeably, the forces reshaping the monetary system have already been set in motion. As our friend Matthew Piepenburg reminds us, “History is very kind to gold”. Investors who position themselves now will benefit as gold reasserts itself; the only variables are time and magnitude.

A natural US dollar adjustment?

Importantly, not all market strategists believe a formal agreement is necessary to achieve US dollar devaluation. Marko Papic contends that “American exceptionalism is the bubble” already popped by the Trump administration’s policies. He argues that the US dollar’s overvaluation stems from excessive fiscal spending rather than structural trade imbalances alone. In this view, a significant 20–30% decline in the US dollar will occur organically as global capital recognizes and adjusts to this reality, rendering elaborate new currency accords unnecessary. Papic observes: “The funny side note here, is that all of the proponents of a Mar-a-Lago Accord that you interview over the next year will tell you they were correct. But, you know, they will not be correct. There wasn’t a need for a grand bargain.” This market-driven reality is now playing out in real time: The DXY has plunged nearly 10%, breaching the 100 level for the first time since 2022. It seems that the dollar’s reckoning is arriving not through diplomacy but through the cold calculus of capital flows.

A complete implementation of the Mar-a-Lago Accord in the form discussed by Miran is unlikely. He is aware of this and recently stated in an interview that Trump focuses more on tariff policy than on the other tools in his playbook. Rather than attempting to manipulate the US dollar through clever tricks, the US government must tackle the problem at its root. Fiscal consolidation would reduce reliance on foreign savings to finance government spending. The resulting decline in the capital account surplus would correspond with a reduction in the current account deficit. However, this fundamental insight appears to be lacking – both in Miran’s thinking and, presumably, in Donald Trump’s as well.[9]

For investors, the multipolar shift underscores gold’s resurgence as a safe-haven asset, further justifying this year’s theme of The Big Long. Even if the US dollar maintains global “dominance”, as the milkshake theory plays out in real-time, gold remains the long game in a fragmenting global order.

Surely, in a paradigm where the US dollar is weaponized as a tool of American economic statecraft, what other asset is there that could substitute for the dollar as a means of exchange in international trade, as well as serve as a store of value in the balance sheets of central banks? Although there may be some suitable candidates to play this role, the best choice is that golden barbarous relic.

[1] See “Enter the Dragon: De-dollarization and the Eastern Push for Gold,” In Gold We Trust report 2024; “De-Dollarization: The Final Showdown?,” In Gold We Trust report 2023; “A New International Order Emerges,” In Gold We Trust report 2022; “De-Dollarization 2021: Europe Buys Gold, China Opens a Digital Front,” In Gold We Trust report 2021

[2] See Stöferle, Ronald (@RonStoeferle): “THREAD: A User’s Guide to Restructuring the Global Trading System” is probably the most important paper that you’ve never heard of!…”, X, March 2025

[3] See “From Wedlock to Deadlock: The East-West Divorce – Debate between Brent Johnson und Louis-Vincent Gave,” In Gold We Trust report 2024

[4] See “Enter the Dragon: De-dollarization and the Eastern Push for Gold,” In Gold We Trust report 2024; “The Rise of Eastern Gold Markets: An Impending Showdown with the West,” In Gold We Trust report 2023; “A New International Order Emerges,” In Gold We Trust report 2022

[5] See “History Does (Not) Repeat Itself – Plaza Accord 2.0?,” In Gold We Trust report 2019

[6] See “Inflation and Investment,” In Gold We Trust report 2016

[7] Gromen, Luke: “Bessent, Powell hint at ‘Not-QE QE’ as Trump Administration policy contradictions mount”, FFTT, March 25, 2025

[8] “The De-Dollarization: Good-bye Dollar, Hello Gold?,” In Gold We Trust report 2017

[9] See Duarte, Pablo: „Mar-a-Lago-Abkommen: viel Lärm um nichts?“ (“Mar-a-Lago-Accord: Much Ado about Nothing?“), Flossbach von Storch, March, 28 2025