Bitcoin: Bull Market in Adoption, Bear Market in Price

“If you just did an overlay of the Nasdaq and the cryptocurrency markets, they are unbelievably correlated for right now, so I think that’s creating a lot of churn and pain in the markets. While that’s happening, billions of dollars are going into Web3.”

Anthony Scaramucci

Key Takeaways

- Although Bitcoin is in a veritable bear market again right now, there are remarkable happenings and progress in terms of adoption.

- Several nation states have declared Bitcoin as their official currency within the past 12 months.

- The stock-to-flow model (S2F model) can explain the price development of Bitcoin remarkably well historically. In the current cycle, the price of Bitcoin is below the range assumed by the model.

- Due to the wide range of the S2F model, it can serve as a guide regarding the halving cycle, but not as the basis of an automated trading strategy.

- A U-turn back to a loose monetary policy could make for a delayed high in the price of Bitcoin within the next 24 months.

Since 2016 – when the price of BTC was trading at around USD 500 – we have been writing an annual chapter on the topic of Bitcoin and cryptocurrencies in the In Gold We Trust report. This year, too, we want to stick to this tradition. Not least because the topic has gained in importance for us, as we now manage two funds that combine precious metals and cryptocurrencies.

Bitcoin vs. Gold

In past years we have dealt with this much-discussed topic in detail several times. We would like to refer interested readers to the chapters “Gold and Bitcoin: Stronger Together?” [1] and “In Bitcoin We Trust?”.[2]

On a philosophical and to some extent on a practical level, gold and Bitcoin are similar because they

- cannot be inflated by central banks,

- do not represent the debt of another party (no counterparty risk),

- are easily transferable and

- represent values outside the fiat money system.

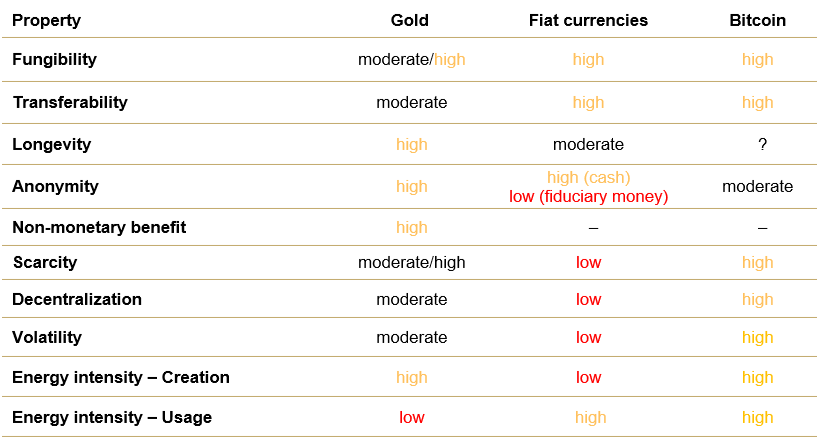

In our view, both asset classes have advantages and disadvantages. Due to their different characteristics, they are not in direct competition with each other but rather complement each other. Gold and Bitcoin are friends, not foes.[3] In the following table we summarize the most important differences between gold, fiat currencies and Bitcoin, knowing full well that one or another nuance can be discussed extensively and passionately here.

Source: Incrementum AG

Probably the most important argument for Bitcoin as a long-term store of value is the non-inflatability of its supply. In this fundamental characteristic, Bitcoin and gold are particularly similar. In both cases, the future development of the money supply is highly predictable. In contrast, fiat currencies are constantly inflated under normal circumstances; in times of crisis, inflation often increases by leaps and bounds.

Bitcoin Stock (lhs), in Coins, and Gold Stock (rhs), in Tonnes, 01/2010-01/2030

Source: blockchain.com, World Gold Council, Incrementum AG

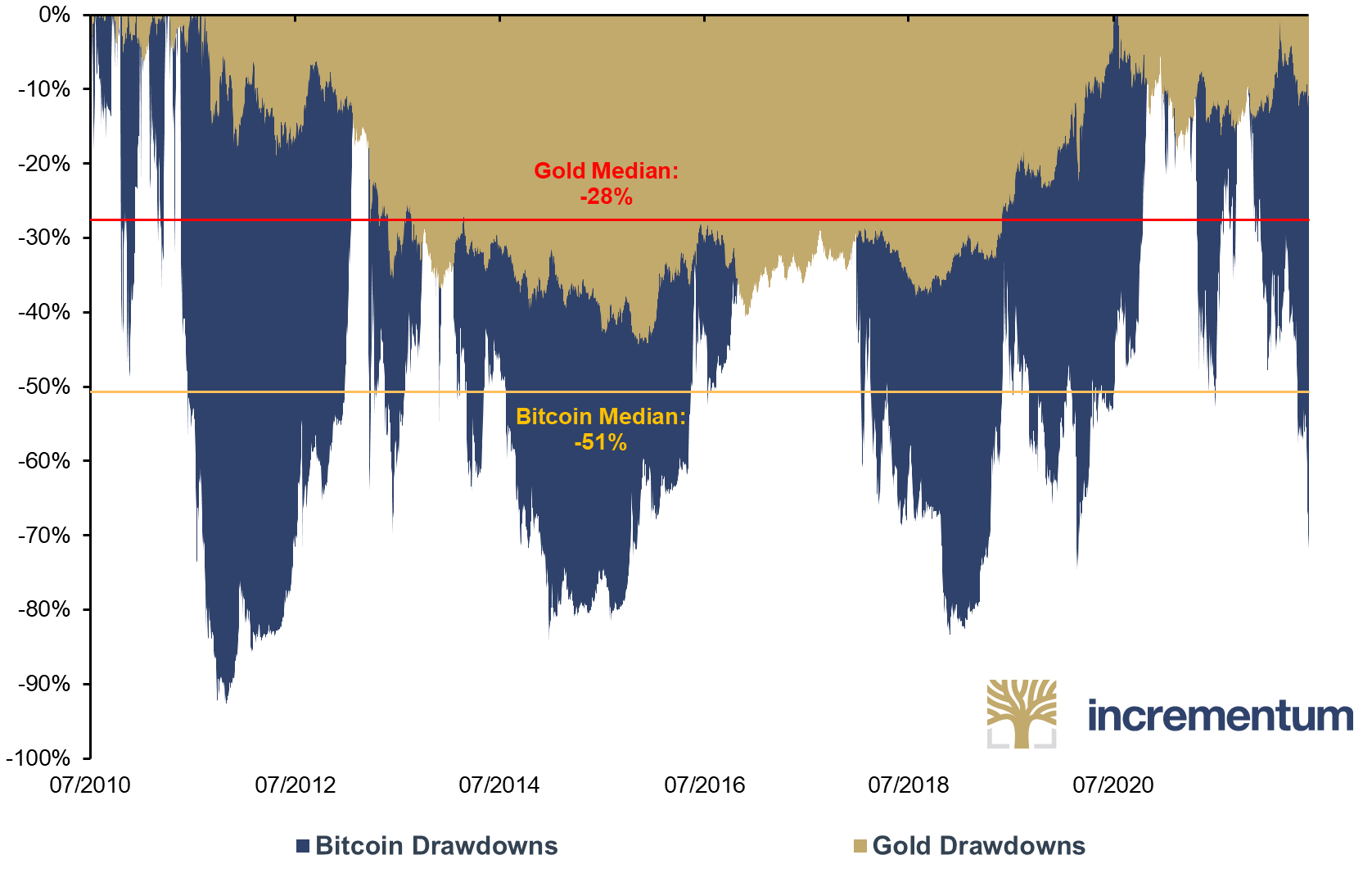

Especially in terms of volatility, gold and Bitcoin have fundamentally different characteristics. Gold is known to have significantly lower volatility than Bitcoin. Measured in annual standard deviation, gold’s volatility is around 15-20% p.a., while Bitcoin’s is between 60 and 100%. Bitcoin holders are currently feeling the high volatility of Bitcoin again on the markets. Historically, the drawdowns from the all-time highs have been over 80% several times.

Bitcoin and Gold Drawdowns from ATH, 07/2010-05/2022

Source: Glassnode, Reuters Eikon, Incrementum AG

Price versus Adoption

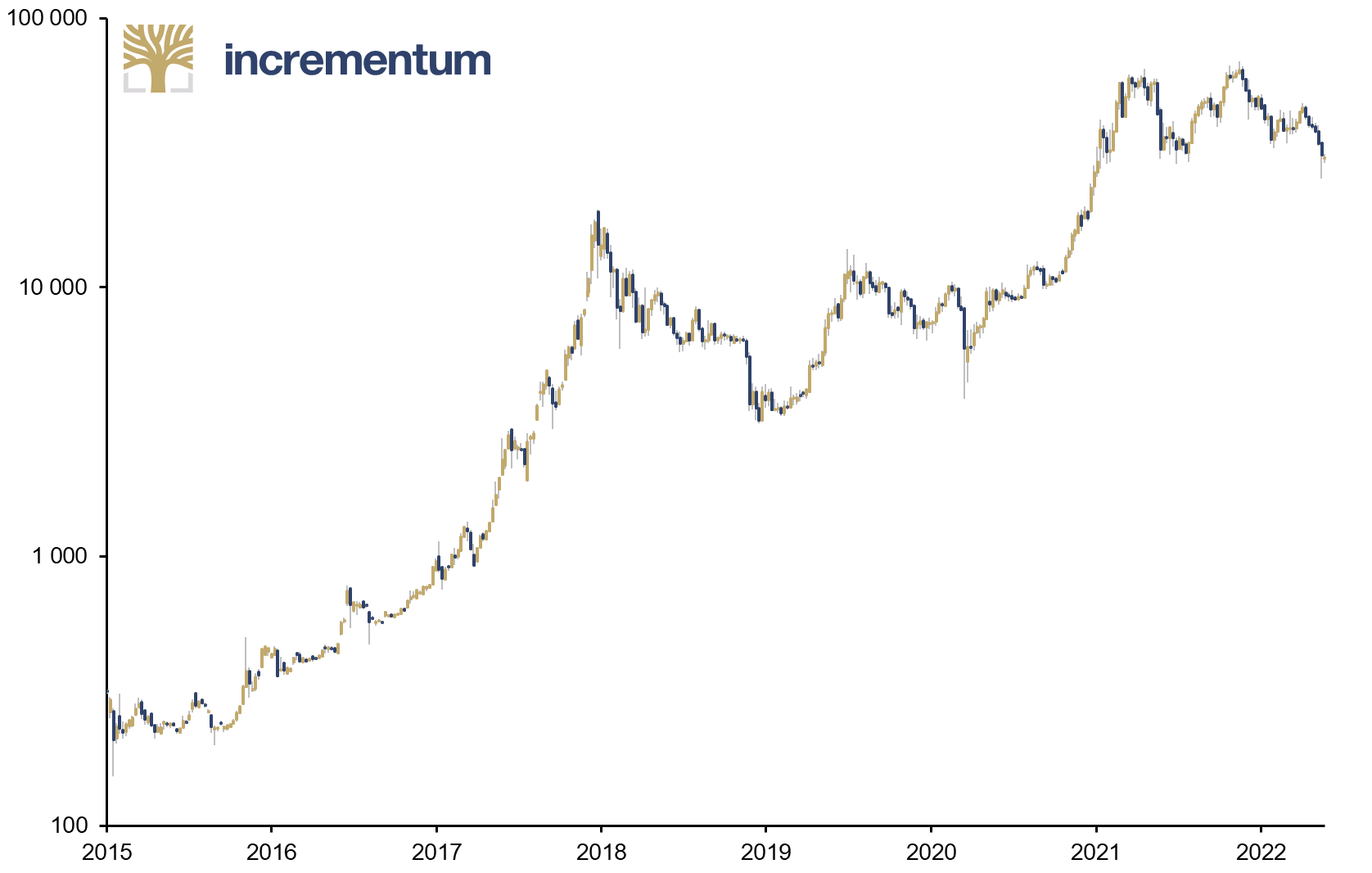

After hitting a new all-time high in November 2021, Bitcoin is now clearly back in a bear market. On the logarithmic scale below, you can see the phenomenal long-term rise. Nevertheless, one should not be fooled by the optics into taking the short-term setbacks seriously.

Bitcoin (log), in USD, 01/2015-05/2022

Source: Reuters Eikon, Incrementum AG

Although Bitcoin is currently in a veritable bear market again, there are remarkable events and progress to report in terms of adoption. Below is a small selection of significant events:

- China introduces a mining ban; the lost hash rate is made up in a few months by miners in other countries.

- Lightning Network will be integrated into Bitcoin’s blockchain.

- Bitcoin hits a new all-time high of USD 69,000 in November 2021, but halves in the following 6 months.

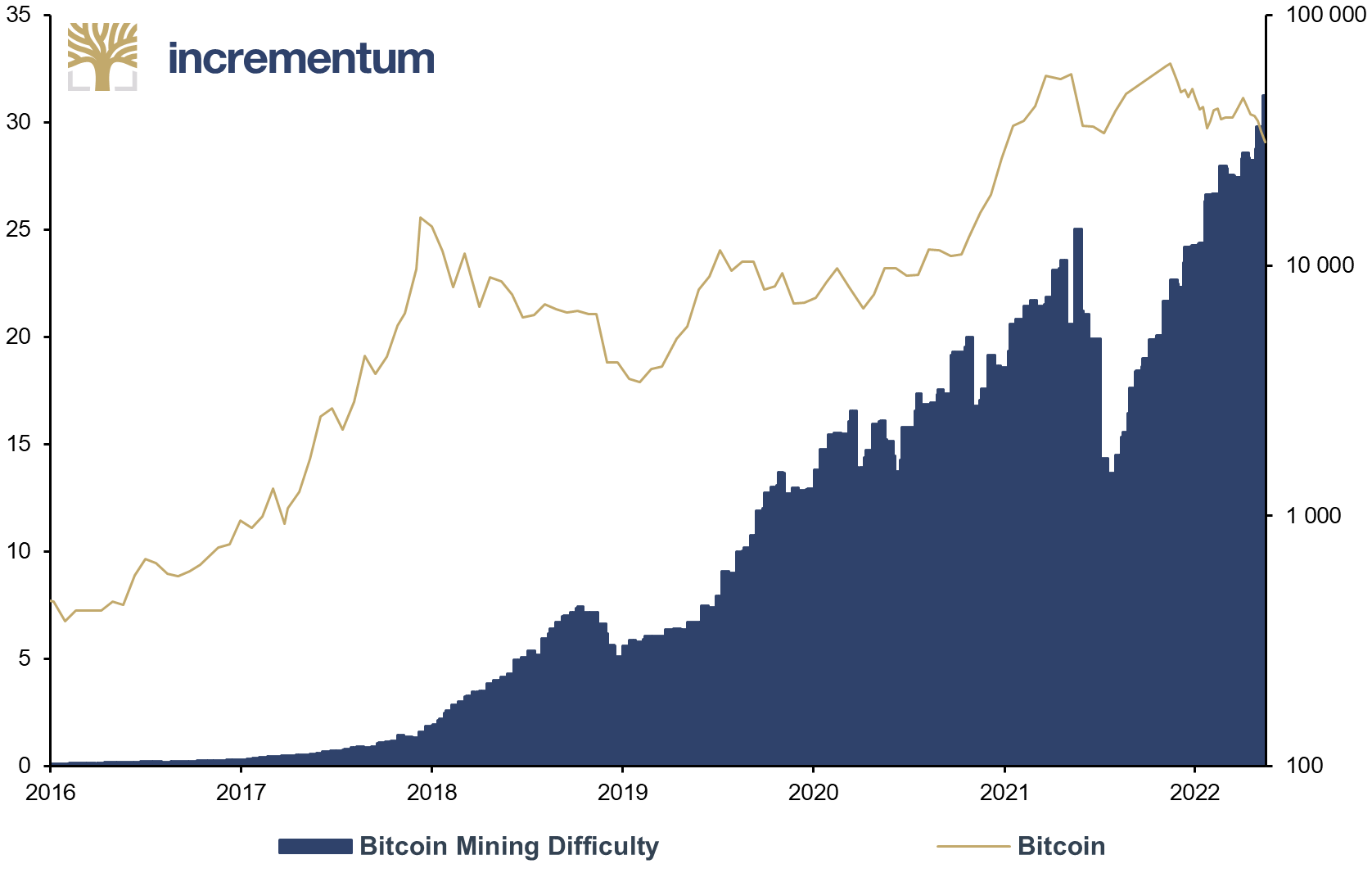

The resilience of the network was once again impressively demonstrated last year. Following the Chinese government’s legal ban on Bitcoin mining, Chinese miners went offline within a few weeks, and some moved to new jurisdictions.

Bitcoin Mining Difficulty (lhs), in trn, and Bitcoin (log, rhs), in USD, 01/2016-05/2022

Source: blockchain.com, Reuters Eikon, Incrementum AG

In the meantime, Bitcoin adoption continues to advance. Around the globe, numerous notable government initiatives have been implemented that are gradually further integrating Bitcoin into highly diverse economies. To name just a few:

- El Salvador declares Bitcoin as official currency in September 2021.

- The Central African Republic introduces Bitcoin as official currency in May 2022.

- Madeira, an autonomous region of Portugal, announced that no taxes will be levied on profits from the purchase and sale of Bitcoin, and that Bitcoin can be freely used as a means of payment.

Although these countries are comparatively small, it is worth noting that just 18 months ago it was inconceivable to anyone that a nation state would adopt Bitcoin as legal tender. Given the current developments on a global level, we would not be surprised if more states follow suit and use Bitcoin as a reserve currency in the future.

But there has also been notable progress at the institutional level. Fidelity Investments, the largest provider of retirement plans (401(k)) in the US, announced in April 2022 that they will allow investors to invest up to 20% of their 401(k) portfolios in Bitcoin. This is the latest in a string of news reports about institutional investor adoption of cryptocurrencies.

Bitcoin-owning companies include Microstrategy, Tesla, Square, Block, and a number of publicly traded crypto and bitcoin-specific companies. A recent report by VanEck mentions that so far this year, nearly 160 separate 13F filings from various hedge funds have referenced their Bitcoin holdings.

S-Curve Adoption

Breakthrough technologies almost always follow an S-curve adoption pattern. This pattern reflects the cumulative rate at which a population adopts a new technology. This pattern has been observed with the introduction of railroads, electricity, radio, telephones, television, fax machines, microwaves, computers, the Internet, cell phones, and so on. The S-curve demonstrates that the time it takes for a new breakthrough technology to achieve 10% penetration is broadly equivalent to that required to increase penetration from 10% to 90%.

Bitcoin was invented in 2009. In 2019, 10% of US households owned Bitcoin. Today, according to the US government, the figure is already 25%. If we look at these numbers using the S-curve model, Bitcoin distribution would reach 90% around 2029. So far, this matches well with the expected numbers in the S-curve model. This means that we are currently in year 3 of 10, where Bitcoin should rise from 10% to 90% adoption according to this model.

Taking a longer-term view of Bitcoin, it appears that we are still in the early stages of the adoption curve and that there is much more potential. It is worth noting that these numbers are for the US, and the US is way ahead of the rest of the world in Bitcoin adoption. Global adoption numbers are extremely difficult to measure, but are estimated to be between 1% and 2% in 2022.

Source: Off the Chain Capital

If adoption continues to follow the S-curve model and takes into account the limited supply of Bitcoin, price is the only other variable that could move to meet increasing demand.

Bitcoin, the Interest Rate Turnaround, and the S2F Model

Adoption and resilience are advancing, but prices are not. As we have already discussed in detail in this report, we have had to record continuously rising inflation rates worldwide over the past 12-18 months. The turnaround in US monetary policy that has been heralded is now having far-reaching implications for financial markets. We therefore want to look at the extent to which this turnaround may also affect Bitcoin.

Bitcoin’s integration into the financial markets

Until now, Bitcoin has led “a life of its own” to a certain extent and has been only peripherally affected by general macro events. As it adapts and begins to be integrated into institutional portfolios, Bitcoin will be increasingly exposed to the vagaries of the financial markets. At its peak, Bitcoin’s market capitalization significantly exceeded USD 1tr by a wide margin; currently it is around USD 600bn. The debate on whether Bitcoin should be valued as an inflation-hedging asset has now fully flared up. We have already expressed some thoughts on this in the chapter “Stagflation 2.0” in this In Gold We Trust report.

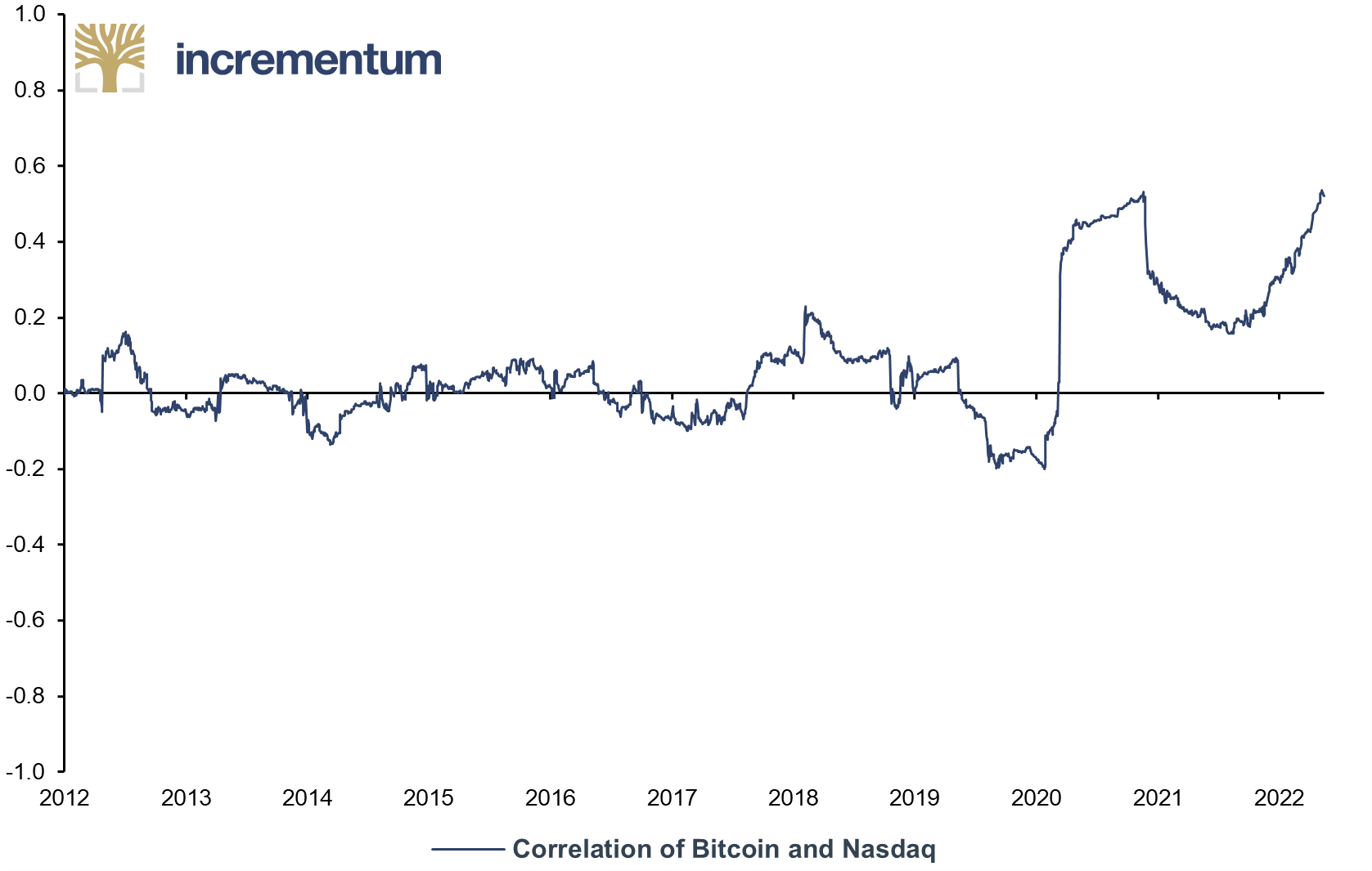

Recently, there has been increasing talk of Bitcoin behaving like a risk asset. This thesis is supported by its increased correlation to stocks, especially to the US technology stock index, Nasdaq. According to Kaiko Research, the 30-day rolling correlation between Bitcoin and the Nasdaq rose to 0.8 on May 9, an all-time high.

Rolling 180d Correlation of Bitcoin and Nasdaq, 01/2012-05/2022

Source: blockchain.com, Reuters Eikon, Incrementum AG

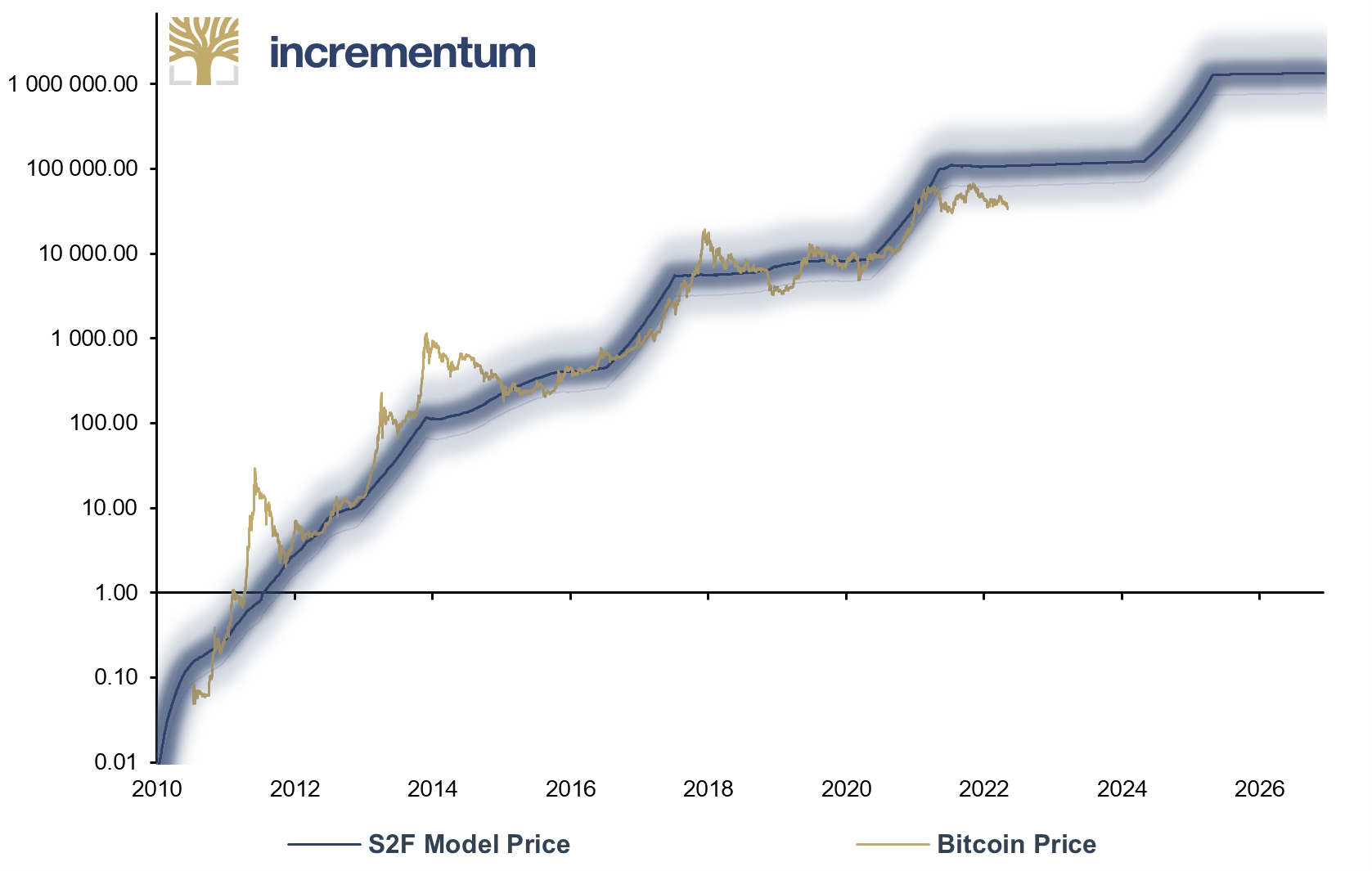

Even though the correlation to technology stocks is currently quite high, it should be noted that correlations tend not to be stable. In the past, Plan B’s stock-to-flow model (S2F model)76F has been able to explain the price trend over longer periods much better than individual stock indices do. We previously presented this model in the In Gold We Trust report 2020[4] and discussed it in detail in a In Gold We Trust classic[5], among others. We would like to take another close look at the S2F model at this point.

The key premise of the S2F model is that the halving of mining rewards every four years (halving) provided for in the Bitcoin protocol has a significant impact on price development. Technically, halving increases Bitcoin’s stock-to-flow ratio, because fewer new bitcoins enter circulation after each halving due to lower mining returns. The SF model leverages the unique feature of the Bitcoin protocol, which transparently and traceably reveals the past and future supply curve, to forecast Bitcoin’s price evolution based on its historical and future stock-to-flow values. The model regresses the log price development of Bitcoin with the prevailing stock-to-flow ratio.

S2F Model Price, and Bitcoin Price, in USD, 01/2010-12/2026

Source: Plan B @100trillionUSD, Glassnode, Reuters Eikon, Incrementum AG

Remarkably, the Bitcoin price has followed the path of the predicted S2F model quite precisely since its first release in March 2019. It must be noted, however, that in relative terms the model forgives a rather high fluctuation range of the price of Bitcoin due to the regression with logarithmic prices. Therefore, its use is probably only suitable to a limited extent, but not, for example, to build an automated trading strategy on it.

In the current cycle, there was a significant price increase last fall, which was also predicted by the SF model, but it remained below expectations. For completeness, it should be noted that there are now several variants of the model. According to the original variant, the price of Bitcoin should average USD 55,000 during this halving cycle (May 2020–May 2024). A later variant, which was frequently cited last year, calculated a significantly higher average price of USD 100,000.

The following questions now arise:

- Will the average price of Bitcoin in this cycle be lower than predicted by the two model variants?

- Will there be a delayed increase in the price of Bitcoin during this cycle, or will the average price of one of the model variants still be reached or even surpassed?

- Has the forecasting quality of the S2F model decreased or has it even become obsolete?

Due in part to too-bullish expectations, many analysts, investors and market observers have asked themselves in recent months whether the current Bitcoin halving cycle is already over. We have also thought about this and published our first Bitcoin chartbook at the end of 2021. In the following, we would like to take a closer look at some key elements in connection with this topic.

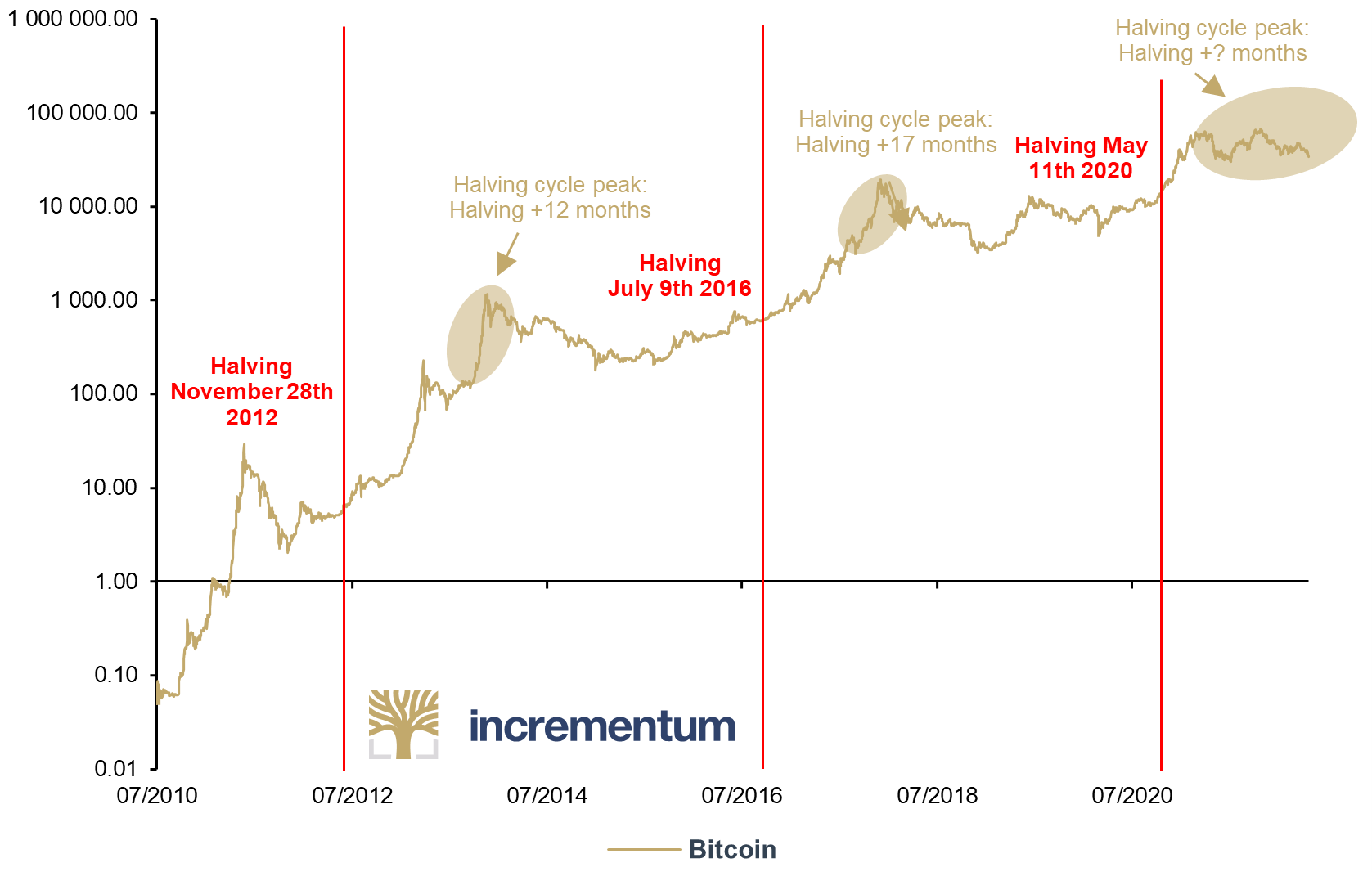

The next chart suggests that the price of Bitcoin formed peaks 12 and 17 months after halving in the last two cycles. The last halving was now 24 months ago, and we wonder whether the cycle already peaked in November 2021 or whether another all-time high could still be in store in this cycle.

Bitcoin (log), in USD, 07/2010-05/2022

Source: blockchain.com, Reuters Eikon, Incrementum AG

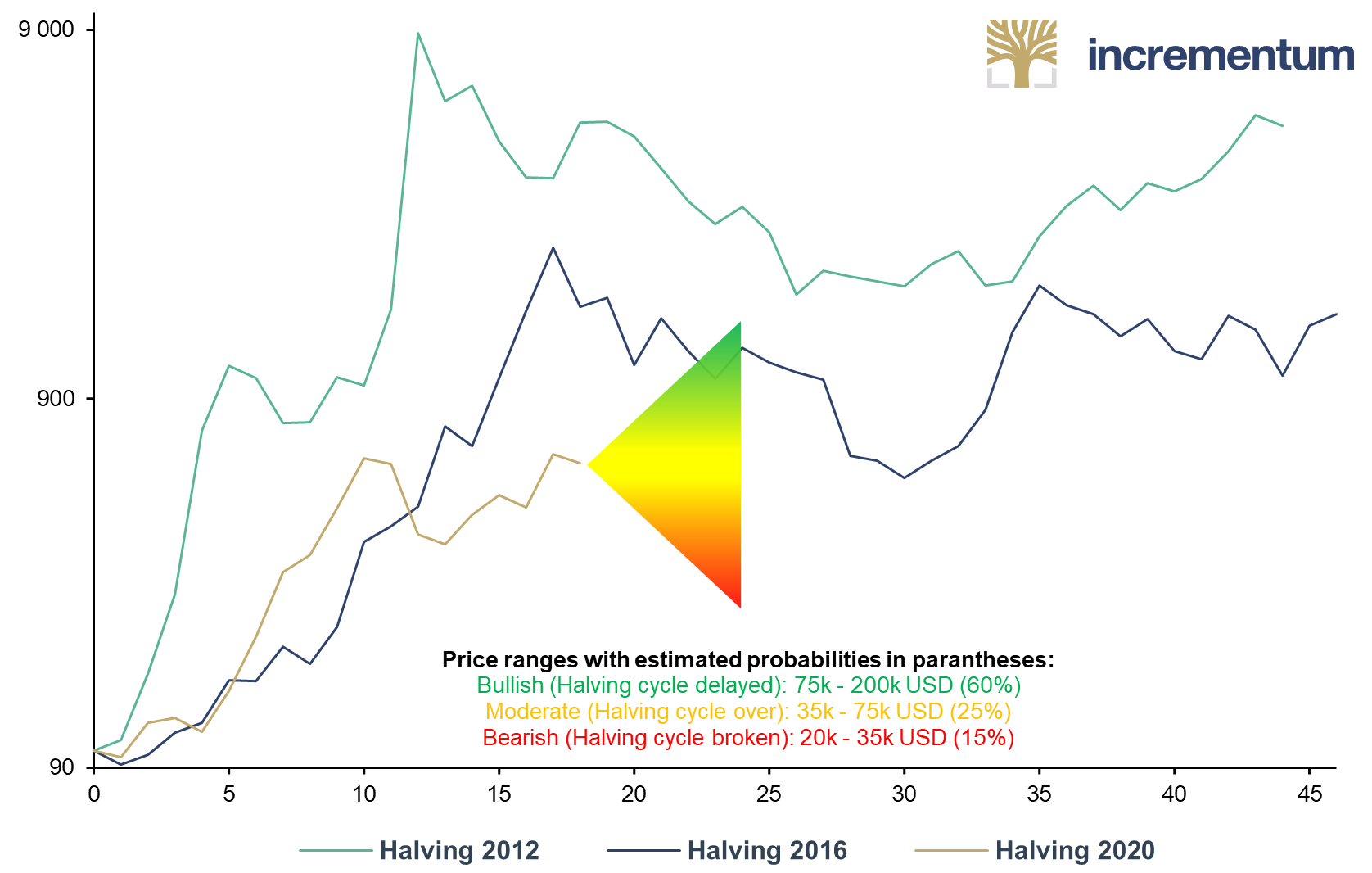

In December, we formulated three scenarios for the current halving cycle in our Bitcoin chartbook. In our opinion, the most likely scenario (60%) was a delayed peak in this bisection cycle. However, we assigned a probability of 40% to the possibility that this bisection cycle is over, or that the model is obsolete.

Bitcoin Performance by Halving (Halving Month = 100, log)

Source: Reuters Eikon, coinmarketcap.com, Incrementum AG

Given Bitcoin’s increasing adoption, higher market capitalization, and the entry of institutional investors into the crypto market, it seems plausible that Bitcoin is becoming increasingly sensitive to macroeconomic trends. For example, it can be noted that the current rise in bond yields is having a strong negative impact on the entire risk asset sector – including cryptocurrencies. Therefore, it cannot be ruled out that these will face further headwinds in the coming months should bond yields continue to rise and the risk-off movement persist.

In our view, current developments on the bond markets could cause a further delay in this bisection cycle. Nevertheless, we want to take account of the advanced stage of the cycle and adjust our December 2021 forecast. From today’s perspective, it has probably become somewhat less likely that we will still see a new all-time high in this halving cycle. Nevertheless, based on macroeconomic conditions, we do consider it possible that there will be a delayed high in this cycle. We put the probability of Bitcoin reaching a new all-time high in the remaining 24 months of this cycle at around 40%. This scenario could manifest itself if the currently priced-in monetary tightening does not materialize.

Conclusion

It seems plausible that due to the increasing adoption of Bitcoin by institutional investors, its sensitivity to macroeconomic events has increased. Due to this, a delay of the high point in the current halving cycle seems possible. Because of the high bandwidth of the S2F model, it can be used as a guide regarding the halving cycle, but not as a basis for an automated trading strategy.

US monetary policy is currently in a phase of transition from loose to tighter. In view of high inflation and recent hawkish communications, markets are expecting a significant change in interest rate policy. In our view, it is quite likely that rising volatilities in the markets will force central banks to revert to a loose monetary policy again.

Therefore, we think that interesting entry opportunities in Bitcoin and other cryptocurrencies could arise in the wake of the current monetary policy-induced turmoil.

[1] “Gold and Bitcoin: Stronger Together?,” In Gold We Trust report 2019

[2] “In Bitcoin We Trust?,” In Gold We Trust report 2017

[3] “Crypto: Friend or Foe?,” In Gold We Trust report 2018

[4] “The Plan B Model: The Holy Grail of Bitcoin Valuation?,” In Gold We Trust report 2020

[5] “The stock-to-flow ratio as the most significant reason for gold’s monetary importance,” In Gold We Trust classic