The Rise of Eastern Gold Markets: An Impending Showdown with the West

“Who is the best

Who holds the aces

The East or the West

This is the crap our children are learning

But oh, oh, oh, the tide is turning.”

“The Tide is Turning”, Roger Waters

- Gold flows to where it is most appreciated and to regions with buoyant economic growth and rising income levels.

- India and China are importing an increasingly large proportion of world gold production, and hoarding huge quantities of gold in private ownership.

- Asia already has sophisticated physical gold trading infrastructure led by the Shanghai Gold Exchange (SGE), and a new Moscow World Standard for gold trading has been proposed to threaten the duopoly of LBMA/COMEX.

- Central banks as a group have been net buyers of gold every year since 2009, and practically all of these central banks are in Asia or the non-West. In 2022, central banks bought the most gold on record, 1,136 tonnes.

- Pushed by rising geopolitical risk, the nonaligned countries are becoming aligned: Tectonic shifts are occurring across the global geopolitical landscape, with countries moving at record pace to embrace alliances with organizations such as the BRICS and the SCO.

- The countries accumulating gold through their central banks are the same countries that are lining up to join these organizations, in preparation for a possible new monetary system connected to gold.

Introduction

Over the last quarter of a century, there has been a huge flow of physical gold from West to East, and in parallel a huge growth in the importance of Asian gold markets.

Theory would suggest that rapid economic growth, rising income levels, and government encouragement of gold ownership across the region are behind this relentless growth in gold demand in Asia. And no doubt this is true. But gold has also flowed to Asia because that’s where it is most appreciated.

When in 1998 Robert Mundell clarified Gresham’s Law by saying that “cheap money drives out dear, if they exchange for the same price”, he could have been talking about the flow of gold from West to East, of unbacked fiat money driving gold out of the West and into the East, and of this gold flowing to where it’s most appreciated, and to where importantly, it is hoarded and treasured.

In the past, gold was universally accepted as both a currency and as a store of value because gold was correctly recognized as being both sound money and having intrinsic value. However, with the great fiat experiments of the world’s central banks especially since the latter half of the twentieth century, fiat currencies – unlimited and unbacked by any physical commodity – emerged in ever increasing quantities to perform the function of currency, and in the process sought to push out and replace gold.

While this new paradigm was readily accepted in most parts of the West, it has not been so thoroughly embraced by the cultures of Asia and the Middle East. Asian and Middle Eastern cultures have a long-standing cultural affinity for gold, and they view gold as a symbol of wealth, as an inflation hedge, and as a safe haven asset. So when these non-Western countries experienced a rise in prosperity over the last number of decades due to rapid economic growth and rising incomes, this was naturally reflected in a desire to use this new purchasing power to accumulate real money in the form of physical gold.

Our friends at Kopernik Global Investors recently highlighted that as much as the world’s economy was driven by the “developed” countries in the distant past, it is clearly being driven now by emerging markets. Collectively, emerging markets account for:

- 87% of the global population

- 76% of the total land area

- 44% of global GDP, up from less than 20% in 2000

- 76% of global GDP growth over the past 20 years

- 76% of global foreign exchange reserves

Many in the Western world still think that the center of the gold world is in the West, particularly on the COMEX gold futures exchange in New York and in LBMA OTC trading in London. But the reality on the ground speaks of a different set of markets, of real physical gold markets all across the non-Western world, including Asia and other emerging markets, where thousands of tonnes of physical gold imports flow in each year to satisfy those regions’ insatiable demand for gold. It is these gold markets and their participants which are becoming increasingly important to the global gold markets, so it is vital to understand these markets’ supply and demand mechanics.

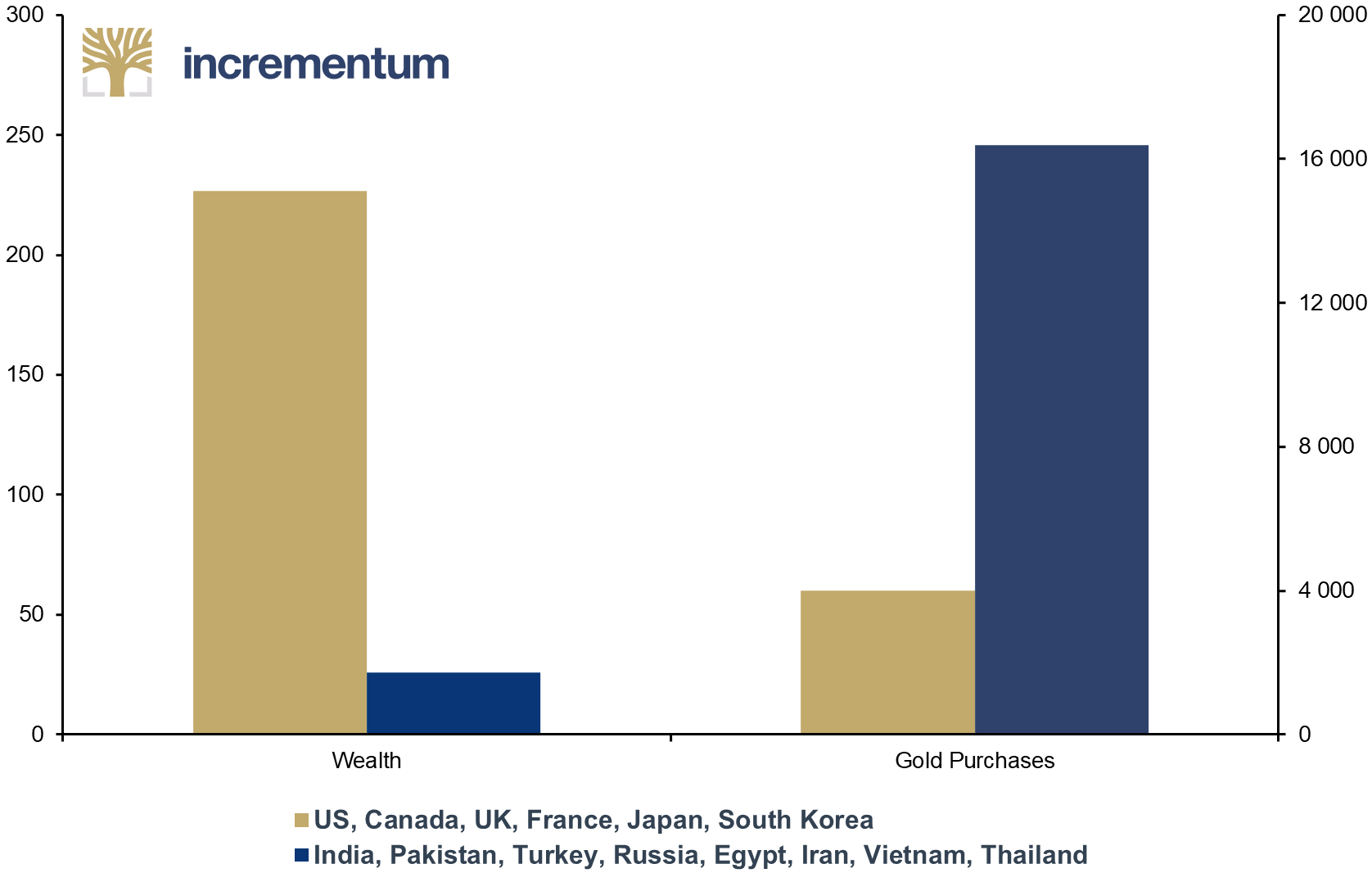

Wealth, and Gold Coins, Bars and Jewelry Purchased from 2010-2022, in %

Source: Quantinvestor, World Gold Council, Incrementum AG

Now, as geopolitical risks take on new dimensions that are pushing the world’s nations to rapidly align between Western and non-Western blocs, it will be crucial to understand who has the most gold, as well as if and when these blocs will move to a monetary showdown involving a new gold-backed international monetary system.

Gold Imports and Gold Stock Held

Over the past few decades, as the global gold market has undergone a significant shift from West to East, one of the key drivers of this trend has been the skyrocketing demand for physical gold in Asia, particularly from India and China. This has led to huge stocks of the world’s gold flowing into these countries, gold that now resides in private hands.

Given that India has little domestic gold mining activity, it has to rely entirely on gold imports to satisfy its vast gold demand. And even though China is the world’s largest gold-producing nation – and has been the number one gold producer since 2008 – domestic gold mining production in China only meets a fraction of China’s annual gold demand, leaving the rest to be fulfilled by gold imports.

Gold imports into India and China therefore perfectly illustrate the global shift in gold markets from West to East, as Asian nations have emerged to dominate physical gold trade flows.

India

While Indian citizens have always been known as huge physical gold holders, their appetite for continued gold purchases appears to know no bounds.

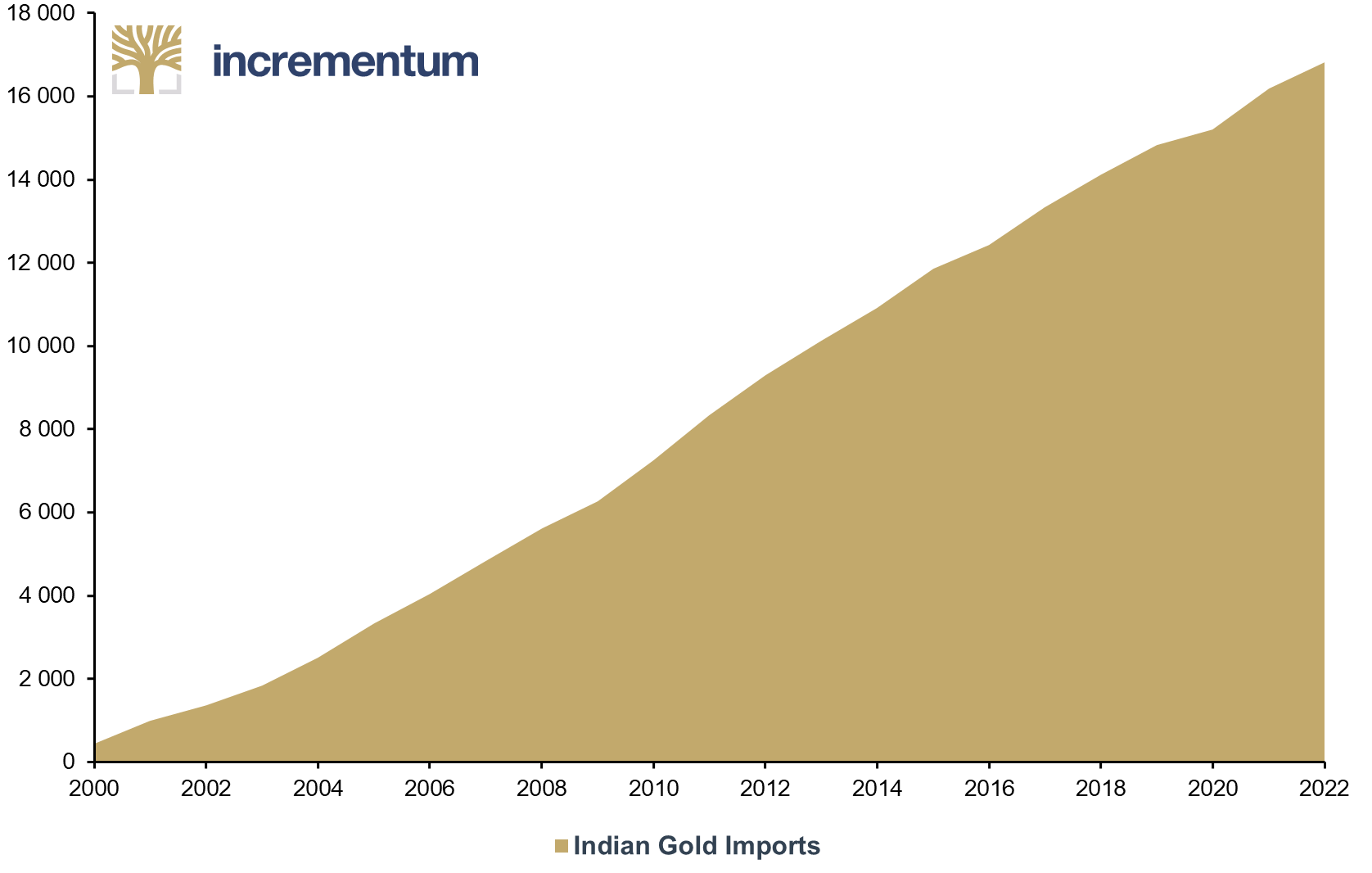

Data from the Indian Government’s Directorate General of Commercial Intelligence and Statistics (DGCIS) shows that between 2000 and 2022, India imported a staggering 16,820 tonnes of gold, from countries such as Switzerland, the UAE, and Hong Kong, and from countries across Africa. That’s an average of 730 tonnes of gold per year imported into India over a 23-year period.

Indian Gold Imports since 2000 (Cumulative), in Tonnes, 2000-2022

Source: Indian Ministry of Commerce and Industry, Incrementum AG

Given that we roughly know how much gold the Indian population has held at various times in the 2000s, we can use these gold import figures to calculate how much gold the Indian population currently holds.

In 2002, Nigel Desebrock of Greedon International Research published an authoritative guide called An Introduction to the Indian Gold Market, in which he stated that as of 2001 there were approximately 12,000 tonnes of gold held in India. Based on DGCIS data, India imported a total of 15,825 tonnes of gold between 2002 and 2022. Therefore that 12,000 tonnes from 2001 have now become a staggering 27,825 tonnes. And this does not even include the unknown quantities of gold held by Indian temples, which could be of extraordinary magnitudes.

At the end of 2016, the World Gold Council estimated that total private gold holdings in India were somewhere between 23,000 and 24,000 tonnes. When we add cumulative gold imports into India of 4,385 tonnes for the six year period from 2017–2022, again based on DGCIS data, the World Gold Council’s total stock of gold held in private ownership in India now becomes a range of between 27,385 and 28,385 tonnes, which perfectly aligns with the 27,825 tonnes estimate calculated above.

This however is not the full story, since DGCIS data excludes gold smuggling into India; and as everyone knows, gold smuggling is a constant and omnipresent activity due to India’s high taxes on gold imports. Another arm of India’s government sprawling bureaucracy, the Directorate of Revenue Intelligence (DRI), estimates in its Smuggling in India Report 2019–2020 that gold smuggling could account for another 150–200 tonnes of gold brought into India each year. Smugglers are highly creative when it comes to hiding their contraband.

Factoring in this 150–200 tonnes for the last 20 years yield another 3,000–4,000 tonnes and boosts the total gold stock in private hands in India to a staggering 31,000–32,000 tonnes. Astonishingly, 32,000 tonnes of gold are more than the combined gold holdings of the top 27 central bank gold holders in the world.

Of this 31,000– 32,000 tonnes of Indian private gold, 20,000–21,000 tonnes have flowed into India during the last 20 years. No other country, except China, comes close to the magnitude of these gold import flows.

China

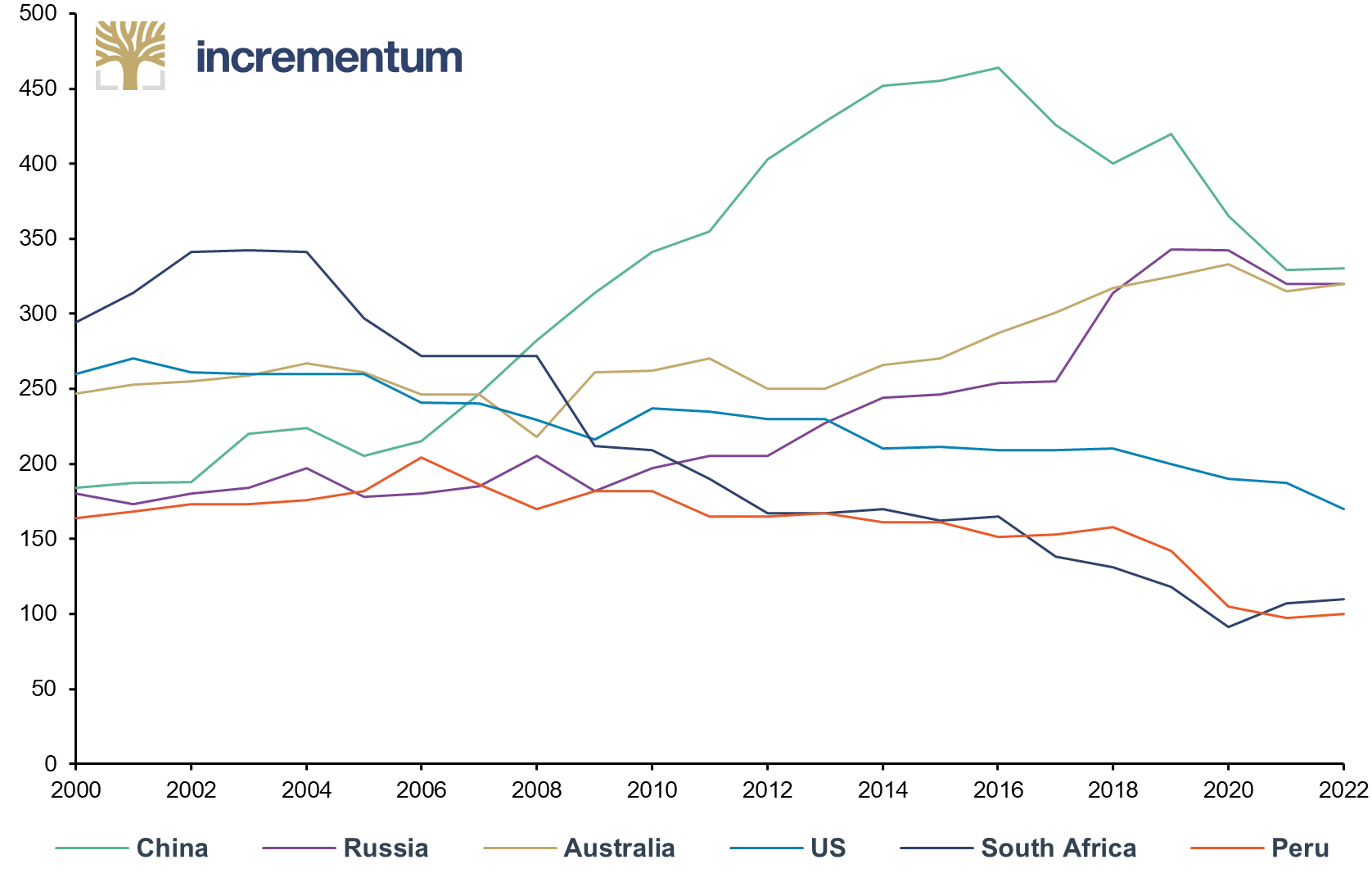

Unlike India, China is a gold mining powerhouse; and in fact, China has been the world’s leading gold mining producer since 2008, when it leapfrogged ahead of the traditional big three gold producers of South Africa, Australia and the US.

This dominance in gold mining by China was made possible by the sheer growth rate of China’s domestic gold mining output in this century. In the year 2000, China produced 170 tonnes of gold; however ten years later, in 2010, China was producing more than double that with an annual 345 tonnes of gold output.

China’s gold output then continued to increase dramatically over the subsequent five years; and by 2015, Chinese gold production peaked with annual output of 450 tonnes. Production then remained above the 400 tonnes level each year for a number of years, before falling slightly in 2019. Despite that drop, China has still remained as the world’s number one gold producer every year since then.

Also notable is that Russia’s gold production has experienced enormous growth in the last two decades, a growth which has allowed Russia to climb the rankings to now become the second largest gold producing country in the world. From not even being in the top 5 gold producers in the 1990s, Russia, like China has seemingly come out of nowhere, becoming the 5th largest gold producer in the 2000s, the 4th largest in in 2009, the 3rd largest in 2014 (when it bypassed the US), and the 2nd largest in 2018, when Russia topped Australia.

We are now witnessing an era where China and Russia are the world’s two leading gold mining producers, ahead of Australia, the US and South Africa.

Annual Gold Mining Production, in Tonnes, 2000-2022

Source: Refinitiv, Incrementum AG

Even given these impressive annual gold mining output figures, the sheer size of China’s annual gold demand since the early 2000s has been far in excess of domestic gold production levels, necessitating that the gap be filled by gold imports. These gold imports come chiefly from countries such as Switzerland, Hong Kong, Australia, and South Africa.

While individual-country gold flows into China can be examined and collated in an attempt to gauge how much gold is entering China, a much simpler way to estimate China’s annual gold imports is to look at the look at the Shanghai Gold Exchange (SGE) since the SGE allocates gold for the entire Chinese gold market.

On the supply side, due to cross border trade rules, all gold imported into China is required to be channeled through the SGE. In addition, due to VAT rules and incentives, where high-purity gold is exempt from VAT when traded on the SGE, most of the remaining Chinese gold supply, from domestic production and recycled gold, also flows through the SGE.

On the demand side, the SGE supplies gold to the entire Chinese market, so physical gold withdrawals from the SGE are a suitable proxy for Chinese wholesale gold demand (consumer demand and institutional demand). We can therefore estimate Chinese gold imports without looking at import trade statistics, but rather by taking SGE gold withdrawals and subtracting domestic gold production.

Between 2002 and 2022, SGE gold withdrawals totaled an enormous 25,800 tonnes. During that period, Chinese domestic gold production totaled 7,400 tonnes. The difference, which is an approximation of Chinese gold imports over the twenty-year period, is 18,400 tonnes. Note that for the same period, the WGC estimates that China imported a total of 17,270 tonnes of gold. So, the approximation is not dissimilar to WGC data.

The key takeaway is that China, like India, has imported a huge amount of gold since the early 2000s; and in China’s case this has been despite China also being the world’s largest gold mining producer. Together, India and China have officially imported somewhere in the region of 34,000–36,000 tonnes of gold over the last 20 years.

With annual gold imports by both China and India growing rapidly since the early 2000s, these two markets have over time imported an increasingly large amount of the world’s annual gold production, especially when we exclude China’s domestic production.

There are also many other Asian markets that have imported increasing quantities of gold since the 2000s, including Türkiye (over 5,400 tonnes imported since 2000), Vietnam (1,200 tonnes), Hong Kong (9,700 tonnes, a lot of which gets reexported to China), Singapore (2,700 tonnes), and Malaysia (1,700 tonnes). The list goes on and on. And as you can see, this trend is right across Asia.

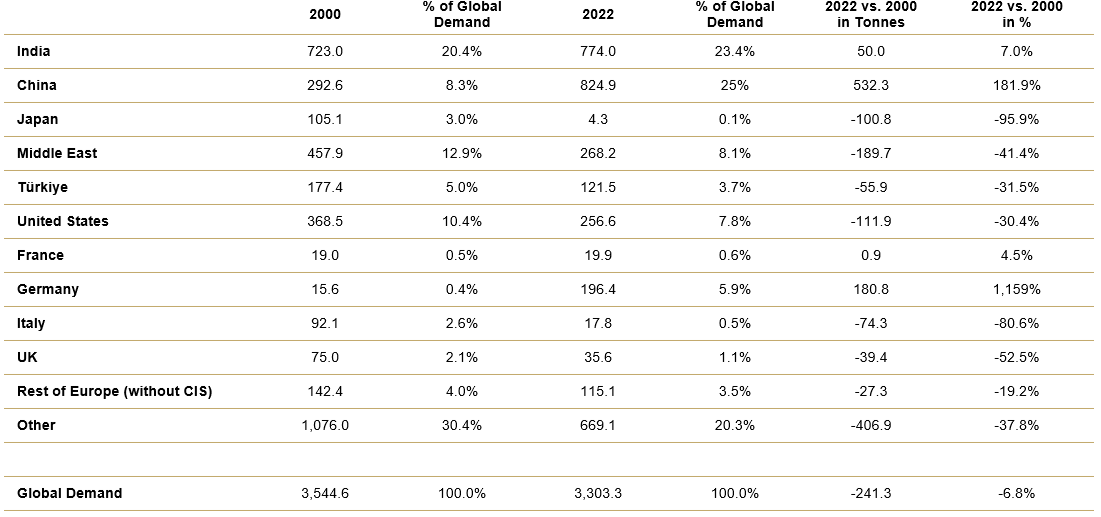

Consumer Gold Demand – 2000 vs. 2022

The following table shows consumer gold demand in the years 2000 and 2022 for selected countries and regions across the world, measured in tonnes. Comparing the demand figures of 2000 with 2022 reveals some interesting trends, with Asian gold markets growing, at the expense of the West.

Consumer Demand for Gold – 2000 vs. 2022

Source: World Gold Council, Incrementum AG

From the table, the most striking development is the huge absolute growth in Chinese consumer gold demand over the period, which rose by 532 tonnes, from 292.6 tonnes in 2000 to 824.9 tonnes in 2022. That’s an increase of 181%. India has also seen its annual consumer gold demand rise since the turn of the millennium, albeit from an already high base in the year 2000.

Together, China and India have gone from representing a combined 28.7% of consumer gold demand in 2000, to now driving nearly half (48.4%) of global consumer demand in 2022, with a combined 1,600 tonnes of demand last year.

In the Western world, only physical-gold stronghold Germany has been an outlier among Western countries, with German consumer gold demand rising an astonishing 1,200% between 2000 and 2022. But factor out Germany, and consumer gold demand in the rest of the West (the US and the rest of Europe) fell dramatically between 2000 and 2022, down 140 tonnes, or 43%, from 328 tonnes to 188 tonnes. This has been primarily due to a contraction of consumer gold demand in the US, and also in Italy and the UK.

These trends are testament to the fact that gold has flowed to where it is most appreciated and to where economic prosperity and savings rates have risen, i.e. gold has flown out of the West and into the East.

Asian Gold Trading Infrastructure

Shanghai Gold Exchange

To gauge the enormous growth of the Chinese gold market since the early 2000s, it’s instructive to look at the Shanghai Gold Exchange (SGE), which is the world’s largest physical gold exchange, and the epicenter of the Chinese gold market.

SGE is primarily a physical gold exchange, where physically delivered gold contracts trade and settle via the delivery of gold bullion between sellers and buyers, and this bullion can then be withdrawn from the SGE’s nationwide network of certified vaults. Kilobars dominate gold trading in not only China but all across Asia including in India and Hong Kong. SGE settlement is therefore predominantly in terms of gold kilobars.

For example, the flagship and highest trading volume contract of the SGE is the Au99.99 contract, which is a physically delivered spot contract for 1 kg gold ingots of 99.99% purity or higher. While kilobars dominate the SGE, there are other SGE spot gold contracts which settle with delivery of gold ingots in 3 kg, 12.5 kg and 0.1 kg weights (all of purity 99.95% or higher).

There are also international versions of the 1 kg, 0.1 kg, and 12.5 kg contracts, which trade on the SGE International Board. In addition, the SGE also trades nonspot gold contracts for deferred delivery (a range of future delivery dates) – but still the delivery is of physical gold.

When the SGE was launched in October 2002 by the People’s Bank of China (PBoC) and Chinese government, its main objectives were to provide a centralized platform for gold trading in China and to promote the development of the country’s gold market. Over time these objectives expanded to include boosting the Exchange’s international influence, promoting the use of the Chinese renminbi in international gold trading, and increasing the influence of SGE pricing on international gold price discovery.

In 2014, the SGE launched its International Board, a.k.a. the Shanghai International Gold Exchange (SGEI), so as to internationalize China’s gold market, by offering “international” members access to renminbi gold trading on the SGE and use of the International Board precious metals vault located in the Shanghai Free Trade Zone (FTZ). The International Board now has 93 members.

In 2016, the SGE also launched its own twice daily gold fixing, called the Shanghai Gold Benchmark Price auction, which was the world’s first renminbi-denominated benchmark gold price auction. The auction aims to establish a benchmark price at which supply and demand are in balance. Trading and settlement in the auction are for 1 kilogram lots of 99.99% purity gold or higher. Commenting on the launch of the Shanghai Gold Benchmark Price on April 19, 2016, Jiao Jinpu, chairman of the SBU, is reported to have said:

“The launch of the ‘Shanghai Gold’ pricing mechanism is another landmark event in the international development of China’s gold market. … The transformations from focusing on commodity attributes to focusing on commodities and financial attributes, and from focusing on domestic markets to focusing on both domestic and international markets will promote the formation of a multi-level and more open Chinese gold market system.” (our translation)

This internationalization has also given the Chinese gold market more representation and influence in global bodies such as the London Bullion Market Association (LBMA). In February 2009, there were six Chinese refineries on the LBMA Good Delivery List for gold. Now there are thirteen. In February 2009, there was only one ordinary (full) member of the LBMA from China, namely the Bank of China. Now there are seven full members from China, all banks, including ICBC, Bank of Communications, and China Construction Bank.

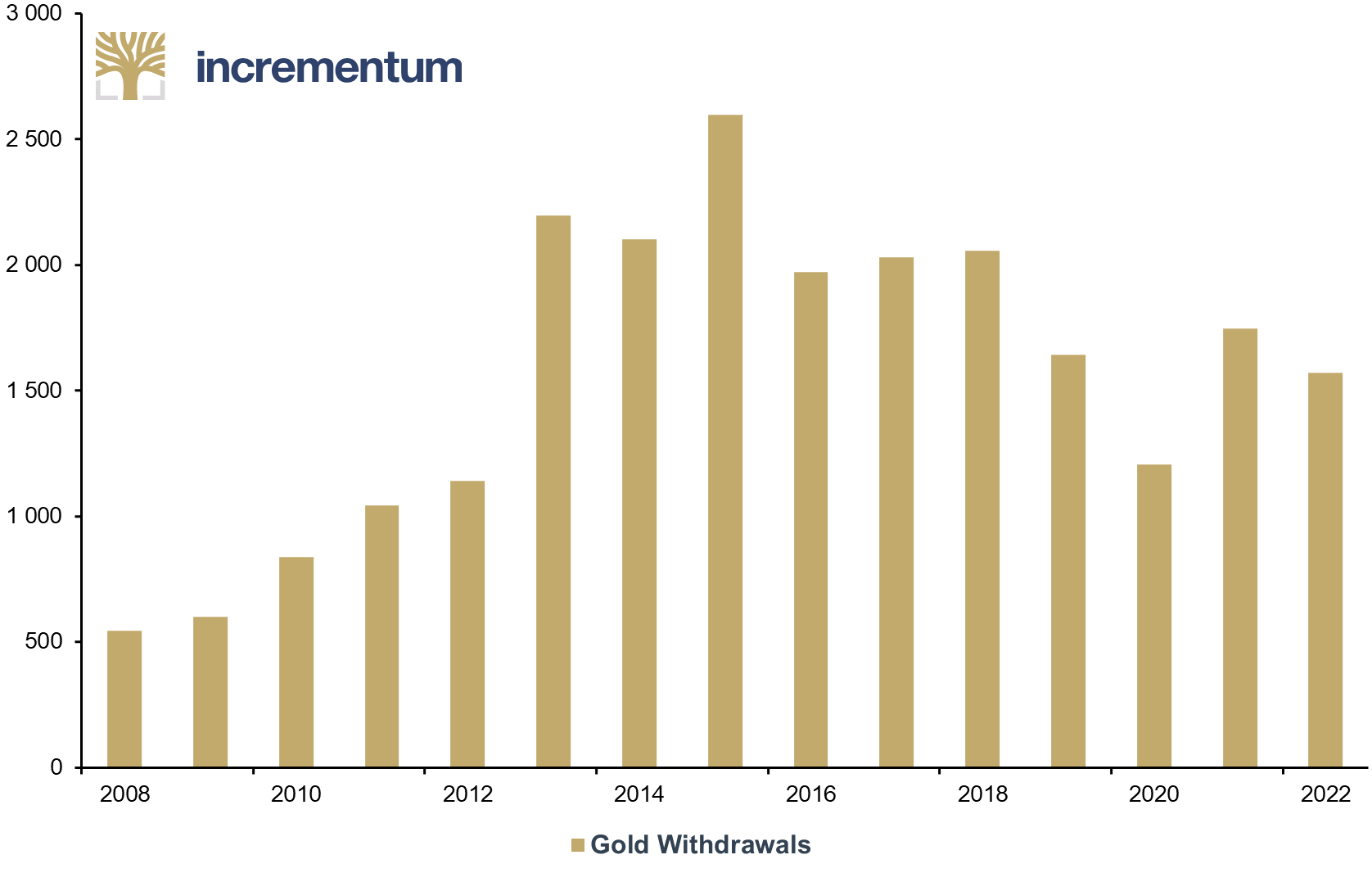

While the SGE was established over twenty years ago in 2002, it was in 2007 that SGE physical gold withdrawals began to equal Chinese wholesale gold demand. This milestone indicated that by 2007 the SGE had begun to fulfill its gold allocation role for the entire Chinese gold market. Now with virtually all gold supply in China coming in through the SGE, nearly all Chinese gold demand has to be met by gold withdrawals from the SGE vaults. Thus, SGE gold withdrawals are a suitable proxy for Chinese wholesale gold demand. One can therefore see the massive growth in the Chinese gold market by merely looking at SGE annual physical gold withdrawals.

Shanghai Gold Exchange (SGE) Gold Withdrawals, in Tonnes, 2008-2022

Source: SGE, Incrementum AG

India International Bullion Exchange (IIBX)

While India has a highly developed OTC gold trading market, and an established trading infrastructure of 1 kg gold futures contracts on the Multi Commodity Exchange of India Limited (MCX), the country’s gold trading mechanisms saw a new entrant in July 2022, with the launch of the Indian government-backed India International Bullion Exchange (IIBX).

IIBX, which offering trading of spot gold contracts backed by physical gold, is located in a special economic zone in GIFT City in the Indian state of Gujarat, and the gold backing the contracts is stored in gold vaults in GIFT City. One aim of IIBX is to facilitate qualified buyers to import gold directly into India without using banks or authorized agencies.

Although trading volumes so far have been minimal, if trading gains traction, it should go some way towards improving gold price transparency in India. Whether it will also create gold price discovery that will influence the international gold price remains to be seen.

Russian gold market infrastructure

It has become increasingly apparent that Western sanctions against Russia have accelerated the increasing array of alliances and convergences between Moscow and its Asian allies in China and beyond, not least in the gold market.

In late February 2022, as the West agreed upon sanctions as an immediate reaction to Russia’s invasion of Ukraine, the LBMA expelled three Russian banks from its membership: VTB, Sovcombank and Otkritie. Days later the LBMA suspended all six Russian precious metals refineries from the LBMA Good Delivery List; and the CME Group followed suit, suspending these same six Russian refiners from the COMEX-approved refiner list.

Less than six months later in July 2022, news emerged that Moscow and its Eurasian Economic Community (EAEU) allies were proposing the creation of a new precious metals trading and pricing infrastructure independent of the LBMA and COMEX, with the objective of breaking London’s and New York’s monopoly over global precious metals pricing. This proposal calls for:

- a Moscow World Standard (MWS) for precious metals trading, similar to the LBMA’s Good Delivery List

- a new international precious metals exchange in Moscow based on the MWS, called the Moscow International Precious Metals Exchange

- new precious metals price fixings based on the MWS, so as to generate gold price discovery and reference prices independent from the LBMA and COMEX

This new proposed Moscow World Standard gold exchange is distinct from the gold trading that currently takes place on the precious metals market of the Moscow Exchange. According to a letter by the Russian Ministry of Finance:

“It is necessary to make membership in this organization attractive to all, without exception, foreign participants in the precious metals market, especially China, India, Venezuela, Peru, and other countries of South America and Africa… The creation of such a structure will be able to destroy the LBMA monopoly in the shortest possible time and create a powerful international association of participants in the precious metals industry and ensure the stable development of the industry both in Russia and around the world.”

The proposal for a Moscow World Standard and a new precious metals exchange emerged following a meeting of finance ministries, central banks, exchanges, and gold producers of Eurasian Economic Union (EAEU) member states, after which the proposal was distributed to all financial market participants in each EAEU state.

The mastermind of the proposal was Sergey Glazyev, who is Minister for Integration and Macroeconomics of the Eurasian Economic Commission (EEC) – the EAEU’s executive body. Glazyev is very close to Putin and was an advisor to the president of the Russian Federation between 2012 and 2019. He is also a former deputy in the Russian State Duma and a former minister of Foreign Economic Relations of the Russian Federation.

Five months after Sergey Glazyev introduced proposals concerning a Moscow World Standard for gold, he updated his ideas in an article published on the Russian news site Vedomosti during the last week of 2022.

In the article titled “Russian Ruble 3.0 – How Russia can change the infrastructure of foreign trade”, Glazyev and co-author Dmitry Mityaev highlight the gravitation of Russia’s trade towards friendly countries, the presence of many trade surpluses with these countries (in yuan, rupees, rial, etc.), and the need to minimize possible exchange-rate and sanctions risks on these surplus balances.

Critically, their bombshell proposal to do so, which has been under-reported in Western media, is to “buy non-sanctioned gold in China, UAE, Türkiye, possibly Iran and other countries for local currencies”.

Cooperation between the Chinese and Russian gold markets

China and Russia are already working closely on interconnecting their gold markets via collaboration between the Shanghai Gold Exchange and Russia’s financial authority, the Self-Regulatory Organization ‘National Financial Association’ (SFO NRA). SFO NRA is a Russian professional body representing the entire Russian financial sector, including the Russian precious metals market.

In November 2020, the SGE and Russia’s SFO NRA signed a memorandum of understanding (MoU) in a live ceremony, by which the countries aim to open a new era of Sino-Russian gold market cooperation, via promoting the development of both markets and facilitating Russian institutions to access China’s gold market. This MoU was followed by a China-Russia precious metals webinar in June 2021, hosted by the SGE. In the press release, the SGE stated that

“[the] two parties will continue to work to establish a communication platform for investors in the two countries, and promote a win-win situation through cooperation, so as to promote the healthy development of the two countries’ gold markets in the post-pandemic period.”

Because of the Western sanctions now targeting Russian gold exports, gold exports to China have already ramped up since mid-2022. With three Russian banks – VTB, Sberbank and Otkritie – already members of the SGE International Board, this cooperation between the gold markets of Russia and China looks set to intensify. This sentiment is echoed in the Russian SFO NFA Facebook account’s comments:

“Russia and China play an essential role in the global gold market as the leading gold producing countries. In this regard, in 2018, the SRO NFA and Shanghai Gold Exchange reached an agreement on the beginning of cooperation, which is now officially enshrined in the Memorandum [MoU]…The purpose of the MOU is to exchange accumulated knowledge and experience to facilitate connectivity and mutual development of the Russian and Chinese precious metals markets.”

Central Bank Monetary Gold Buying

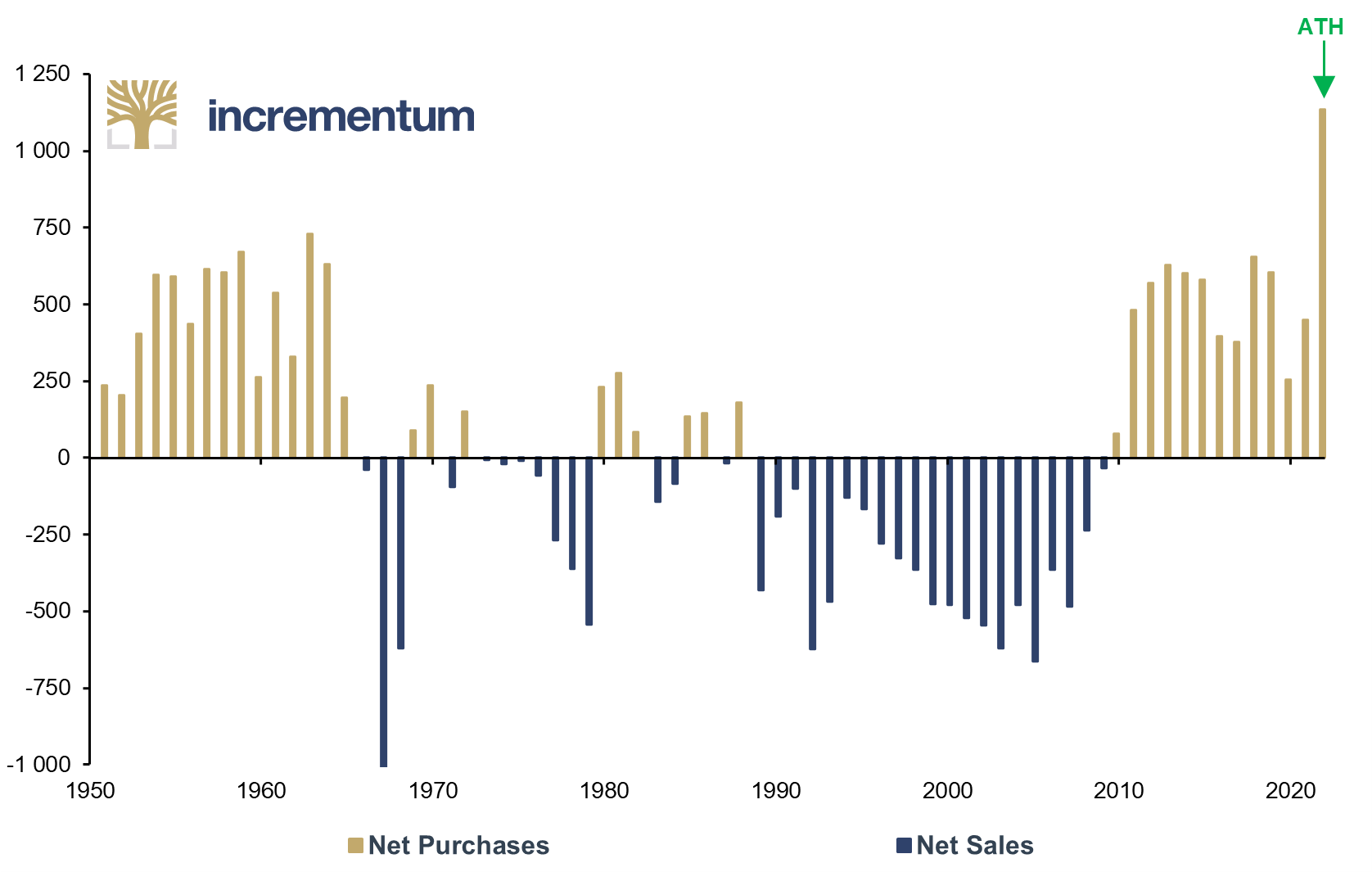

When looking at the shift in the global gold market from West to East, one segment which arguably gets more attention than any other is the central bank gold market. Over the last 15 years, non-Western central banks, mostly but not exclusively in Asia and mostly but not exclusively emerging market nations, have literally monopolized central bank gold buying and become increasingly important players in the sector.

For many years from the early 1990s, Western central banks dominated the central bank gold market, and their transactions, mostly sales from their huge stockpiles, had a significant impact on sentiment. In the 1990s, this included significant gold sales by countries such as Australia, Canada, the UK, Belgium and the Netherlands; and in the 2000s further huge gold sales were undertaken within the framework of a series of Central Bank Gold Agreements (CBGAs), including gold sales by Spain, France, Switzerland, Austria, the Netherlands, and the ECB.

Global Central Bank Gold Purchases, in Tonnes, 1950-2022

Source: World Gold Council, Incrementum AG

Pivot 2009, and net buyers 2010–2022

Then, in 2009, a critical pivot occurred, when, for the first time in 20 years, central banks as a group turned from being net sellers to being net buyers of gold. While this pivot was partially triggered by the Global Financial Crisis and the ensuing deep recession of 2007–2009 as central banks moved to diversify their foreign exchange reserves, the shift was also supported by the growing economic and geopolitical influence of Asian powers such as China and Russia. It was also a pivot which signaled the beginning of a new multi-year trend of central banks being sizeable and continuous net buyers of gold.

The year 2009 was also the year in which China threw down the gauntlet by announcing an addition of 454 tonnes of gold to its reserves, i.e. gold which had been accumulated over the previous 6 years, and in which India bought 200 tonnes of gold from the IMF in one off-market transaction.

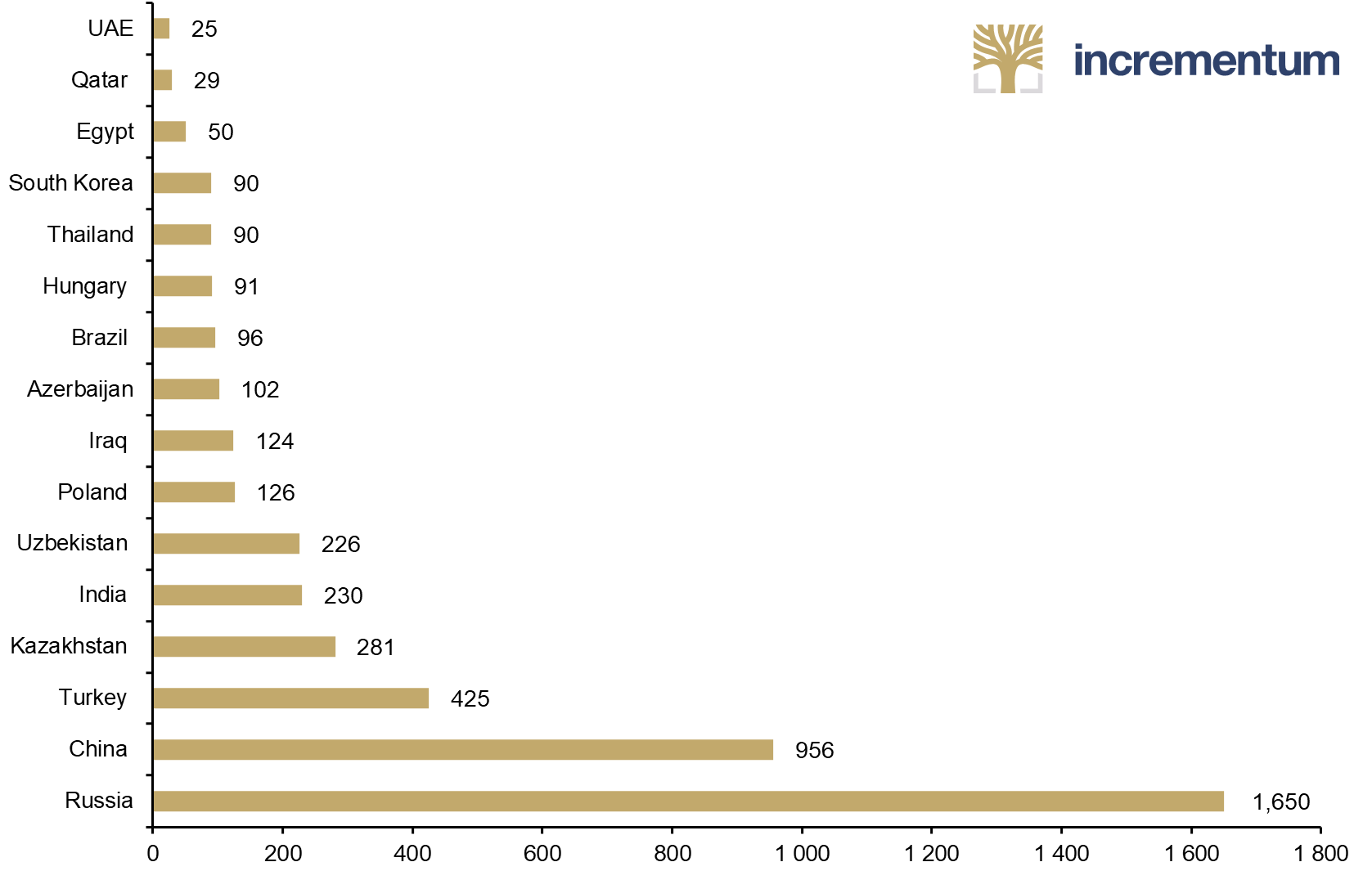

According to the WGC, between 2010 and 2022, central banks and other official financial institutions added a cumulative 6,800 tonnes of gold and were net buyers of gold every single year over this timeframe. Of this total, 4,984 tonnes of gold purchases have been reported, either directly by the central banks or via the IMF’s International Financial Statistics (IFS) database and can be attributed to buying by specific countries.

The largest ‘reported’ central bank gold buyers over this 2010-2022 period were the Russian Federation (1,650 tonnes), China (956 tonnes), Türkiye (425 tonnes), Kazakhstan (281 tonnes), India (230 tonnes), and Uzbekistan (226 tonnes).

But the list of gold buyers goes on and on: Poland (126 tonnes), Iraq (124 tonnes), Azerbaijan – State Oil Fund SOFAZ (102 tonnes), Brazil (96 tonnes), Hungary (91 tonnes), Thailand (90 tonnes), Korea (90 tonnes), Qatar (79 tonnes), United Arab Emirates (75 tonnes), and Egypt (50 tonnes).

The above 16 countries collectively bought a staggering 4,700 tonnes of gold over that 2010–2022 period. Apart from Poland and Hungary, all of these central banks are located within Asia or the Middle East or else have an affiliation – like Brazil – to institutions where the majority of countries represented are Asian countries.

Largest (Reported) Gold Buyers, in Tonnes, 2010-2022

Source: World Gold Council, Incrementum AG

2022 – Record Year for Central Bank Gold Buying

Indeed, the central bank gold buying trend is still accelerating, since according to WGC data, 2022 was a record year, with central banks buying a combined 1,136 tonnes of gold. Of this total, 862 tonnes or over 75% occurred in the second half of the year, and a majority, over 655 tonnes, was “a substantial estimate for unreported buying”.

For example, of the 445 tonnes of gold said to have been bought by central banks in Q3/2022, nearly 300 tonnes of this were ‘unreported’. In Q4/2022, the trend was similar, with over 270 tonnes of Q4 central bank gold buying not attributable to reported purchases.

While the reported purchases are sourced from central bank reports and the IMF’s IFS database, the unreported buying is confidential information sourced by the WGC and its data consultant Metals Focus. Although we cannot by definition verify which central banks represent the unreported buying during 2022, much of this was likely to have been by emerging market central banks, and some of it would have involved China and Russia.

What is apparent, though, is that the ‘reported buying’ by central banks during 2022 was predominantly from Asia and the Middle East (including Türkiye). Central bank gold buying across the Middle East was particularly buoyant in 2022, with Türkiye adding a huge 147.3 tonnes, Egypt 44.7 tonnes, Iraq 33.9 tonnes, Qatar 35 tonnes, and the United Arab Emirates 19.5 tonnes.

As well as Russia, Central Asia was represented by Uzbekistan, which added 34 tonnes. In South Asia, the Reserve Bank of India bought 33.3 tonnes of gold during 2022. In East Asia, the Central Bank of Mongolia says it accumulated 22.9 tonnes of gold in 2022.

Not surprisingly, the trend of 2022 has continued into 2023, with Singapore’s central bank, the Monetary Authority of Singapore (MAS), revealing that it returned to substantial gold buying for the second time in two years with the announcement of a combined 68.6 tonnes of gold buying over January, February, and March 2023. These early 2023 purchases followed an earlier bout of gold purchases by MAS of 26 tonnes over the period May and June 2021. The combined purchases of 95 tonnes of gold by MAS from May 2021 to March 2023 have together boosted Singapore’s gold reserves by 75% in less than two years. MAS now holds 222.4 tonnes of gold.

Interestingly, prior to May-June 2021, Singapore had held 127.42 tonnes of gold and had not bought any gold for many years, so the country’s return to gold buying is notable in that one of the most sophisticated central banks in Asia is returning to gold buying after many years of sitting on the sidelines.

Leaving the largest until last, central bank heavyweights China and Russia have also recently returned to the gold market with a bang and have now begun to announce monthly gold buying again. And in both cases the strategic timing of the announcements and their geopolitical importance cannot be understated.

China recommences gold buying announcements

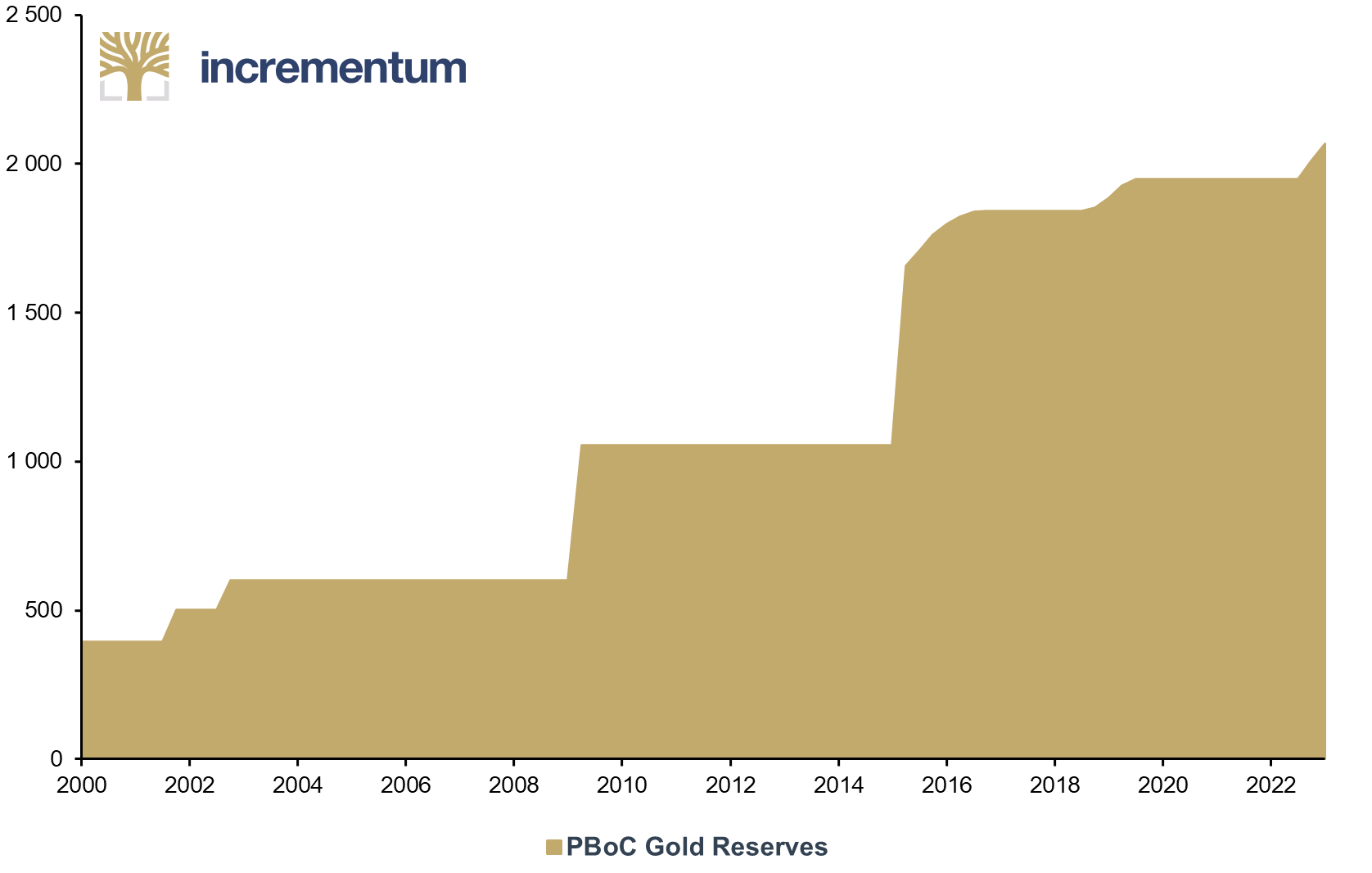

In December 2022, China surprised the global gold market when it announced that during November 2022, the People’s Bank of China had purchased 32 tonnes of gold. Surprising, because before November 2022 it had been 37 months, or more than a 3-year hiatus, since the PBoC had officially last added to its gold reserves, in September 2019.

These monthly gold buying announcements by China have continued for another five months now, with China’s State Administration of Foreign Exchange (SAFE), which publishes China’s official reserve asset data, announcing on a monthly basis that between December 2022 and April 2023, the PBoC added another 96 tonnes of gold –That’s a very substantial 128 tonnes of

gold added to China’s monetary gold reserves over just a six-month period between November 2022 and April 2023. The PBoC’s gold reserves now officially stand at 2,076 tonnes.

PBoC Gold Reserves, in Tonnes, Q1/2000-Q1/2023

Source: World Gold Council, Incrementum AG

Russia recommences gold buying updates

Towards the end of March 2023, the Russian central bank also returned to announcing its gold holdings, following a one-year hiatus, and revealed that in the one-year period between February 2022 and February 2023, it had officially accumulated another 1 million ounces of gold, or 31 tonnes, thereby taking Russia’s total gold holdings to 2,330 tonnes.

This one-year pause had begun in February 2022, following Russia’s invasion of Ukraine and the West’s move to freeze Russia’s US dollar and euro FX reserves, at which point Russia decided to halt publication of its international reserves data, including for gold. That created a shroud of secrecy as to whether Russia was continuing to add to its monetary gold reserves. Now this shroud has been lifted.

Strategic timing of Chinese and Russian gold updates

The dates on which both China and Russia restarted monthly updates to their monetary gold reserves have huge strategic and geopolitical significance, since they both coincided with geopolitical dialogs involving China and its global allies. Similar to China’s previous multi-month gold buying announcements in 2015 and 2018, which coincided with or preceded important economic or monetary events (i.e. China’s desire in 2015 for the yuan to be added to the IMF’s SDR, and the Chinese-US trade war of 2018-2019, respectively), China’s latest monthly gold buying announcements recommenced on the very day, December 7, 2022, that Xi Jinping began a visit to the world’s largest oil exporter, Saudi Arabia, to attend meetings with Gulf Arab states and Arab leaders, meetings which were described by Chinese foreign ministry spokeswoman Mao Ning as “an epoch-making milestone in the history of the development of China-Arab relations”.

A few months later, Chinese Premier Xi Jinping was back in the picture, with the Bank of Russia commencing publication of its gold holdings less than 24 hours after Xi Jinping met with Russia’s Putin in Moscow on March 21, during which they signed an agreement on a new era of cooperation between China and Russia.

The timing of both China’s and Russia’s new gold buying announcements following meetings between Xi and the Arab world, and Xi and Putin, respectively, are surely signals that these new-era strategic partnerships will undoubtedly include gold as a component of future monetary arrangements.

As to how much sovereign gold China and Russia really hold, that is the billion US dollar question. When China announces in a certain month that it added XYZ tonnes of gold to its reserves during the previous month, are we to take that statement at face value, that the purchase was actually in the previous month? Probably not.

In reality, the Chinese state is most likely constantly accumulating gold bullion through multiple channels and into multiple holdings, and has never stopped accumulating, both on the international market as well as possibly from undisclosed domestic gold production. China therefore most likely has significant undisclosed gold reserves.

When China feels the need to reveal slightly more of its golden hand, as it is currently doing, it reclassifies a portion of this gold from an opaque holding into a more transparent PBoC account holding. These opaque holdings could include gold held by SAFE , or by China Investment Corp (CIC), or gold holdings under the control of the large Chinese banks. Remember that all of these entities were founded by and are under the control of the Chinese state.

The real size of Chinese gold reserves could therefore be far higher than the PBoC’s stated holdings of 2068 tonnes. Jan Nieuwenhuijs estimates that the Chinese central bank already holds 4,400 tonnes of gold, more than twice what the PBoC discloses.

Excursus: The PBoC holds more than twice the amount of gold officially disclosed[1] – by Jan Nieuwenhuijs

One of the best kept secrets on this planet is the true size of the PBoC’s monetary gold reserves. Based on industry sources, my estimate is that the PBoC held 4,400 tonnes at the end of 2022, which is more than double what they officially disclosed. This amount would make China the second largest gold reserve country after the USA.

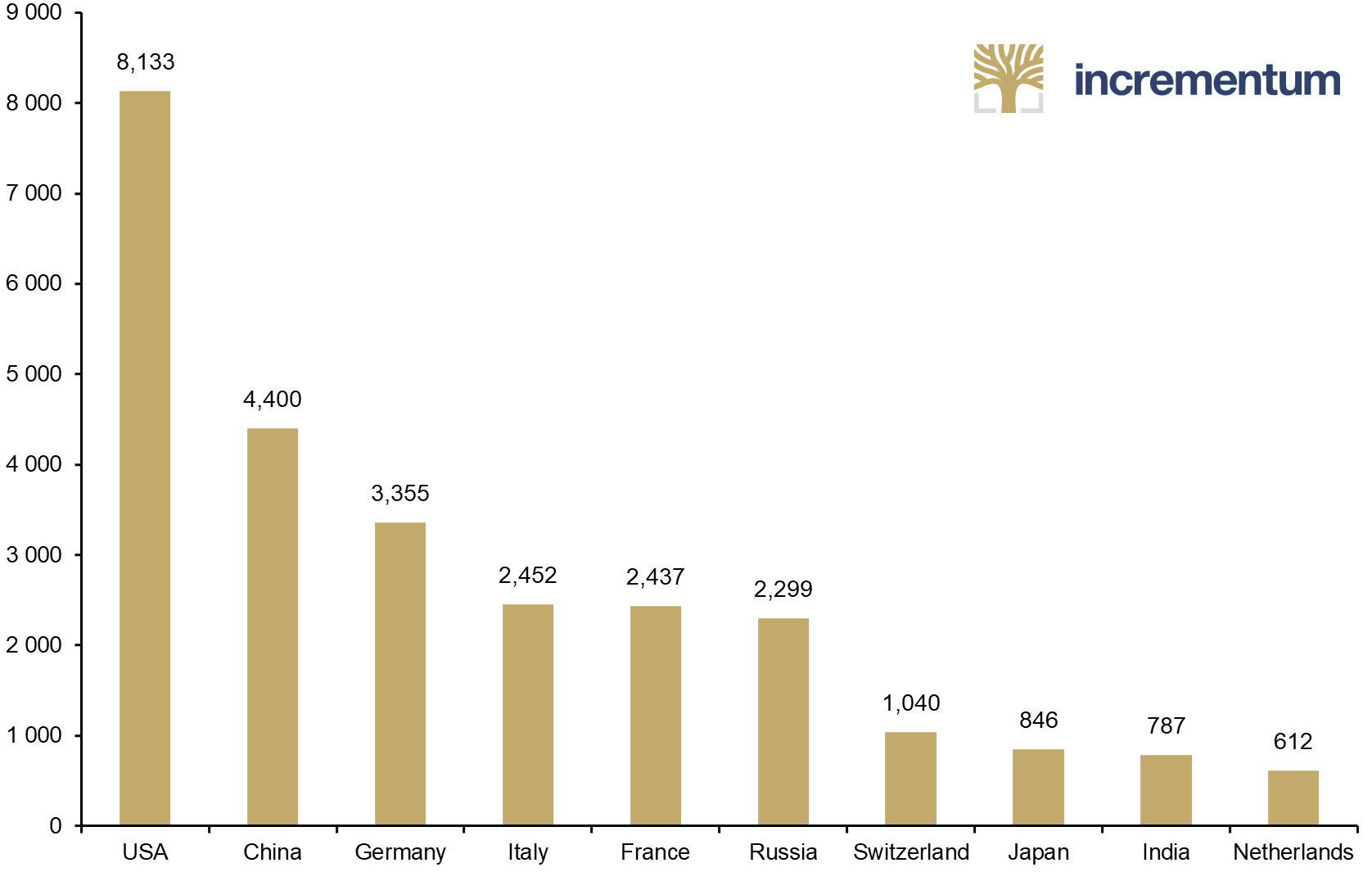

Top 10 Countries by Gold Reserves (China is an Estimate), in Tonnes, Q4/2022

Source: Gainesville Coins, World Gold Council, Incrementum AG

Most investors in the gold space are aware that the PBoC underreports its gold reserves. China is a very large player in the global economy, with massive foreign exchange, but their gold reserves are relatively low. Officially they held 2,010 tonnes by December 2022. For the PBoC to openly buy significant amounts of gold would rock the gold market and drive up the price. Therefore, they choose to buy covertly to get more gold for their US dollars.

Some gold commentators try to gauge the true size of the PBoC gold reserves by using Chinese mine production and import numbers, and then estimate what share is bought by the central bank. This approach is flawed, in my view. In the Chinese domestic market, virtually all mine output, nonmonetary import flows, and recycled gold is sold through its central bourse, the Shanghai Gold Exchange (SGE), where gold is traded in renminbi. But this is not where the PBoC buys its gold.

First, by purchasing gold the PBoC wants to diversify its foreign exchange reserves. Gold on the SGE is traded in renminbi, which is not suitable for the Chinese central bank. Second, gold on the SGE often attracts a premium, while metal abroad does not. Third, monetary gold crossing borders is exempt from being included in customs statistics. Abroad the PBoC can purchase metal by stealth. Fourth, a gold trader at one of the biggest state-owned Chinese banks told me the PBoC does not buy gold at the SGE but though proxy banks, such as the one he works for, abroad. Countless other industry sources have also confirmed the PBoC doesn’t buy gold at the SGE. In early 2017, author and gold commentator Jim Rickards met with three heads of the precious metals departments of large Chinese banks. Rickards stated in the Gold Chronicles podcast published January 17, 2017:

“What I don’t know is about the Shanghai Gold Exchange sales; they’re pretty transparent – how much of that is private and how much of that is the government [PBoC]? And I was sort of guessing 50/50, 70/30, whatever. What they told me, and these guys are the dealers, it’s 100% private. Meaning, the government operates through completely separate channels. The government does not operate through the Shanghai Gold Exchange. … None of what’s going on on the Shanghai Gold Exchange is going to the People’s Bank of China.”

The above implies there is but one approach to figure out how much the PBoC actually holds: through intelligence from those dealing with the PBoC – bullion bankers and people at refineries and secure logistics companies around the world.

In 2015, I had the opportunity to talk to a gentleman who worked at one of the big consultancy firms. Obviously, he was well connected in the industry. For political reasons it was very difficult for his company to go on record with the PBoC’s true holdings, though he told me his team estimated they were almost twice the official number. At the time, the PBoC disclosed to have 1,700 tonnes, so in reality it was closer to 3,300 tonnes. But how do we know how much they’ve bought since then?

Every quarter, the WGC publishes the Gold Demand Trends report, which contains data provided by Metals Focus (MF) on mining output, scrap supply, retail bar demand, ETF hoarding/dishoarding, etc. In these reports there is a total stated for the official sector: the net purchase or sale by all central banks and international financial institutions combined. This is an estimate based on MF’s field research and doesn’t necessarily align with what central banks openly declare.

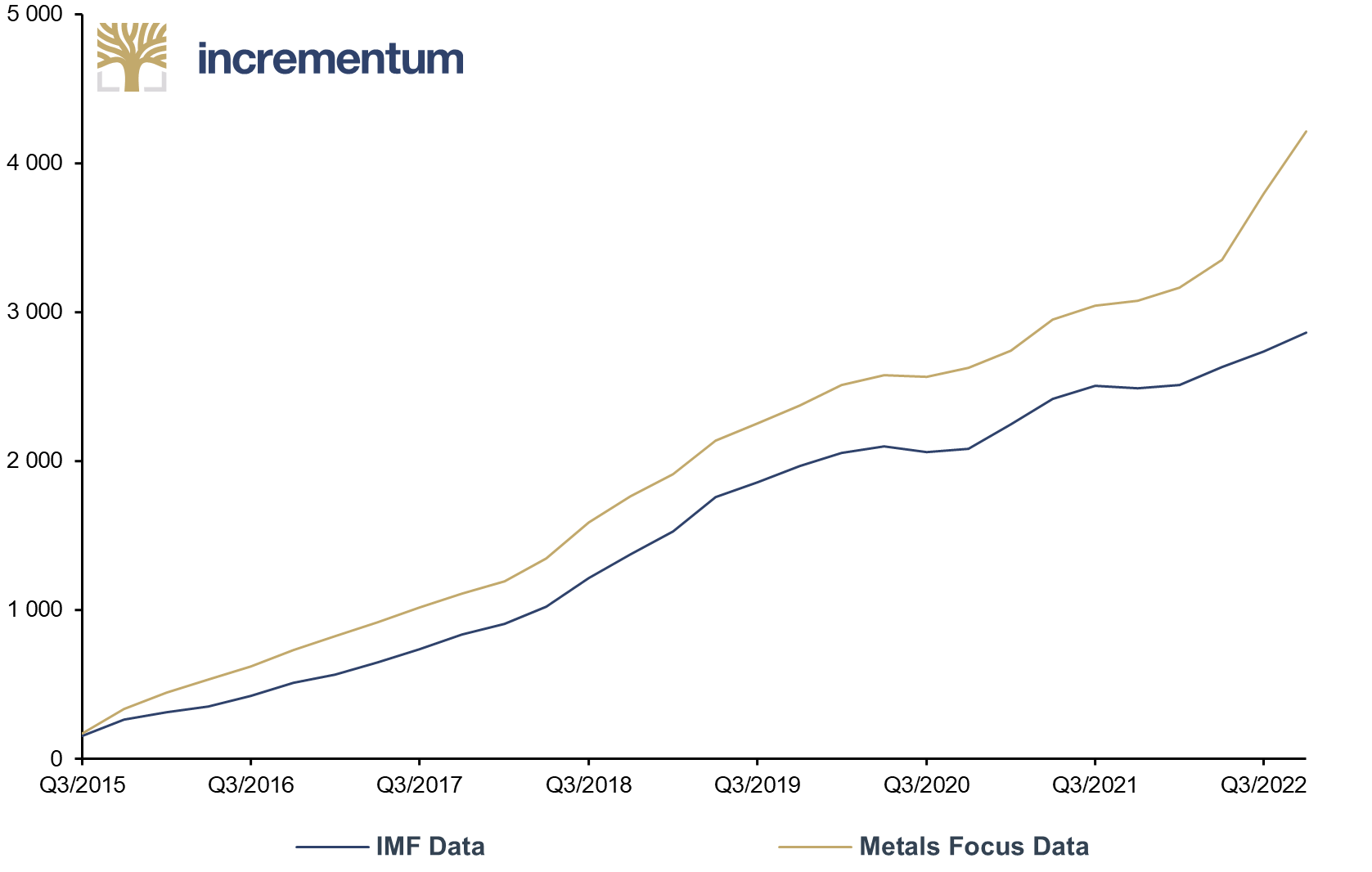

By comparing the WGC’s official sector estimates to what the official sector publishes, we can deduce what’s bought covertly. Two people familiar with the matter, who prefer to stay anonymous, told me that the majority of these clandestine purchases can be ascribed to the Chinese central bank. Let’s take 80% of the difference between the WGC’s data and the official numbers released by the IMF as PBoC acquisitions. Since 2015, the gross difference has mushroomed to 1,375 tonnes. The PBoC thus may hold about 1,100 tonnes, i.e. 80% of 1,375 tonnes, more than in 2015, or 4,400 tonnes.

Cumulative Gold Purchases since Q3/2015, in Tonnes, Q3/2015-Q4/2022

Source: Gainesville Coins, IMF, Metals Focus, Incrementum AG

To the data “reported by the IMF,” the reserves of all countries and international financial institutions were added. Then the numbers for Australia, Türkiye, and the BIS were corrected, due to gold loans and swaps on their books. The IMF doesn’t take loans and swaps into account when estimating official sector buying. The resulting series differs from the IMF’s “world” series.

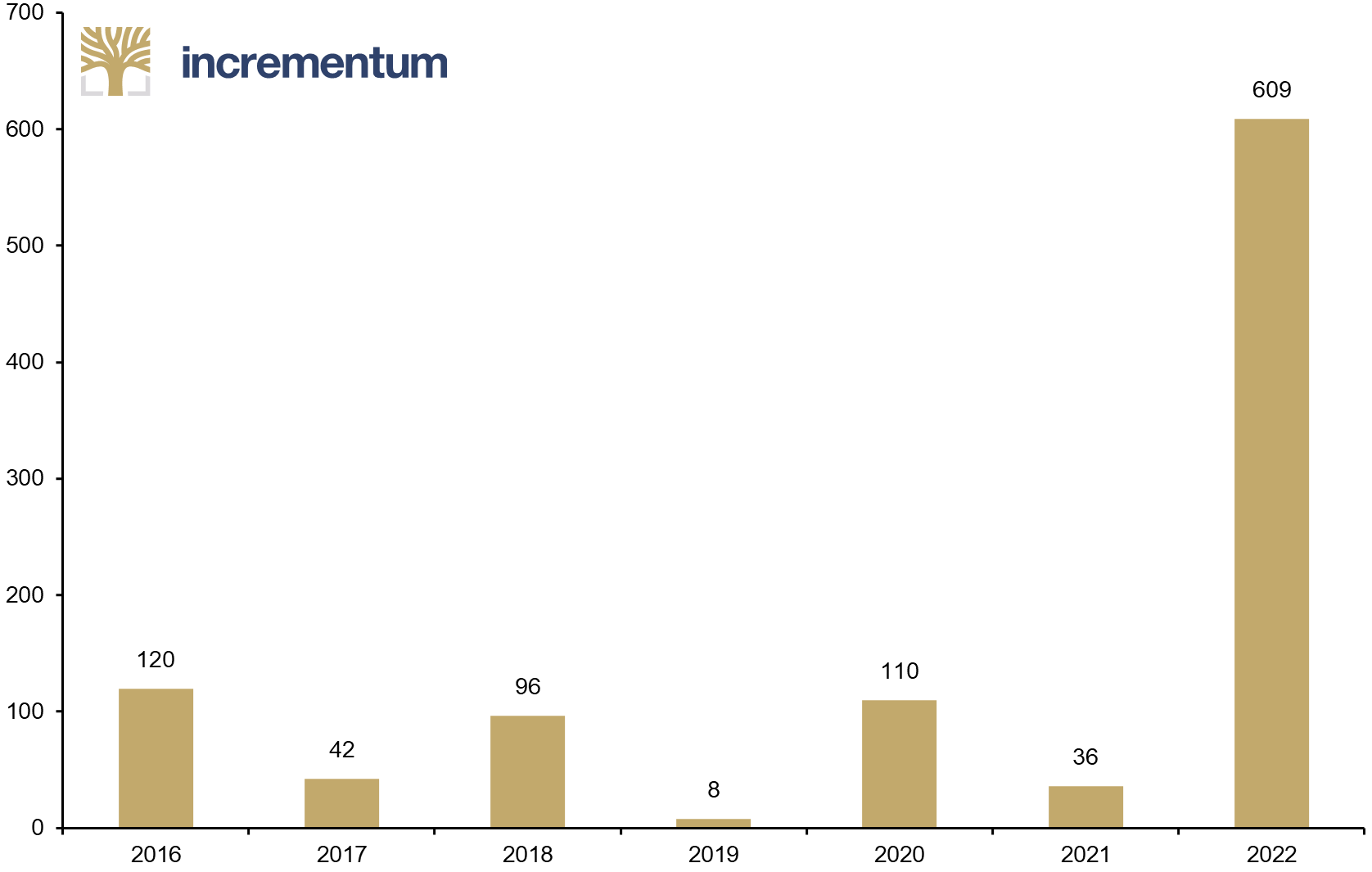

Most of the PBoC’s surreptitious purchases since 2015 were made in 2022, when it bought 600 tonnes. The war in Ukraine – and the US and the EU freezing US dollar assets of the Russian central bank as a result – have pushed the PBoC into speeding up purchases. At 4,400 tonnes, the Chinese still hold relatively little gold compared to other large economies, such as Germany, France, and the US. We can expect the PBoC to continue to buy large amounts of gold in the years ahead, which is supportive of the gold price.

Estimated Annual PBoC Gold Purchases, in Tonnes, 2016-2022

Source: BIS, Gainesville Coins, IMF, Metals Focus, World Gold Council, Incrementum AG

After this excursus into the Chinese gold holdings, we now turn our attention to Russia, as the Russian Federation could also have far more gold than its disclosed reserves of 2,330 tonnes. As well as undisclosed gold reserves that could be held by the Bank of Russia, Russia may be holding undisclosed gold in its sovereign wealth fund, i.e. the National Wealth Fund, and in the Russian State Fund of Precious Metals and Precious Stones, i.e. the Gosfund, and even elsewhere.

Russia’s National Wealth Fund is administered by the Russian Ministry of Finance, and its operational investments are carried out by the Bank of Russia. The Gosfund is managed by the state organization Gokhran, which reports to the Russian Ministry of Finance. Like China, Russia is probably accumulating gold bullion all the time through multiple channels and into multiple holdings, and only reveals slightly more of its golden hand when it feels the need to do so.

In a centralized and highly controlled society where citizens readily obey all government rules, it is possible that the Chinese government could, if it deemed it necessary, exert control over China’s huge private gold holdings, either asking that physical gold be transferred to the authorities for patriotic reasons and the greater economic good, or by even making it mandatory to do so. This would give the Chinese sovereign control over far greater gold holdings than just the monetary gold held by the PBoC and other Chinese government entities.

The ability of the Indian authorities to collect or gain control over India’s 30,000 + tonnes of private gold looks less promising. Indian households are obsessed with hoarding physical gold, and previous government attempts to convince Indian citizens to hand in their gold via schemes such as the Gold Monetization Scheme (GMS) met with nearly total failure.

Geostrategic central bank gold buying: SCO / BRICS / EAEU / BRI

When central banks are asked why they hold gold, they will mostly reply that they hold gold in their reserves for security and liquidity, while citing reasons such as gold’s lack of counterparty risk and default risk, that gold performs well in times of crisis, and that gold is a store of value and a portfolio diversifier.

While all of these reasons for gold buying are valid and true, many Asian and emerging-market central banks are also accumulating gold for strategic reasons, i.e. to reduce their exposure to the US dollar, to hedge against the ever-heightening geopolitical risk from the West, and even in preparation for gold’s reemergence at the core of a new multi-polar monetary system and trading system which could replace the US dollar.

This becomes apparent when you compare the identities of the largest central bank buyers over the last 15 years to the memberships of non-Western regional groupings such as the regional security and economic cooperation-focused Shanghai Cooperation Organisation (SCO) and the economic-focused BRICS grouping. And the overlaps here are indeed striking.

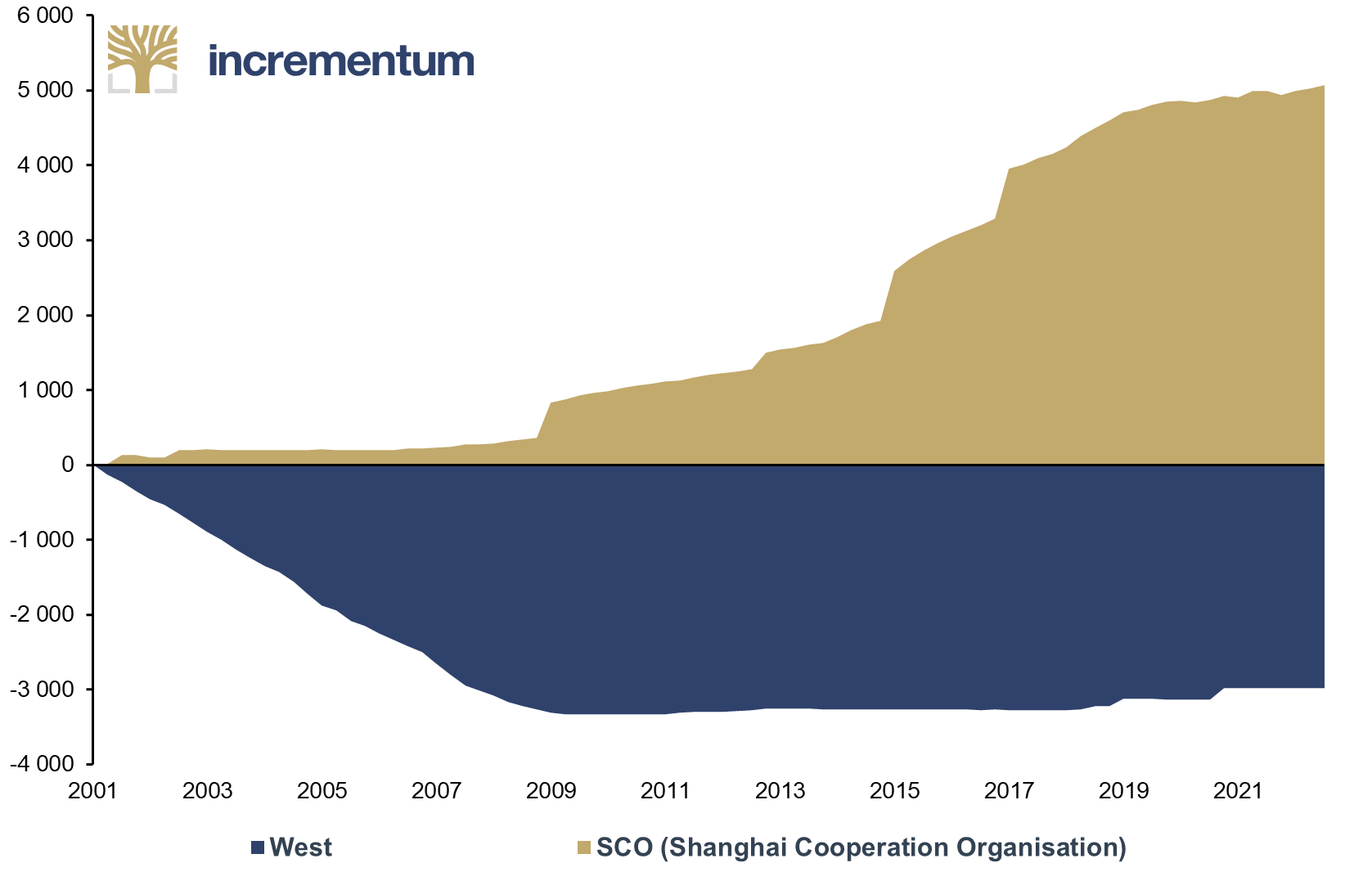

The SCO’s eight full-member countries consist of China, Russia, India, Kazakhstan, Uzbekistan, Kyrgyzstan, Pakistan and Tajikistan. Of these eight SCO members, five have been central bank gold buyers over the last 15 years: China, India, Russia, Kazakhstan, and Uzbekistan. These five central banks together purchased 3,343 tonnes of gold between 2010-2022, and furthermore were five of the top six central bank gold buyers in the world over this timeframe.

Cumulative Gold Purchases since Q2/2001, in Tonnes, Q2/2001-Q4/2022

Source: World Gold Council, Incrementum AG

Add in the remaining top-six central bank gold buyer over this period, i.e. Türkiye – which by the way is also an SCO dialogue partner – and the cumulative gold purchases by SCO members + Türkiye becomes 3,768 tonnes over 2010–2022.

Looking at the BRICS, we also see a striking overlap, with central banks from four of the five BRICS countries – Brazil, Russia, India and China – buying a cumulative 2,932 tonnes of gold over 2010–2022. There is also a long line of other countries interested in joining BRICS, such as Argentina, Algeria, Iran, Indonesia, Türkiye, Mexico, Nigeria, Saudi Arabia, UAE, and Egypt, many of which are also active central bank gold buyers. Adding to the strategic and geopolitical mix, the UAE, Saudi Arabia, Nigeria, Iran and Algeria are all members of OPEC. This interest is evidenced by recent comments from South African foreign minister, Naledi Pandor:

“On my desk, I suspect 12 letters. And I suspect other foreign ministers have had approaches from their own region…[Those that have] come out publicly. Saudi Arabia is one… United Arab Emirates, Egypt, Algeria, and Argentina, so it’s a growing list of Mexico and Nigeria. So, there’s huge interest worldwide. And once we’ve shaped the criteria, we will then make the decision.”

In fact, Russian Deputy Foreign Minister Sergei Ryabkov said recently that there are 16 potential applicant countries interested in joining BRICS.

Looking at the Eurasian Economic Union (EAEU), whose member countries are Armenia, Belarus, Kazakhstan, Kyrgyzstan, and Russia, we can see that EAEU members Russia and Kazakhstan together added 1,931 tonnes of gold over 2010-2022. Moreover, the EAEU is in negotiations to introduce free trade agreements with Iran, Egypt, UAE, China and Indonesia.

The overlaps between central bank gold buyers and China’s Belt and Road Initiative (BRI), a.k.a. One Belt, One Road (OBOR), are also striking. As a reminder, BRI is a Chinese initiative launched in 2013 to build a huge multi-country network of transportation, energy, and communication infrastructure to connect China with countries across Asia, the Middle East, Africa and Europe, so as to accelerate economic growth, trade, and investment across this network.

The initiative takes the form of land-based transportation routes, from China through Central Asia to Europe, i.e. the Silk Road Economic Belt, and sea-based transportation routes from China via Southeast and South Asia to the Middle East, North Africa and Europe, i.e. the Maritime Silk Road. Yet again, nearly all of the countries appearing on the top central bank gold buyers list over the last 15 years are also in one way or another connected to the Belt and Road Initiative.

While the parallels between the BRI and gold are striking, China’s thinking on this topic had already been telegraphed. In 2016, the SGE launched the SGE Gold Road initiative, proposing a physical gold trading route from China to Europe, which aims to “promote gold market cooperation between China and the countries along the ‘One Belt and One Road’ route”, and which would connect international gold supply chains to the Chinese gold market.

Following this in 2018, Hong Kong’s Chinese Gold and Silver Exchange (CGSE) proposed a gold trading corridor that would connect the CGSE and the CGSE’s bonded warehouse in the Qianhai free-trade zone, near Shenzhen, with precious metals traders and commercial users in countries along the OBOR routes, such as Cambodia, Singapore, Myanmar and Dubai.

The SGE and CGSE initiatives are similar in that they both aim to promote the integration of Asian gold markets along the Belt and Road countries. Both instances could be thought of as versions of a Belt and Road Gold Route idea, or a 21st century Silk Route but for gold, i.e. a Gold Route.

According to a Russian foreign policy statement from March 31, 2023:

“In order to help adapt the world order to the realities of a multipolar world, the Russian Federation intends to make it a priority to enhance the capacity and international role of the interstate association of BRICS, the Shanghai Cooperation Organization (SCO), the Commonwealth of Independent States (CIS), the Eurasian Economic Union (EAEU), the Collective Security Treaty Organization (CSTO), the RIC (Russia, India, China) and other interstate associations and international organizations, as well as mechanisms with strong Russian participation”

Western sanctions and Russian asset freezes have now jolted all nonWestern countries to sit up and realize that any one of them could become a sanction target of the US and its allies. So, these countries, such as Saudi Arabia, are motivated to join and align with alternative organizations and initiatives such as the SCO and BRICS for reasons of protection and safety in numbers, as there is more powerful representation from being in one or more of these grouping.

These same countries are also motivated to buy and accumulate gold, because they realize that the world is moving towards a new global system based on cooperationand not coercion, and that gold is undoubtedly going to play a part in such a new global monetary system and international settlement system, via initiatives to be launched by the very same organizations and initiatives (SCO/BRICS/BRI/EAEU) that these countries are scrambling to join.

The nonaligned are becoming aligned

In fact, it is not too far-fetched to say that many of the ca. 120 (!) nonaligned countries – those countries in the Non-Aligned Movement (NAM) – are now explicitly becoming aligned. As this alignment gains critical mass, expect it to accelerate and pull in countries across the Global South and the “non-West”.

This alignment could also put a strain on the relationships between the member states of the Group of Twenty (G20), which, remember, is a grouping of 19 large industrialized and emerging economies plus the EU. Starting with the G20, take away the EU and the G7 (Canada, France, Germany, Italy, Japan, UK and US) and you are left with the BRICS and seven other countries: Argentina, Australia, Indonesia, South Korea, Mexico, Saudi Arabia and Türkiye.

While Australia will always side with the G7, and possibly so too would South Korea, the remaining five nations are far more affiliated with the BRICS. Indeed, all five of the remaining countries – Argentina, Indonesia, Mexico, Saudi Arabia and Türkiye – have already expressed interest in joining BRICS.

Conclusion

It is now apparent that Western financial sanctions against Russia have sent seismic shocks across the geopolitical landscape and triggered many nations into examining how best to deal with these new-found risks and into questioning when and not if the world will become more multipolar. All of this is happening in a world in which gold has been flowing from West to East, thereby boosting gold holdings of the East at the expense of the West, while increasing the importance of Asian gold markets.

There is a huge and unmistakable overlap between the central bank buyers of gold and the countries that are members and aspiring members of institutions such as the SCO, BRICS, and China’s Belt Road Initiative. Russia, China and India are even actively facilitating discussions for more countries to align with SCO and BRICS. In effect, the nonaligned countries across Asia and beyond are now aligning into an alternative gold-anchored bloc. Countries are now taking sides, with the G7 countries and allies on one side and the BRICS/SCO-led coalitions on the other.

China via the SGE has the infrastructure in place to create gold pricing based on physical supply and demand of gold, and Russia’s proposal for a Moscow World Standard would be complementary. If and when they need to detach from the gold pricing of London and New York, China, Russia and their allies have a deep, liquid market of physical trading, physical settlement, physical vaulting and international linkages, to initiate a physically-led gold price discovery system.

When China and Russia restarted announcing updates on their gold reserves following Xi Jinping’s visits to Saudi Arabia in December and Russia in March, this was China and Russia symbolically saying: “We have gold, we have more gold than we’re saying, and we are going to use this gold in a new international system”. Given the high proportion of ‘undisclosed’ gold buying by central banks, many other countries may also not be showing all their golden cards yet.

Central bank buyers from these actively accumulating countries are holding gold as a geopolitical weapon and a monetary tool, knowing that gold can now become part of a new monetary system. These central banks want the gold price to be higher.

By definition, a showdown involves two or more sides who use all of their resources and power to bring matters to a head, to reach a conclusive settlement of an issue, or to reach a decisive outcome. In poker, a showdown refers to the last round of the game, when the players are required to all at once reveal their hands so as to declare the winner.

While we may not yet be at the final showdown, we appear to be entering this final round. This round could be triggered when the major Eastern powers and their allies, through the introduction of a gold-backed currency or gold-backed international settlement unit, force the West to react. That could then precipitate the showdown, where the countries on each side are literally forced to reveal all of their golden cards, that is, how much gold they each hold. With gold having flowed in vast quantities from West to East over the last two decades, it would appear that the East has the upper hand.

[1] The following section was written by Jan Nieuwenhuijs of Gainesville Coins.