Stagflation and a New Gold Standard – Exclusive Interview with Alasdair Macleod

“When fiat currency really does begin to fail, there will come a point where central bankers’ own pay will need to be secured. The last resort will be to come up with some sort of gold standard. The real question is, how long will it take until we get to that point?”

Alasdair Macleod

Key Takeaways

- We are now in a situation where we have a lack of economic growth and rising prices. This is temporary. The collapse of the purchasing power of paper currencies and what is actually driving that is what we should be thinking of.

- During the stagflationary period of the 1970s, central banks had to raise interest rates to as high as 20% in order to fend off inflation. This is impossible in today’s economy because of high levels of debt and deficits. This is made even worse by globalization.

- Central banks could be forced to recapitalize by increasing the value of their gold holdings significantly. This could usher in a new world monetary system based on gold.

- Central bankers seem to believe that small rate hikes could solve the problem, but the real problem is the amount of currency in circulation.

Alasdair Macleod is the Head of Research for Goldmoney. For most of his 40 years in the finance industry, he has been demystifying macroeconomic events for his investing clients. The accumulation of this experience has convinced him that unsound monetary policies are the most destructive weapon governments use against the common man. Accordingly, his mission is to educate and inform the public in layman’s terms about what governments do with money and how to protect themselves from the consequences.

Find him on Twitter at @MacleodFinance.

Ronnie Stöferle and Mark Valek conducted this interview with Alasdair Macleod by Zoom on April 2, 2022. We publish the highlights of the interview below. The full version is available for download here.

The video of the entire conversation, “Stagflation and a New Gold Standard”, can be viewed on YouTube here.

Ronnie Stöferle:

It’s my great pleasure to have my dear old friend Alasdair Macleod here as a guest for a special interview on the topic of stagflation. Alasdair, thanks for taking the time.

Let’s start with the official definition of stagflation. I don’t know if there’s a right or wrong definition, but I had a look at the definition by Investopedia, and it says:

“Stagflation is characterized by slow economic growth and relatively high unemployment or economic stagnation. Which is at the same time accompanied by rising prices. Stagflation can be alternatively defined as a period of inflation combined with a decline in the gross domestic product.”

Now, I know that your uncle, Ian Macleod, was the shadow chancellor in 1965, and he basically coined the term stagflation, but he had a slightly different interpretation, or I think the context was different. In what context did your uncle first use this term stagflation, and how did he define it?

Alasdair Macleod:

He invented the term basically to describe the economic situation at that time. And it was a mixture of falling productivity on the one side and rising wage inflation on the other side. So that was the original context in which stagflation was defined; but since then, people have taken it into the broader sense of describing a situation, as you rightly sort of indicated from the Investopedia definition. If you have an economy which is not doing terribly well and you have rising prices at the same time, it’s a combination of stagnation and inflation, so it’s “stagflation”.

I think that the modern interpretation shows an ignorance of economics, because it’s the Keynesians, in effect, saying that the only driver of prices is demand, consumer demand. Therefore, you now have a situation where you have a lack of economic growth or a recession and rising prices, which is completely impossible. But they have come to call this stagflation.

In other words, they see it as something which is essentially temporary. I don’t know whether you ever discussed what happened in Austria in 1921/22 with your grandparents. When we had a collapse of the Austrian crown?

The idea that the Austrian economy somehow was booming while this was going on is complete nonsense; but in Keynesian analysis, you cannot have a situation where you’ve got inflation, in other words rising prices, and a collapsing economy. So how do they explain that? I mean, it seems to me that one way or another, we are in the sort of crisis which is probably not best described as stagflation, except in the temporary sense. At the moment what we see is the dilemma of a global economy which is slowing in its growth; or at least the big locomotive, China, is certainly slowing big-time, and all the other economies are slowing as well. Yet, at the same time, we have rising prices.

Thus, stagflation, in the modern sense, actually does describe the current situation, but I think that’s temporary; and I’m sure that as this interview moves along, we will address the issue of why stagflation is temporary and that what we should actually be thinking in terms of is the collapse of the purchasing power of paper currencies and what is really driving that.

Mark Valek:

I think that’s a great introduction, so when it comes to the term stagflation, as you already described in the modern interpretation, we had this great example in the 1970s in the US, and it’s often referred to as the only example of stagflation. At the start of the 1980s, the US was able to get out of this kind of environment. How would you describe this? How was this able to happen, and do you think this could be happening again this time around?

Alasdair Macleod:

I think it actually gets to the center of the issue. At the end of the 1970s, Paul Volcker jacked up interest rates to unprecedented levels. The Fed Funds Rate went to close to 20%. This meant that the prime rate, which is a margin over that, was something like 20.5%. That had one specific purpose, which was to stop the incipient inflation from turning into hyperinflation. If they had not done that, we would have seen the destruction of the dollar, because, remember, we went off the gold standard or what was left of the gold standard at the beginning of the decade. That was a necessary action.

Now imagine the situation today. If they raise interest rates even to five percent, let alone 20 percent, the industries that are stuffed full of malinvestments are going to come unstuck. Which means that the banks will have to be rescued. Not only will financial collateral values be collapsing, but loans to industry and all the rest of it will start to become unstuck. The central bank will have to rescue the banks to rescue the economy. We’re talking about 5%, not 20%; and think of what a 5% interest rate does to government finances.

When you go back into the 1970s and 1980s, we didn’t have these huge budget deficits to finance. We had budget deficits, but they tended to be more cyclical than permanent. Now, not only are they permanent but they are unimaginably large; and you have governments, not just in America but all over the world, who seem to think that the money tree is there just to be plucked, and that they can borrow. They think they’re borrowing with impunity, to deal with their existing problems; but the problem is that the other side of inflation is debt, so just to look at debt is actually looking at the wrong thing.

You should be looking at the amount of currency and credit in circulation, because real money, which is gold, doesn’t circulate at all in this current environment. You’ve got to be looking at that and thinking: “What happens when the situation destabilizes?” Coming back to your question, I just cannot see how today anyone either has the mandate or the will to introduce an interest rate policy which is designed to kill inflation, in the way Volcker did.

Ronnie Stöferle:

I just got this book that I’m currently reading, Keeping at It, by Paul Volcker. It’s a good read, and he emphasizes the topic of trust and trust in the US dollar, why people trust gold. I found it pretty fascinating that Jerome Powell, in a recent hearing, referred to Paul Volcker as one of the greatest servants in the history of the United States. I think he was trying to sound like a “mini-Paul Volcker”, obviously, but I think we all know that, as you rightly said, it’s impossible to go back to those interest rate levels. However, for some reason, most market participants really think that now we’re seeing a big turnaround in interest rates. Seven to nine hikes in the next couple of months. I think we both agree that’s pretty much impossible within this monetary system and at this stage of the financialization of our economies.

But let’s briefly go back to the 1970s. From your point of view, what are the major similarities and also the major differences between the economy today and the economy of the 1970s, and do you think the situation at the moment is more serious or less serious than back then?

Alasdair Macleod:

Well, there are obviously huge differences between the economy now and in the 1970s, and I think one thing I would point out is the fact that today we are in a globalized economy. We are all tied into exactly the same policies. It was less so in the 1970s. You could have a situation where one economy was having trouble but there were other economies that were all right and some or other arbitrage came to the rescue of some of the economies that weren’t performing too well.

Now we are all going in exactly the same direction, and there’s globalization. People talk about globalization in terms of supply chains and the disruption that it causes, but the one thing they don’t look at is the globalization of money and currencies, and that is actually the problem. Everyone is tied into exactly the same interest rate policies and ways of managing their economy in terms of trying to suppress interest rates as much as possible. Keep the cost of government borrowing down and aim for a 2% inflation target, while at the same time fostering maximum employment. We are all on the same crazy spreadsheet, and that I think is the big fundamental difference between then and now.

Mark Valek:

In my view a very obvious part of the problem is that the whole system is plagued with debt, and I think this is basically a function of our debt-based currency system. We have to go deeper and deeper into debt because this whole system is built on debt, and this results in these exponential curves of currency supply and also of debt mounting higher and higher.

At the end of the 1970s, what happened was due to the fact that the gold price actually increased that much. This was kind of a recapitalization of the system. My question to you would be, do you think that a significant revaluation of the gold price could recapitalize the system, starting from central bank balance sheets? Because at the end of the day, in my view at least, the real equity of a central bank balance sheet is gold, right? Since the gold position in relative terms to the debt positions has shrunk significantly, it would be possible to basically recapitalize the central bank and, at the end of the day, the whole economy, if the central banks’ gold position were to increase significantly. What are your views on this thought?

Alasdair Macleod:

Undoubtedly, that is correct. I think that’s the end solution, because what we’re likely to see is a speeding up of the falling purchasing power of currencies. At the moment they’re sitting on the price of gold; they sit on it because it’s a rival in this fiat paradigm. But when fiat currency really does begin to fail, there will come a point where central bankers’ own pay will need to be secured, and so will the politicians’ pay. At that stage, the last resort will be to come up with some sort of gold standard. I think the real question is, how long will it take until we get to that point? My view is that it will actually happen quite rapidly from here, and the reason is that major central banks are already running into enormous financial difficulties on their own books, because they have taken on board massive amounts of government debt.

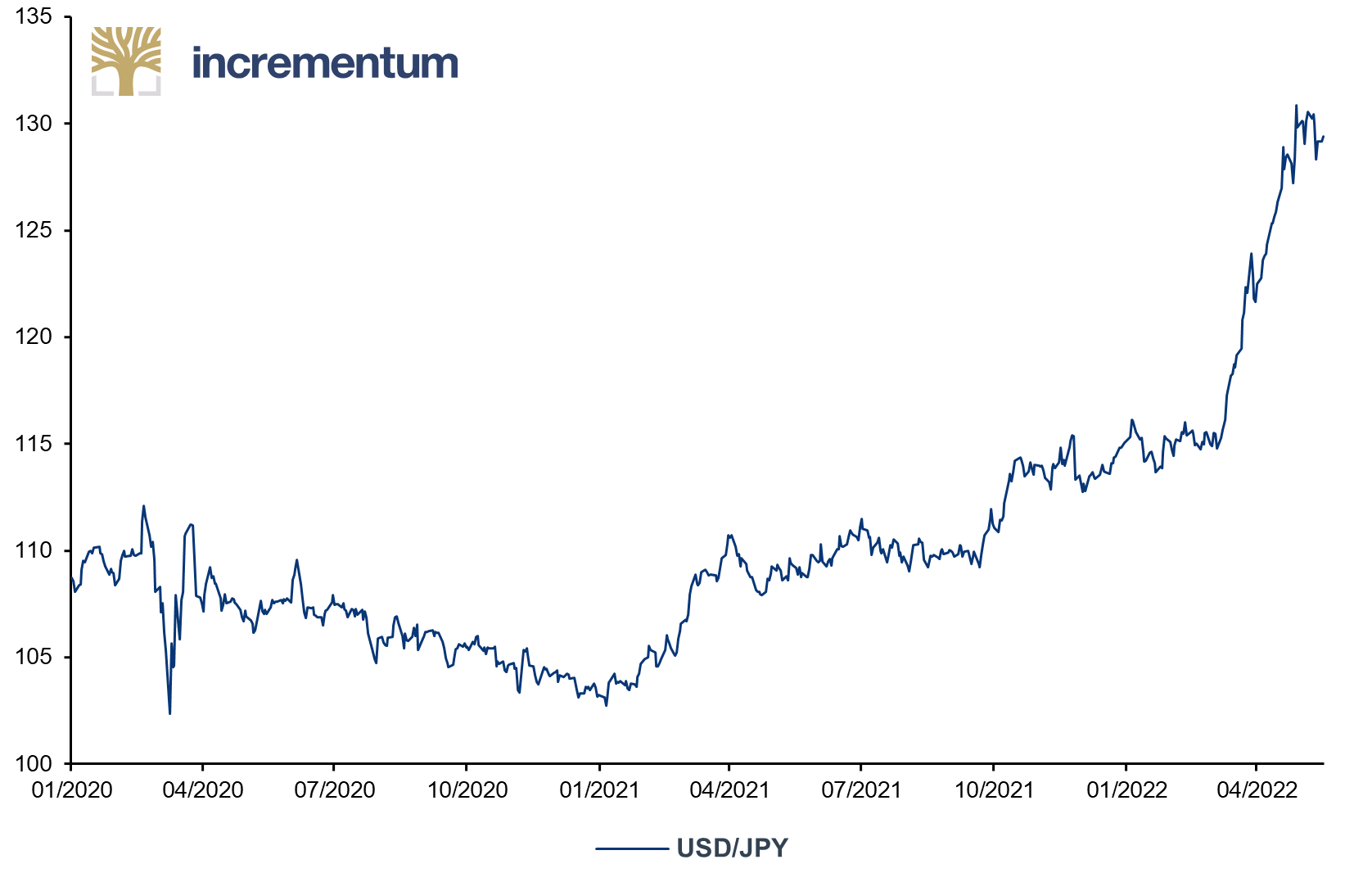

If you look at Japan, it’s not just government debt, it’s also corporate bonds and it’s also equity ETFs. They have done what a central bank shouldn’t do; their balance sheet is like 80/90 percent bonds now, rather than being the counterparty to currency. Which is really what a central bank should do. What happens as we see those rising yields? Obviously, all these central banks go into negative equity. They are already there, and what’s interesting is that as we speak, we see the yen appears to be in the early stages of a collapse.

USD/JPY, 01/2020-05/2022

Source: Reuters Eikon, Incrementum AG

In the last four or five weeks it’s gone from JPY 115 to the dollar, to this morning we’re looking at JPY 121–122. It really is a very serious fall in the purchasing power of that currency, and this reflects the overall financial situation and the fact that the Japanese central bank is in negative equity. Now, these things can be resolved, but the worst time to resolve a central bank in negative equity is when there is a financial crisis developing, and that’s roughly the combination that I see. The other real weakness is the euro system.

The euro system is potentially worse because there you’ve got the ECB. It’s now hugely in negative equity itself, and all its shareholders, who are the national central banks, are in negative equity as well, with a few very, very minor exceptions. Their banking system, if you look at the euro area G-SIBs, there again you have leverage – assets to equity – of well over 20 times. How are you going to resolve this situation when we see rising interest rates, when we see the ECB being forced to raise its deposit rate above zero? There are potential collapses looming.

To get back to your point about the role of gold, at some stage, unfortunately, you’ve got the French central bank, you’ve got the Italian central bank, the German central bank, and so on. They’ve actually got significant holdings of physical gold, or at least we are told they have. But quite a lot of their gold might be leased out; and this is a very serious issue, because when the fiat system fails, we will find out who actually has the gold. They are going to have to back their currencies with gold, and in the case of the euro I think we are probably going back to the Deutsche Mark and maybe one or two other currencies. The second-tier currencies will fail. I can tell you that because this revolves around trust. The Italian central bank has got a lot of gold. But can you imagine going back to the Italian lira? How much respect would the lira have? I mean, they can deal with it, but they would have to have a proper “gold coin standard” in order to make it stick. I think what we’re likely to see is, yes, gold will come back to underwrite the whole of the monetary system by being exchangeable for paper.

It will have to be, and it’s not just a question of doing what Germany did in 1923 with Hjalmar Schacht, where they said, “We are going to introduce a new standard but not actually make it convertible into anything”. This has got to be real this time in order for it to stick; and of course, the other side of it is that government is going to have to stop spending all this money on welfare and fancy projects and all the rest of it. They’re going to have to cut right back. It’s not going to be an easy transition from this Keynesian world back into the real world, where it’s the productive side of the economy that matters and government should be as small as possible. A lot is going to have to happen to get back to a situation where gold is backing a currency, turning a currency into a gold substitute. A lot has to happen before that is going to work.

Ronnie Stöferle:

I have so many thoughts to pick up on from your answer. What’s really fascinating is the fact that central bankers seem to believe that by making small rate hikes they will get the inflation problem under control again. If we look back to the hiking cycle from 2004-2006, the Federal Reserve did 17 rate hikes. But inflation only peaked one year after that. I think it’s interesting that it seems central bankers still believe that they have got everything under control, while the market is already telling us that things aren’t going so well. Basically, everybody is still blaming the energy shock and saying that it is mainly responsible for rising inflation. However, if you look at headline inflation and core inflation, the differential is quite low. It’s not only energy and food that is rising, it’s much broader.

In last year’s In Gold We Trust report, we wrote at length that we are seeing amonetary climate change and that this pendulum is now really swinging into the direction of rising inflation, and there’s actually quite a number of factors, for example this move from monetary to fiscal dominance. We’re seeing that central bankers now seem to have new mandates, for example, saving our planet, climate change and dealing with inequality. What other inflationary drivers do you see that the mainstream is missing at the moment?

Alasdair Macleod:

The thing that the mainstream is missing, more than anything else, is the increase in the amount of currency and credit in the economy. That is the root cause of it all.

Inflation isn’t rising prices, inflation is actually the expansion of the quantity of money. The thing that I think is amazing is that the FOMC (Federal Open Markets Committee) never mentions the quantity of money in its deliberations. They are always talking about prices rising here or temporary rises there or supply chain problems or all the rest of it. Those are the only things that get picked up by the people who are licensed by the establishment to manage money and to run banking licenses. They just literally follow this meme the whole way through, and the result is that the underlying cause is completely neglected. IIt is always the increase in the quantity of money and credit. Now, I don’t subscribe to the monetarist theory, on the basis that it is not the only thing that drives the purchasing power of a currency.

The other thing, which is actually desperately important, is how the public rate a currency. Now, I’ll give you an extreme example. If the public decide that irrespective of any change in the quantity of currency, that they don’t want to use it for transactions, then, rather like the Russians now finding out that the dollars and euros in their reserves are completely worthless, the public perception of the purchasing power of a currency, or its use value as a medium of exchange, is the factor that monetarists miss.

The thing is, fluctuations in the quantity of money and credit created the Austrian business cycle, in other words the periodic boom and bust that we see; and this periodic boom and bust is a very human thing, it’s bankers getting more encouraged by the initial stimulation of an economy, which comes from the central bank reducing interest rates, encouraging people to borrow, and eventually it builds up. Then you get to a situation where perhaps a bank has a leverage of, say, 10x or 12x assets to equity. Remember what I was saying about over 20 times in Japan and the euro area, so you can see how this is a cycle of events, and that’s the next one they’re going to have to try and save us from. The whole situation is completely misread. I look at it from another angle: What if Jerome Powell was actually to stand up and say, “The real problem we have is not supply chains, it’s not energy prices, it’s the excessive production of currency and credit, and that is the situation we’ve got to deal with.” I mean, that would be shock, horror – can you just imagine what would happen if he spoke the truth? Now, I don’t know how much he believes in money being the “driver” of the price of currency. I’m sure he believes a lot more than he’s letting on, but the one thing he cannot say is the truth, because it would destabilize the whole economic system.

Mark Valek:

Fascinating. Perhaps going back to the comparison between the stagflation of the 1970s and the current situation, one of the similarities, I would argue is – and we wrote this in last year’s report – the new ice age between East and West. In the 1970s we were in the midst of the Cold War, obviously, and unfortunately it seems we are back there. We even have hot war now, so I think this comparison is also very interesting from a geopolitical standpoint and very relevant also to the global architecture of the currency system and the financial system. What are your thoughts in that regard? I mean, I’m obviously alluding to de-dollarization and especially to what I think was really a key event, the freezing of Russian assets. What do you think will be the effects of these developments?

Alasdair Macleod:

It’s a very dynamic situation. I mean, between my commenting here and this interview actually coming out, you never know, it might all change. But I think the underlying problem is that Ukraine is a proxy war. That’s the first thing. The real enemies in this are, on the one side Russia, on the other side NATO, and particularly the domination of NATO by America. This is essentially the continuation of a financial war by other means – I think that’s the way to look at it. The sanctions that have been imposed on Russia are undoubtedly going to cause great pain for the West, and we’re seeing this with oil prices. As we speak, US oil is $109.50 per barrel, and that’s up recently from sort of $60-$70, something like that. This is a very serious impact. There are other things happening, as well. Interestingly, China seems to be backing off a little bit from its partnership with Russia, and that’s being put about by the people who interpret this as China’s being worried that there may be sanctions extended to Chinese companies.

Sinopec, for example, has stopped or put a temporary hold on a joint project, a refinery project, with Russia, but I think this is another aspect of a huge global financial war. If you look at it in that context, the Chinese economy itself is now beginning to struggle. It’s a different sort of struggle from what we’re seeing in the West. I think what we’re seeing in China is actually similar to the situation at the end of the 1920s and into the early ‘ 30s. You have got a property bust which is slowly coming through, and the result of that is that international money is tending to leave China rather than continue to go into China. So China, is more worried that capital flows going out of China than about sanctions in the direct sense.

You can see that this is a very complex situation, and there are a number of ways in which it can evolve. My view at the moment is that the way it is evolving is that it will make Putin more desperate. I don’t think you’re going to see a regime change tomorrow, as Biden might hope. You’ll have a leader who’s going to get more and more desperate. The one thing he cannot do is back down, because to back down is to admit defeat, and I think this is the point about his change of policy over Ukraine. Apparently, he’s now no longer focused on taking over the whole country but rather on taking over the borderline of the Sea of Azov and joining Crimea with Donetsk and so on. So, he has a lot less ambition and he can then call an end to the “special operation”. That, I think, is the way he’s playing it, but we’re not going to stop putting pressure on him by saying, “Well done, we’ve achieved our objective, we’re going to back off and remove the sanctions on central bank reserves and people who are not directly related with president Putin but might be”, and so on.

I just don’t see how at the moment that we’re going to back off quickly, even if Putin achieves his new objective, so I’m afraid the situation is just going to get worse and worse, and I can see that a more desperate Putin will not only insist that the protagonists in the West pay for their oil with rubles, which echoes the Kissinger-Nixon agreement with the Saudis which created the petrodollar in 1973. But also, the question now is gold, because it’s been rumored – or at least I think there was a statement from the chairman of one of the subcommittees in the Russian parliament – that they would accept gold as payment.

I’m sure they would accept gold, but this is something which can be intensified; and at current prices, Russia can discount its oil to India, China, whoever else wants to take it, even down to below $60 a barrel, and still profit. The idea that the Russian economy is under pressure is actually wrong – yes, obviously it is under pressure, but the sort of pressure to destabilize it, I don’t think so. It’s actually a lot stronger than the West generally thinks; and remember, the West got the Soviet economy completely wrong before the Berlin Wall fell.

All the intelligence was that the Soviet economy was strong, so the economic advice behind their intelligence was rubbish. So now we’ve got a situation that I’m afraid is going to get worse before there’s any chance of it getting better, in terms of the supply of commodities and the financial situation. And this to me has always been a financial war.

It has now turned into a financial and commodity war, and we’re not going to walk away from winning. It’s going to be a Pyrrhic victory. If we’re lucky, we will win in the sense that we’re the last one standing, but that’s about it; and this is not good when you’ve got back channels between America and Russia, America and Germany and the UK, not working. In other words, the chance of this escalating into something completely out of control in the military sense should not be dismissed.

Ronnie Stöferle:

I agree, Alasdair, and it’s a frightening situation when your kids ask you if there’s a third world war going to start soon. I think you recently tweeted out that Russia’s debt to GDP is just under 25%, which is the lowest for the OECD countries. I think the average there is above 110% debt to GDP.

But what I would like to ask you is, we saw that basically with a stroke of a pen, the West took Russia’s FX reserves and made them completely worthless – $630bn. Isn’t that basically the strongest case for gold for every central bank on the globe that has ever been made? I mean, if you’re somewhat critical of the United States and if you, as a central banker, want to avoid counterparty risk, then obviously there are only very few choices left; and I think the primary choice is probably gold.

Alasdair Macleod:

I would agree with that entirely, and the situation is even more alarming than you have just stated, because the point about gold is that it’s nobody’s liability. You can always use it as money. The fact that we don’t use it as money is because we value money more than we value currency, and we probably value currency more than we value a bank deposit account.

In terms of the hierarchy, gold is right up there, and make no mistake about it. Not only that, but legally that is the situation as well, and this is a point people miss. You know the thing about gold is that you can exchange it, you can use it as money, and money escapes the criminal recovery process that you have with any other asset. I mean, if I steal a painting from you, then I have committed a crime. If I pass the painting on to someone else and that person doesn’t know it’s stolen, you can recover it off that someone else, no compensation required. That is what the law says, and it’s common more or less throughout the world. But when it comes to money or currency, if I steal a gold coin off you and I then go and spend it somewhere, and the person who takes that money takes it in good faith, not realizing that it was stolen, he can pass it on and you can’t recover it.

Gold still has that fundamental difference, which nothing else has, not even CBDCs, not even cryptocurrencies. So, we’re talking about the top, the real top, top asset; and this has been brought out very, very clearly by the West’s actions against Russia.

I would go further than you suggested. Imagine that you’re a central bank, you might even be the Austrian National Bank, and you sort of think, “Hold on, I have got x tonnes stored with the Federal Reserve; I have got x tonnes stored with the Bank of England; I think I’d better get that back under my control, because look what they’ve done.” I don’t know whether Russia’s got any gold in terms of market liquidity in the Bank of England vaults. We’re not given that information; but if they have, that’s basically been frozen; so every central banker will be saying, you know, we really need to get our gold back under our control; and even if they haven’t got storage facilities, they’re going to start building them damn quickly. So this, was a major move, and I think it will turn out to be a major mistake by the West. I mean, going back to the Second World War, the Bank of International Settlements still operated as a bank, as far as the Nazis were concerned. It took a neutral position, as indeed Switzerland did. But now, none of the central banks that store earmarked gold on behalf of other central banks are taking that position, and it started with the Bank of England, with Venezuela’s gold.

We were told by the Americans, don’t give Venezuela back its gold; so what did the Bank of England do? It rolled over and said, right, we’re not giving Venezuela its gold. This is not the role of a custodian, and we’re seeing these fundamental changes, which I think have got unintended consequences way down the line. And there is another thing, Ronnie, and that is, there was an analyst called Frank Veneroso who gave a speech in Lima, back in 2002, concerning gold leases from the central banks. He concluded in that speech that central banks had probably leased out between ten thousand and fifteen thousand tonnes of gold – fourteen thousand, I think, was the exact figure. Which had become the ornamentation of Indian ladies, you know, and the central banks weren’t going to get it back. Now, at that time 15,000 tonnes was roughly half the total world central bank gold reserves. I don’t know what’s happened today; I would hope the situation hasn’t deteriorated; but you can be sure there is a lot of gold out there on lease. Now, not even assuming that that gold is gone forever, if it does come back, I don’t think central banks are going to be releasing it. So there’s going to be tightness in the market, which is going to do a lot of damage to fiat currencies. There’s an old saying, “The market always wins”, and I think that’s what we’re going to see.

Mark Valek:

That’s so fascinating, and I think there’s a lot of agreement from Ronnie and myself with you. When we think about this kind of revaluation, which probably will have to happen to some extent, we see it being forced upon by the market, as you just said, perhaps even kind of in a legislated way. But what do you think would be a price level that would have to be achieved, so that the system could keep on working?

Alasdair Macleod:

I never give a price target, and for a start, experience has told me that I never get it right. The second thing is that I think looking at it that way is actually looking at it from the wrong end of the telescope. Really, what we’re talking about is not the gold price rising but the purchasing power of currencies falling, so really, your question should be, if I may venture to suggest, how far down do you see currencies’ purchasing power collapsing? And I can see that, without action, they will become completely valueless. Coming back to the way you phrased the question, that means an infinite price of gold, which could be the reciprocal of valuelessness in a paper currency. But I don’t think it’s going to quite get there because, as I said earlier, I think that nations will be forced to back their currencies with gold.

It’ll have to be done credibly, and the only way to do it credibly is to reintroduce, if they haven’t got it at the moment, gold coin, and make that exchangeable for currency notes at the central bank. If you have a stash of Austrian shillings, say, under a new currency arrangement, rather than euros, you can take it to the central bank, and you can say, “I have got a hundred thousand shillings”, or whatever the figure is, and “I want coins” in return for it; and the central bank will be obliged to supply those coins to you.

That I think is the endpoint, and when that happens, I don’t know. It’s a pain threshold problem; I think it comes to the point where the Keynesians throw in the towel, let’s put it that way. On the one hand you’ve got the Keynesians who are saying, “Oh, this is impossible to understand. We don’t understand it, this is completely wrong, stimulate more”, or whatever they come up with. And you’ll have the politicians and the central bankers who are in the practical situation of finding that their currency is disappearing down the plughole, becoming worthless. How do we stabilize it? I know that we’ve turned our backs on gold since 1971, or at least the Americans have forced us to do so. But the only way we can stabilize this is to return to gold; and whether that’s with gold, say, at a hundred thousand dollars an ounce, a quarter-million dollars an ounce, or ten thousand dollars, I honestly don’t know. But I think it’s going to be further down the rabbit hole than we would think possible at this moment.

Mark Valek:

I could imagine. I mean, I actually stated that on Twitter a few weeks ago. That, getting back to Russia, that would be a kind of solution for their problem. They have the gold, and they are in the desperate situation of already having very high inflation. If they really would consider such a thing, they would have to go to some kind of real circulation of gold; and as I said, they could do it, and they could also probably do it politically. I’m not an expert on that, but they would have to somehow opt out of the IMF, right? Because the IMF currently is forbidding you to do such a thing; but at this stage, why shouldn’t they do that? Also, they’ve been pushed out of every international organization I can think of. Why shouldn’t they leave the IMF? I don’t know if that’s a realistic option; any thoughts on that?

Alasdair Macleod:

Yeah, I agree with you entirely, and I would go slightly further and say that my information – I can’t verify this – is that actually Russia has got a lot more gold than it declares in its reserves. As one of the major producers in the world, I mean, that statement shouldn’t be too surprising. Also, we have seen that President Putin is a “gold bug”, if I can put in those terms, or appears to be. So yeah, that’s certainly possible; but the problem is you have to get over the overwhelming global establishment consensus, and that is that the way to manage an economy is to have the flexibility to be able to increase the amount of currency and credit in the economy as the primary means of managing the economy.

Now, if you’re going to go the gold standard route, then effectively, you’re turning your back on that. You’re saying the economy is not the government’s affair; it’s the private sector’s affair and we should, as much as possible, ensure that we don’t intervene. So we’re talking about a change in the way in which government views its own economy, but let us posit that if the change is accepted in Russia, then they’ve got the economy which makes this eminently possible. I mean, as Ronnie said earlier, their level of government debt is closer to 20% than 25%, so you’ve got a government which has got very little debt, as well as an income tax that is a flat tax at 13%. They don’t have the respect for property rights that I would like to see, but that could be dealt with.

This is an environment, actually, where they can quite easily introduce a working gold coin standard, not just on the back of the existing reserves, but on the back of more reserves which they could declare and that actually could be the next stage. At some stage, I think Russia might drop a bombshell on us and say: “Do you know what? It’s not 2,000 tonnes, we’ve got 5,000 tonnes”, or whatever the figure is. I mean it would work, because we’re not die-hard Keynesians, but the die-hard Keynesians who run the world have a problem and so, incidentally, do the monetarists, because the monetarists are inflationists, as von Mises realized when he spoke to Milton Friedman at the Mont Pelerin Society way back whenever it was, I think it was in the late 1960s, early 1970s.

Ronnie Stöferle:

I just found a great quote by Mises regarding the wishful thinking around unlimited government, and he called it the “Santa Claus principle”. I don’t know if you’re aware of that, but he said:

“An essential point in the social philosophy of interventionism is the existence of the inexhaustible fund, which can be squeezed forever. The whole system of interventionism collapses when this fountain is drained off, the Santa Claus principle liquidates itself.”

I think that’s a very good summary, basically, of the discussion that we just had. Mark, is there anything else you want to ask Alasdair?

Mark Valek:

Alasdair, I want to say thank you very much for joining us. It was a great pleasure and looking forward to keeping in touch and following your great research on gold money.

These were the highlights of our interview with Alasdair Macleod. The full version is available for download here.

The video of the entire interview, “Stagflation and a New Gold Standard”, can be viewed on YouTube here.