Stagflation 2.0

“It was the biggest inflation and the most sustained inflation that the United States had ever had.”

Paul Volcker

Key Takeaways

- In this chapter, we take an in-depth look at the topic of stagflation, provide an outline of precedents from the recent past, venture a look into the future, and then analyze the concrete consequences for portfolio construction.

- Historically, the last pronounced stagflation phases occurred between 1970 and 1983. These were made possible by a liquidity overhang, which had its origins in an excessively loose monetary policy, and were triggered by oil shocks caused by geopolitical tensions.

- While some parallels exist today with the environment of that time in terms of monetary and geopolitical policy, certain circumstances are significantly different. In particular, high indebtedness makes a rigorous monetary policy to combat inflation virtually impossible.

- Our baseline scenario is that we will experience several waves of inflation in the coming years, which will significantly change the investment environment.

- The disinflationary environment that prevailed for decades has strongly shaped investors’ asset allocation. Stagflation is the blind spot for most balanced portfolios. Precious metals and commodities investments can be excellent additions to portfolios in this environment, although there are some pitfalls to consider.

In the middle of the year 2021, the time had come. The monetary policy Elysium, an inflation rate of 2%, was finally achieved on both sides of the Atlantic. But inflation rates did not stop at the 2% mark. Without pause, one percentage mark after another was broken and numerous new decade highs in inflation rates were reached. The ketchup was out of the bottle.

However, central bankers initially dismissed the trend, saying at the top of their voices that inflation was merely transitory. Anyone who took a different view was dismissed as a crash prophet. But the narrative of merely temporarily elevated inflation inevitably began to crumble the longer this “transitory” lasted. Only in Frankfurt has it not yet been possible to completely break away from this narrative, especially not in practice.

In order to give the rising inflation a positive connotation after all, reference was recently made to the strong economic growth, which is supposed to be partly responsible for the inflation. However, while the growth figures were above average, mainly due to the Covid-19 induced base effect, they have now already clouded over noticeably, while inflation rates continue to soar.

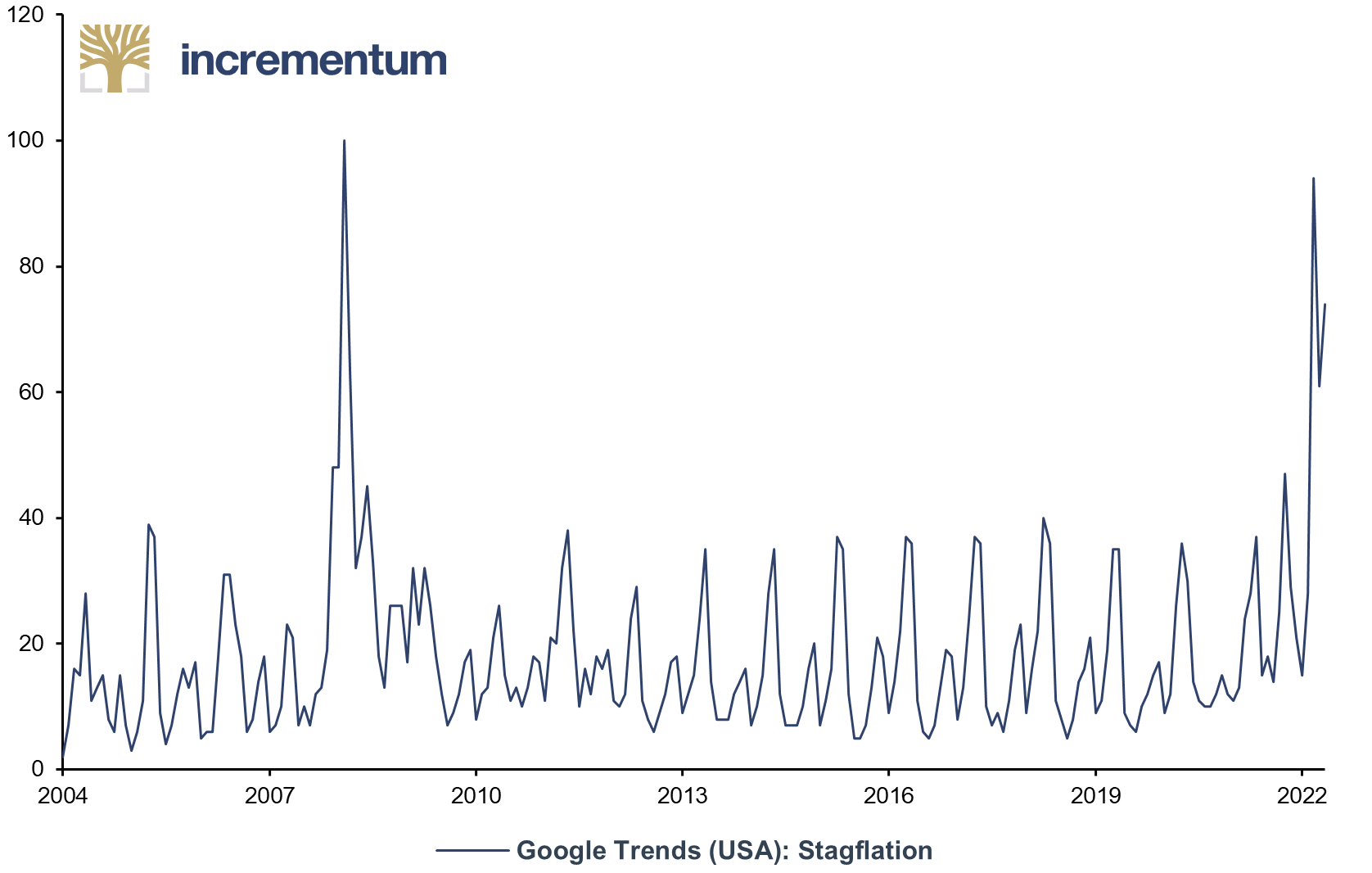

The Russian invasion of Ukraine now represents the next fundamental game changer after the Covid-19 crisis. It seems as if the world is slipping seamlessly from one exceptional situation into the next. Is the war now threatening a stagnant economy with rising inflation? As the frequency of Google searches for the term “stagflation” suggests, more and more people fear precisely this scenario.

Google Trends (USA): Stagflation, 01/2004-05/2022

Source: Google, Incrementum AG

In this chapter, we will therefore take an in-depth look at the topic of stagflation, provide an outline of precedents from the recent past, venture a look into the future and then analyze the concrete consequences for portfolio construction.

Stagflation – Definition and Economic Policy Views

The term stagflation refers to the economic state in which economic stagnation and noticeable inflation coincide. The term was coined by the British Member of Parliament and later Secretary to the Treasury Iain Macleod, who first used it in 1965. He employed it again in the summer of 1970, when inflation in Great Britain had reached the 6% mark and the economy shrank by 0.9% in Q1/1970. During the stagflationary 1970s, the term entered common usage.[1]

The classic stagflation definition is based on four pillars:

- High inflation

- Low or negative economic growth

- High unemployment

- Growth below potential growth

The coincidence of economic stagnation with increased inflation was considered impossible according to the prevailing theory in the 1960s, which clung to a simplistic view of the Philips curve, which postulates an opposite dependence between unemployment and inflation. This was because a cooling economy would release workers, causing wages and inflation to begin to fall. By contrast, only a booming economy would be accompanied by rising wages and permanently high inflation, according to the generally accepted thesis at the time.

Criticism of this Keynesian view was voiced as early as the late 1960s by Edmund Phelps[2] and Milton Friedman[3]. They argued that there is no long-term trade-off between inflation and unemployment. Rather, over time, loose central bank policies create the conditions for lower real economic growth and higher inflation, i.e., stagflation. This is because a low-interest-rate policy would make it more difficult to build up the capital stock and thus weaken economic growth.

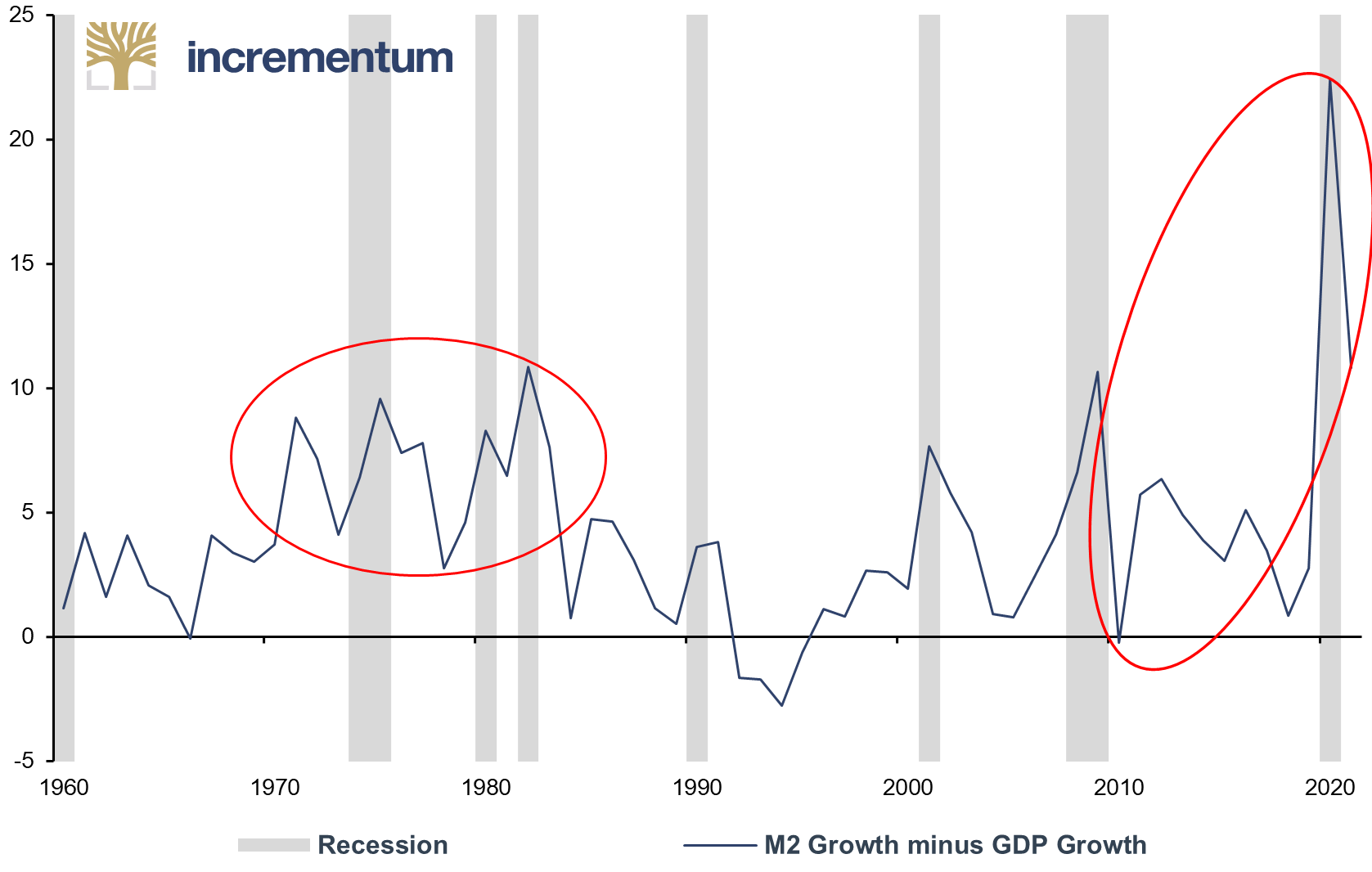

Representatives of the Austrian School of Economics saw the expansionary monetary policy – in the 1960s, the annual growth rate of M2 increased from 3.7% in 1961 to 8.3% in 1968 – as the main reason why the boom triggered by it must inevitably end in a bust. The positive discrepancy between money supply growth and real economic growth caused a monetary overhang which unloaded in several waves of inflation in the 1970s and early 1980s.

M2 Growth minus GDP Growth, in %, 1960-2021

Source: Reuters Eikon, Incrementum AG

The stagflation of the 1970s heralded the triumph of monetarism at the level of economic theory. One of the key insights of the Chicago School around the charismatic economist Milton Friedman, who was awarded the Nobel Prize in Economics in 1976, was that central banks must exercise rigorous control over money supply growth in order to prevent inflation or tame high inflation. It was only on the basis of this quantity theory of money with the well-known equation MV = PQ that the Federal Reserve under Paul Volcker succeeded in bringing high inflation under control in the early 1980s, thus laying the foundation for the resurgence of the US economy.

The slowdown in money supply growth was not painless, however. As a result of the sharp rise in interest rates, the US economy plunged into two successive severe recessions in the early 1980s. The high interest rates, which were the prerequisite for curbing money supply growth, were so unpopular that Paul Volcker was even threatened with death. Nevertheless, he stuck to his tough course and was later celebrated for it by investors and is revered by monetary policy hawks to this day.

Despite this success, monetarist ideas fell behind over the years. A notable example is the evolution of the ECB’s monetary policy strategy. At the instigation of the Deutsche Bundesbank, the ECB was given a two-pillar strategy, one pillar of which was the inflation target and the other a money supply target. The M3 money supply was to grow by no more than 4.5% p.a., it said. But this money supply focus became less and less important over time.

Keynesian economists also partially turned away from the Phillips curve after the 1970s. Instead, the inflation expectations of the population were given a high priority. The widespread view today is that as long as inflation expectations are anchored in the low range, there is no danger of employees triggering a price-wage spiral by demanding high wages to compensate for their expected real wage losses.

Low inflation rates thus become a self-fulfilling prophecy. To put it bluntly: As long as no one believes that prices will rise across the board, they will not rise. The monetary side of the inflation equation thus becomes almost irrelevant; expectations are (almost) everything.

The academic debate on the appropriate mix of fiscal and monetary policy measures to combat stagflation also began early. The later-Nobel laureate Robert A. Mundell presented his proposal as early as 1971 (!) , i.e. immediately after the end of the first stagflation period in 1970: “The correct policy mix was a reduction in the rate of monetary expansion (perhaps best achieved by a credit ceiling) combined with a tax reduction. This would have stopped the inflation rate without causing a depression”[4]. At least in terms of monetary policy, however, the reins were kept too loose for far too long.

In the present, the application of this mix of measures – interest rate hikes and budget deficits – is hardly feasible due to significantly higher levels of debt. In the 1970s, for example, total debt (government + companies + private households) in relation to economic output was not even half as high in the USA as it is today. Significant interest rate hikes today would therefore not only cause a sharp recession but also a veritable debt crisis.

Stagflation 2.0 – A Proprietary Definition

The classic definitions of stagflation are largely qualitative and thus vague. To make it easier to operationalize, we want to provide our own objectively measurable, quantitative definition, which we also keep deliberately lean by including the two main factors, economic growth and inflation.

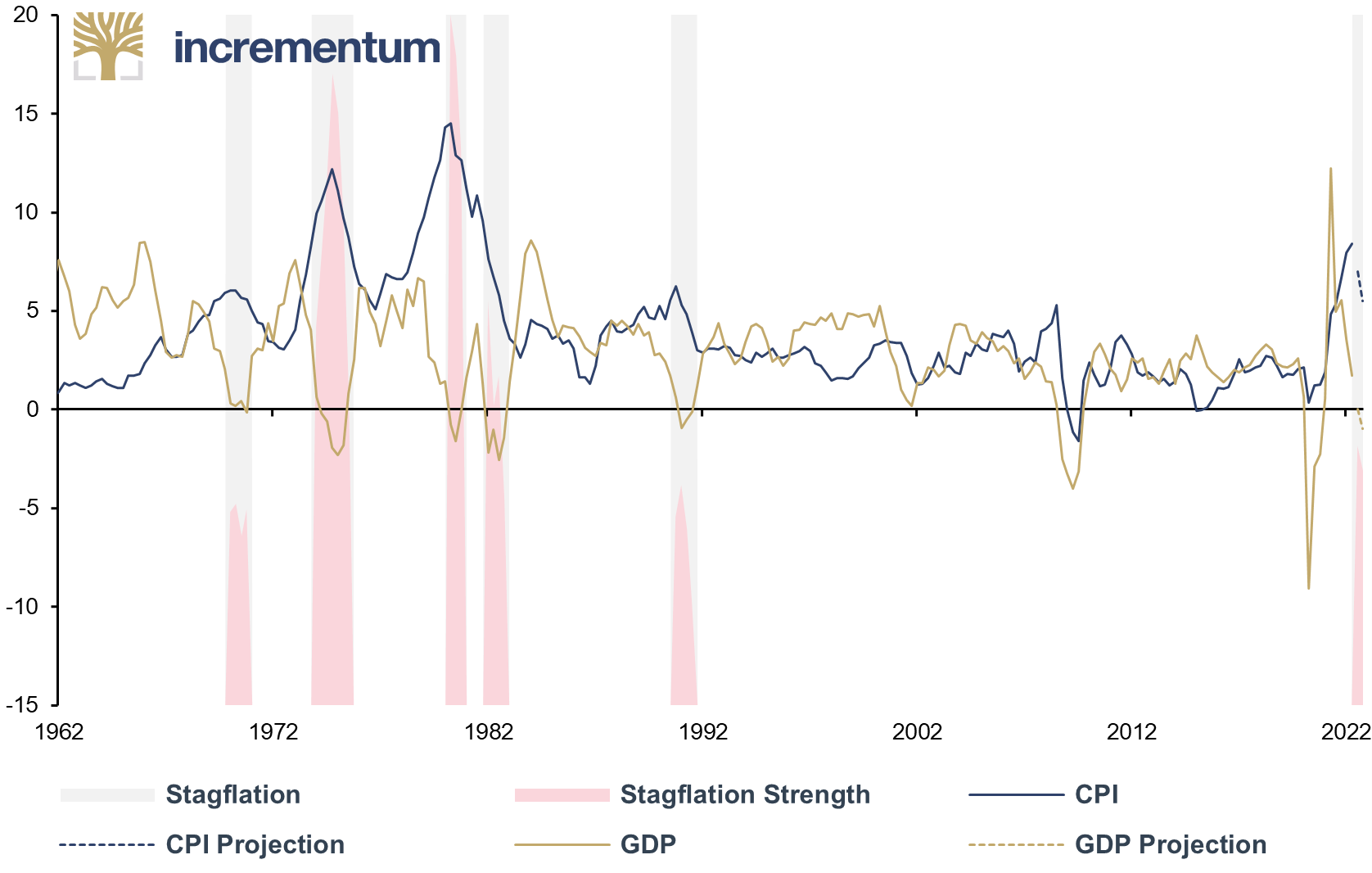

We define an economy as stagnant if real economic growth is less than 1% year-on-year. We consider inflation to be elevated if it exceeds 3% year-on-year. We collect these data on a quarterly basis. Both conditions must be met for at least two consecutive quarters in order to declare stagflation.

In addition, we have calculated stagflation strength, which we define as the sum of the deviation of the two variables inflation and GDP growth from their respective targets, assuming that our proprietary stagflation definition holds. The scale is then normalized so that the maximum value of stagflation strength is 1.

US GDP, US CPI, and Projections, yoy%, and Stagflation Periods, Q1/1962-Q4/2022e

Source: Reuters Eikon, Incrementum AG

Based on this definition, there have been a total of five stagflationary phases in the USA over the past 60 years. Four of them took place over a period of 14 years between 1970 and 1983, and another weak stagflation occurred in the early 1990s.

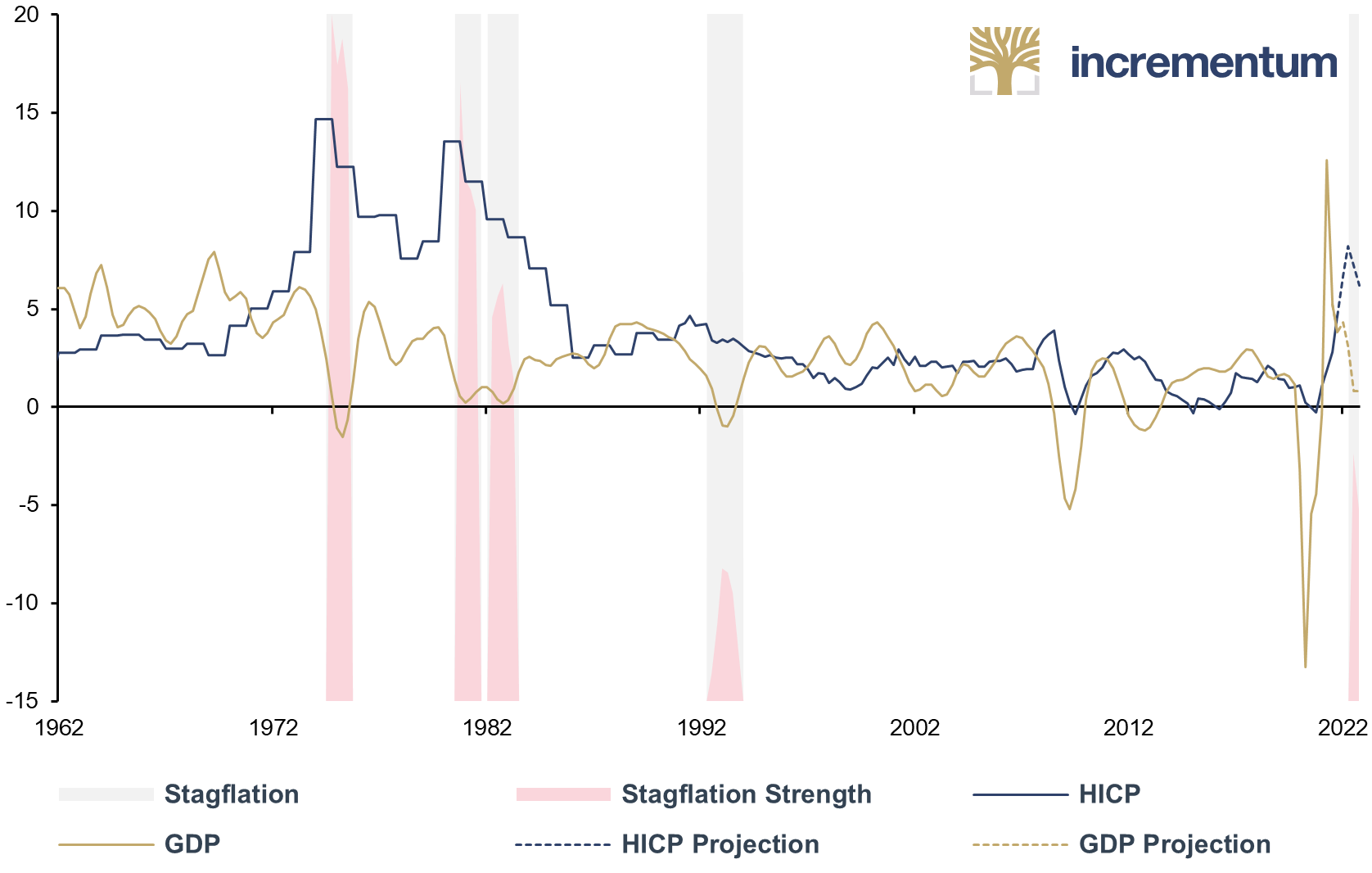

The picture is quite similar within today’s euro area (EA-19). We register three phases of stagflation between 1974 and 1983, and the euro area also fell into a weak stagflation in the early 1990s.

Euro Area GDP, Euro Area HICP*, and Projections, yoy%, and Stagflation Periods, Q1/1962-Q4/2022e

Source: Reuters Eikon, Incrementum AG

*Quarterly data available since 1991

The pronounced periods of stagflation in the 1970s and early 1980s were triggered by supply shocks. As a result of geopolitical tensions that were obvious to everyone, the public debate initially focused exclusively on supply shocks as the cause of stagflation. Little attention was paid to the monetary dimension. The fact is, however, that without a marked monetary overhang as a result of a previous excessive expansion of the money supply, a rise in the general price level to such an extreme extent would have been inconceivable. The stagflation phase of 1991/1992 also follows this pattern, because it was preceded by the oil price shock in 1990 resulting from the Iraqi invasion of Kuwait.

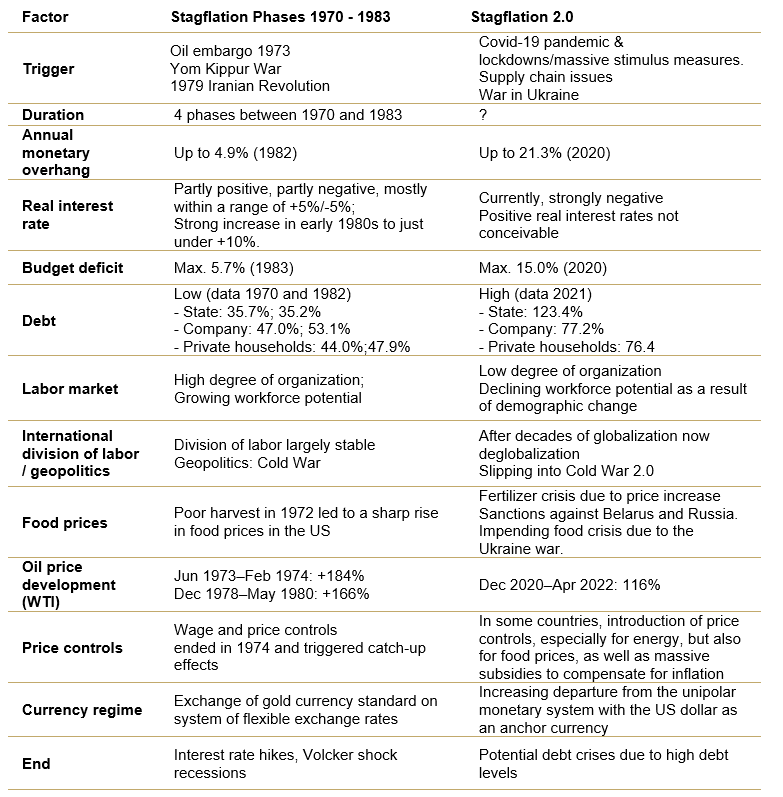

Stagflation vs. Stagflation 2.0 – A Comparison

“History does not repeat itself, but it rhymes!” Into these words Mark Twain poured the insight that many things repeat themselves in the course of history, but never exactly one to one. Every era has its own peculiarities, despite some similarities. What the stagflation phases of the 1970s and the early 1980s have in common with the emerging Stagflation 2.0, apart from the coincidence of a weakening economy and an elevated inflation rate, and what separates the historical original from the new edition fifty years later, we contrast in the following table for the US:

Source: Incrementum AG

Where Do the US and the Eurozone Stand?

Let us recapitulate: According to our definition, for stagflation to occur, the two criteria of an inflation rate above 3.0% and economic growth below 1.0% over a period of two quarters must be met simultaneously.

The latest growth rates continue to be strongly influenced by the Covid-19-related base effect, which distorted both inflation rates and economic growth upward in 2021. In the case of inflation rates, the base effect, which was mainly due to the marked drop in energy prices in the first three quarters of 2020, has largely been overcome. The base effect on economic growth, on the other hand, was barely addressed and is still having an impact in 2021 due to the numerous lockdowns.

Let’s now take a closer look at the current stagflation situation in the US and the euro area.

USA

Inflation at 8.3% (CPI, April 2022) is significantly above our 3% mark, and has been consistently so since April 2021, meeting the minimum 2-quarter length requirement. Even the core rate for the PCE Index, the Federal Reserve’s preferred inflation indicator, is well above this mark at 5.2%, also since April 2021. Moreover, one-year inflation expectations have climbed from 3.4% to 5.4% in a year, and the much less volatile five-year inflation expectations have risen to 3.0%. A rapid abatement of inflationary pressure is thus not to be expected.

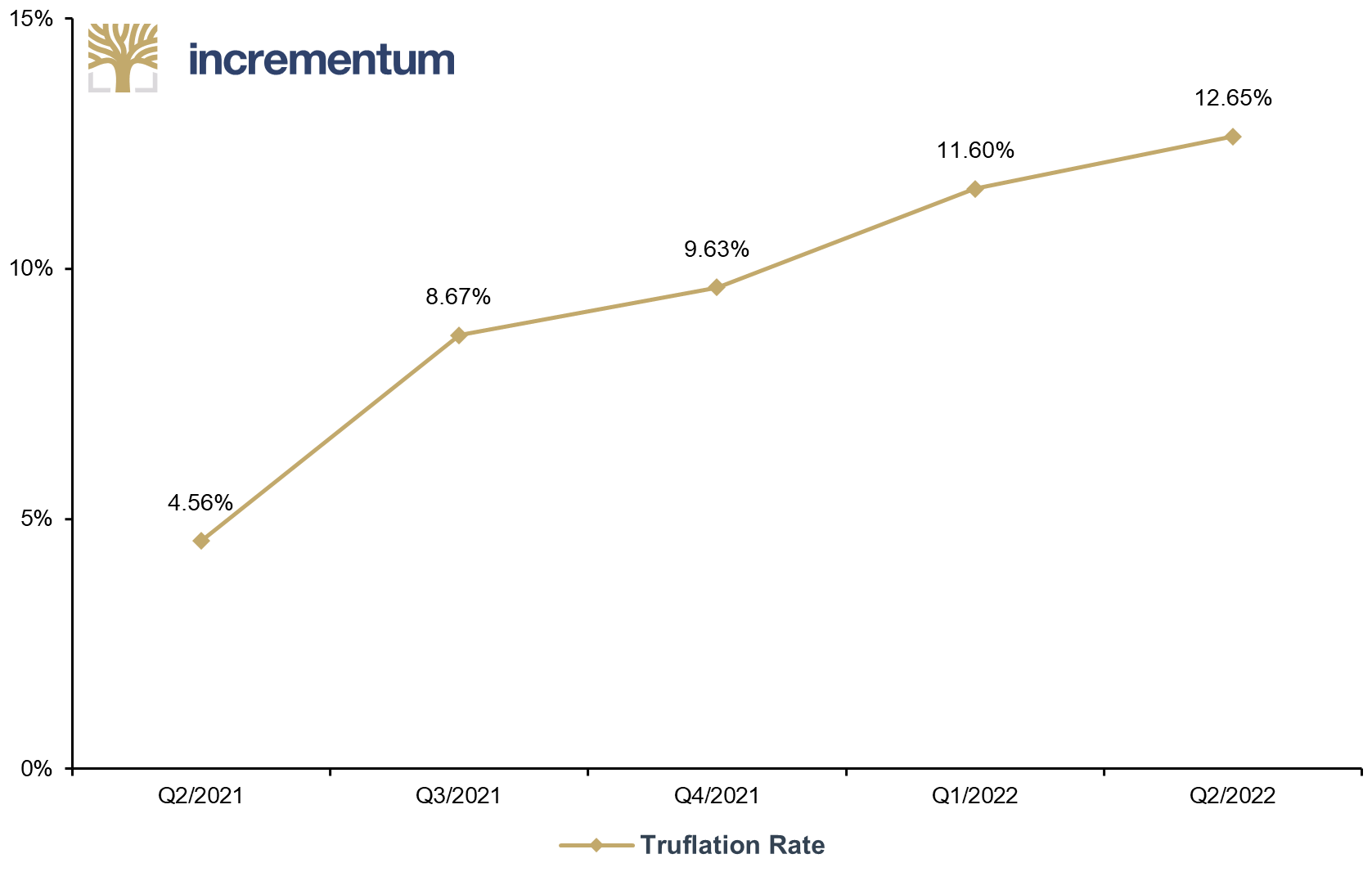

If the official inflation rates are already high, the price increases experienced by many citizens in their everyday lives could deviate significantly upwards from the official data. Truflation, a provider that calculates inflation based on real-time data, shows significantly higher inflation rates. In mid-April, the Truflation inflation rate stood at 12.7% year-on-year, with a serious 26.4% year-on-year increase in food prices.

Truflation Rate, Q2/2021-Q2/2022e

Source: Truflation, Incrementum AG

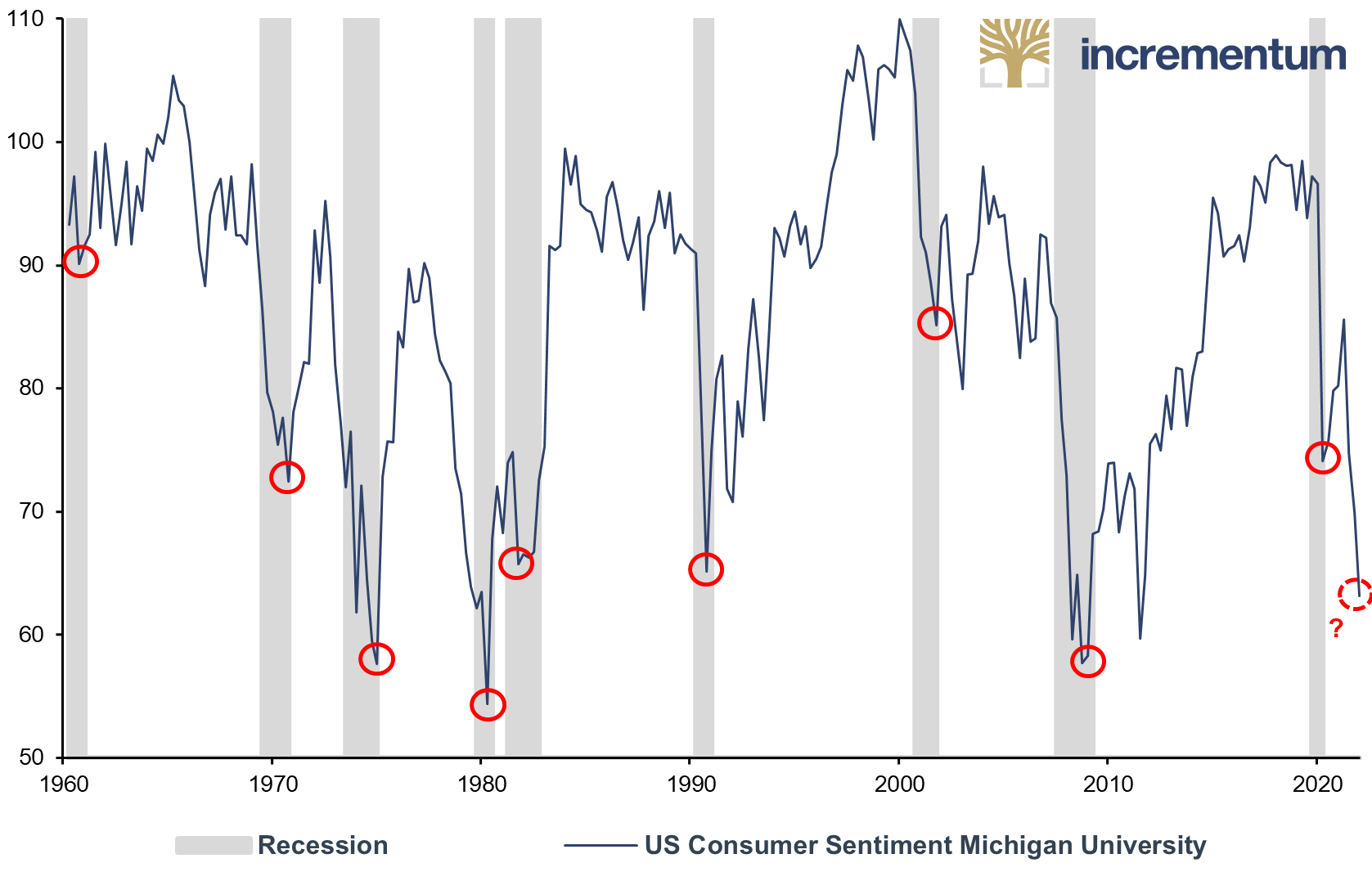

Given the eroding purchasing power, it is hardly surprising that consumer confidence has been on a downward spiral for several months. The high inflation rates are making themselves felt in people’s wallets. When asked about their financial outlook for the coming year, more households in March than at any time in the history of the University of Michigan Consumer Sentiment Survey said they expected their finances to deteriorate. Given the high importance of consumption for US GDP, the economic outlook is anything but rosy.

US Consumer Sentiment Michigan University, Q1/1960-Q1/2022

Source: Reuters Eikon, Incrementum AG

The reverse wealth effect is also likely to dampen consumer spending. The ordinary wealth effect occurs when investors believe they are wealthy as a result of rising share prices and real estate prices due to the book gains achieved, and increase their consumer spending accordingly. When prices fall, the reverse wealth effect has a correspondingly negative impact on consumer spending. In the current calendar year, US equities have already lost more than USD 10trn in market capitalization, while bonds suffer their worst losses in decades. And the first cracks can already be seen in the real estate market.

Jerome Powell has recently reminded us that the Federal Reserve’s focus is currently on fighting inflation. If his pronouncements are followed by corresponding actions, this would implicitly mean the end of the Fed put. The first time the Federal Reserve’s then-chairman Maestro Alan Greenspan invoked this practice was in the wake of the 1987 stock market crash. Now it appears the Federal Reserve is removing the safety net from the market, at least temporarily. Bill Dudley, former FOMC member, goes much further. He calls for the Federal Reserve to “force” the stock markets to correct, should they not correct on their own.

In any case, stagflation confronts monetary policymakers who continue to trust the Philips curve with the greatest possible dilemma. They are faced with the uncomfortable question of whether to stimulate the weakening economy with monetary easing or to curb inflation with tighter monetary policy. Lacy Hunt argues that with respect to the question of higher inflation with lower unemployment or lower inflation with higher unemployment, the Federal Reserve would have no choice at all, since it is a Hobson’s choice. Indeed, without containing inflation, economic recovery and thus a low unemployment rate are not even possible. However, the Federal Reserve’s decision will probably depend heavily on day-to-day political sentiment. As long as asset markets remain at high levels and growth is not disastrous, a more restrictive monetary policy stance could prevail. However, the matter will become more difficult if equity and credit markets come under further pressure and growth suffers accordingly.

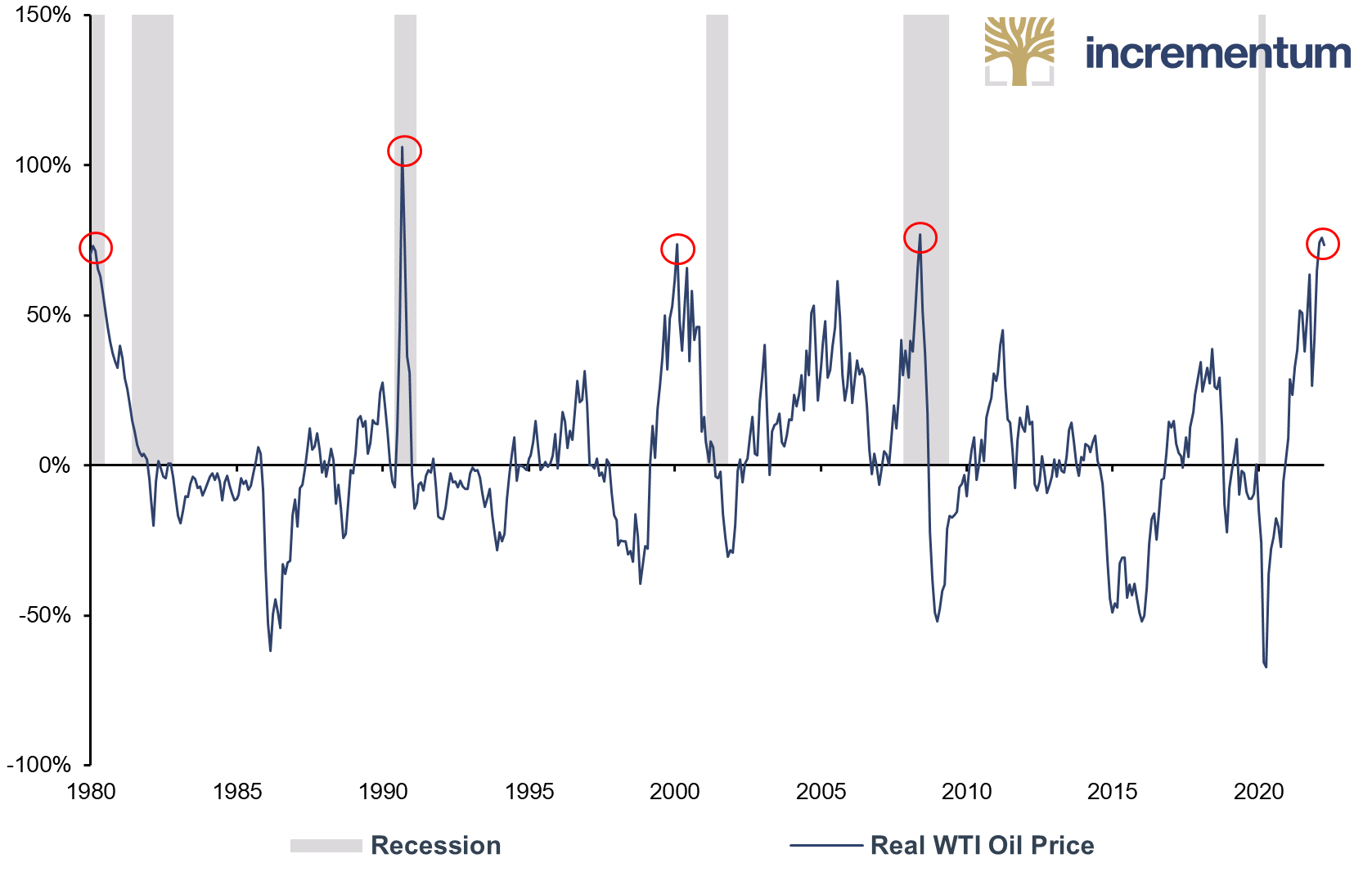

One small consolation from the perspective of monetary policy is that, as far as the cause of the bleak situation is concerned, the Ukraine conflict can be comfortably blamed for inflation. The following chart shows how high the probability of recession is as a result of oil price spikes. We would not be surprised if the next recession were to go down in the US history books as the “Putin Recession”.

Real WTI Oil Price, Deviation from Trend*, 01/1980-04/2022

Source: Reuters Eikon, Incrementum AG

*Trend is based on 2-year MA

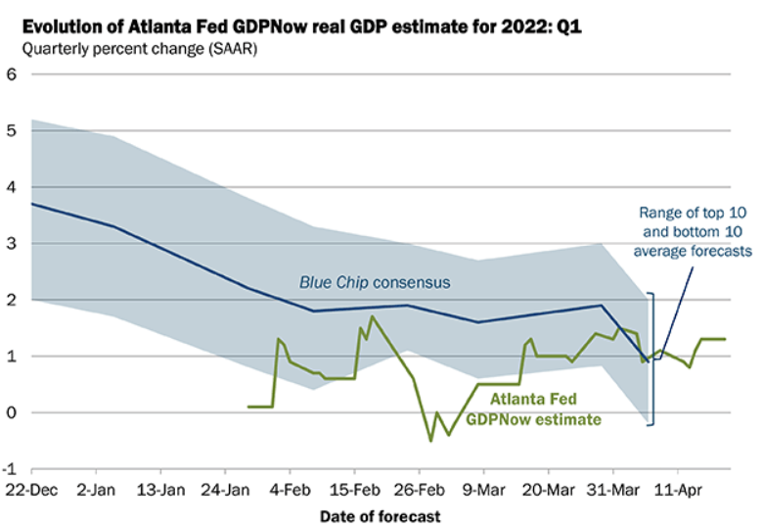

In the meantime, the economic situation in the US has already deteriorated sharply. The estimate of the Bureau of Economic Analysis (BEA) for annualized growth in Q1/2022 turned out unexpectedly low for many at -1.4%. This means that expected growth for this quarter is already well below our stagflation threshold of + 1 %. At 1.9%, the Federal Reserve Bank of Atlanta’s current forecast for Q2/2022 is also not promising and is well below the 3.0% calculated as the initial forecast for Q1/2022.

In its most recent forecast, the IMF also made a significant downward revision to its figures for the USA. While the IMF forecast growth of 5.2% for the calendar year 2022 in October 2021 and 4.0% in January, the figure has now been reduced to 3.7%. In 2023, growth is expected to be only 2.3%. However, the persistent inflationary pressure could lead to a negative surprise in terms of growth, as higher prices lead to lower growth in a highly indebted society.

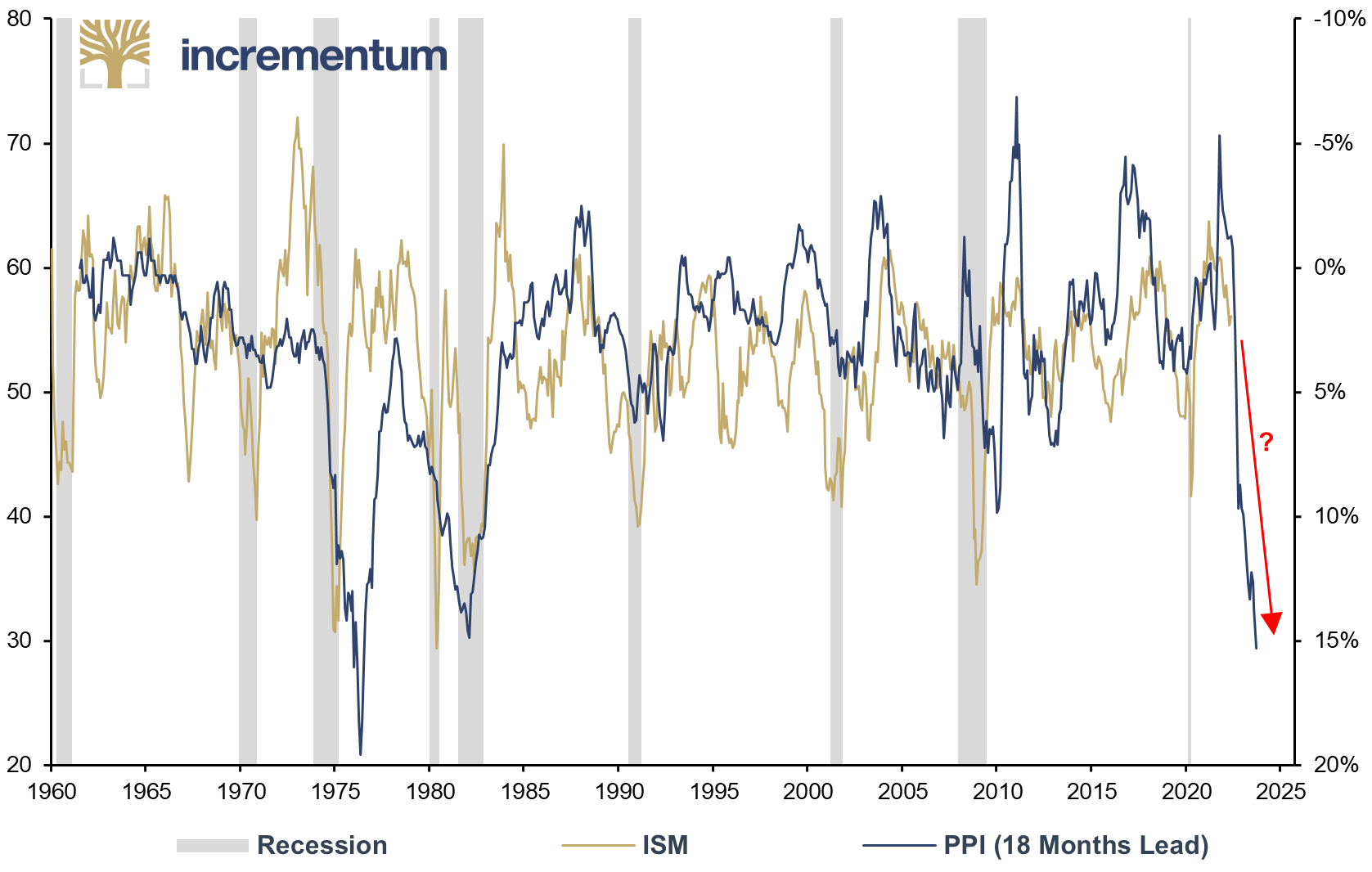

ISM (lhs), and PPI (18 Months Lead, rhs, inverted), 01/1960-04/2022

Source: Reuters Eikon, Incrementum AG

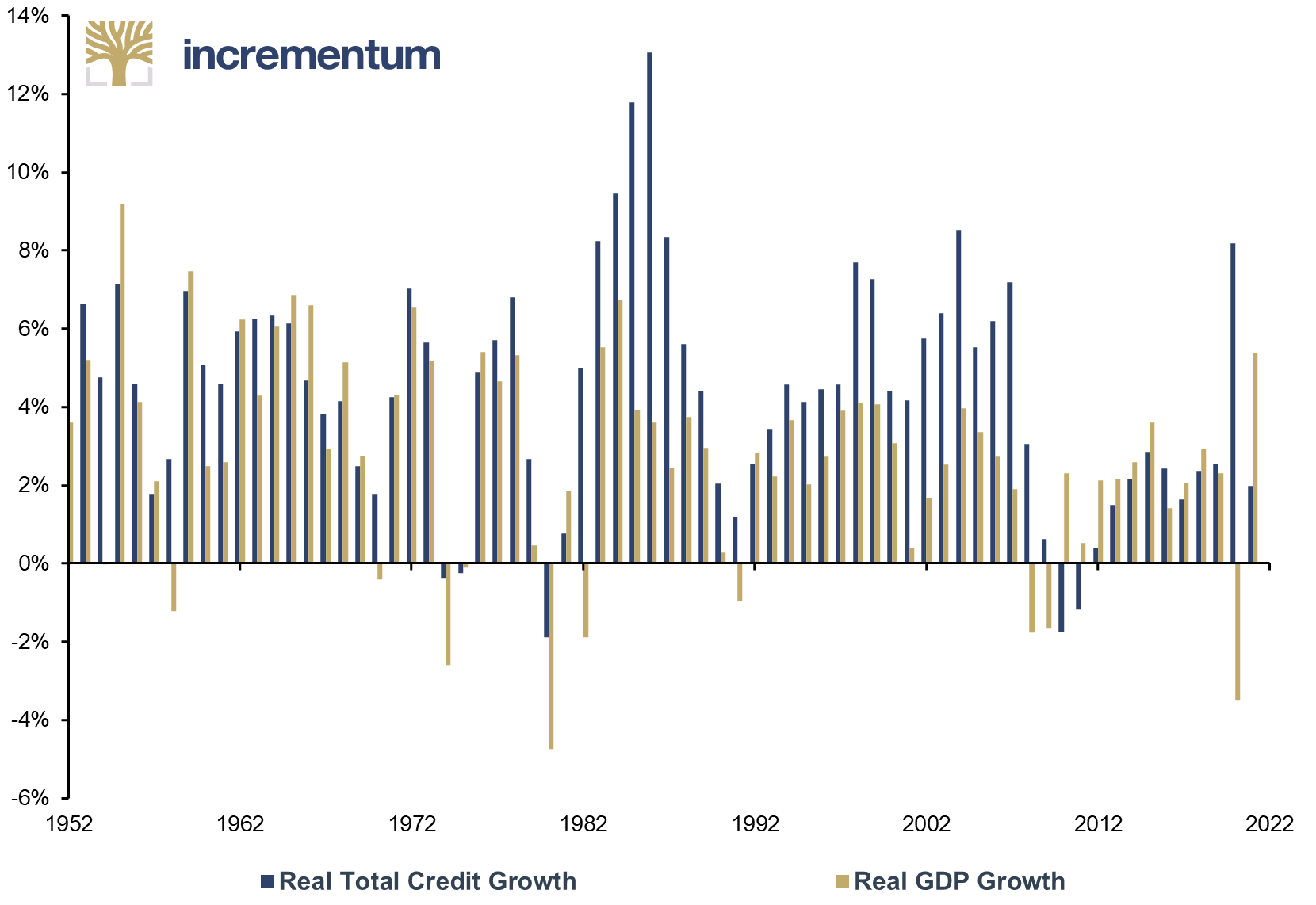

The announced interest rate hikes and the equally announced QT – i.e. the reduction of the central bank’s balance sheet by selling securities – will also have a strong dampening effect on economic growth. The previously seemingly limitless liquidity is now slowly drying up. According to Richard Duncan, the US economy needs annual credit growth of at least 2% in real terms to escape recession.[5] In all nine instances between 1952 and 2009 in which inflation-adjusted total credit grew by less than 2%, the US entered a recession. Currently, it looks as if this mark could be reached this year.

Real Total Credit Growth, and Real GDP Growth, 1952-2021

Source: Federal Reserve St. Louis, Incrementum AG

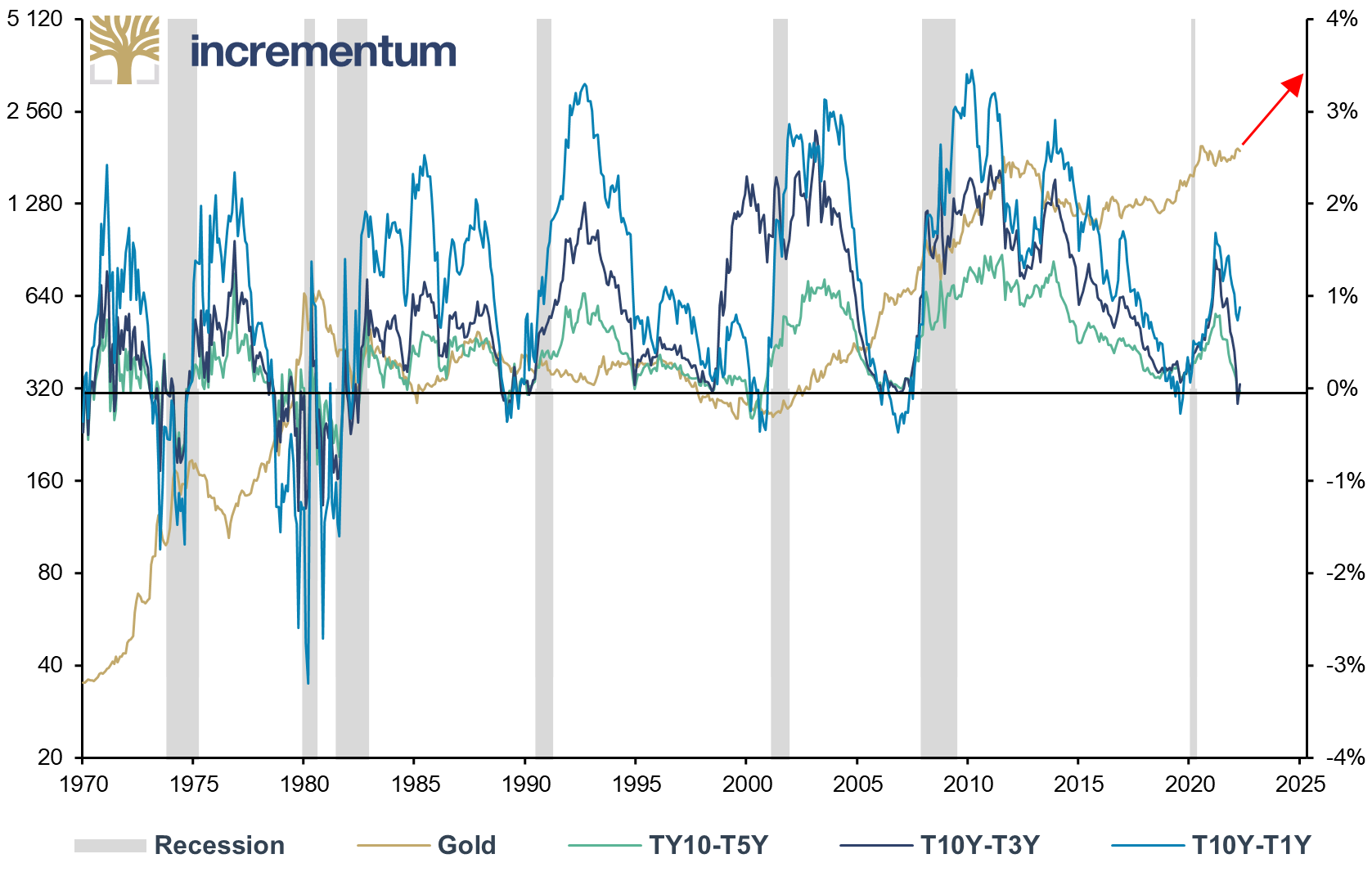

The shape of the US yield curve also points to a marked slowdown in US economic growth. A study published by the San Francisco Federal Reserve in 2018 shows that inverted yield curves have presaged most recessions since the 1950s. From an empirical perspective, narrowing interest rate spreads are followed by economic downturns and then gold appreciation. This chronological sequence has been particularly evident since the Nixon shock in 1971.

Gold (lhs, log), in USD, and US Treasury Yield Spreads (rhs), 01/1970-04/2022

Source: Federal Reserve St. Louis, Robert J. Shiller, Reuters Eikon, Incrementum AG

Euro area

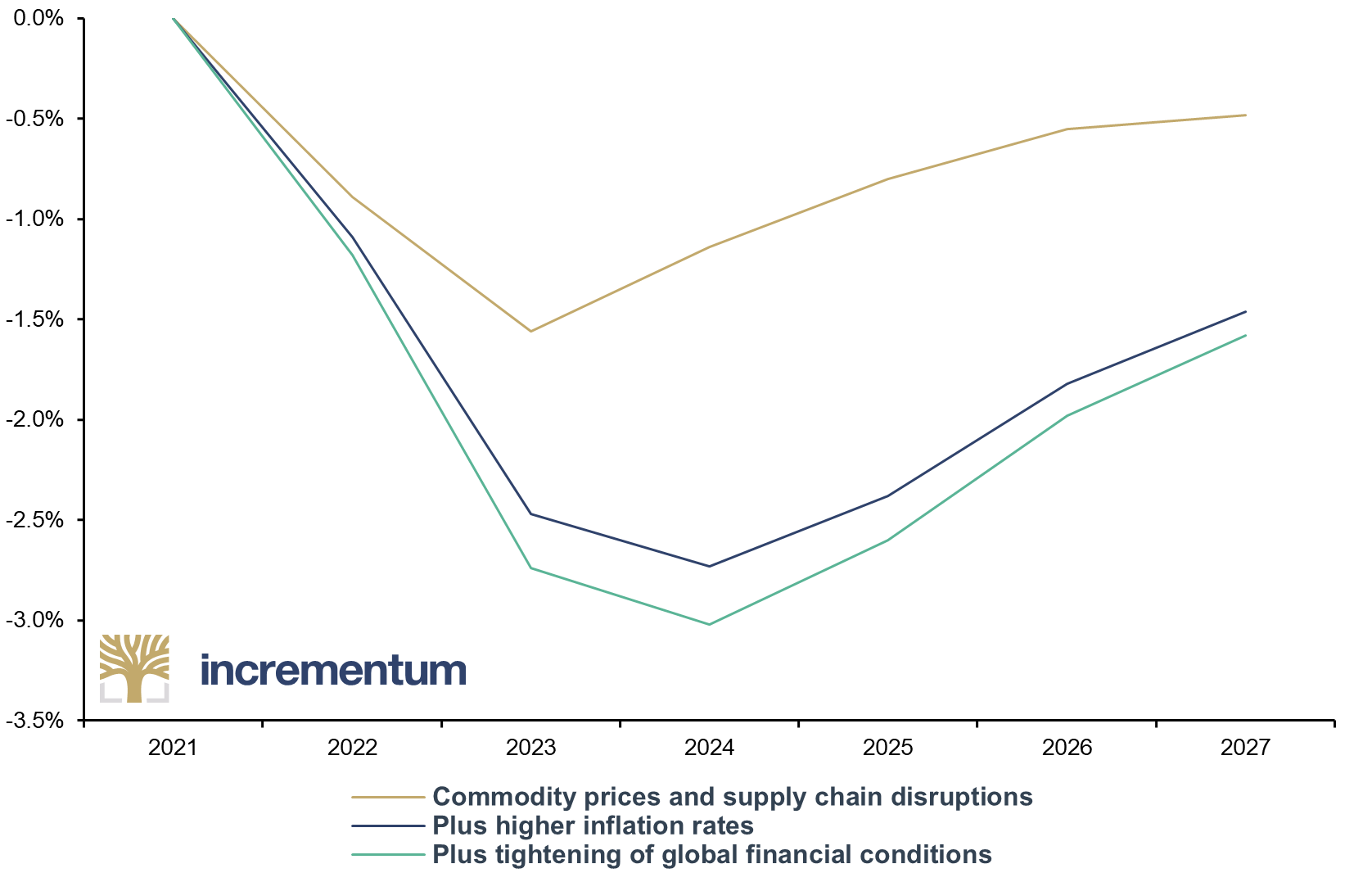

Even more so than in the US, growth rates in the euro area continue to be distorted upward by the base effect. Nevertheless, the IMF’s latest World Economic Outlook forecasts growth of only 2.8% for the euro area in 2022, compared with 4.3% projected in October 2021 and 3.9% in January, with the IMF noting considerable downward risks.

Effects on EU Real GDP, 2021-2027e

Source: IMF, Incrementum AG

Moreover, the war in Ukraine has had a large impact on the European economies, both as regards the direct consequences and the knock-on effects caused by the incessantly spiraling sanctions. In its Monthly Report – April 2022, the German Bundesbank calculates the impact of an EU energy embargo on Russia on euro area GDP. The negative effects are fed by three sources: higher commodity prices, lower foreign demand, and higher uncertainty. For 2022 and 2023, GDP in the euro area would be around 1.75% lower in each case, and for 2024 the GDP losses would be only marginally lower. For Germany in isolation, the GDP losses would be considerably higher at around 2% in the current year and around 3.5% in each of the next two years. A drop in the growth rate below the 1% mark would be unavoidable in these scenarios for the three years 2022-2024.

The potential impact on GDP is even worse if, in addition to price effects, the impact of volume restrictions resulting from an embargo is taken into account. German GDP could slump by up to 5% compared with the baseline scenario. In this case, German economic output would fall by around 2% in 2022. The Gemeinschaftsdiagnose (Joint Economic Forecast) published somewhat earlier by leading German economic research institutes arrives at similar dramatically negative consequences of an oil and gas embargo for the German economy. For 2023, this alternative scenario deviates by 5.3 percentage points downward from the baseline scenario, with growth of 3.1% forecast for 2023. For the current year, however, the 0.8 percentage point drag on GDP caused by an embargo would still be manageable.

We are certainly not going out on a limb with our assessment that these forecasts are all on the optimistic side. At present, it looks as if the escalating spiral that has been set in motion will be continued by all parties involved. In the event that the war escalates further or, even worse, spreads to other states, the effects on the economy could be catastrophic.

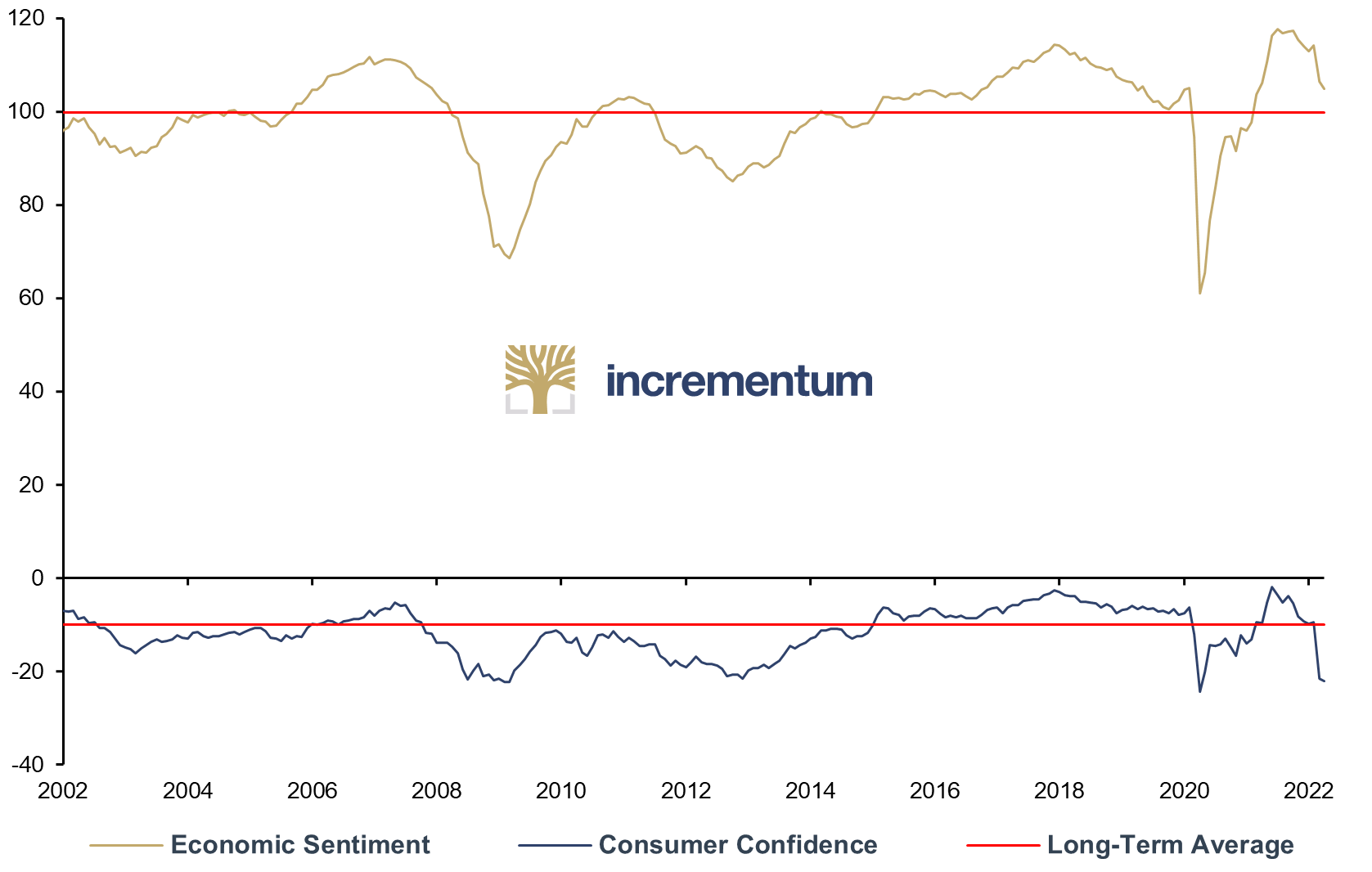

A telling risk assessment was made by Christine Lagarde at the press conference following the ECB Governing Council meeting on April 14: “The downside risks to the growth outlook have increased substantially as a result of the war in Ukraine…. The upside risks surrounding the inflation outlook have also intensified, especially in the near term.” In this context, the HICP for the euro area has already been above the 3.0% mark since August 2021 and is now at 7.5% (April 2022). If the ECB were to take its own statements seriously, it would have to assume that a stagflation scenario is extremely likely. In any case, consumer confidence has rattled to an all-time low since the outbreak of war.

Economic Sentiment and Consumer Confidence in the Euro Area, 01/2002-04/2022

Source: Reuters Eikon, Incrementum AG

Once again, we would like to draw attention to the development of sentiment in the years before the Covid-19 breakout. Since the beginning of 2018, the economic sentiment barometer had been on a continuous downward trend. The brief recovery immediately before the Covid-19 crash was not a trend break that could now be followed up. This upswing was solely due to the anticipation of certain sales that could not be completed because of circumstances no one could foresee at the time.

Despite all the (purposefully) optimistic forecasts, a number of factors currently point to increasingly recessionary trends in large parts of the world:

- Rising interest rates, quantitative tightening (QT)

- Strongly flattening yield curve, which is already partially inverted

- Falling stock markets

- Sharp rise in oil, gas and electricity prices

- Sharp drop in consumer confidence

- Slowly rising loan default rates

- Weakening of economy due to lockdowns to combat Covid-19 pandemic

- Persistence of supply chain issues

- Threat of fertilizer and food crises due to war in Ukraine

- An increasingly fragile Chinese economy stubbornly adhering to the zero-Covid policy.

- Sharp rise in geopolitical tensions

Stagflation-Proof Portfolios

“I think that most likely what we are going to have is a period of stagflation. And then you have to understand how to build a portfolio that’s balanced for that kind of environment.”

Ray Dalio

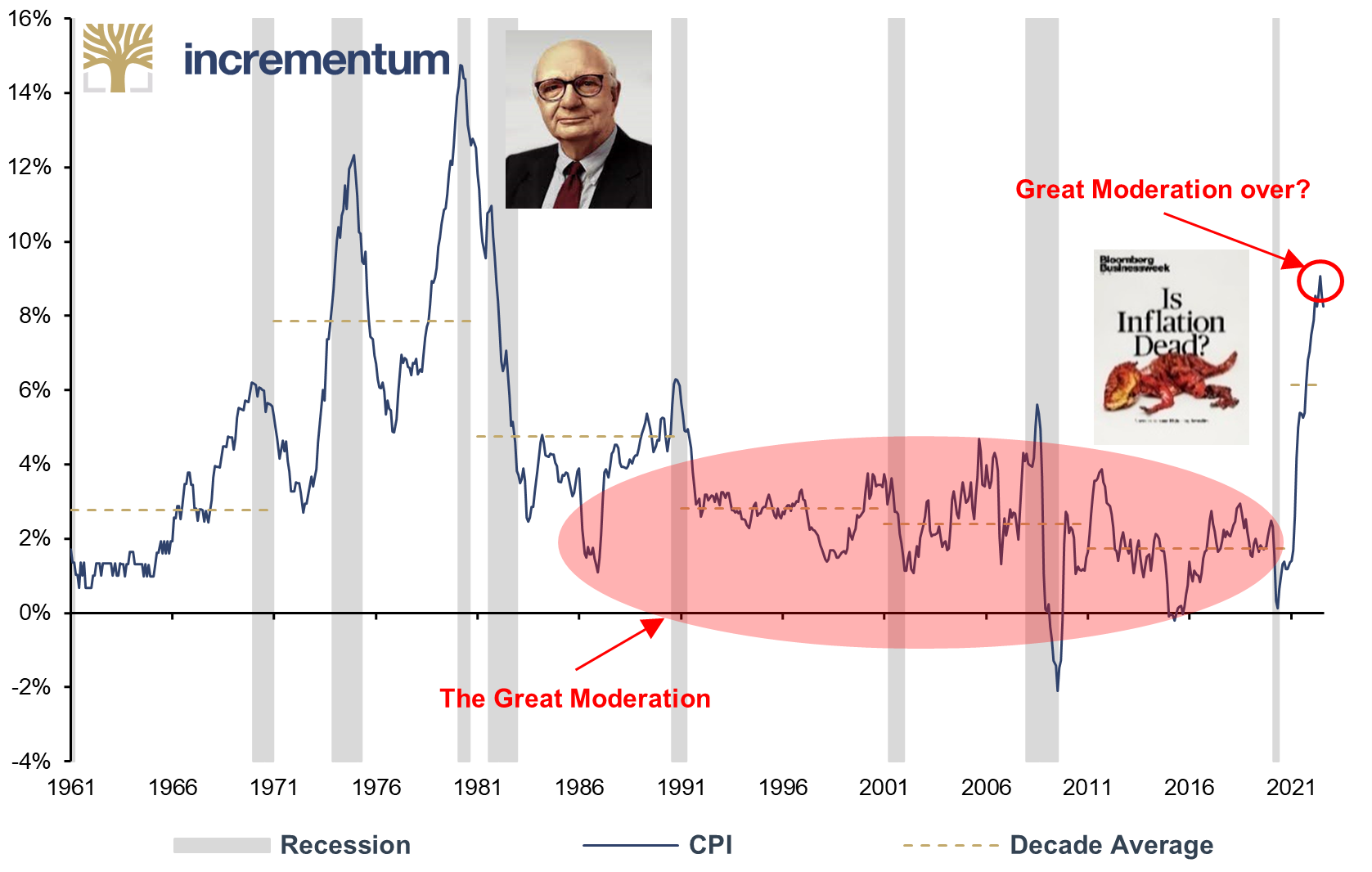

If our assessment that we are currently experiencing the end of the 40-year disinflationary Great Moderation is correct, there are serious consequences for investors. In our view, there will probably be a longer-term process until the collective mindset of investors has completed this paradigm shift. A fundamental repositioning of many portfolios and thus a reallocation of enormous amounts of financial capital will be the consequence of this paradigm shift. These reallocation processes will probably last for several quarters, if not years.

US CPI, yoy%, 01/1961-05/2022

Source: Reuters Eikon, Incrementum AG

The narrative of temporary inflation was able to reassure most market participants for a surprisingly long time. This is in large part because the bulk of Western investors have never been confronted with a significant increase in inflation during their active careers as investors, let alone with a prolonged inflationary or even stagflationary period.

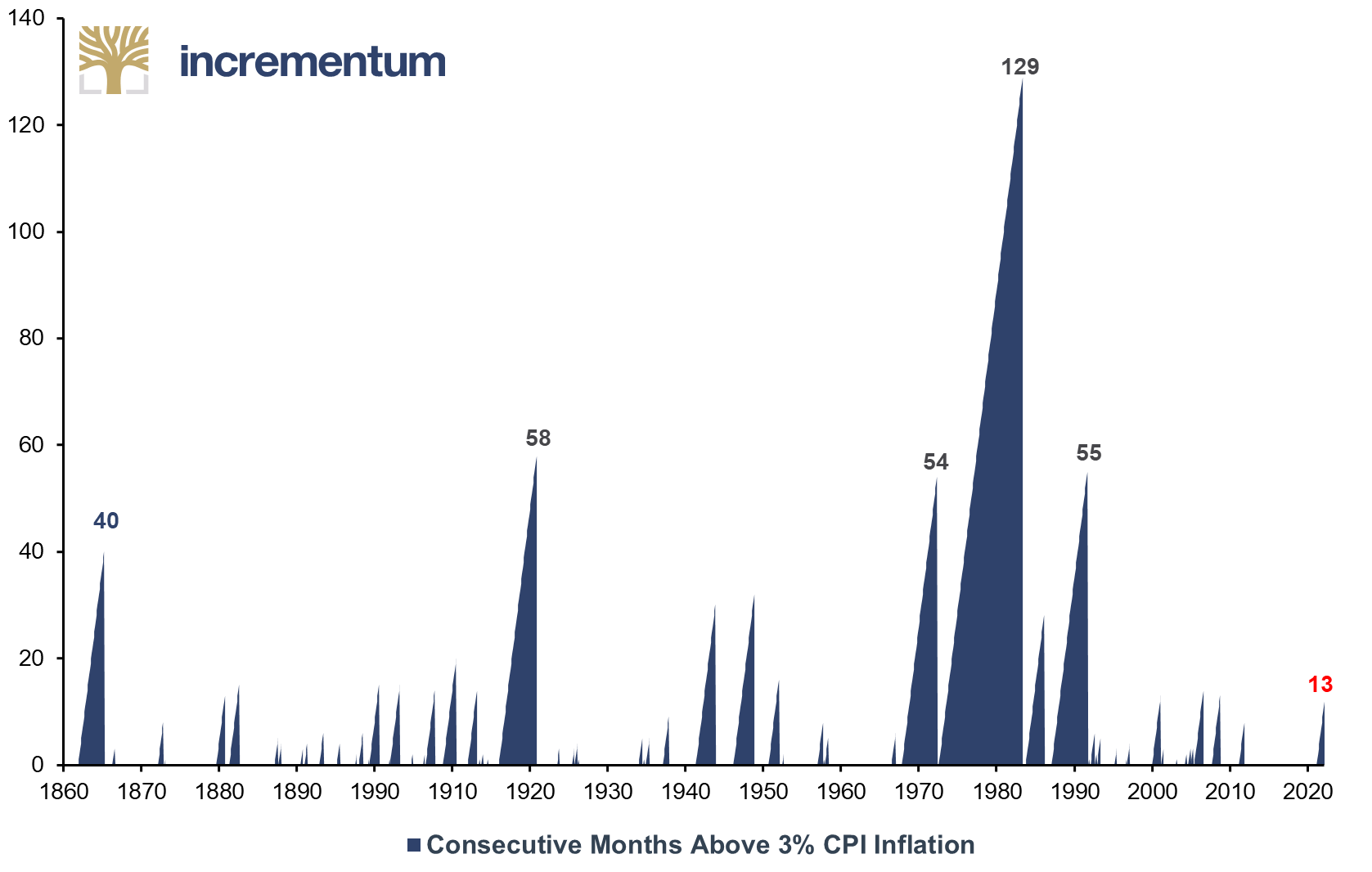

Consecutive Months Above 3% CPI Inflation, 01/1860-04/2022

Source: Crescat Capital LLC, Reuters Eikon, goldchartsrus.com, Incrementum AG

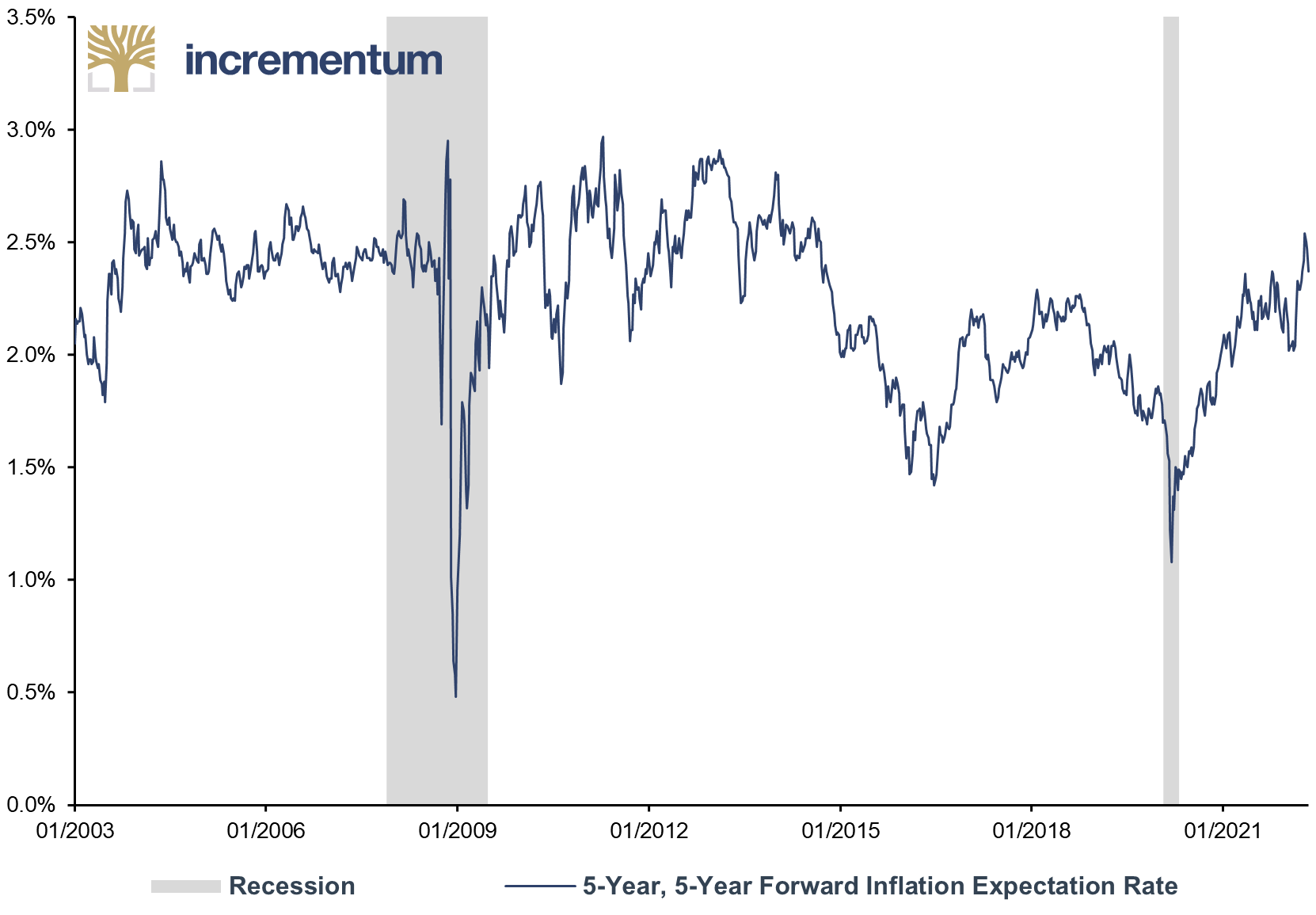

Many investors are still significantly influenced by the disinflationary past of the last decades. A look at 5y5y inflation expectations shows a significant probability that elevated inflation figures could be a multi-year condition, and it is one that is still not nearly priced into the market.

5-Year, 5-Year Forward Inflation Expectation Rate, 01/2003-05/2022

Source: Federal Reserve St. Louis, Incrementum AG

From an investor’s point of view, however, this is precisely where a promising opportunity lies, as enormous amounts of capital will be reallocated in the course of this inflation paradigm shift.

Stagflation: Poison for the Balanced Portfolio?

Stagflation is possibly the most challenging environment for investors. At this point, we would like to take a rough overview of the different asset classes in times of stagflation. As mentioned, there are not too many recent precedents for pronounced stagflation in Western countries. We will therefore focus on the 1970s.

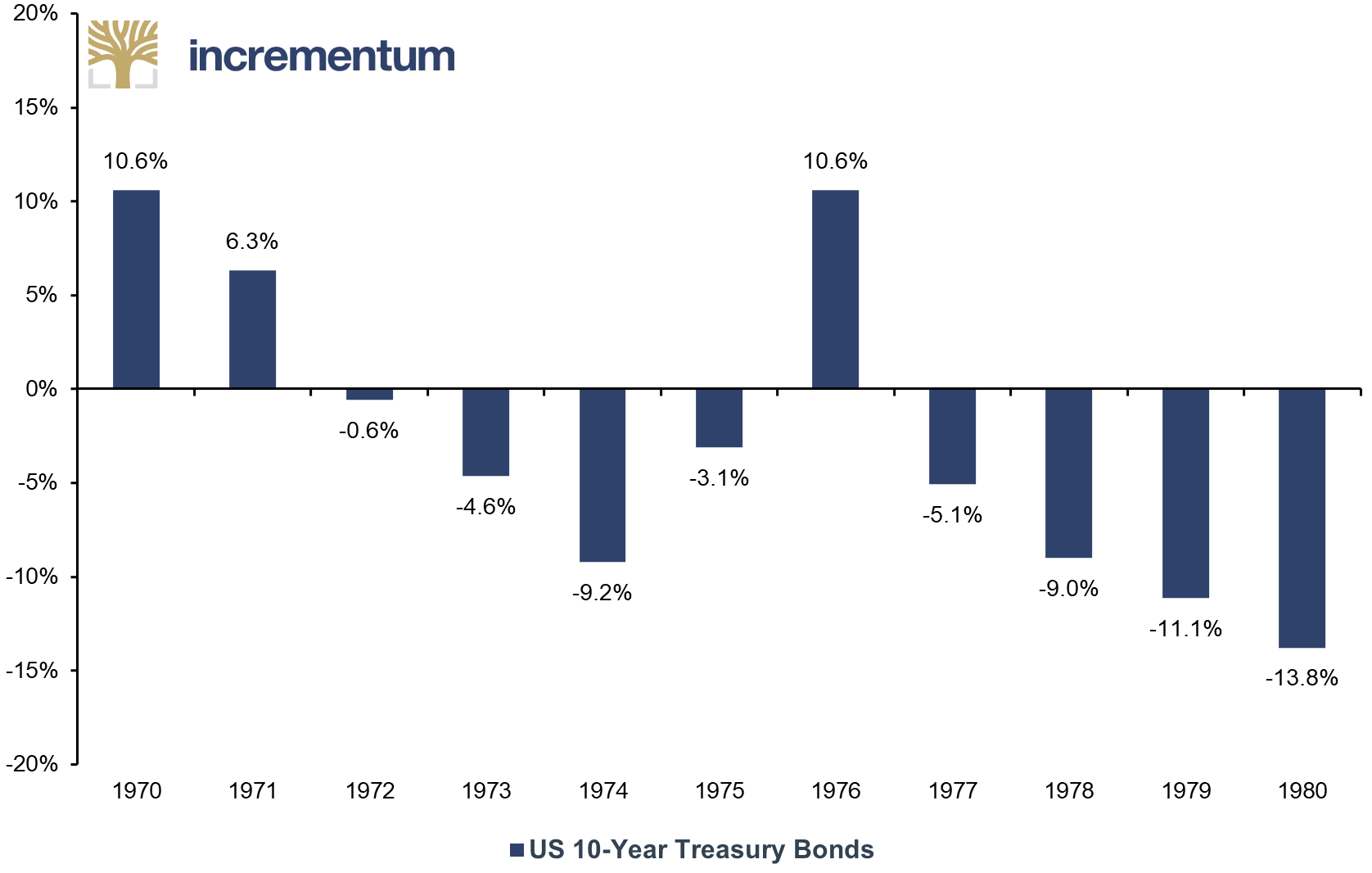

With high inflation and rising yields, fixed-income securities are the obvious losers. Constant interest payments in the face of ongoing monetary depreciation reduce the value of a security. The longer the maturity, the higher the purchasing power-adjusted risk of loss. Values are also nominally at risk, namely when returns on the capital markets rise and the market value of the security falls. Investors suffered significant losses on bonds in the 1970s. In 2022, too, bondholders have recorded painful losses so far.

Real Annual Returns of US 10-Year Treasury Bonds, 1970-1980

Source: Stern School of Business, Incrementum AG

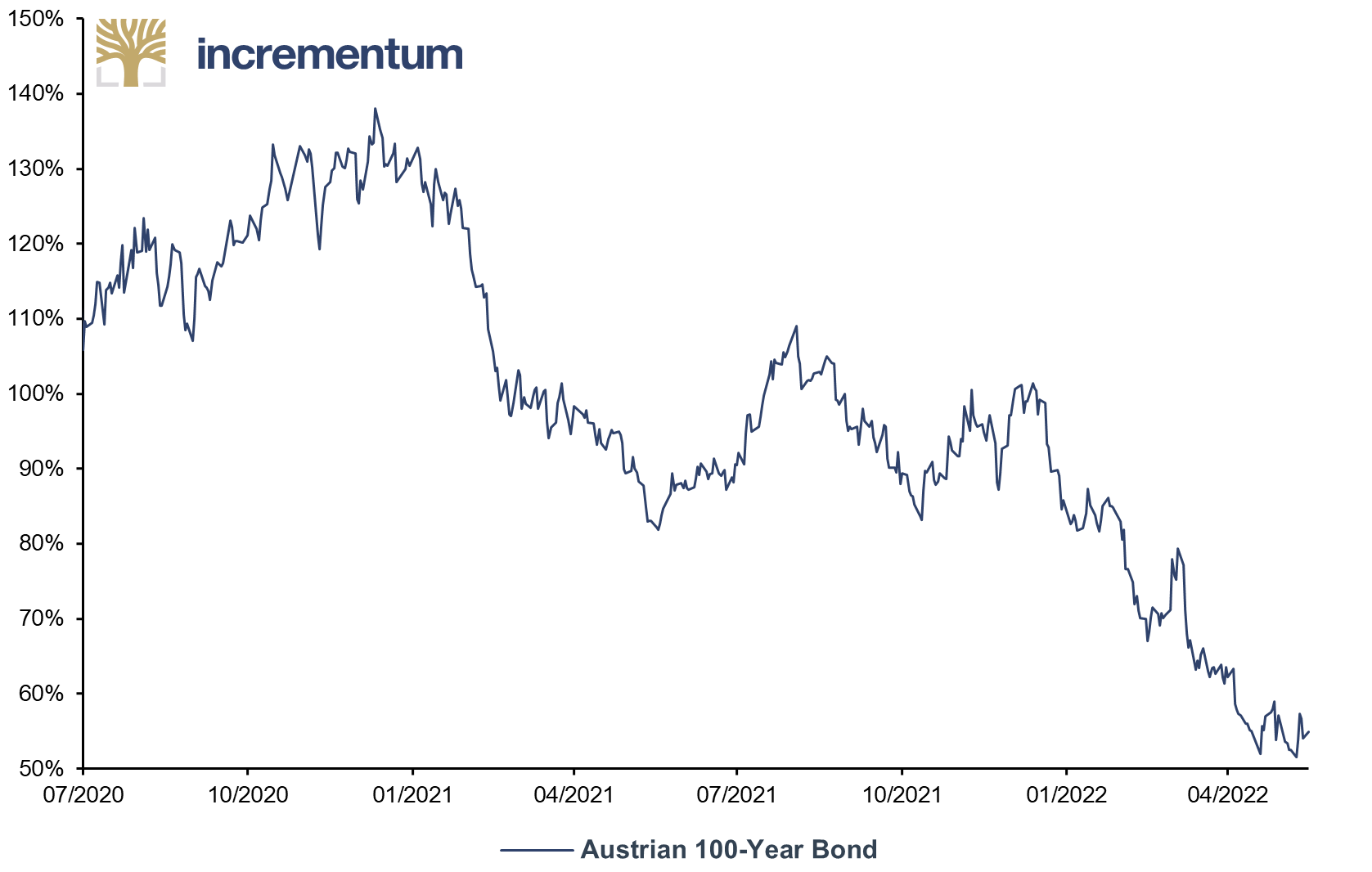

As the following chart shows, for the second of the two 100-year Austrian government bonds issued to date, with a coupon of a measly 0.850% and an issue yield of 0.880%, the investment has been anything but a good one so far. As a reminder, this bond, with a volume of EUR 2bn, was oversubscribed 12 times (!!!) when it was issued in 2020, not so long ago.

Austrian 100-Year Bond (0.85%, 06/30/2120), in %, 07/2020-05/2022

Source: Deutsche Börse, Incrementum AG

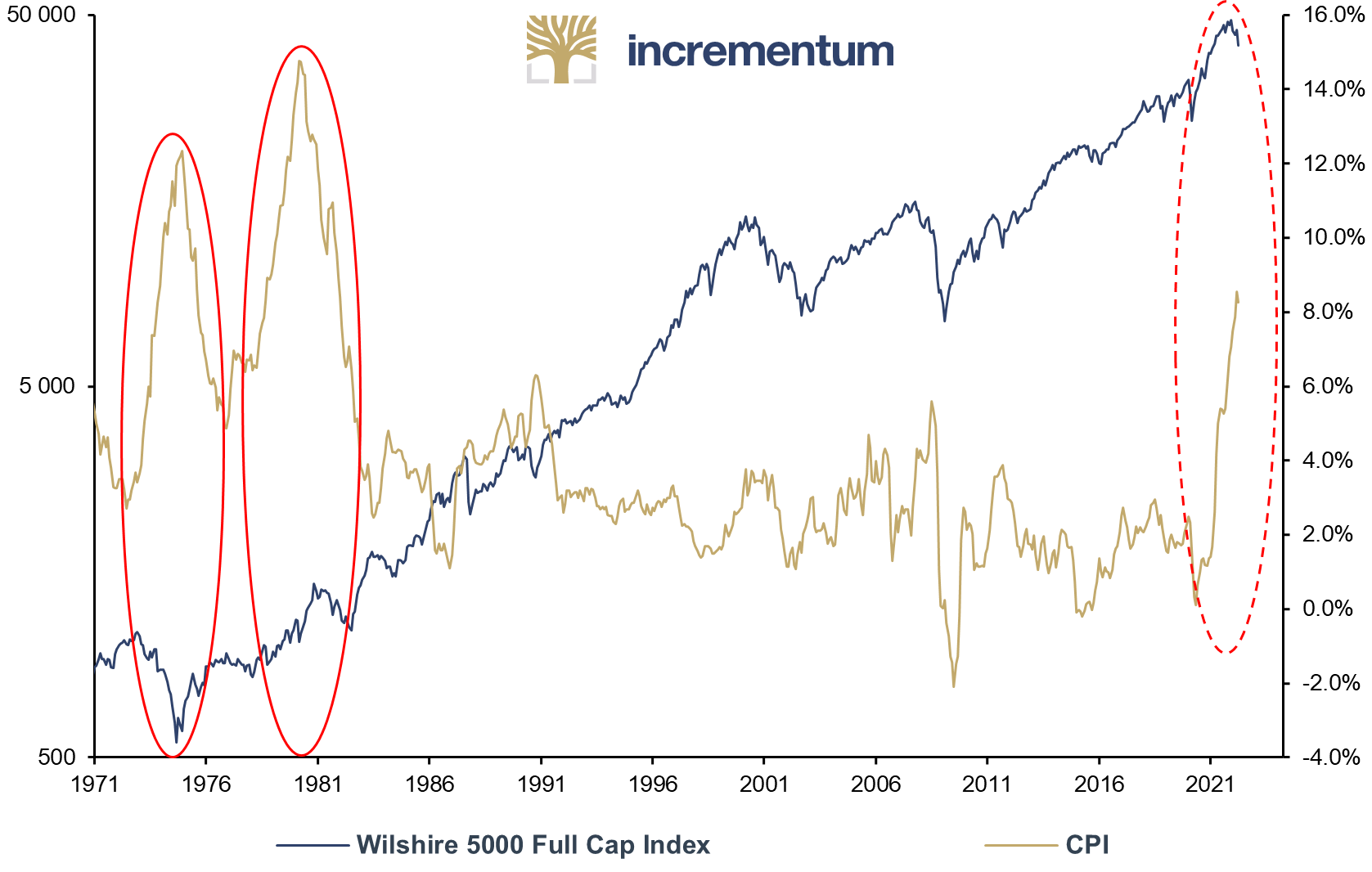

But stocks as an asset class are not inflation-proof per se, either. During the stagflationary decade of the 1970s, US equities also performed weakly in real terms.

Wilshire 5000 Full Cap Index (lhs, log), and CPI (rhs), yoy%, 01/1971-04/2022

Source: Reuters Eikon, Incrementum AG

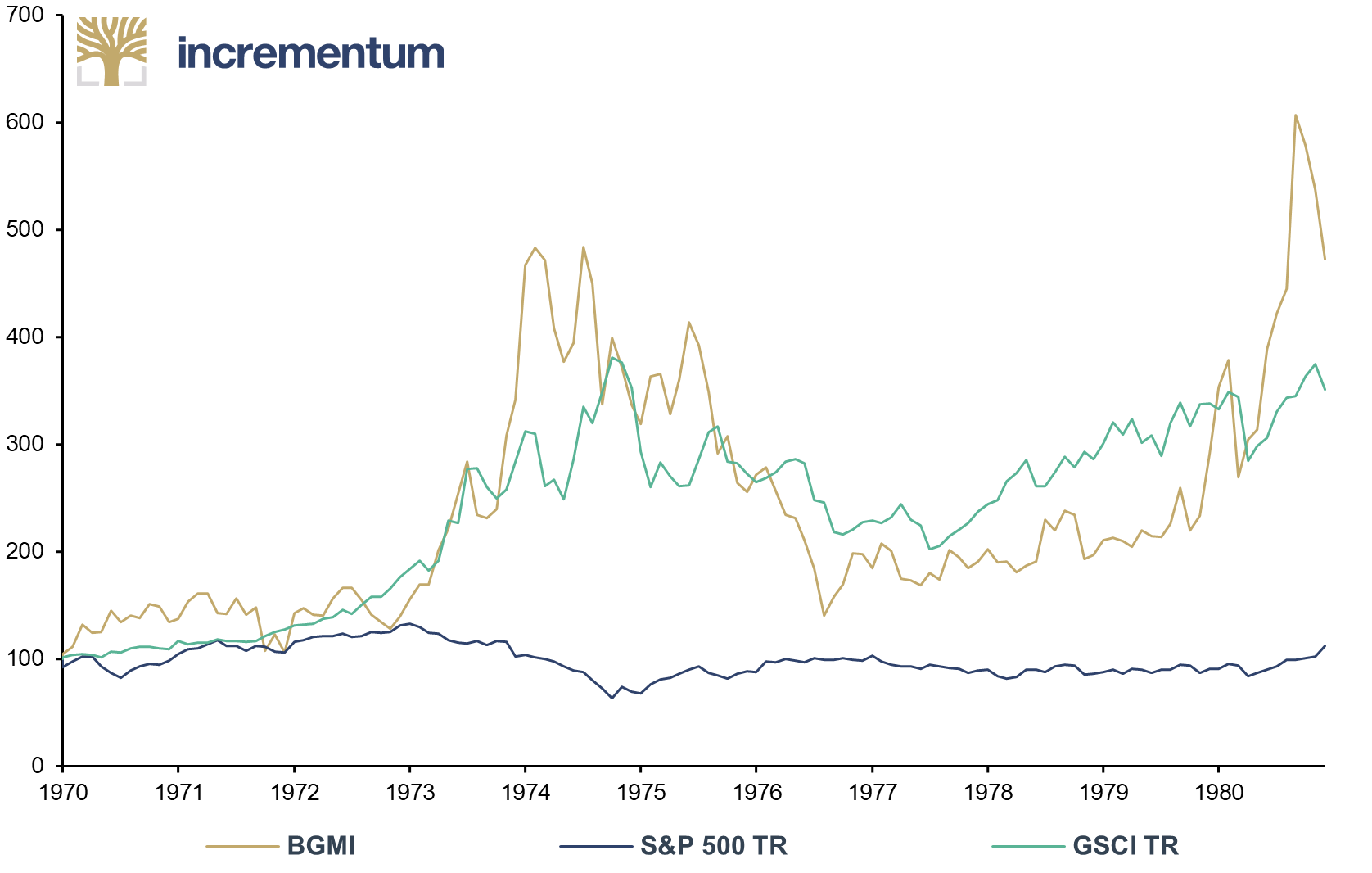

Only selected sectors, such as mining stocks and commodity shares, were able to escape the negative overall trend.

Inflation Adjusted Performance of BGMI, GSCI TR, and S&P 500 TR, 100 = 12/31/1969, 01/1970-12/1980

Source: Reuters Eikon, goldchartsrus.com, Incrementum AG

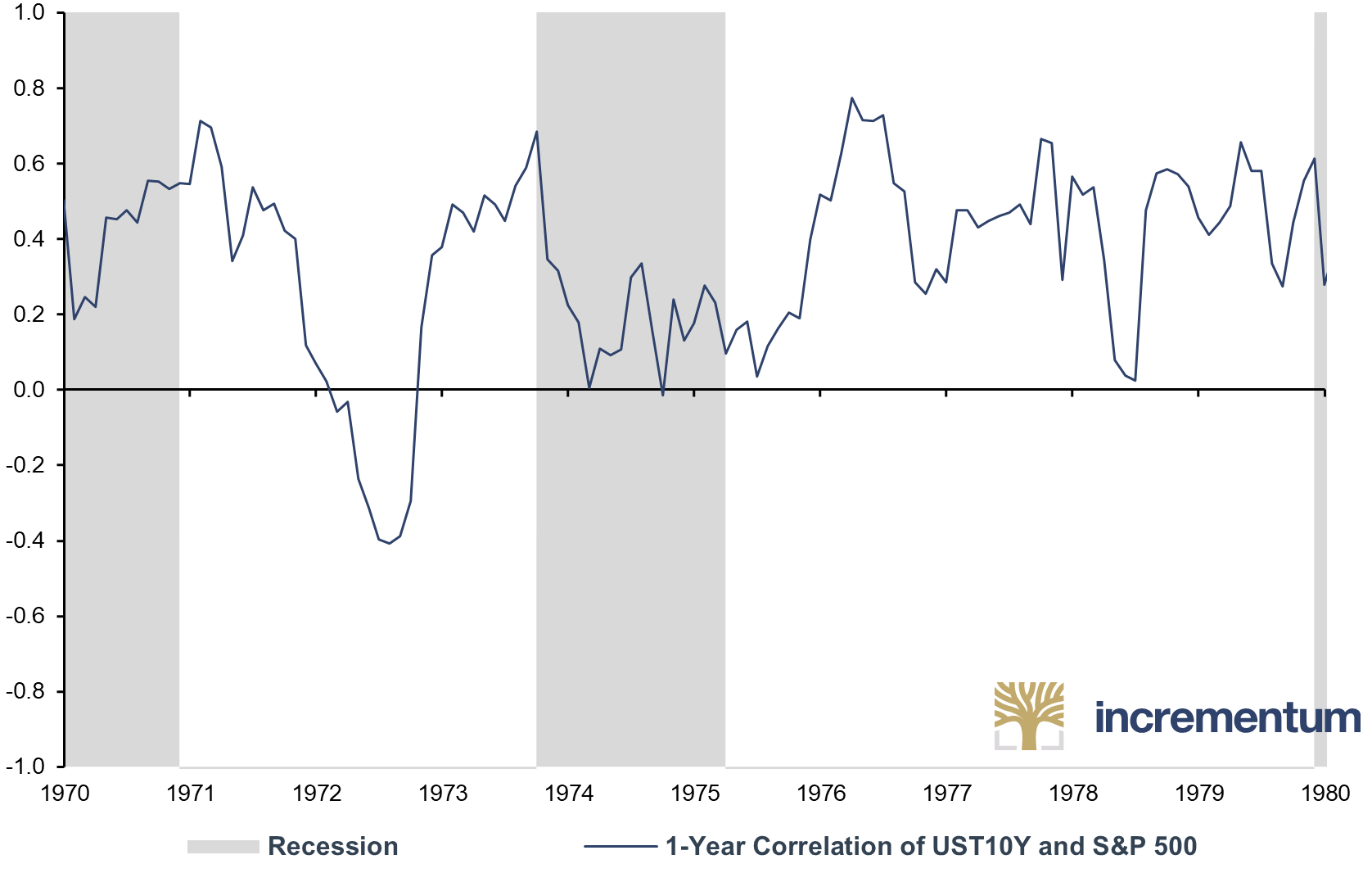

And therein lies the crux for investors: Both asset classes, equities and bonds, are clobbered at the same time during stagflation. This is clearly reflected in the correlation between the two asset classes and is precisely what makes construction of a diversified portfolio so challenging. Conventional mixed portfolios face unusually high losses when the correlation between these two asset classes increases.

1-Year Correlation of UST10Y and S&P 500, 01/1970-01/1980

Source: Reuters Eikon, Incrementum AG

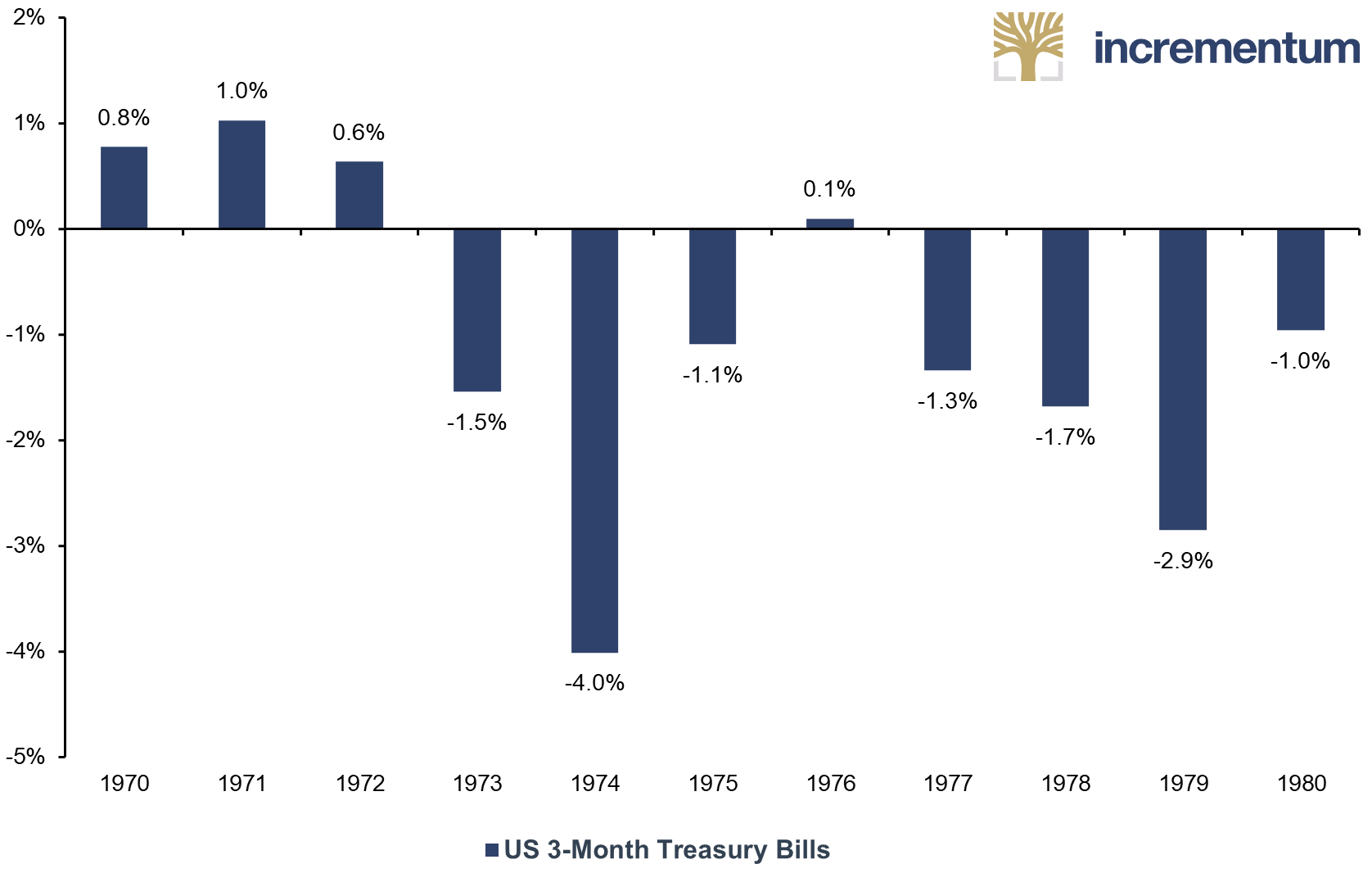

Another problem is that holding cash reserves at negative real interest rates obviously leads to capital destruction. Therefore, cash should at best be held only in the short term as part of tactical asset allocation.

Real Annual Returns of US 3-Month Treasury Bills, 1970-1980

Source: Stern School of Business, Incrementum AG

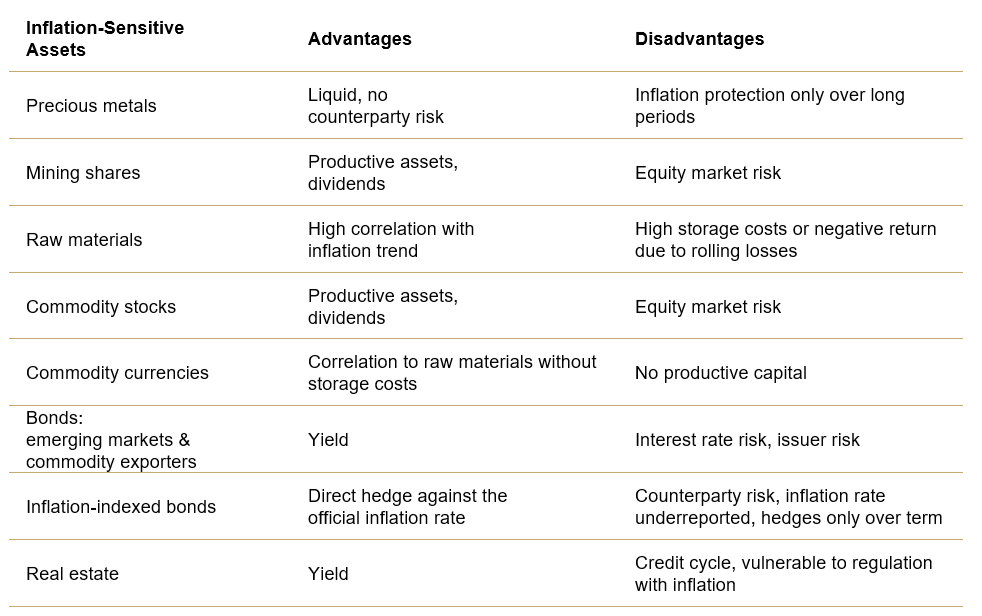

In an environment of rising inflation, inflation-sensitive investments are indeed in demand. These typically include commodities or commodity-related investments such as commodity equities or commodity currencies. Furthermore, bonds of commodity-exporting countries such as Brazil or Australia, inflation-indexed bonds, and real estate can be considered as inflation-sensitive investments. However, none of these asset classes is flawless. We have compared the most important inflation-sensitive asset classes below, including their advantages and disadvantages.

Source: Incrementum AG

It seems intuitive that an investment in commodities is profitable in times of high inflation. However, implementation in the portfolio involves some pitfalls. Direct, physical investment in commodities is often difficult. The main problems with direct investments are that they involve high storage costs or that it is impractical to invest in the commodities themselves due to their perishable nature (agricultural commodities, for example). This is one of the advantages of investing in physical precious metals, as they can be stored for a long time at a reasonable cost without any loss of quality.

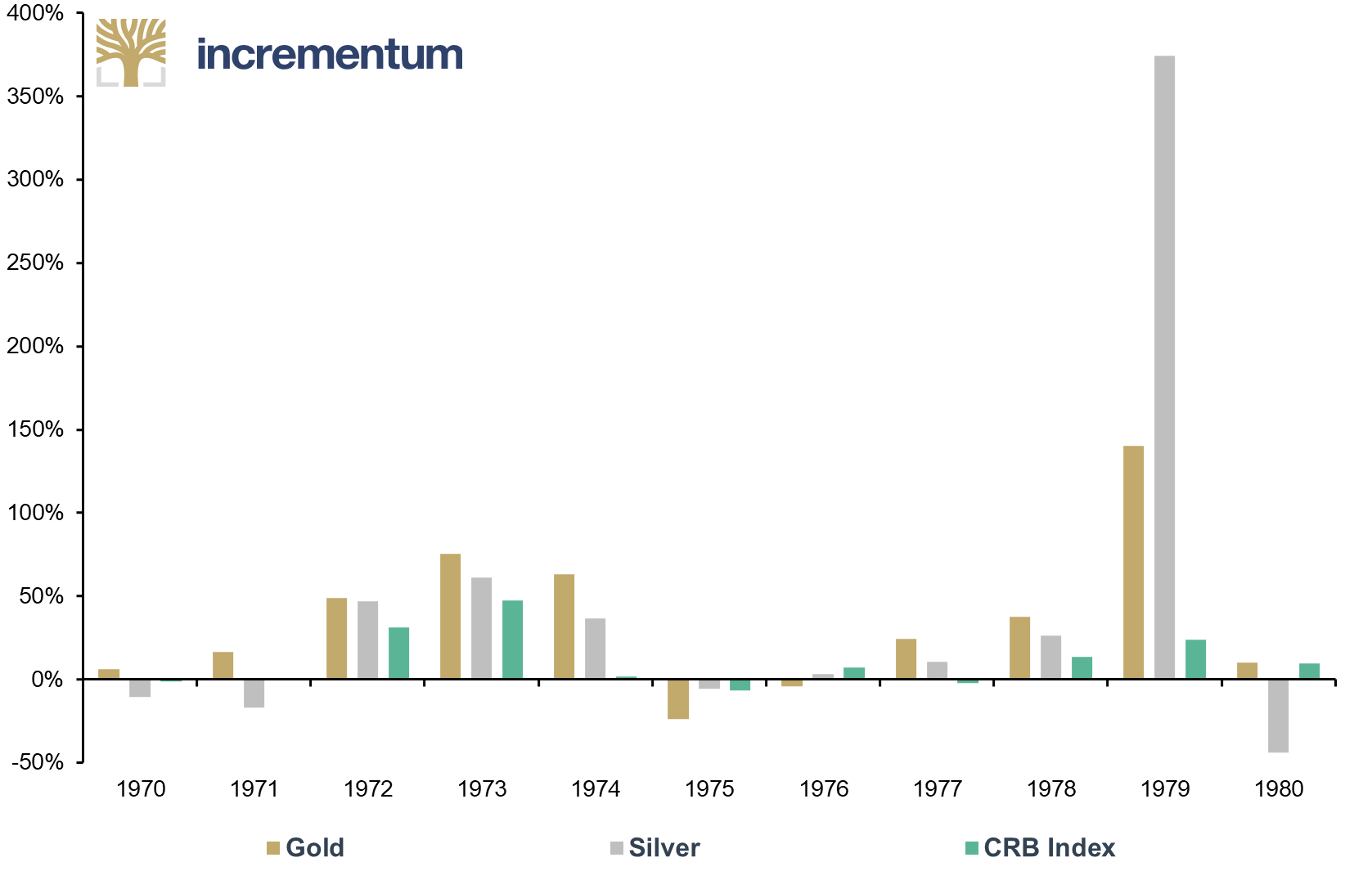

Annual Returns of Gold, Silver and CRB Index, 1970-1980

Source: goldchartsrus.com, Incrementum AG

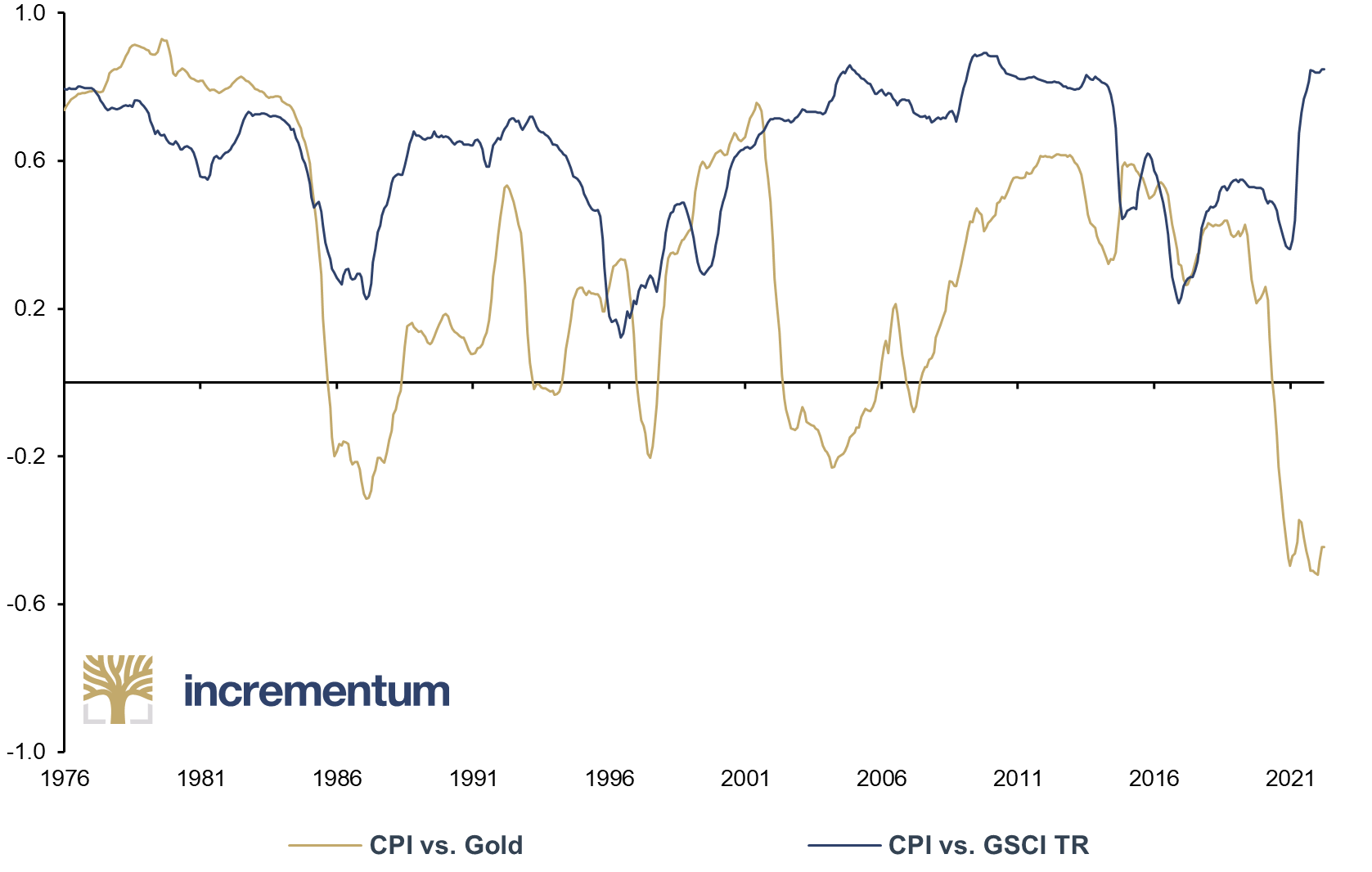

An investment in gold is therefore the simplest and most favorable way to invest in a physical commodity over the longer term. However, it should be noted that gold has a significantly lower correlation to the inflation rate than broad commodity indices.

Rolling 5-Year Correlation of CPI Inflation Rate, yoy, Gold, and GSCI TR, yoy%, 01/1976-04/2022

Source: Reuters Eikon, Incrementum AG

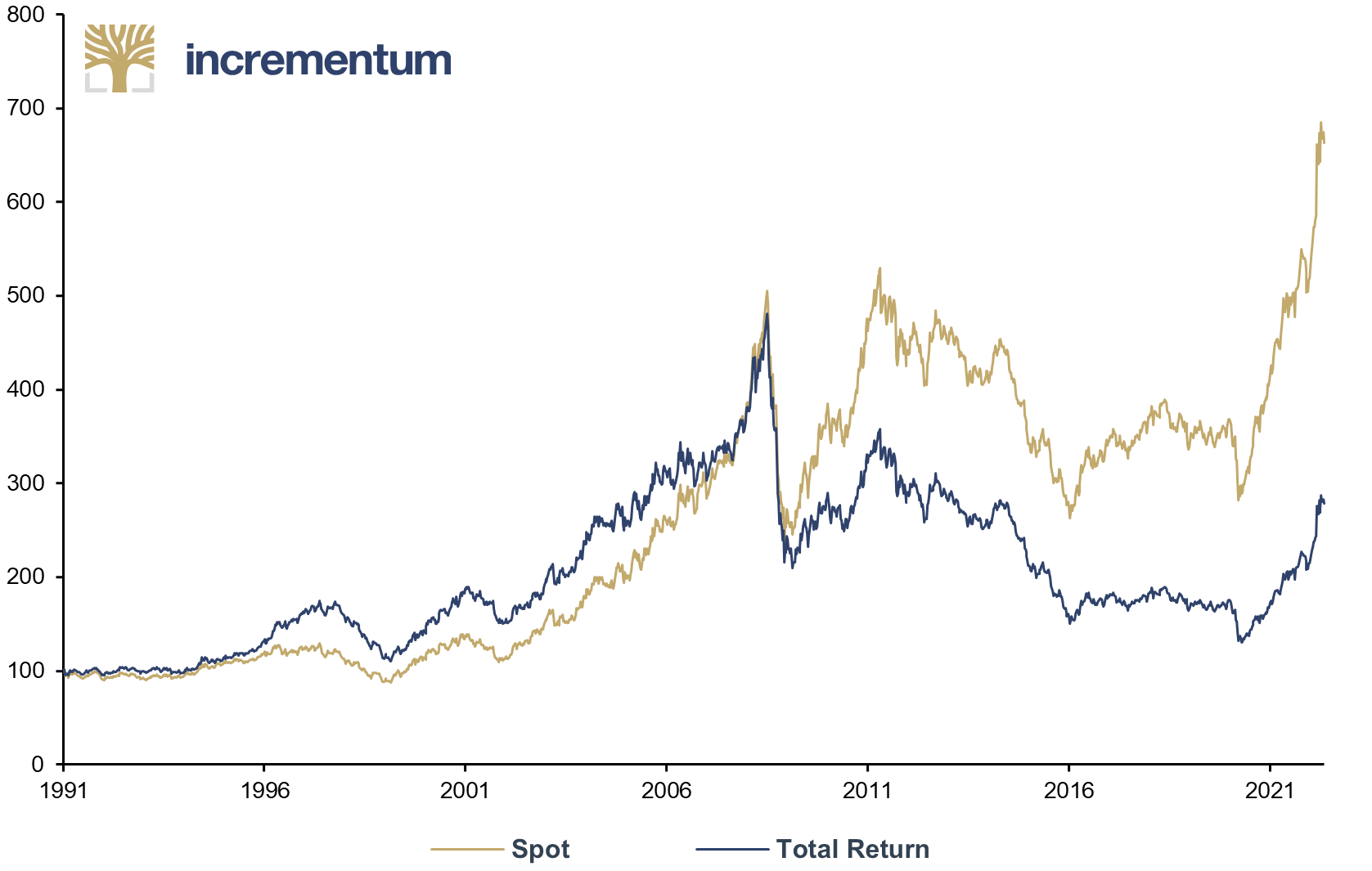

If investors want to hedge more directly against rising inflation, a broader commodity exposure is appropriate. Futures contracts of exchange-traded commodities are a possible alternative to physical direct investments. The disadvantage of using these instruments is that a buy-and-hold-investment in commodity derivatives is typically accompanied by rolling losses. Ultimately, these losses reflect storage and financing costs.

BCOM Spot, and BCOM Total Return, 01/1991-05/2022

Source: Reuters Eikon, Incrementum AG

The situation is different for shares in companies that participate in the value chain of commodity production. An investment in such stocks means co-ownership of productive capital which – disregarding the potentially significant company-specific risks – basically generates positive returns. Nevertheless, as a shareholder you are typically at the mercy of general stock market sensitivity, i.e. beta, which can be a consistent headwind in a stagflationary environment – especially when a recession is looming.

Of course, there are also companies in other equity sectors that can, for example, pass on increased costs due to their pricing power or benefit from the substitution of expensive goods. In any case, the correlation with the inflation rate is lower with equity investments, and company-specific risk is correspondingly present.

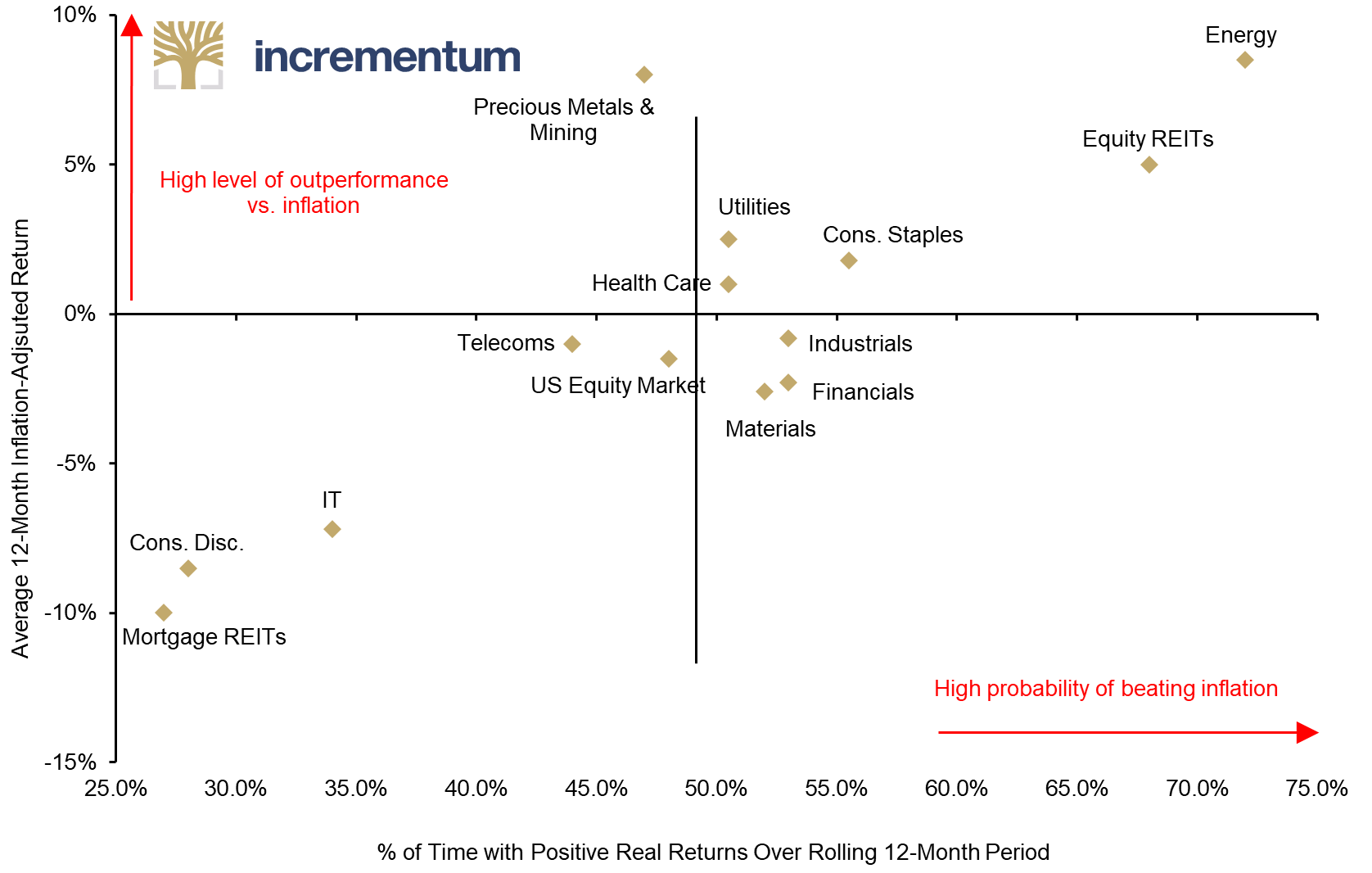

US Equity Sector Performance in High (+3% on average) and Rising Inflation Environments, 1973-2020

Source: Schroders, Incrementum AG

While commodity stocks are typically among the winners in a stagflationary phase, technology stocks are particularly negatively affected. This is because growth stocks typically discount profits that lie far in the future in order to price them in today. Therefore, there is also an especially high sensitivity to long-term yields – i.e. a duration risk – which typically provide the basis for a discount rate. But any profit margins are also at risk if costs rise. Provided investors have the appropriate risk tolerance and financial market knowledge, tactical short positions within this sector can be promising trades. The same applies to government bonds, which experienced investors can short via futures, for example, in order to profit from rising yields.

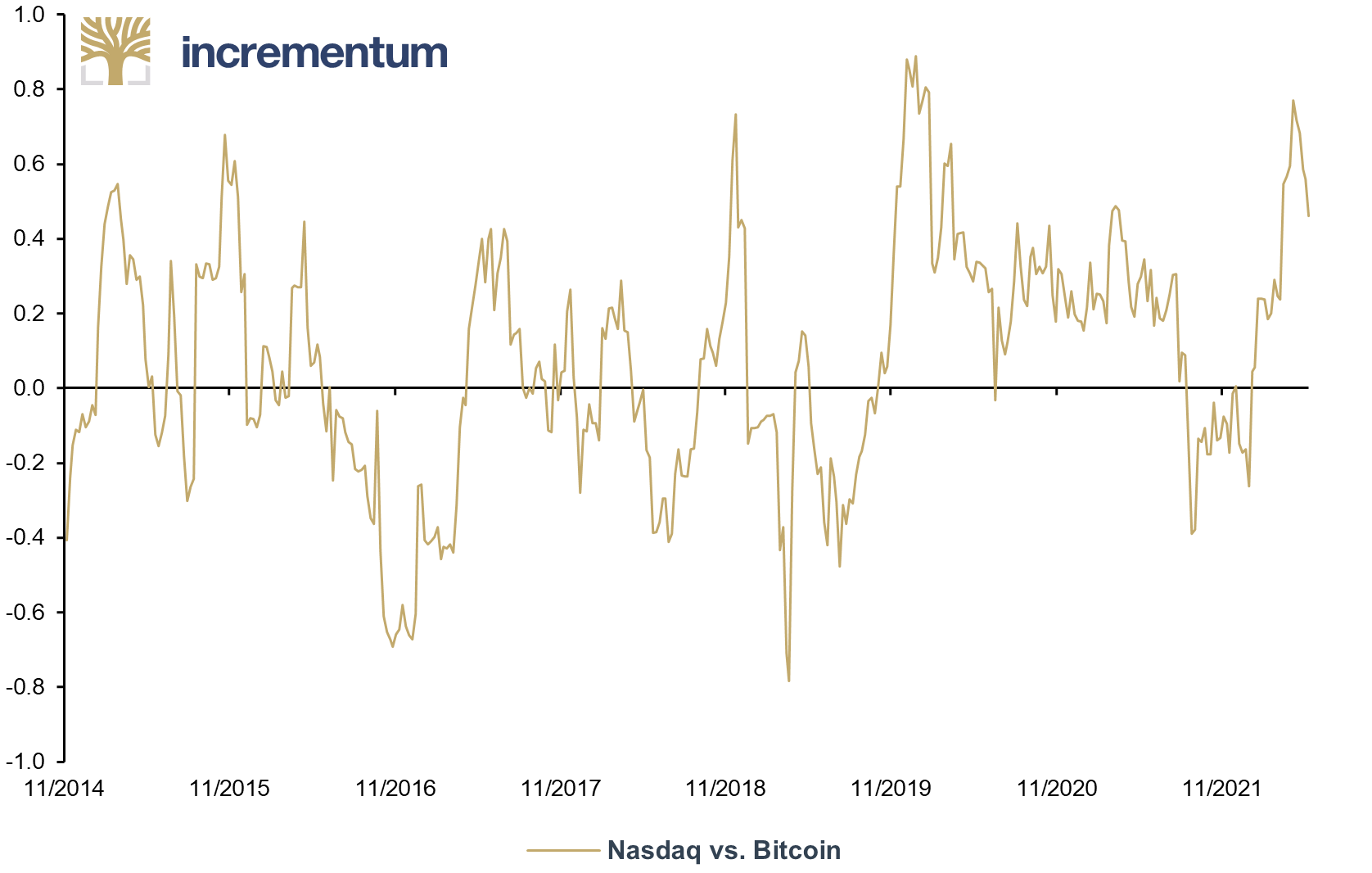

How the young asset class of cryptocurrencies will fare within a stagflation remains to be seen. In particular, store-of-value tokens such as Bitcoin could increasingly be seen as an alternative store of value due to their noninflationary nature. Most recently, Bitcoin has tended to show a high correlation with technology stocks, which, as mentioned above, tend to suffer from rising inflation.

3-Month Rolling Correlation of Nasdaq and Bitcoin, 11/2014-05/2022

Source: Reuters Eikon, Incrementum AG

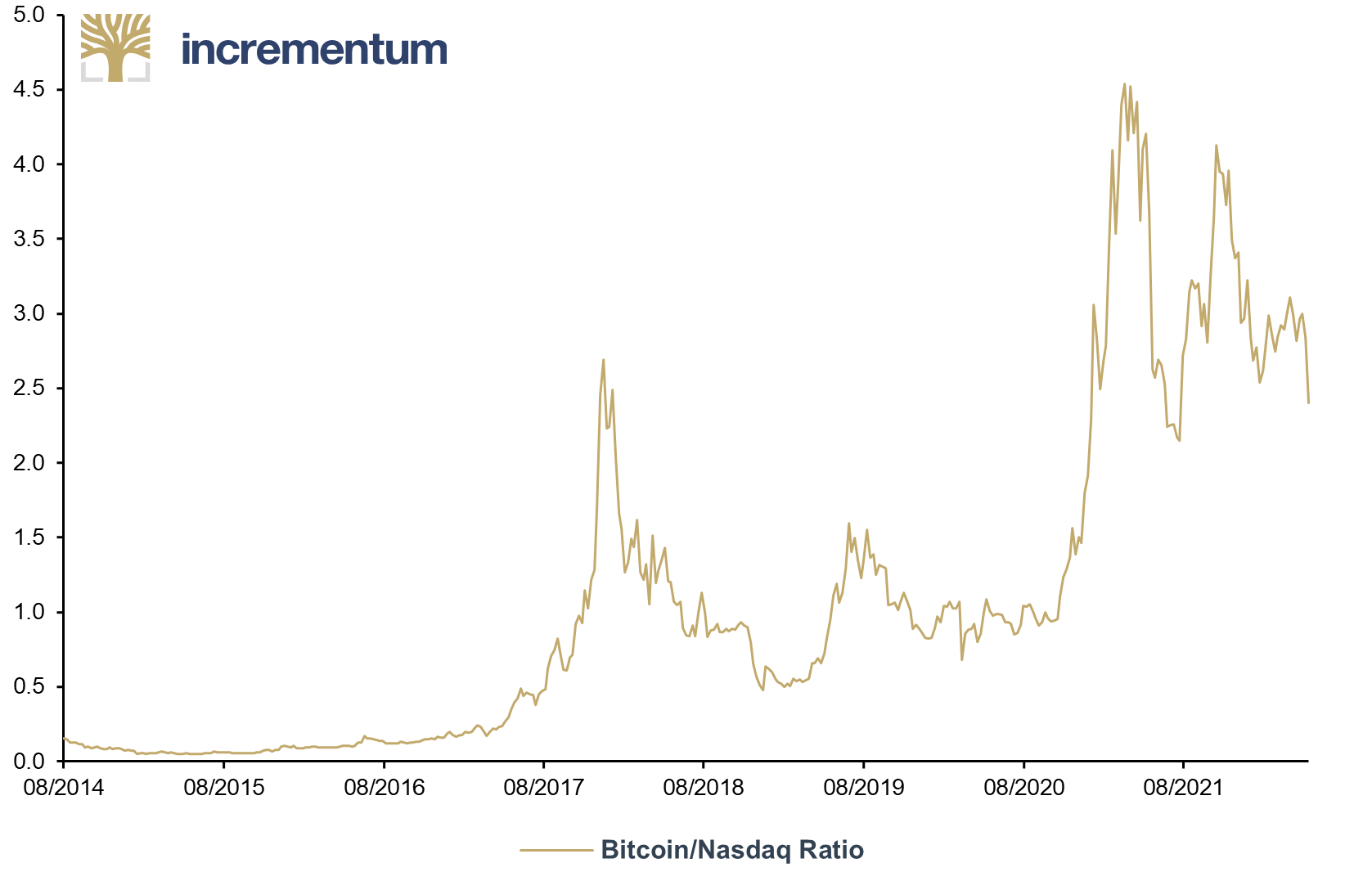

Nevertheless, one should not only look at the correlations in this respect but also keep an eye on the relative performance of the assets. The Bitcoin/Nasdaq ratio shows that Bitcoin has significantly outperformed Nasdaq over time. Against this backdrop, a certain admixture of Bitcoin with other inflation-sensitive assets seems consistently advisable in a balanced portfolio.

Bitcoin/Nasdaq Ratio, 08/2014-05/2022

Source: Reuters Eikon, Incrementum AG

Stagflation-proof fund strategies

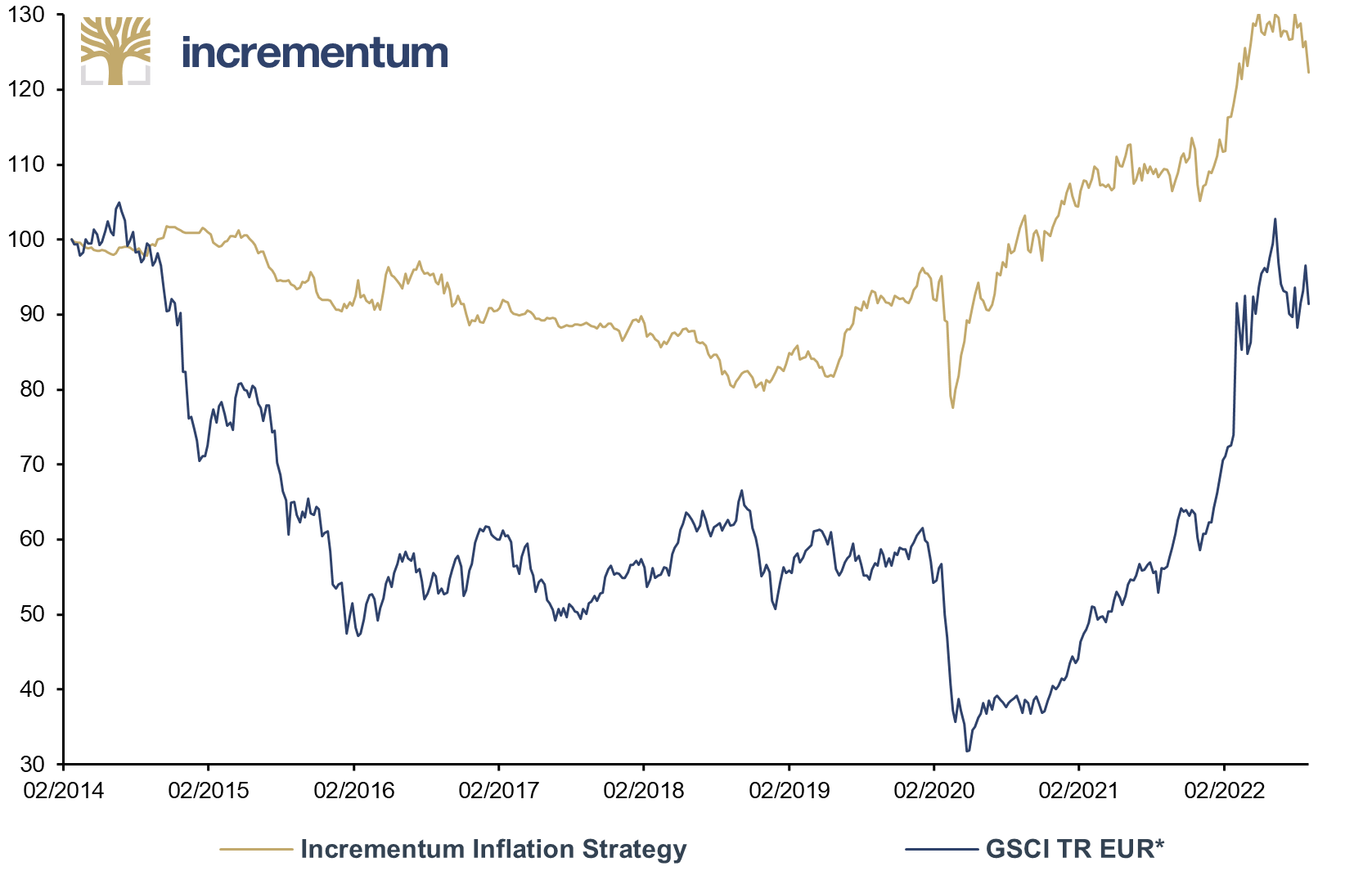

As we have seen, conventional portfolios are particularly vulnerable to rapidly rising inflation or stagflation. To diversify a broad portfolio, we designed an investment strategy more than eight years ago that focuses on inflation-sensitive asset classes. Our Incrementum Inflation Strategy is managed using an absolute return approach. The investment process focuses on flexible positioning for inflationary or disinflationary phases. The positioning is largely determined by our Incrementum Inflation Signal[6]. In this fund, we invest in a broad range of inflation-sensitive assets such as precious metals accounts, commodity stocks, derivatives on commodity indices, or inflation-indexed bonds. In addition, within this strategy we can tactically short technology stocks and bonds, for example. The strategy serves as a portfolio building block that can be added to a broad portfolio for diversification purposes.

Incrementum Inflation Strategy, and GSCI TR EUR*, 100 = 21.02.2014, 02/2014-09/2022

Source: Reuters Eikon, Incrementum AG

*Calculation incl. 1% p.a. TER

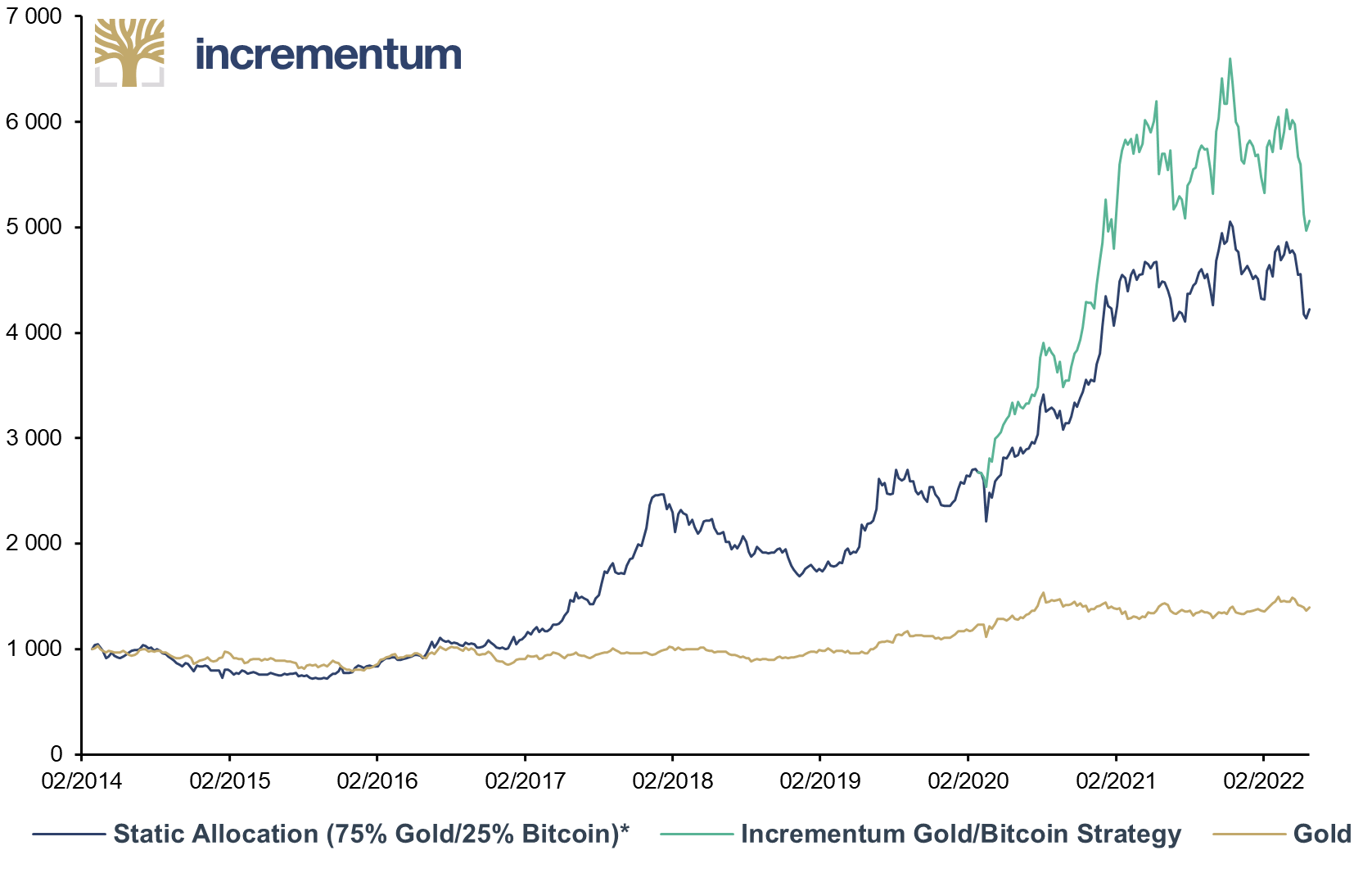

For crypto-savvy investors, we provide additional stagflation portfolio building blocks with our two crypto/gold strategies. We featured the strategy in the In Gold We Trust report 2019[7] and provided an interim report of excellent results in the In Gold We Trust report 2021[8]. We have taken the liberty to extend the price time series of the investment strategy by a back-calculated performance of the strategy’s strategic allocation of 75% gold and 25% Bitcoin by a few years to convey a better sense of the results.

Static Allocation (75% Gold/25% Bitcoin), Incrementum Gold/Bitcoin Strategy, and Gold, in USD, 1.000 = 02/2014, 02/2014-05/2022

Source: Reuters Eikon, Incrementum AG

*Calculation incl. 3% p.a. TER

The strategy has a low correlation to most other asset classes, which is why it can be considered as a diversification building block for balanced portfolios. We looked at some different combinations of these two portfolio building blocks. Again, to be able to look at a longer time horizon, we have extended the time series for the younger of the two funds, the gold/Bitcoin fund, by adding the strategic asset allocation of 75% gold, 25% Bitcoin.

Static Portfolio of Incrementum Inflation Strategy, and Incrementum Gold/Bitcoin Strategy*, 02/2014-05/2022

Source: Reuters Eikon, Incrementum AG

*until 02/26/2020 static allocation (75% Gold/25% Bitcoin), in USD

Conclusion

Stagflation means an extraordinarily challenging environment for investors. Conventional investment concepts, shaped by the disinflation of the past decades, are already starting to cost their investors dearly. An admixture of inflation-sensitive asset classes is recommended for anyone who wants to diversify their portfolio and hedge against increasingly likely stagflation. In addition to gold, these are primarily commodity-heavy investments such as commodity index derivatives, commodity equities or, with some exceptions, inflation-indexed bonds.

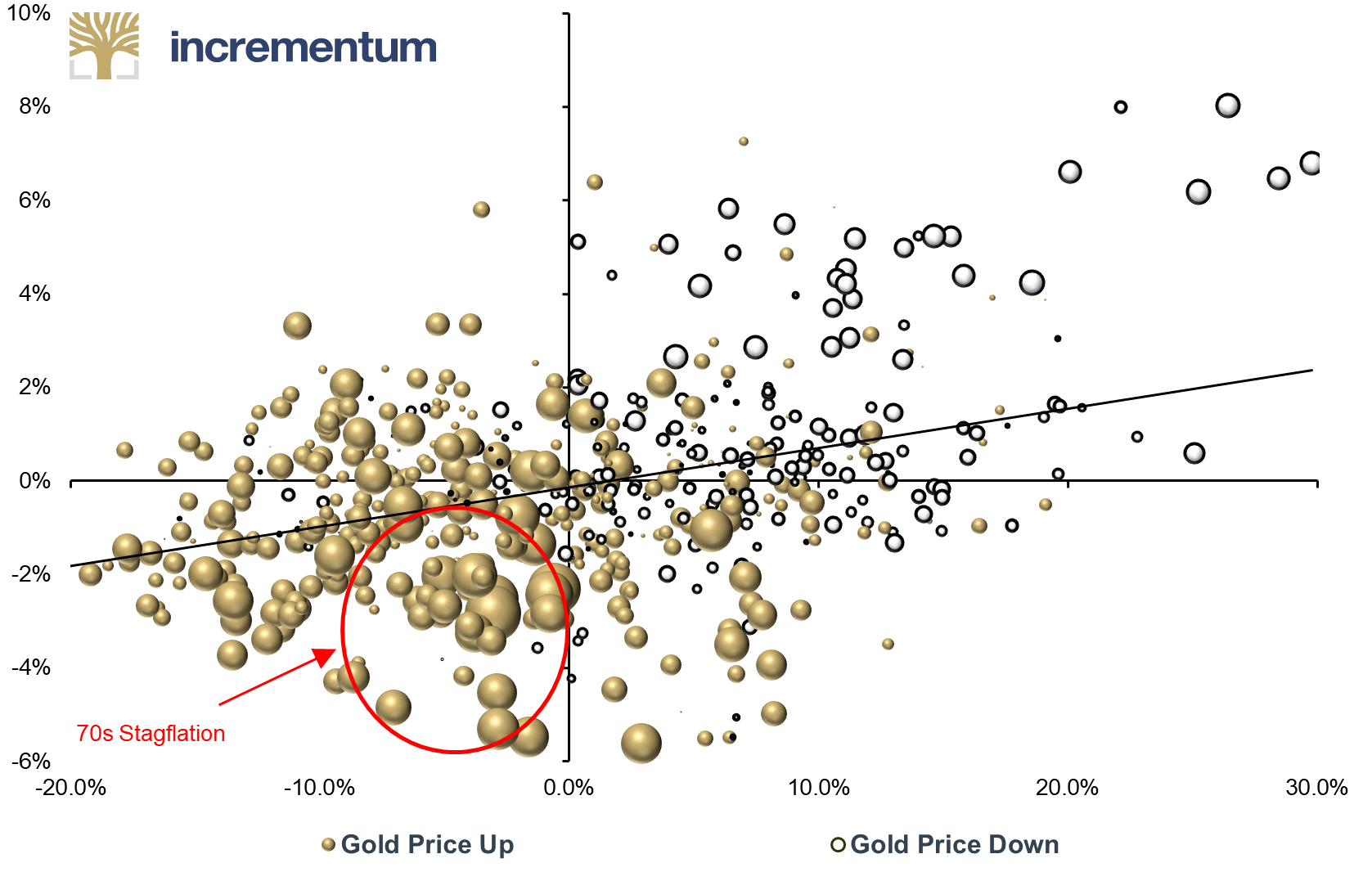

US Dollar Index (x-axis), yoy%, US Real 10Y Bond Yield (y-axis), yoy, and Gold Performance (Bubble Size), yoy%, 01/1972-04/2022

Source: Reuters Eikon, Incrementum AG

[1] See our interview with Iain Macleod’s nephew, Alasdair Macleod, titled “Stagflation and a New Gold Standard” in this In Gold We Trust report.

[2] Phelps, Edmund S.: “PCs, Expectations of Inflation, and Optimal Unemployment Over Time,” Economica, Vol. 34, August 1967, pp. 254-81; Phelps, Edmund S.: “Money-wage Dynamics and Labor-Market Equilbirum,” Journal of Political Economy, Vol. 76, July-August 1968, pp. 678-711

[3] Friedman, Milton: “The Role of Monetary Policy,” American Economic Review, 58, May 1968, pp. 1-17

[4] Mundell, Robert A.: “The Dollar and the Policy MixThe Dollar and the Policy Mix: 1971,” Essays in International Finance, No. 85, May 1971, p. 4

[5] See Duncan, Richard: “Stormy Weather Ahead,” October 15, 2021

[6] See chapter “Status Quo of the Inflation Trend” in this In Gold We Trust report

[7] See “Gold and Bitcoin: Stronger Together?,” In Gold We Trust report 2019

[8] See “Bitcoin & Gold – Our Multi-Asset Investment Strategy in Practice,” In Gold We Trust report 2021