Silver’s Decade

“The Federal Reserve has survived the fifty-year-old trial of fiat currency, but that period is less than a heartbeat in world history. Central bankers remain on trial, and the uncertain verdict sustains the ancient role of gold and silver as storehouses of value in the new millennium.”

William L. Silber, The Story of Silver

Key Takeaways

- Silver’s rally is likely to continue for the rest of the decade. We could be moving into an inflationary politician-led era of universal basic income, modern monetary theory, and government-guaranteed bank loan schemes. These trends will put upward pressure on the silver price.

- Silver is far and away the most heavily leveraged exchange-traded commodity. An August 2020 report by Macquarie put the ratio of derivatives to physical market at 193 for silver, compared to 86 for nickel and 74 for gold. This creates potential for a GameStop-style short squeeze on silver.

- The consensus opinion of professional silver analysts is that the world will broadly go back to the way it was before 2020. They are forecasting falling investment demand and lower silver prices for 2021–25, but we think they are mistaken.

- We believe the ‘go back to the way things were’ assumption will be proven wrong. The virus may have had little impact on silver sources, but it has had a profound impact on government and society.

Introduction

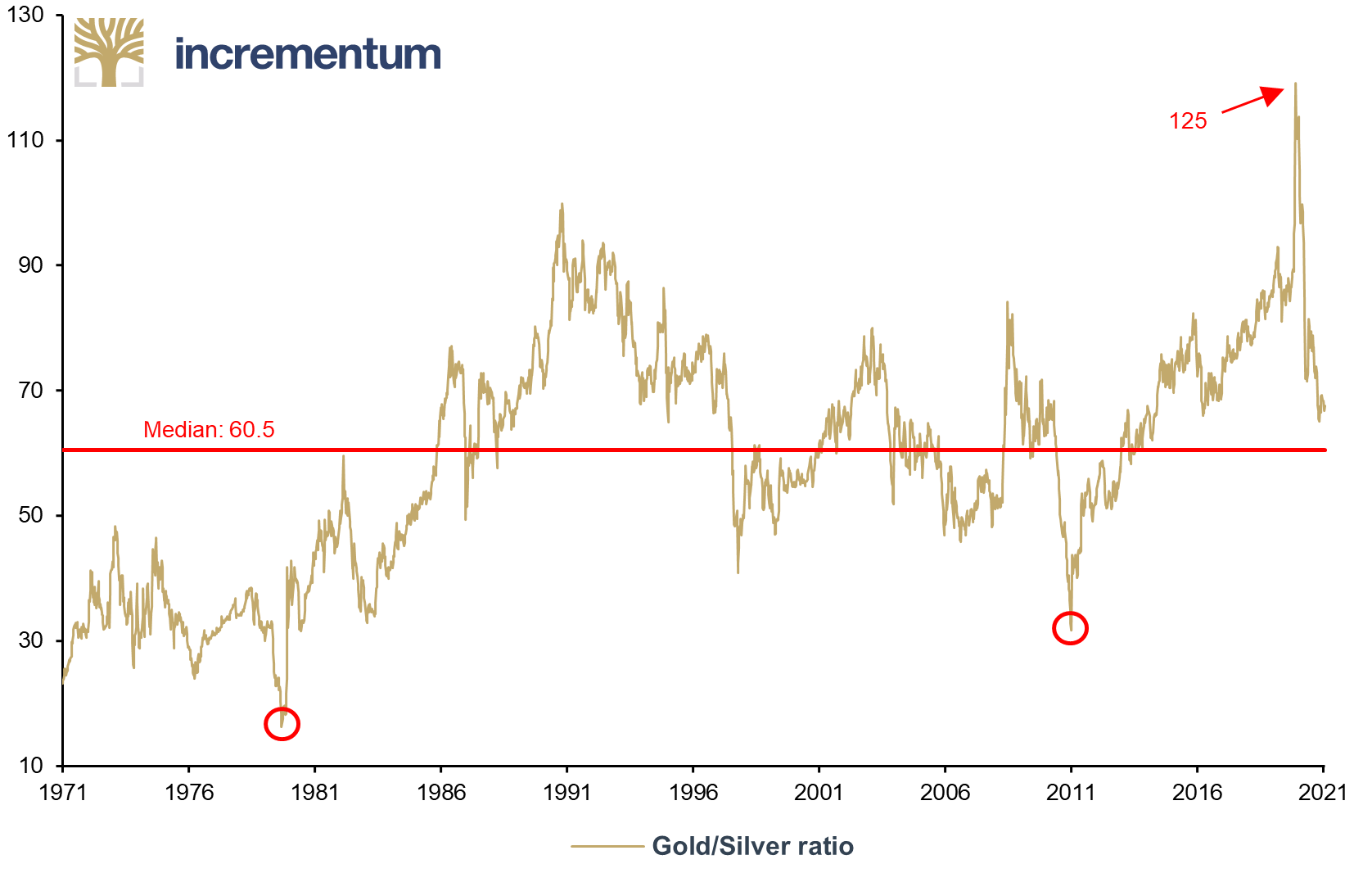

Last year, the In Gold We Trust legal department paled when our first draft offered the following investment advice: “Margin everything and buy silver! ”. To placate them, we couched the message as: “[T]his is history’s greatest discount on one of humanity’s most important and useful metals.” [1] Those words graced these pages after silver had just been valued as worth only 1/125th the price of gold.

The discount was truly the deepest recorded across the varied annals of humanity’s many civilizations. The sale remains very steep, even today. With the gold/silver ratio averaging 68.6 since the beginning of 2021, there remains much profitable territory to traverse. As noted last year, in the climactic final year of previous inflation eras, the ratio reached for example 16 in 1980 or 31 in the year 2011.

Gold/Silver Ratio, 05/1971-05/2021

Source: Nick Laird, goldchartsrus.com, Reuters Eikon, Incrementum AG

Silver’s advantage over gold is likely to continue for the rest of the decade, on the increasingly reasonable assumption that the world has exited the disinflationary, technocrat-led era of quantitative easing and entered the inflationary, politician-led era of universal basic income, modern monetary theory, and government-guaranteed bank loan schemes.

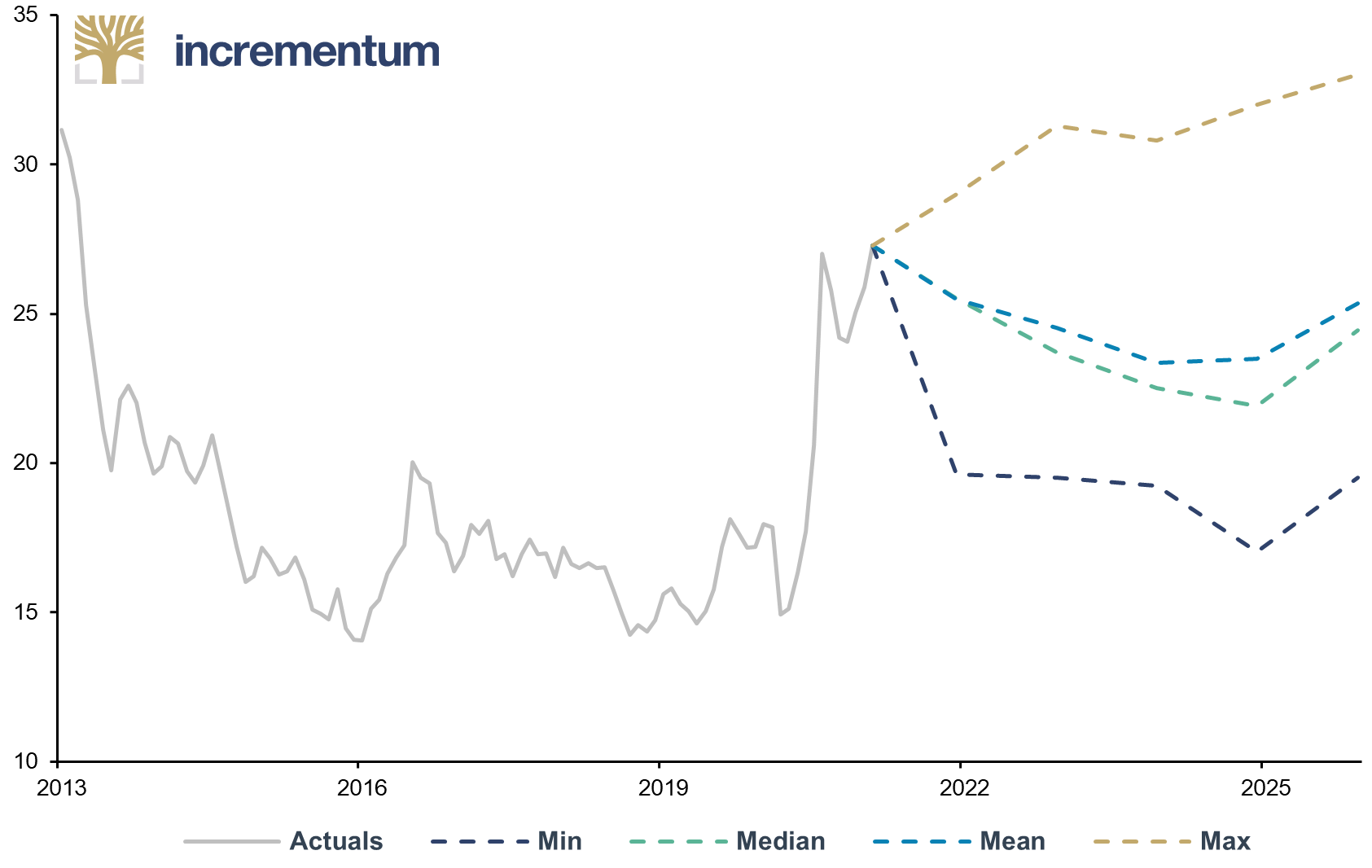

And yet the professional analyst community[2] seems oblivious to the changes 2020 catalyzed! Consequently, they are forecasting that everything will go back to the way it was, and they anticipate lower silver prices and meek investment demand through 2025.

Silver Price Forecasts, in USD, 2015-2025e

Source: The Silver Institute, Reuters Eikon, Bloomberg, Incrementum AG

In response to that forecast please allow us to state – in terms that counsel says will obviate any liability – that it is disheartening how little faith professional forecasters have in politicians’ resourcefulness and earnest desire to help millions… of registered voters.

Silver’s Outperformance of Gold

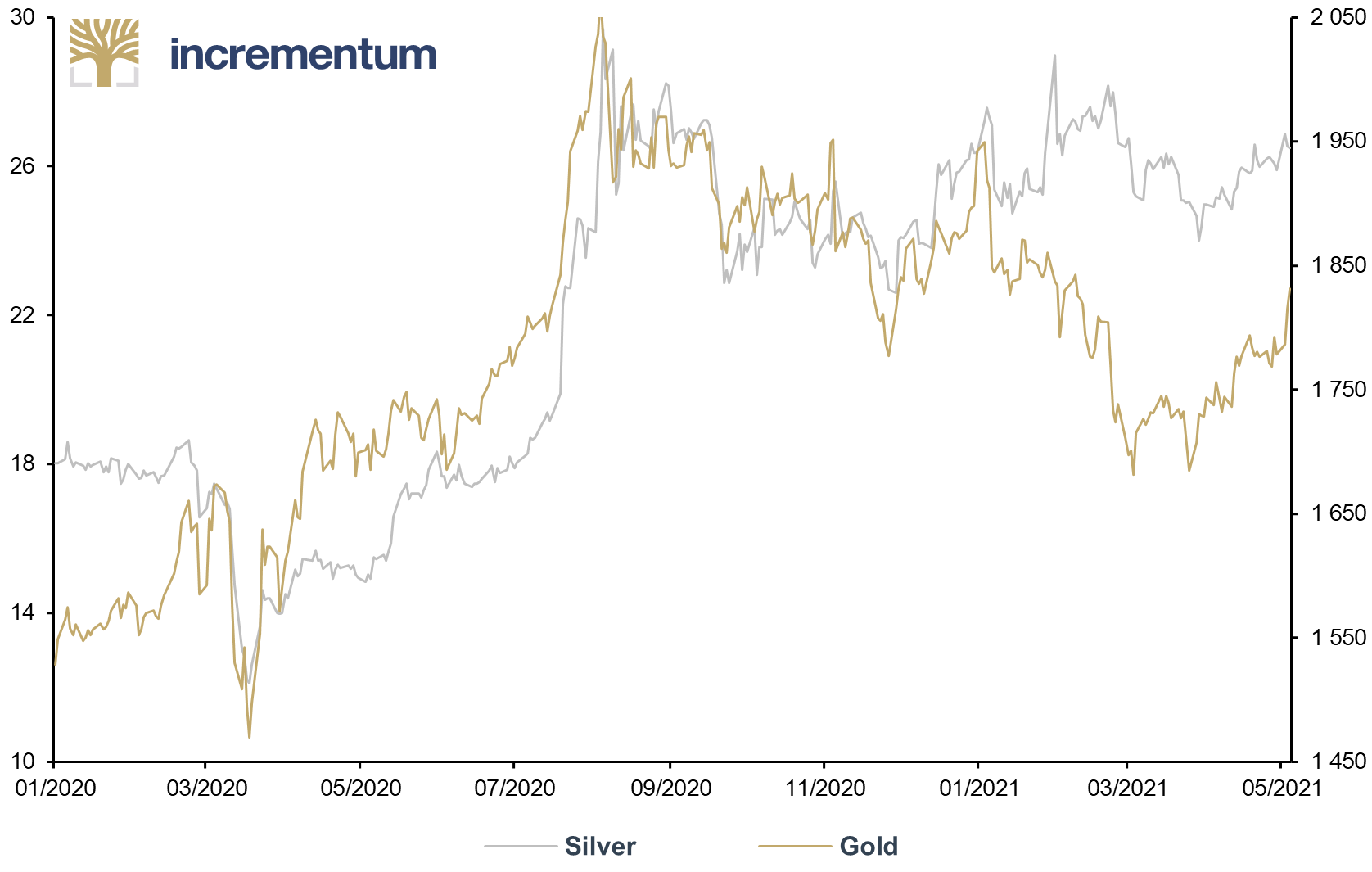

The US dollar price of both silver and gold peaked in August 2020, but whereas gold has been trickling lower ever since, silver has established a range. The difference can be explained simply enough, in that gold is a (the?) currency and silver is a commodity.

Silver’s cool gray quenches investors during the hot days of economic summer, when real economic activity heats up and inflation burns bright. Conversely, gold’s warm glow is prized most during economic winter, when business is in icy-cold deceleration, or outright contraction.

It is the latter condition that the world’s 19 largest economies have inhabited for six of the last eight quarters, from the third quarter of 2018 through the second quarter of 2020.[3] During that economic winter gold outperformed silver.

Silver (lhs), in USD, and Gold (rhs), in USD, 01/2020-05/2021

Source: The Silver Institute, Reuters Eikon, Incrementum AG

Courtesy of Hedgeye

Gold’s nominal US dollar rally continued through the first month of the third quarter, but the worst of the Covid-19 crisis was now passing – the virus was not the Black Death, and draconian government lockdowns began to phase out. Four consecutive quarters of accelerating economic growth lay ahead (through the second quarter of 2021). With an economic thaw it was silver’s turn to outperform.

Though both silver and gold were once monetary metals, the two elements have followed different evolutionary paths since the middle of the last century, and today they inhabit different financial ecosystems. Two out of every three ounces of gold demand is devoted to wealth preservation, demand by either central banks or households in the form of coins, bars and/or jewelry bought by weight. For silver that proportion is only one out of five ounces.

The reader may wonder if there exists an ecosystem where the two metals’ preferred “financial ecotones” overlap? Indeed, there is: stagflation. When an economy’s real growth rate decelerates as inflation accelerates both gold and silver – and commodities in general – appreciate nominally.

Covid-19’s Impact on Supply in 2020

The following section evaluates how the professional precious-metals analyst community reacted to the events of 2020. How have they adjusted their supply forecasts for 2021–25? What implicit assumptions are they making about the state of the world? Are there risks that the consensus underappreciates?

Total silver supply was 950mn troy ounces (Moz) in 2020, a 5.6% reduction to 2019’s total. The year took the analyst community by complete surprise, coming in at 98 Moz lower than forecast: equivalent to 9.3% of total supply.[4] Total supply from primary, secondary and other sources was the lowest since 2009.

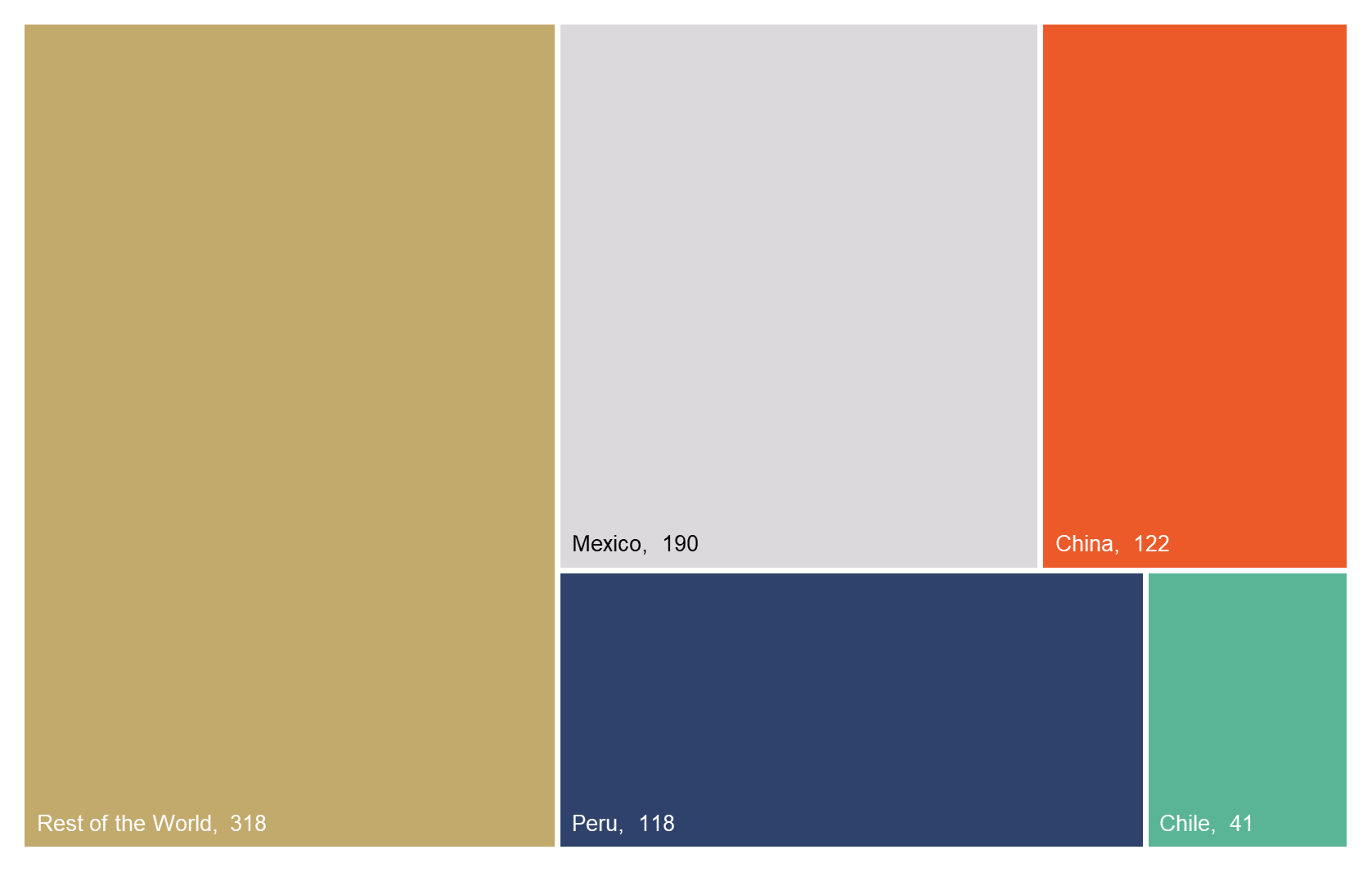

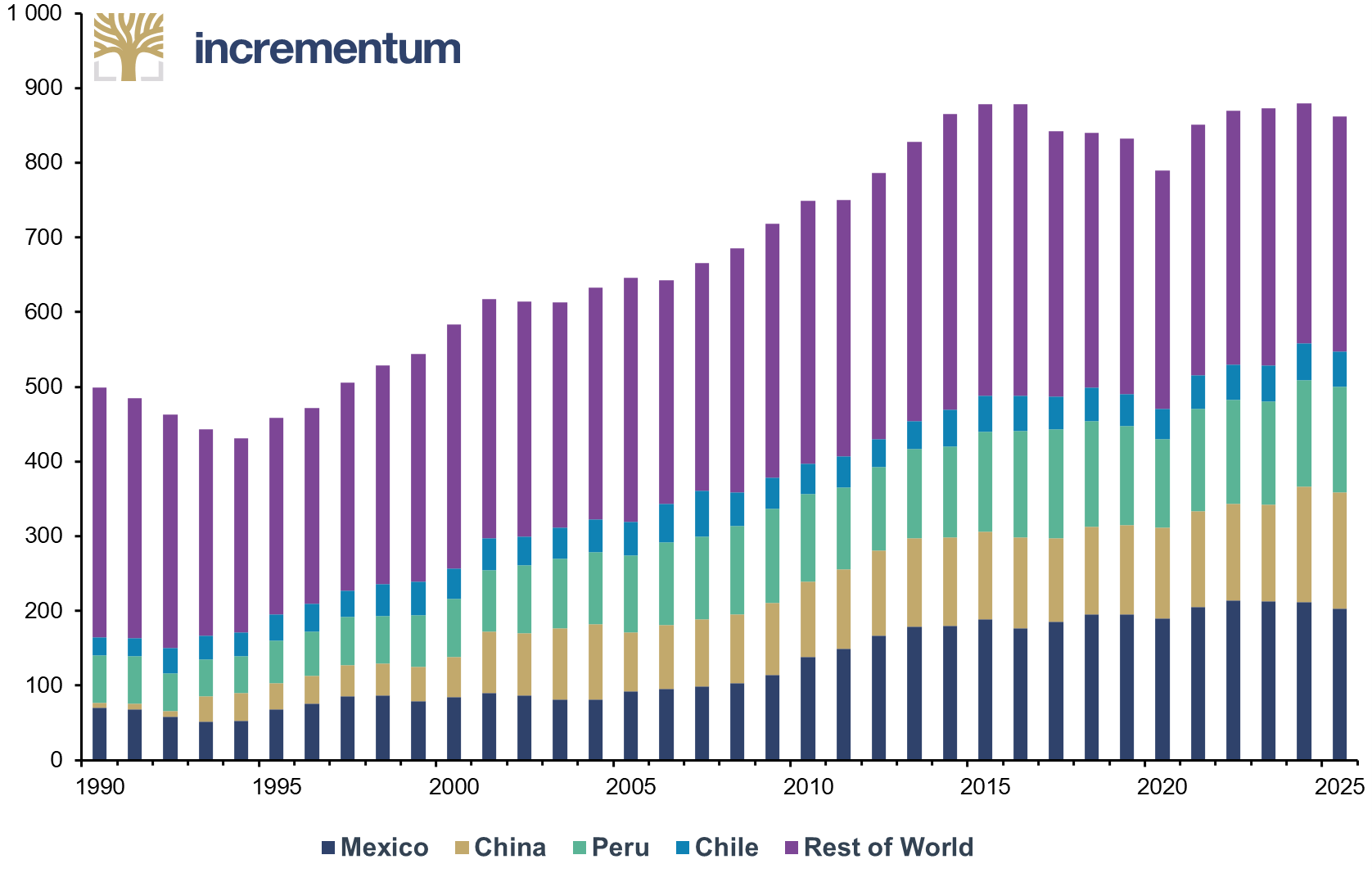

A combination of government-mandated shutdowns, on-site capacity reductions for social-distancing purposes, and logistical disruptions caused mine supply to come in at only 789 Moz, a 5.2% cut. The top producers of silver were Mexico, China, Peru and Chile, which in combination accounted for 59.7% of global mine supply.

Total Silver Mine Supply, in Moz, 2020

Source: The Silver Institute, Incrementum AG

Secondary sources of supply, like industrial scrap or recycled jewelry, which account for 16% of supply in a typical year, were likewise underwhelming.[5] Secondary supply is shepherded to the market by one of three factors: industrial processing, price increases, or economic hardship. With industrial activity at a stop world-around for weeks at a time, one would expect less scrap from that source. But this should be offset by jewelry, silverware, and coin turned in due to surging unemployment and rising silver prices, which climbed from a low of USD 12 per troy ounce in late March to just under USD 30 in early August. On net, secondary supply fell 3.8% year-over-year to 158 Moz. Relative to forecasters’ expectations the drop was steeper, a 6.0% loss to the pre-Corona outlook.

Covid-19’s Impact on Medium-Term Supply

How has the virus, and more importantly, governments’ and societies’ reactions to it, changed how forecasters now see the first half of this decade? Overall, analysts have lowered their expectations by 112 Moz for total silver supply over the 2021–25 period, a 2.2% reduction. Total supply is expected to average 1,039 Moz per year. The five years prior to 2020 produced a total supply average of 1,018 Moz.

Mine Supply by Country, in Moz, 1990-2025E

Source: The Silver Institute, Incrementum AG

Relative to 2020, pre-Covid forecasts, the consensus outlook for 2021–25 mine supply is now lower by 84 Moz. Though this represents a 1.9% reduction in expectations for the five-year forecast period, the 867 Moz annual average will be 1.5% more than the 854 Moz average achieved in 2015–19.

According to the consensus, secondary supply will contribute 169 Moz per year in 2021–25. That represents a total reduction of 21 Moz and 2.4% cut to expectations. The 2015–19 average was 163 Moz.

Secondary Supply by Sector, in Moz, 1990-2025E

Source: The Silver Institute, Incrementum AG

Points of Disagreement with Analyst Supply Consensus

It could be fairly said that the professional silver community does not believe the virus has had much impact on medium-term silver supply. During 2010–19 total supply was surprisingly consistent, only fluctuating between 999 and 1,064 Moz. The post-2020 forecasts have been reduced relative to pre-Covid-19 expectations, but those expectations were at the upper end of the decade-long range.

We believe the ‘go back to the way things were’ assumption will be proven wrong. Though the virus may have little to no impact on the silver sources themselves, it has had all the impact in the world on government and society. That will translate to a higher price – a price that reflects the new inflationary era we have entered.

We do not believe politicians, having tasted the sweet nectar of the magic money tree, will foreswear it in a display of stoic statesmanship. If it is election-facing politicians that will be determining money supply, and not appointed economists with bureaucratic tenure, silver will not stand idly by. Yet that is what the analyst community expects. The April 2021 analyst consensus forecast is for prices to fall throughout 2021–25.

Increases in silver’s price will likely result in more jewelry, silverware, and coin scrap supply than the analyst community expects. Similarly, mine supply, which is unable to accelerate as quickly, will likely be beating expectations by the end of the forecast period.

Covid-19’s Impact on Demand in 2020

The following section evaluates how the professional precious-metals analyst community have adjusted their demand forecasts for 2021–25. What implicit assumptions are they making about the state of the world? Are there risks that the consensus underappreciates?[6]

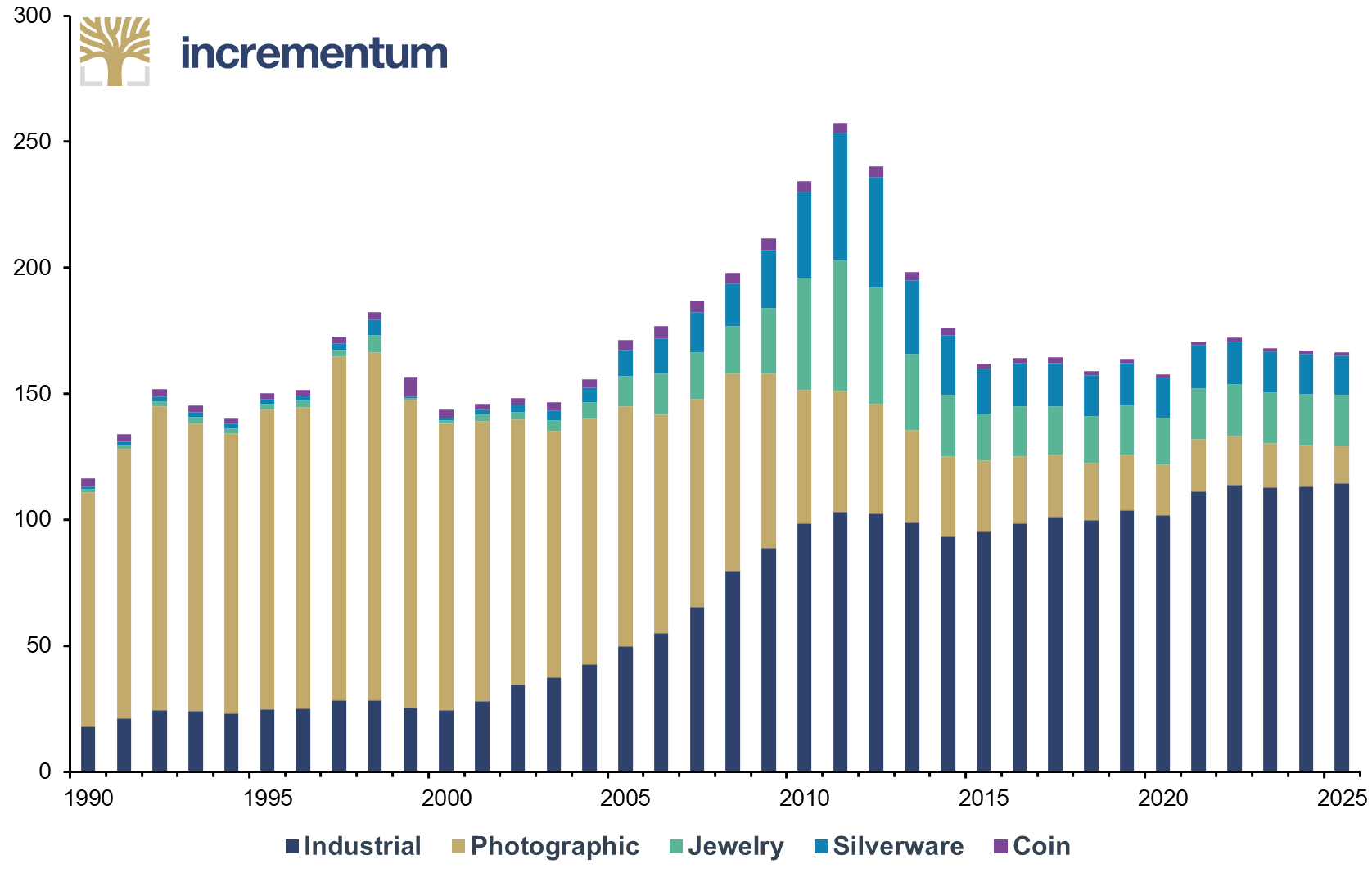

The four main categories of silver demand are: industrial, photographic, decorative and investment. Year-over-year demand fell by 4.3% to 942 Moz and came in a whopping 8.1% below analyst expectations. It was the lowest total since 2009.

Industrial Demand, in Moz, 1990-2020E

Source: The Silver Institute, Incrementum AG

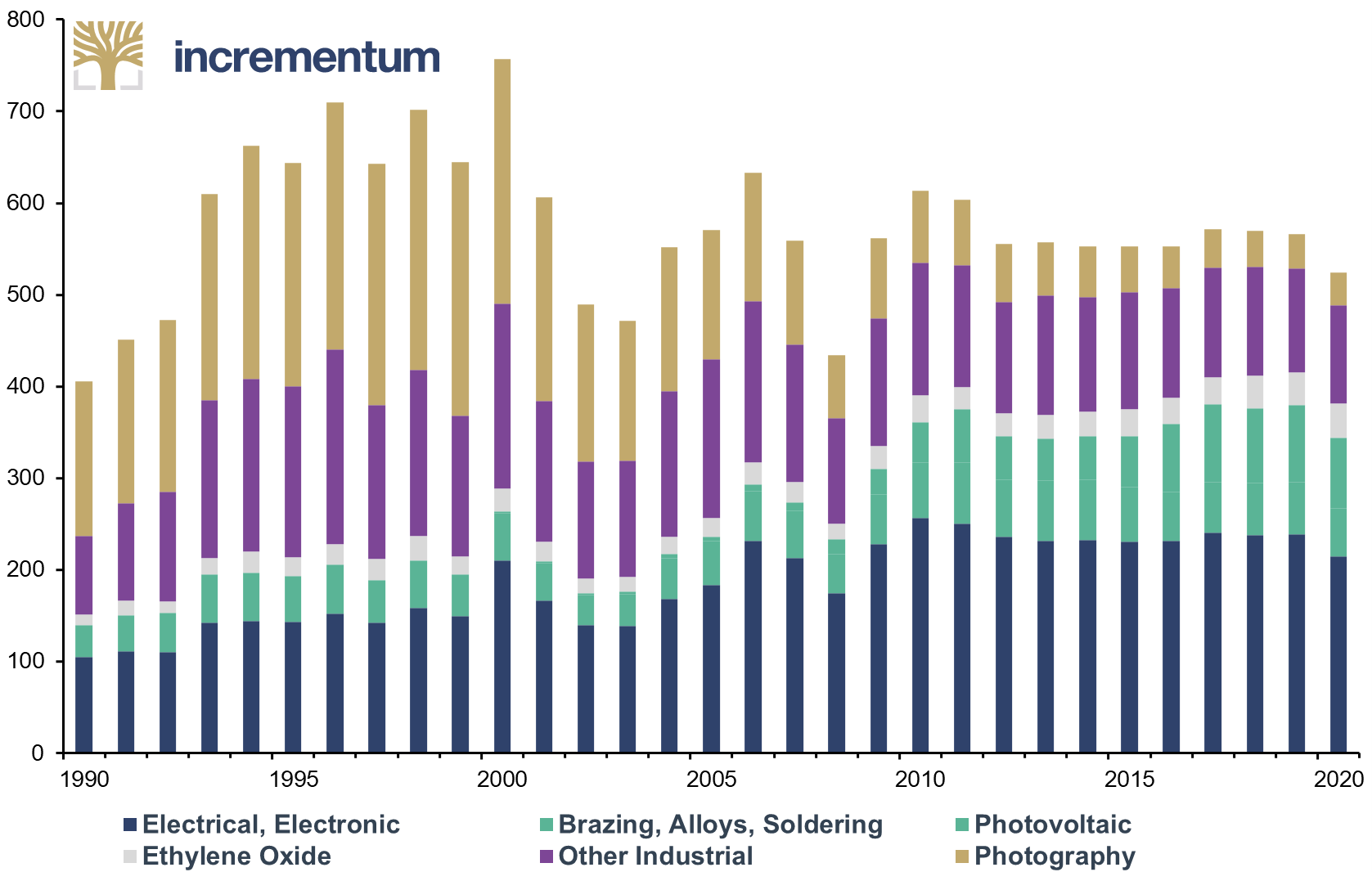

Industrial demand comprises solar panels, biocides, ethylene oxide, electrical connectivity, electronics, and brazing, alloying and soldering with silver, along with countless other applications. It accounts for 51.3% of total demand.[7] Last year the market only drew 490 Moz for industry, a total first reached in 2005. The year-over-year contraction was 7.3%. Analysts had expected 533 Moz, an 8.1% forecast shortfall.

Photographic film has been in a long-term decline with the advent of digital photography. From a high of 209 Moz in 2000 the industry only consumed 35 Moz in 2020. Analysts had anticipated 40 Moz.

The virus felled the decorative segment to just 237 Moz in 2020, a level first reached in 1993. Analysts had predicted that 276 Moz of silver would be adorned on the body and wielded at the dinner table. That would have been at the upper end of the jeweler-silverware range of the 2004–19 period, which averaged 252 Moz per year.[8]

Investment – in our opinion the most important price driver for the metal – is our last segment, and the trickiest to measure. It undoubtedly exceeded demand expectations, but it’s not entirely clear by how much. The segment contributes at least 18.0% to total annual demand. Looking at coins, medals and bars alone, the consensus expected 177 Moz in January of 2020 for the year ahead. When the year concluded, the figure is believed to have totaled 180 Moz.

What is not included in the above figures are changes in inventory held by exchange-traded funds (ETFs) or commodity exchanges. Estimates put the 2020 global ETF draw at 259 Moz, the largest in history. Commodity exchanges drew another 48 Moz, one of the largest draws in history.[9] If we added together coins, medals, bars, and visible financial inventories, then the total would stand at 488 Moz, the largest ever and on par with industrial demand.

Such a surge would correlate to the economic and social disorder we witnessed. It would be similar in spirit to the 118 Moz increase in 2006, the first year of the iShares Silver Trust exchange-traded fund. It would be akin to 2009, the first time this broad definition of financial silver breached 200 Moz and the last time the world was in such an economic hole.

Unfortunately, it is not clear what proportion of these financial-market products drew on newly minted bullion and how much came from existing stock. Some market analysts put this line item of ‘financial exchange silver’ above the bottom-line balance of annual supply and demand, but other analysts leave it as a memo item.

For our purposes, we can be satisfied in knowing that in 2020 investment was the only segment of silver demand that came in ahead of analyst expectations and grew year-over-year. This is true even if we entirely exclude ETFs and commodity exchanges.

Covid-19’s Impact on Medium-Term Demand

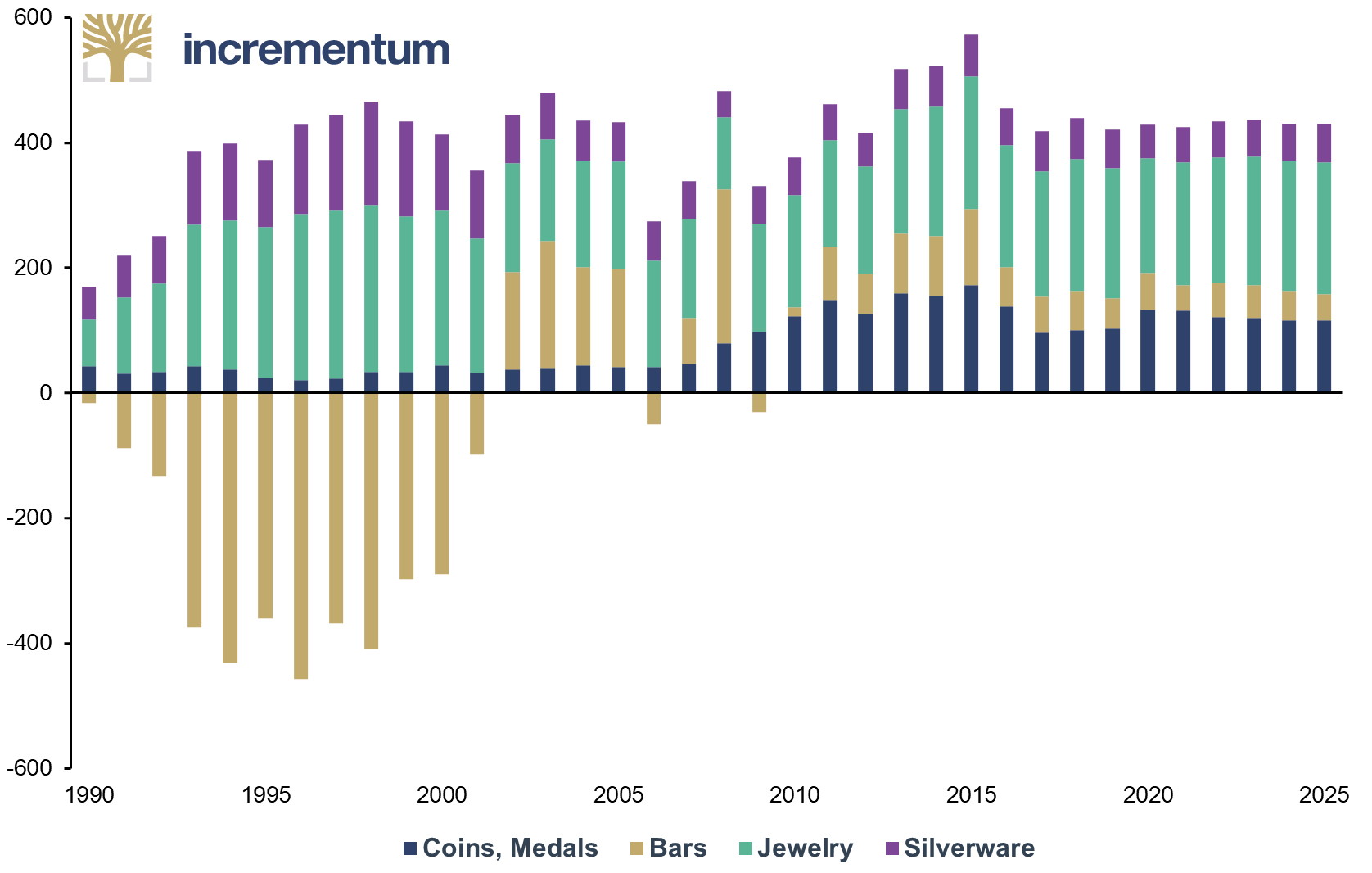

To summarize, the analyst community is optimistic that the monetary disorder is behind us, necessitating no further increase in investment demand for the 2021–25 period. At the same time, seemingly in contradiction, they are expecting non-photovoltaic industrial demand to be worse than previously anticipated because the economy will not have recovered to pre-2020 trends. This assumption about a weak economy is corroborated by their forecasted decrease in decorative end use, which is driven in part by gross domestic product growth.

Change in Demand by Category, in Moz, 1990-2025E

Source: The Silver Institute, Incrementum AG

Furthermore, analysts expect non-photovoltaic end uses to struggle while simultaneously expecting solar panel demand to rise faster than previously anticipated. Silver’s “green power” has been increased by 31 Moz in total for 2021–25. Whereas previously an average of 86 Moz per year were anticipated, that has been moved to 92 Moz by the analyst community. Experts are predicting that industrial demand will account for a greater share of overall silver demand, rising to 54.4% of overall demand from 2015–19’s average of 51.3%.

Photography has lost 10 Moz after Covid-19-inspired revisions. The dying segment is anticipated to die even faster now and only contribute 3.4% of demand per year on average (down from 4.2%).

Jewelry and silverware have been stripped by 68 Moz in this new consensus forecast. Instead of averaging 276 Moz per annum, we are told to expect 263 Moz annually for the decorative segment.

Investment, represented by coins, medals, and bars held outside of ETFs and commodity exchanges, is expected to be reduced by 14 Moz in total. The segment is being downgraded from 18.0% of overall silver demand to 16.5%.

Points of Disagreement with Analyst Demand Consensus

As suggested in the opening to the previous section, there is a disconnect in the analyst community regarding their acknowledgement that an economic disorder will continue to sap non-photovoltaic industrial demand, while at the same time they predict less investment demand. Let us now review where silver investors can profit from misplaced expectations.

We believe that analysts think 2020 did not change socioeconomic circumstances and that the world will return to the pattern of the 2007–19 period, where central bankers retain the primary role as economic steward, with occasional fiscal forays by politicians. In such an environment, nothing will help the real economy or real demand, as has been the case in Japan since 1999 and in Europe and America since 2007. That worldview would make the consensus analyst forecast for industrial and decorative demand perfectly reasonable. But then why are they expecting investment demand not to rise if the socioeconomic malaise is to continue? The 2015–19 average for bars and coins was 183 Moz per year, and yet that is expected to fall to 169 Moz for 2021–25!

The events of last year have raised the stakes on a 13-year Silent Depression, which bears an unwelcome resemblance to the 1873–1896 Long Depression and 1929–1947 Great Depression.[10] Politicians sense this, as do their challengers. Therefore, we believe it entirely reasonable to expect an increase in industrial demand outside of just photovoltaic demand, because the incumbents or their challengers are greatly incentivized to assume the primary role of economic steward.

Government will also step forward to push green energy. Silver can benefit in one of three ways here. Firstly, via the continued use of silver in solar panels. A review of seven forecasts for the year 2023 shows a range of between 8.4% and 15.0% of silver supply being devoted to solar panels. The high end of that range would demand 40 Moz more ounces per year relative to the existing consensus forecast. It could happen. As we explained in last year’s In Gold We Trust report, the history of the solar panel sector has been one where government drives demand. In the early 2000s it was Germany; then the baton was passed to Japan in 2011 and on to China in 2016. Who will anchor the solar panel relay? Perhaps the United States.[11]

Secondly, electric vehicles. For metal investors the focus is on electrification and battery materials, but that is not where silver’s star shines. Instead, the metal is doing very well as part of a revolution in network connectivity, a broad term that captures the idea of the car as a rolling collection of sensors. Silver use has increased dramatically over the years because of the myriad electronic gizmos attached to and integrated with the vehicle: display screens, blind-spot indicators, tire-pressure sensors, et cetera. For vehicle manufacturers silver is a high-quality product and a minor cost to the overall car. Other than gold, silver is the metal family’s best conductor of electricity.

Estimates put silver demand by the auto sector at 48 Moz in 2019. 2020 saw a reduction to 43 Moz owing to the Covid-19 recession. In 2016 the total was 45 Moz, which is indicative of the current lousy state of the global economy. In 2011 the figure was 20 Moz, and in 2006 it was 8 Moz. The analyst consensus is for this figure to incrementally rise to 71 Moz by 2025.

If politicians continue to offer a tax cut here or a spending program there, then the total just may remain more or less unchanged. However, if the rapid and comprehensive replacement of the combustion engine by electric cars were to occur, this would lead to a surge in demand for silver far in excess of the forecast 71 Moz.

The third ecological gain for silver would be a push into nuclear power. There are serious people who believe nuclear power is the antithesis of environmentally friendly. There are also serious people who argue that there is nothing greener than nuclear power. This is not the place to dwell on that debate, but we will mention that in 2018 CRU, the metals consultancy, estimated that nuclear power demand for silver was between 1 and 2 Moz per year.

The coming employment-heavy policies will need to be financed. Whether that is done via sovereign debt or modern monetary theory ‘printing’ or government-guaranteed loan schemes, in the end it is savers who will pay. Such financing will be a strong wind at the back of investment demand.

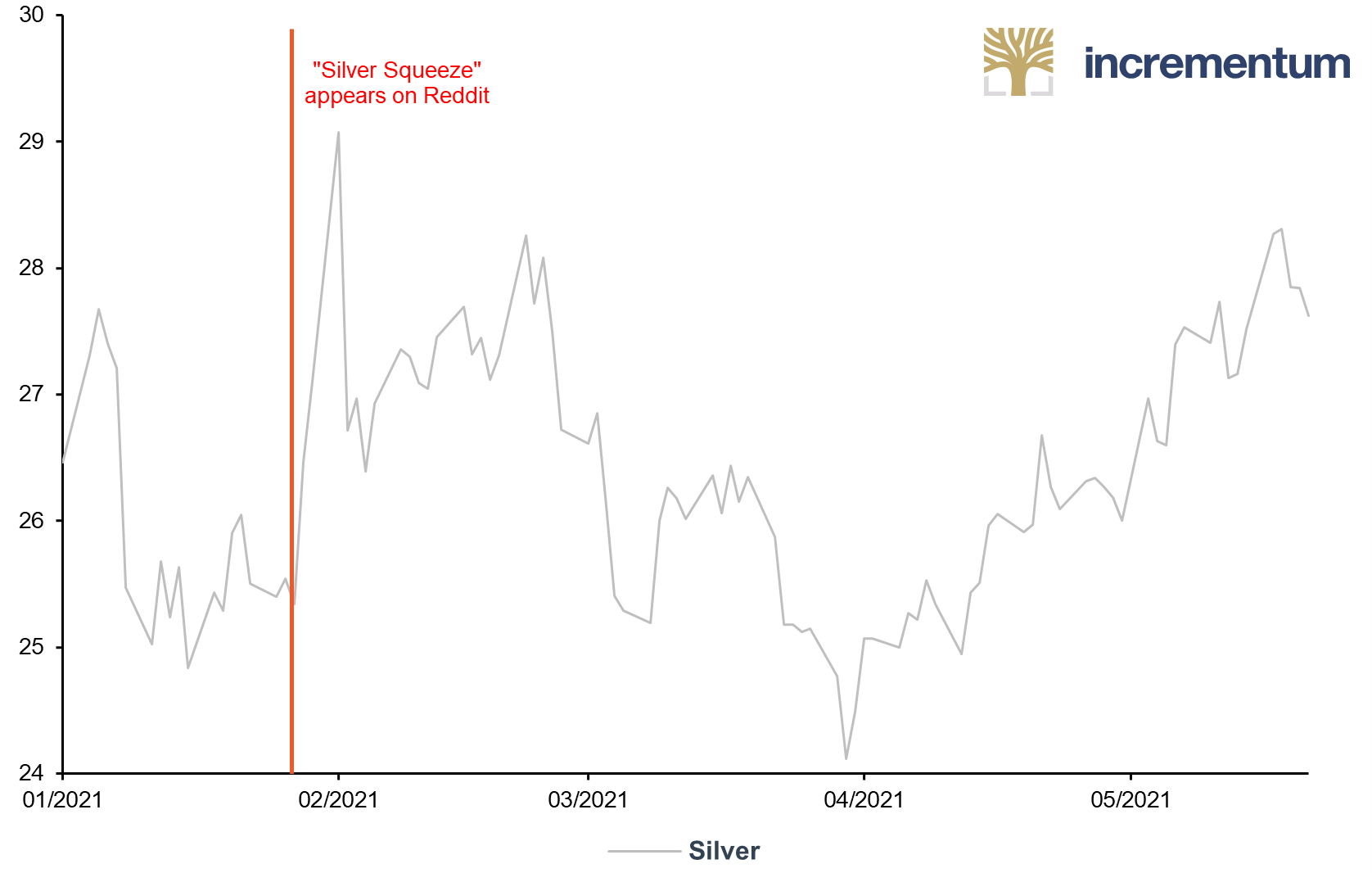

Silver GameStop Shorts

The other big event recently was the identification of silver as the next Reddit opportunity. Speculators, investors, day traders, and the most delightfully wretched collection of lovable rogues in all of finance inhabit the wallstreetbets thread.[12] They identified several stocks that were held very short. And they began to buy, hoping to tip the balance of the market in their favor. Over the course of just 4 trading days, the largest 10 physical silver ETF’s added an additional 3,600 tonnes of silver. However, the GameStop story we will not repeat here – you have no doubt heard it explained already. But one can see the result on this chart.

Silver, in USD, 01/2021-05/2021

Source: Reuters Eikon, Incrementum AG

Immediately thereafter this stunning success, silver was identified as the next such opportunity. Why silver? As explained in last year’s In Gold We Trust report,[13] the metal is far and away the most heavily leveraged exchange-traded commodity. An August 2020 report by Macquarie put the ratio of derivatives to physical market at 193 for silver. The second largest derivatives market relative to the underlying physical commodity was nickel, at only 86. Gold’s ratio was at 74.[14] It was no surprise silver was chosen.

But what was the impact on the price of silver? Can you identify it in the chart? We cannot. There was apparently a serious difficulty in buying physical silver in coin and bullion form. Delays were reported. There are some analysts that dismiss this as excited buying, exacerbating Covid-19-related supply chain disruptions. ‘Logistics’, they say, not the storming of the Bastille and revolution of the people.

Our sympathies lie with the ‘villainous’ Redditors. Yes, silver is ludicrously leveraged. Yes, the financialization of society and the economy is lurid. But no, the precious metals investor does not need to hope for the commodity exchanges to have their comeuppance to profit from silver. The trends are in the metal’s favor from a supply, demand, investment and inflation perspective. The decade ahead will likely show Wall Street Bets’ heart was in the right place; they were just impatient.

Conclusion

“Everyone’s looking for gold. So, I’ll be the one collecting the silver.”

Rehan Khan, A Tudor Turk

Silver’s rally is likely to last the rest of the decade, on the increasingly reasonable assumption that the world has exited the disinflationary, technocrat-led era of quantitative easing and entered the inflationary, politician-led era of universal basic income, modern monetary theory, and government-guaranteed bank loan schemes.

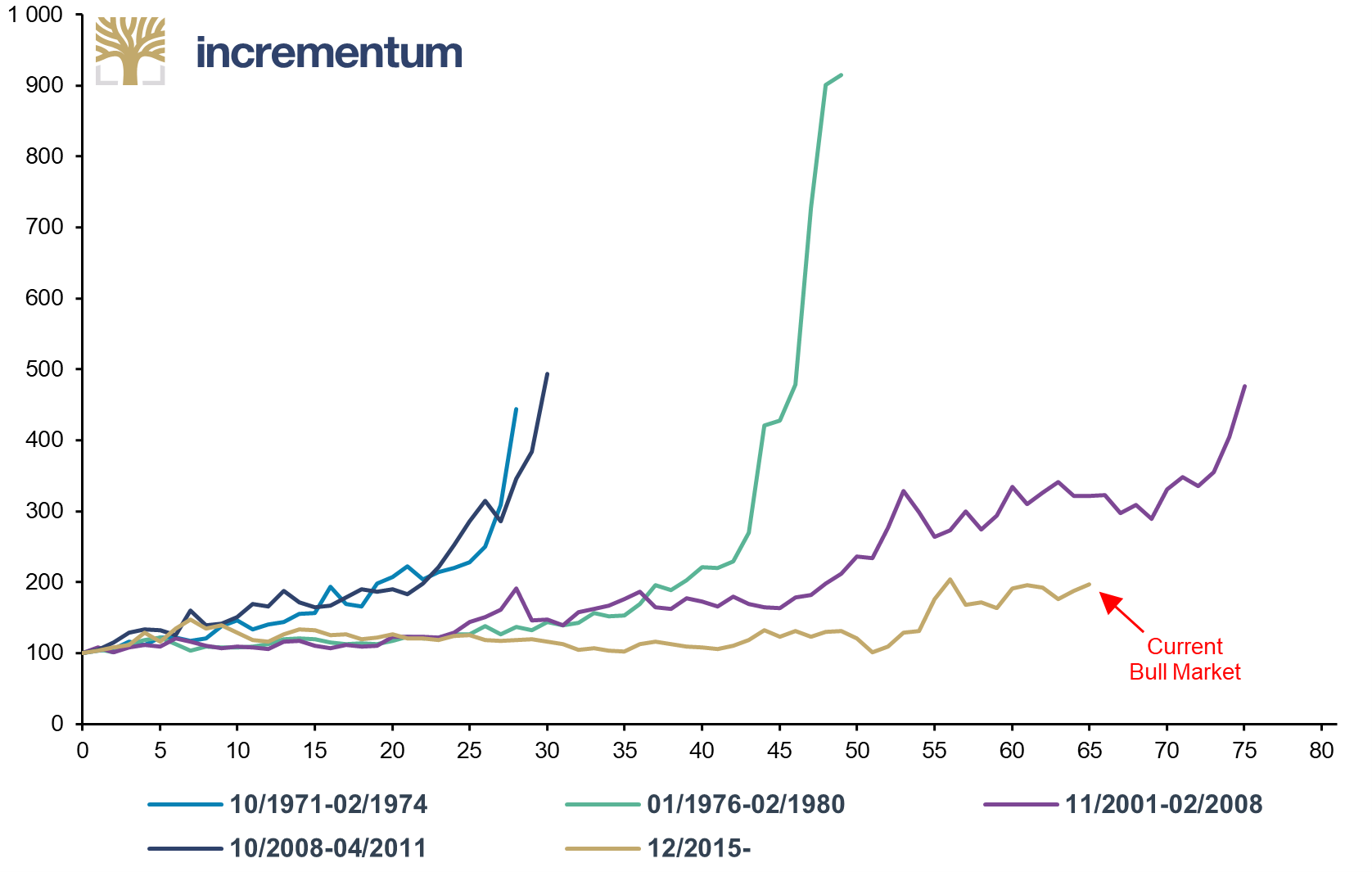

This does not appear to be the broad consensus of the analyst community, which is forecasting falling prices. If 2020 will not bring about a change in the socioeconomic scene, then perhaps they are correct. But if we are not going to back to the way things were, if last year represents a break with the existing political order, then an inflationary future lies ahead, and it’ll be a decade during which silver performs well. If history is any guide, as our last chart shows, the “fun” part of the move in silver has not started. Yet!

Silver Bull Markets, 100 = Start of Bull Market Cycle, 01/1971-05/2021

Source: Nick Laird, goldcharts.com, Reuters Eikon, Visual Capitalist, Katusa Research, Incrementum AG

[1] See “Silver’s Silver Lining”, In Gold We Trust report 2020

[2] All references to “analysts” or “consensus” in this chapter refer to the author’s collection of periodic commentaries produced by 19 different sources from: financial media, e.g. Bloomberg New Energy Finance; banks, e.g. Macquarie Strategy; consultancies, e.g. Metals Focus; industry associations, e.g. the Silver Institute; and government agencies, e.g. United States Geological Survey.

[3] “Jeffrey Snider: Making Sense and Money Out of The Global Monetary Madness”, Hedgeye Investing Summit, March 18, 2021

[4] When this article references the 2020 analyst consensus it is in reference to projections made in, or before, January 2020.

[5] The 2015-19 silver supply average is as follows: 83.9% primary mine supply, 16.0% secondary scrap/recycling, and 0.1% government sales and/or producer hedging.

[6] For a more in-depth review of demand end-use, see “Silver’s Silver Lining”, In Gold We Trust report 2020

[7] The 2015-19 silver demand average is as follows: 51.3% industrial applications, 26.5% decorative use, 18.0% investment bullion and 4.2% photography.

[8] There had been an even more auspicious period for silver decorative use, from 1996 to 2003 the world consumed an average of 294 Moz, reaching a high of 310 Moz in 1999, just before the good times ended. People used to approve of pleasure.

[9] We calculate 2016’s 69 Moz draw as the largest.

[10] As explained in greater detail in last year’s silver chapter, economic depression began in 2007 and has not stopped. A depression is not a very sharp recession, it is the inability to return back to the long-term growth trend that existed pre-crisis. A recession is a retreat from AND recovery back onto the growth path. A depression is retreat and then meandering growth. It is the lack of any economic upside. You may hear it referred to by other names like “lost decade” or “slowest recovery on record”.

[11] See “Silver’s Silver Lining”, In Gold We Trust report 2020

[12] Reddit.com: r/wallstreetbets

[13] See “The Dawning of a Golden Decade”, In Gold We Trust report 2020

[14] See “Derivative Market Dominance”, Macquarie, August 25, 2020