Quo Vadis, Aurum?

“Bad dreamer, what’s your name?

Looks like we’re ridin’ on the same train

Looks as through there’ll be more pain

There’s gonna be a showdown.”

Electric Light Orchestra, “Showdown”

- The time factor is significantly underestimated in terms of the impact of interest rate hikes. Given the rapid pace of monetary tightening, we expect a recession in the next 12 months.

- We are approaching a decision point in monetary policy. Due to the increasing fragility of banks, the real economy and financial markets, there will be a monetary policy showdown in connection with the expected downturn.

- The geopolitical showdown around the reshuffling of the world order is already in full swing. The structurally higher demand for gold from central banks will be a key driver of the gold bull market.

- Even though inflation rates in the US and the euro zone have fallen recently, we assume that another wave of inflation will follow and that the “Stagflation 2.0” environment will continue to accompany us.

- Gold price outlook: Based on the Incrementum Recession Phase Model, in the event of a recession, we would expect gold prices at USD 2,300–2,400 over the next 12 months. We continue to adhere to our decade price target of USD 4,800.

The Era of Multiple Showdowns

Stubbornly high inflation numbers, rising interest rates, recession warnings, a banking crisis with war going on simultaneously in Europe, tectonic shifts in geopolitical alliances, and intensified dedollarization efforts. We are not only in a time of multiple crises, but also multiple showdowns. The Chinese saying “May you live in interesting times” has an uneasy connotation and is quite possibly seen as a curse in China.

However, we do not want to see the circumstance of interesting times as a curse but rather as a challenge, as a task that now needs to be mastered. To this end, we should realize that while times of uncertainty and instability are challenging, they also represent an opportunity to sharpen our historical awareness and prepare for future developments. So what factors are particularly important for investors to consider in the current period of uncertainty and instability?

The Credibility of Central Banks Is Eroding

Confidence in central banks has undoubtedly taken a hit following their colossal misjudgment of inflation trends. Last year, we took a trip into the world of ornithology. We wrote:“While central bankers in the US, the UK, and other countries have been late in getting the cycle of interest rate hikes underway, ECB President Christine Lagarde and many other representatives of the Governing Council seem to have no idea at all what a monetary policy hawk is. An ornithologicaleconomic tutorial seems in order, because there are now fewer hawks in the ECB than chamois in the Netherlands. With the supposed gentleness of the dove, i.e. the greatest possible monetary policy passivity, the ECB hopes the inflation problem will disappear of its own accord. However, this view is not gentle or naïve, but rather incendiary.” [1]

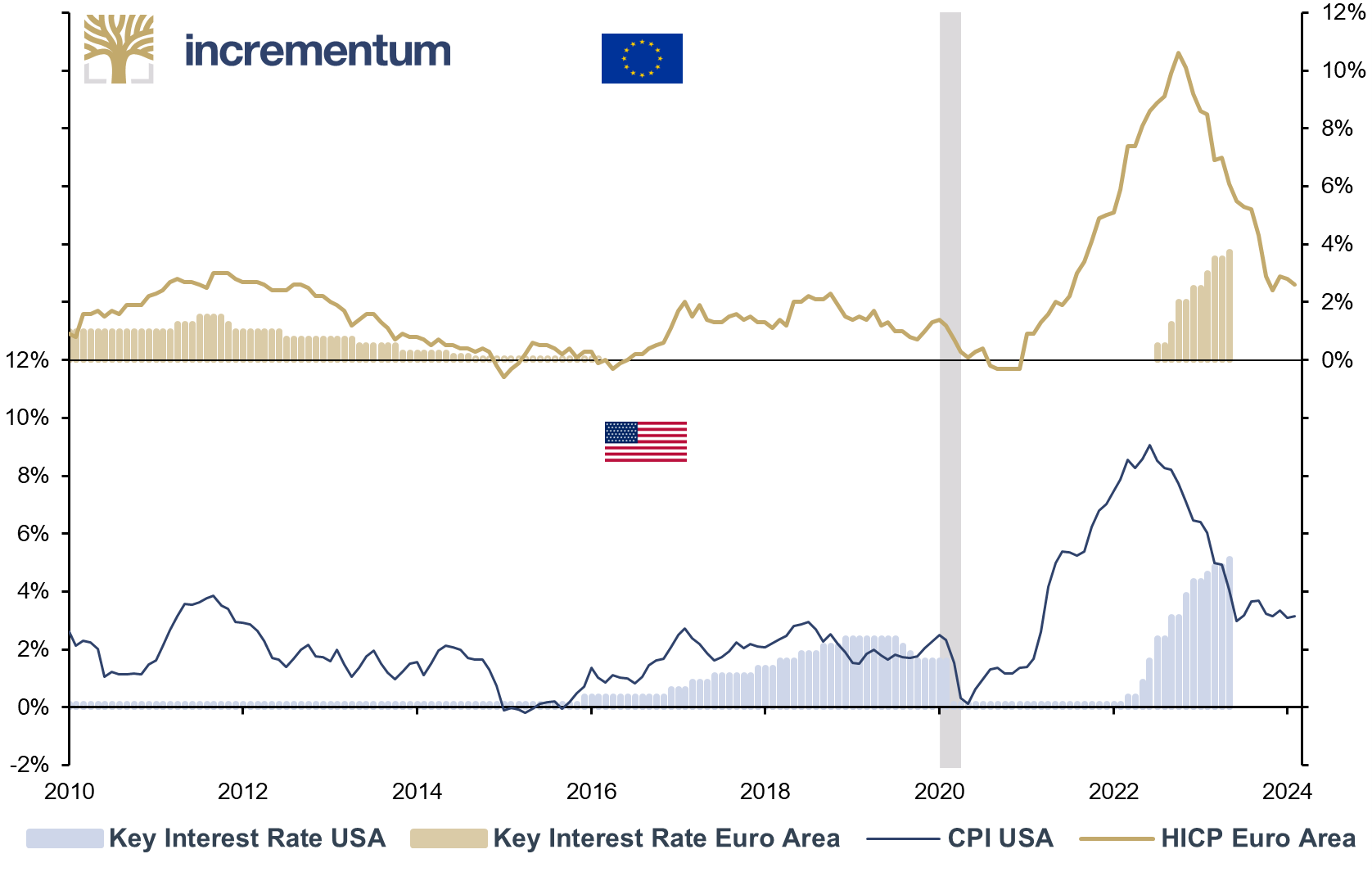

One year later, it can be said that the ornithological-economic tutorial we recommended was obviously urgently needed. While the Federal Reserve tackled the interest rate hike cycle late but ultimately consistently, the ECB reacted even later and far less spiritedly. In the US, the last wave of inflation peaked at 9.1% in June 2022, while in the euro zone it peaked at 10.6% in October 2022. The cycle of interest rate hikes has continued since then, rising to 5.25% in the US and 3.75% in the euro zone.Key Interest Rate, and CPI/HICP, USA (lhs), and Euro Area (rhs), 01/2010-05/2023

Source: Reuters Eikon, Incrementum AG

Are central banks now really in the process of turning their dove’s nest into a hawk’s aerie? We will only get the answer in the coming months, when the monetary policy showdown takes place. The Federal Reserve in particular has already been under pressure to act in the wake of the turmoil surrounding the three major bank failures and has reacted quickly. The recent expansion of the central bank’s balance sheet by USD 400bn is probably a tangible indication that, in case of doubt, it attaches higher priority to the stability of the banking sector and thus of the financial markets than to price stability. The bank failures that have occurred so far have not yet led to a system-threatening cataclysm. However, we firmly believe that a worsening of the crisis will also lead to an official reversal of the restrictive monetary policy.

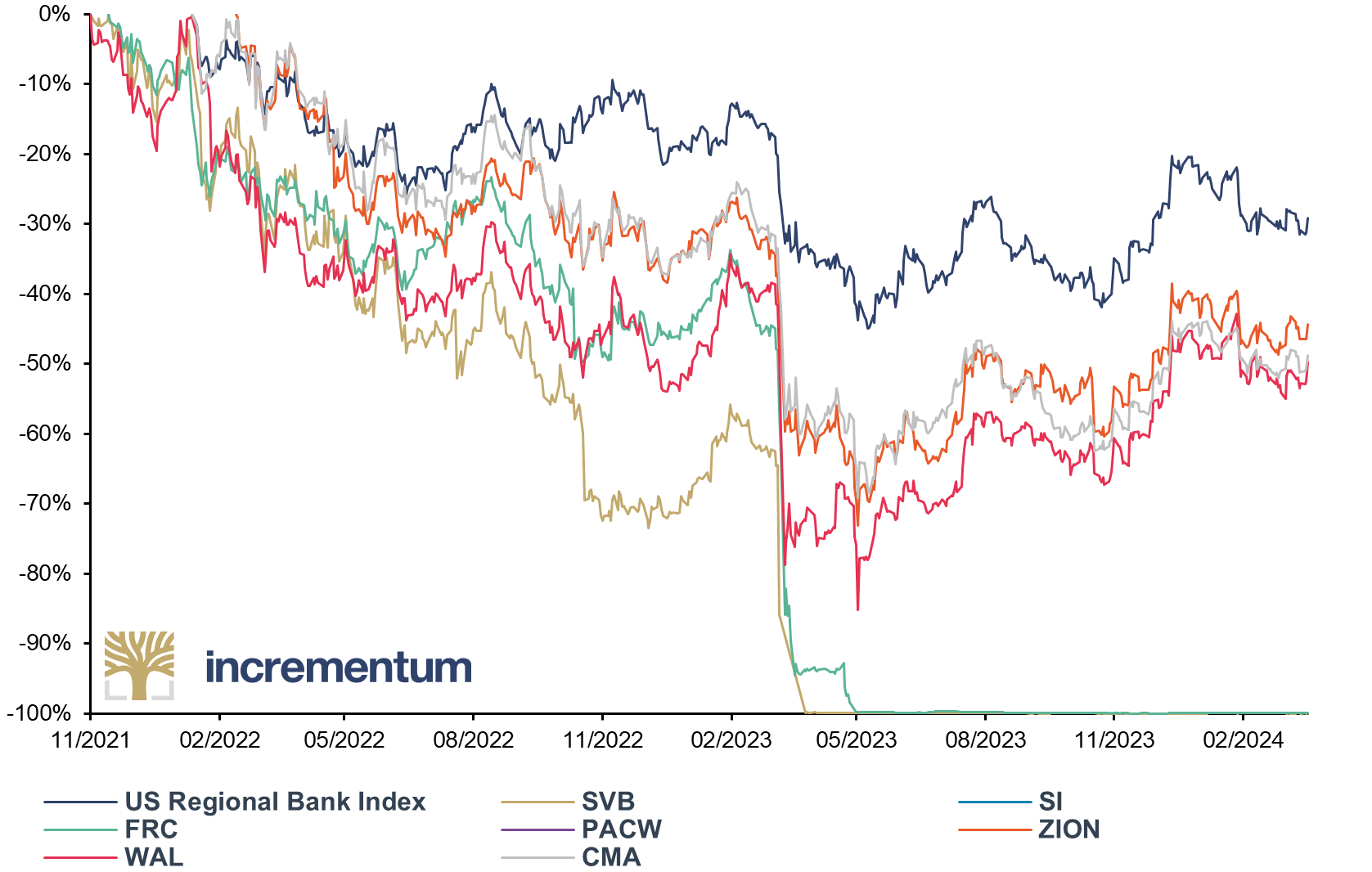

Recent events suggest that the hitherto tentative recovery in the reputation of central banks is already threatening to collapse again. On May 4, for example, Jerome Powell was still affirming that the US banking system was “stable and resilient”. But already on May 5, the share prices of some regional US banks collapsed again, in some cases even by half. Should further serious problems arise in the banking sector in the coming weeks, this could quickly lead to a calamitous loss of credibility, despite the central bank’s assurances to the contrary.

US Regional Bank Index and Various Banks from 2021 Highs, 11/2021-02/2024

Source: Reuters Eikon, Incrementum AG

The Underestimated Factor of Time

As we detailed in last year’s In Gold We Trust report, the originally stated monetary policy goal of managing monetary tightening and pushing inflation below 2% without triggering a recession, is unrealistic. We believe that an abundance of economic malaise is being revealed before us as a result of the full-throttle monetary policy stance. Monetarily induced booms always mask a multitude of financial sins and encourage herd behavior, false risk awareness, recklessness, and a this time is different mentality.

Warren Buffett compared interest rates to gravity: Just as the Earth’s gravitational pull affects mass, interest rates affect valuations. The more interest rates fall, the more valuations rise due to the discounting effect, to astronomical heights in the case of low and zero interest rates. When interest rates start to rise again, valuations come back down to earth. In view of the years-long boom in valuations during the many, many years of zero and low interest rates, this return to “normal” interest rate levels is tantamount to landing with a brutal thud on the hard ground of reality for many asset classes.

In our opinion, the time factor is completely underestimated. First, it takes some time for the expansion of the money supply to unfold in the real economy and drive up inflation rates. We once jokingly called this time lag the “Tequila Theory of Money”. A few shots of tequila in the evening undoubtedly help to lift the spirits at a party. It’s not until the next day that the inevitable consequences make themselves felt in the form of nausea, a stinging headache, and potential amorous missteps.

In 2022, the price dams began to burst, and after a few months of appeasement rhetoric about the supposedly temporary nature of inflation, panic broke out among central banks. In the US in particular, the emergency monetary policy brake was pulled. However, pulling hard on this brake – unlike applying a mechanical emergency brake – does not trigger any immediate consequences.

Now we have come full circle, and once again we have to warn about the lag effects, but this time in the opposite direction. The effects of QT and higher interest rates will be felt more clearly, day by day.

To illustrate the time lag of monetary policy actions, it is advisable for investors, especially the pessimistic bulls, to look at the recent past. In September 2007, then-Federal Reserve Chairman Ben Bernanke felt compelled to cut interest rates for the first time since June 2003, despite inflation exceeding 2%. By that time, the US housing market had already declined sharply. Although Wall Street initially went into a frenzy of joy, in 2008/2009 the US and with it the global economy slid into the biggest crisis since the Great Depression. The initial interest rate cuts completely fizzled out. The US CPI fell from 5.6% in July 2008 to -2% a year later. Stock markets hit their lows on March 9, 2009, only 19 months after the first rate cut and five months after the launch of QE1. So despite numerous headache pills, tequila continued to play havoc for a long time.

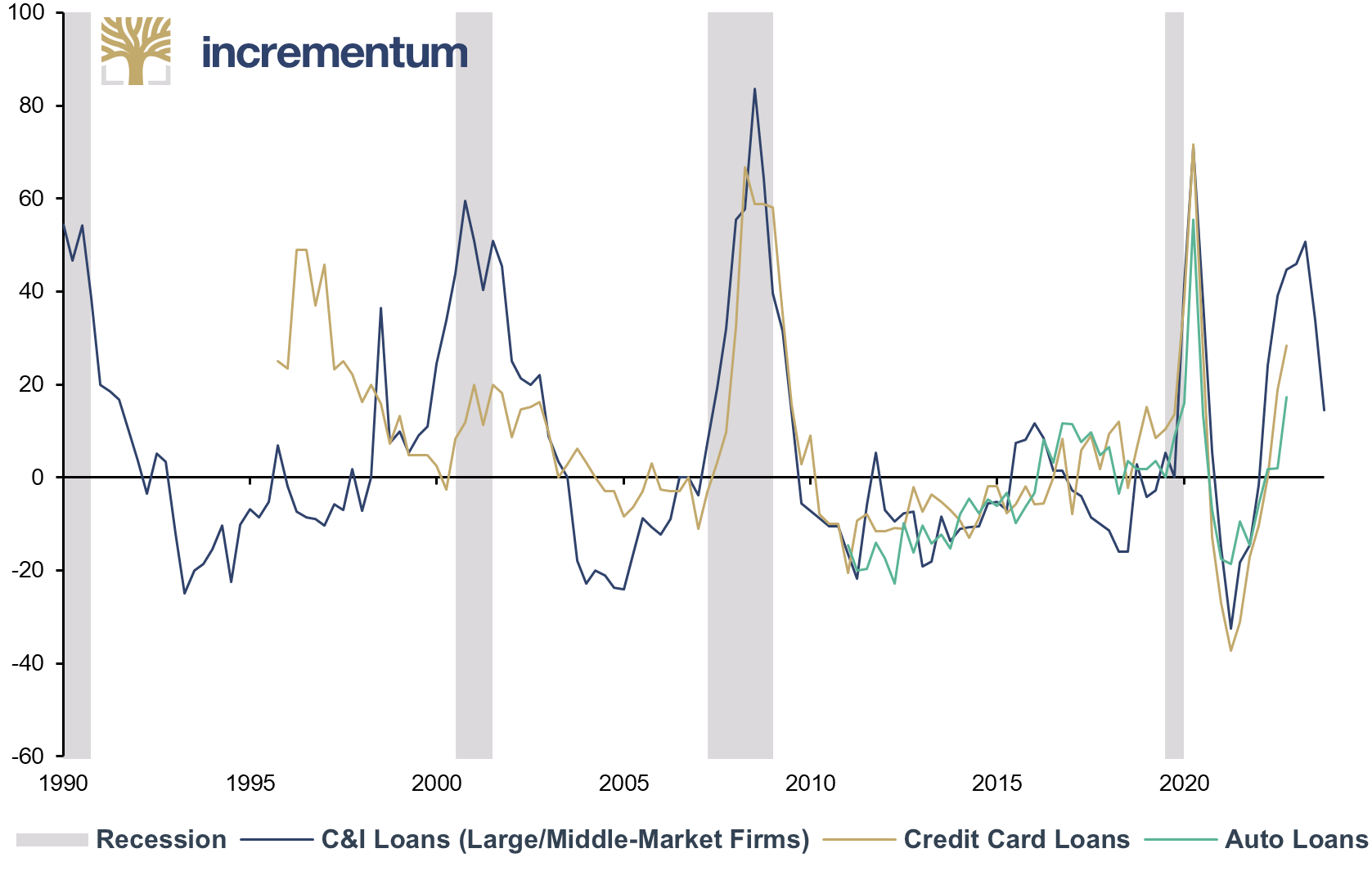

This example illustrates the considerable lag effects of monetary policy. It will take several more quarters before the consequences of the interest rate hikes of the past 14 months are fully apparent. The now-tighter lending conditions for businesses and consumers lead us to suspect that a disinflationary recession is becoming more likely by the day.

Net Percentage of US Banks Tightening Standards (Various Categories), Q2/1990-Q1/2023

Source: Federal Reserve St. Louis, Reuters Eikon, Incrementum AG

The crucial questions now are: Will the monetary tightening process reduce inflation far enough for central banks to save face and then loosen the reins again? And can the monetary policy withdrawal course be completed without causing too much damage to the economy and the financial markets? This will probably require iron discipline and political independence at the level of central bank leadership. Even if Jerome Powell wants to regain credibility and trust by alluding to Paul Volcker, we think the Volcker vs. Powell comparison is inappropriate. The main reason? The significantly worsened debt situation.

The Systemic Debt Problem

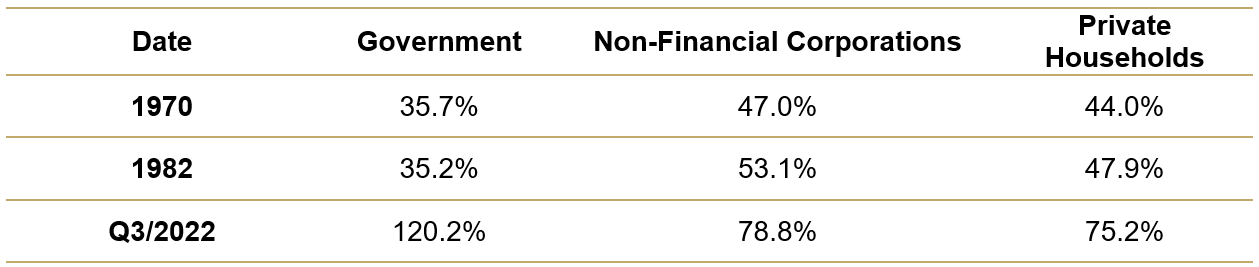

Both at the government and at the household and corporate level, debt is close to its peaks and many times higher than during Paul Volcker’s time. Accordingly, systemic interest rate sensitivity is also high today. The debt ratios by sector show the striking difference between today’s picture and the situation when Volcker was fighting inflation.

Debt by Sector, USA, as % of GDP

Source: BIS, Incrementum AG

While the commitment to sustainability is omnipresent in all areas of our lives, the sustainability of today’s monetary order is de facto not questioned at all. Banks and asset managers like to adorn themselves and the names of their investment products with fashionable terms such as ESG or sustainability, but seem to be completely ignorant of the ecological and social implications of the current monetary system.

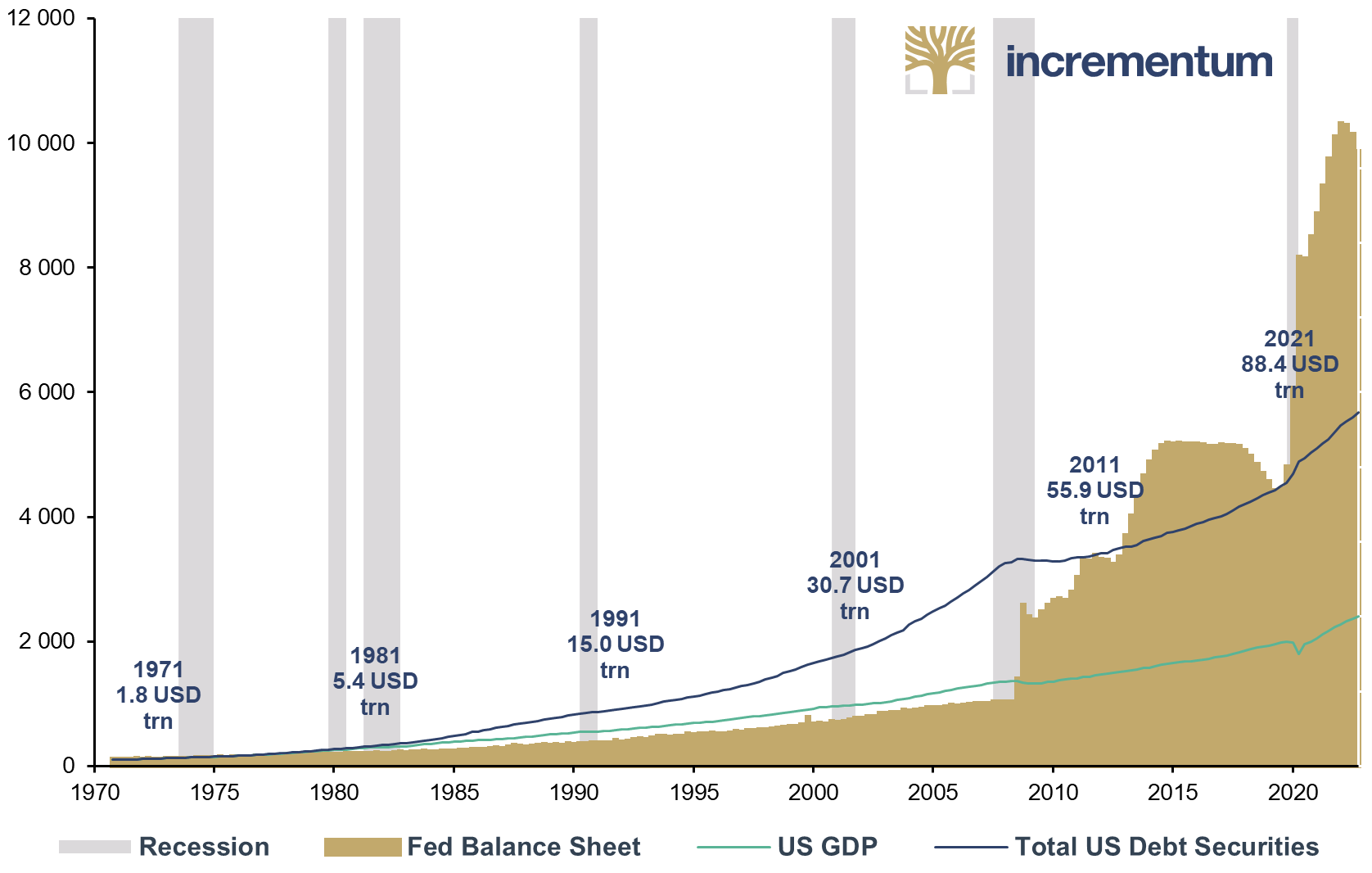

The unsustainability of debt-induced growth is impressively demonstrated by the following chart. Since 1971, total credit market debt – the broadest aggregate of debt in the US – has increased by a factor of 60, total assets of the Federal Reserve by a factor of 100, and GDP by a factor of only 24. In each decade, the volume of credit has roughly doubled over the past 50 years. A watershed occurred in 2009. For the first time, a decline in total debt was recorded in the course of the financial crisis, which was countered by the Federal Reserve with a massive inflation of the base money supply in the form of QE.

Fed Balance Sheet, US GDP, and Total US Debt Securities, 100 = Q4/1970, Q4/1970-Q4/2022

Source: Federal Reserve St. Louis, Reuters Eikon, Incrementum AG

This impressive illustration of the exponential growth of debt and money supply shows two things: on the one hand, the systemic unsustainability of the monetary system and, on the other hand, the impossibility of not leaving economic skid marks by a cold withdrawal of the drug credit.

The exorbitant level of debt is ultimately the main reason why the pressure on central banks not to raise interest rates further, or even to lower them again soon, is increasing with each passing day. It can be assumed that in the real economy, in society, and ultimately also politically, the calls for looser credit and QE are getting louder and louder. Whether the trigger for the next measures will be the stumbling real estate market, the troubled banking system, or rising unemployment is ultimately secondary.

Further Inflation Wave(s) Ahead?!

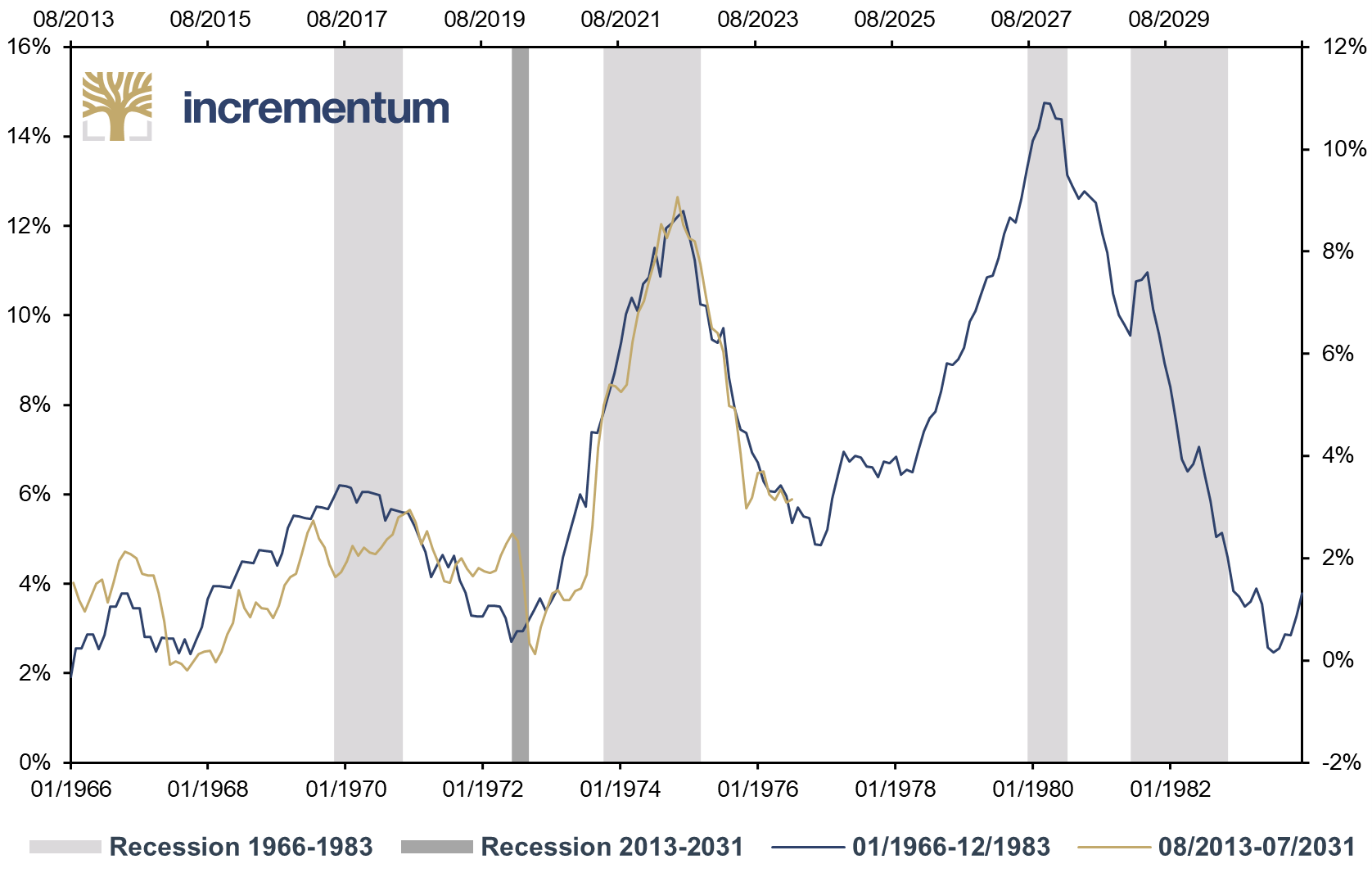

As we already explained in detail last year, we expect inflation to occur in waves. As the past has shown, the volatility of inflation also increases in an environment of elevated inflation rates. Comparing the current wave of inflation with those of the 1970s is interesting in this context, although the scaling is not the same. What is remarkable is that this comparison, which we already made in exactly this form last year, is still surprisingly apt 12 months later.

US CPI, yoy, 01/1966–12/1983 (lhs), and 08/2013–07/2031 (rhs)

Source: Andreas Steno, Reuters Eikon, Incrementum AG

We think the course of inflation in the 1970s provides a good indication of the future. Against the background of the problems described above, we still see predominantly disinflationary trends in the months ahead. However, this does not mean that the danger of inflation has been banished. On the contrary, a second wave of inflation will become all the more likely the sooner the restrictive monetary policy has to be abandoned. Moreover, there are a number of structural reasons for high inflation rates and high inflation volatility in the medium to long term. So what are the reasons for high inflationary pressure in the longer term?

On the demand side, the following reasons can be cited:

• Chronic budget deficits and increasing fiscal dominance

• Energy price mitigation programs

• Energy transition, decarbonization

• Rearmament and war economy

On the supply side, the following inflationary trends can be identified:

• Rising trade barriers, environmentally as well as (geo-)politically motivated

• Sanctions from unpleasant trading partners

• The trend toward nationalization of commodity producers

• Nearshoring of supply chains at the expense of efficiency

• Change of strategy in China: reduced dependence on exports

• Demographic change: working population (baby boomers) declining throughout the OECD as well as in China.

Monetary History Is World History

The current phase of the monetary policy showdown is accompanied by many uncertainties. However, the general degree of complexity is further increased by geopolitical dynamics and uncertainties. One intersection of (geo)economics and (geo)politics is particularly evident in the dedollarization we have been analyzing for years. In recent months, the BRICS countries have further intensified their efforts to reduce their dependence on the US dollar.

Paraphrasing Mark Twain, however, the obituaries for the US dollar are still premature, because currencies are network assets, and the US dollar, as the No. 1 global currency, enjoys all the advantages of a network asset. Louis-Vincent Gave compares the US dollar to Microsoft Windows. Even though Windows crashes from time to time and has numerous flaws, it is by far the most widely used operating system. A new operating system would not only have to be better but would also have to overcome the disadvantage of not being a network good to begin with. While many similar products can coexist in normal consumer goods, network goods tend to be a natural monopoly. Sometimes there are other competing products such as Mac OS or Linux, but these tend to have a shadowy existence in the overall picture and their use only brings advantages in certain networks. In these sub segments, however, they are the undisputed top dog. A currency is a classic network good; but law, language, messaging services such as WhatsApp, social media platforms, and ultimately cryptocurrencies are also network goods.

Gold is also a network good, perhaps even the ultimate monetary network good. In a fragmenting world, gold could be the monetary intermediary that prevents even greater economic disintegration. After all, gold is supranational, neutral, and without counterparty risk. Gold itself could be used in international trade, or in currencies (partially) backed by gold, with tokenized solutions playing a role here. This idea has already been floated by the BRICS. The high demand for gold by central banks suggests that gold is regaining importance in this time of multiple crises.

Central Bank Gold Holdings (lhs), as a % of Foreign Reserves, and 5 Year Rolling Gold Purchases (rhs), in moz, 01/1970-10/2022

Source: Crescat Capital, Reuters Eikon, Incrementum AG

Future Prospects: Money, Gold, and Bitcoin

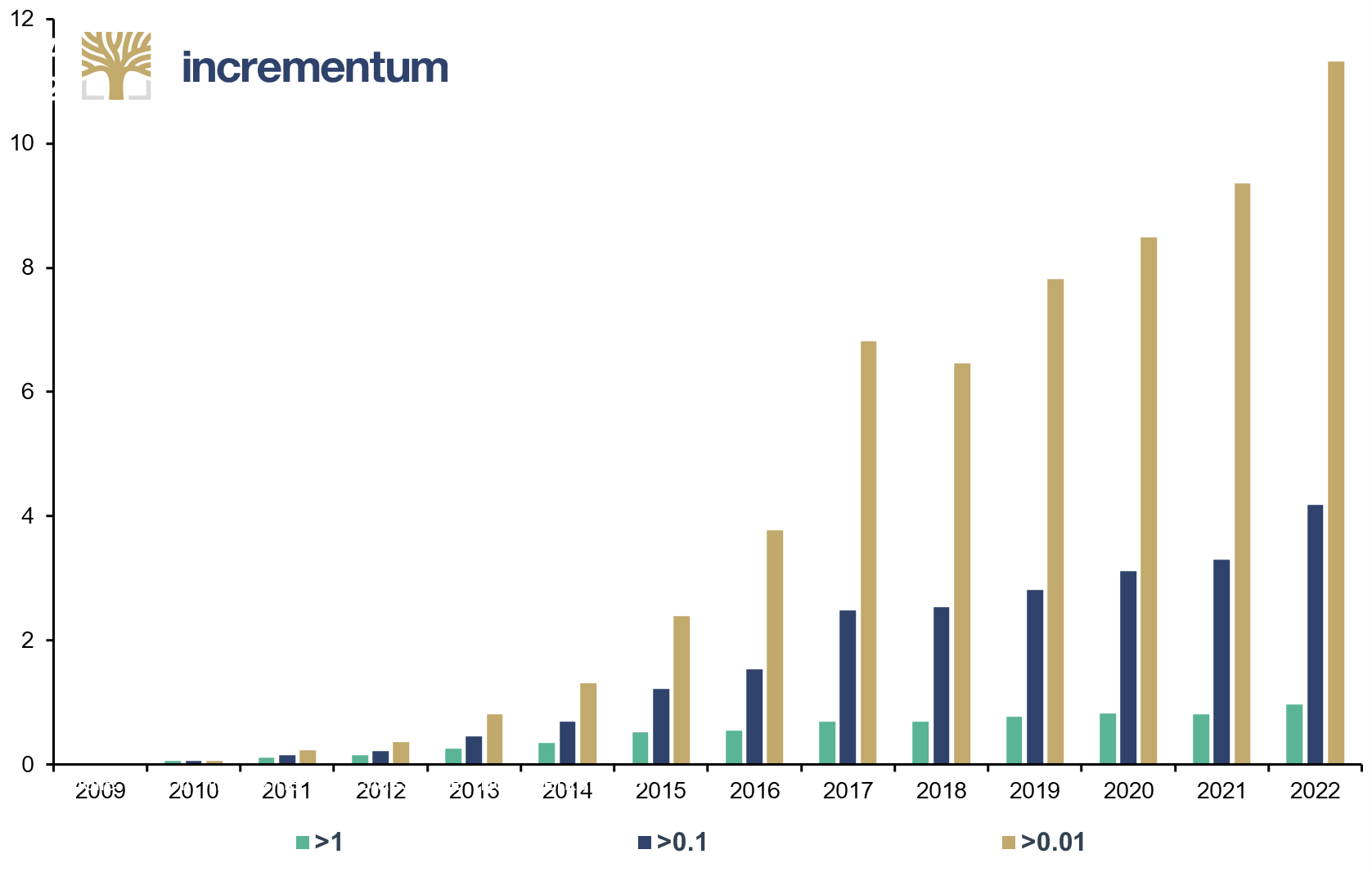

Knowledge of monetary history is essential when considering the role of money in times of change. In addition to awareness of the past, however, we also want to attentively examine recent technological evolutions. In 2015, we first looked at Bitcoin as part of the In Gold We Trust report.[2] Digital stores of value, especially Bitcoin, may change the way we think about money and store of value.Number of Bitcoin Addresses Holding at Least X Amount, in mn, 2009-2022

Source: Bitcoin Magazine Pro, Glassnode, Incrementum AG

Bitcoin’s network effect is clearly visible through the increasing number of users and wallets. As Bitcoin becomes more widespread and adopted, it becomes more attractive and increases its utility. Each new active user and wallet strengthens the network by increasing liquidity. This positive feedback effect strengthens Bitcoin’s position as the leading cryptocurrency and supports its potential as a money of the future.

An essential prerequisite for the increasing attractiveness of Bitcoin is its absolute scarcity due to the mathematically fixed upper limit of the supply to 21 million units. Currently, the number of Bitcoins mined is still increasing at about 1.6% p.a. – similarly slowly as the amount of gold mined annually. However, Bitcoin’s “inflation rate” halves at four-year intervals. Thus, after the next halving in April 2024, Bitcoin’s inflation rate will be lower than that of gold. In past cycles, the price of Bitcoin has invariably risen particularly strongly in the months before and after halving.

Bitcoin Performance after Halvings, 100 = Halving (log), 11/2012-05/2023

Source: Reuters Eikon, Incrementum AG

An intriguing question arises in the context of the geopolitical showdown: Can Bitcoin emerge as a winner from the current re-sorting of the world (dis)order? Despite the current de-globalization trends, it is inconceivable that trade between the rival blocks will completely collapse. Against the backdrop of growing geopolitical tensions, certain advantages of a decentralized cryptocurrency like Bitcoin seem obvious. Through its independence from government control and its cross-border transaction capability, Bitcoin would indeed offer an alternative to traditional currencies. We do not see such widespread adoption – aka “hyperbitcoinization” – at the nation-state level immediately. In the long term, however, such a breakthrough in the acceptance of Bitcoin cannot be ruled out and would probably cause an enormous stir – also with regard to the price.

The Renaissance of Commodities?

The sufficient availability of commodities was long taken for granted. Price increases and supply bottlenecks have brought a possible shortage of resources back into the public consciousness. On the one hand, the topic is relevant in connection with the energy transition, whose political prioritization raises the question of the availability of needed raw materials. On the other hand, there is burgeoning resource nationalism. A good example of the paradigm shift in the importance of raw materials is the automotive manufacturers. They are increasingly making direct investments in mine operators or strategic supply agreements in order to ensure secure access to raw materials.

As we stated in our chapter about the capex situation,[3] the lack of investment in the past is an obstacle on the way towards better availability, greater independence and, above all, lower prices of raw materials. Copper is an excellent example. The size of the gap between supply and demand is illustrated by some of the discussion papers at the April 2023 “World Copper Conference”, presented in the Wall Street Journal under the title “Copper Shortage Threatens Green Transition”.

According to a study by McKinsey, copper demand will rise to 36mn tons by 2031. Under extremely optimistic assumptions, production could be expanded from today’s 21.8mn to 30mn tons. Even under the most favorable conditions, however, the deficit would be substantial, at 6.5mn tons. To achieve the net-zero emissions goal, the world would need 54% additional copper by 2030, according to Goldman Sachs. “Green” applications of copper still accounted for only 4% of copper consumption in 2020, but this is expected to rise to 17% by 2030.

According to Guy Wolf, the price of copper would have to nearly double to USD 15,000 to provide an incentive to develop new copper deposits. This shows that the budgeted funds for the energy turnaround are clearly set too low. Moreover, in our opinion, the situation with copper is not an exception but the rule. In some cases even more extreme supply deficits are to be expected, for instance for lithium, but also for nickel and silver.

The calculations of the “World Energy Transitions Outlook 2023” by the International Renewable Energy Agency (IRENA) also show that political will is likely to fail in the face of reality. According to this study, the cumulative investment volume required to achieve the 1.5°C target by 2050 amounts to USD 150 tr. Even if we consider these amounts to be exaggerated and unaffordable, it confirms a statement made by our friend Marko Papic. He speaks in this context of an “absolute orgy of industrial metal capex”. We thus expect a – state-financed – capex renaissance to force the energy turnaround.

A recently published study by Cornell University shows that not only does the world have a structural shortage of the raw materials needed for the energy transition, but also that many significant deposits are located in geopolitically unstable countries such as Chile, South Africa, Russia, the Congo, or China, which represents a further risk factor with the potential to increase prices. The West’s attempt to become more independent of countries that do not share its values through the energy transition is therefore unlikely to be crowned with success.

In addition, the processing and refining of green metals is also far more concentrated in China. This means that the geopolitical risks for the supply of industrial metals may be even greater than for the supply of fossil fuels. The West would therefore still need to invest in processing outside China if the current geopolitical rivalry between Washington – and the West more broadly – and Beijing continues. For all the justified fears of a less peaceful future, rivalry between states and blocs has historically often led to leaps in technological innovation. Thus, one result of the current polarization could be technological breakthroughs that make raw materials cheaper in the long term and open up more resource-efficient growth opportunities.

Best of In Gold We Trust Report 2023

Other key findings from this year’s In Gold We Trust report, “Showdown,” include the following:

- Inflation: Central bankers fear a repeat of history as happened under Arthur Burns in the 1970s. Our baseline scenario points to structurally higher inflation with higher volatility in inflation rates. The chapter includes extensive analysis that looks in depth at fundamentals as well as historical and potential future waves of inflation.

- Debt: Behind the veil of sustainability discourse lies an underestimated danger: growing government debt. In this chapter, we uncover the alarming implications of the Covid-19 pandemic, analyze the underestimated implications of low interest rates, and shed light on the underestimated link to sustainable economic development. In particular, we question the solvency situation with regard to the zero interest rate trap we have highlighted many times in recent years.

- De-dollarization: Already last year, we emphatically pointed out that the freezing of Russian currency reserves in 2022 will probably go down in international monetary history as a historic moment. Europe has clearly sided with the US on this. Meanwhile, Saudi Arabia is flirting intensively with the BRICS countries, which are seeking a multipolar currency system with increasing intensity. The question remains: How will the US respond to these challenges and how will the US dollar fare in this evolving geopolitical context?

- Gold flows: China, like India, has imported a huge amount of gold since the early 2000s; and in China’s case this has been despite China also being the world’s largest gold mining producer. Together, India and China have officially imported somewhere in the region of 34,000–36,000 tonnes of gold over the last 20 years. And if Jan Nieuwenhuijs’ thesis is correct, China’s official gold reserves could be up to twice as high as reported. Together, China and India have gone from representing a combined 28.7% of consumer gold demand in 2000, to now driving nearly half (48.4%) of global consumer demand in 2022, with a combined 1,600 tonnes of demand last year.

- Bitcoin vs. Gold: Bitcoin has been the catalyst for a new wave of interest in sound money, giving the movement a new generation of motivated advocates of a denationalized monetary system. Nevertheless, there is often harsh intellectual trench warfare between the goldbugs and the bitcoiners. In the chapter, we elaborate on how the respective views differ and which theoretical concepts, if any, are misunderstood by both sides.

- Silver: The combination of a shrinking silver supply and strong industrial demand provides a solid foundation for rising silver prices. The energy transition is driving innovation in the solar industry, increasing the use of silver in technologies such as TOPCON and HJT. Price trends show that when gold rises, silver tends to follow, so gold prices will be critical to silver’s fate in 2023. Our analysis shows that silver can benefit from reflationary dynamics that typically occur at the end of a recession.

- Mining stocks: The value proposition of mining stocks continues to improve, while the market still largely ignores their profitability. With a stable gold price in 2023, miners can continue to generate high margins despite rising costs. Producer cash flows are expected to lead to increased M&A activity, benefiting especially junior producers, developers and explorers in stable regions.

- Capex cycle: Although commodity prices have increased significantly in 2021 and 2022, this has not yet led to a significant increase in capital expenditure (capex). The commodity sector has been struggling with various barriers to investment for over a decade. The return of investment is initially expected in the oil and gas sector. Given tight supply and historically low commodity valuations, the expected return of investment will mark the beginning of a new commodity supercycle.

- ESG: As a result of the politically desired implementation of net zero, the environmental component has dominated ESG activities in recent years. To redress the balance, we are focusing our analysis this year mainly on the social aspect of ESG. New Responsible Gold certifications are helping to accelerate sustainability efforts. The ability to turn these challenges into opportunities to strengthen social engagement will be critical to companies’ ESG success.

- Technical analysis: Gold prices have been flirting with a new all-time USD high for a while now. While long-term indicators such as the Coppock indicator remain clearly bullish, shorter-term models such as the Midas Touch Gold Model™ or even the seasonal patterns currently tend to argue for a more cautious outlook.

Quo Vadis, Aurum?

Has the gold price already reached its ceiling? The last great inflationinduced bull market found the media touting the bubble myth of gold. The German weekly magazine Der Spiegel wrote at the peak of the bull market in 1980, “This is no longer a bull market in the usual sense, but hysteria, panic, a frenzy”. Le Monde Diplomatique spoke of “gold fever and the disease of capitalism,” while the Financial Times thought it saw the revival of the “myth” of gold.

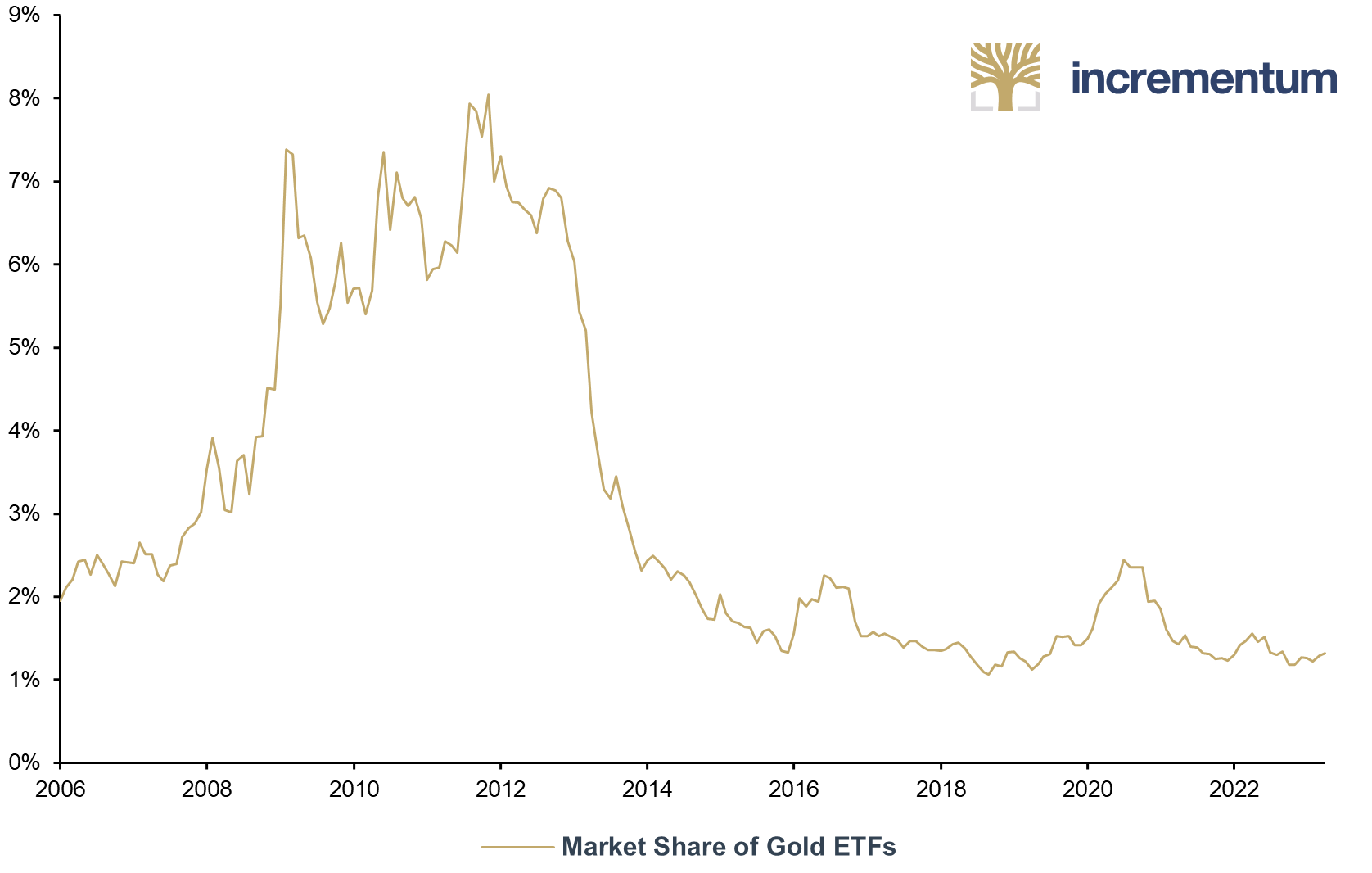

But now back to the present: A comparison of gold demand from institutional as well as private investors shows that gold is still a guest at a discreet private party and is by far not yet dancing at the big summer festivals like Burning Man in the Nevada desert, the Donauinselfest in Vienna, or the Montreal Jazz Festival.

Market Share of Gold ETFs, as % of Total ETF Market Measured by AUM, 01/2006-04/2023

Source: Topdown Charts, Incrementum AG

Based on the situation we have described in detail, we expect an increasing flight into real assets, in particular gold and commodities, especially with the expected uncovering of the central bank bluff. Looking at the next chart, we can see that yields on two-year US bonds exploded from 0.11% in mid-2021 to almost 5% at their peak. Most recently, yields at the short end came under significant pressure again. However, from our point of view the bond market is increasingly confirming that the tightening cycle is nearing its end and that the Federal Reserve will have to cut rates sooner rather than later. Each time yields fell from highs, the gold price began an impulsive bull market phase.

UST 2Y (lhs), and Gold (rhs), 01/1996-05/2023

Source: 13D Research & Strategy, Reuters Eikon, Incrementum AG

Inflation-indexed bonds (TIPS) and gold are currently showing the biggest divergence since 2005. Are we heading for a showdown between real interest-rate expectations priced by TIPS and the gold price? In this context, it is interesting to compare the price movements of the two corresponding assets. Grosso modo, a synchronization is discernible, but at phases the gold price has decoupled significantly from the performance of TIPS. In particular, the phase in the mid-2000s stands out, when the gold price entered a pronounced bull market in an environment of a weak US dollar. TIPS consolidated first on the back of slightly rising nominal yields and unspectacular inflation data. A repeat of this scenario would be possible in the near future, especially if the current US dollar weakness gains momentum.

GLD (lhs), in USD, and TIP (rhs), in USD, 01/2005–05/2023

Source: Reuters Eikon, Incrementum AG

As already emphasized, we see gold as a structural beneficiary of the geopolitical showdown. On the central bank side, gold demand is currently driven by emerging markets. From a game-theoretical perspective, however, it is quite likely that Western central banks will also experience a renaissance in gold demand in the coming years. After all, gold reserves are a guarantee of having a strong hand in the geopolitical showdown.

An extremely interesting indicator in this context is the degree of coverage of the money supply by the gold reserves held by central banks. It shows what percentage of legal tender and commercial banks’ deposits with the central bank are covered by central bank gold reserves.

Required gold price to cover monetary aggregates, in USD, 2023

Source: Brent Johnson, Santiago Capital, Bloomberg, World Gold Council, tradingeconomics.com, Incrementum AG

Rip Current – after the wave break comes the current

The next few months will show us whether the US economy can withstand the recessionary current. We are putting in our bid against it, because the breaking of the biggest inflation wave of the last four decades is now manifesting itself in an ever stronger current that can hardly be withstood.

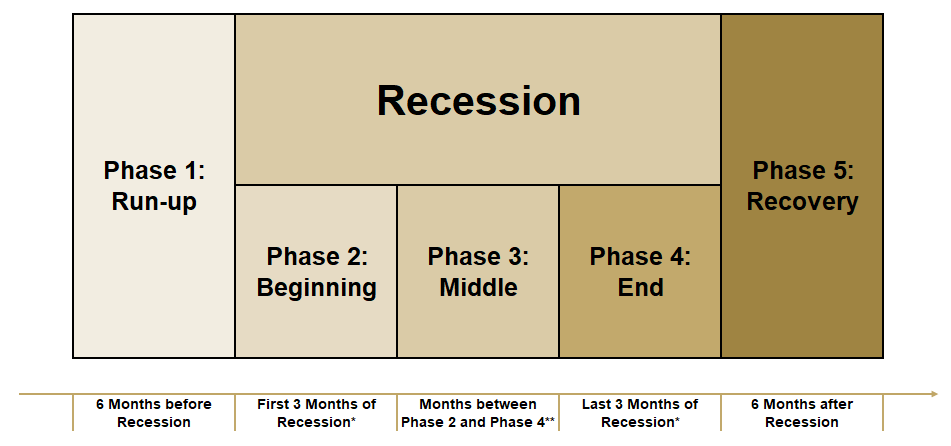

After focusing primarily on stagflation in the In Gold We Trust report 2022, we have turned our focus this year to how investors can best navigate recessionary flows. In this context, we developed the Incrementum Recession Phase Model (IRPM), which is presented in detail in the chapter “The Showdown in Monetary Policy”. This model aims to analyze asset performances during the different phases of a recession and offers insightful insights into which assets can be used profitably and at what times during a recession to mitigate risk. The model is divided into the following 5 recession phases: a pre-recession phase (phase 1), the actual recession broken down into three phases, and the recovery (phase 5).

Incrementum Recession Phase Model

Source: Incrementum AG

*For short recession periods less than 3 months

** For recession periods with 6 or less months no Phase 3 is identified

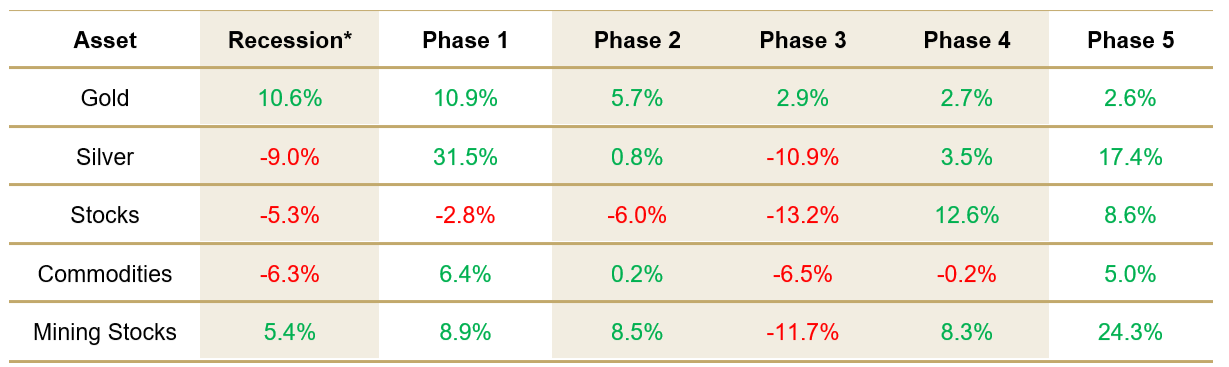

The evaluation for gold, silver, equities, commodities, and mining stocks shows that, overall, gold is best suited as a recession hedge, with an average performance of 10.6% throughout the recession. However, there are significant differences in gold’s performance during the different recession phases. While in phase 1 and phase 2 gold’s performance is still very positive at 10.9% and 5.7%, respectively, especially compared to the performance of the other assets, it is much weaker in the later phases (3-5) at only 2.9%, 2.7% and 2.6%.

Average Asset Performance – Incrementum Recession Phase Model

Source: Reuters Eikon, Incrementum AG

Silver is not a reliable recession hedge, with an average performance of -9.0% throughout the recession. This is probably because silver is perceived much more as a cyclically sensitive industrial metal than as a monetary metal in the midst of the downturn. In the months before and after the recession (phases 1 and 5), however, silver performs above average in comparison.

On average, equities and commodities have a negative performance during a recession, with equities performing best in phase 5, with 12.6%, and commodities in phase 1, with 6.4%. However, mining stocks show that not all stocks post losses during a recession. Except for phase 3, mining stocks show a positive performance on average. It is remarkable that all assets except for commodities can gain in phases 4 and 5. Once again, mining stocks stand out, with an average performance in phase 4 of 8.3% and 24.3% in phase 5.

Overall, our analysis shows that there are significant differences in the performance of different assets during a recession and that investors need to proceed cautiously and strategically to be successful in each phase of the recession cycle.

The Gold Price Forecast in Times of Recessionary Flow

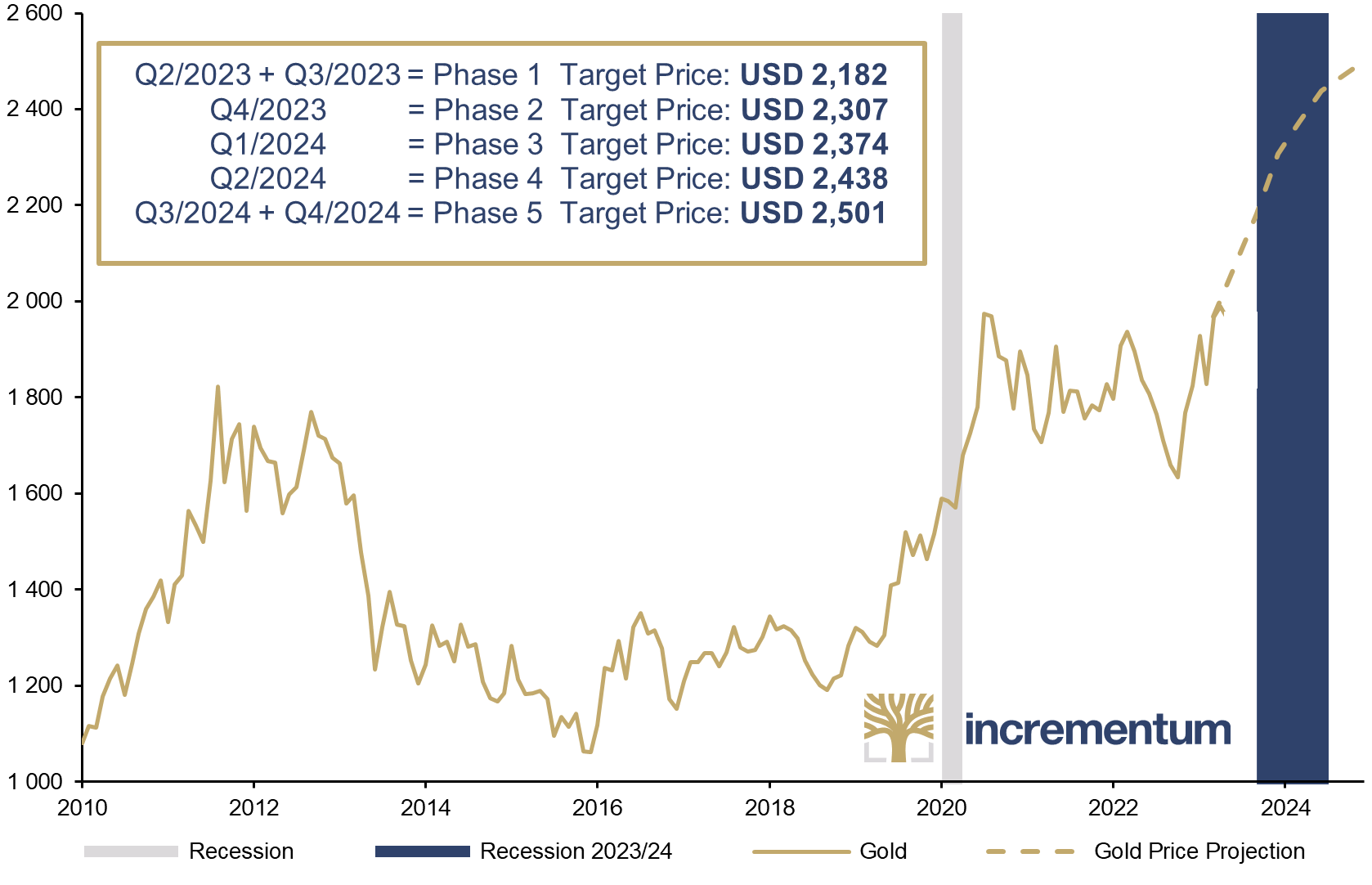

As every year, we want to conclude with the short-term development of the gold price. This year, due to the high probability of a recession, we draw on the economic trend for our gold price forecast. We think that recessionary tendencies, which are becoming more and more pronounced, as we detailed in the chapter “The Showdown in Monetary Policy”, will be the main driver for gold in the near future. Our Incrementum Recession Phase Model is ideally suited to anticipate gold price developments in this environment.

As with any forecast, numerous assumptions have to be made. Our gold price forecast was calculated based on the average gold performance in each phase, assuming the onset of a recession in the US as of Q4/2023, implying that we have already been in phase 1 of our proprietary recession phase model since the beginning of Q2/2023. The forecast extends to year-end 2024, the point at which all recession phases will have been completed under the assumptions we have made.

As a short-term price target, we have set the closing price of gold in US dollars at the end of the current year, which also marks the end of the second phase (initial phase of the recession itself). According to our projection, the gold price would be trading at around USD 2,300 at this time.

Gold, and Gold Price Projection Based on the Incrementum Recession Phase Model*, in USD, 01/2000-12/2024e

Source: Reuters Eikon, Incrementum AG

*based on the assumption of a recession start in the USA in Q4/2023

If the forecast is allowed to continue until the end of the last phase of the Incrementum Recession Phase Model, the final result is a gold price of just under USD 2,500 at the end of 2024.

However, it is important to emphasize that the fulfillment of the recession prerequisite is crucial to achieve this price development. In the absence of a recession, there is a possibility of significant deviation from the projected price.

Update on gold price forecast until the end of the decade

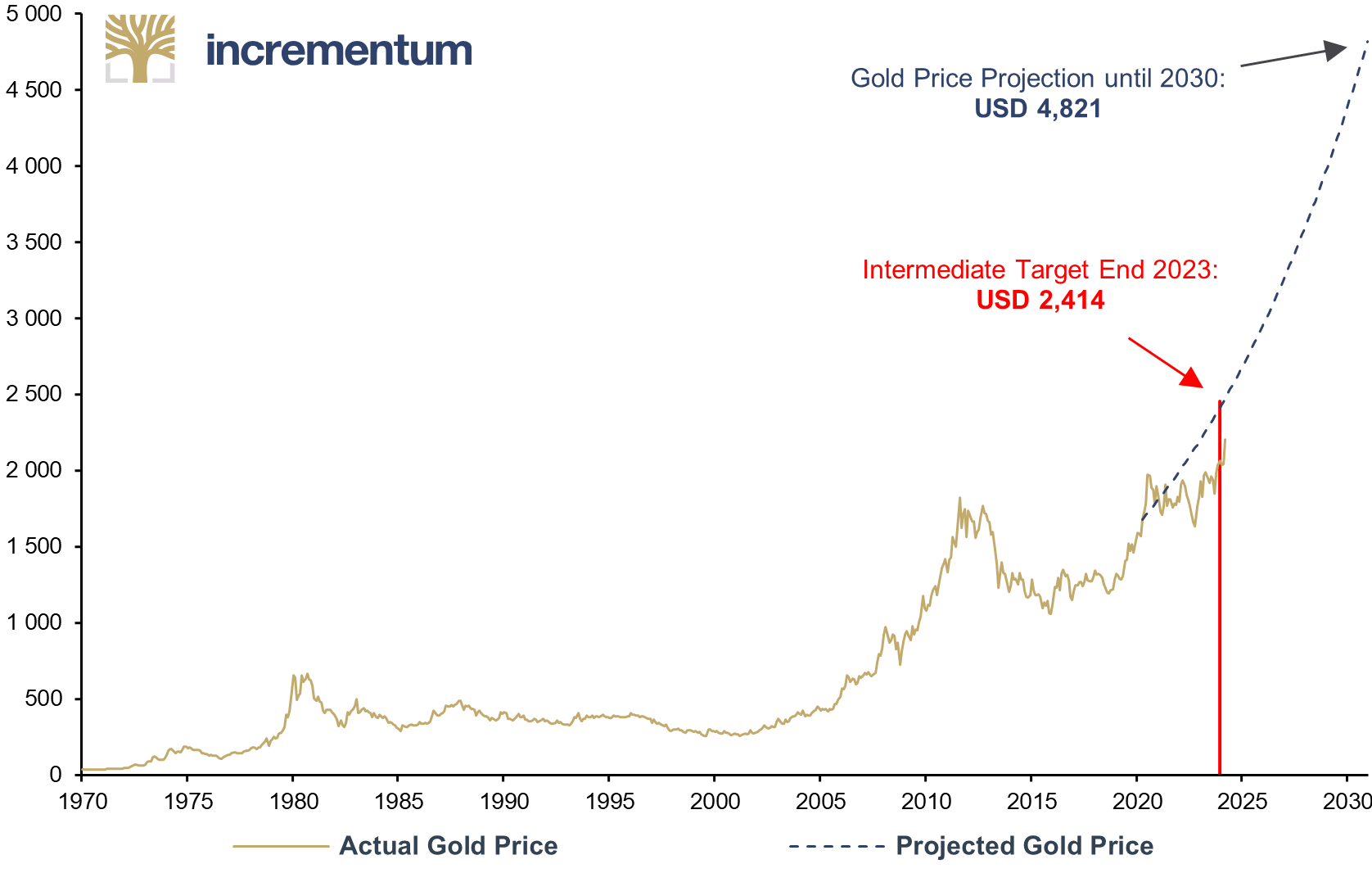

Loyal readers will also remember the gold price forecast model we published in our In Gold We Trust report 2020,[4] with a price target at the end of the decade. At that time we calculated – with the gold coverage ratio as the central input factor – a price target of just under USD 4,800 by the end of 2030.

As last year, we do not want to deprive you of the interim status of our long-term forecast. In order to remain exactly on track, the gold price would have to rise to just above USD 2,400 by the end of this year. That is just under 4.6% or around USD 100 higher than the price target of our recession phase model of USD 2,307. Based on the April 2023 closing price of USD 1,990, this would correspond to a 21.3% increase in the gold price by the end of 2023.

Intermediate Status of the Gold Price Projection until 2030: Gold, and Projected Gold Price, in USD, 01/1970-12/2030

Source: Reuters Eikon, Incrementum AG

We acknowledge the ambitious nature of the projected price increase until the year’s end. Such a rapid price increase within a period of 8 months requires an exceptionally bullish environment for gold in the short term, which we do not consider as the base scenario but also do not want to dismiss. Nevertheless, we firmly believe it is realistic for gold to at least reach new all-time highs in USD this year.

We continue to adhere to our decade price target of approximately USD 4,800, as monetary policy dynamics, the economic outlook and, in particular, the geopolitical situation should provide considerable support for the gold price in the medium to long term. After all, should uncertainty increase further in the coming months and a recession be priced in by the market in the course of the year, gold will play out its full potential.

There are undoubtedly challenging times ahead for investors in the coming years as we find ourselves in the midst of monetary and geopolitical showdowns. Just as in a strategic move in a high-stakes poker game, gold not only plays the role of a reliable bet during uncertain times but also acts as ace in the hole, protecting the purchasing power of individuals and providing a steadfast defense against the wild swings of the financial markets. For us, gold is the expression of a strong hand for investors.

Even if it is not always easy, we would like to look to the future with optimism. The disappointments ahead will probably not be painless, but they could ultimately set in motion exciting economic and social dynamics. In these exciting times, we assert, as ever:

IN GOLD WE TRUST

[1] “Stagflation 2.0,” In Gold We Trust report 2022, p. 372

[2] See “Past, Present, and Future of the Monetary Order,” In Gold We Trust report 2015

[3] See chapter “Capex Come Back: A Raging Bull Market for Commodities Beckons” in this In Gold We Trust report.

[4] “Quo vadis, aurum?,” In Gold We Trust report 2020