Quo Vadis, Aurum?

“Our New World Disorder will be characterized by greater volatility, higher inflation and deeper financial repression.”

Alexander Chartres

Key Takeaways

- Monetary policy has its back to the wall. It is forced to at least pretend to stand up to wolfish inflation without causing a recessionary bear.

- The Federal Reserve is acting late but (for now) decisively. Internationally, this is increasingly putting central banks under pressure to follow suit.

- The balancing act of fighting inflation without triggering distortions on the markets is doomed to failure. The vehemence of the tightening cycle that has begun threatens to end the Everything Bubble in an Everything Crash.

- The current wave of inflation could peak this year in the wake of rising asset price deflation. However, a reversal of monetary policy could already usher in the next wave of inflation.

- The price of gold has also been affected by the Federal Reserve’s tightening. Even though gold is doing well relative to all other asset classes this year, further headwinds are to be expected for gold in the short term.

- We are sticking to our long-term price target of USD 4,800 by 2030. For the gold price to remain on track until the end of the year, it would have to rise to around USD 2,200. Provided that monetary policy departs from the announced hawkish path, we consider this to be realistic.

Everything Bubble, Stagflation, Everything Crash…

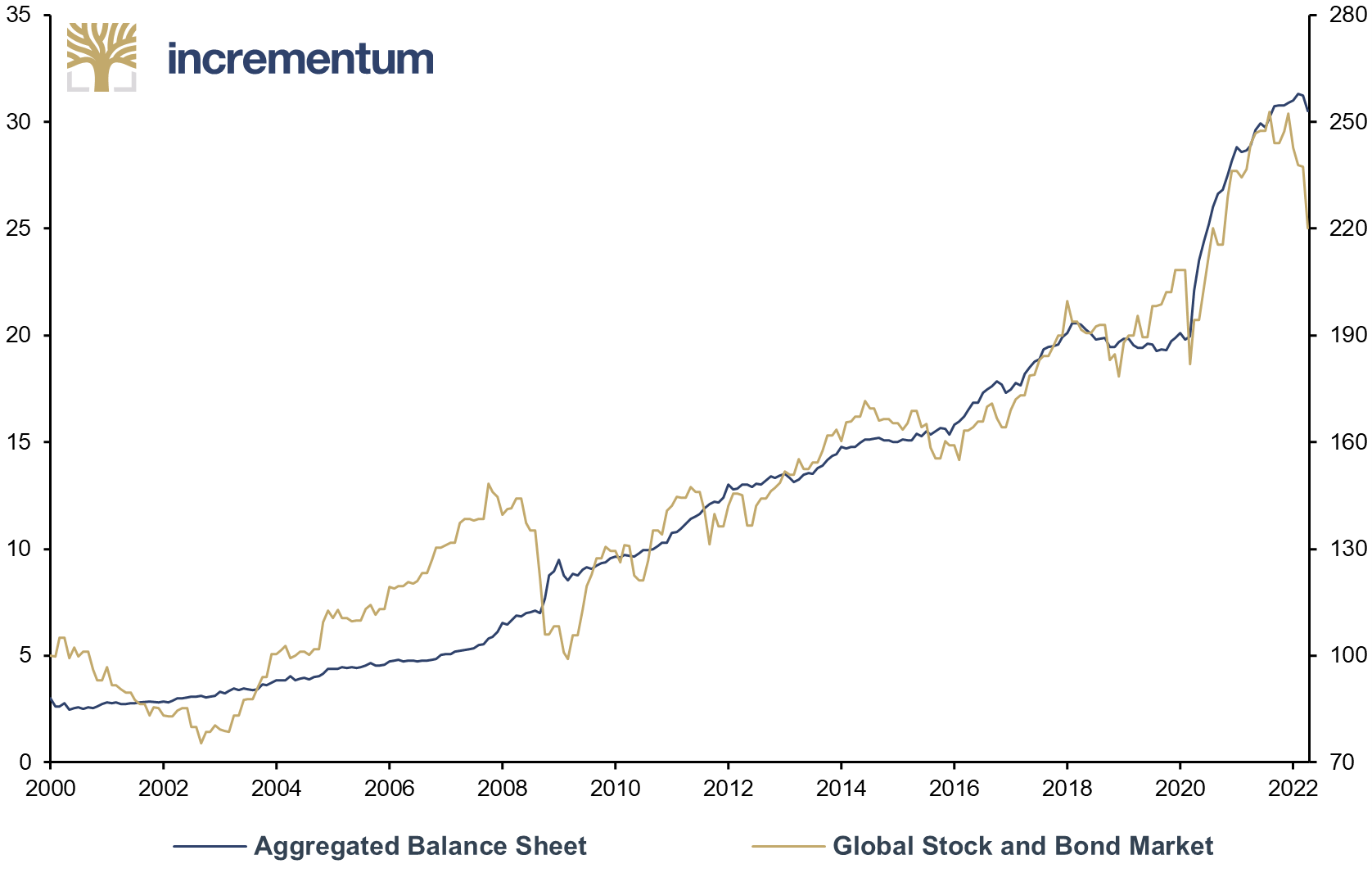

For years, the news has been dominated by reports of global crises. One disaster seems to follow the next: financial crisis, euro crisis, climate crisis, pandemic, and now, since February, a war in the middle of Europe. The seemingly chaotic and fragile times in which we live are causing increasing uncertainty and disenchantment with the news among large sections of the population. Remarkably, however, this uncertainty has so far manifested itself on the capital markets only in the short term. If you look at the long-term development of global stock and bond markets, you might think that all these crises had never happened.

Aggregated Balance Sheet of Fed, ECB, BoJ, and PBoC (lhs), in USD trn, and Global Stock and Bond Market Price Development* (rhs), 01/2000-04/2022

Source: Reuters Eikon, Incrementum AG

*consisting of 60% MSCI ACWI and 40% FTSE Global Gov. Bond Index

A major reason for the spectacular returns for stock investors, but also for real estate and bond investors, especially in the past 25 years, is that every crisis was answered with ever more extreme monetary policy measures in line with the prevailing interventionist zeitgeist. Market participants have been conditioned like Pavlovian dogs to the Fed put. The true costs of this policy of monetary largesse remained hidden for a long time.

The prerequisite for maintaining this deception was, first and foremost, the strong, structurally disinflationary forces. The flood of liquidity created out of nothing initially spilled into the capital markets and increasingly inflated asset prices. This everything bubble gave the impression that growth could continue unabated, that deficits and monetary expansion were not a problem, and that even global lockdowns and production stoppages could harm the economy only in the short term. However, the interventions in response to the Covid-19 crisis ushered in a change. What we call monetary climate change was the beginning of a paradigm shift toward an inflationary environment. The war in Ukraine and the accompanying sanctions and export restrictions are just another accelerant.

Now we are at the beginning of a major disappointment. While at least a small part of the population was able to enjoy rising asset values in times of disinflation, consumers as well as investors are finding life increasingly difficult in a time of increased inflation rates.

The omnipresent inflation means a noticeable reduction in the standard of living of the majority of people. When the real pie becomes smaller – whether in the form of higher prices, smaller package sizes, or thinner soups – this has far-reaching consequences for consumer behavior and investment activity. Distributional issues will be fought even harder socially, contributing to national and international tensions and further exacerbating the polarization that already exists. The return of the wolf and all the calamities associated with it are increasing the pressure on monetary guardians to actually guard the purchasing power of the currency.

Monetary policymakers therefore have their backs to the wall. They are forced to at least pretend to face the wolf. However, tentative attempts to stem the tide of liquidity are beginning to expose problems that have been masked for years, if not decades, by emergency measures. Just as in 2018, when we warned of the inevitable consequences of the attempted turning of the monetary tides, we are now issuing another explicit warning. In addition to wolfish inflation, a bearish recession now looms.

The Doomed Balancing Act

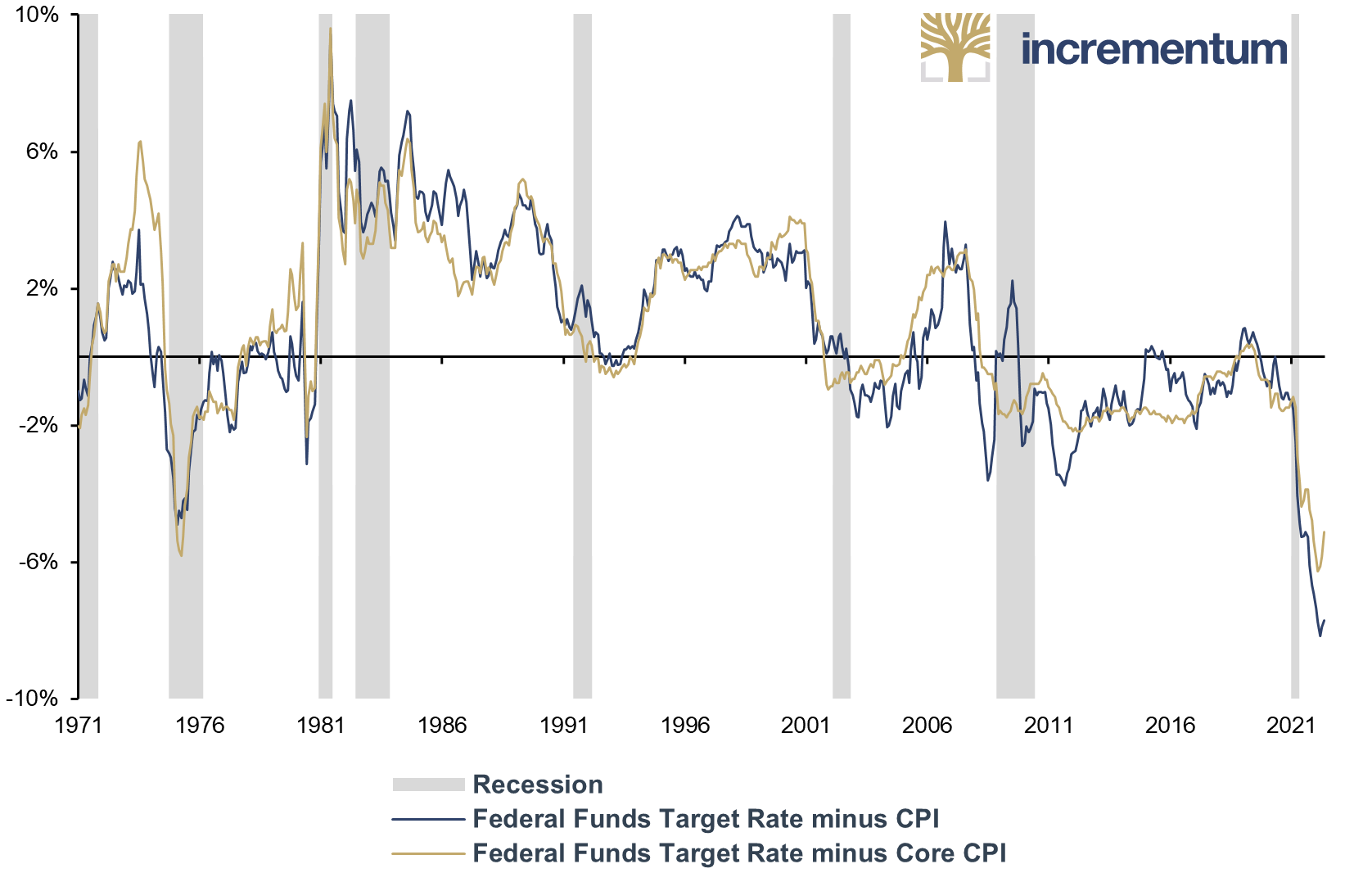

In view of the decade highs in various inflation indicators – consumer prices, core inflation, producer prices, import prices – many a monetary policy dove has mutated into a hawk in recent months. In the US, there is currently the impression that the Federal Reserve cannot raise interest rates fast enough. This is hardly surprising in view of an inflation rate of 8.3%.

The real key interest rate has never been as low as it currently is. The first interest rate hikes have done nothing to change this. If the calculation of the real interest rate is based on the core inflation rate, the real key interest rate is at its lowest level since 1971.

Fed Funds Target Rate minus CPI, and Fed Funds Target Rate minus Core CPI, 01/1971-04/2022

Source: Reuters Eikon, Incrementum AG

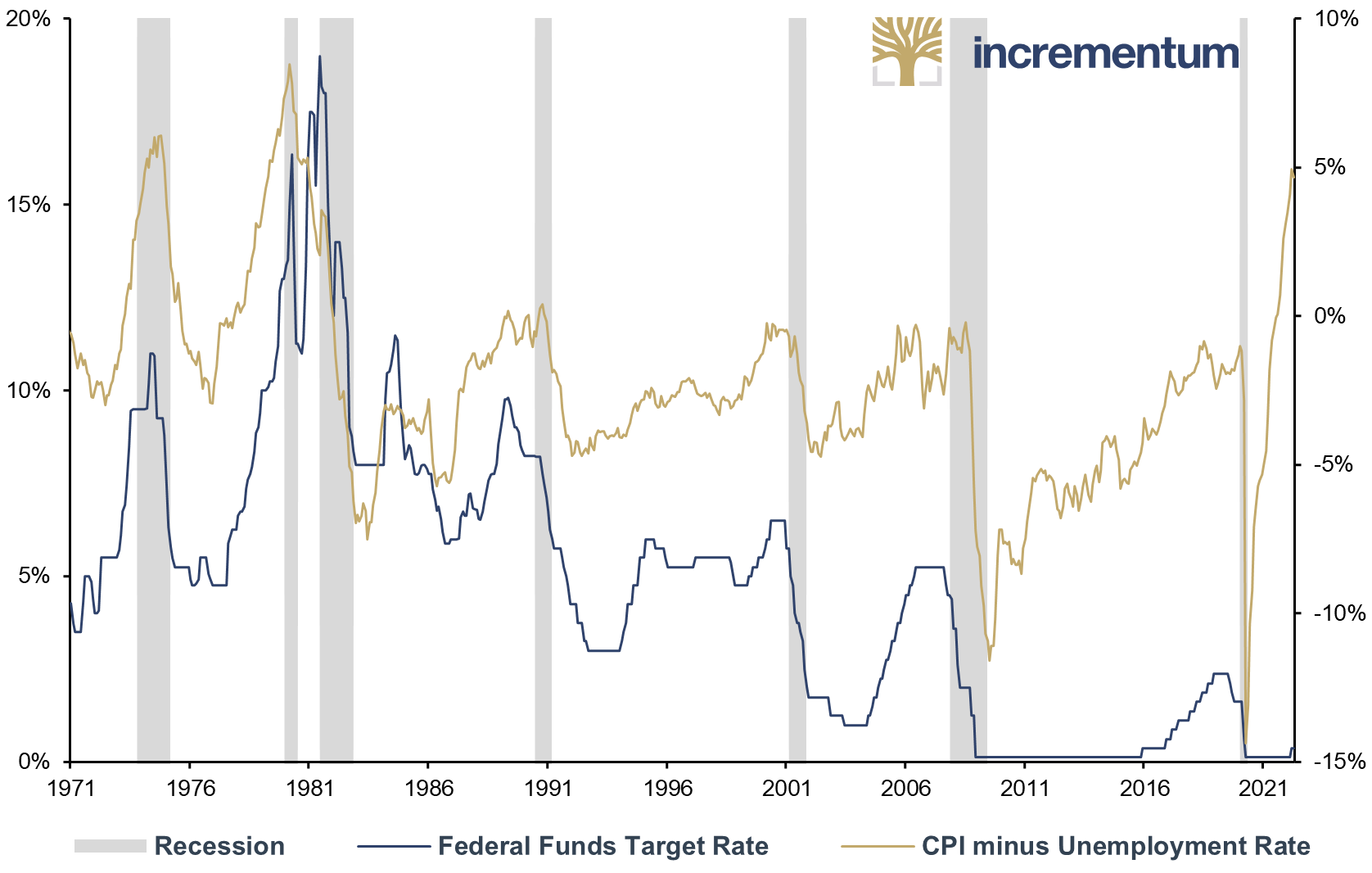

According to official unemployment and inflation statistics, the Federal Reserve, which pursues a dual mandate regarding employment and price stability, should have acted long ago. The spread between the CPI and the unemployment rate in the US is currently higher than it has been for four decades. Back then, however, the key interest rate was 15 percentage points (!) higher than today.

Federal Funds Target Rate (lhs), and CPI minus Unemployment Rate (rhs), 01/1971-04/2022

Source: Reuters Eikon, Incrementum AG

Remarkably, even Jerome Powell has recently admitted that the Federal Reserve is now too late: “If you had perfect hindsight you’d go back and it probably would have been better for us to have raised rates a little sooner.” Therefore, to preserve what was left of its credibility, the Federal Reserve had no choice but to announce aggressive interest rate moves and start implementing them. The pace and vehemence of the expected tightening cycle that has already begun – a Fed Funds Rate of nearly 3.50% by the summer of 2023 and an annualized QT pace of USD 1.14trn – would be the most aggressive monetary tightening since Paul Volcker.

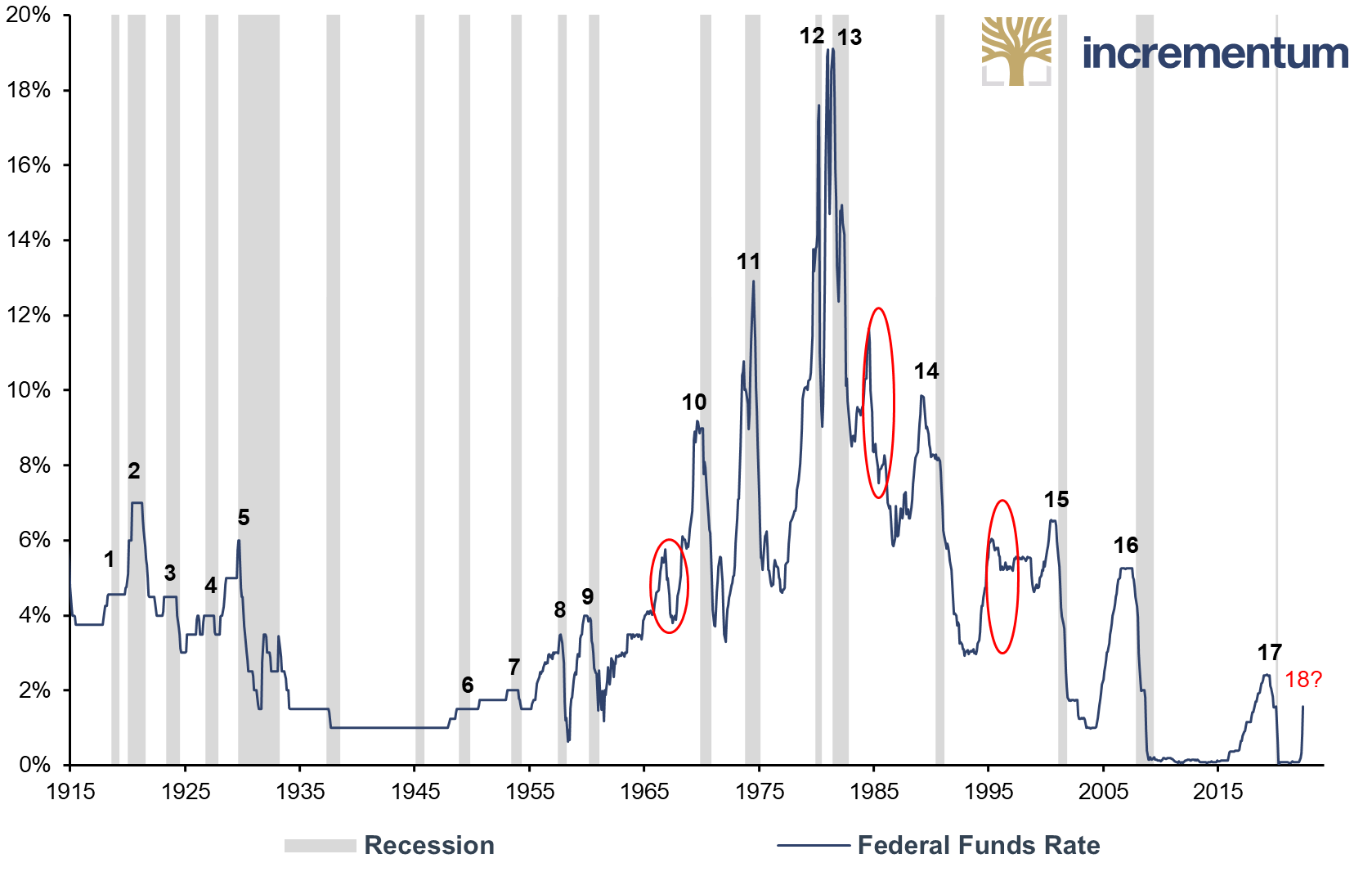

In addition to curbing inflation, the declared further goal is to manage the turnaround in monetary policy without triggering a recession. However, in our view, this balancing act of a soft landing is doomed to failure from the outset. A look at history and the latest In Gold We Trust reports[1] confirms our doubts .

As a reminder, since the early 1980s, every interest rate hike cycle has ended below the peak of the previous cycle. This would mean that, according to the old pattern, rate hikes would stall at the very latest at an interest rate spread of 2.25–2.50%. Thus, in Q4/2018 the Federal Reserve was forced by markets to make a monetary policy U-turn towards a looser policy.

The S&P 500 gave up more than 20% in the meantime; and already by January 2019 Powell abandoned the “autopilot” mode, which he had only announced at the beginning of December 2018, to the financial markets’ consternation.

But this time everything is supposed to be different – at least that is what the Federal Reserve and large parts of the economists’ guild want us to believe. However, the following chart tells a different tale, as only 3 out of 20 interest rate hike cycles did not end in a recession.

Federal Funds Rate, 01/1915-05/2022

Source: Reuters Eikon, Incrementum AG

Quantitative tightening: very, very frightening

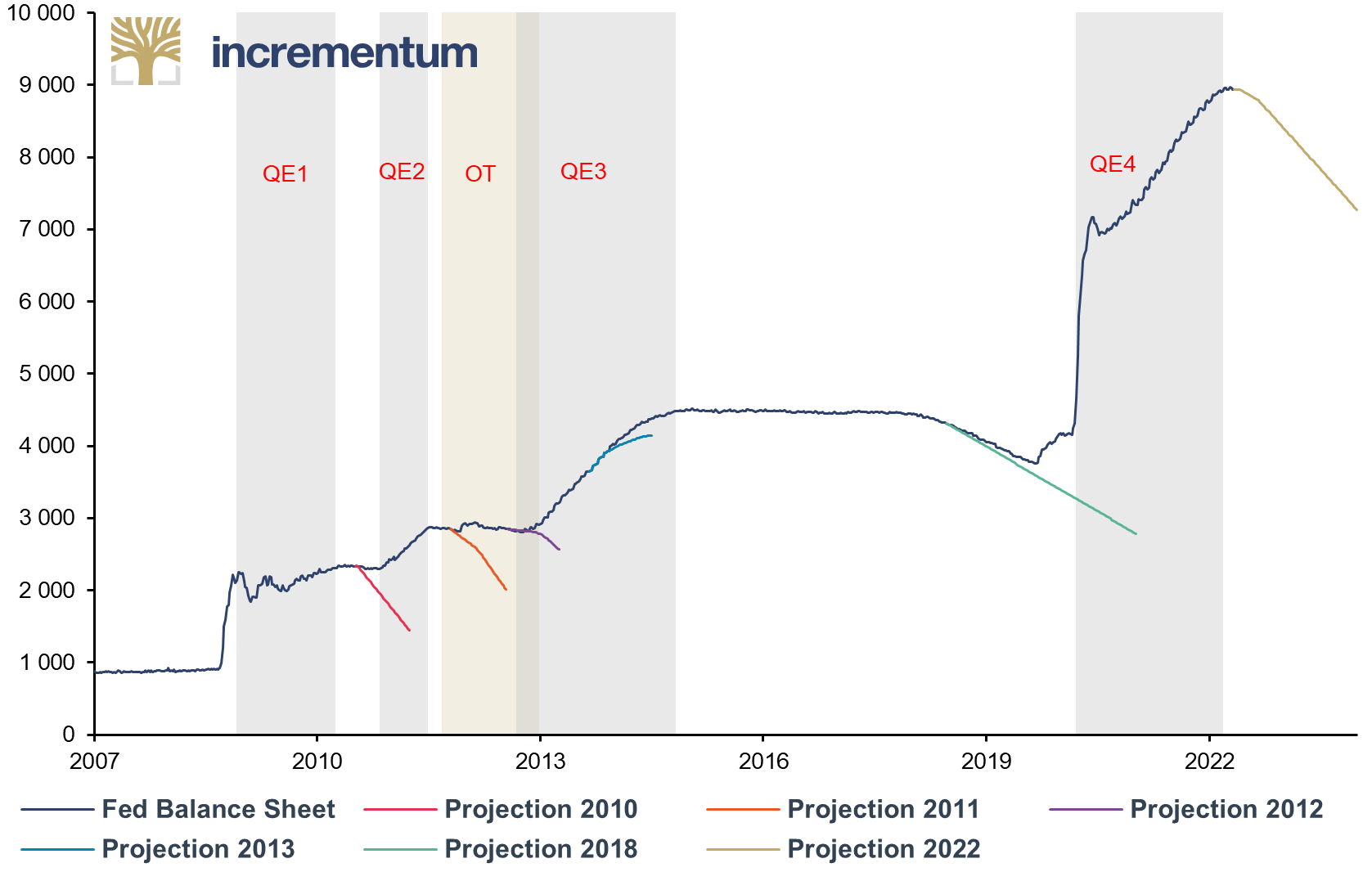

The tightening of US monetary policy does not only consist of aggressive interest rate hikes. At the same time, quantiative tightening (QT), i.e. a reduction of the Federal Reserve’s balance sheet, is also planned. In our opinion, the QT plans are ambitious, not to say illusory. The Federal Reserve’s balance sheet is to be shortened by USD 522.5bn in 2022 alone and by USD 1,140bn in 2023. That would be a reduction of nearly 6% in the current year and another 13% or so next year. This process is set to continue until the Federal Reserve decides that the balance sheet has “normalized” or until the next crisis forces a turnaround. The latter is definitely more likely to occur.

Let’s take a look at the past. The Federal Reserve’s QE programs to date have had the following effects on capital markets:

- Rising stock markets

- Increasing risk appetite

- Falling yield spreads (corporate bonds, junk)

- Falling interest rates

- Subdued price inflation

- Record low volatility

It seems obvious that QT has exactly the opposite consequences as QE. As a reminder, the last tightening process was gradual and cautious. The Federal Reserve began QT in October 2017, almost two years after the first rate hike. QT volume was increased only slowly, from USD 10bn per month to USD 50bn per month in Q4/2018. The sharp equity market correction in December 2018 forced the Federal Reserve to suspend rate hikes and announce a quick end to QT. Just a few quarters later, the Federal Reserve’s balance sheet grew again.

Fed Balance Sheet Path, in USD bn, 01/2007-01/2024e

Source: Reuters Eikon, Federal Reserve, Incrementum AG

Can the reduction of the central bank balance sheet succeed this time without causing a recession and/or a replay of a financial crisis? Considerable doubt is warranted. In its 109-year history, the Federal Reserve has attempted to reduce its balance sheet exactly seven times (1921-22, 1928-1930, 1937, 1941, 1948-1950, 2000, and 2017-2019).[2] The 2017-2019 episode can be virtually disregarded, because the Federal Reserve had to quickly abandon its tightening policy. Prior to this experience, five of the Federal Reserve’s six historical QT efforts were followed by a recession, with 1941, the year of US entry into World War 2, being the only exception.

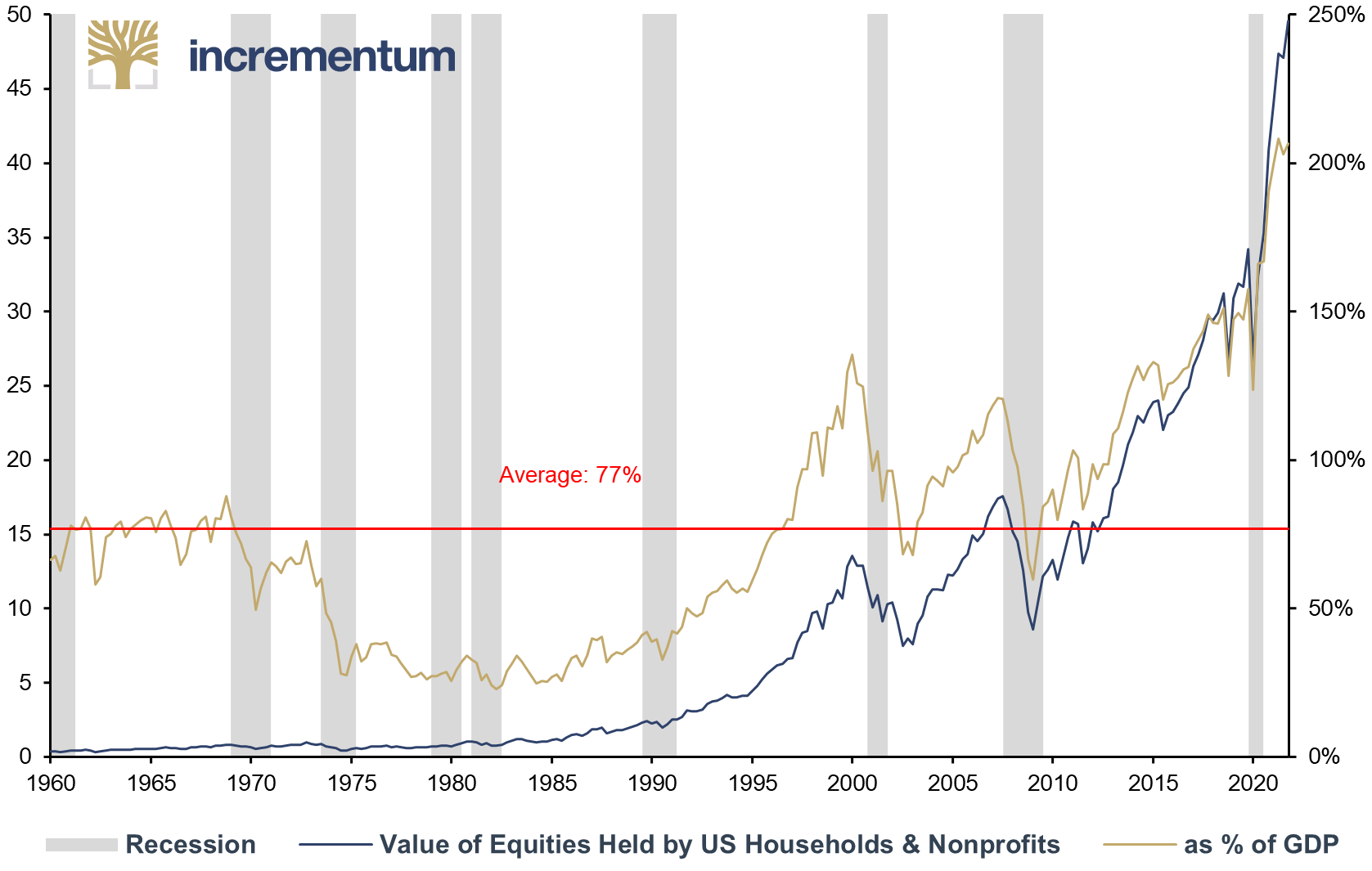

The Federal Reserve runs the risk of overestimating the impact of rate hikes and balance sheet reductions on containing inflation, just as it has underestimated the impact of rate cuts on boosting inflation. This is because the US consumer’s dependence on high and rising asset prices is greater than ever. As of Q4/2021, household equity holdings were at a new all-time high of USD 50trn. This amount is equivalent to twice the annual US economic output, well above the historical average of 77%. A decade ago, households owned only USD 12.8trn worth of stocks or about 80% of GDP. For this reason, a 20% correction today feels like a 60% plunge 10 years ago.

Value of Equities Held by Households and Nonprofits (lhs), in USD trn, and as % of GDP (rhs), Q1/1960-Q4/2021

Source: Federal Reserve St. Louis, Incrementum AG

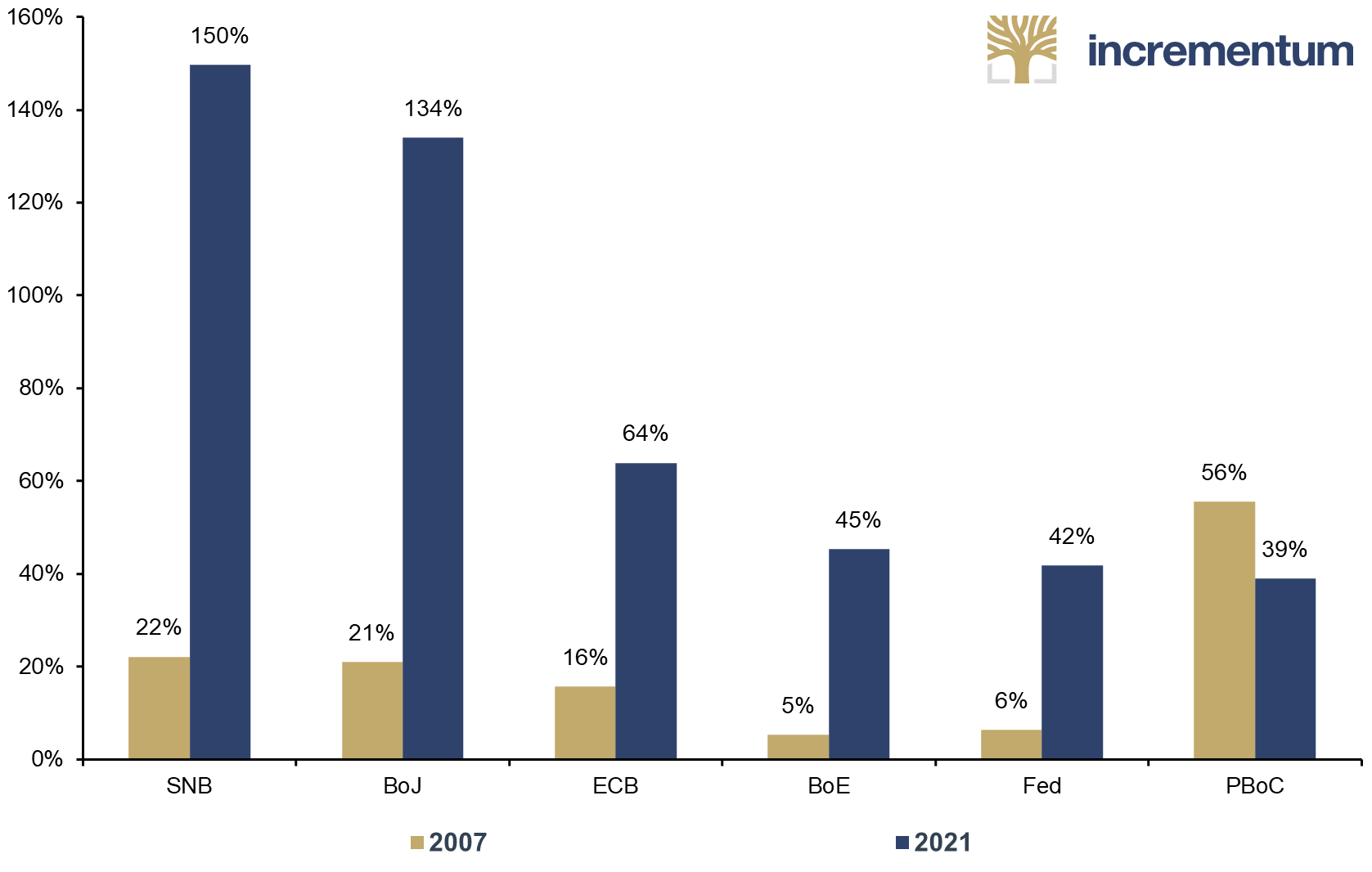

While the Federal Reserve is attempting to pull back on monetary policy, monetary surrealism is being blithely practiced elsewhere. The QE programs of the other major central banks, such as the ECB and the BoJ, are still ongoing, although here, too, there are increasing voices in favor of a cautious exit. The next chart clearly shows that the balance sheets of the BoJ and the SNB are significantly larger relative to GDP than those of their counterparts. It can also be seen that – with the exception of the Chinese central bank – central bank balance sheets have expanded massively in relation to GDP.

Central Bank Balance Sheets, as % of GDP, 2007 and 2021

Source: Central Bank Statistics, World Bank, Incrementum AG

While central bankers in the US, the UK, and other countries have been late in getting the cycle of interest rate hikes underway, ECB President Christine Lagarde and many other representatives of the Governing Council seem to have no idea at all what a monetary policy hawk is. An ornithological-economic tutorial seems in order, because there are now fewer hawks in the ECB than chamois in the Netherlands. With the supposed gentleness of the dove, i.e. the greatest possible monetary policy passivity, the ECB hopes the inflation problem will disappear of its own accord. However, this view is not gentle or naïve, but rather incendiary. In the euro area, for example, producer prices are now rising at a rate of 5.3% per month, which is stronger growth than there used to be for the whole year.

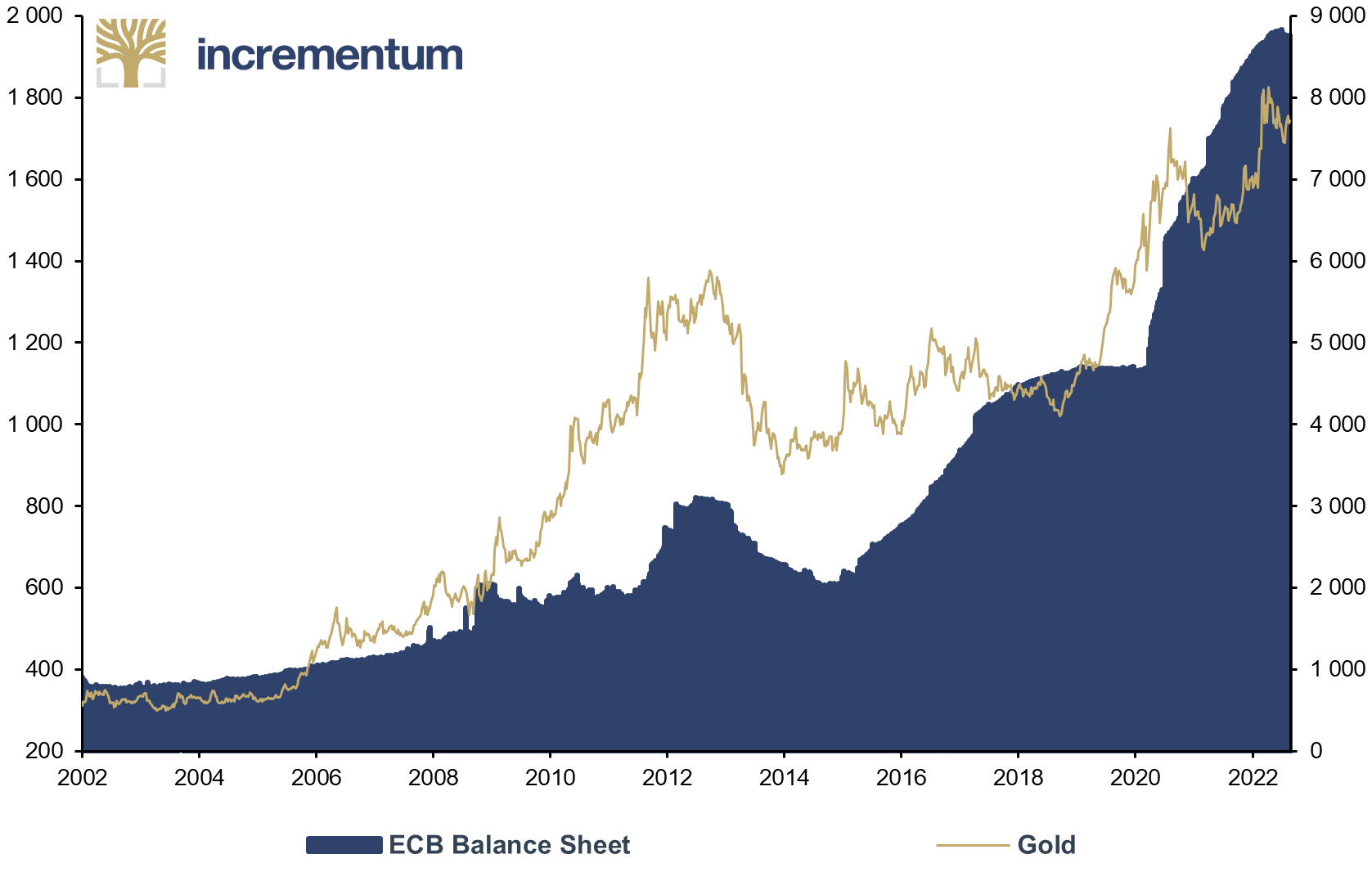

The hope that this wait-and-see approach will prevent another euro crisis will prove to be false. The bitter losses of the euro against the US dollar – which only further increase inflationary pressure in the euro area – and the resulting performance of the gold price on a euro basis show this impressively.

Gold (lhs), in EUR, and ECB Balance Sheet (rhs), in EUR bn, 01/2002-05/2022

Source: Reuters Eikon, Incrementum AG

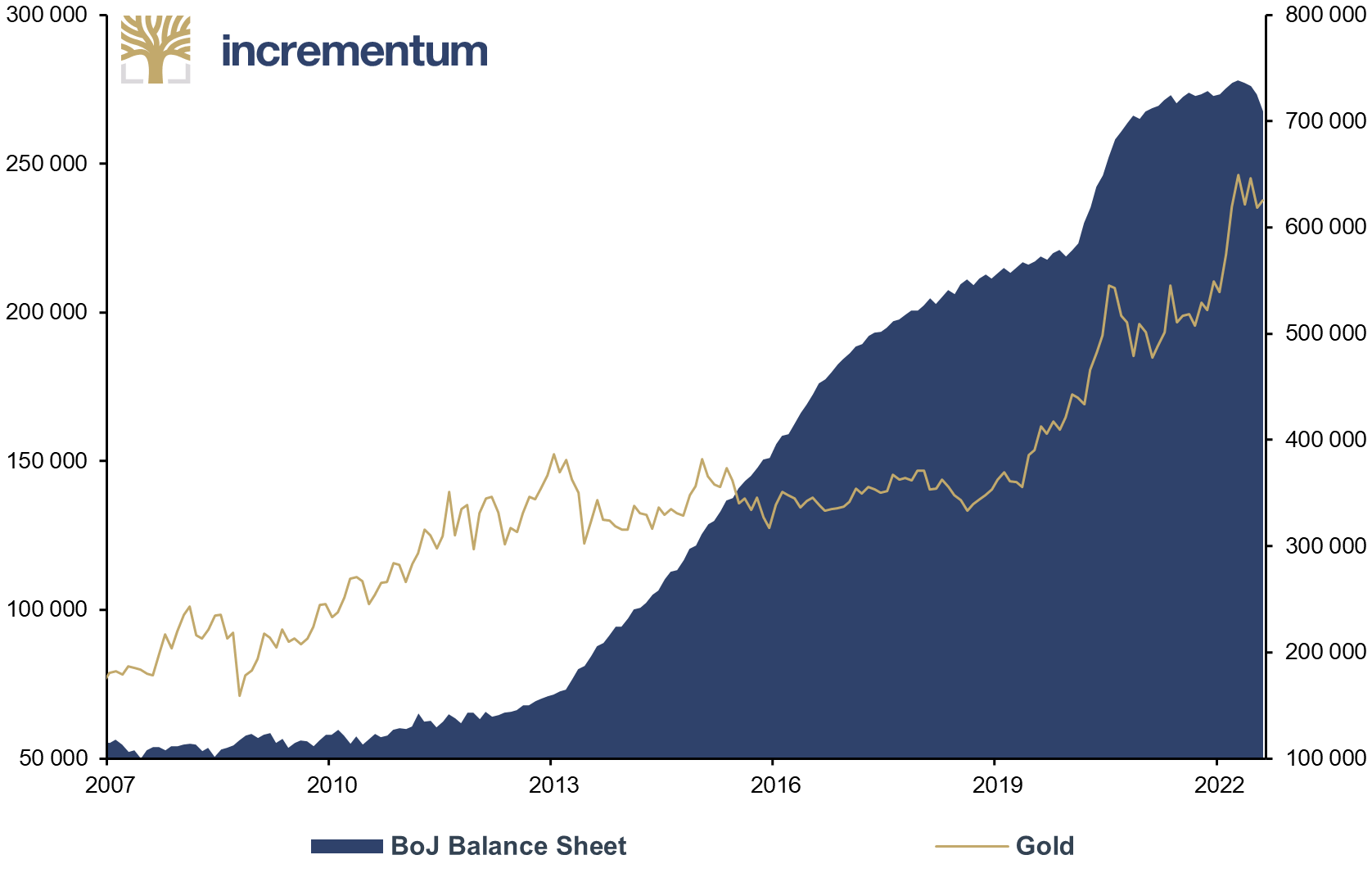

Among the industrialized countries, monetary loosening seems to have progressed furthest in the Land of the Rising Sun. One should therefore pay particular attention to monetary policy developments in Japan, as they could serve as a blueprint for the Western world. The escalating yield curve control in Japan is already having an effect. The gold price recently marked numerous all-time highs in JPY.

Gold (lhs), in JPY, and BoJ Balance Sheet (rhs), in JPY bn, 01/2007-04/2022

Source: Reuters Eikon, Incrementum AG

The central banks thus face an insoluble dilemma, a dilemma they themselves caused by their ultra-lax monetary policy and aggravated for months by their denial of the inflation surge. They are now sitting in that pit they dug for themselves.[3] The big question is: What happens if central banks have to hit the monetary policy pause button and then punch rewind? In our view, this would usher in the next wave of devaluation and inflation and further fragilize the currencies of the Western world. In this case, nothing less than the credibility of central banks would ultimately be at stake. And with it, confidence in fiat money itself.

Stagflation 2.0 – the Nightmare for Balanced Portfolios?

For a long time, the topic of inflation was as important to the capital markets as studying the snow report in the Sahara; so long that many investors forgot or never had to think about how certain asset classes behave in a highly inflationary environment.

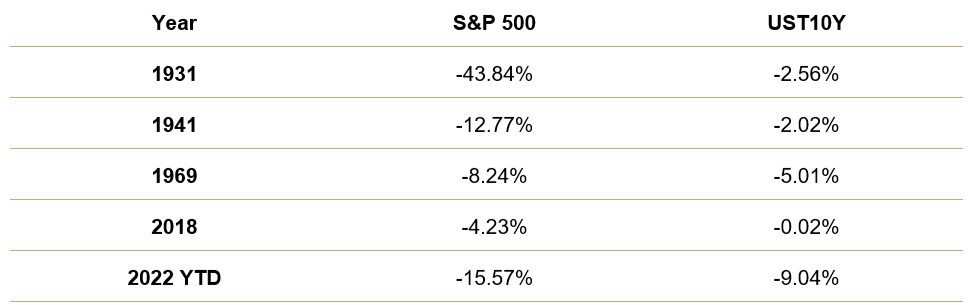

For a large proportion of mixed portfolios, simultaneously falling stocks and bonds are the absolute worst-case scenario. In the last 90 years, there have been only four years in which both US stocks and bonds had negative performance in the same year. Currently, all indications are that 2022 could be the fifth year.

Source: NYU, Reuters Eikon (as of May 13, 2022), Incrementum AG.

But what were actually the reasons for this double whammy back then?[4]

- In 1931, in the midst of the Great Depression, the British pound, then the world’s reserve currency, was devalued and taken off the gold standard. This had an inflationary effect.

- In 1941, the US was attacked by Japan and drawn into World War 2. Shortly thereafter, explicit yield curve control (YCC) was introduced, which was also inflationary.[5]

- 1969 marked the beginning of a highly inflationary era, with the US devaluing the US dollar only 18 months later and Nixon releasing the US – initially temporarily – from the gold redemption obligation. This again had an inflationary effect.

- In 2018, the Federal Reserve was forced to end its interest rate hike program after heavy losses on the stock markets. Seven months later, the next rate-cutting cycle began. In response to the rise in repo rates, the Federal Reserve again began to expand its balance sheet. The effect was again inflationary.

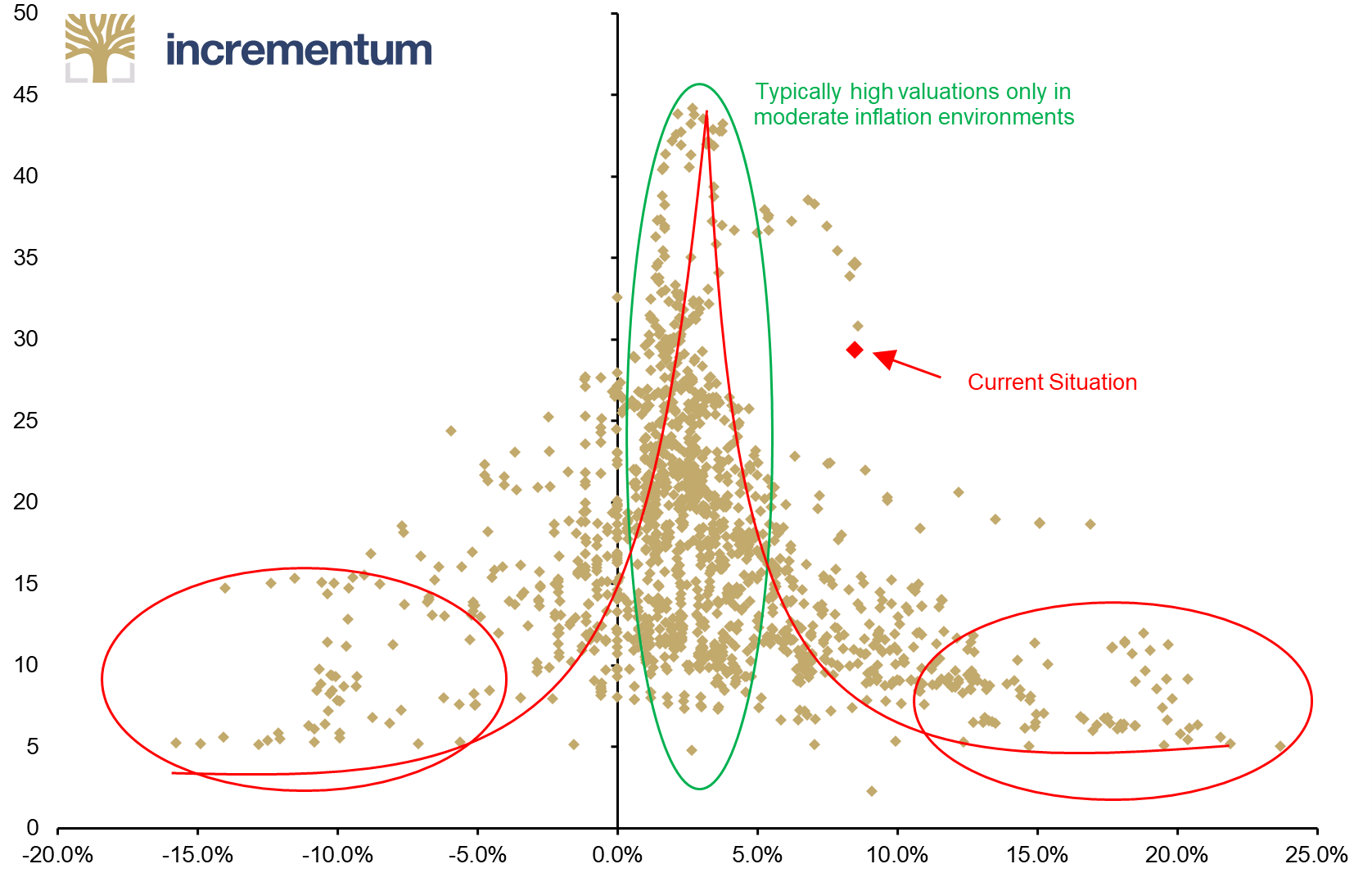

It can be seen that inflation played a central role in all the cases mentioned. But it is not only assets that are devalued by inflation but also the business models of many companies. This is why we have repeatedly pointed out in previous years that selecting the right equity sector or the right company becomes significantly more important when inflation is above the “feelgood zone” of around 4%. The fact that high inflation rates initially represent a headwind for equities is also confirmed by the next chart, which shows the monthly valuations of the S&P 500 based on the Shiller P/E ratio and the associated inflation rate.

CPI Inflation Rate (x-axis), and Shiller P/E Ratio (y-axis), 01/1900-04/2022

Source: Robert J. Shiller, Incrementum AG

It turns out that equities usually perform poorly in strongly deflationary and highly inflationary environments. This is mainly because companies’ sales and margins come under pressure. Because of the current high inflation rates, the S&P 500 is still too highly valued, with a Shiller P/E of just under 34. In order to remain true to the previous empirical pattern, the Shiller P/E ratio would have to be roughly halved if the inflation rate remained constant.

To return to a value within the general statistical pattern, therefore, either prices, the inflation rate, or both would have to fall. We expect inflation in the USA to reach its interim high in the course of this year. Driven by weakening demand, increasingly recessionary tendencies, and fading base effects, inflation will slow down but is expected to remain above 5% yoy this year. In this case, a continuation of the correction on the US equity market would be entirely appropriate from a valuation perspective.

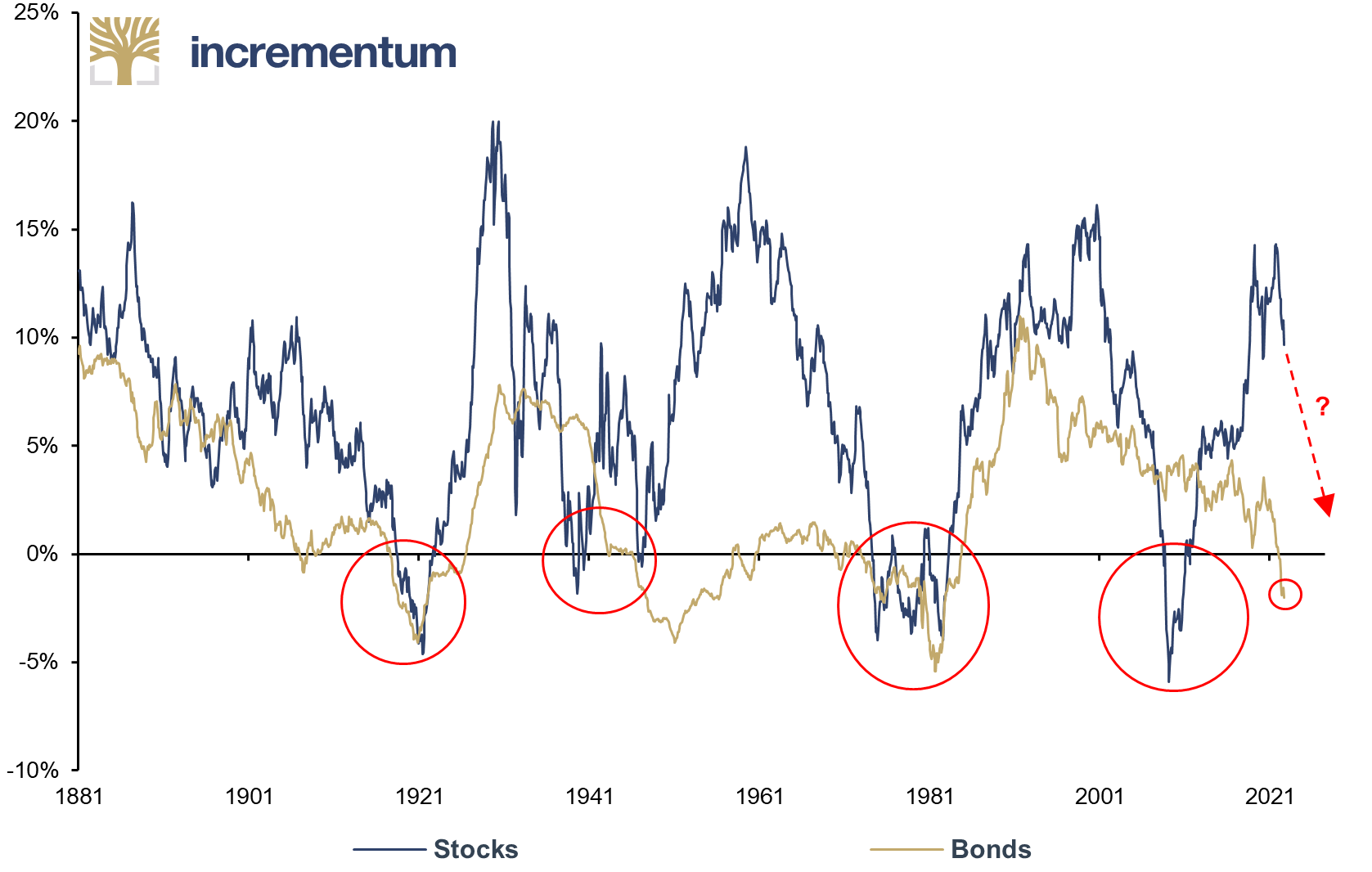

The following chart shows the course of 10-year annualized real returns of stocks (S&P 500 TR) and bonds (10-year US Treasuries) over the past 140 years. It is noteworthy that the returns are mostly symmetrical, suggesting a positive correlation between the two asset classes over the longer term. But while equities are still yielding high returns, the annualized real return on bonds is in negative territory for the first time in almost 40 years.

10-Year Annualized Real Returns of Stocks and Bonds*, 01/1881-04/2022

Source: Robert J. Shiller, Incrementum AG

*Stocks = S&P 500 TR/Bonds = 10-Year US Treasuries

In the past 140 years, stock returns have slipped into negative territory only four times. The triggers were the two world wars, stagflation in the 1970s and the financial crisis of 2007/08. And each time before the long-term return collapsed, the stock market had previously been in a phase of euphoria, characterized by annualized returns of well over 10% in some cases.

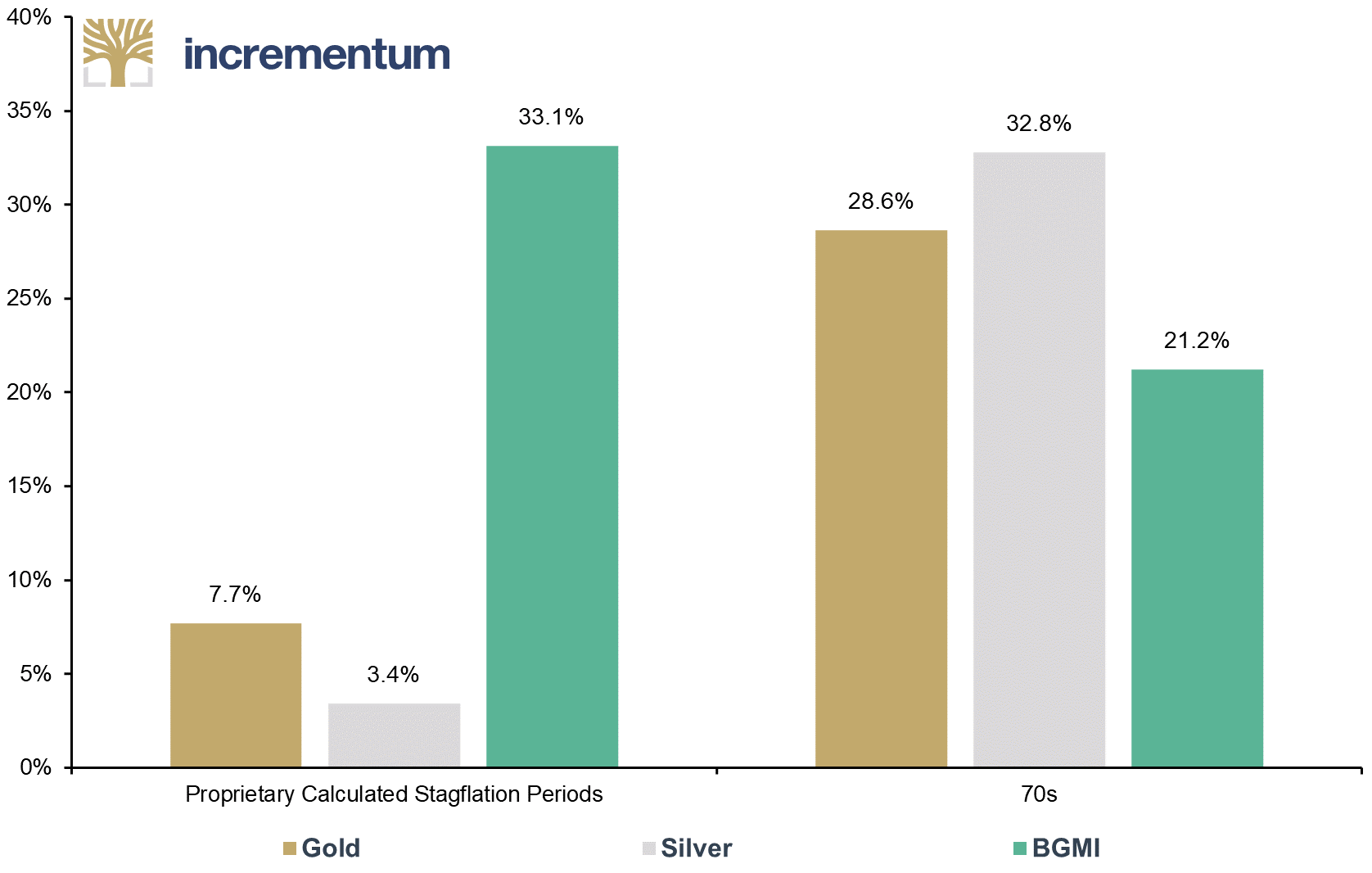

The high of the current cycle dates from September 2021 with a return of 14.3%. Since then, the return has gone slightly downhill. The question now is, what is the alternative or ideal portfolio companion to the broad equity market when bonds, with a high positive correlation to equities, have a negative long-term real return in the stagflationary environment? Our quantitative evaluations show that gold, silver and mining stocks have historically outperformed in stagflationary times.

Average Annualized Real Returns of Gold, Silver, and BGMI During Proprietary Calculated Stagflation Periods and 70s

Source: Reuters Eikon, goldchartsrus.com, Incrementum AG

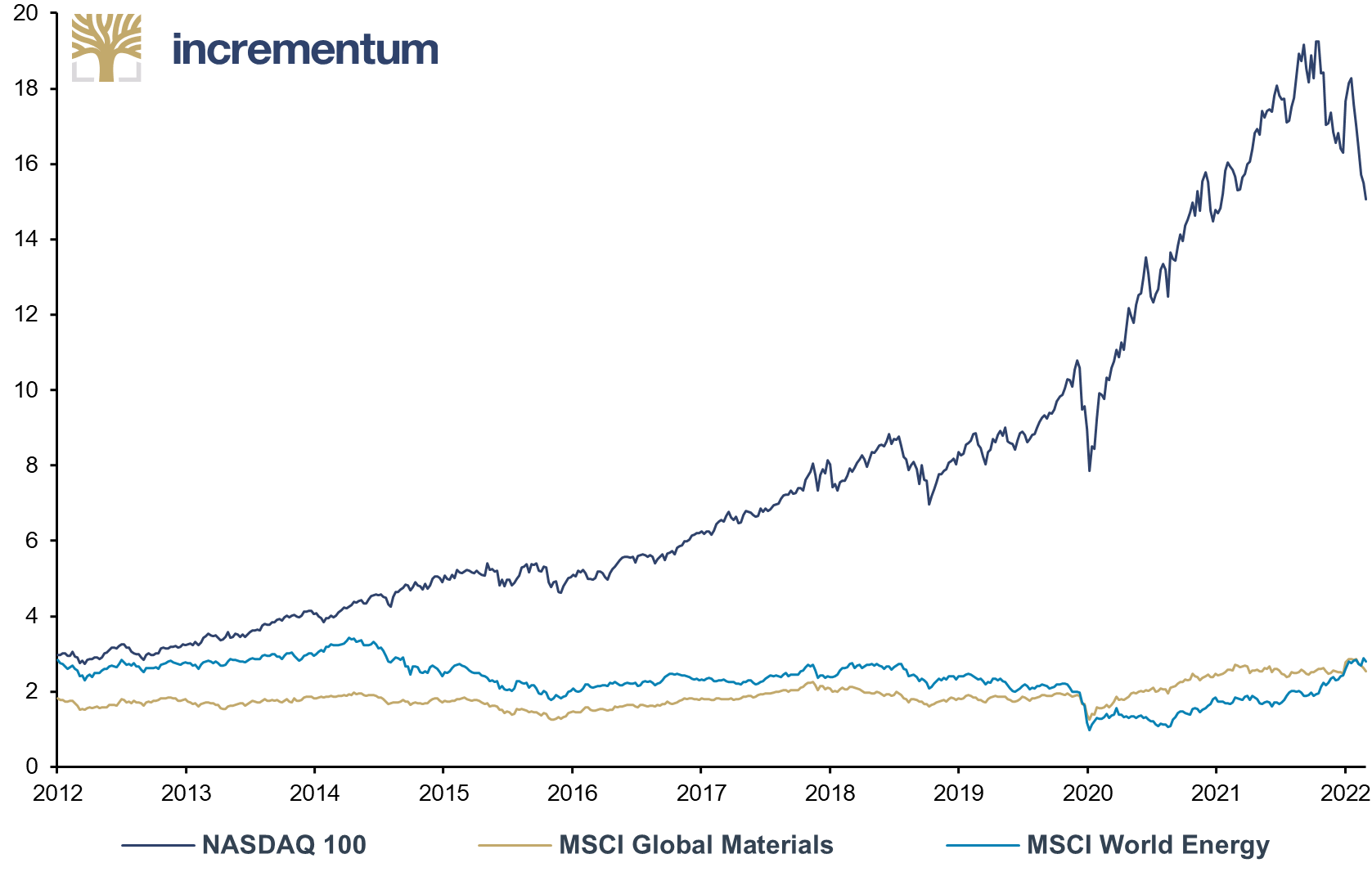

One thing is certain: You will not be able to defeat a wolf and a bear in combination with a classic 60/40 portfolio. The historical performance of gold, silver and commodities in past periods of stagflation argue for a correspondingly higher weighting of these assets than under normal circumstances. But also, the relative valuation of technology companies to commodity producers is an argument for a countercyclical investment in the latter. BoA’s market strategists are already talking about FAANG 2.0:

- Fuels

- Aerospace

- Agriculture

- Nuclear and renewables

- Gold and metals/minerals

Market Capitalization of NASDAQ 100, MSCI Global Materials, and MSCI World Energy, in USD trn, 03/2012-05/2022

Source: Bloomberg, Incrementum AG

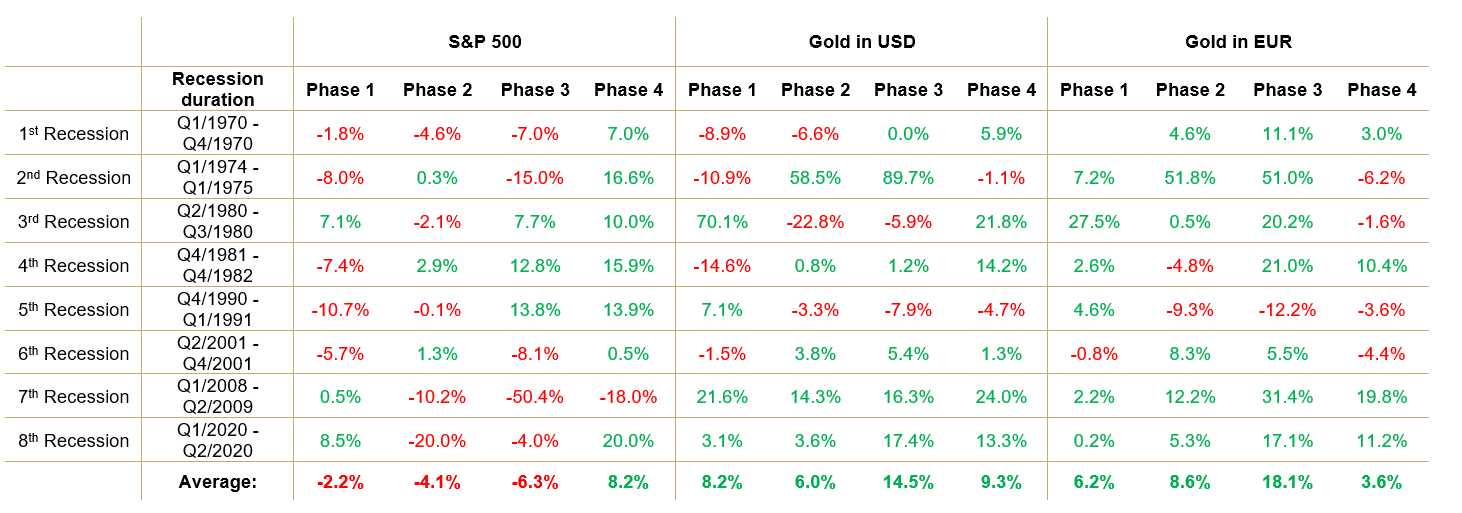

For gold, recessions are typically a positive environment. As our analysis in the In Gold We Trust report 2019[6] has shown, times when the bear dominates in markets and the real economy are good times for gold. If we look at performance over the entire recession cycle, it is notable that in each of the four recessionary periods[7] gold saw significant price gains on average in both US dollar and euro terms. In contrast, equities as measured by the S&P 500 were only able to make significant gains in the final phase of the recession. Thus, gold was able to superbly compensate for equity losses in the early phases of the recession. Moreover, it is striking that, on average, the higher the price losses of the S&P 500, the stronger gold performed. Once again, this worked well during the most recent recession in 2020.

Source: Federal Reserve St. Louis, World Gold Council, Incrementum AG

Overall, it can be seen that gold has largely been able to cushion share price losses during recessions. For bonds, the classic equity diversifier, on the other hand, things look less good. The high level of debt, the zombification of the economy, and the still very loose monetary policy reduce the potential of bonds as an equity hedge. Gold will therefore remain an indispensable portfolio component in the future, allowing investors to sleep soundly in stressful situations in financial markets.

Cold War 2.0 as a Structural Inflation Driver?

In his bestseller The Great Illusion, published in 1911, Norman Angell, who was later to be awarded the Nobel Peace Prize, made the game-theoretical argument that wars between industrialized nations, in view of international economic interdependence, would entail such high economic and social costs that it would henceforth be irrational to start one. Accordingly, the great illusion was suffered by the state leader who expected a positive payoff for his country from a war.

It is distressing how, after more than a hundred years, a large part of the public and the political elite could once again have fallen under exactly the same delusion. Until February 23 of this year, the belief in a world order persisted, in view of which, according to Peter Sloterdijk, people in large parts of Europe convinced themselves that “we had left the epoch in which wars take place”, while Putin mobilized his forces before everyone’s eyes but in the blind spot of this world view.

We hope and believe that an escalation to the extreme between NATO and Russia will be avoided. But entering into a protracted, expensive and grueling second Cold War seems increasingly likely. Turning point, paradigm shift, and caesura are among the terms that have recently been used in an almost hyperinflationary manner. The fact is that numerous asset classes have already priced in a geopolitical (war) premium and that the heyday of globalization and its disinflationary effect have come to an end.

Russia will be a pariah state for the Western community for many years to come. In reaction, Russia will turn more and more to Asia economically and politically. The planned 2,600km long gas pipeline Power of Siberia 2, for example, will enable Russia to supply Western Siberian gas from the Yamal Peninsula to China in the future. Currently, only exports to Europe are feasible via the existing pipeline network.

Thus, it seems likely that a Western community of shared values and a pan-Asian community of convenience dominated by China and Russia will contest world affairs in the future. Regions that traditionally have not hewn to either of the two blocs (Latin America, the Gulf states, Southeast Asia, Africa) will presumably enter into temporary alliances on a situational basis and opportunistically, or will decide for or against strategic integration into one of the two spheres after weighing up their economic, political and cultural interests.

The striving for block self-sufficiency will prove to be almost impossible, especially for Europe, and in any case very expensive. The commodityleverage that Russia, but also China, have vis-à-vis Europe is underestimated.[8] Zoltan Pozsar highlights the case of Germany, where commodity imports – mainly energy imports from Russia – worth USD 27bn support economic activity worth USD 2trn. However, the leverage effect of commodities has a striking impact not only on economic development but also on inflation.

For the EU, for example, Russia is a major supplier of palladium, an important element for chemical and automotive catalysts, fuel cells and electronic applications. According to the US Geological Survey, the EU imports 98% of its rare earth elements (REEs) from China. Rare earths are indispensable components of many high-tech products, including military equipment and renewable-energy equipment. However, the shift from carbon-based forms of energy to so-called renewable energies, which are now also referred to as “the energy of freedom”, only exchanges one dependency (Russia) for another (China).

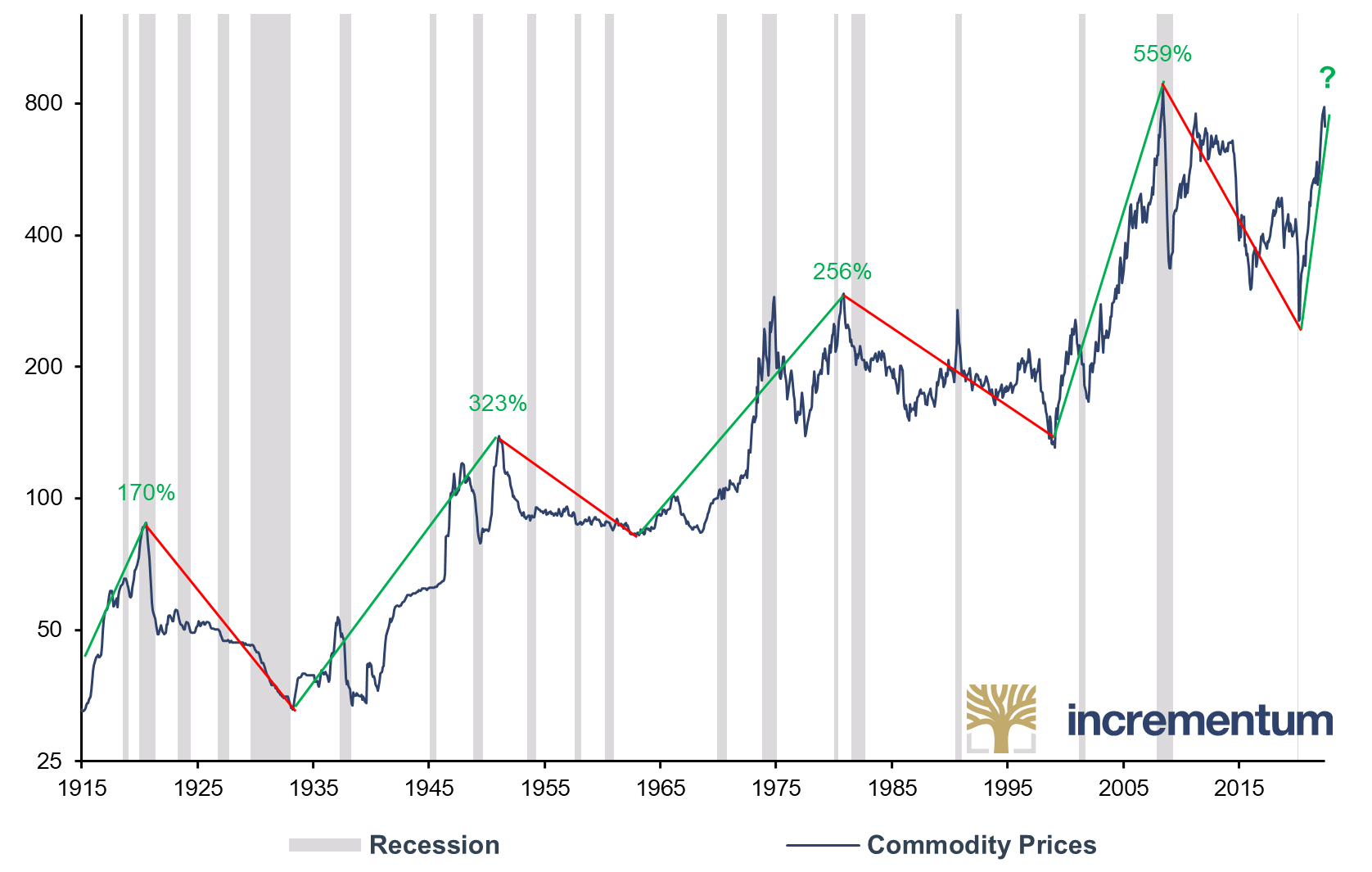

From energy to base and battery metals to precious metals and agricultural commodities, the Ukraine war is now further disrupting supply chains and long-established supply/demand patterns. This will cause commodity prices to settle at a new, higher level.

Commodity Prices*, 01/1915-04/2022

Source: Alpine Macro, Federal Reserve St. Louis, Reuters Eikon, Incrementum AG

*1913-1934 US PPI Industrial Commodities, 1935-1949 Spot Price 28 Commodities, 1950-1969 Spot Price 22 Commodities, since 1970 S&P GSCI

In the short term, the situation on the commodity markets looks overbought. As long as the Federal Reserve makes no move to leave the path of interest rate hikes, the general environment for risk assets will remain difficult. A reversal of monetary policy or the Federal Reserve’s pushing the monetary policy pause button will give the starting signal for the next upward cycle. This will probably be accompanied by a weaker US dollar. The upward momentum in recent months despite the firm US dollar has been surprising to us and at the same time a sign of the inherent strength of the commodity bull market. An increasingly expansionary China – after all, a new president will be elected by the National People’s Congress in the fall – should also provide further support for the sector.

Gold and the weaponization of money

The emerging bloc formation will fundamentally reshape the existing global monetary order. The ization of money through the freezing of Russian foreign exchange reserves has further accelerated the process of de-dollarization. Certainly, new multinational institutions and arrangements do not emerge overnight. But confidence in the existing US dollar-centric monetary order is likely to become passé in many strategically important countries.

Given the multipolarity that can be expected, the new world monetary order will need an internationally recognized anchor of trust, and gold seems predestined for this purpose for several reasons.

- Gold is neutral

- The US dollar, hitherto the global reserve and trading currency, has, with the freezing of Russia’s currency reserves, given up the appearance of political neutrality that is necessary for this status. Gold, on the other hand, belongs to no state, no political party, no dictator. In a new world monetary order, gold can thus represent the unifying element in a multi-polar world that has become much more fragile.

- Gold has no counterparty risk

- Financial assets have a counterparty risk. If the debtor does not want to pay or cannot pay, the creditor’s claim is worth nothing. Gold, on the other hand, has no counterparty risk. And the risk of the owner being prohibited from accessing his gold is easily solved for states by storing their gold within the state’s borders or with a friendly state.

- Gold is liquid

- Gold is one of the most liquid assets worldwide. In 2021, gold was traded daily to the tune of almost EUR 150 In a study, the LBMA showed that gold has higher liquidity than government bonds in some cases.

Best of In Gold We Trust Report 2022

Other key findings from this year’s In Gold We Trust report, Stagflation 2.0, include the following:

- Debt: Appearances are deceptive – this is how the development of the debt situation in 2021 can be summarized. The decline in (government) debt ratios is primarily attributable to the fact that economic growth in 2021 was well above average due to the pronounced economic slump in 2020. The decline in debt ratios due to this base effect is by no means an indication that the trend toward ever higher debt (ratios) has been broken. Nominal debt, on the other hand, exceeded USD 300trn for the first time.

- Inflation: Even though we think it likely that inflation rates will slowly pull back in H2 2022, we expect successive waves of inflation – analogous to the Covid-19 waves. And it seems that the next inflation virus variant is already being announced. One thing is certain: The era of the “Great Moderation” is definitely over.

- De-dollarization: The freezing of Russian currency reserves is comparable in its impact on the global monetary order to Richard Nixon’s closing of the gold window in 1971. And while the Ukraine war preoccupies the West, Moscow and Beijing are expanding their cooperation. The long-unchallenged (petro)dollar is battered, as evidenced by the fact that the relationship between Saudi Arabia and the US has rarely been worse than it is right now. What the global monetary order will look like when the dust settles is unclear. What seems certain is that gold and commodities will gain considerably in importance.

- Bitcoin: The stock-to-flow model (S2F model) has been able to explain the price development of Bitcoin remarkably well historically. In the current cycle, however, Bitcoin’s price is significantly below the range assumed by the model. Although Bitcoin is currently back in a veritable bear market, its adoption continues to grow, particularly among institutional investors but also among governments.

- Silver: The price of silver has disappointed many investors in view of the explosion of inflation. Is silver no longer a monetary precious metal that hedges against inflation? There were two weighty reasons for this disappointment. First, real interest rates stopped falling in August 2020. The inverse correlation of silver and real rates stopped the price rise. Second, consumer price inflation does not necessarily equate to monetary inflation. The good news – at least for silver investors – is that the probability of an inflationary decade is high.

- Mining stocks: The main reasons for the weak performance of the gold mining sector are capital expenditure (CAPEX) overruns, rising production costs, problems with permitting new mines, political instability, and declining reserves and new discoveries. Due to rising energy and construction material prices, increasing wage demands, and general inflation, all-in sustaining costs (AISC) are expected to increase further in the foreseeable future.

- Royalty and streaming companies: The market capitalization of this segment of the mining sector has increased from USD 2bn to more than USD 60bn in 15 years. An index of royalty and streaming companies in the precious metals sector outperformed gold and silver mining companies.

- ESG: In the new low-emissions economy, a new economic metric needs to be created for the mining sector: the all-in emissions cost (AIEC). This metric will transform nonfinancial costs into financial costs for investors and stakeholders. In principle, an increase in the proportion of gold in an investor’s portfolio will translate to a significant positive impact on the CO2 footprint and emissions intensity of the overall portfolio.

- Technical analysis: The analysis of market structure, sentiment and price patterns leads us to a rather mixed technical assessment in the short term. Although sentiment has clouded recently, an extreme bearish wash-out has not (yet) taken place. From a seasonal perspective, the next few weeks could still bring headwinds.

Quo Vadis, Aurum?

For gold investors, 2021 was disappointing due to the sharp rise in inflation. Perhaps expectations were also too high, as 2019 and 2020 were fantastic years for chrysophiles. But in the last couple of months, gold fulfilled its role quite well, in our opinion, even if its 2021 performance lagged general expectations. It has provided stability and calm to portfolios in the wake of recent volatility. The gold price has stood up to collapsing equities, bonds, and crypto markets, as well as the rallying US dollar.

However, real upward momentum in the gold price can only be expected again when a turnaround to ultra-loose monetary policy is once more heralded. When that will happen is the crucial question.

So how seriously can the Federal Reserve’s hard line be taken? During his semi-annual questioning before the Senate Banking Committee, Jerome Powell was asked by Senator Richard Shelby (Rep): “Volcker put the economy in a recession to get inflation under control. Are you prepared to do what it takes to get inflation under control?”, to which Powell replied, “I hope history will record that the answer to your question is yes.”

The Federal Reserve seems to be serious. However, if the communicated tightening is implemented consistently, the Everything Bubble threatens to end in the Everything Crash. Stocks, bonds and cryptocurrencies have already fallen victim to the tighter monetary policy. Real estate would be next on the list.

Internationally, too, distortions are to be expected as a consequence of monetary policy tightening in the US. The euro area, but also Japan, could be threatened with trouble due to rising yields. In the short term, gold holders should therefore probably still expect headwinds, especially if further price declines trigger a panicky situation in markets. However, the bigger the storm on the financial markets, the more likely it is that there will be a renewed abandonment of tight monetary policy.

As soon as the Federal Reserve is forced to deviate from its planned course, we expect the gold rally to continue and new all-time highs to be reached. We believe it is illusory that the Federal Reserve can deprive the market of the proverbial “punchbowl” for any length of time, and we seriously doubt that the transformation of doves into hawks will last. Most hawks will merely turn out to be doves in hawk’s clothing and will shed their hawkish garb sooner rather than later as a result of the inevitable consequences of monetary tightening: recession, rising yields, stock market corrections, bankruptcies, unemployment.

If the downward trend on the stock and bond markets that has persisted since the beginning of the year continues, a brash counter-reaction by the Federal Reserve seems to be only a matter of time. What might a new U-turn look like? What novel rabbit can central bankers pull out of their capacious hat? The following instruments are still in the toolbox of monetary and fiscal policymakers:

- Yield curve control

- Renewed QE or QQE

- Financial repression

- Other fiscal stimuli

- MMT or helicopter money

- CBDCs

- In the euro area: further communitization of debt via issuance of additional eurobonds

The use of one or more of these instruments is a foregone conclusion, with the further merging of monetary and fiscal policy proceeding inexorably. One thing is certain: The coming rescue measures will take on increasingly larger, more aggressive, and more abstruse features.

A successively higher share of deficits will be financed via the digital printing press. The longer and closer this liaison between monetary and fiscal policy continues, the greater the stagflationary forces and the higher the probability of a complete loss of confidence.

Many portfolios still seem inadequately prepared for Stagflation 2.0. This is probably due in part to the fact that there are almost no fund managers in service today who have experienced an inflationary, much less a stagflationary environment during their investment careers. In addition, most portfolio approaches are based on backtesting strategies that go back 10, 20, or at most 30 years. However, very few portfolio strategies take into account the stagflationary environment of the 1970s.

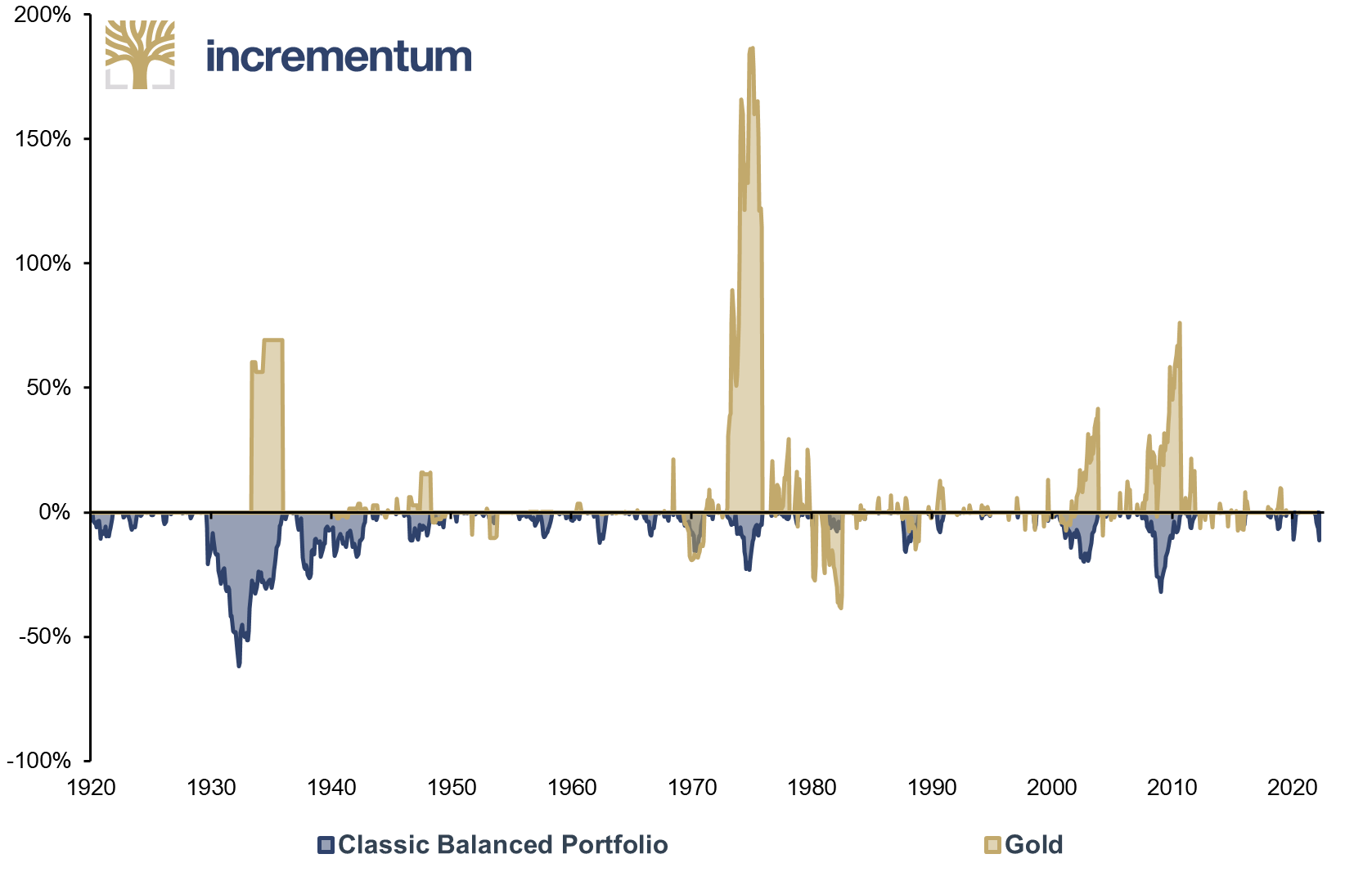

In the current phase, which is characterized by the resurgence of stagflation, the positive correlation between equities and bonds means that a portfolio diversifier is needed that works. History suggests that gold has fulfilled this role admirably. Whenever the traditional portfolio experienced a drawdown, gold proved its capabilities as a reliable portfolio hedge.

Gold Performance During Classic Balanced Portfolio* Drawdowns, 01/1920-04/2022

Source: Bridgewater, Reuters Eikon, goldchartsrus.com, Incrementum AG

*60% Stocks (S&P 500 TR)/ 40% IG Bonds

Two years ago, on the occasion of the transition into a new decade, we presented our gold price forecast until 2030 in the In Gold We Trust report 2020.[9] The central input factor of this estimate was the gold coverage ratio of the money supply. In our base case scenario at that time, we assumed an annual M2 money supply expansion of 6.3%. The resulting price target was around USD 4,800.

So far, gold has aligned itself quite well with our predicted price trend. For gold to remain on track through the end of the year, it would need to rise to USD 2,187. Taking into account the developments discussed in this year’s In Gold We Trust report, we firmly believe that this is a realistic target, provided that monetary policy moves away from the announced hawkish path. Likewise, we maintain our long-term price target of around USD 4,800 by 2030.

Intermediate Status of the Gold Price Projection until 2030: Gold, and Projected Gold Price, in USD, 01/1970-12/2030

Source: Reuters Eikon, Incrementum AG

The coming years will undoubtedly be challenging for investors. Wolf and bear are fascinating predators, but in the economy they are a duo infernale that will demand everything from investors during Stagflation 2.0. Volatility in capital markets, in global politics, in the economy, in interest rates, and especially the volatility of inflation will be with us for some time. We are firmly convinced that gold increases the resilience of a broad portfolio, especially in this environment, and should be an indispensable portfolio component in the context of Stagflation 2.0.

We look forward to continuing to analyze gold-related developments for you and to sharing our thoughts with you. Together we will master these challenges. Because, even more so in the maw of Stagflation 2.0:

IN GOLD WE TRUST

[1] All previous In Gold We Trust reports can be found in our archive.

[2] See Reik, Trey: “Broad Equity Valuation and Market Internals,” Bristol Gold Group, March 31, 2022

[3] See Stöferle, Ronald, Taghizadegan, Rahim and Hochreiter, Gregor: The Zero Interest Trap, 2019

[4] Gromen, Luke: FFTT, February 18, 2022

[5] See “The Status Quo of Gold,” In Gold We Trust report 2021, pp. 43–45

[6] See “Portfolio characteristics: gold as an equity diversifier in recessions,” In Gold We Trust report 2019.

[7] Phase 1: Entry phase; Phase 2: Unofficial recession; Phase 3: Official recession; Phase 4: Last quarter of recession.

[8] See 13D Research: What I learned this week, April 21, 2022

[9] See “Quo vadis, aurum?”, In Gold We Trust report 2020