My View of the Nixon Shock – Exclusive Interview with FOFOA

“Severing the link between physical gold and XAU will usher in a new golden age that I like to call Freegold.”

FOFOA

Key Takeaways

- The Nixon Shock 50 years ago marked the halfway point in the life of the US dollar-based financial system.

- FOFOA outlines four distinct periods in recent monetary history, and predicts we are now on the cusp of change.

- The gold market is currently run like a fractional reserve currency by the bullion banks, but we could soon move to a new system where gold is freely traded.

- There is a risk to the stability of “paper markets” for gold, which pose a systemic threat to the financial system.

- Gold will be freed of the fractional reserve banking practices of today. The monetary reforms this will lead to will result in a repricing of physical gold.

The whole interview with FOFOA is significantly longer. Thus, we are publishing the interview’s highlights here and making the full version available for download on the following page:

https://ingoldwetrust.report/igwt/exclusive-interview-with-fofoa/?lang=en

Preface

A little more than 20 years ago an anonymous writer who called himself “Another” appeared on the biggest gold discussion board the young internet knew at that time. He seemed to be an insider with deep knowledge of history, politics, and economics. He would go on to write for many years and had an heir, called “Friend of Another” (FOA), who took the torch once Another himself “retired”. To this day we do not know who Another was, where he got his information, and why he chose to share it with the world. But we do know one thing: Some (not all) of his sometimes-outlandish predictions did turn out to be true.

Their body of work stretches from the Bretton Woods deal to the Nixon Shock and the introduction of the euro. It represents one of the most fascinating perspectives on the role of gold in the current and future monetary systems. It also makes a compelling case for a much, much higher price of gold.

To this day people study their work to make sense of it and learn about the gold market. The best-known student of Another and FOA is a blogger who calls himself “FOFOA”, Friend of Friend of Another. He has been working on the topic known as “Freegold” for more than a decade. FOFOA kindly agreed to do an interview for this year’s In Gold We Trust report – his second with us, the first being in 2019. We want to thank him for his effort and time, as this project was conducted over several weeks.

Here are the highlights of our conversation with FOFOA:

The Interview

Q: From your perspective, what happened in August 1971 when Nixon closed the gold window? (I think you once wrote that that was the first time Freegold was tried.)

Yes, in a sense the Nixon Shock did set gold free from the US dollar. Previously, the US dollar had been defined as a weight of gold, and the price of gold was thereby fixed to the US dollar, the same way you would fix the exchange rate of different currencies to the US dollar. It also, however, gave birth to the modern concept of bullion banking. And that’s what the free in Freegold refers to today – the inevitable end of fractional reserve gold banking, which is simply a carryover from the pre-71 gold standard.

The concept of a “singularity” is used in many applications as a point at which either a small change can cause large, sweeping effects, or else so much changes at once that the far side of the singularity is almost impossible to imagine. I like to think of it as passing through a black hole and emerging in a different world on the other side. So what I hope to do here is to give you a 30,000-foot view in which 1971 is both the halfway point in the 100-year life of the International US dollar Reserve Monetary and Financial System (the $IMFS) and also the first of two singularities, the second being Freegold.

The Genoa Conference, which gave birth to the $IMFS, was just over 99 years ago, and the Nixon Shock is virtually the halfway point between then and now. But this isn’t just a story of the last century split in half by the Nixon Shock; there are actually four distinct quarters in this story.

$IMFS Q1

The first quarter, broadly, was the interwar period, or the period between the First and Second World Wars. It really had its economic ups and downs. It began with the prosperity and decadence of the Roaring Twenties; then the stock market crashed in 1929, followed by the Great Depression, the social welfare programs of the New Deal, and finally the devastation of World War 2, which set the stage for the second quarter to begin at Bretton Woods.

$IMFS Q2

Bretton Woods, the IMF, the World Bank, and the Marshall Plan were all structured to help Europe rebuild its economy after the war, by overvaluing European currencies and undervaluing the US dollar with fixed exchange rates. This allowed Europe to run a trade deficit with the US while it rebuilt its productive capacity.

That situation reversed around 1958, when Europe was back on its feet enough to start running a surplus while the US slipped into recession. That year also marked the beginning of the decline of US gold holdings, from 20,312 tonnes in 1957 down to 9,070 tonnes in 1971.

One of the pillars of Freegold is the concept of the saver. The idea is that the vast majority of people are actually savers as opposed to being real investors or traders. But in today’s $IMFS, they are forced to swim with the sharks, so to speak. Today we call savings passive investment, but in Freegold everything will have changed for the savers – like passing through a singularity.

Something similar happened to the concept of the saver as it passed through the first singularity, the Nixon Shock. One of the outcomes of the prosperity and growth of the 1950s was the concept of the defined-benefit retirement fund. The idea was that you didn’t need to save for retirement because your employer did it for you. The obligations this concept generated were based on an unsustainable growth model. It was the idea that the rate of growth in the 1950s would continue forever, and it became something like a Ponzi scheme. The collapse of the Studebaker Corporation[1] and its pension fund is a prime example, and it gave birth to the idea of the individual retirement account.

Q2 began with the promise of recovery, high growth and prosperity, and ended with a systemic collapse and broken promises.

The 1st Singularity

There’s a website called wtfhappenedin1971.com, and all it contains is about 50 charts that make it look like everything went haywire in 1971. And, in effect, everything did change. But from a systemic perspective, the closing of the gold window and the ending of the Bretton Woods monetary system were simply inevitable. The 1st Singularity was inevitable. It wasn’t an effect of what Nixon did, it was the cause.

The financial system changed as well. We went from the centralized obligations of defined-benefit retirement funds to the more distributed “defined-contribution” system of individual IRAs and 401Ks through the passing of the Employee Retirement Income Security Act of 1974. This had the effect of funneling everyone’s savings into paper assets, giving birth to the massive bubble machine we call the financial system today.

What happened in 1971 was bigger than Nixon. Yes, gold was set free from the US dollar, and Nixon gets credit for that. But systemic transitions of that magnitude simply become inevitable at some point, and while we like to heap credit on those in power when they happen, the reality is that they were going to happen anyway, no matter who was in the White House at the time.

$IMFS Q3

An overarching theme of the third quarter was that, following the Nixon Shock, Europe no longer trusted the US dollar reserve system. They had just watched Bretton Woods collapse, and they didn’t like the global economy being at the mercy of a single national currency that would eventually collapse and drag the world into another global depression.

The solution was to create a new international reserve currency that rivaled the US dollar in both size and scope. At least then, if the US dollar collapsed, Europe’s economy wouldn’t suffer as much. But these things take time. A lot of time, it turns out.

There are three points in Q3 when Another and his associates apparently worried that the $IMFS might collapse even before they could launch the euro. The first was in 1979, when a group of European central bankers confronted Paul Volcker at the IMF meeting in Belgrade.

The Federal Reserve’s actions four days later have been called the most significant change in the Federal Reserve’s policy since 1932. But more importantly, the Belgrade confrontation marks the resumption of the dirty float, the European central banks’ support for the US dollar, which had ended a year earlier in 1978. So while Volcker’s actions made all the headlines, there was more going on quietly in the background, on the European side.

The second point in Q3 came in 1988. The US Dollar Index had reached a high of 164 in February 1985. The Plaza Accord, reached in September of that year, aimed to drive down the US dollar through coordinated exchange rate manipulation. The stock market soared, while the US dollar declined. Then the Louvre Accord, reached in February 1987, aimed to halt the decline caused by the Plaza Accord.[2] Eight months later was Black Monday, the stock market crash of 1987.

In a post titled “Some things I know”, FOA wrote:

“This work [meaning what he and Another were explaining] started back in 1988, not long after the 87 crash. Important people were asking some very serious questions about the timeline of the world monetary system. They expected a long-term evolving report… the effort you have seen to date is one of sharing somewhat for the common good of all.”

What he was revealing there was that the view presented by Another beginning in 1997 was at least in part the result of a high-level “long-term evolving report” that had been commissioned shortly after the stock market crash of 1987. He continued:

“Leaders wanted to know how one could retain the most wealth during such an event. It was thought that if the basic extended family blocks of a nation could survive such a collapse, savings intact, those nations and their children would be a benefit to economic affairs of the future. In effect, negate a possible return to the Dark Ages of European history.”

The third Q3 point was in 1996, and it was what led Another to start posting on the Kitco forum. An explosive jump in the volume of paper gold trading occurred in 1996 and was publicly revealed by the LBMA in the Financial Times on January 30, 1997.[3] To understand why this mattered to Another, and why it still matters today, we need to go back to the early 1970s and trace the evolution of the gold market following the Nixon Shock.

Gold’s Transformation from Being a US Dollar to Becoming a Foreign (FX) Currency

The first step, after the closing of the gold window, came in 1974, when President Ford repealed FDR’s ban on gold ownership in the US. Then, in 1975, COMEX gold futures began trading. London responded to COMEX by giving birth to the bullion bank and opening its gold market up to foreign banks that wanted bullion trading rooms in London.

In 1981, gold (and only gold) received its official ISO 4217 currency code: XAU. (XAG/silver, XPT/platinum and XPD/palladium were added years later.)

In 1984, the pioneer of modern bullion banking, Johnson Matthey Bankers, also one of the London fixers, collapsed. In the aftermath, the Bank of England demanded that the bullion banks create a formal body to represent them as a group. And so in 1987 the LBMA was born. Around the same time, in the mid-1980s, CB gold lending and gold mining forward sales began, creating a new form of paper gold.

European central bankers apparently thought that keeping the price of gold under control was a necessary part of supporting the $IMFS until they could launch the euro, because, according to Another, they enabled the massive expansion of this forward selling scheme by guaranteeing the paper with their own central bank gold. The Saudi demand for real gold, which was greater than the available supply at the going price, was the big threat to the gold price at that time, and so a deal was made.

This kept the prices of gold and oil, both of which were priced in US dollars, low when they otherwise would have exploded, as during the Gulf War in 1990 and 1991. And that’s how this new paper gold market helped support the US dollar and the US dollar system through the 1980s and 1990s. What was happening was that gold was being used as a foreign currency to hedge the $IMFS, which ever since the Nixon Shock had evolved away from being used mainly for trade in real goods, and had become primarily a financial-asset trading arena – a bubble machine – which needed a hedge in order to continue its expansion.

$IMFS Q4

Q4 runs from 1997 to present, and begins with the launch of the euro, Brown’s Bottom, the dotcom bubble, and China’s admission into the World Trade Organization in 2001. It continues with the housing bubble and its collapse, which caused the Global Financial Crisis and stock market crash in 2008, followed by a decade of monetary stimulus which brings us to today’s everything bubble and the end of the road.

I say “end of the road” because, from here on out, we’re in uncharted territory. There is no road, no trailhead, no tracks; we are completely off the rails and careening out into the great unknown. But I’m getting a little ahead of myself. Let’s go back to the late 1990s and look at what changed during the transition from Q3 to Q4.

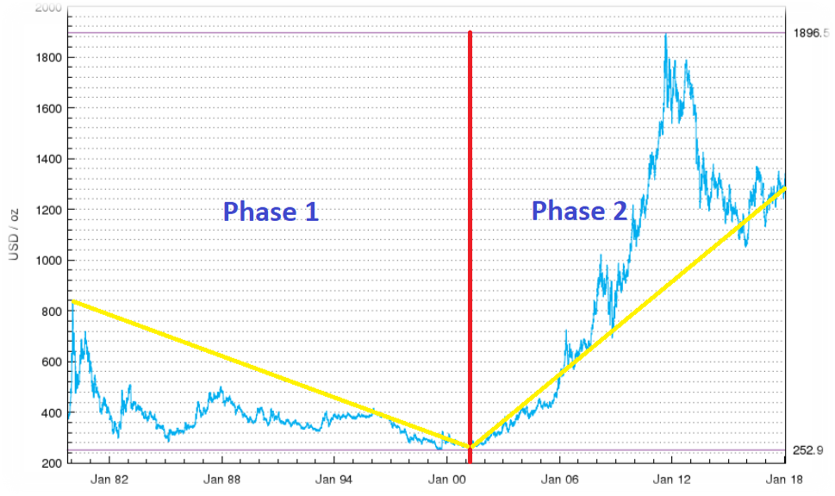

Brown’s Bottom was when Gordon Brown sold off half of the UK’s gold in a series of auctions, between July 1999 and March 2002. That period marked the lowest gold prices in the last 42 years. The purported reason for the sales was the diversification of the UK’s reserves, away from gold and into foreign currencies including the new euro. But many believe the sales’ true purpose was to bail out the bullion banks, which were running out of physical.

A few months after the first Brown’s Bottom auction, 15 European central banks signed what was called the “Joint Statement on Gold” and came to be known as the Washington Agreement on Gold (WAG), or Central Bank Gold Agreement (CBGA). In short, the European central banks agreed to limit their gold sales, but more importantly, they agreed to stop leasing. This was important because it was the CB leasing that had supported the expansion of the paper gold market over the previous 15 years or so.

Also, it was the expansion of the paper gold market that caused the price to decline over time; so with the expansion halted, we entered a new phase in this paper gold market that had begun in the 1980s:

Source: “Comex is a Side Show“, FOFOA, May 4, 2018

On the US dollar front, Europe stopped supporting the US dollar with CB purchases after the euro launched. But in 2001, with its admission into the WTO, China ramped up its CB purchases in order to peg its currency to the US dollar. By 2014, however, that US dollar support had ended. In fact, if we compare China’s current US Treasury holdings with their peak in November, 2013, we see a reduction of USD 221bn, or 17% over the last seven years. And as far as I can tell, that’s when the dirty float ended.

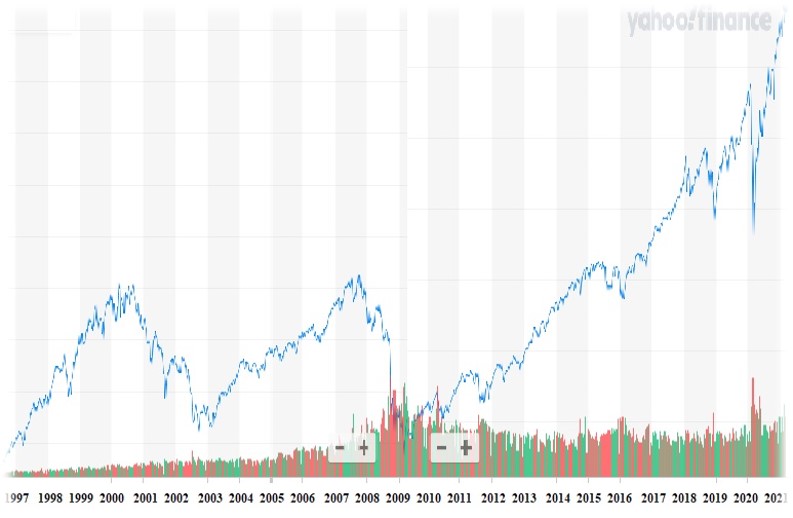

As for the financial system, Q4 compressed into a single image basically looks like this. It’s one bubble after another, ending in a superbubble:

Source: Yahoo Finance

The Nixon Shock, i.e., the 1st Singularity, changed the financial system into a bubble machine; it changed gold from being defined as a US dollar into being a foreign currency; and it changed the US dollar from a unit used mainly for real trade into one used primarily for trading financial assets. In the process, it changed the US economy from the world’s greatest producer into the world’s biggest consumer, financial derivative production notwithstanding.

The 2nd Singularity

This section is about what I see, what I imagine is on the other side of the 2nd Singularity, which I think is just as inevitable as the 1st Singularity. It was going to happen regardless of who was in the White House at the time; but I must admit, it seems even more inevitable given the current administration.

I need to explain a simple concept about gold, however, before I tell you what I see. At the time of this writing, Bitcoin is right around USD 55,000 per coin, which is a number that I have long used for Freegold. Meanwhile, gold is down more than 15% from its high last August. So something I’m hearing a lot is that Bitcoin has done what gold was supposed to do; therefore Bitcoin is the new gold, or something along those lines.

I see this flawed premise everywhere: “Look at gold, it’s down, it’s not doing what it’s supposed to do, which is rise against all this printing and monetary inflation like commodities and other inflation hedges.” But if we look back at history, that’s not how gold works. And it’s not what Freegold predicts.

Historically, gold does its best work at transition points, not in day-to-day price movements. For example, when it was being used as part of the money supply, it didn’t track price inflation, but every 40–50 years or so it would have to be repriced, or it would jump in price due to some sort of transition or crisis (e.g., 1934 and the 1970s). It has never really worked well as an inflation hedge. Everyone assumes it should, but I think that’s a flawed premise, at least in the current system. It’s more of a transition hedge, or a singularity hedge. As Another liked to say, it will be repriced once, and that will be more than enough!

Bitcoin, on the other hand, is performing like the many bubbles throughout history. And while bubbles do not perform well at transition points, they very often pop just prior to them. I’m not making a prediction about Bitcoin here, just explaining a concept. We are in a pretty unique situation right now. We have this sort of traditional bubble dynamic in almost everything, where investors are starting to believe that asset prices can only go up, and are buying some of the strangest things. And at the same time, we have unprecedented levels of monetary inflation and stimulus, which are also pumping the bubbles in a more nontraditional dynamic.

So I think what we’ll get in the end has to be a kind of hyperinflationary price collapse, where the price of everything that’s in a bubble right now collapses in real terms, but not necessarily in nominal terms. That’s “in the end”. We could definitely see a nominal collapse of asset prices initially; but in the end, I think it’ll be in real terms, which can be a lot worse than nominal.

As for the gold market, it is currently run like a fractional reserve currency by the bullion banks. I’m talking about the market where gold trades as XAU. It dwarfs other markets by an order of magnitude, and is therefore the primary driver of the price. You need only to think of it as a currency with its own banking system to see what’s going to happen. It’s not so different from what happened in 1934 and 1971.

In 1933, there were paper US dollars and credit US dollars, and they were all backed by fractionally reserved gold US dollars. Then there were bank runs, essentially redemptions and withdrawals, that drained the gold from the banks, followed by a national bank holiday, which halted the redemptions and withdrawals. One month later, gold coins were called in and removed from the banking system, which was effectively a forced cash settlement of all US dollar balances at the old price of USD 20.67/oz. The link between the currency and the reserve was severed domestically. Then, once that was done, about nine months later, in January 1934, the reserve (gold) was repriced to USD 35/oz., almost a 70% increase.

In 1971, international US dollars were backed by fractionally reserved gold in the US Treasury, which was some of the same gold that had been removed from the domestic banking system in 1933. About half of the Treasury’s reserves had been drained during the previous decade, and the rest could be gone in a flash, given the amount of US dollars held overseas. Then, with a flood of fresh redemption requests coming in from Europe beginning in May of 1971, Nixon closed the gold window, ending redemptions altogether. The link between the currency and the reserve was severed internationally. The Treasury Dept. officially repriced its gold reserves in 1972 and again in 1973, but by then the definition of a US dollar as a weight of gold was meaningless.

Likewise, the gold market today is dominated by a fractionally reserved paper gold currency trade, run by the same banks that also finance and manage the much smaller flow of the global physical gold market. The slack in that flow constitutes the fractional reserves of the system. Redemption and withdrawal of physical from this paper gold currency system is only possible at the margins, not en masse. So, when the financial system collapses, physical redemptions will cease and paper gold balances will be settled in cash at the paper price. The link between the currency (paper gold) and the reserve (physical gold) will be severed.

This is what I see coming on the other side of the 2nd Singularity. I think we’re going to have a collapse, a reset, and a grand liquidation that will lead to a period of rebuilding, which will last perhaps decades. But it won’t be the “Great Reset” agenda of the World Economic Forum (WEF). The collapse is going to include the collapse of such oversized, centralized thinking as the WEF, and the reset is going to usher in a more localized, resilient way of thinking. As Another put it, the old ideas of building solid, enduring, long-term wealth will return.

The collapse will be a collapse of the US dollar system, the financial system, and the paper gold market, and the reset will include the repricing of physical gold. I don’t see the repricing as something that someone needs to enact, but more of a natural and obvious outcome of the collapse. The “grand liquidation” will effectively pass economic assets from the old guard to the new generation, at fire-sale prices that will make them profitable once again, and the rebuilding of a more real and more robust economy will commence. You might even call it a renaissance, or my preference, a new golden age.

My view of the Nixon Shock is that it marked the halfway point in the life of the $IMFS. And while it set gold free from the US dollar, it also gave birth to the modern concept of bullion banking, which entangled gold in a new kind of fractional reserve currency scheme. And as I wrote more than a decade ago, in a 2011 post titled “Freegold Foundations”, that’s what the free in Freegold refers to today – that gold will be freed from the fractional reserve banking practice, which is simply a carryover from the pre-Nixon gold standard. And that newfound freedom, that severing of the link between physical gold and XAU, will usher in a new golden age that I like to call Freegold.

The whole interview with FOFOA is available for download on the following page:

https://ingoldwetrust.report/igwt/exclusive-interview-with-fofoa/?lang=en

[1] See “The Studebaker Effect“, Fofoa, January 11, 2012

[2] See “History Does (Not) Repeat Itself – Plaza Accord 2.0?”, In Gold We Trust report 2019

[3] “Extent of global gold market revealed: London clears 930 tonnes of bullion each day”, Financial Times, January 30, 1997