Introduction: The Big Long

“There is no fever like gold fever.”

Richard Russell

- A new, secular bull market is forming. The golden decade we announced in our In Gold We Trust report 2020, when gold was trading at only USD 1,500, is in full swing. The Big Long is our renewed call to question the generally low gold allocation among investors and to weight safe-haven gold and performance gold to a considerable extent.

- The US’s much-discussed customs and trade policy is just one aspect of a comprehensive realignment. With Liberation Day, Donald Trump has triggered a systemic quake that could result in a reorganization of the monetary architecture.

- The Triffin dilemma is once again taking center stage in the currency debate: A sustainable solution can only be found via a neutral reserve asset such as gold or Bitcoin.

- Drawdowns are an integral part of secular bull markets. Sensible diversification and an active investment approach are particularly advantageous for performance gold. Corrections are opportunities, not threats, for patient investors.

- The “New Gold Playbook” presented in the In Gold We Trust report 2024 remains intact. Asia is becoming increasingly important for the gold price. Western financial investors are now – finally – beginning to rediscover their penchant for gold.

- The softening of the debt brake and the adoption of special debts euphemistically referred to as special assets have heralded the end of fiscal virtue in Germany. However, the euro area’s big problem child remains France.

“The truth is like poetry – and most people hate poetry.” This is how a bartender in the movie “The Big Short” formulates the unflattering insight that “If you tell the truth, you need a fast horse.” Until recently, gold had a similar fate, especially in the Western financial industry. As a safe haven – i.e. safe-haven gold – it was long considered antiquated. As a yielding asset, i.e. as performance gold, it was dismissed as a pipe dream.

At its core, The Big Short – originally a book by Michael Lewis – is about detecting and profiting from economic misallocations. The Big Short illustrates how a combination of low interest rates, lax credit ratings, and excessive leverage created a dangerous euphoria amplified by seemingly infallible financial innovations and embellished ratings from credit rating agencies. Some saw what all could have seen – but few dared to go against the market and take on The Big Short.

In a deeper sense, The Big Short is about philosophical opposites: contrarians versus the mainstream, Main Street versus Wall Street, critics versus believers in the system. Just as outsiders positioned themselves around the investors Michael Burry and Steve Eisman, the situation on the capital market has come to a head in recent months. Investors are currently confronted with the following questions:

- Are government bonds, even US and German benchmark bonds, still safe havens?

- Has the era of US dominance come to an end? Is the US dollar at the beginning of a bear market? Were the interim valuations of the MAG 7 ultimately hopelessly exaggerated?

- Is gold now too expensive?

The conventional answer to the last question is that it is too late to get into gold. The gold price is already too high, so further price potential is limited at best.

The Golden Decade: The Beginning of the 2nd Half

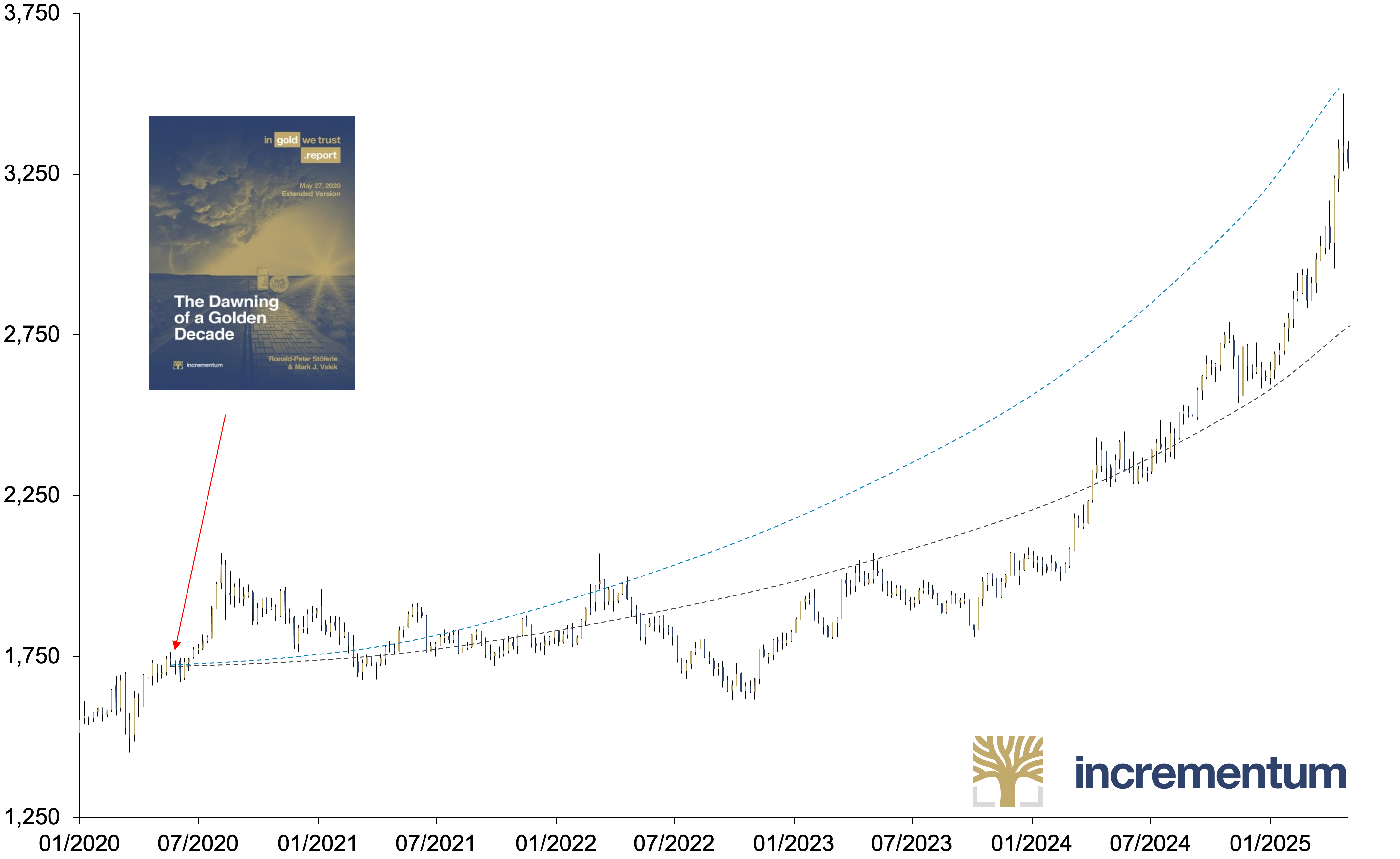

However, we are convinced that this widespread assessment is incorrect. Being strategically clever means acting unconventionally, especially when it comes to investing. Our core thesis is that the gold bull market of recent quarters manifests a long-term upward movement that we forecasted in the In Gold We Trust report 2020, “The Dawning of a Golden Decade”. Back then, we were met with skepticism and sometimes even malice from the mainstream, like some of the protagonists in The Big Short in the mid-2000s. But the figures speak for themselves. Since we proclaimed the golden decade, the gold price in US dollars has risen by 92%, and the US dollar has depreciated by almost 50% against gold.

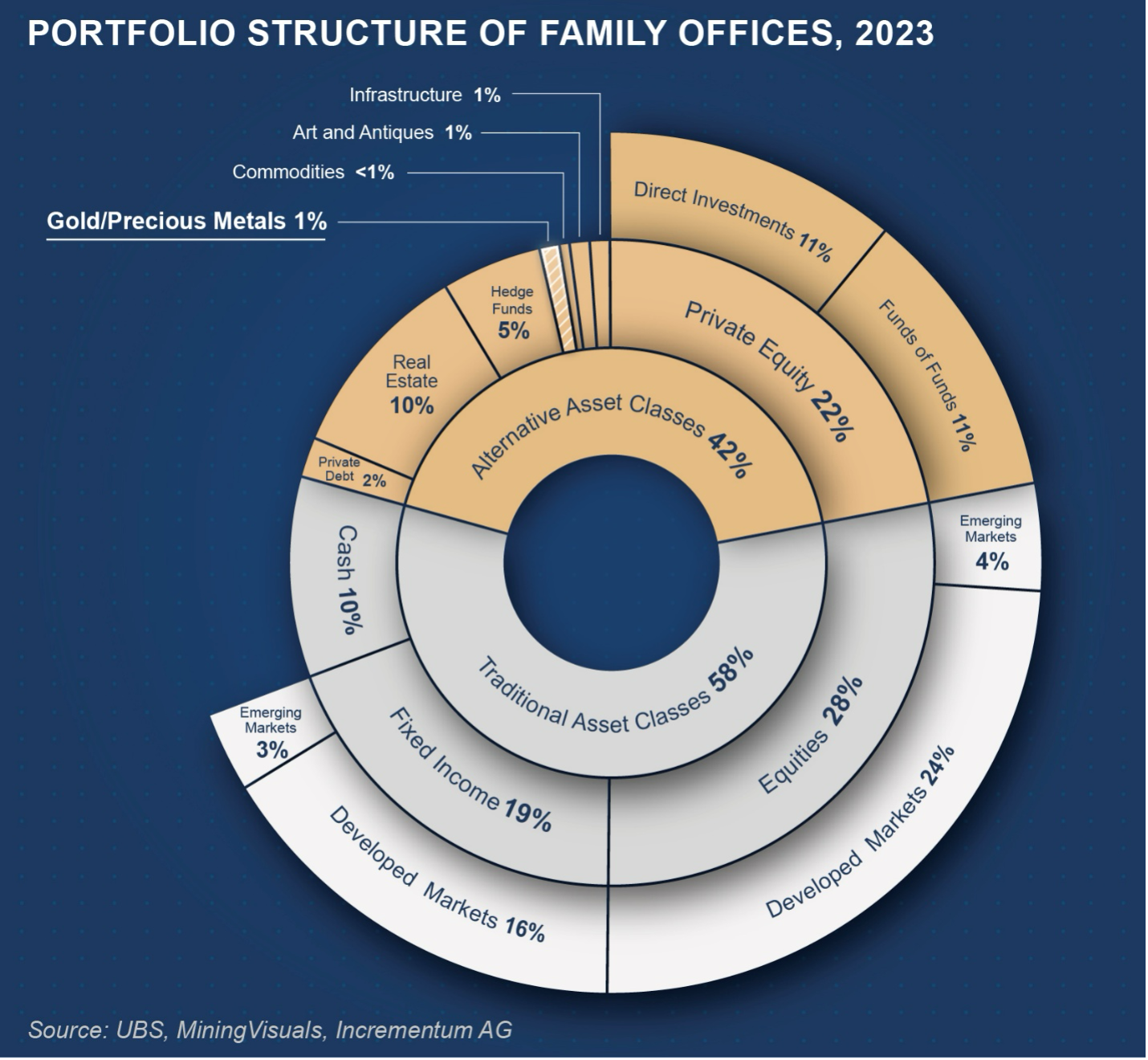

Despite growing interest in gold as a strategic asset, institutional allocations remain strikingly low. As shown in the chart below, family offices allocate just 1% of their portfolios to gold and precious metals – placing it on par with art and antiques, as well as infrastructure, and well below allocations to private equity, real estate, or even cash.

Based on our Incrementum Gold Price Model,[1] introduced in the In Gold We Trust report 2020, we presented the following gold price projections – a base case scenario and an inflationary scenario – in 2020. Since the beginning of the year, the impulsive bull market has already pushed the gold price closer to the inflationary scenario’s projection path than to that of the base scenario.

Gold, in USD, 01/2020–04/2025

Source: LSEG, Incrementum AG

Evidently, in May 2020, when the first Covid-19 lockdowns had just ended, it was impossible to predict how turbulent the first five years of this decade would be. However, our analyses of the changes in the thinking and actions of political and economic players, both before 2020 and in the years thereafter,[2] clearly showed that the course was set for gold.

There is no reason to deviate from this conviction halfway through the decade. Gold is the Ronald Koeman of asset allocation: defensively reliable, strategically astute, and at the same time equipped with offensive potential. Koeman, the highest-goal-scoring defender in soccer history, exemplifies this dual function. Gold also fulfills both roles – it acts as defensive cover and opens up opportunities on the offensive.

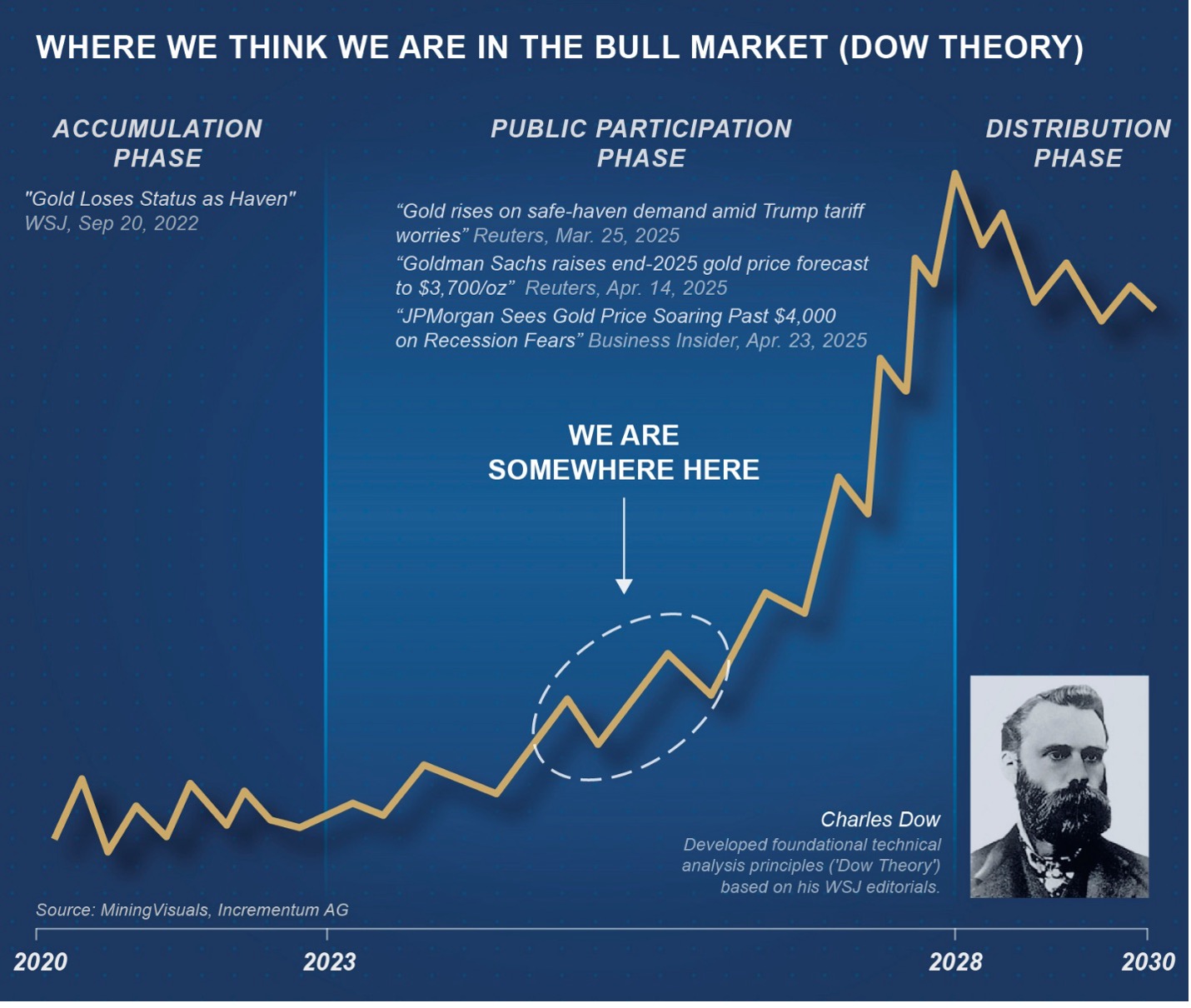

We are now witnessing how a secular bull market is slowly becoming mainstream. The public participation phase – also known as the big move phase – is the second of three phases in a bull market according to Dow Theory. This longest and most dynamic bull market stage is characterized by increasingly optimistic media coverage. At the same time, speculative interest and trading volumes rise, new financial products are launched, and analysts adjust their price targets upwards. In our opinion, we are currently in the midst of this phase, which will ultimately lead to a final mania phase.

The momentum of the gold price is impressive. Gold reached 43 new all-time highs in US dollars last year, the second-highest number after 1979 with 57, closely followed by 1972 and 2011 with 38 each. Since the beginning of the year, gold has recorded 22 new all-time highs as of 30 April.

Gold, in USD, and New ATH Closes, 01/1970–04/2025

Source: 3Fourteen Research, World Gold Council, LSEG, Incrementum AG

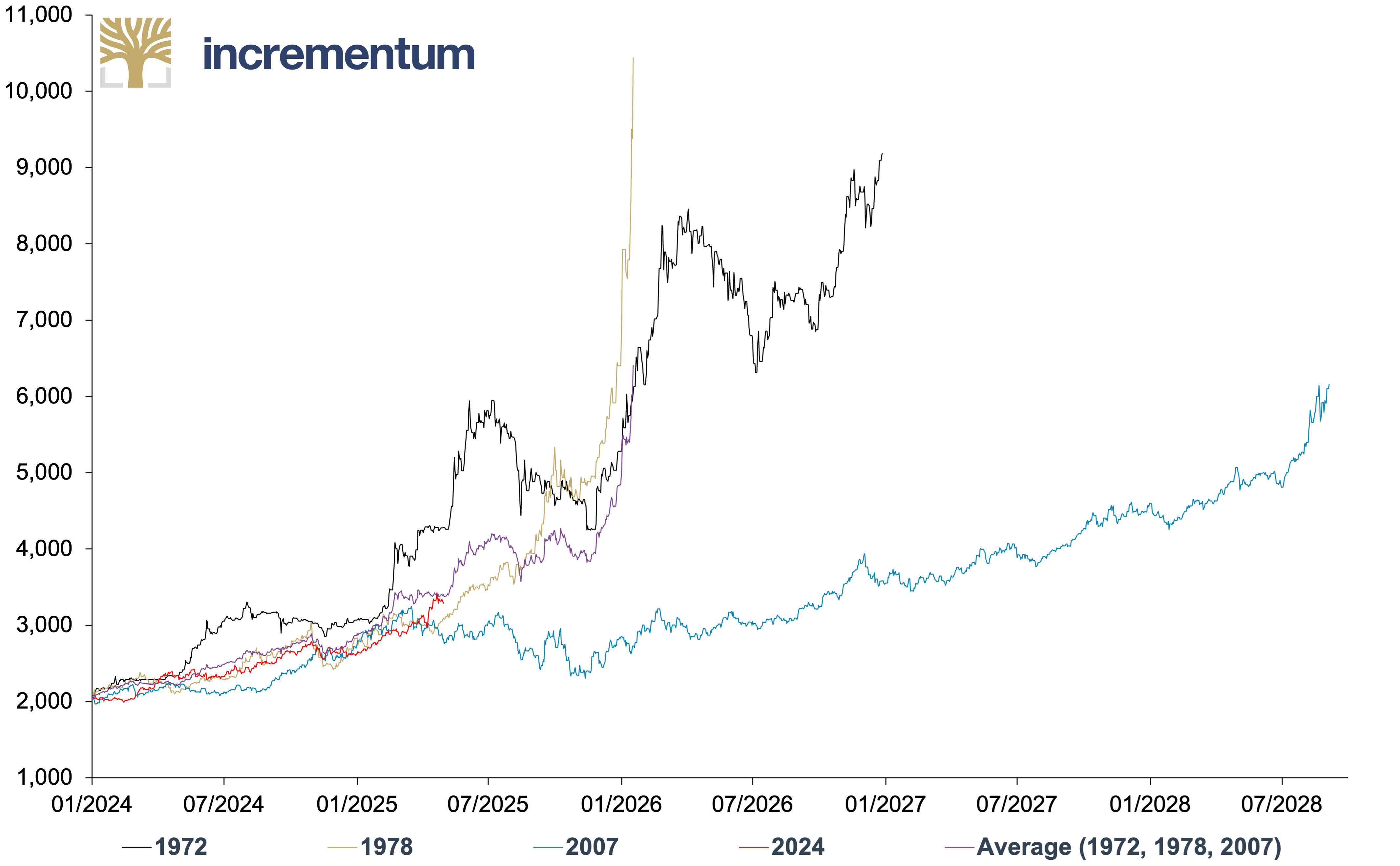

Even if it may not seem so at first glance, given several all-time highs and the rapid breakthrough of the USD 3,000 mark, the current gold rally has been comparatively moderate by historical standards.

Historical Gold Breakouts (Start Price = 01/01/2024), in USD, 01/2024–09/2028

Source: TheDailyGold, LSEG, Incrementum AG

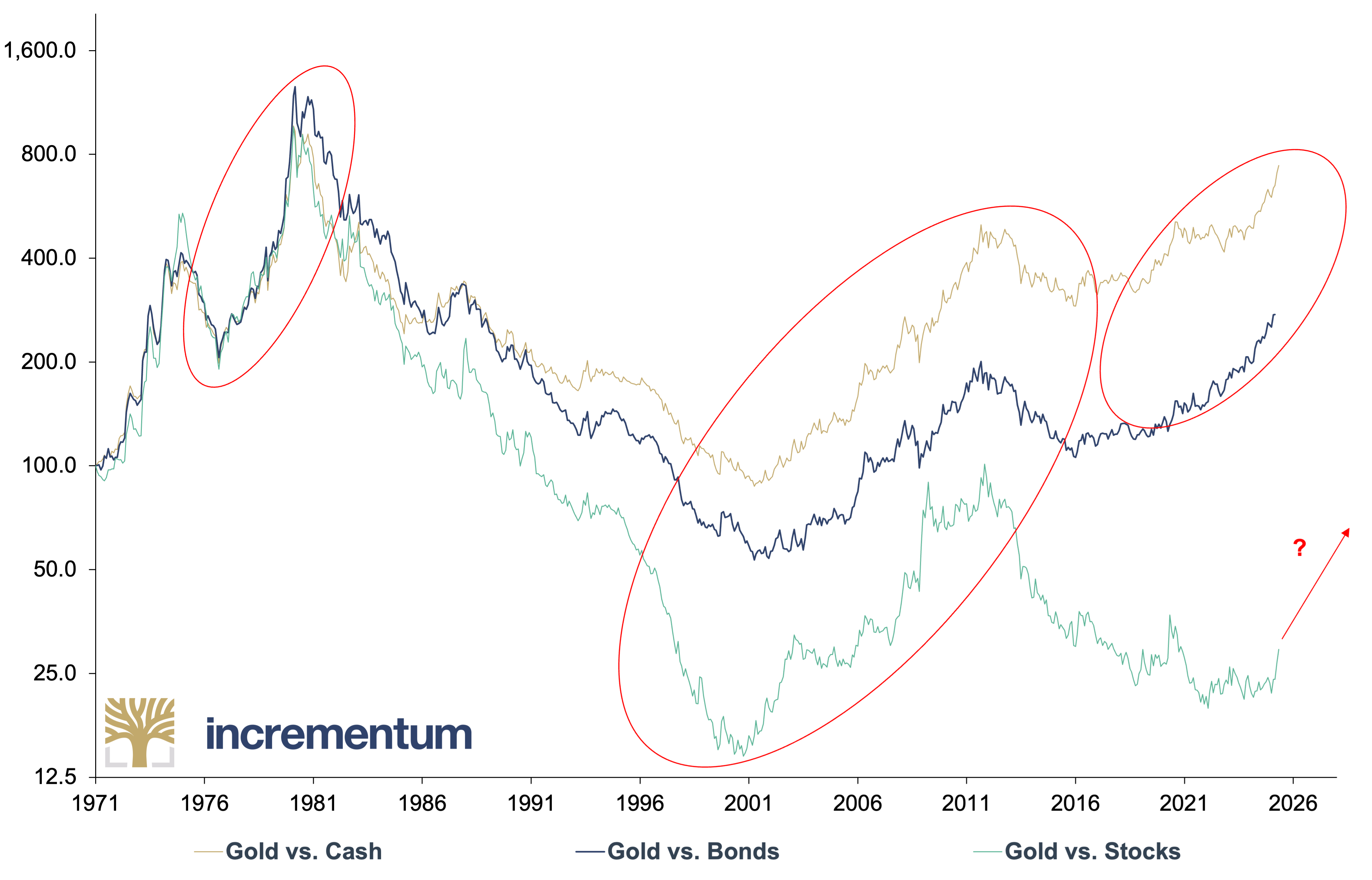

In recent months, gold has increasingly become the focus of public attention as it has reached numerous new all-time highs on an absolute basis and thus entered terra incognita. In our view, however, another aspect deserves even greater attention: Anyone looking “under the hood” of the market will recognize that gold is also recording technical breakouts on a relative basis. In particular, the relative strength now emerging against equities points to the start of a new trend phase.

Gold vs. Cash (US 3M TR), Bonds (US 10Y TR), and Stocks (S&P 500 TR) (log), 100 = 31/12/1970, 01/1971–04/2025

Source: Topdown Charts, LSEG, Robert J. Shiller, Incrementum AG

In this context, The Big Long means one thing above all: holding remains the strategically sensible option for those already invested in gold. However, for newcomers, too, an entry remains attractive. The ideal portfolio weighting of gold is a matter of debate. However, the investment mainstream usually only recommends and implements gold allocations in the low single-digit percentage range, if at all. This reluctance stems from the fact that gold, being a nonproductive asset, does not pay dividends. However, historical observation shows: Gold outperformed yield-generating assets such as equities and bonds, particularly during market-critical phases. Investors should certainly consider this in their strategic asset allocation.[3]

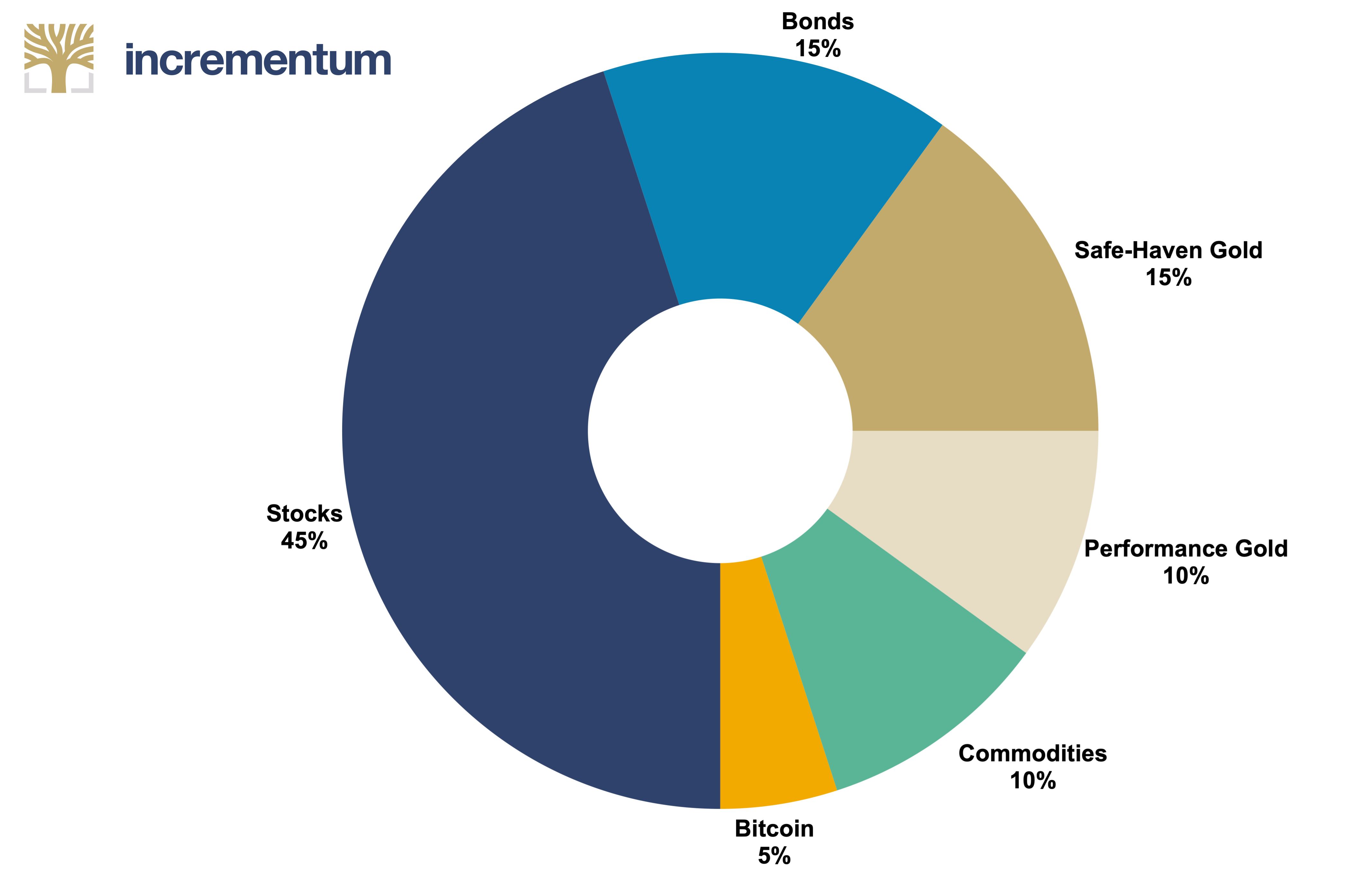

When dealing with the specific level of gold allocation, it is advisable to differentiate between safe-haven gold and performance gold. The Big Long emphasizes the potential of performance gold in the coming years: In our view, silver, mining stocks, but also commodities are among the promising portfolio components of The Big Long, which we presented in detail as part of our new 60/40 portfolio in “The New Gold Playbook” last year.

The New 60/40 Portfolio: Subcategories

Source: Incrementum AG

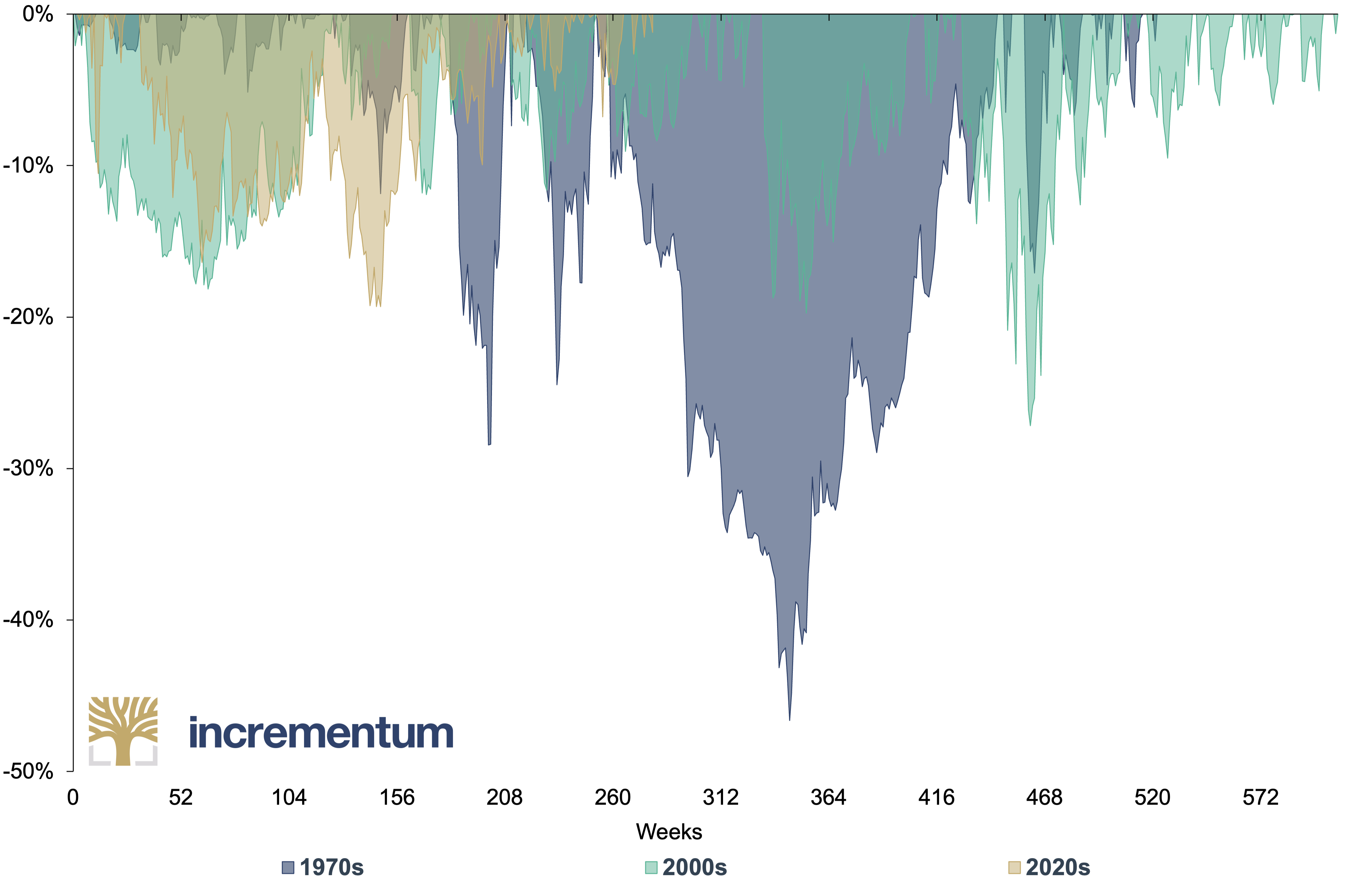

Despite our confidence, we would like to emphasize that a secular bull market is never without setbacks. Corrections of 20, 30, and even up to 40% have been observed several times in previous bull markets. The price turbulence following Liberation Day on April 2 was a reminder of this, even if gold recovered quickly and marked further all-time highs in US dollars a few days later.

Gold Drawdown Comparison During Bull Markets, in USD, 12/1969–04/2025

Source: LSEG, Incrementum AG

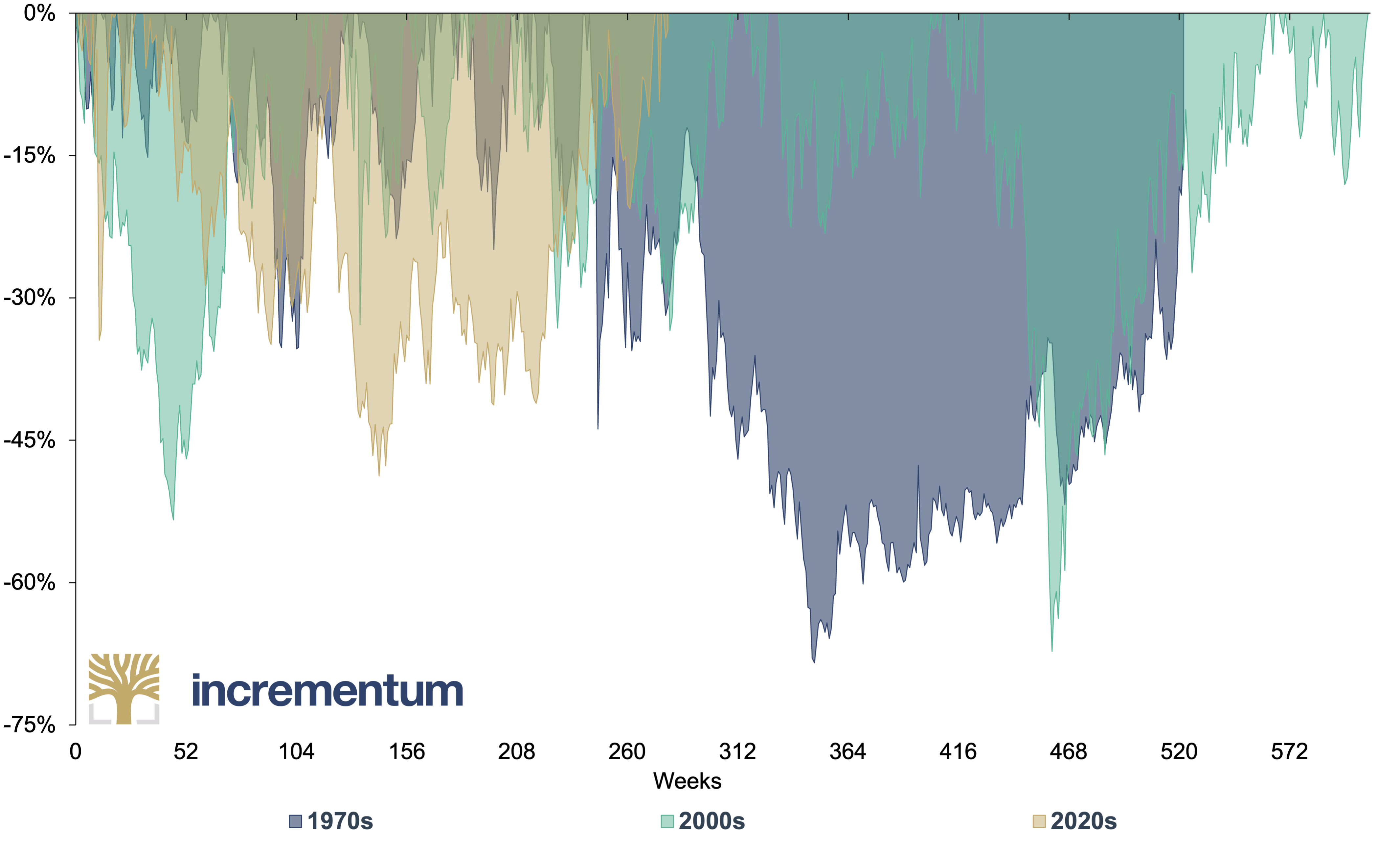

In the case of performance gold, such as silver or mining shares, corrections are usually even more pronounced, as the following chart shows. Consistent risk management is therefore essential.[4]

Gold Mining Stocks* Drawdown Comparison During Bull Markets, in USD, 12/1969–04/2025

Source: LSEG, Nick Laird, Incrementum AG

*BGMI 12/1969–05/1996, HUI 05/1996–

The Trump Shock: The Economic and Political Realignment of the US

Within a few weeks, Donald Trump has created a bear market in credibility and trust. With Trump’s return to the White House, a profound realignment of the US and thus the global economy, and possibly even the global (monetary) order, has been initiated. Even if the consequences of Trump’s many, sometimes seemingly chaotic measures are not entirely foreseeable, they significantly contribute to a positive environment for gold and The Big Long.

Trump’s intention to fundamentally reform the US economy is of imminent importance for the global economy. The sweeping election victory, with majorities in the Senate and House of Representatives and a Republican-dominated Supreme Court, gives Trump enormous political power. Despite all the difficulties in interpreting his strategy, three fundamental trends can be identified that are to be halted or reversed:

- the steadily increasing government overindebtedness

- the chronic trade deficits and the associated de-industrialization of the US

- the threat to the reserve currency status of the US dollar posed by de-dollarization

Deficits, DOGE & detox: The US on an austerity course?

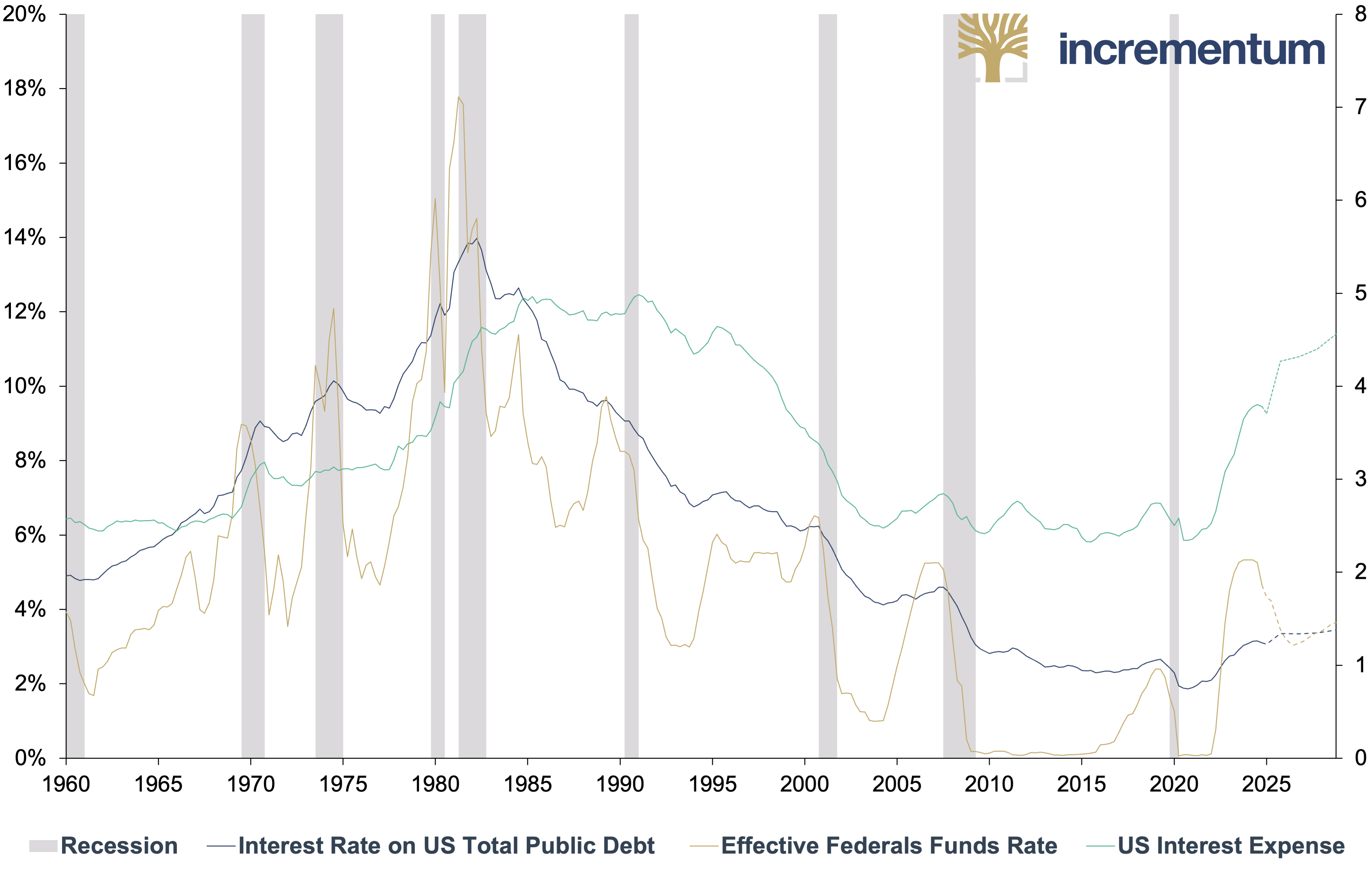

The self-proclaimed king of debt has – at least verbally – abdicated. The stability-threatening dynamics of government debt, which we have regularly highlighted in previous In Gold We Trust reports, have entered the mainstream and are now the focus of the Trump administration. Few things illustrate this debt situation better than that, at over USD 1trn a year, the US now has to pay more interest on its national debt than it spends on its generous defense budget.

Interest Rate on US Total Public Debt and Effective Federals Funds Rate (lhs), and US Interest Expense (rhs), as % of US GDP, Q1/1960–Q4/2028e

Source: CBO, Federal Reserve St. Louis, LSEG, Incrementum AG

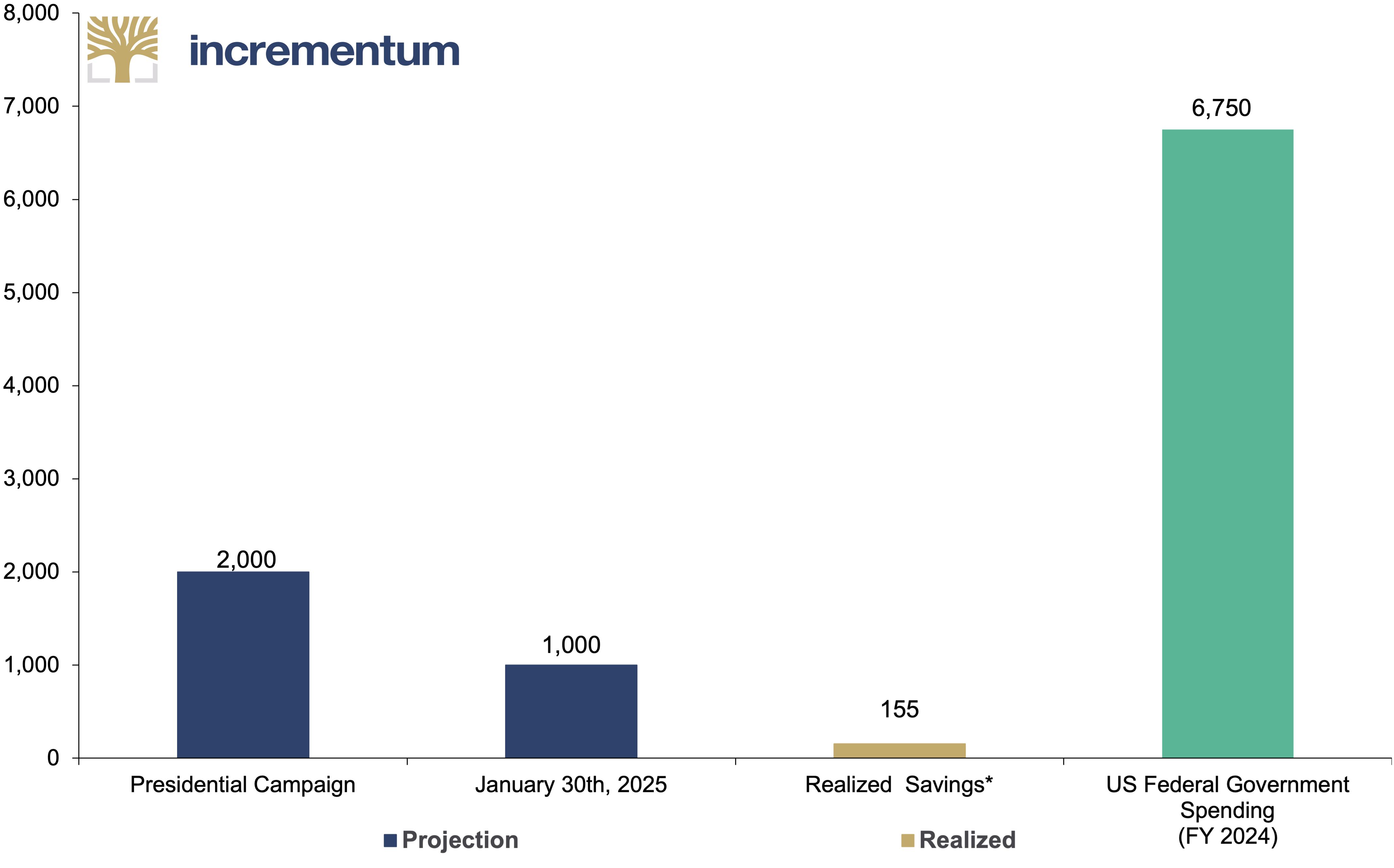

Part of the attempt to get a grip on overindebtedness is identifying bureaucratic inefficiencies. DOGE initially hoped to achieve annual savings of USD 1trn, corresponding to around 15% of Washington’s expenditure. This would roughly halve the deficit and bring it almost below the 3% target set out in the 3-3-3 plan. Musk has recently rowed back considerably and now mentions a savings potential of USD 155bn. It currently seems doubtful that DOGE activities will stop the spiral of overindebtedness in the long term.

Forecasted & Realized DOGE Savings and US Federal Government Spending, in USD bn

Source: The New York Times, DOGE, Incrementum AG

*Data as of 04/30/2025

There are indications that Trump and his team are willing to send the US economy into a detox recession. Conceptually, the idea is reminiscent of the teachings of the Austrian School, whose advocates emphasize that real value is created in the private sector. Shrinking the bloated state apparatus is intended to free up resources for entrepreneurship, comparable to a fasting process in which the organism is purged to become more resilient and efficient in the long term.

But as with fasting, detoxes are rarely pleasant. Pain, dizziness, psychological irritation, and ravenous appetite are all part of it, as is the temptation to break off the program early. The crucial question is: Will the government stick to the detox course – or will it revert to the sweet poison of debt-financed spending at the first sign of a marked economic downturn, severe market turbulence, or the threat of election defeats?

According to GDPNow, the detox recession is already taking hold in the US. Even if high import figures distort the GDP figures due to strong gold imports on the one hand and early imports in the run-up to Liberation Day on the other, the indicator adjusted for special effects has now slipped into the red. As negative as a recession is, the gold price tends to receive a tailwind from a recession in the US, as our analyses have shown in recent years.[5]

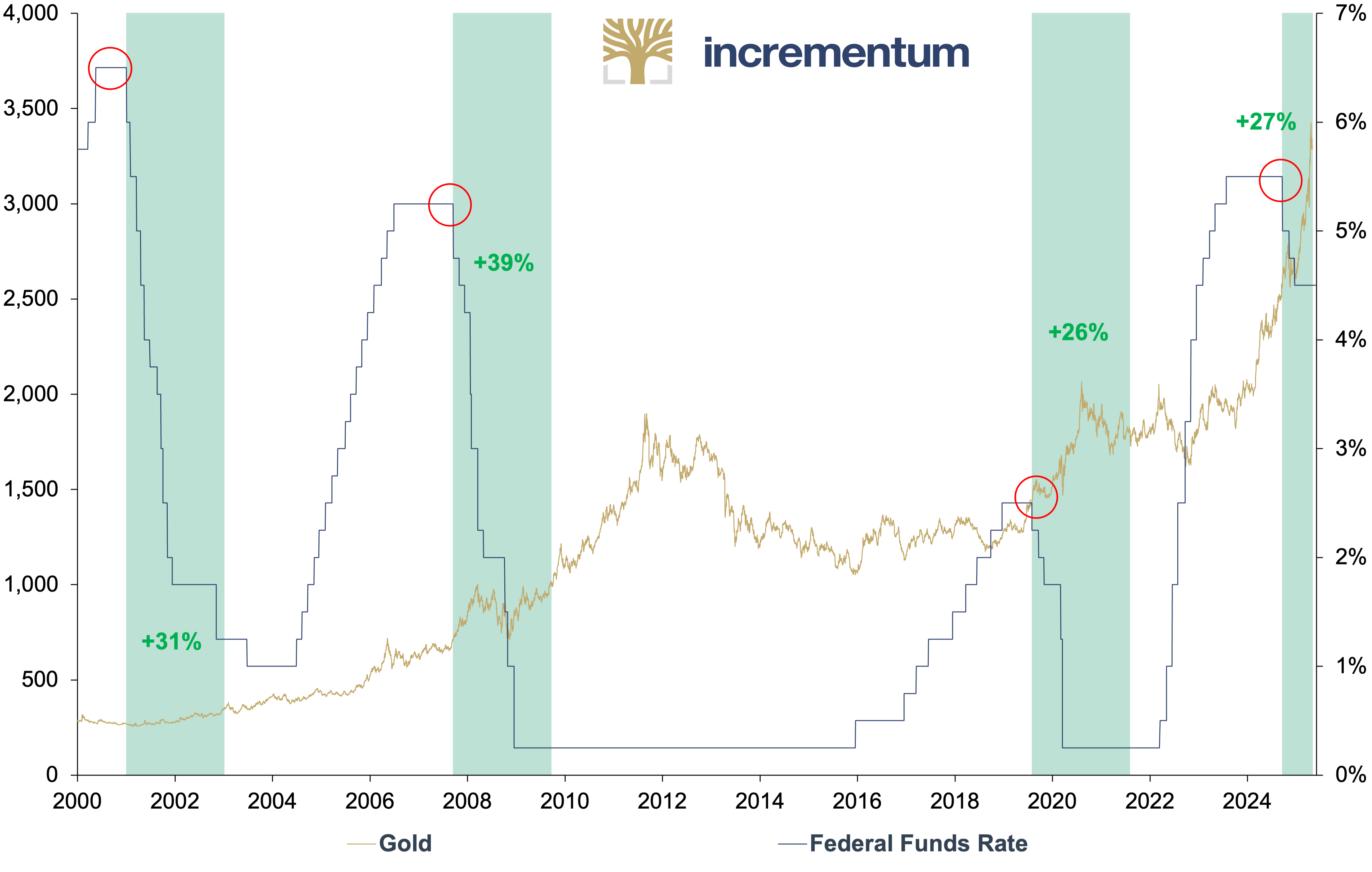

If this trend continues, the pressure on the Federal Reserve to loosen monetary policy more aggressively will increase considerably. We therefore expect interest rate cuts beyond what is currently priced in. The following chart shows that in the 24 months following the first interest rate cut, the gold price generally experienced a strong tailwind. Interest rate cuts in quick succession or significant interest rate hikes of 50 basis points or more benefit the gold price.

Gold, in USD (lhs), and Federal Funds Rate (rhs), 01/2000–04/2025

Source: LSEG, Incrementum AG

To reduce the debt burden, the US would like to use unconventional methods in addition to operational savings. Possible playbooks have been formulated by the two thought leaders, Zoltan Pozsar[6] and Stephen Miran. The latter has explained in “A User’s Guide to Restructuring the Global Trading System” how allies of the US should be persuaded to subscribe to ultra-long-term bonds with a maturity of 50 or even 100 years, while the Federal Reserve provides USD swap lines to secure liquidity in the eurodollar system.[7],[8]

In addition, duty-free access to the US market and protection by US military power would become dependent on the willingness to guarantee Washington’s long-term financing needs. The result? An acceleration of dollarization, combined with the integration of other countries into the US geopolitical sphere of power.

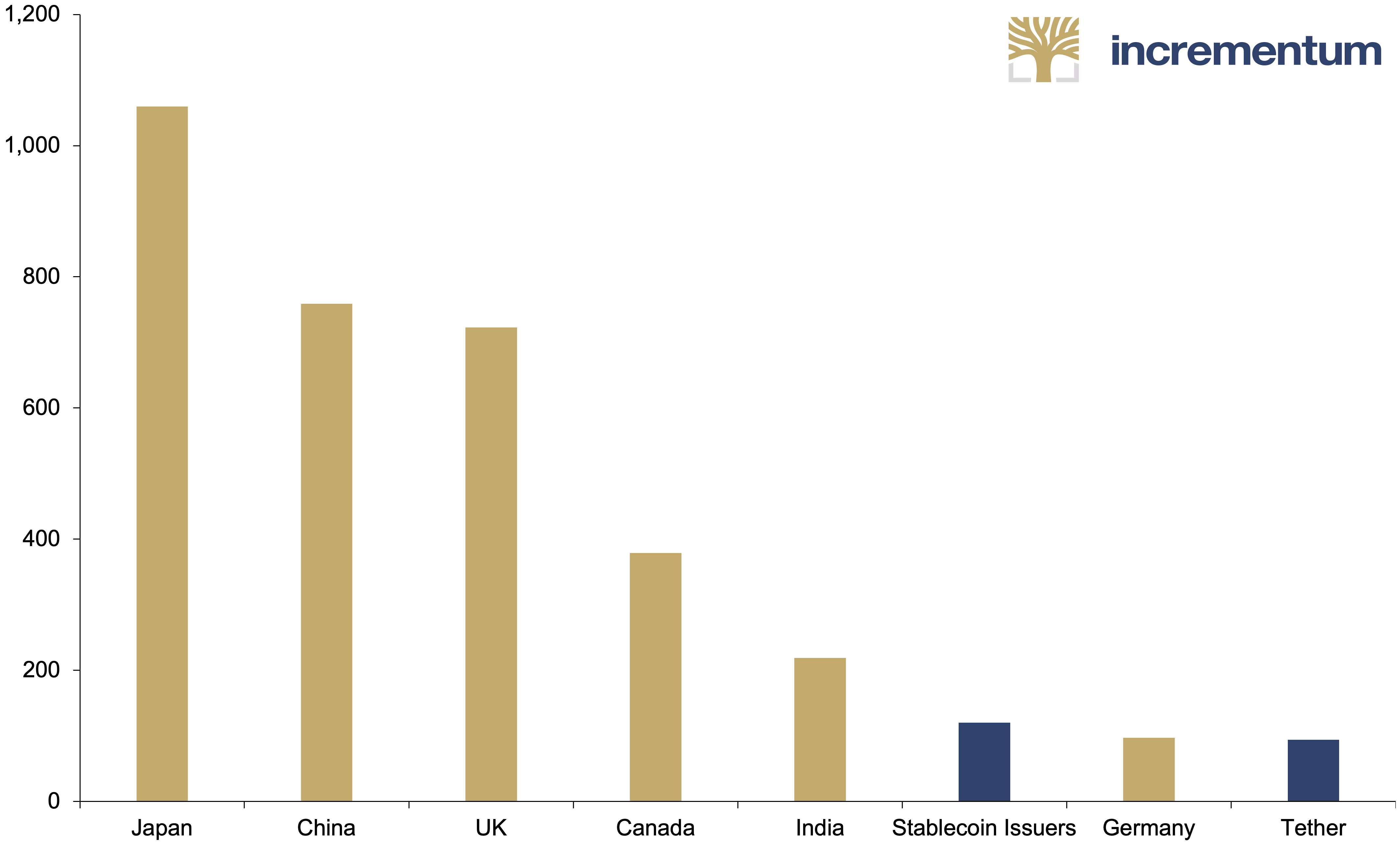

The Trump administration has also positioned itself against introducing a central bank digital currency (CBDC). Executive Order 14178 stopped any government initiative establishing a central bank digital currency in the US. Instead, the government promotes private-sector innovations in digital financial technology, above all US-dollar-based stablecoins.

This strategy is not only ideologically based but also follows a financial strategy: Stablecoin issuers such as Tether and Circle are now among the largest buyers of US government bonds. In total, stablecoin issuers have over USD 120 billion in US Treasuries on their books, and the trend is rising sharply.

Major Holders of Treasury Securities, 12/2024

Source: U.S. Department of the Treasury, Incrementum AG

Industrial policy through trade policy: The return of the US as an industrial location?

Another element of the economic realignment is the reform of trade relations. For President Trump, the high structural current account deficit is evidence of the US being exploited by the rest of the world. He staged Liberation Day on April 2, when the US’s new tariff policy was announced. According to initial calculations, the average US tariff reached almost 30%, significantly higher than in the interwar period at just under 20% due to the Smoot-Hawley Tariff Act.

The global response at that time was a wave of retaliatory tariffs, which crippled international trade and deepened the crisis triggered by the 1929 stock market crash. Between 1929 and 1933, US imports plummeted by 66% and exports by 61%, demonstrating how protectionism can magnify economic collapse. Today, the risks are even greater: Global supply chains are exponentially more integrated, rendering tariffs far more damaging than protective. Modern manufacturing relies on cross-border flows of components, machinery, and semi-finished goods, meaning trade barriers now undermine the very industries they aim to shield. In the US, for example, over two-thirds of manufacturing firms depend on imports, leaving them exposed to cost surges and supply chain disruptions when tariffs strike. Unlike the 1930s, today’s interconnected economy means protectionist measures don’t just distort trade—they risk cascading failures across production networks worldwide.

The trade conflict with China escalated sharply in the meantime, but in mid-May tensions eased, with a 90-day reduction in tariffs while further negotiations continue. A 90-day “ceasefire” with a base tariff of 10% has been in place for some time with other countries, which is also to be used for negotiations. Whether dozens of trade agreements can be negotiated in 90 days is unlikely, given the average negotiation period of 18 months for trade agreements to date.

OECD data shows that the United States is about three times more dependent on Chinese inputs than China is on American ones, a fitting fact considering that China’s manufacturing base is also three times larger. Against this backdrop, it appears that China holds the better cards in this conflict.

All these measures will harm US GDP growth in the short and medium term. President Trump hopes that these initiatives will accelerate the reindustrialization of the US. A devaluation of the US dollar should make a significant contribution to this. At the same time, however, the US dollar’s position as the undisputed global reserve, trading and reserve currency is to be secured. Trump has repeatedly threatened countries that want to replace the US dollar as a trading currency with drastic tariffs of 100%.

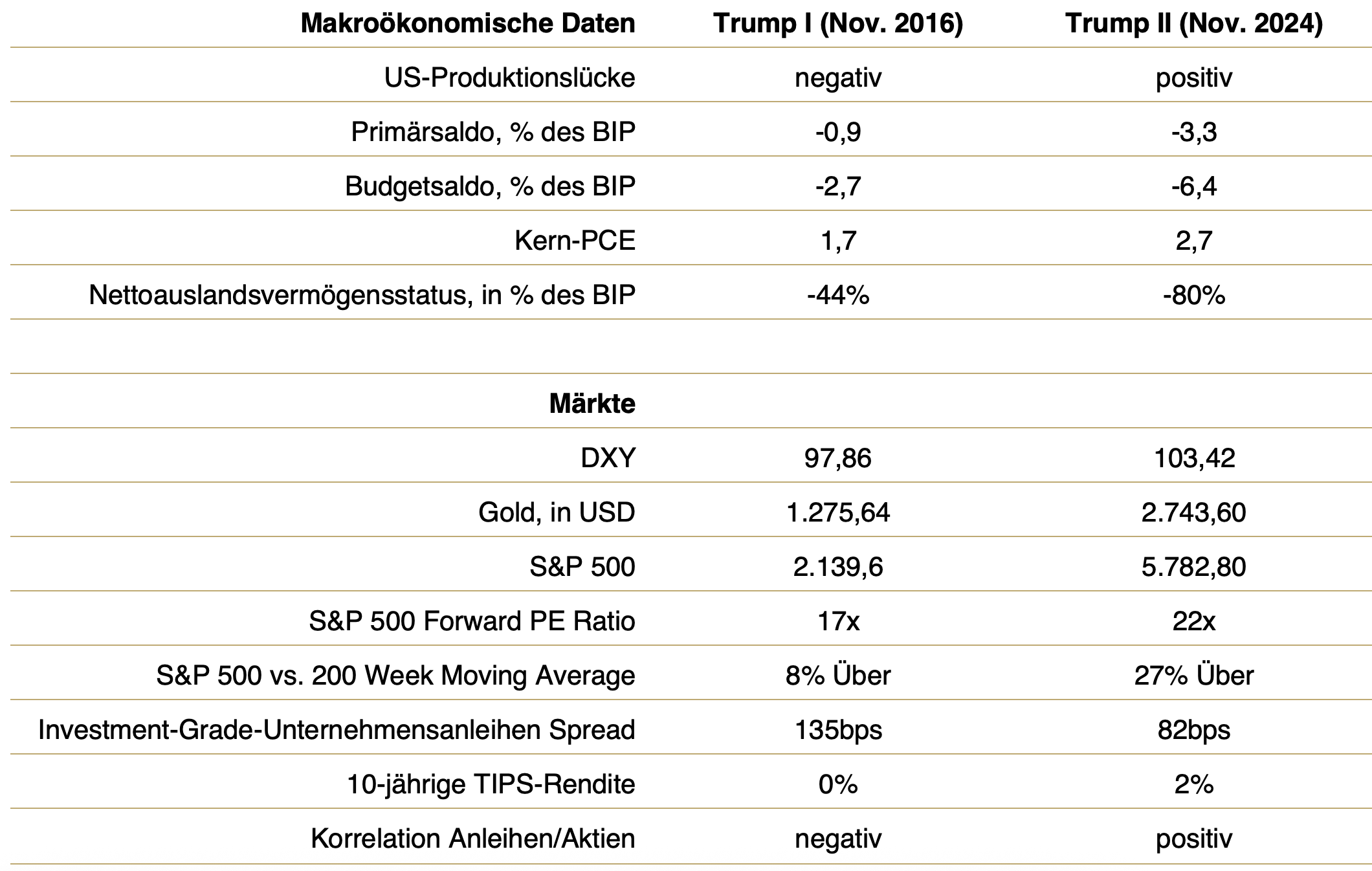

This combination of a weak US dollar and retention of reserve currency status sounds like the proverbial wish for “warm ice lollies”, or like squaring the circle. However, the economic omens at the time of his second victory in the presidential election were significantly worse for Donald Trump than they had been when he first won.

US Macro and Market Environment at the Start of Trump I vs. Trump II

Source: Ruffer, LSEG, Incrementum AG

Re-dollarization or de-dollarization?

As far as plans for the future significance of the US dollar are concerned, much is still uncertain. Based on the two currency agreements in the 1980s,[9] the plan to significantly devalue the US dollar against other leading currencies is circulating under the term Mar-a-Lago Accord. Trump and his team are of the – economically debatable – opinion that the overvalued US dollar is a major reason for the deindustrialization of the US.

At the heart of this discussion is a structural dilemma. In the 1960s, economist Robert Triffin, who worked at the Federal Reserve and the International Monetary Fund (IMF), noted that a nation issuing a global reserve currency faces a conflict of objectives between its short-term national interests and long-term international objectives. The following two characteristics of an ideal reserve currency are therefore incompatible and form the Triffin dilemma:

- Stability: A currency is only stable if the issuer has a balanced current account.

- Sufficient international supply of the reserve currency: In order to meet the international demand for the reserve currency, the issuing nation must have a current account deficit.

In the long term, the reserve currency status is both a blessing and a curse – a blessing because it allows the US to consume more than it produces and to export monetary inflation abroad.

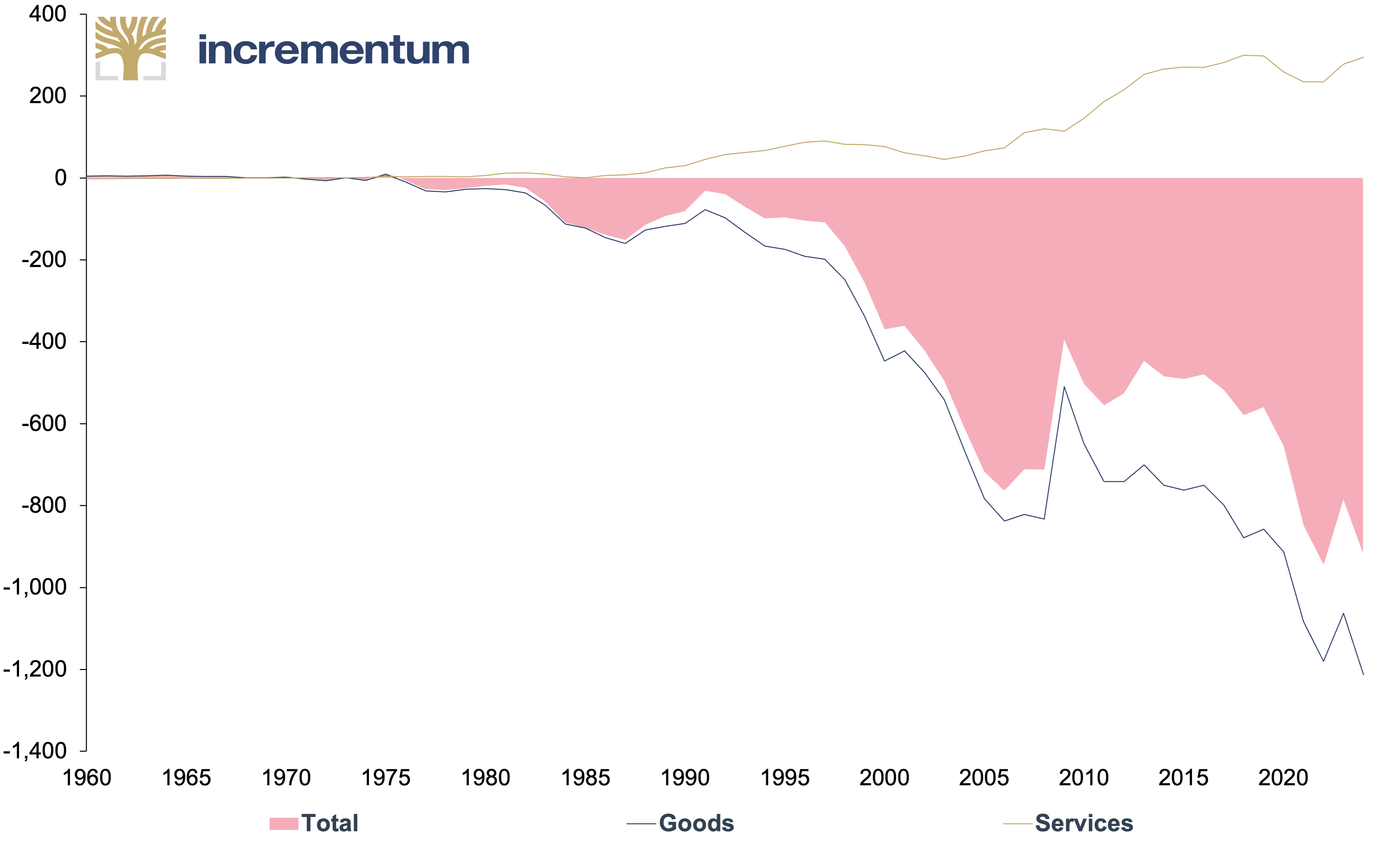

US Current Account, in USD bn, 1960–2024

Source: Bureau of Economic Analysis, Incrementum AG

This status is a curse because a permanent current account deficit encourages deindustrialization and undermines confidence in the reserve currency in the long term. The global financial system demands more and more US dollar liquidity, while at the same time, the basis for its stability is eroding.

What options are there for solving the Triffin dilemma?

- Multipolar reserve system (euro, yuan, etc.): This approach does not solve the paradox but distributes the pressure across several currencies. Furthermore, it would be necessary for several countries to have chronic current account deficits to avoid an appreciation of their currencies.

- Supranational reserve currency (special drawing rights): John M. Keynes already proposed this during the reorganization of the global monetary order at the end of World War 2, under the name bancor. This approach makes the supply of international liquidity independent of the country’s current account deficit with the world’s reserve currency. Its implementation requires close global cooperation.

- Neutral reserve asset: The paradox can only be resolved sustainably by using neutral reserve assets such as gold or Bitcoin. It is crucial that the assets are non-inflationary, have no counterparty risk, and exhibit corresponding market depth. This currently only applies to gold.

We must emphasize that the debate surrounding the Triffin dilemma is highly controversial. Skeptics argue that a current account deficit is not necessarily negative, as it can also signify high foreign confidence in the domestic location. Eugen von Böhm-Bawerk once even emphasized that the capital account commands the current account. A high current account deficit would therefore result from strong capital inflows and evidence of the attractiveness of a jurisdiction.

There are also objections to the thesis that a country that issues the world’s reserve currency must necessarily have a current account deficit. The issuer of the world reserve currency is not dependent on using the additional money supply put into circulation primarily to import goods; instead, foreign securities could just as easily be purchased, or its currency could be significantly revalued. In the former D-Mark bloc, the currency’s strength was seen as a prerequisite for economic success because it continuously “forced” productivity increases and innovations to compensate for the impending loss of competitiveness due to revaluations.

Classical-liberal economic critics of Trump’s tariff policy argue that the massively increased budget deficit is the real cause of the economic imbalances. Tariffs are merely a way of combating symptoms, with potentially serious adverse side effects. There seems to be a consensus that there are structural distortions, which raises the question of resetting the global monetary order.[10]

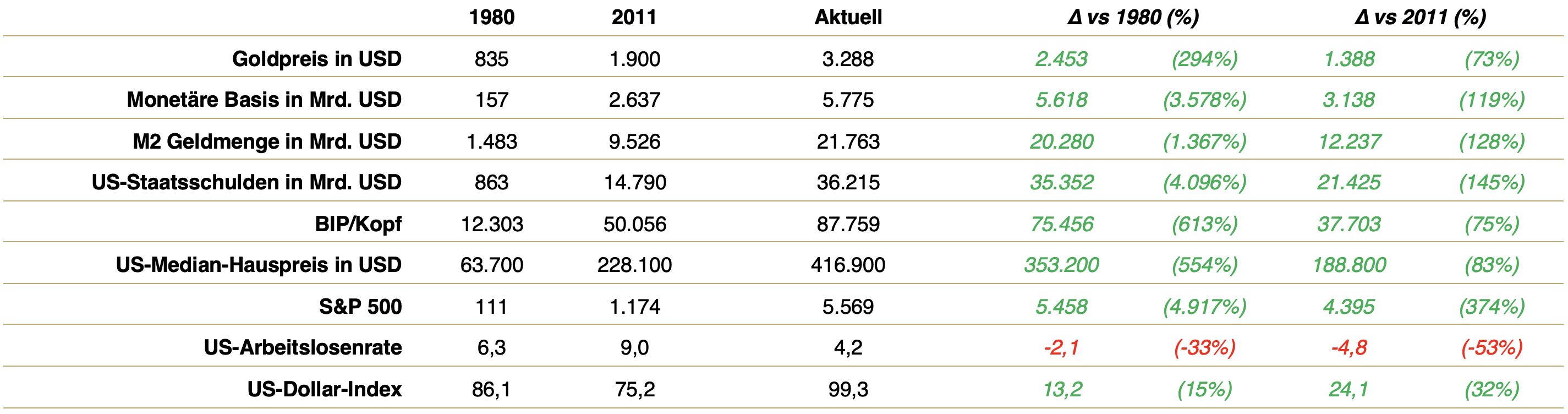

A further, possibly even rapid devaluation of the US dollar could initiate the next push in this gold bull market. A comparison of various key figures at the time of the last two secular all-time highs in 1980 and 2011 with the current situation confirms our Big Long thesis: The gold price still has room to rise. The currently notably higher US Dollar Index seems particularly important to us – at around 99.3 points, it is well above the values during gold’s last secular highs.

Comparison of various Macro- and Market Key Figures at Gold ATH in 1980, 2011 and Current

Source: treasury.gov, Federal Reserve St. Louis, LSEG (as of 04/30/2024), Incrementum AG

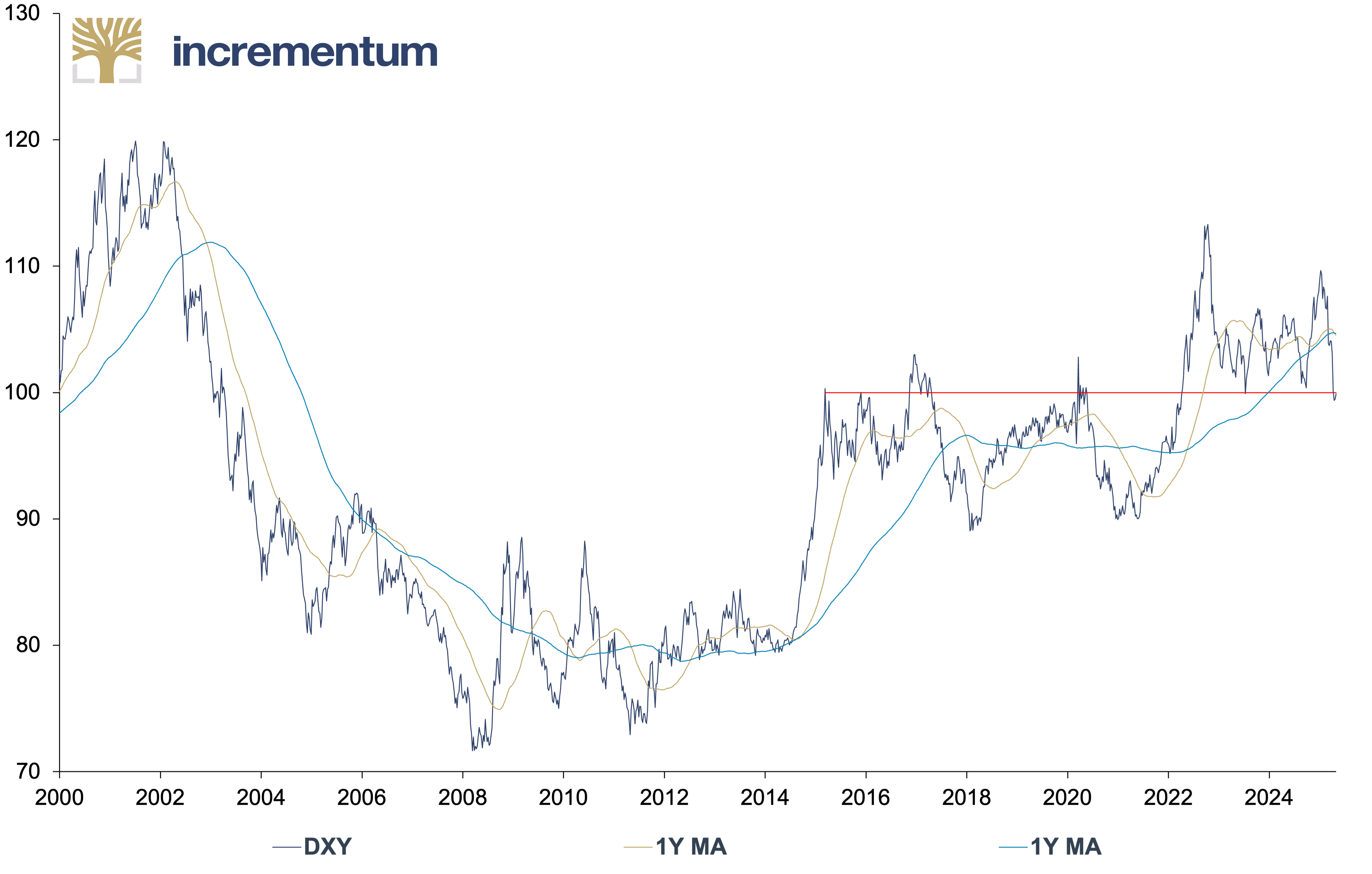

One thing is sure to us: A controlled and significant devaluation of the US dollar is one of Donald Trump’s central concerns. However, artificially weakening the US dollar to promote reindustrialization would be a grave mistake. Currency devaluations do not solve structural problems. They generate inflation, make imports more expensive, reduce the purchasing power of wages and savings, which are the backbone of the US economy.

In addition, a strong currency is an expression of international trustworthiness. Those who deliberately devalue the US dollar are scaring away capital urgently needed to modernize infrastructure and production capacities, as well as to secure technological leadership. Instead of relying on the deceptive advantages of a weaker US dollar, US economic policy should focus on fiscal discipline, a streamlined bureaucracy, and targeted promotion of innovation to attract new industries and strengthen existing ones – without devaluing the assets of citizens, including foreign citizens who hold bonds denominated in US dollars, and without gambling away prosperity in a devaluation race. To put it bluntly, if a soft-currency policy were the key to economic success, Zimbabwe would top the list of the most successful countries, not Switzerland.

DXY, 01/2000–04/2025

Source: LSEG, Incrementum AG

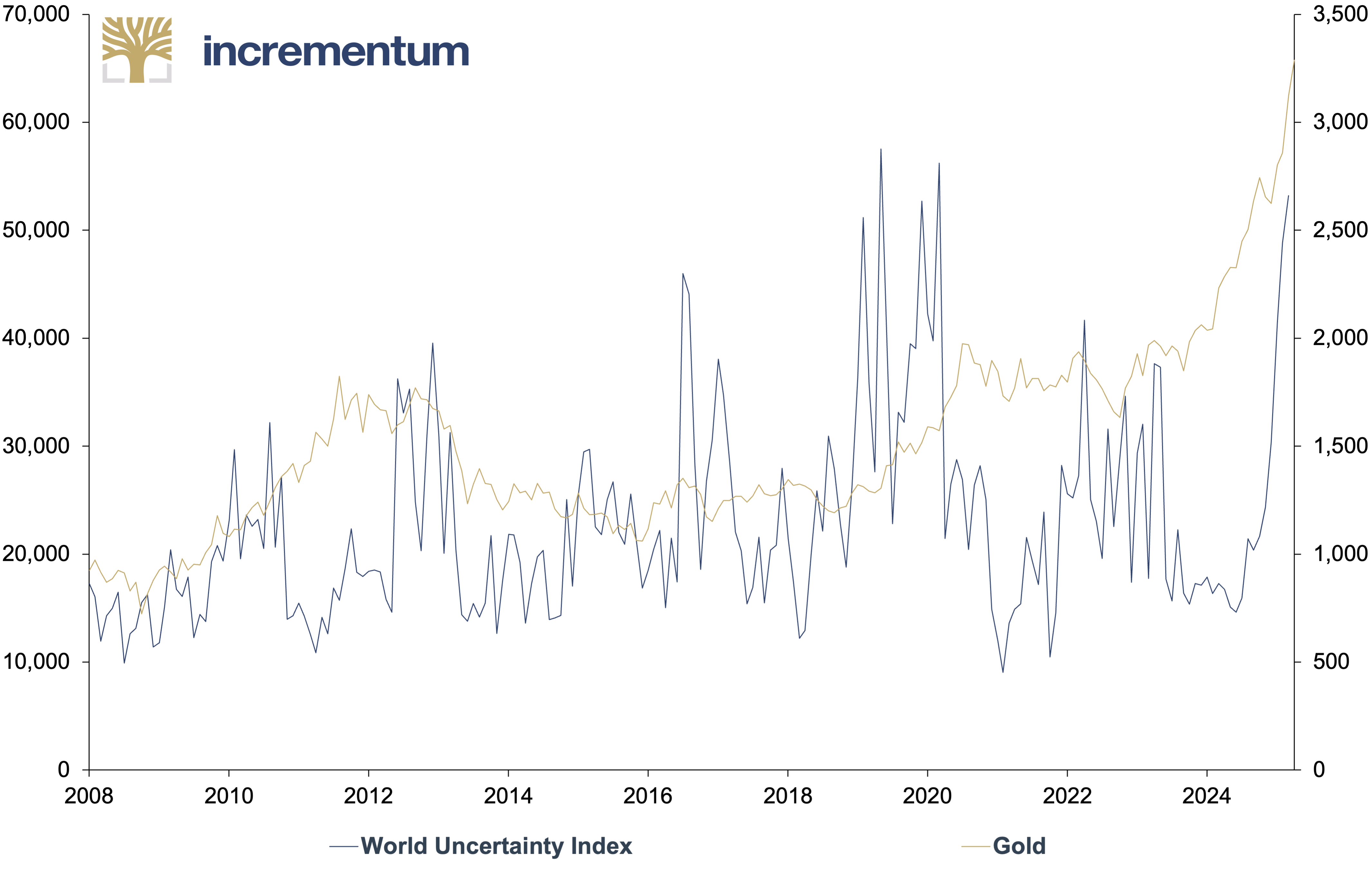

These developments – from the unclear direction of the US dollar strategy to the unresolved Triffin paradox and possible currency devaluations – are causing considerable uncertainty. This is another parallel to the Nixon shock of 1971, when an existing global monetary system became history from one moment to the next and it took years for the new system of flexible exchange rates to establish itself. Trust is the central currency in (international) economic transactions and is decisive for the success of a country’s location policy. The costs of an erosion of confidence cannot be overestimated.[11] In spring 2025, gold proved itself – once again – to be a reliable hedge against geopolitical and economic upheaval. Gold remains what it has always been: a stable anchor.

World Uncertainty Index (lhs), and Gold (rhs), in USD, 01/2008–04/2025

Source: LSEG, Incrementum AG

Especially as traditional safe havens such as US or German government bonds lose trust and dilute their stability function, gold is now moving back into the center of long-term investment strategies.

Meanwhile in Europe: Monetary Climate Change Is Accelerating

While unfamiliar words of fiscal common sense can be heard from Washington, Friedrich Merz (CDU), Germany’s new chancellor, has made a 180-degree turnaround under the magic formula “Whatever it takes!” in what many see as a voter deception. Merz has proposed that defense spending above 1% of GDP be exempt from the fiscal brake debt rule. In addition, a debt-financed program – euphemistically referred to as “special assets” – amounting to EUR 500bn is to be created for infrastructure and climate protection. Forecasts assume that German national debt will rise from 60% of GDP to 90%.

This marks a historic moment for Germany: Under the leadership of the conservative CDU/CSU, the official renunciation of fiscal conservatism has now been completed. What had already been foreshadowed in the wake of the Covid-19 pandemic – and which we described as monetary climate change in the 2021 In Gold We Trust report – has now reached a new level. With Germany breaking away from its role as a model of fiscal discipline, it is likely that the euro countries with a greater propensity to spend – we are looking in particular at Paris – will interpret the new fiscal generosity as a free pass.

German government bonds, which are considered the ultimate “risk-free investment” in the eurozone, reacted noticeably to the turnaround. The yields on Bunds recorded their largest daily movement in 35 years following the announcement. A problem for many countries with significantly higher debt levels, such as France and Italy, is that their bond yields have also risen substantially.

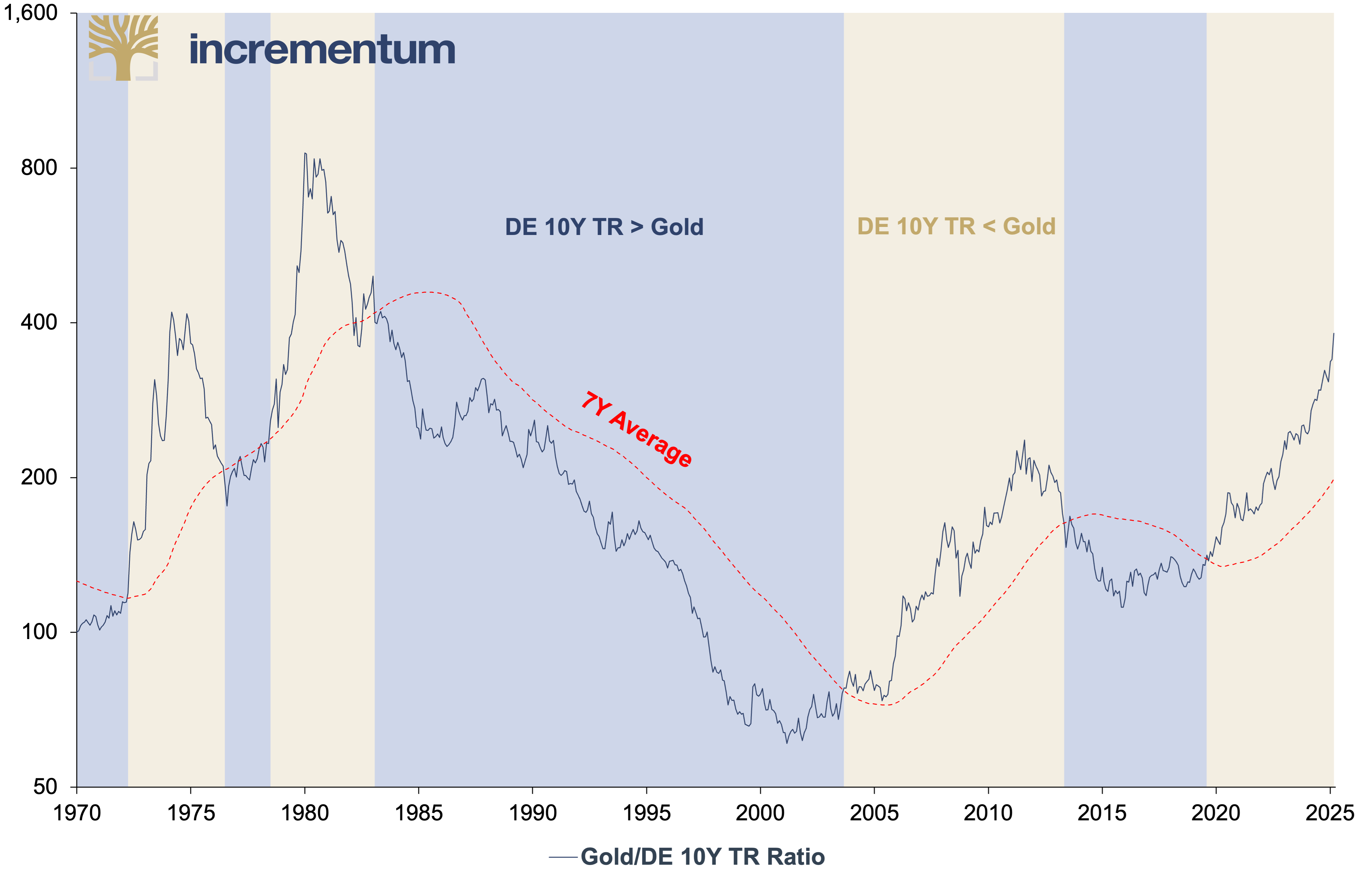

For more than half a century, international market participants were certain that German Bunds had de facto no counterparty risk. Especially during the Great Moderation, Bunds outperformed gold. This ratio began to change gradually in 2002. Since 2020, the trend has strengthened in favor of gold. In addition to the existing risk of a renewed wave of inflation, another issue is coming to the fore with the demise of the Swabian housewife: counterparty risk. In the medium term, this could – for the first time in a long time – once again be perceived as a risk factor in government bond valuations.

Gold/DE 10Y TR Ratio, 01/1970–04/2025

Source: Gavekal Research, LSEG, Incrementum AG

Louis-Vincent Gave argues that German and US government bonds have been the all-star asset class for a generation, but their golden era appears to be coming to an end. Many portfolios now find themselves in a situation akin to the French national football team after the retirement of Zinedine Zidane—missing a central figure to build around. A new difference-maker is needed. Gold, already warming up on the sidelines, could be ready to step into that role, much like a young Kylian Mbappé, poised to take the field and change the game.

The New Gold Playbook – Bolstered by the Trump Shock

Our central thesis in the In Gold We Trust report 2024, “The New Gold Playbook”, was that the investment environment for gold has fundamentally changed. Developments over the past 12 months confirm this change.

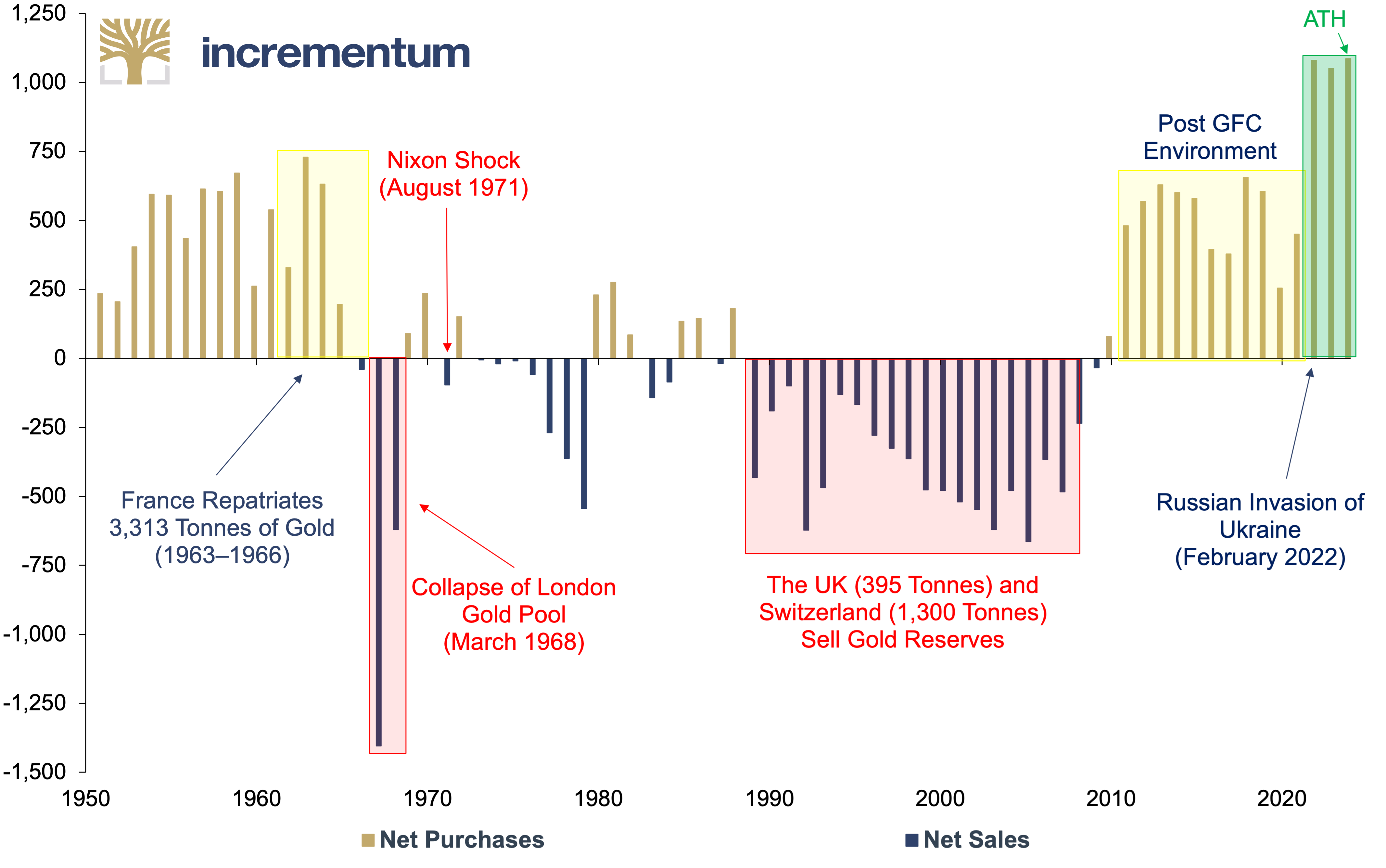

A key cornerstone of The Big Long is the strong physical demand from central banks. They have been net buyers on the gold market since 2009. This trend has accelerated significantly since the confiscation of Russian currency reserves at the end of February 2022. For three years in a row, central banks increased their gold reserves by more than 1,000 t each year, achieving a special kind of hat-trick.

Global Central Bank Gold Purchases, in Tonnes, 1950–2024

Source: World Gold Council, Incrementum AG

Asian central banks again made the lion’s share of these purchases. It is worth noting, however, that Poland took the top spot in 2024. This geopolitically motivated reallocation towards gold exemplifies a growing mistrust of the existing Western financial system and the gradual increase in the economic importance of the emerging markets.

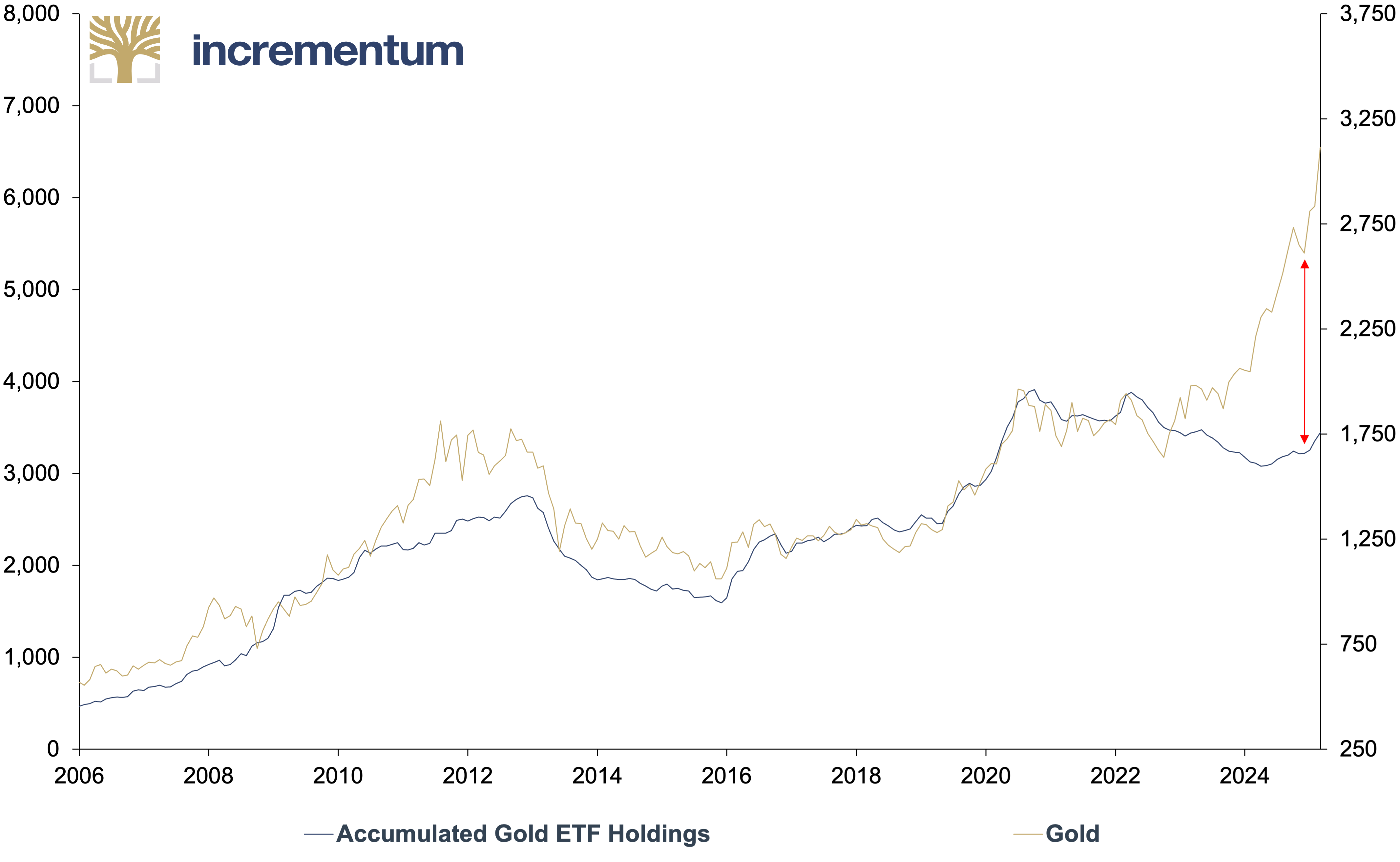

And it is no longer just central banks that are backing gold, but also Western financial investors, who are increasingly seeking investment opportunities in the precious metals sector after a prolonged period of inactivity. In 2024, ETF demand picked up over the year, except for Europe, which only returned to the buying side in Q1/2025. The strong inflows in North America show the first signs of a gold FOMO. Investment demand from gold ETFs could be a key driver for the continuation of the gold bull market.

Accumulated Gold ETF Holdings (lhs), in Tonnes, and Gold (rhs), in USD, 01/2006–03/2025

Source: World Gold Council, Incrementum AG

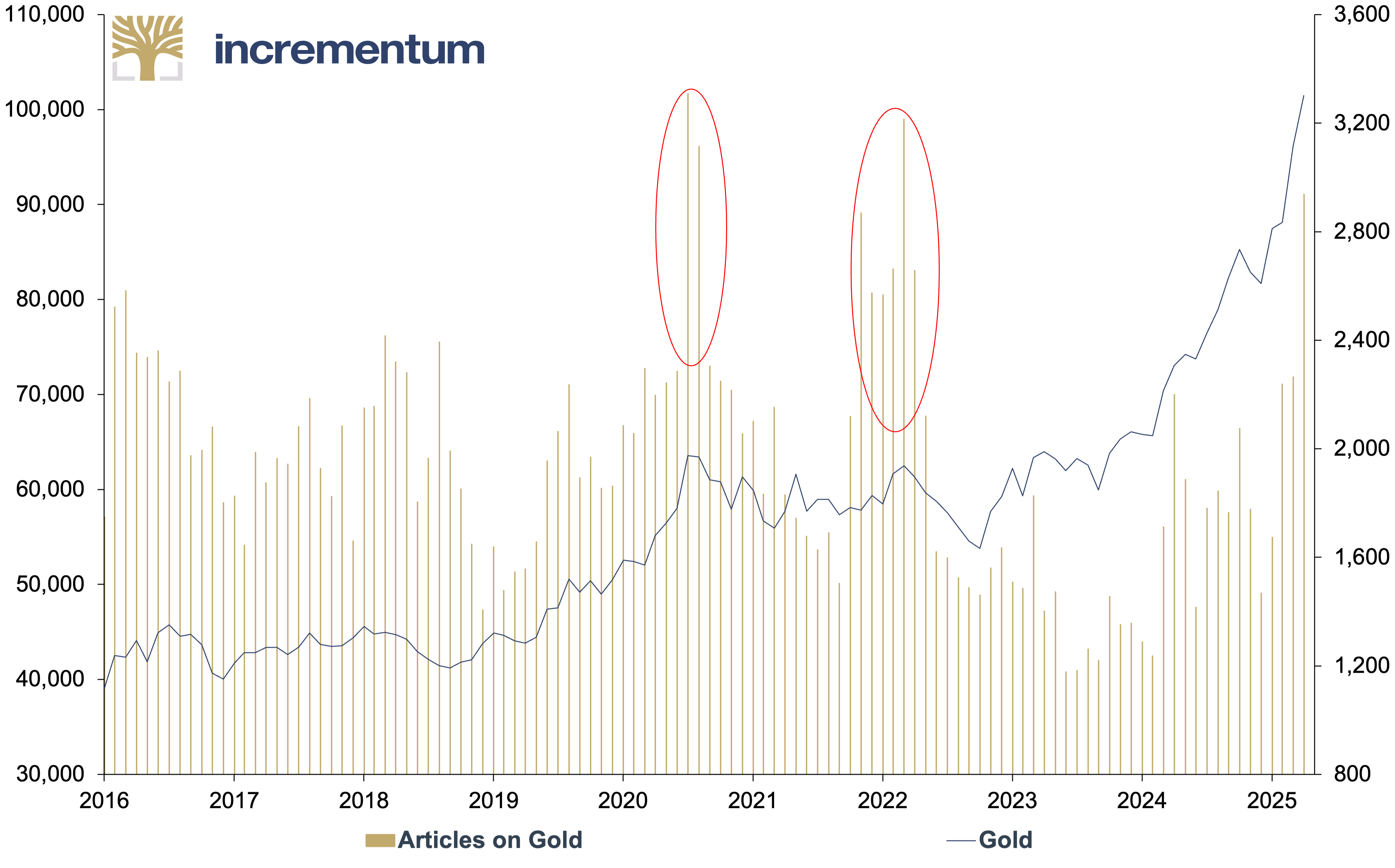

The general media enthusiasm for gold in the West is not as pronounced today as it was in 2020, for example, when gold reached its first new all-time high in nearly a decade. This suggests that, despite the record run in the past few quarters, the gold market is not yet in an overly euphoric state.

Articles on Gold (lhs), and Gold (rhs), in USD, 01/2016–04/2025

Source: World Gold Council, Bloomberg, LSEG, Incrementum AG

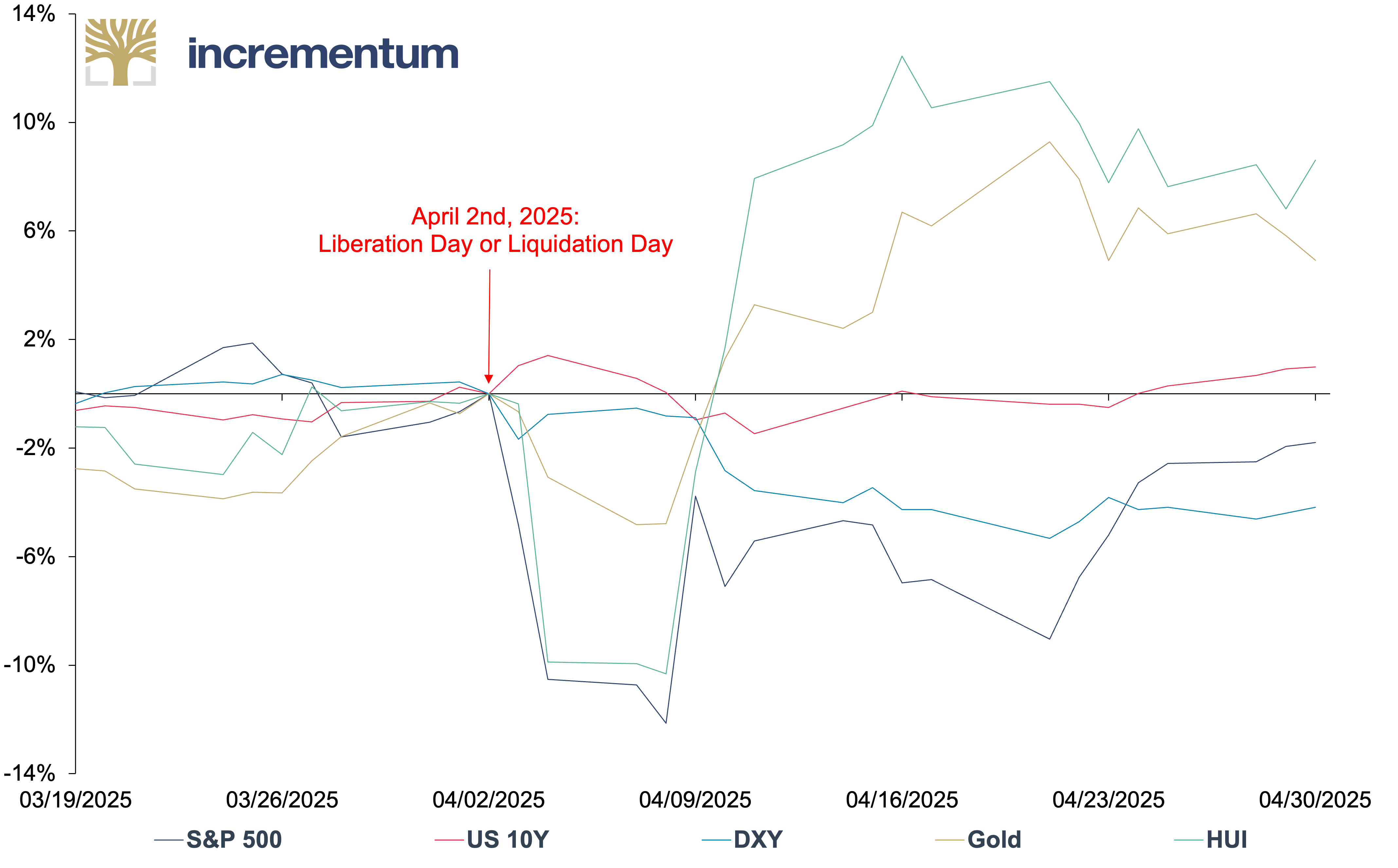

Our Big Long thesis receives additional support from the capital market reactions after Liberation Day. It is unusual for the US dollar to fall during a volatile risk-off phase. Even rarer is a simultaneous slump in bonds and equities. Such constellations are typical for emerging markets, but not for the most important haven of the global capital market. Instead of finding refuge in the safe haven, many investors, especially international investors, have fled. How likely is it that they will return voluntarily after such a shock?

Various Assets, in USD, 100 = 04/02/2024, 03/2025–04/2025

Source: LSEG, Incrementum AG

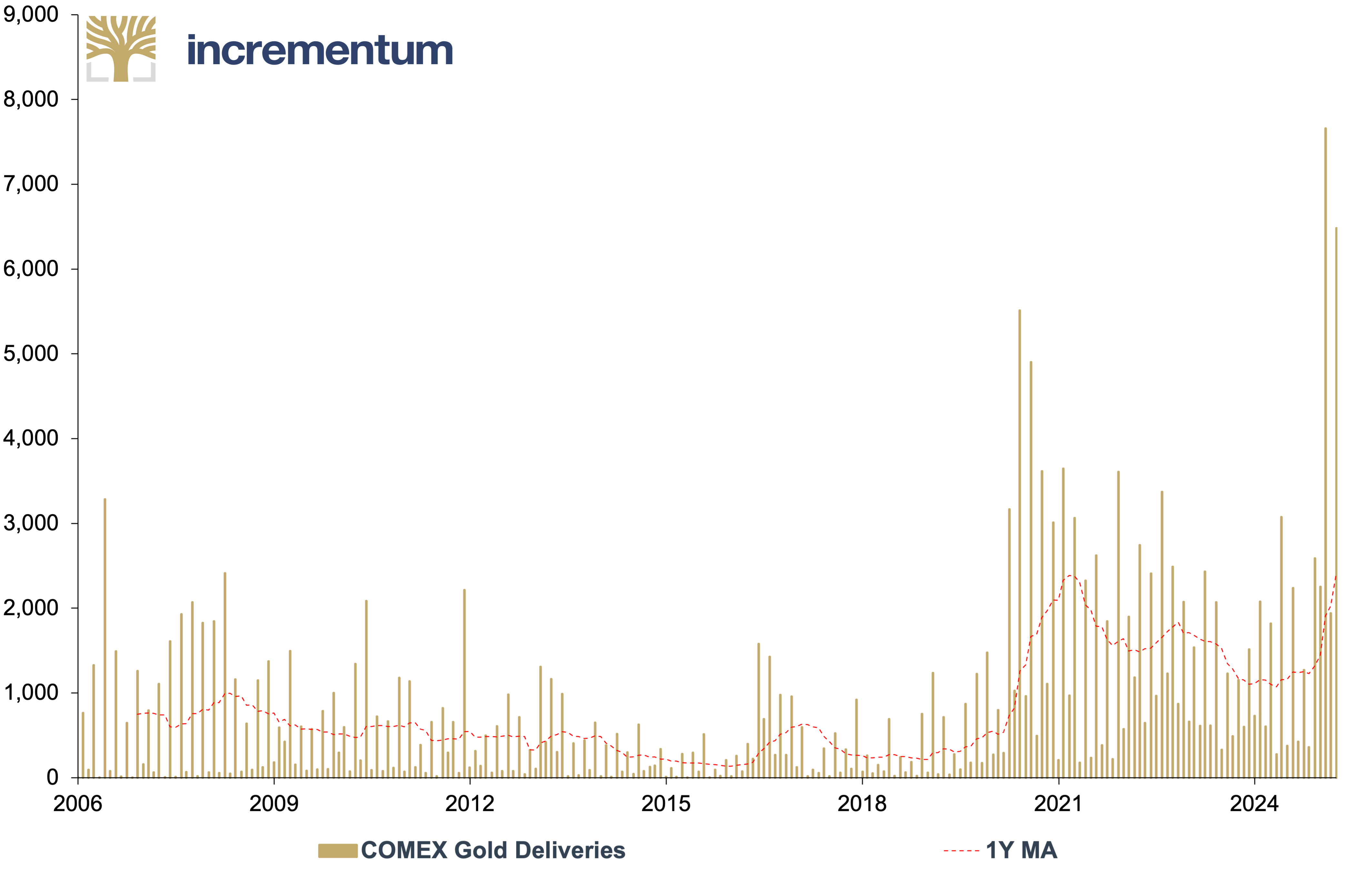

Let’s get physical: safe-haven gold on the way from London to New York

Another clear sign of waning confidence is the rising demand for physical gold, especially among long-term investors looking for safe-haven gold. Physical deliveries from futures exchanges have increased since 2020, presumably driven by family offices, wealthy private investors, and state actors. These buyers are less price-critical than system-critical: They prefer real physical gold over “paper gold”.

COMEX Gold Deliveries, in Thousands of Troy Ounces, 01/2006–04/2025

Source: LSEG, Incrementum AG

Before Liberation Day, huge quantities of gold were transferred from London to New York, amounting to over 2,000 tons, according to Philip Smith, CEO of StoneX. This was triggered by an unusually high premium of up to USD 68 between the COMEX price and the LBMA spot price. This forced bullion banks to make extraordinary physical deliveries. At the same time, LBMA gold inventories shrank by 8.6 million ounces (Moz) between October 2024 and the end of March, while COMEX inventories reached a new record high of 45 Moz at the beginning of April.

Gold, the New Outperformer in the Portfolio?

The relative strength of gold against bonds – and now also against stocks – is likely to attract increased investor interest. Now that gold has recently gained strength against equities, it is worth examining the long-term trend of the Dow/gold ratio. In the past three major downward trends in this ratio in the 1930s, 1970s and 2000s, this development was always accompanied by a significant rise in the price of gold and stagnating US stock markets. The Dow/gold ratio currently stands at 11.91 and is therefore clearly above the historical median of 7.09, indicating that gold is still attractively valued compared to US equities.

Dow/Gold Ratio, 01/1900–04/2025

Source: Nick Laird, LSEG, Incrementum AG

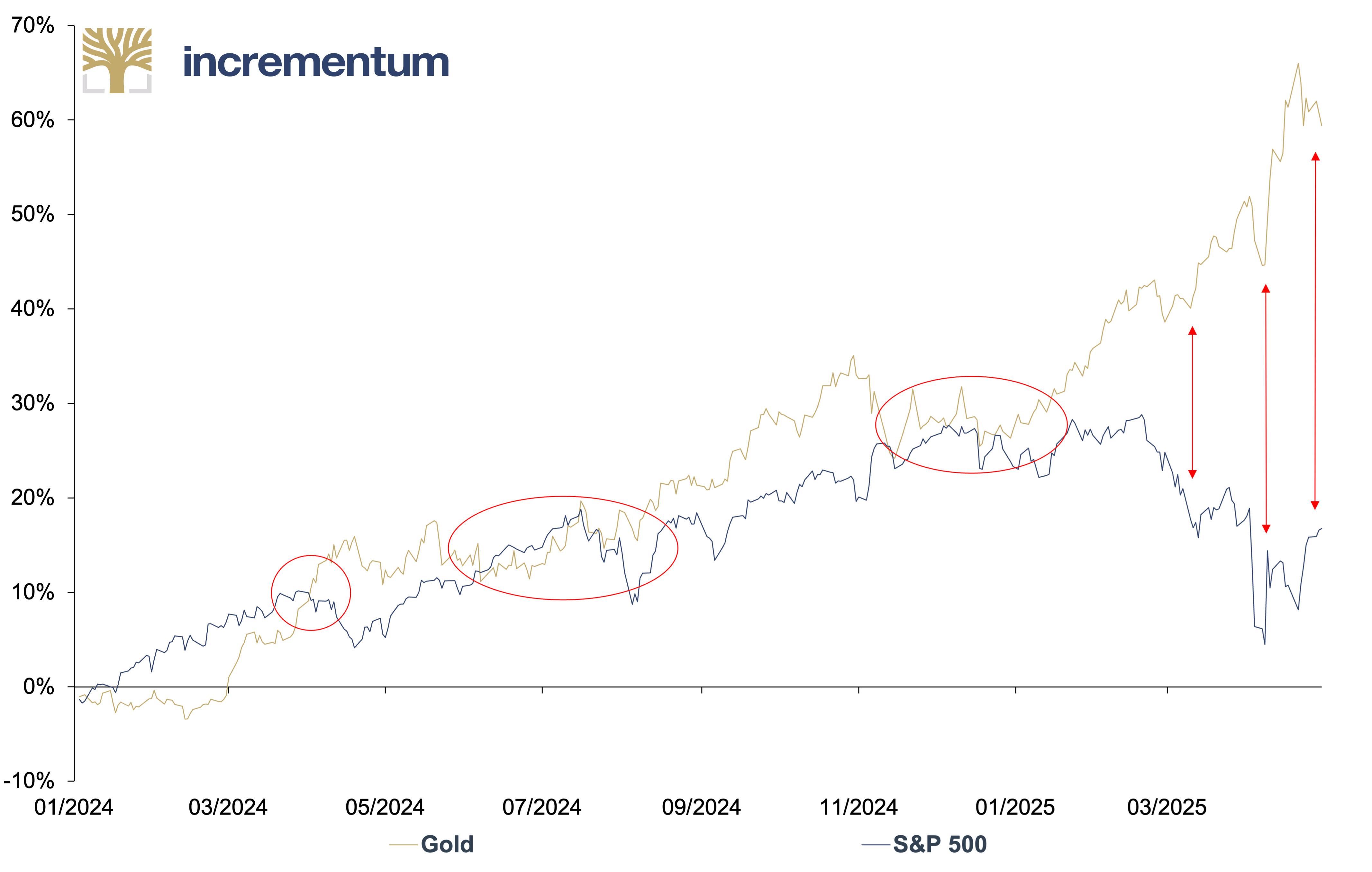

The growing gap between gold and the S&P 500 since the beginning of the year points to fundamental changes. Capital is increasingly flowing from US markets into the safe haven of gold, as well as into Europe and select emerging markets. If this trend is confirmed, it would be a clear signal of a sectoral and geographical rotation with far-reaching consequences for global investment strategies.

Gold and S&P 500, in USD, 100 = 01/01/2024, 01/2024–04/2025

Source: LSEG, Incrementum AG

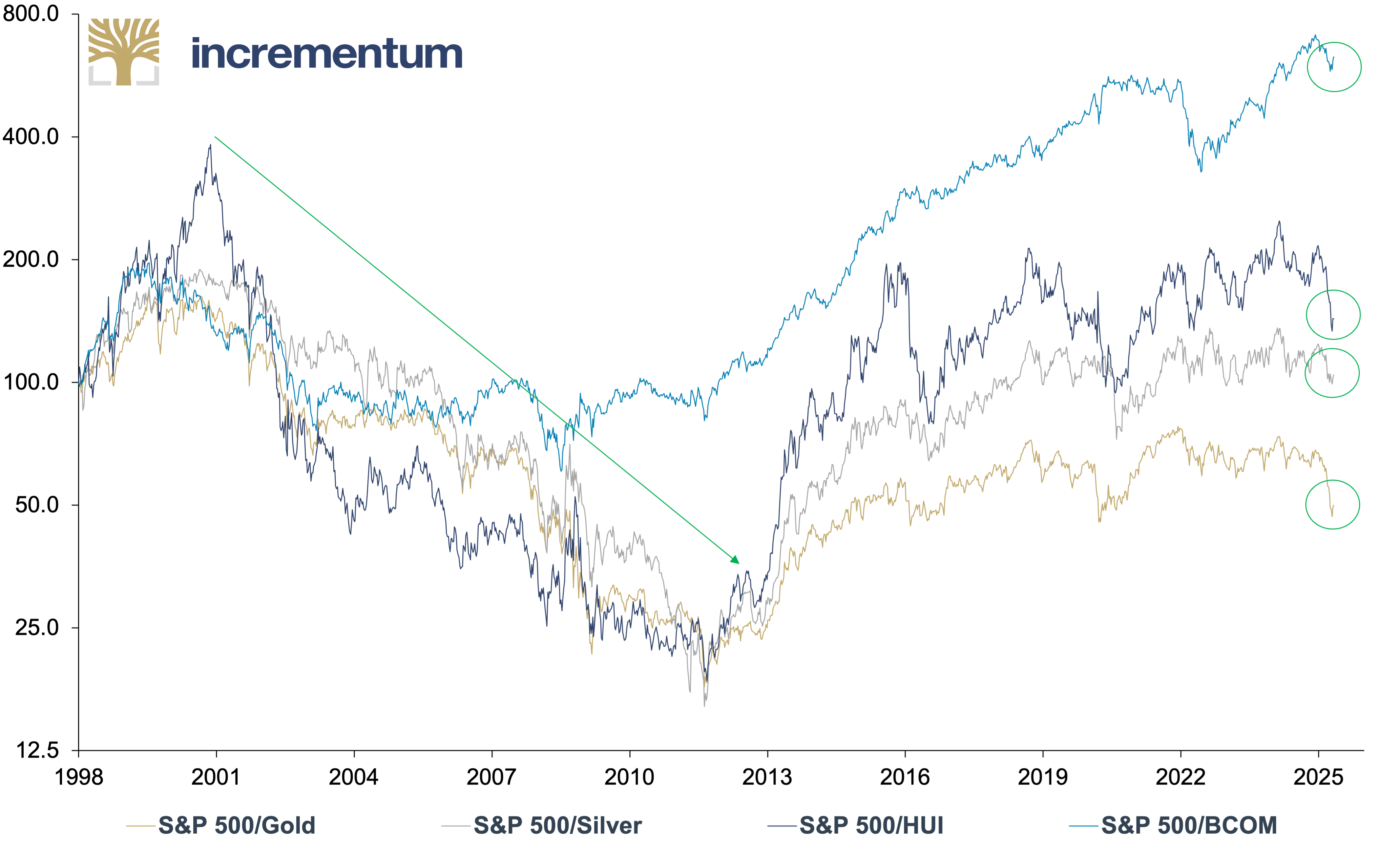

A look at the relative performance of the S&P 500 against gold, silver, mining stocks (HUI), and commodities (BCOM Index) also reveals a rotation. A cyclical turning point can be identified with the relative strength of silver and mining stocks against gold. A sustained downward breakout of the S&P 500 would indicate a significant shift in capital flows.

In other words, we are witnessing capital outflows from a once immensely popular and widely held sector into performance gold, an asset that has lingered in the shadows for nearly a decade. The Big Long is not merely beginning – it is awakening.

S&P 500 vs. Gold, Silver, HUI and BCOM (log), 100 = 01/1998, 01/1998–04/2025

Source: LSEG, Incrementum AG

Thank you very much!

Year after year, the In Gold We Trust report strives to live up to its reputation as the gold standard of gold studies. We aim to produce the world’s most respected, widely read, and comprehensive analysis of gold. Mark Baum[12] said in his criticism of the financial sector, “Nobody pays attention to detail”. But it is precisely these details that count, and it is the mission of the In Gold We Trust report to bring you, dear readers, closer to the crucial details of the gold market.

That’s why every year we retreat from the hustle and bustle of everyday life to reflect, research facts and figures, and finally write the In Gold We Trust report. Over the past few months, many events have presented us with a real challenge. And like many other market watchers, Trump’s Liberation Day has given us a few headaches, as has Mr. Trump’s skittishness in general.

This 19th edition of the In Gold We Trust report also features several firsts. The short version of the report is published in Japanese for the first time, in addition to German, English, and Spanish. With Mining Visuals, a Swedish company specializing in the graphical processing of data relevant to the mining sector, we have brought competent and enthusiastic reinforcement on board. For the first time, the In Gold We Trust report is also available in print via this link.

We thank our more than 20 fantastic colleagues on four continents for their energetic and tireless efforts over 20,000 hours and numerous time zones. Special thanks go to our Premium Partners[13]. Without their support, it would not be possible to make the In Gold We Trust report available free of charge and to expand our range of services year after year. In addition to the annual publication in five languages, we provide a monthly Monthly Gold Compass and ongoing information on our In Gold We Trust report website at ingoldwetrust.report.

We are convinced that the current gold bull market has not yet reached its end. Now we invite you to our annual tour de force and hope that you enjoy reading our 19th In Gold We Trust report as much as we enjoyed writing it.

With best regards from Liechtenstein,

Ronald-Peter Stöferle and Mark J. Valek

[1] See “Quo vadis, aurum?,” In Gold We Trust report 2020; we provide a comprehensive update of the Incrementum Gold Price Model in the chapter “1970s, 2000s, 2020s…: A déjà vu in two acts – Act Two” in this In Gold We Trust report.

[2] All previous 18 issues of the In Gold We Trust report can be found in our archive.

[3] Our thoughts on the optimal gold allocation can be found in “The Optimal Gold Allocation – How Much Gold Does Your Portfolio Need?”, In Gold We Trust Special, August 2024.

[4] See chapter “Performance Gold – Is It Time for Mining Stocks?” in this In Gold We Trust report, presenting the Incrementum Active Aurum Signal. This proprietary signal supports the weightings of the Incrementum Active Gold Fund.

[5] See the Incrementum Recession Phase Model in “The Showdown in Monetary Policy,” In Gold We Trust report 2023 and “Portfolio Characteristics: Gold as Equity Diversifier in Recessions,” In Gold We Trust report 2019

[6] See “Exclusive Interview with Zoltan Pozsar: Adapting to the New World Order,” In Gold We Trust report 2023

[7] See “How Bankers Turned Money into ‘Σ 0 ∞ € ¥’,” In Gold We Trust report 2021

[8] See Stöferle, Ronald (@RonStoeferle): “THREAD: A User’s Guide to Restructuring the Global Trading System’ is probably the most important paper you’ve never heard of!…”, X, March 2025

[9] See “History Does (Not) Repeat Itself – Plaza Accord 2.0?,” In Gold We Trust report 2019

[10] See chapter “Dollar Milkshake Meets Golden Anchor: Mar-a-Lago and the New Economic Order” in this In Gold We Trust report

[11] See “Gold in the age of trust erosion”, In Gold We Trust report 2019

[12] Mark Baum is a fictional character from the film The Big Short (2015), based on the real-life investor Steve Eisman.

[13] At the end of the In Gold We Trust report you will find an overview of our Premium Partners, including a brief description of the companies.