Introduction

“The balancing act of fighting inflation without triggering distortions on the markets is doomed to failure. The vehemence of the tightening cycle that has begun threatens to end the Everything Bubble in an Everything Crash.”

In Gold We Trust report 2022

- It’s a showdown foregone. For as we predicted in the two In Gold We Trust reports “Monetary Climate Change” and “Stagflation 2.0”, it was only a matter of time before the consequences of years of zero and low, sometimes even negative, interest rates, come to light.

- The persistent underestimation of inflation dynamics ultimately forced central banks to sharply and quickly raise interest rates.

- Tight monetary policy has initiated a painful unraveling of various misallocations that formed during the low-interest-rate environment that lasted for more than a decade.

- The recession we anticipate will force a monetary policy showdown against the backdrop of inflation rates that remain too high.

- A geopolitical showdown is brewing between the West and several emerging economies. The US dollar-centric global monetary system is coming under increasing pressure.

- The gold price already anticipates that the restrictive US monetary policy will turn out to be a bluff. Even if the gold price in US dollars has not yet marked a new all time high, the all-time highs in various other currencies are a harbinger for a breakout in US dollars.

We live in a time when events unfold at an ever-accelerating pace. The quote erroneously attributed to Lenin, “There are decades in which nothing happens, and weeks in which decades happen”, now seems to be our reality. Certainties of decades past are being made obsolete overnight. As we follow the news, many of us experience uncertainty, trepidation, and overwhelm. The global pandemic, the inflation crisis, increasing political polarization, technological breakthroughs such as artificial intelligence – which, by the way, we used to create the cover of this In Gold We Trust report – but also the impending geopolitical realignment are changing our lives in ways that were unimaginable to many of us just a few years ago.

We have referred to these looming epochal changes many times in past In Gold We Trust reports. We chose titles such as “Gold in the Age of Eroding Trust” (2019) and “Monetary Climate Change” (2021) for good reason. And this year, too, calls for a pointed title that captures the complexity of the current situation. We’re going with Showdown.

If you search the dictionary for the meaning of showdown, you will get the following definition:

- “the laying down of one’s cards, face upward, in a card game, especially poker.

- a conclusive settlement of an issue, difference, etc., in which all resources, power, or the like, are used; decisive confrontation.“

In our opinion, the term showdown is an apt description of the current situation, in which economic, political and social developments are on the brink of a fundamental change of course.

The current situation is also unique because we are not dealing with a singular showdown. Multiple escalations are occurring simultaneously and have the potential to further inflame each other. These showdowns are all related to issues we have already analyzed in detail in previous years in our In Gold We Trust report:

- the monetary policy showdown

- the geopolitical showdown and the associated de-dollarization

- the showdown in the gold price

The Monetary Policy Showdown

It’s a showdown foregone. For as we predicted in the two In Gold We Trust reports “Monetary Climate Change” and “Stagflation 2.0”, it was only a matter of time before the consequences of years of zero and low, sometimes even negative, interest rates, come to light. Actions have consequences – expected consequences, that is.

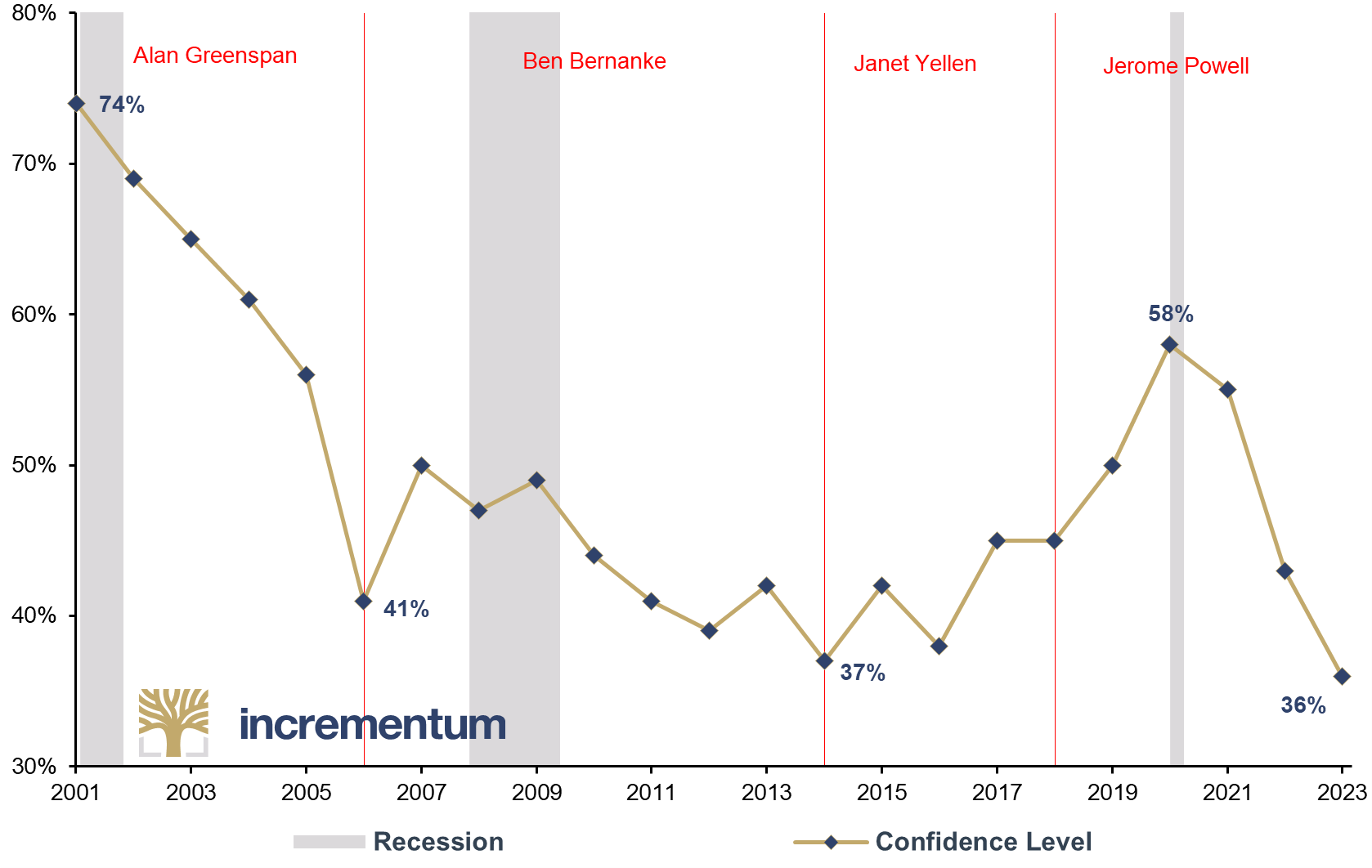

However, central bankers had trotted out appeasement rhetoric even at inflation rates well beyond their 2% inflation target. Jerome Powell’s insistence that inflation was merely transitory is now as legendary as Christine Lagarde’s belittling description of the inflation surge as a hump. Not surprisingly, confidence in central banking is in a steep decline.

Confidence Level in the Fed Chair*, 2001-2023

Source: Gallup, Incrementum AG

*Percentage of people who have a “great deal” or “fair amount” of confidence in the Federal Reserve chairman.

This negligence resulted in an emergency monetary policy brake. With the economic slowdown now underway and inflation rates still clearly too high, the monetary policy trilemma – price stability vs. financial market stability vs. economic support – that we warned about is now a reality.

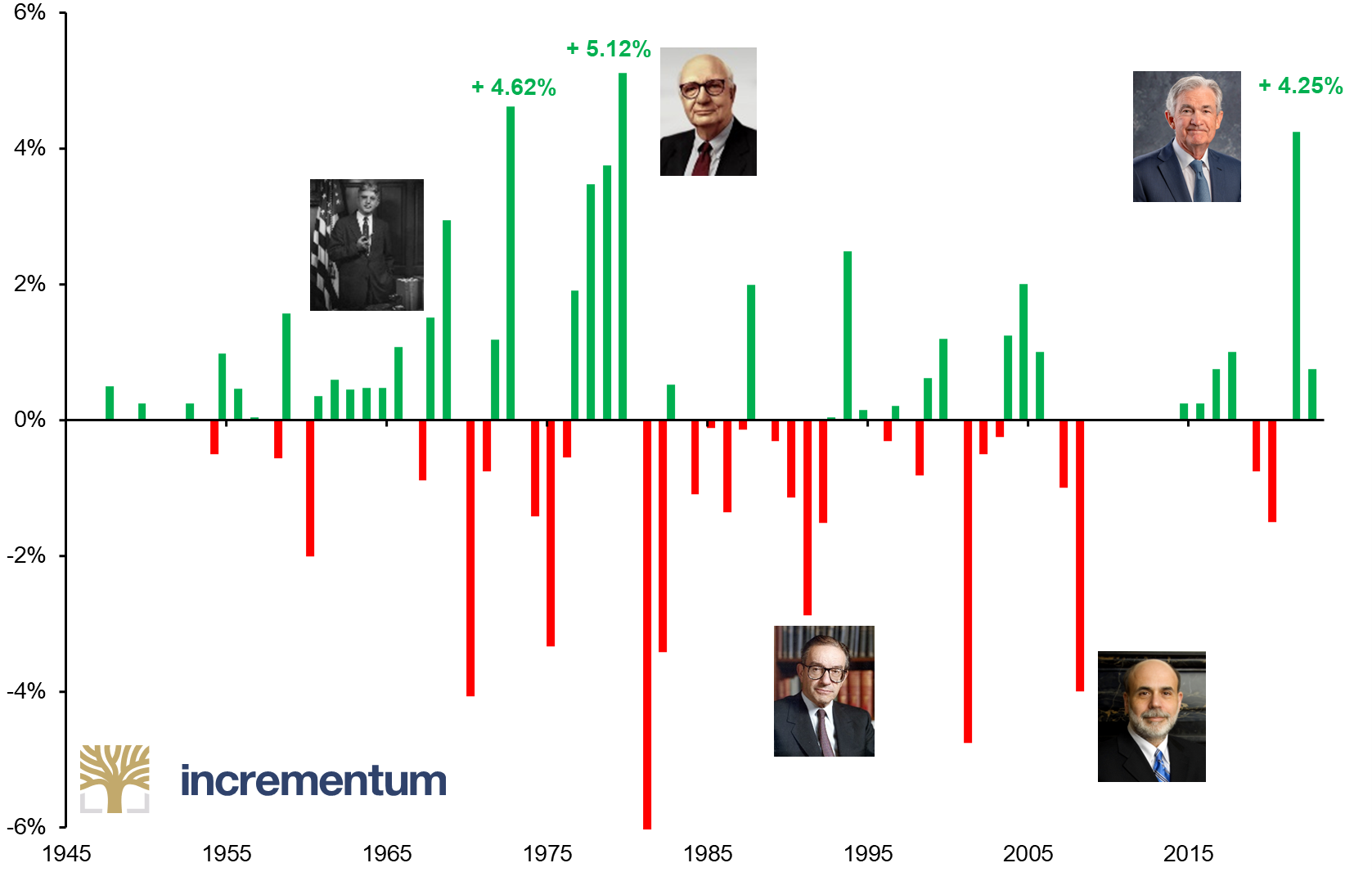

When central bankers finally recognized the severity of the situation, however, they acted with unexpected rigor. Jerome Powell raised interest rates twice as much in less than a third the time that Janet Yellen took in the last hiking cycle. His vehemence surprised us, as it probably did every other analyst, market strategist, fund manager – and astrologer. But it’s true: If you hit the brakes too late, you have to hit harder!

Annual Change in Federal Funds Rate, 1945-2023

Source: Reuters Eikon, Incrementum AG

Despite the radical tightening of monetary policy, inflation is proving to be extremely stubborn. Until recently, the Federal Reserve had signaled that it was prepared to do everything in its power to get inflation back under control. After a decade and a half of a flood of liquidity and ultra-low interest rates, withdrawal symptoms are now increasingly appearing after the abrupt removal of the punchbowl. It is becoming apparent which business models have been supported only by low interest rates in recent years and which are fundamentally standing on their own two feet.

The strongest and fastest interest rate hikes in the industrialized nations in over 40 years have already claimed their first victims. The pension fund debacle in the UK, the closure of the Blackstone Real Estate Income Trust, various calamities in the crypto sector, – above all the spectacular FTX bankruptcy – are just a few examples of the consequences of the abrupt interest rate turnaround.

In March, another economic problem front opened up when Silicon Valley Bank (SVB ) collapsed without warning, followed shortly by Signature Bank. In early May, another regional bank, First Republic, followed suit. We believe it would be too simplistic to blame the regional bank collapse solely on poor management or on their exposure to the stumbling technology sector, which is known to be highly interest rate sensitive.

Three of the four largest US bank failures in history took place in the past few weeks; only the collapse of Washington Mutual in September 2008 caused significantly higher losses, both in nominal and real terms. All in all, more than USD 500bn has already had to be written off since the beginning of March. This is a clear warning signal that the financial system is much more fragile than generally assumed. And on this side of the Atlantic, too, a major bank has already had to pull up stakes, and with the venerable Credit Suisse, it is not just any bank that has been hit. In mid-March, the bank was sold off to UBS in a smoke and-mirrors operation.

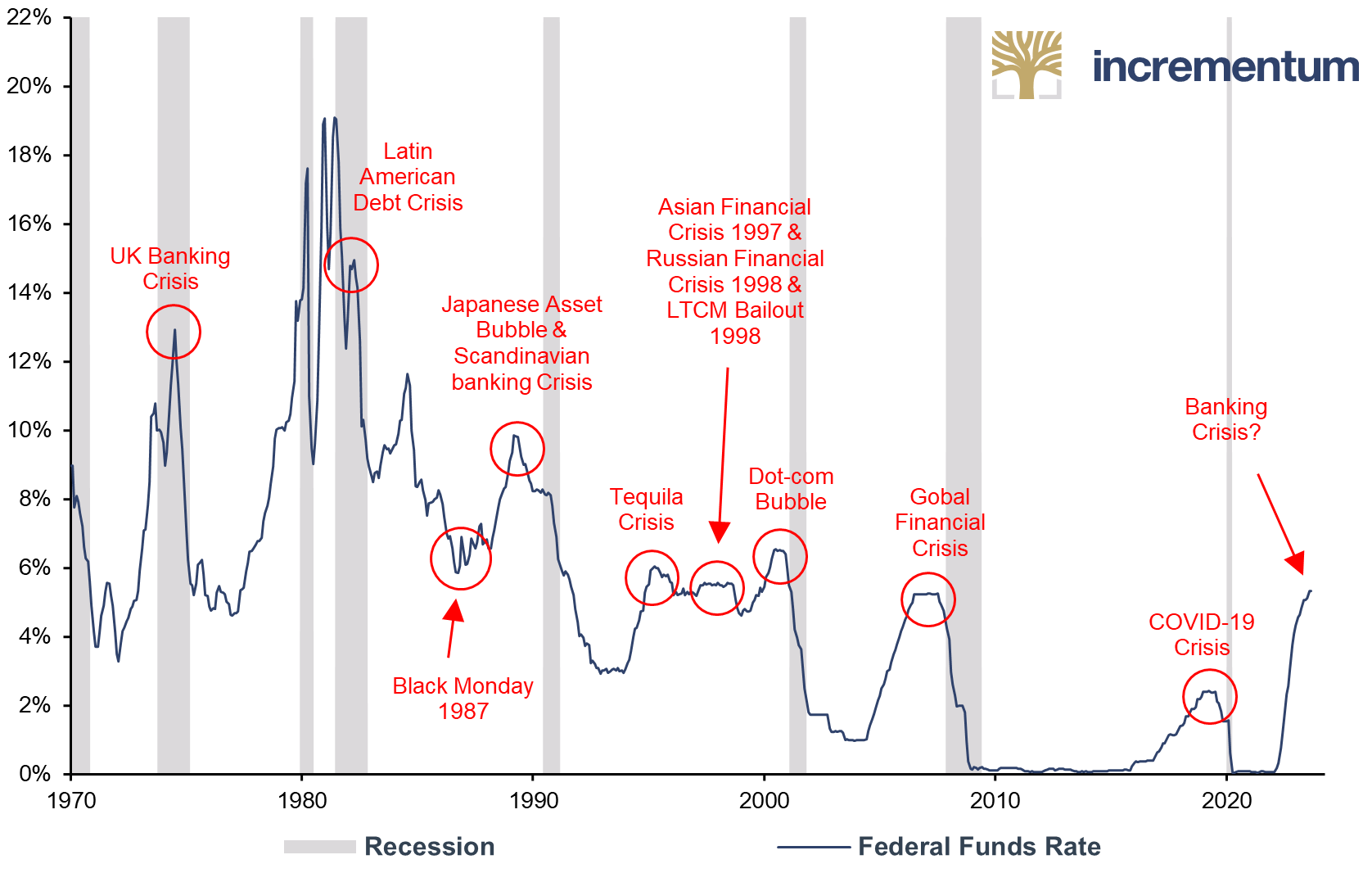

Undeterred, the mainstream continues to hail the resilience of the US economy and downplay the problems. However, for all those familiar with the Austrian Business Cycle Theory pioneered by Ludwig von Mises and Friedrich August von Hayek, it is no surprise that the radical turnaround in interest rates is causing acute pain. Financial history is full of precedents where flooding the markets with liquidity triggers an artificial boom.

Federal Funds Rate, 01/1970-05/2023

Source: Reuters Eikon, Incrementum AG

When the artificial stimuli are withdrawn, the misallocations are ruthlessly exposed and then cleaned up by painful price collapses, insolvencies, and recessions. “Only when the tide goes out do you discover who’s been swimming naked,” is how Warren Buffett so aptly described this phenomenon. And there is much to suggest that many more swimmers will turn out to be nudists. In this context, we particularly recommend our chapter on the crack-up boom in this In Gold We Trust report to interested readers.

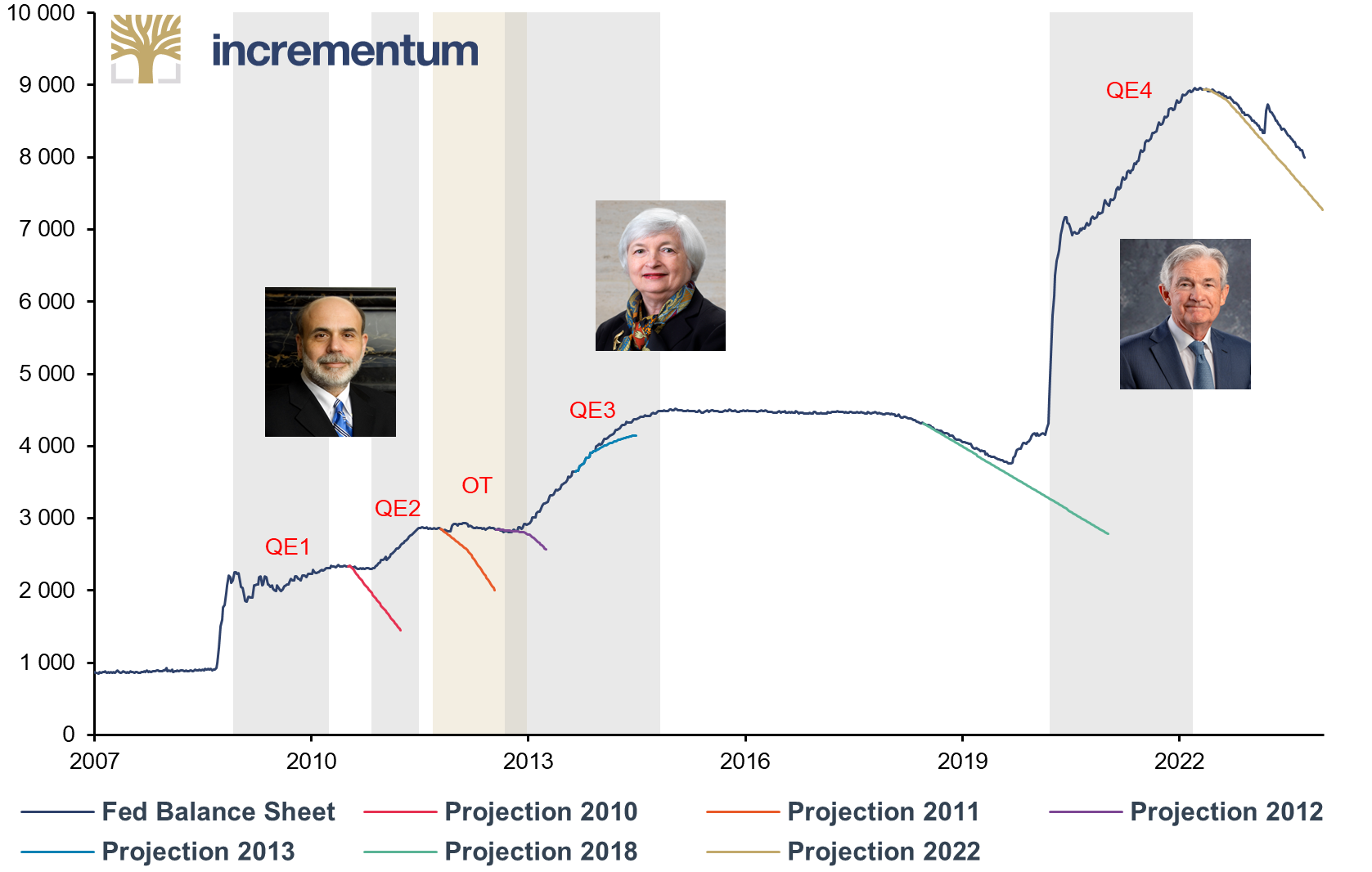

In addition to interest rate hikes, a key component of current policy is quantitative tightening, i.e. the reduction of the central bank’s balance sheet. According to schedule, the Federal Reserve’s balance sheet is currently being reduced by USD 95bn per month, which corresponds to a reduction of 12% p.a. in total assets. However, this schedule already had to be deviated from at short notice in connection with the bank failures in March, and the balance sheet total had to be inflated again by USD 400bn.

Fed Balance Sheet Path, in USD bn, 01/2007-01/2024e

Source: Reuters Eikon, Federal Reserve St. Louis, Incrementum AG

Subsequently, there was heated debate in financial market circles as to whether this rescue measure should be classified as a reversion to quantitative easing. In our opinion, this terminological hair-splitting distracts from the much more important point: When systemic problems arise, central banks ultimately have only one remedy, and that is to provide additional liquidity. Every attempt over the past 15 years to reduce the central bank balance sheet has usually failed miserably after only a few quarters.

Against this backdrop, the monetary policy showdown between price stability, economic activity, and financial market stability is now looming. The all-important question is: Can the Federal Reserve continue its restrictive monetary policy and push inflation back down to 2% without triggering a severe recession or a new financial crisis, or will it have to rescue the system once more with expansive stimulative measures and thus risk another wave of inflation? The cards must be laid on the table, at the latest, when the pain at the banks, on the capital markets, or in the real economy becomes too great.

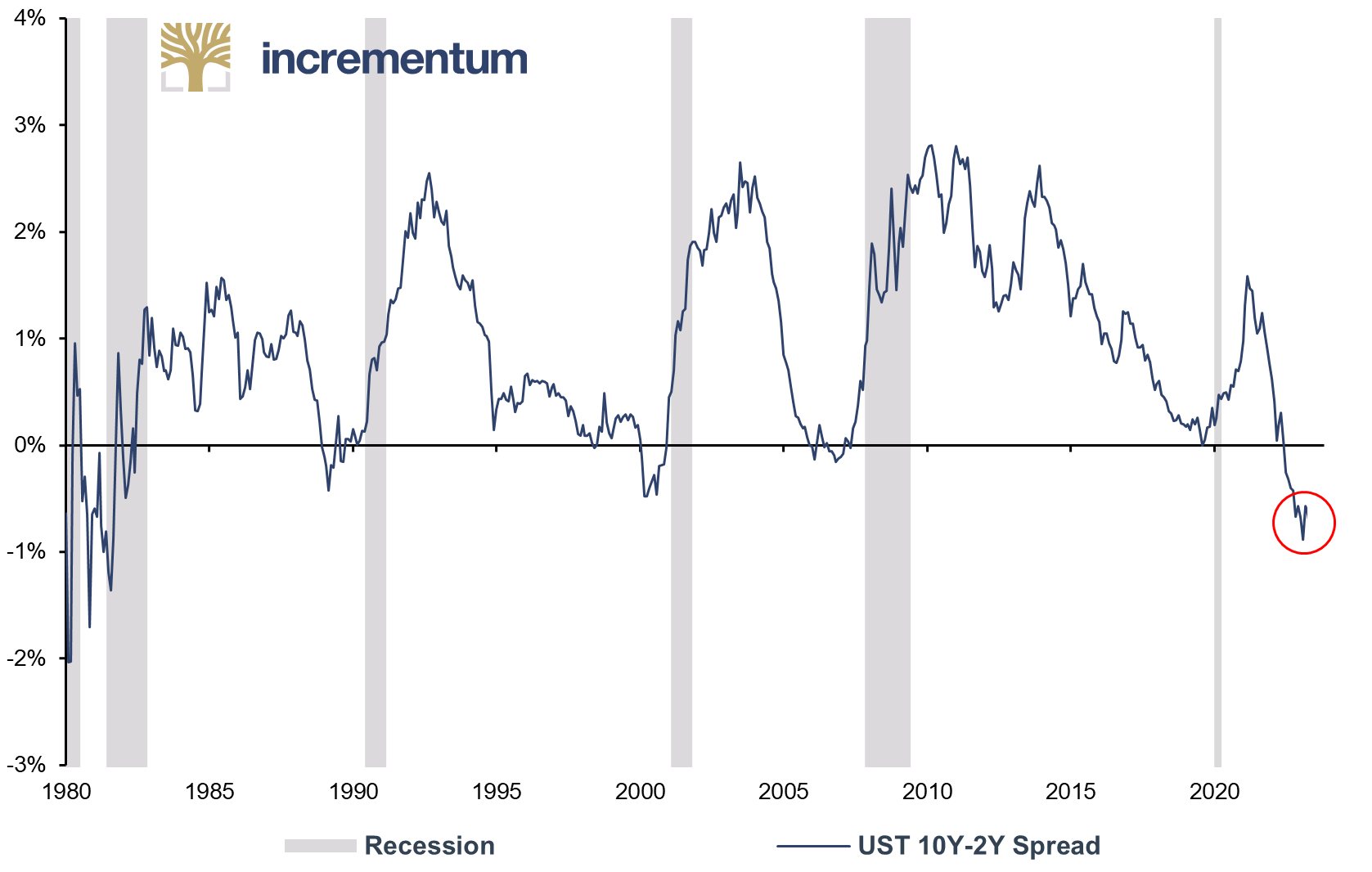

Negative money supply growth is unchartered territory

And the signs of an imminent recession in the USA are growing stronger. The strongly inverted yield curve, a slowly weakening labor market, the Conference Board Leading Economic Index (LEI) – all these leave little room for economic optimism. For a more in-depth analysis of the state of the US economy, see chapter 3, “The Monetary Policy Showdown”.

UST 10Y-2Y Spread, 01/1980-05/2023

Source: Reuters Eikon, Incrementum AG

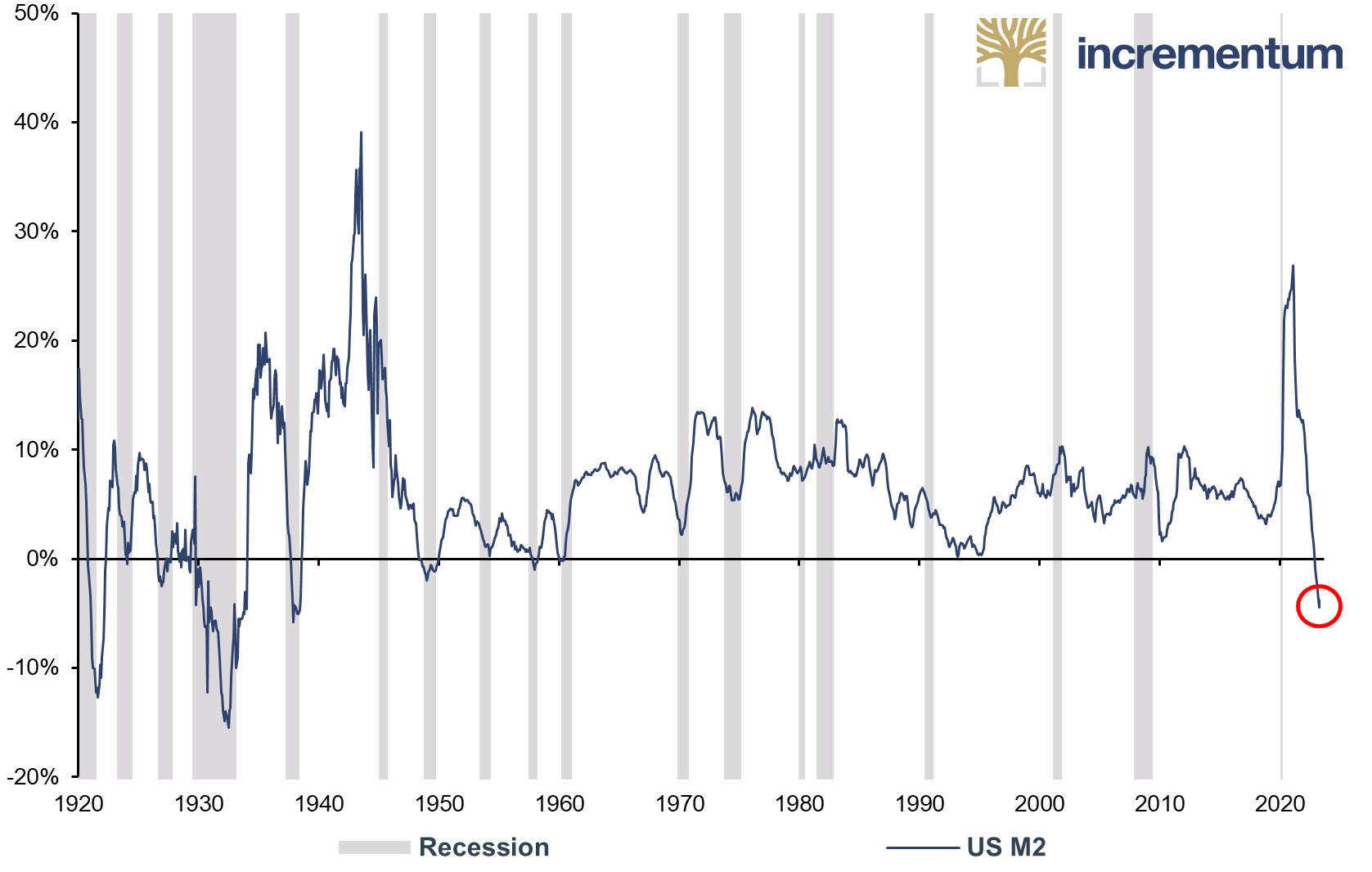

“Historically, whenever US M2 money supply has contracted on an annual basis, there’s been a banking crisis, a depression and/or deflation. Whilst all those prior occurrences happened prior to WWII, and since then ‘deposit insurance’ has been introduced (1933) and the Fed has become an active ‘lender of last resort’, it’s also the case that M2 money supply hasn’t been contracted since the Great Depression. In that sense the current framework is untested.” [1]

US M2, yoy, 01/1920-03/2023

Source: Federal Reserve St. Louis, Reuters Eikon, Incrementum AG

Although recessions but also capital market slumps have a disinflationary and sometimes even deflationary effect, the response will be highly inflationary: QE, YCC, and interest rate cuts. What is certain in these uncertain times is that the longer and deeper the financial markets fall, the more stimulative, aggressive and desperate the monetary and fiscal policy responses will be, ultimately laying the foundation for another, higher wave of inflation.

For us, one thing is certain: The soft landing much invoked by the Federal Reserve seems to become less likely by the day. The coming showdown will reveal whether the Federal Reserve is actually holding the strong hand it claims to be holding, or whether it will be called by the market and its strategy exposed as a bluff.

The Geopolitical Showdown

In geopolitics, we are also approaching a gripping showdown. Relations between the world’s political power centers are increasingly strained, and there is a showdown between the saturated establishment and the hungry upstarts.

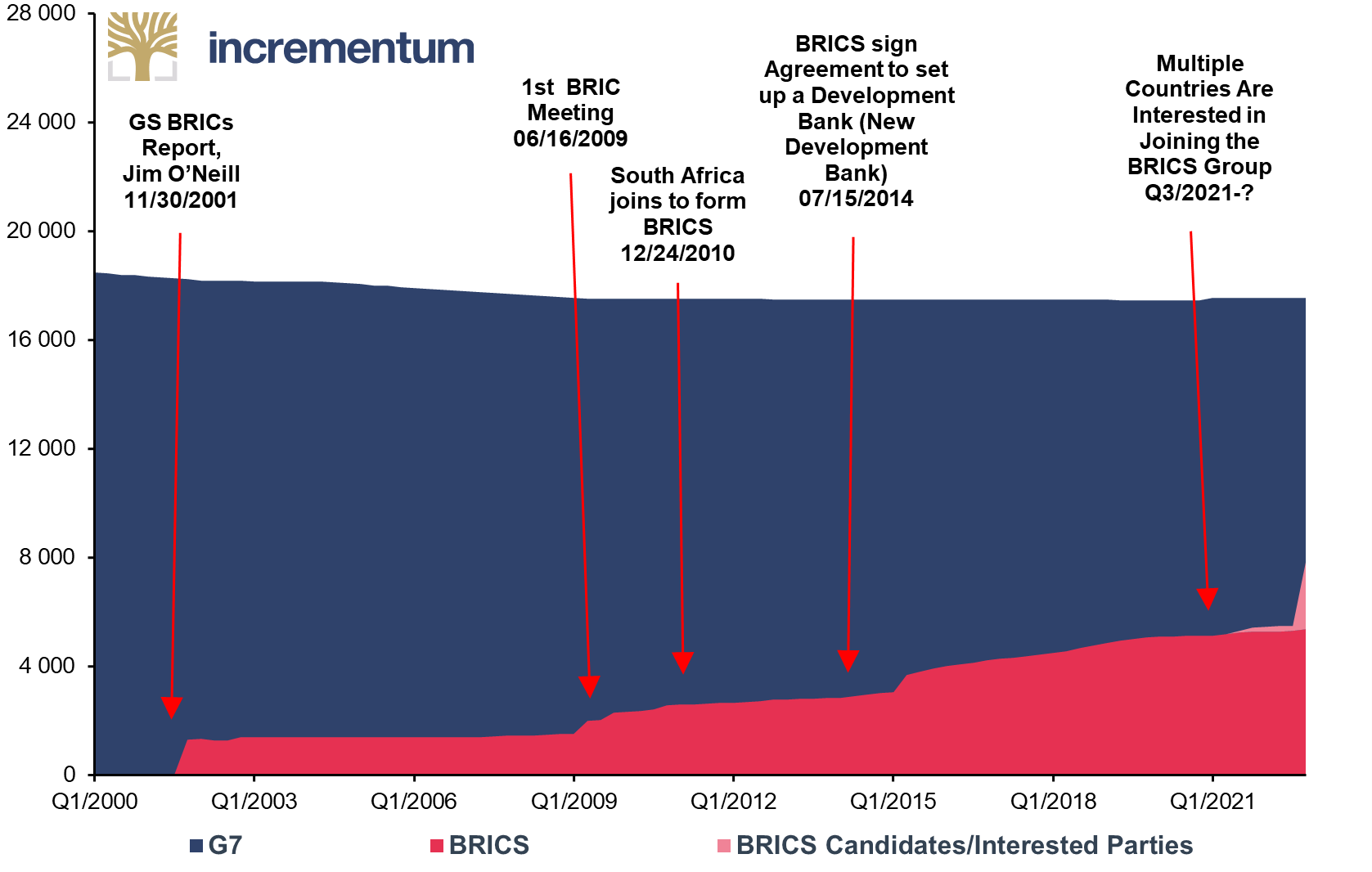

At the forefront are the collective West under the leadership of the US, on the one side, and China, Russia and the bloc forming around these two heavyweights on the other. A considerable number of emerging economies associate themselves with the latter, some formally through organizations that challenge the US-centric world order. A central example of such an association is the BRICS states, which 19 other states from Asia, Africa and South America want to join. And it is precisely these states that have been increasingly building up gold reserves and reducing US dollar reserves since 2008.

Global Gold Reserves, G7 and BRICS + BRICS Candidates/Interested Parties, in Tonnes, Q1/2000-Q4/2022

Source: World Gold Council, Incrementum AG

This trend has accelerated again as a result of the sanctions against Russia, as we projected in the In Gold We Trust report 2022. The emerging-market countries have taken careful note of the militarization of money and are now trying to reduce their dependence on the US dollar. One of the few neutral and liquid reserve currencies in this political environment remains gold. The accumulation of the precious metal as an alternative is now being discussed by highly official circles. Christine Lagarde recently noted, “We are also seeing increased accumulation of gold as an alternative reserve asset, possibly driven by countries with closer geopolitical ties to China and Russia.”

Similarly, efforts to reduce the role of the US dollar as a trading currency are increasing. China, for example, made virtually no use of the yuan for foreign trade transactions in 2010. By contrast, at the end of March, for the first time, China conducted more sales in the yuan than in the US dollar, which was still responsible for 83% of China’s foreign trade in 2010. There are also increasing efforts to develop alternative trade currencies and payment systems. As early as March 2022, Zoltan Pozsar had initiated this debate in a stimulating way with his article Bretton Woods III. He concluded his remarks with the following forecast: “From the Bretton Woods era backed by gold bullion, to Bretton Woods II backed by inside money (Treasuries with unhedgeable confiscation risks), to Bretton Woods III backed by outside money (gold bullion and other commodities)”. Where exactly this journey will lead us, nobody knows at the moment. However, there is no question that we are irrevocably on the journey to a new global (monetary) order.

The historic rapprochement between Iran and Saudi Arabia, which China played a leading role in mediating, should also be mentioned in this context. In the course of this diplomatic masterstroke, new trade agreements were concluded for oil and gas deliveries, which are settled in yuan. These and other developments significantly undermine the petrodollar system institutionalized between the US and Saudi Arabia half a century ago. This year, we again take an in depth look at this issue, both in our traditional dedollarization chapter and in an interview with star analyst Zoltan Pozsar.[2]

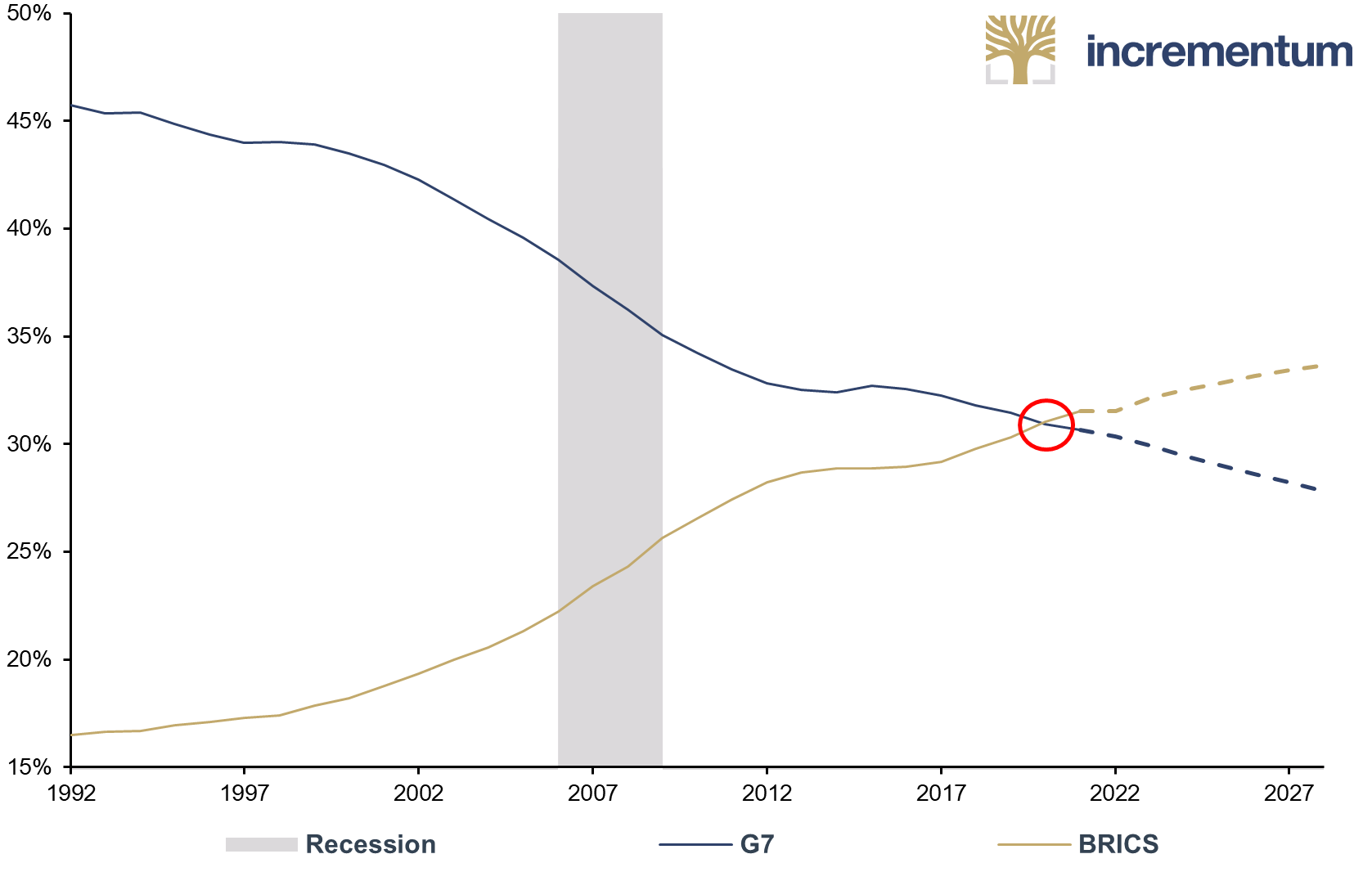

The growing political self-confidence of the BRICS countries is a logical consequence of their increasing economic importance. Measured in purchasing power parity, these countries have had a higher aggregate GDP than the G7 countries since 2021. With the exception of China, the demographic situation also argues for significantly higher long-term growth potential in the BRICS countries than in the West.

Share of Global GDP (PPP), G7 and BRICS, 1992–2027e

Source: Acorn MC Ltd, World Economic Outlook, Reuters Eikon, Incrementum AG

Given these dynamics, it is fair to ask to what extent we are in the Thucydides Trap today. This theory states that the rise of an emerging power leads to conflicts with the established world power. The term goes back to the Greek historian Thucydides. He noted that the rise of Athens in the 5th century B.C. would inevitably lead to tensions with Sparta and ultimately to war between the two powers for supremacy, for the position of hegemon. At worst, China’s growing strength and the resulting shift in the global power structure could lead to a warlike confrontation between the US and China-and their respective allies – as it did back then between the Attic Sea League led by Athens and the Peloponnesian League led by Sparta. The Thucydides Trap should be a warning to political elites to try everything possible to avoid war and keep the peace.

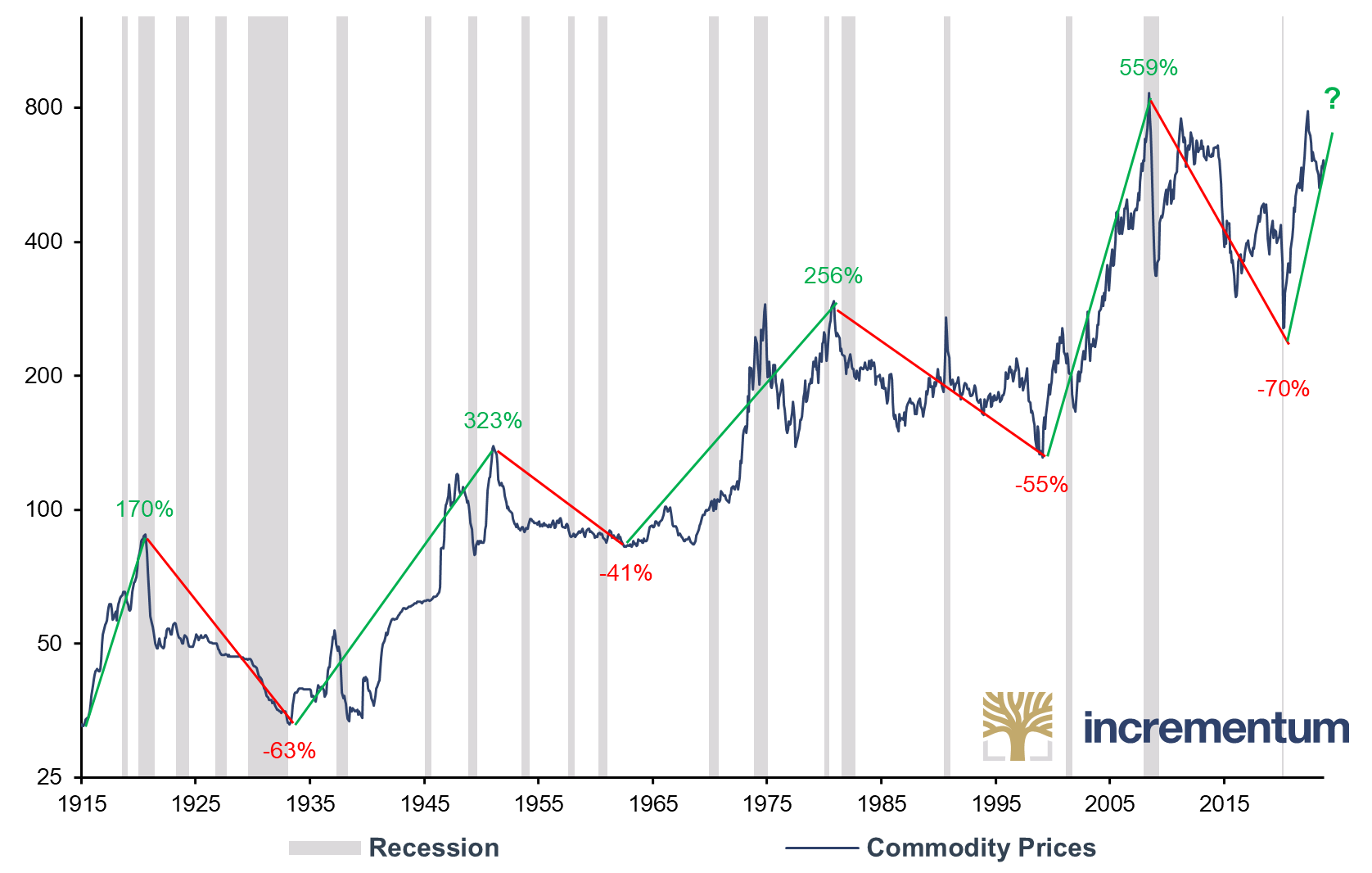

A showdown is also looming in the area of raw materials. Resource nationalism is gaining momentum. Chile, which has the world’s largest lithium reserves, announced it would nationalize SQM and Albemarle, two companies involved in lithium production. Indonesia has imposed export bans on nickel and tin so as not to jeopardize the development of domestic production of batteries. Our dear friend Alexander Stahel aptly noted recently,[3] that the prevailing view among policymakers that supply curves are elastic has been disproved by the pandemic, the energy transition and geopolitics. This represents a massive shift in the global investment environment. Global commodity supply curves may now be nearly vertical – a recipe for medium-term stagflation.

The consequences? Both fossilflation, after the supplies of natural gas, oil, and coal decrease in succession, and greenflation, meaning higher metal and mineral prices due to increased demand for green commodities. Energy innovations will eventually help make energy cleaner, cheaper, and more abundant worldwide. But such breakthroughs will require many trillions in investment or an energy miracle such as fusion technology. The commodity supercycle, which we have regularly highlighted in recent years, is clearly intact in our view and could gain significant momentum once the current correction phase is over.

Commodity Prices*, 01/1915-04/2023

Source: Alpine Macro, Federal Reserve St. Louis, Reuters Eikon, Incrementum AG

*1913-1934 US PPI Industrial Commodities, 1935-1949 Spot Price 28 Commodities, 1950-1969 Spot Price 22 Commodities, since 1970 S&P GSCI

The Showdown in the Gold Price

This leads us to the central topic of our In Gold We Trust report, the showdown in the gold price. We are convinced that the monetary and geopolitical situation as well as the chart development of the gold price suggest that a showdown in gold is imminent.

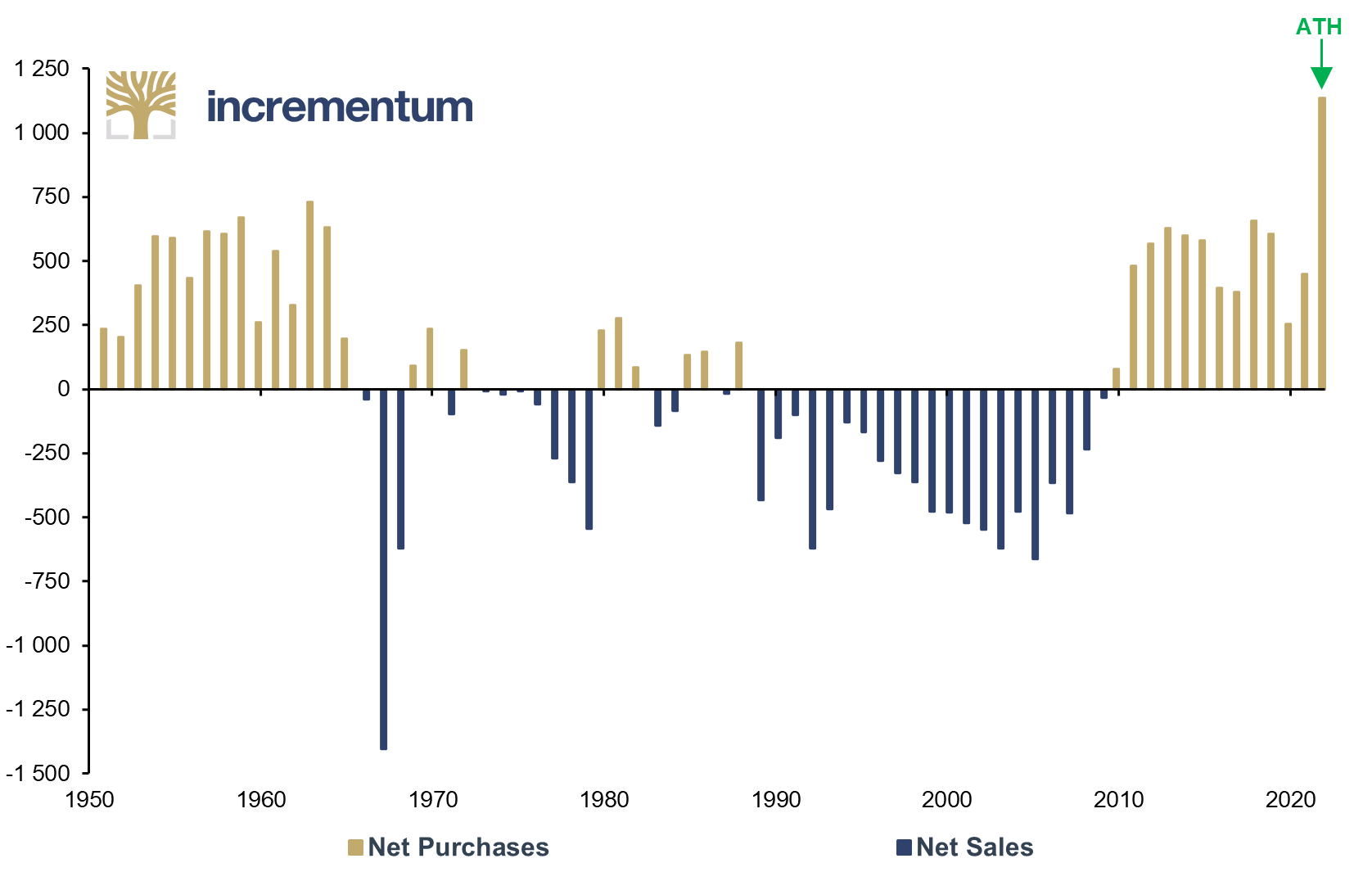

Central banks have been net buyers of gold since 2009. This momentum has accelerated significantly again in the past year. In 2022, central banks increased their purchases by 152%, to over 1,136 tons. Foreign exchange reserves, on the other hand, fell by a record USD 950bn. Asian central banks again made the bulk of gold purchases. For the first time in many years, China also made an official appearance as a buyer. It is noteworthy that with Qatar, Iraq, and the United Arab Emirates, three major energy exporters are now among the top ten gold buyers. We expect that central bank demand will become a key driver of this gold bull market.

Global Central Bank Gold Purchases, in Tonnes, 1950-2022

Source: World Gold Council, Incrementum AG

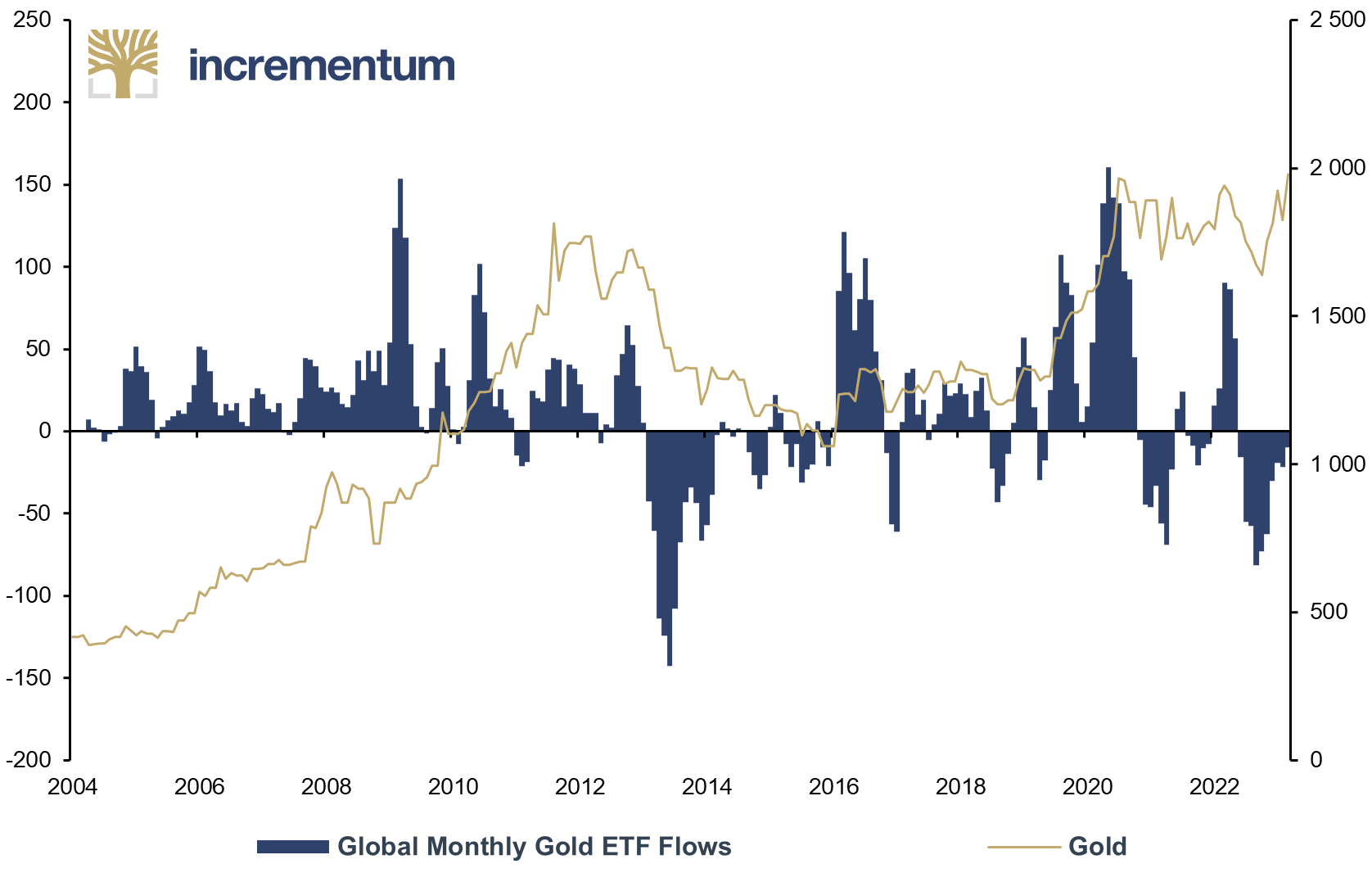

Not only central banks but also investors will be looking to protect themselves from stubborn inflation, a possible recession, and increasing default risks in the financial system. Currently, however, investor demand remains subdued. Although gold ETFs saw inflows again in March as a result of the banking crisis, this was after 10 straight months of outflows. In our view, the bulk of Western financial investors, for whose behavior ETF flows are a good indicator, remain on the sidelines. We expect that at new all-time highs, FOMO will kick in and new players will then enter the field in a flash. Investment demand from gold ETFs could tip the gold price scales.

Global Monthly Gold ETF Flows (3 Month Average) (lhs), in Tonnes, and Gold (rhs), in USD, 01/2004-03/2023

Source: World Gold Council, Incrementum AG

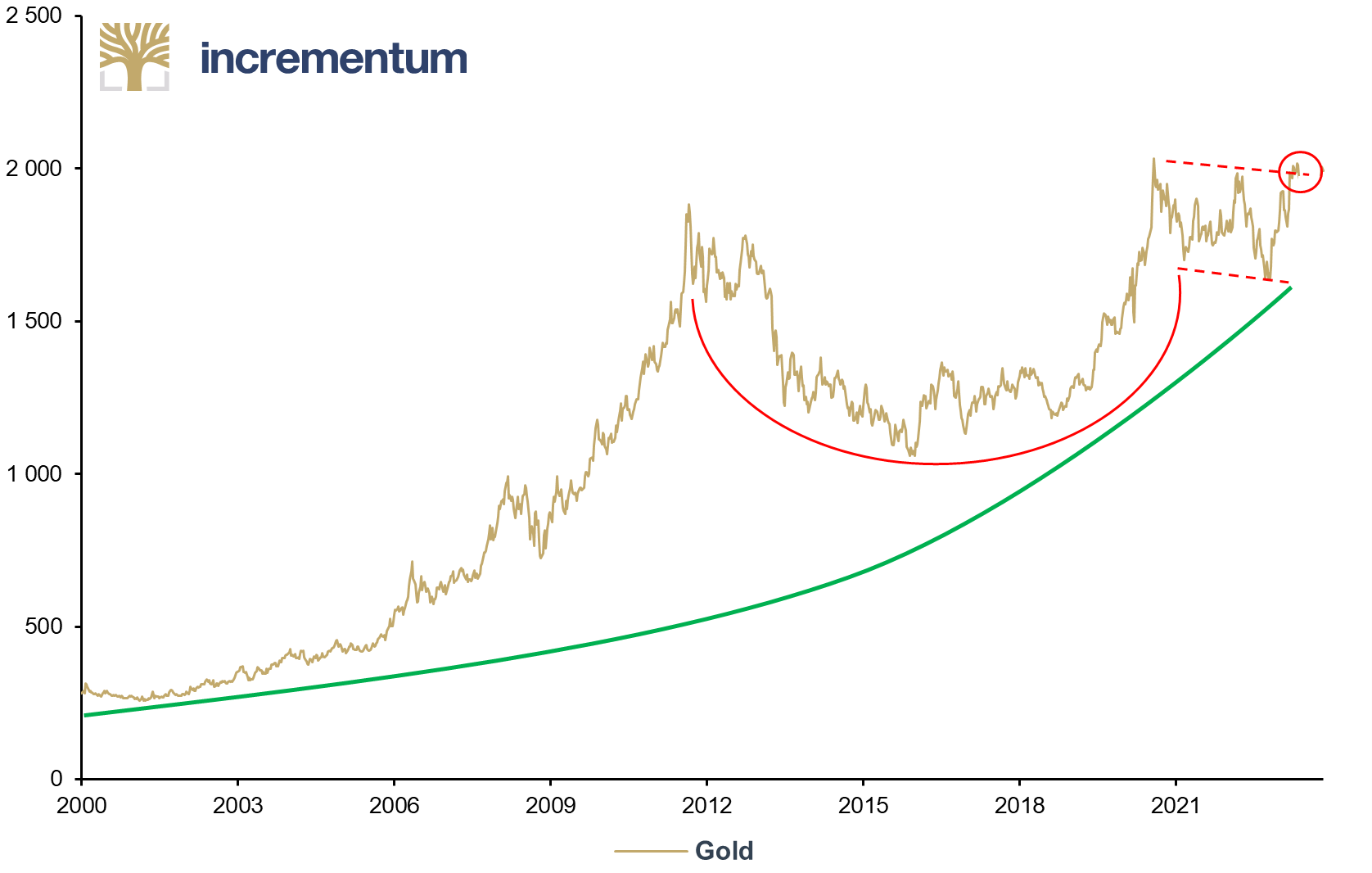

The gold price already seems to anticipate that the restrictive US monetary policy will turn out to be a bluff. Even if the gold price in US dollars has not yet marked a new all time high, the all-time highs in various other currencies are a harbinger for a breakout in US dollars.

Gold Cup-and-Handle Formation, in USD, 01/2000–05/2022

Source: Reuters Eikon, Incrementum AG

Other Highlights from this Year’s In Gold We Trust report:

- An in-depth analysis of the state of the US economy, including the presentation of our Incrementum Recession Phase Model. This model is designed to guide investors in their investment decisions during the five different recession phases.

- An exclusive interview with star analyst Zoltan Pozsar on the opportunities and risks of a reorganization of the monetary world order (Bretton Woods III).

- A detailed discussion of the process of de-dollarization and the specific initiatives to reduce dependence on the US dollar.

- An exclusive interview with Russell Napier on inflation, financial repression, and the capex cycle.

- An in-depth look at the flow of gold from West to East and the Chinese gold market in particular.

- A suggestion for goodwill to end the squabbles in the sound money camp between supporters of gold and those who favor Bitcoin.

- Background articles on various topics such as the crack-up boom phenomenon, the Chinese silver standard, and a proprietary bull market indicator.

- A detailed chapter on silver and its portfolio characteristics.

- A look at the capex issues in the mining sector and the technical analysis of the gold price.

- In the last chapter, as every year, we ask ourselves the question “Quo vadis, aurum?” and present an update of our gold price forecast.

Thank you very much!

Year after year, the In Gold We Trust report strives to be the world’s most recognized, widely read, and most comprehensive analysis on gold.

Every year we retire to our bower for a few weeks to do research; sort thoughts, data and facts; reflect; and finally write the In Gold We Trust report. After all, we want to offer you not only a comprehensive analysis of current developments but also historical, philosophical, and economic-theoretical insights around the topic of gold. In doing so, you, dear readers, are our greatest incentive. It is our pleasure to bring you closer to the always fascinating world of gold in an informative, entertaining, and understandable way. We thank you for your interest and the trust you place in our analyses.

This is the 11th time that this annual publication is being published under the umbrella of Incrementum AG. We would like to take this opportunity to thank our Incrementum AG partners, who regularly assist us as experienced and well-read sparring mates in matters of market analysis, company valuation, and fund management. We would also like to take this opportunity to thank Erste Group, the publisher of the first editions of the report. Without the support of Erste Group, the In Gold We Trust report would probably not have come into being in its current form.

We would also like to thank our more than 20 fantastic colleagues on four continents and in countless time zones [4] for their energetic and tireless efforts over more than 20,000 hours.

Last but not least, special thanks go to our Premium Partners.[5] Without their support, it would not be possible to make the In Gold We Trust report available free of charge and to expand our range of services year after year. In addition to the annual publication of the In Gold We Trust report in four languages, we publish our Monthly Gold Compass, as well as ongoing information on our In Gold We Trust homepage at ingoldwetrust.report.

We consider the examination of the past as indispensable for a successful preparation of the future. As a guide to the topic of gold, we would therefore like to once again offer you, our valued readers, a comprehensive, informative and concise compilation.

Now, we invite you on our annual tour de force and hope that you enjoy reading our 17th In Gold We Trust report as much as we enjoyed writing it.

With warm regards from Liechtenstein,

Ronald-Peter Stöferle and Mark J. Valek

[1] Longview Economics, “A Year of Shrinking Deposits – Now What? a.k.a. Banking Crisis Round Two,” March 22, 2023

[2] The short version of our interview with Zoltan Pozsar is part of this In Gold We Trust report, see “Exclusive Interview with Zoltan Pozsar: Adapting to the New World Order”. The long version is available here.

[3] Burggraben Investment Letter, February 2023

[4] All colleagues are pictured in the gallery at the end of the In Gold We Trust report.

[5] At the end of the In Gold We Trust report you will find an overview of our Premium Partners, including brief descriptions of the companies.