Global Demographics Turn Inflationary

“Demographics is destiny.”

Arthur Kemp

Key Takeaways

- Since in the 1980s the world has experienced a “demographic dividend” that has boosted growth and helped to keep inflation low. But that dividend is now turning into a deficit as the global dependency ratio begins to rise again.

- Between 1991 and 2018, the opening-up of China and Eastern Europe constituted an effective doubling of the labor supply available to advanced economies.

- Over that period, the value of exported goods as a share of global GDP jumped by 70%. Efficiencies from international trade and increased specialization helped to keep inflation low.

- A falling dependency ratio in China was particularly important as it buoyed the country’s productivity and allowed for the export of cheap goods to the developed world.

- But China’s dependency ratio has recently started to rise again due to ageing. From 41 today, it is forecast to reach 50 by 2030, and 70 by 2050.

- Western populations face huge demographic headwinds as well, which will lead to a steep rise in care-intensive diseases such as dementia.

- Demographics will serve as an important, and until now widely overlooked, contributor to the ongoing shift toward higher inflation in the decade ahead.

Introduction

In this chapter we focus on global demographic trends and discuss why we foresee demography, in addition to the monetary and fiscal factors discussed in other chapters, contributing to rising levels of inflation in the coming decades.

We argue that the relatively low inflation that advanced economies have experienced since the 1990s was made possible by the entry of hundreds of millions of new workers into the global economy, at a time when demographic conditions were favorable. The resulting increase in global productivity helped to keep prices low.

In the following pages, we outline how this came about, why the conditions of the post-1990 era are changing, and what this means for the future.

The Rise and Fall of Post-War Inflation

During the decades that followed the Second World War, the major economic powers of the world transitioned to a more state-led economic model. Government spending gradually rose until the 1970s, when the strains this placed on the private economy led to double-digit inflation and stagnant growth.

Consumer Price Inflation started to come down again in the late 1980s, falling to the 2-3% level, or even lower, where it has remained ever since. We argue that disinflationary supply-side forces of globalization were largely responsible for this trend.

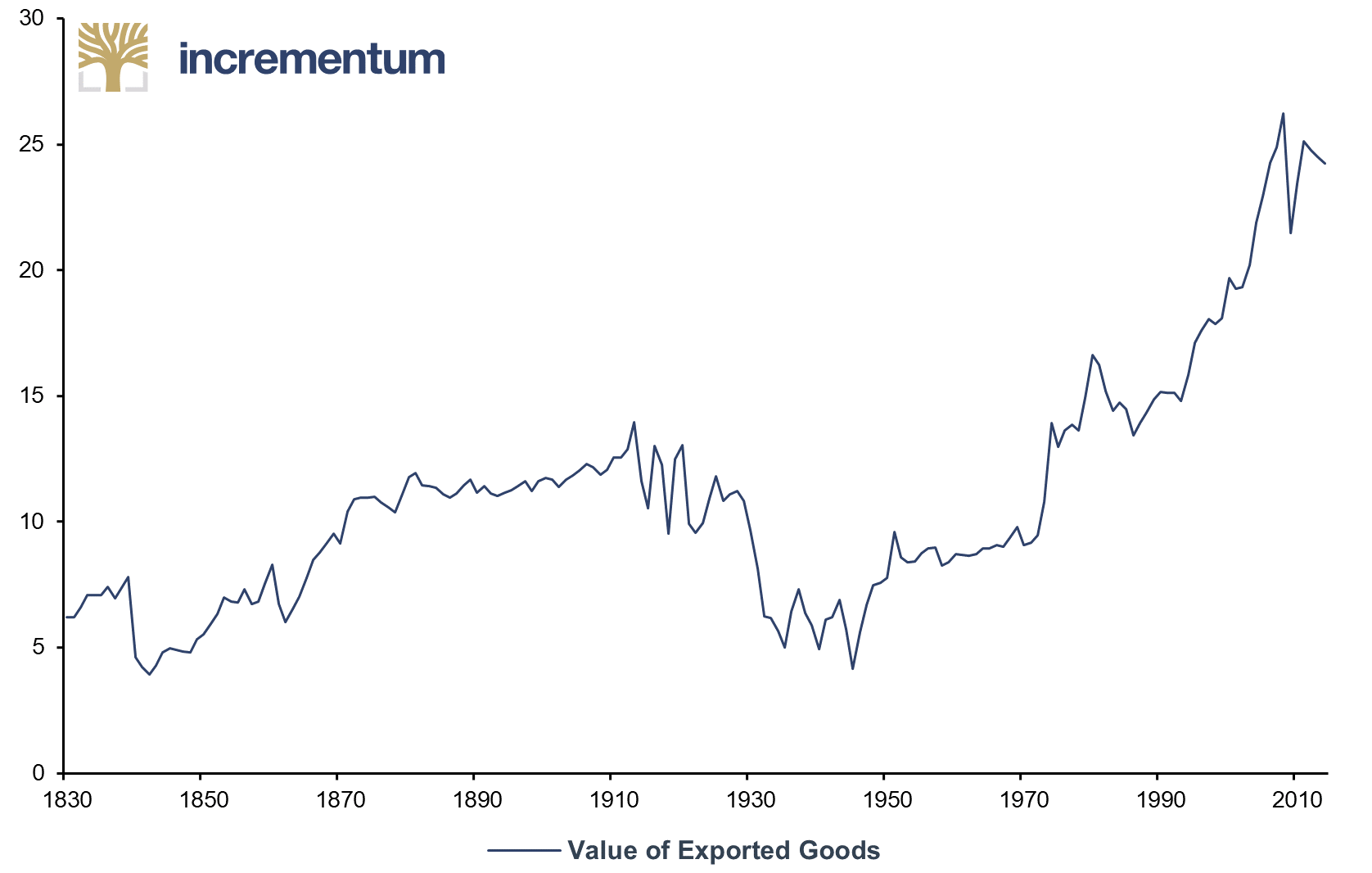

Between 1990 and the mid-2010s, as previously closed countries of the communist bloc liberalized and started to trade globally, the value of exported goods as a share of global GDP rose by 70%.[1] Cheap consumer goods flowed into developed nations, and this helped keep their inflation figures low, even as government spending remained high[2] and monetary policy remained accommodative.

Value of Exported Goods, in % of GDP, 1830-2014

Source: Fouqin and Hugot (CEPII 2016), ourworldindata.org, Incrementum AG

The opening up of China – home to one fifth of the world’s population – played a particularly important role in shaping international trade dynamics during this period. Between the late 1970s and 2009, China went from being an effectively closed economy to becoming the world’s largest exporter. The liberalization of China’s policies has been discussed at length elsewhere,[3] so in the paragraphs below we focus on the demographic factors that buoyed China’s growth, and why these are now starting to change.

The End of the Cold War and Entry of China into the Global Economy

During the 1970s one third of the world’s population lived in socialist command economies and truly global supply chains had yet to emerge. Things started to change in the later years of the decade in China – which represented a large part of the Communist world – following the death of Chairman Mao Zedong.

Mao’s successor, Deng Xiaoping, introduced the “Reform and Opening-up” policies that liberalized the Chinese economy and gave foreign investors access to the Chinese market. Deng’s pro-market reforms led to soaring economic growth, which averaged 10% per annum over the subsequent three decades. Given China’s huge population, this development had a profound impact on international trade.

Whilst China was liberalizing, it simultaneously experienced a large and sustained boost to economic productivity due to growing numbers of people in the workforce relative to the number of dependents.[4] Such a shift in demographics is known as a “dividend” because, when the proportion of working people in the population is high there is greater potential for productivity and growth, and fewer resources need to be diverted towards supporting those not engaged in economic activity.

Various empirical studies have shown that there is a strong association between demographic dividends and economic growth. For example, Bloom and Canning found that increasing the growth rate in the working-age population as a share of the total population by one percentage point, increases the rate of per capita GDP growth by 1.394 percentage points.[5] The following chart illustrates this correlation.[6]

10-Year Annualized % Growth of Working-Age Population (y-axis), and of Real GDP (x-axis), 2005-2015

Source: Haver, US Census Bureau, ourworldindata.org, UN, Incrementum AG

China’s demographic dividend, which manifested itself from the mid-1970s onwards, was primarily the result of three turbulent periods in Chinese 20th-century history, which we outline below. China serves as an extreme example of a demographic development that can also be found in Europe.

The Great Leap Forward

From the founding of the People’s Republic of China in 1949 until 1976, China was under the autocratic rule of Chairman Mao. Society was frequently disrupted by domestic political campaigns, the most impactful of which was the “Great Leap Forward” that began in 1958. In an attempt to boost industrial production through central planning, agricultural workers were pulled off the farms and ordered to work on uneconomic projects, such as the production of steel in small-scale furnaces.[7]

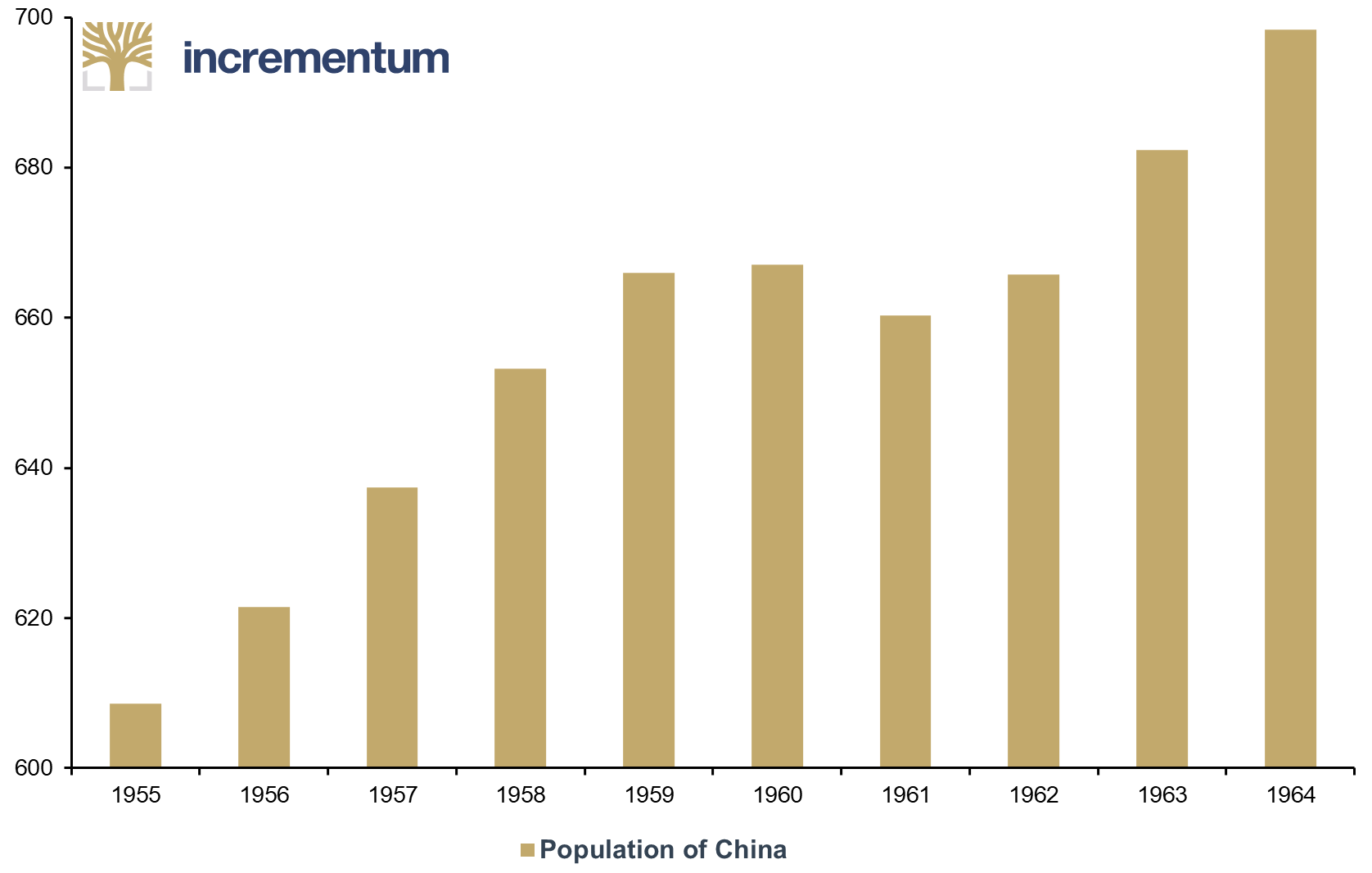

The reduction in farm labor this policy brought about led to crop failures and a famine that, according to research by Yang Jisheng, claimed an estimated 30-40 million Chinese lives.[8] These events were a tragedy of historic proportions that led to a sharp drop in China’s population from 1959-1961. This fall in population would go on to shape the age profile of China’s population in the decades ahead.

Population of China, in mn, 1955-1964

Source: National Bureau of Statistics China, Incrementum AG

The 1963–1973 baby boom

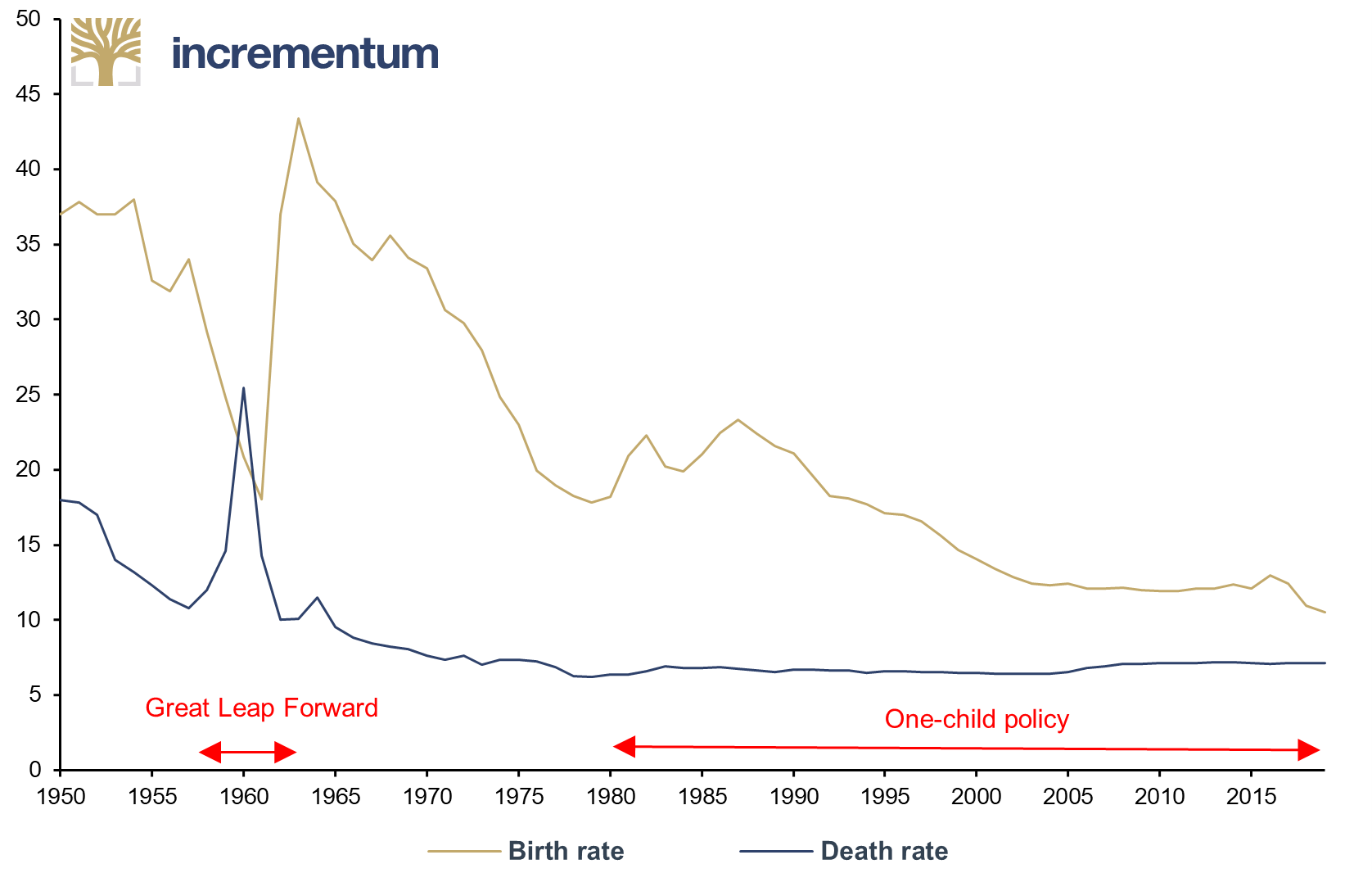

The policies of the Great Leap Forward were abandoned in the early 1960s, and the Chinese economy made a brief return to what was relative normalcy for the period. The government renewed calls for families to have as many children as possible, which had been official policy since the founding of the People’s Republic in 1949. China’s fertility rate doubled between 1961 and 1963, and a decade-long “baby boom” ensued.

Birth rate and Death rate in China (per 1,000 inhabitants), 1950-2019

Source: National Bureau of Statistics China, Incrementum AG

Smaller families and the one-child policy

China’s population grew by 30% from 1963 to 1973, rising from 680mn to 880mn people in total. After a peak following the Great Leap Forward, birth rates naturally started to fall again. As noted by Heise, the decline was made more pronounced by changes in Chinese domestic policy in the early 1970s.[9] By that time Chinese policymakers had become concerned that China’s population was growing too quickly, and they began to discourage large families. The country’s well-known One-Child Policy came into effect in 1979 and contributed to birth rates remaining low.

The demographic dividend

The combination of developments during these three historical periods meant that from the mid-1970s China experienced a rapid fall in its dependency ratio. On the one hand, the number of retirees that China’s working-age population needed to support had been reduced due to the mass fatalities of the late 1950s. On the other, there were fewer children due to the recent fall in birth rates. Until the mid-1970s China’s dependency ratio was around 80; i.e., for every 100 persons of working age (15–64), there were 80 persons to be cared for. However, the dependency ratio fell drastically over the subsequent three decades to reach a historic low of just 36 in 2010. Alongside China’s political liberalization, this falling dependency ratio was a significant contributor to the country’s record-breaking economic growth.

Eastern Europe

As China underwent rapid development, political change was also underway within the Soviet bloc. The Berlin Wall fell in 1989. Eastern Europe was reintegrated into global trade, resulting in an additional 209 million working-age people becoming available to the global economy as a labor force.[10] The result was further disinflationary pressure as the world benefited from the productivity of these new workers, both through international trade and – in the case of many Western European countries – direct migration and the downward pressure it puts on wages, especially for low-skilled workers. For example, in 2018 roughly 1.5mn people from Eastern Europe were working in Germany[11] and around 1.1mn were working in the UK.[12]

The disinflationary forces of China and Eastern Europe

The opening up of China and Eastern Europe constituted an effective doubling of the labor supply available to the world’s advanced economies between the years 1991 and 2018.[13] This opening-up was accompanied by the lifting of barriers to international trade on a global level, through trade rounds in Uruguay in 1986 and Doha in 2001.

These political developments, and the demographic trends that accompanied them, were disinflationary for the following reasons. Statisticians measure inflation by calculating the change in the money price of the Consumer Price Index: a weighted basket of commonly purchased consumer goods and services. When other factors, such as the money supply, are constant, a larger quantity of consumer goods produced means there will be more goods on the market per unit of currency. This pushes down consumer goods prices, which lowers inflation. Post-1990s globalization was disinflationary because the efficiency it created through international division of labor brought about a worldwide surge in the production of goods.[14]

At the same time a falling global dependency ratio had a further disinflationary effect on the world economy.[15] In general, workers produce more than they consume – otherwise it would not be profitable to employ them – while dependents such as children and the elderly tend to consume but not produce. This means that when the share of people of working age increases, there is greater production relative to consumption, which pushes the price of goods down.

This relationship between dependency ratio and inflation, and its impact on the post-1990s period, has been demonstrated empirically by the work of Juselius and Takáts. They studied data from 22 advanced economies from 1955 to 2014 and found a significant relationship between a high dependency ratio and inflationary pressure. Juselius and Takáts conclude that the age-structure effect is forecastable. They see demographics as pointing to an increase in inflationary pressures over the coming decades.[16]

As we have seen, the disinflationary forces that resulted from a combination of political liberalization, free trade, and favorable demographics allowed headline inflation figures in advanced economies to stay low despite the massive monetary and fiscal expansion these countries undertook.[17] When analyzing the causes of inflation trends in the post-1990s period, Grendal and Ayers point to China’s ascension to the World Trade Organization (WTO) in 2001 as being particularly significant in creating disinflationary pressure.[18] Without globalization and favorable demographics, it is safe to say that inflation figures would have been a lot higher in the post-1990 period.

Rather than embracing the benefits of falling prices and reducing their national debt, developed economies instead chose to maintain historically high levels of government spending. Most continued to run persistent deficits, which had the effect of pushing government debt-to-GDP ratios to new all-time highs.[19]

Under normal circumstances, persistent deficits and accommodative monetary policy would have led to higher rates of inflation; but, as discussed above, inflationary pressures were offset by the disinflationary forces of globalization coupled with favorable demographics. Headline CPI figures therefore remained close to central bank target levels of 2–3%, and often fell below them.[20]

Chinese trade surpluses

Disinflationary trends were influenced further by the large trade surpluses that China started to run from the mid-2000s, which reached up to 8% of its GDP. The size of these surpluses was largely the result of the policies of the People’s Bank of China (PBoC), which aimed to maintain relative exchange rate stability with the US dollar.[21]

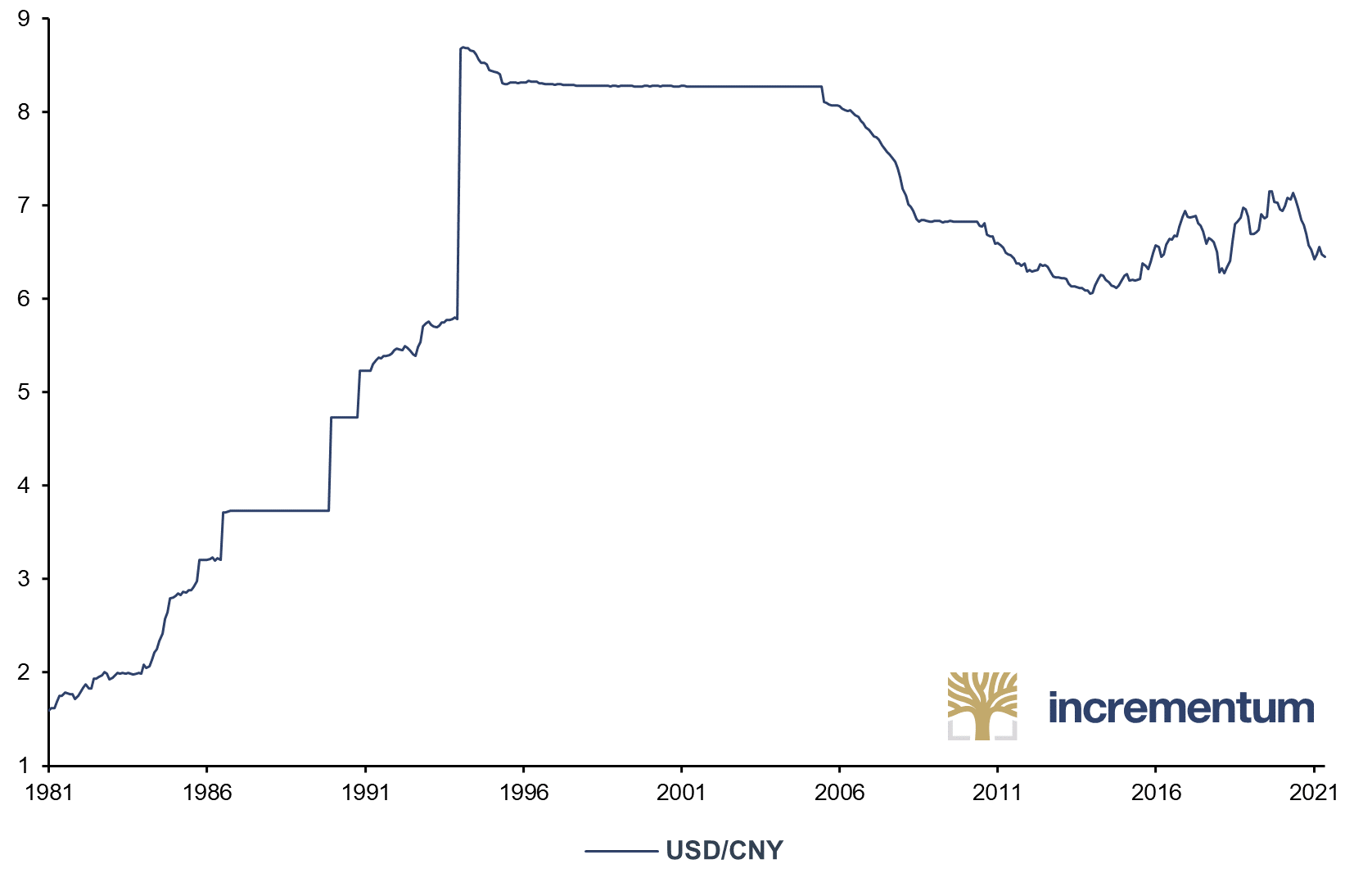

Between the start of the Reform and Opening-Up period in 1978 and 1997, the yuan underwent a radical revaluation. According to economist Arthur Kroeber, China had a severely overvalued exchange rate during the Mao era, reflecting the Communist economic principle that domestic investment in heavy industry, rather than international trade, was the route to wealth.[22] A strong currency allowed China to import expensive capital goods from other Communist states more easily.

However, following the introduction of the Reform and Opening-Up policies, the PBoC allowed the yuan’s exchange rate to fluctuate freely, resulting in a heavy devaluation from 1.5 to the US dollar in 1979 to 8.7 in 1997. The PBoC then started to control the value of the yuan to provide currency stability to international investors, initially maintaining an exchange rate of 8.7 yuan to the US dollar, and then allowing modest appreciation.

USD/CNY, 01/1981-05/2021

Source: Reuters Eikon, Incrementum AG

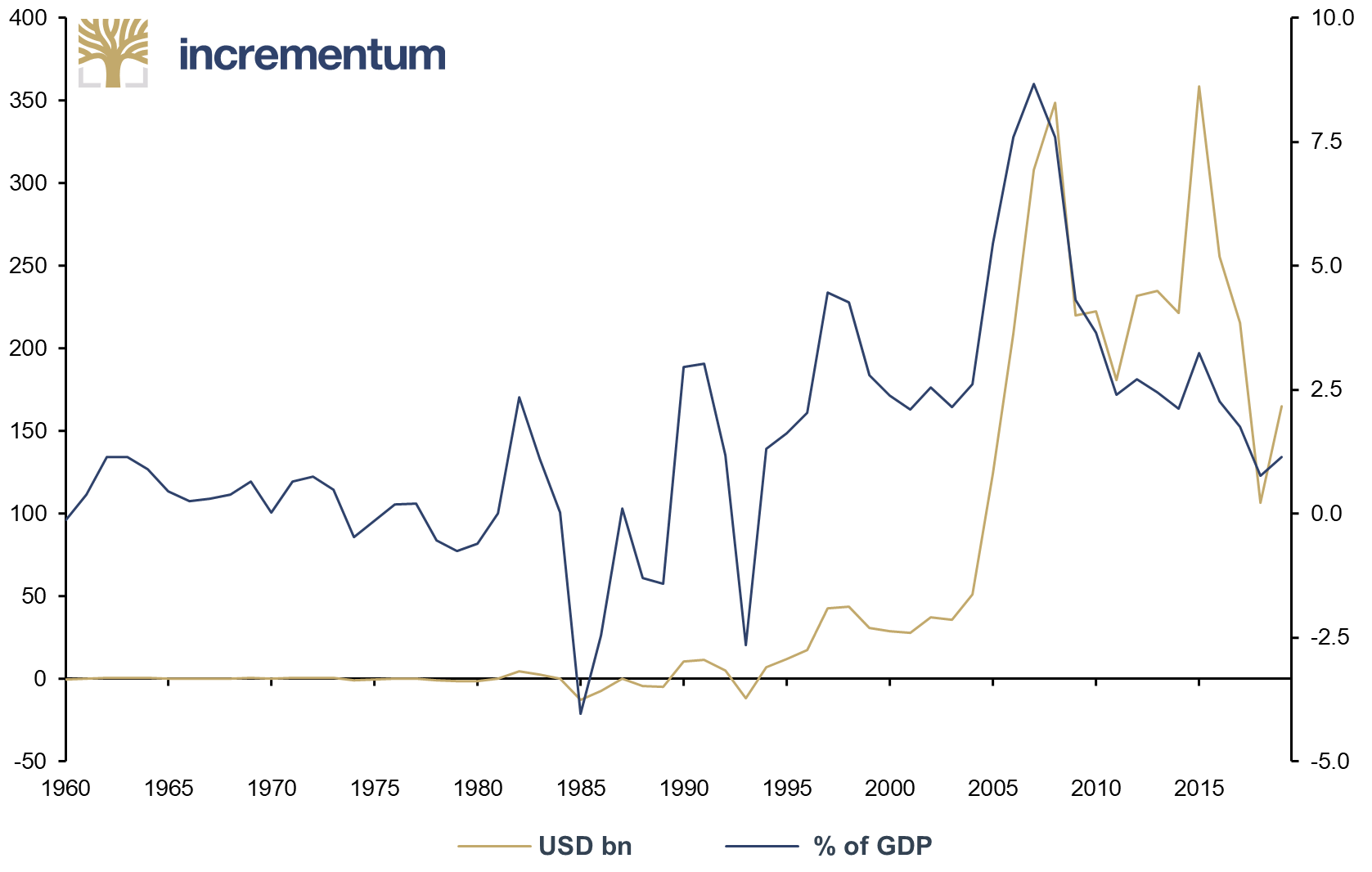

Whilst the PBoC’s policies helped to achieve relative exchange rate stability, the yuan was likely greatly undervalued relative to what its price would have been on the free market. The result was that China ended up consistently exporting more real goods to the rest of the world than it was importing, with the trade surplus being invested by the PBoC in US Treasuries.

By the late 2000s, China’s export surplus was the largest in the world, amounting to around 0.5% of global GDP. The countries to which China exported – primarily advanced economies – benefited from this effective subsidy to the price of their consumer goods. As a result of China’s exchange rate policies, it was effectively exporting price deflation to the rest of the world.

Trade Balance of China, in USD bn (lhs), and in % of GDP (rhs), 1960-2019

Source: Macrotrends.net, Incrementum AG

This dynamic was made possible by financial repression within China’s borders. Chinese bank deposit rates were held below the rate of domestic inflation from the mid-2000s, and foreign investment by Chinese citizens was limited by capital controls.[23] This meant that Chinese citizens took on the costs of subsidizing their exports to the rest of the world in the form of higher domestic inflation.

Favorable Conditions Are Starting to Reverse

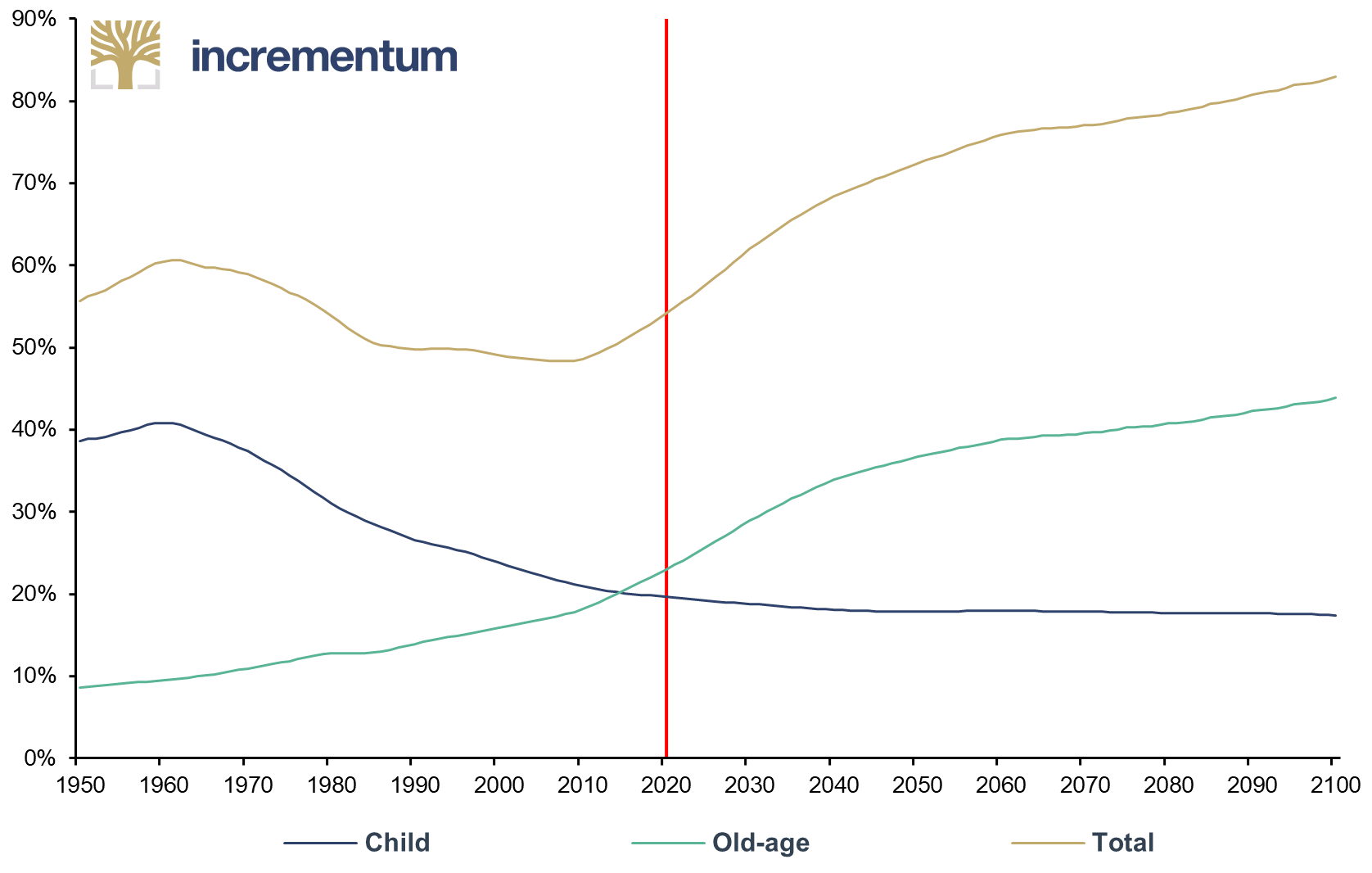

Today, the favorable demographic conditions that the world has enjoyed since the 1990s are starting to change. The population of the world is ageing, and this ageing is particularly pronounced in developed economies.

Age Dependency Ratios of High Income Countries, 1950-2100

Source: Engelgau, Michael et. al: Capitalizing on the Demographic Transition: Tackling Noncommunicable Diseases in South, 2011, p. 18, ourworldindata.org, UN, Incrementum AG

According to UN projections, the number of over-80s globally is forecast to triple between now and 2050.[24] This trend is of great economic significance given the over-80s age group’s vulnerability to diseases such as dementia that require a large amount of labor-intensive care to manage. Along with the growth in the number of elderly people, the number of dementia sufferers globally is forecast to almost triple between now and 2050 as populations age.[25]

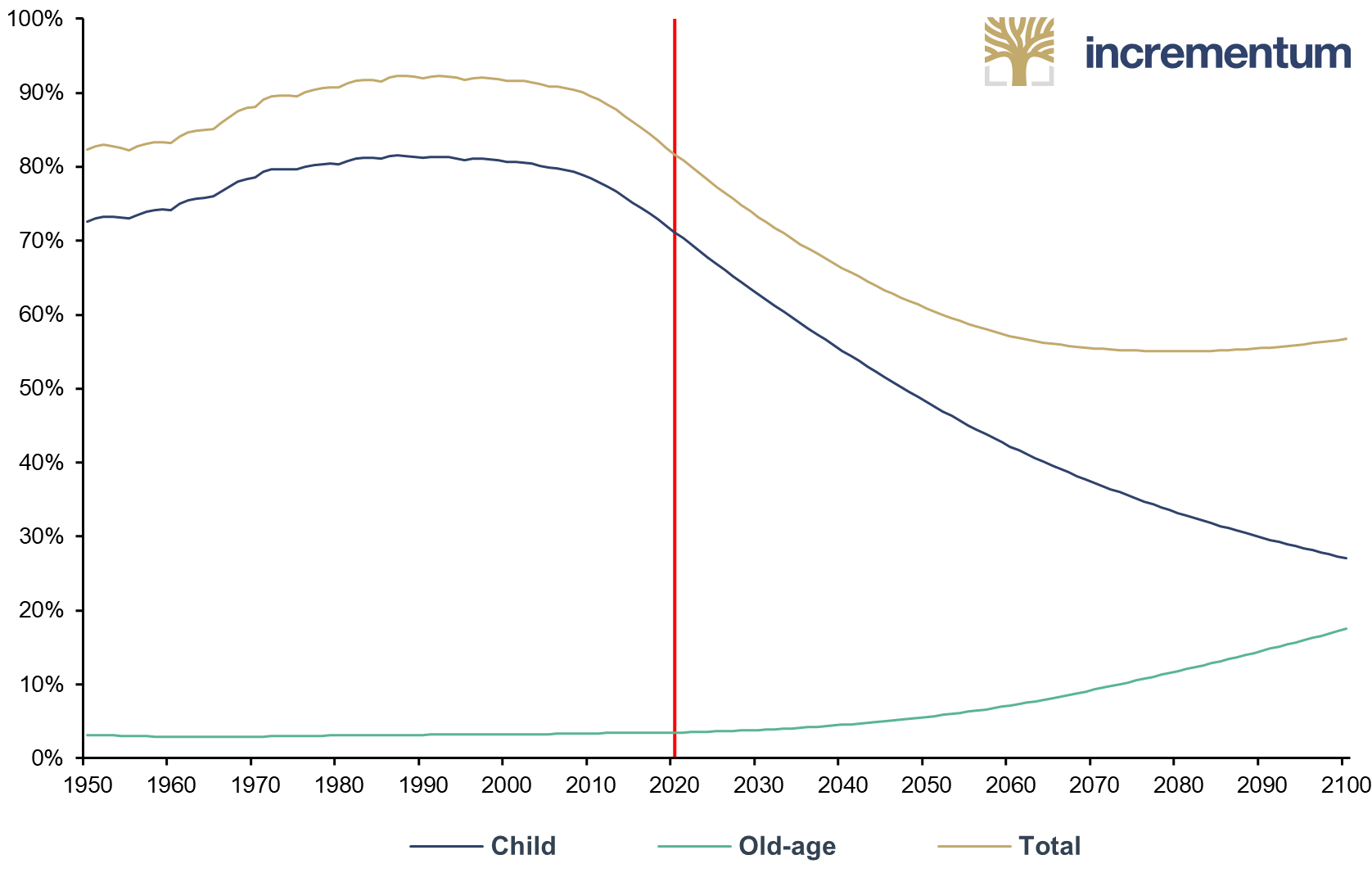

Age Dependency Ratios of Low Income Countries, 1950-2100

Source: Engelgau, Michael et. al: Capitalizing on the Demographic Transition: Tackling Noncommunicable Diseases in South, 2011, p. 18, ourworldindata.org, UN, Incrementum AG

Whilst there has been much talk about both negative and positive effects of the rise of automation and its impact on the labor market, it seems unlikely that technological advances will be able to replace the need for real human contact in the realm of caregiving in the foreseeable future.[26] This situation impacts on inflation, because the increased demand for labor in caregiving will bid labor away from other productive uses, reducing the supply of consumer goods and pushing up their prices.

Furthermore, the costs of caring for ageing populations will inevitably fall on governments, which will need to find ways to fund this additional spending when their national debts are already at record highs. It seems likely that there will be recourse to accommodative monetary policy to ease government debt burdens, which will act as a further inflationary factor.

In addition, various studies confirm a link between ageing and lower economic growth. For example, Chapter 3 of the 2014 World Economic Outlook by Callen et al. finds that per capita GDP growth is positively correlated with increases in the working-age population share and negatively correlated with increases in the elderly share.[27]

China’s Coming Demographic Deficit

As referenced above, China will be one of the countries most impacted by ageing, as the demographic dividend it has enjoyed in recent decades turns into a demographic deficit. The Chinese baby boomers of the 1963-1973 period that we described above are now starting to retire on a mass scale. The country’s proportion of over 60s is due to rise from 17% to 25% by 2030, with the trend continuing to rise toward 35% by the middle of the century.[28]

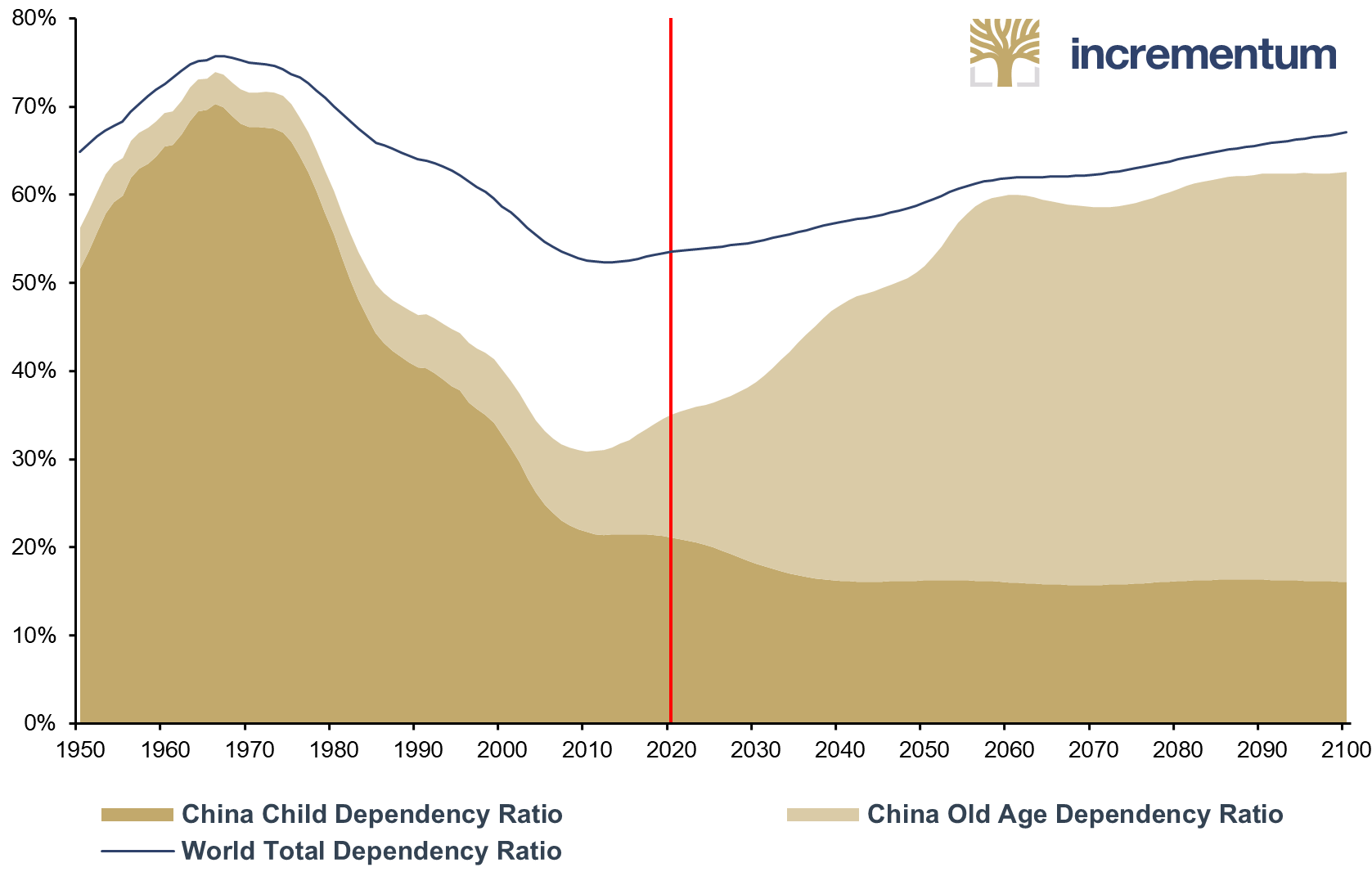

Due to the lack of children born during the One-Child Policy era – which only ended in 2015 – the ratio of dependents to the working-age population will undergo a dramatic shift, moving from current levels of around 41% towards 50% by the year 2030 and 75% by the middle of the century.

Age Dependency Ratios of China and the World, 1950-2100

Source: ourworldindata.org, UN, Incrementum AG

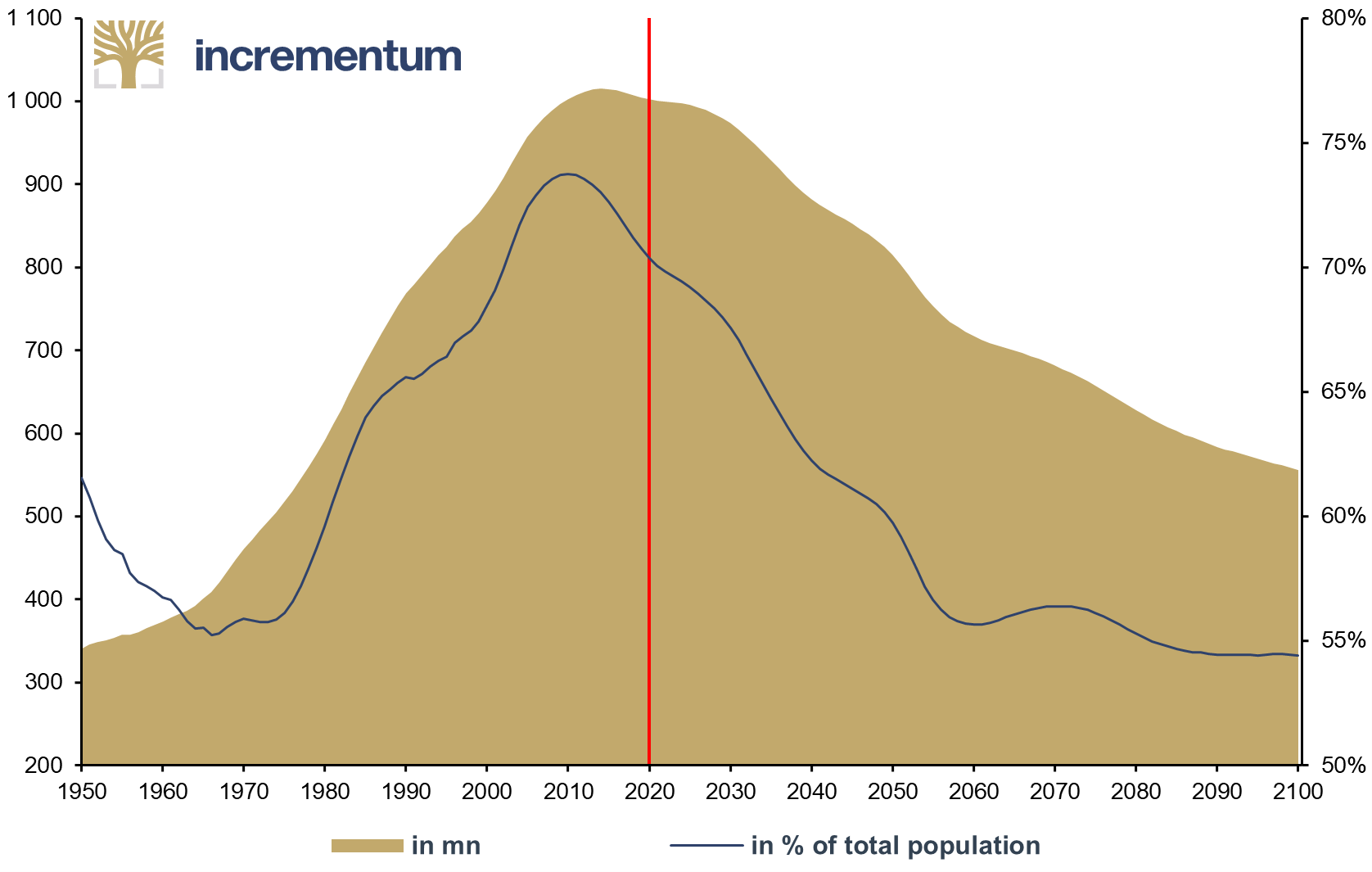

Along with the changes in the dependency ratio, the size of China’s working-age population has already peaked in absolute terms and is now starting to shrink. Projections are shown in the chart below.

Working-Age Population of China, in mn (lhs), and in % of total population (rhs), 1950-2100

Source: ourworldindata.org, UN, Incrementum AG

The fact that there will be fewer workers in China overall and that these workers will have to support an increasing number of dependents will put a drag on productivity and reduce the country’s current account surplus, potentially turning it into a deficit within a few years.[29] These factors will neutralize the disinflationary impact of China that the world has gotten used to in recent decades.

What About Demographic Dividends in the Rest of the World?

Whilst the average age of the world population is rising, demographic projections for some developing regions such as Africa and South Asia remain relatively favorable.[30] These regions will contribute significantly to global growth, but the scale of change we will see in the next couple of decades is unlikely to rival that of post-1990 China. The reasons for this are both political and geographic. Whilst China has benefited from both a large population and relatively unhindered trade within its borders, South Asia and Africa are much more politically fragmented.

Goodhart and Pradhan provide the following analysis of the political obstacles to growth in India, which we believe apply to many parts of the developing world. They write:

“India will be able to attract global capital to its shores, but the lack of administrative capital and its system of democratic checks and balances will not allow a single-minded, China-esque model of growth to materialise. India’s administrative capital is starting off from an extremely weak level and internal collisions within its multi-party system as well as between the states and the federal government make a coordinated policy of growth difficult to manage.” [31]

Whilst we would question the need for growth strategies to be centrally coordinated, we agree with the contention that competing local interests in many parts of the developing world will make it harder to achieve the pace of development seen in China.

Furthermore, in the case of Africa there are additional challenges related to the continent’s geography. While Africa has a similar population to China, it is roughly three times its physical size, giving it a much lower population density. As discussed in Tim Marshall’s book Prisoners of Geography, Africa also faces natural development challenges such as a lack of navigable waterways, which could connect inland populations to the rest of the country.[32] Geographic factors and low population density will make large-scale manufacturing across the African continent a difficult task on a scale that will significantly impact global price developments.

Why didn’t inflation happen in Japan?

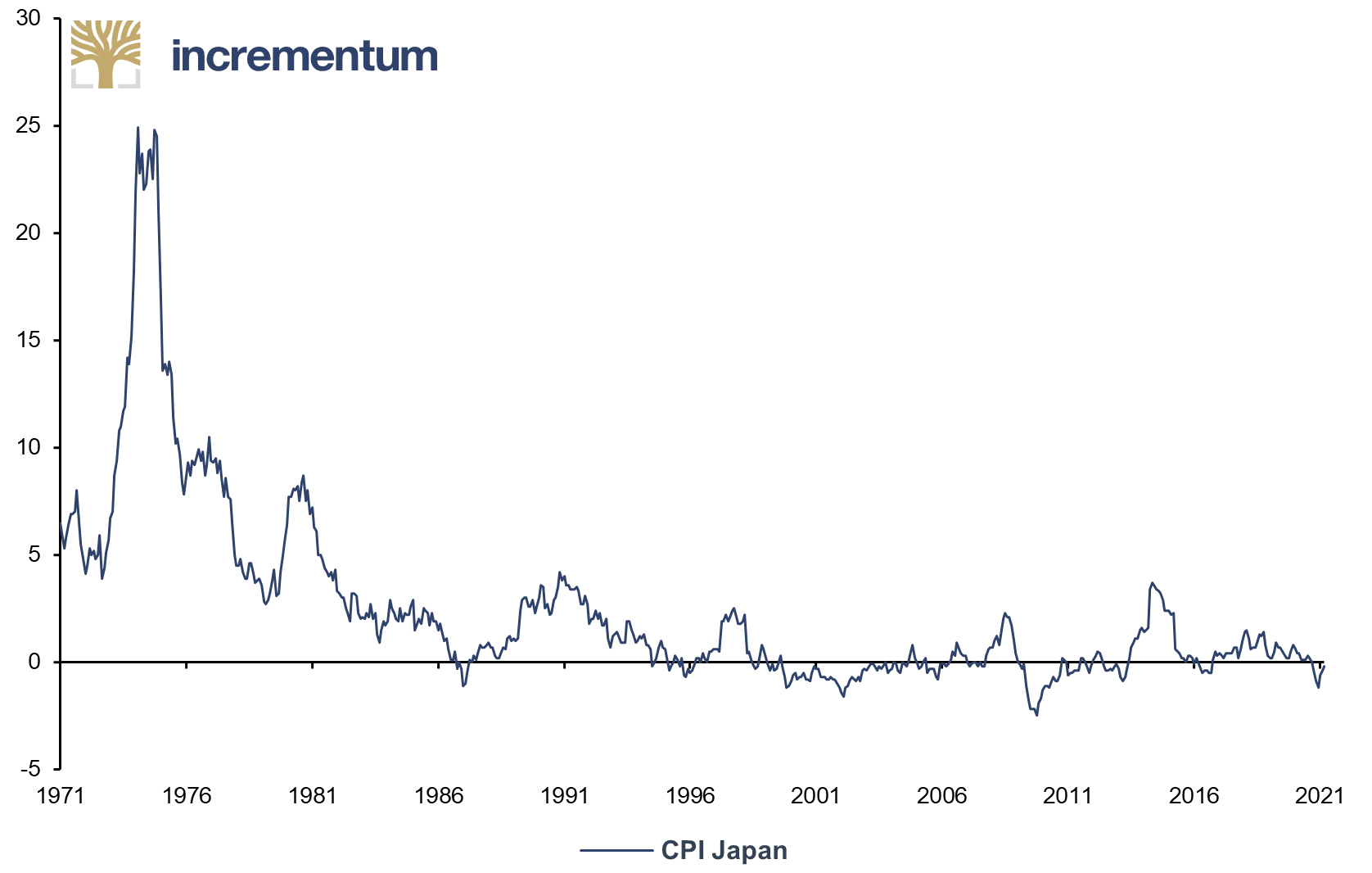

If ageing is inflationary, then why is it that the Japanese economy has experienced very low inflation – averaging 0.5% per annum – over the last couple of decades as its population has aged?

CPI Japan, in %, 01/1971-03/2021

Source: Reuters Eikon, Incrementum AG

While the shrinking of Japan’s workforce was indeed inflationary, Japan was a particular beneficiary of the global demographic dividends we describe in this chapter. From the 1990s Japanese corporations engaged in a large investment drive that allowed them to increase domestic worker productivity through outsourcing. Japan’s proximity to a booming China, from which it receives around a quarter of its imports[33], played an important role in buoying its economy and preventing inflation. As Goodhart and Pradhan write, “Japan’s labour force was shrinking just as the world became overflowing with cheaper but efficient labour.” [34]

In addition, Japanese monetary policy was much less expansionary than is commonly believed. As Lyn Alden points out in her article Economic Japanification: Not What You Think – despite huge expansions in Japan’s base money supply – from 2000 to 2020 broad money supply growth averaged just 2.9% per year, compared to 5.5% for the Euro Area and 6.2% for the United States.[35] It is broad money supply rather than base money supply that has a direct impact on consumer prices. It is our view that global deflationary trends and low money supply growth are better explanations of Japan’s low post-1990s inflation than ageing demographics.

When we compare Japan’s situation to the global economy today, we see that the economies that make up the global manufacturing complex are now ageing together. This limits the ability of developed economies to pursue a Japan-style strategy of expanding supply chains to developing economies with abundant labor.

Alongside demographics, there are additional reasons why Japan’s ability to accrue high levels of government debt without suffering high inflation will not be repeatable in other developed economies such as the US. As Luke Gromen writes:

“Japan is a current account surplus, internally-funded nation, non-reserve currency issuing nation with a massively positive Net International Investment Position (NIIP) as a % of GDP. In contrast, the US has the biggest Current Account deficit in the world, the US has historically been externally-funded, the USD is the global reserve currency, and the US has a massively negative NIIP (-62% of US GDP).” [36]

Conclusion

The advantage of studying demographics is that they are relatively predictable: If one knows the fertility rate at a given time, it is possible to predict the age make-up of a country’s population decades into the future with a relatively low margin of error.

As we have seen, the world has just been through an era where demographic and political conditions were highly favorable to economic growth, but our analysis suggests that era is now coming to an end.

As the world ages, the disinflationary forces resulting from favorable demographics that we have become used to are starting to reverse. These developments will contribute to causing the global pendulum to swing from lower to higher inflation in the coming decade.

[1] Fouquin, Michele and Hugot Jules: “Two Centuries of Bilateral Trade and Gravity Data: 1827-2014”, CEPII Working Paper, May 14, 2016; Our World in Data: Trade and Globalization

[2] Government spending as a percentage of GDP has not changed substantially since the 1970s in most developed economies. For figures see Our World in Data: Government spending: 1880 to 2011

[3] See Kroeber, Arthur R.: China’s Economy: What Everyone Needs to Know, 2016

[4] Dependents are defined as those under 15 and over 65.

[5] See Bloom, David E., David Canning, Guenther Fink, and Jocelyn E. Finlay: “Does Age Structure Forecast Economic Growth?”, NBER Working Papers, July 2007

[6] Grindal, Alejandra and Ayers, Patrick: “Demographic Demise or Opportunity?”, Ned Davis Research Group, September 21, 2017, p. 12

[7] Kroeber, Arthur R.: China’s Economy: What Everyone Needs to Know, 2016, p. 164

[8] See Yang, Jisheng: Tombstone: The Untold Story of Mao’s Great Famine, 2012

[9] See Heise L.: China’s baby boomers, World Watch, January-February 1988

[10] Goodhart, Charles, and Manoj Pradhan: The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, 2020, p. 2

[11] See “Arbeitsmarkt: Osteuropäer füllen Lücken” (“Labor market: Eastern Europeans fill gaps”), Deutsche Welle, October 7, 2018

[12] See “80% of Britain’s 1.4m eastern European residents are in work”, July 10, 2017

[13] Goodhart, Charles, and Manoj Pradhan: The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, 2020, p. 3

[14] See Statista.com: “Trends in global export volume of trade in goods from 1950 to 2019”, January 4, 2021

[15] See Our World in Data: Age dependency ratio projected to 2100, World

[16] See Juselius, Mikael and Takáts, Előd: “The Age-Structure–Inflation Puzzle”, Bank of Finland Research Discussion Paper No. 4, 2006

[17] See Kodaki, Mariko and Manabe, Kazuya: “No end in sight for record-high public debt fueled by COVID-19”, NIKKEI Asia, October 25, 2020

[18] Grindal, A. and Ayers, P.: Demographic Demise or Opportunity?, Ned Davis Research Group, September 21, 2017, p. 22

[19] See Kodaki, Mariko and Manabe, Kazuya: “No end in sight for record-high public debt fueled by COVID-19”, NIKKEI Asia, October 25, 2020

[20] See Macrotrends: OECD members Inflation Rate 1960-2021

[21] Kroeber, Arthur R.: China’s Economy: What Everyone Needs to Know, 2016, p. 141f.

[22] Kroeber, Arthur R.: China’s Economy: What Everyone Needs to Know, 2016, p. 142

[23] Kroeber, Arthur R.: China’s Economy: What Everyone Needs to Know, 2016, p. 132

[24] See UN: “World Population Aging”, 2017

[25] See Pratchett, Terry: “A global assessment of dementia, now and in the future”, The Lancet, September 5, 2015

[26] See Goodhart, Charles, and Pradhan, Manoj: The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, 2020, p. 63

[27] See Yoon, Jong-Won, Kim, Jinill and Lee, Jungjin: “Impact of Demographic Changes on Inflation and the Macroeconomy”, IMF Working Papers, November 201427

[28] Statista: Share of population aged 60 and older in China from 1950 to 2010 with forecasts until 2100; A recent PBoC study therefore recommends that the government encourages Chinese to have families with three or more children. See “China population: what’s driving central bank concern about the nation’s ageing workforce?”, SCMP, April 25, 2021, “关于我国人口转型的认识和应对之策”, PBC Working Paper, No. 2021/2, March 26, 2021 (published in Chinese).

[29] See “China may soon run its first annual current-account deficit in decades”, The Economist, March 16, 2019

[30] See Subrahmanyam, Sanjay et al.: “India – Demographic trends”, Encyclopedia Britannica; Bloom, David, Kuhn, Michael and Prettner, Klaus: “Africa’s prospects for enjoying a demographic dividend”, voxeu.org, October 20, 2016

[31] Goodhart, Charles, and Pradhan, Manoj: The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, 2020, p. 159

[32] See Marshall, Tim: Prisoners of Geography, Chapter 5, 2016

[33] See Watanabe, Akira et al.: “Japan – Trade in Japan”, Encyclopedia Britannica

[34] Goodhart, Charles, and Manoj Pradhan: The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, 2020, p. 142

[35] See Alden, Lyn: “Economic Japanification: Not What You Think”, Lyn Alden, Investment Strategy

[36] Gromen, Luke: “Eagle Pointe 63 (1)”, March 25, 2021