De-Dollarization 2021: Europe Buys Gold, China Opens a Digital Front

“For almost 60 years, the world complained but did nothing about it. Those days are over.”

Stephen Roach

Key Takeaways

- China is working on all fronts to undermine the hegemony of the US dollar. Russia and Europe are as well benefiting from this.

- The digital yuan has come a long way – but the fact that China is using the currency as a surveillance tool puts many off. What will Europe and the US do?

- The Biden administration has already set its sights on the digital yuan, but the Federal Reserve is still hesitant about a digital dollar.

- Central banks around the world continue to buy gold – especially in Eastern Europe. The euro could emerge stronger from the crisis.

New Love Does Not Rust

Fifty years. That is how long Saudi Arabia wants to guarantee to supply emerging superpower China with “black gold”. This was the statement by the CEO of the Saudi oil company Saudi Aramco, Amin Nasser, at the China Development Forum at the end of March. He called China’s energy supply a “top priority” for his company.[1] It is another step by Saudi Arabia towards their new love: China.

Saudi Arabia is the largest oil producer in the world. China is the largest importer. The Saudis are China’s most important supplier – but Russia is always hot on their heels. In a world increasingly characterized by the shift to renewable energy, the Saudis’ promises to Beijing seem a bit odd. But one should not make the mistake of underestimating their importance. Ever since Washington signed on to its infamous petrodollar pact with Riyadh in the 1970s, the oil trade has been of elemental importance to the world’s monetary operating system. It is not so much who buys oil or how much, but with what currency they buy it.

In previous issues of the In Gold We Trust report we have described in detail the dissatisfaction of Europe, Russia, China and Iran with having to trade oil in US dollars.[2] Europe and China do not understand why they should have to depend on Washington. Iran does not, in any case. But Saudi Arabia has a special role to play in this game, which is increasingly turning into a conflict between Washington and Beijing. China now wants to turn its currency into a “petroyuan”. And Saudi Arabia is finding it increasingly difficult to deny its most important customer this wish. There is still no official confirmation that the two nations trade some of their oil in the Chinese currency. Riyadh does not yet allow itself to provoke Washington in this way. But Saudi Aramco’s announcement that it will soon issue yuan bonds tells the whole story.[3]

This is another significant step toward de-dollarization – the slow but steady move from a system with a single world reserve currency to a multipolar world in which the euro and yuan play supporting roles alongside the US dollar.

However, the US has so far showed no signs of giving up its “exorbitant privilege” and saying goodbye to the advantages that the US dollar grants it. And China is pursuing several goals at once: developing its financial center; strengthening its own currency, the renminbi (yuan), in international trade; and expanding its economic dominance in Asia. Officially, China has wanted a supranational solution to the reserve currency issue since 2009,[4] but its actions tell a different story.

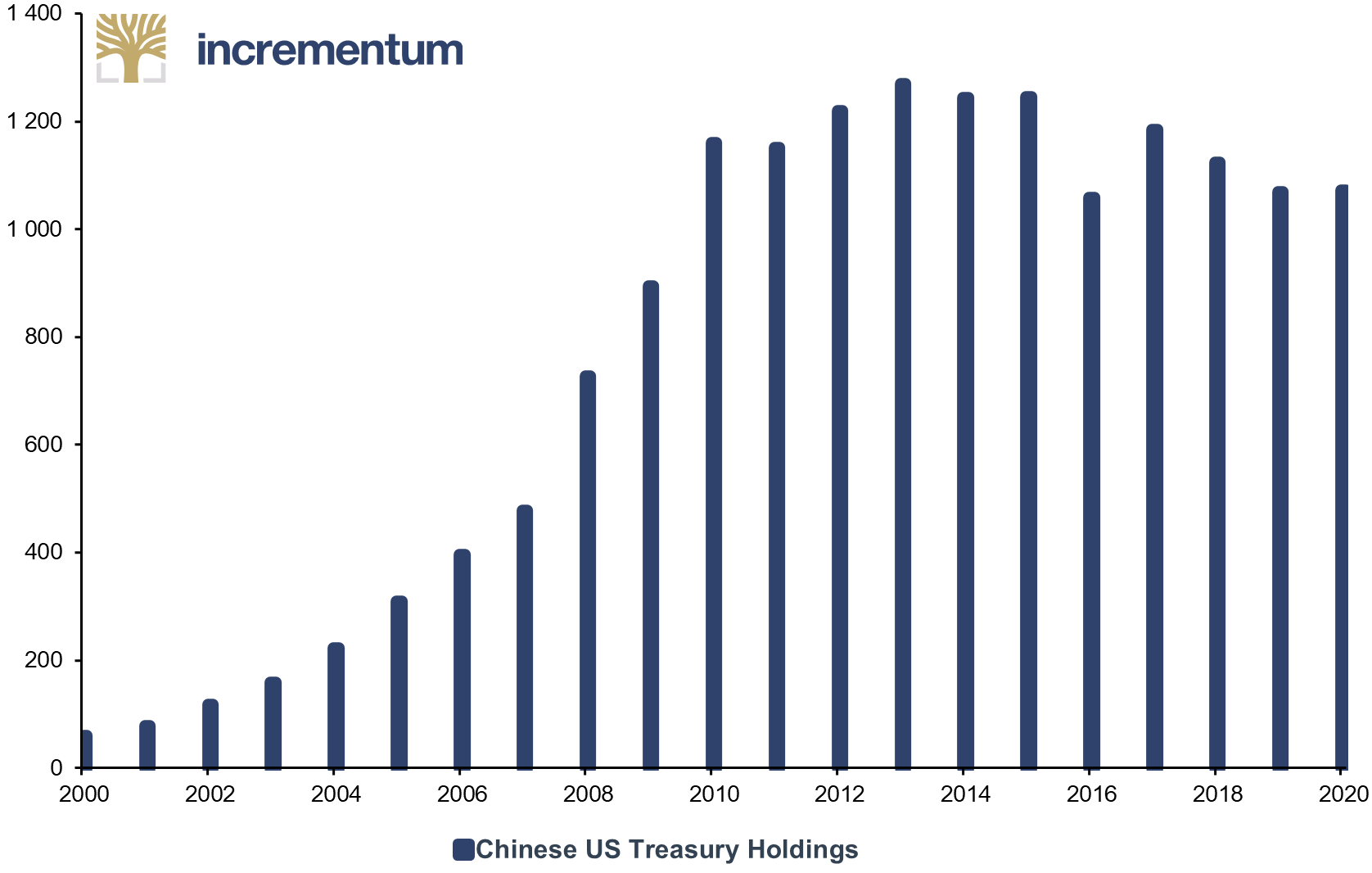

The aim is to gradually bring the renminbi on a par with the US dollar and the euro. This goal is a long way off; only a very small part of international reserves is currently held in the Chinese national currency. But Beijing has improved its position in recent years through clever maneuvers in the oil and gold trade. The central bank’s first verbal assault on the US dollar monopoly came in 2009 and was followed four years later by an announcement that China would no longer accumulate US bonds. Then, in September 2014, China launched a gold fixing in yuan.[5] Four years later, the basis for oil trading in the Chinese national currency was laid.[6]

Chinese US Treasury Holdings, in USD bn, 2000-2020

Source: Reuters Eikon, Incrementum AG

Now the digital battle has started. China is leading in the race to digital central bank currencies (CBDC). Europe and the US are lagging. In this chapter we document how the battle for dominance in the field of currencies has evolved over the past year and the role gold plays in it. And how and why the digital front is rapidly becoming the most important one. The focus remains on the conflict that will likely occupy us for generations to come: the US versus China.

China and Russia Are Driving De-Dollarization

At the end of 2020, the world was again entertained as US President Donald Trump was ushered out of office, replaced by Joe Biden, Barack Obama’s vice president. Around the globe, much has been said about the differences between Trump and Biden, but regular readers of the In Gold We Trust report know that it basically does not matter who sits in the White House. The long-term conflicts between the world’s major power centers are hardly affected by US elections.

It is no wonder that Moscow and Beijing have continued to move closer together after Biden’s election, even if the supposedly much more aggressive Trump is now history. At the end of March, Russian Foreign Minister Sergei Lavrov was in China, and even the Western news agencies reported on the talks in the first paragraphs of their articles:

“Russian Foreign Minister Sergei Lavrov began a visit to China on Monday with a call for Moscow and Beijing to reduce their dependence on the U.S. dollar and Western payment systems to push back against what he called the West’s ideological agenda.” [7]

The relationship between Russia and China is currently better than ever before in history, Lavrov said:

“The international situation is undergoing profound changes, with new centres of economic, financial and political influence growing stronger. (…) However, these objective developments, which are leading to the formation of a truly multipolar and democratic world, are unfortunately being hindered by Western countries, particularly the United States. (…) They seek to continue to dominate at any cost on global economy and politics and impose their will and requirements on others.” [8]

And, lest anyone forget what it is all about, the Russian foreign minister added:

“We need to reduce sanctions risks by bolstering our technological independence, by switching to payments in our national currencies and global currencies that serve as an alternative to the US-Dollar. (…) We need to move away from using international payment systems controlled by the West.” [9]

The talks between Lavrov and Chinese Foreign Minister Wang Yi were preceded by an unsuccessful rapprochement between Washington and Beijing. However, Beijing is always more reserved than Moscow when it comes to differences of opinion with Washington. Nevertheless, it is clear that Washington’s claim to sole monetary power is no longer acceptable. A Chinese Foreign Ministry spokeswoman said after the meeting: “China and Russia always stand together in close cooperation, firmly reject hegemony and bullying practice, and have become a major force for world peace and stability.” [10]

In addition to China and Russia, which have been expanding bilateral trade in their own currencies for years and already conduct at least a quarter of cross-border business in rubles and yuan,[11] Iran and NATO member Turkey also belong to the club of US dollar opponents.[12] It is also striking that Lavrov, in addition to his mention of “ our national currencies”, also speaks of “global currencies that serve as an alternative to the dollar”, which clearly refers to the euro. The latter is increasingly used in trade between states that want to move away from the US dollar. Russia holds most of its currency reserves in euros, although relations with the EU remain strained. Apparently, the long-term ties have not been broken despite the conflict over Crimea and the European sanctions.

After all, Russia’s President Vladimir Putin even said in 2010 that Russia wanted to join the euro one day.[13] And earlier this year, he underscored his desire to improve relations with Europe again:

“Of course, Western Europe and Russia should be together. Today’s situation is not normal. (…) If we can rise above the problems of the past, then a positive phase of relationships would await us. (…) But love is impossible if it is only declared by one side. It should be mutual.” [14]

Russia followed up its words with deeds and is currently preparing to issue a euro bond.[15] Russia is also the only big country where de-dollarization is a matter of state policy and where the state media celebrates every sale of US bonds.[16]

…And the Euro Benefits

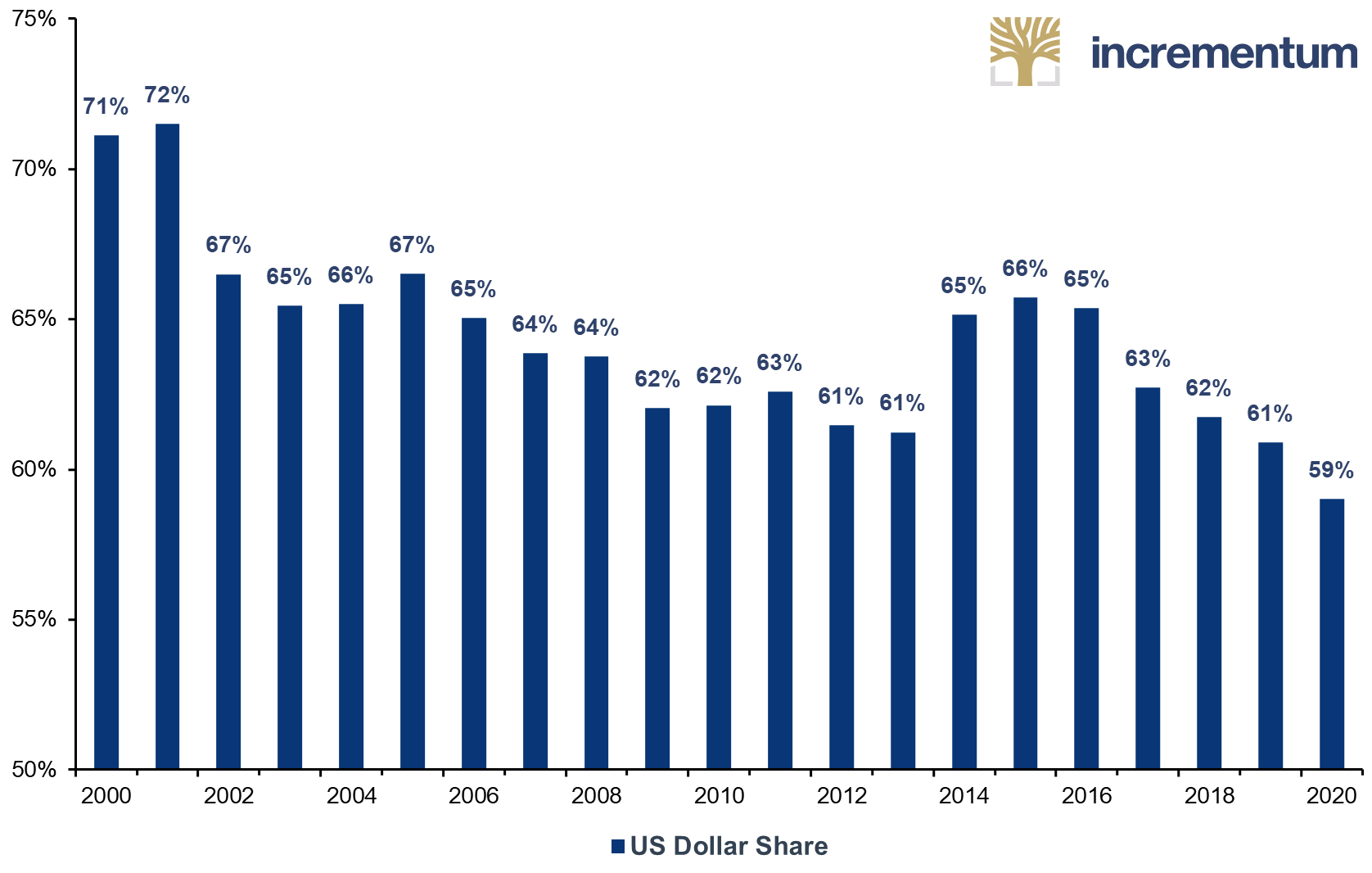

In general, the euro always benefits as a neutral third currency when members of the anti-US dollar club do not want to resort to their own currencies. Like the US dollar, the euro offers a stable, widely accepted alternative; and the euro is the only currency that has been able to establish itself to some extent alongside the US dollar. However, it has always ranked second by some margin. Two-thirds of the international bond markets are denominated in US dollars, and three-fifths of all cross-border payments are made in the US currency.[17]

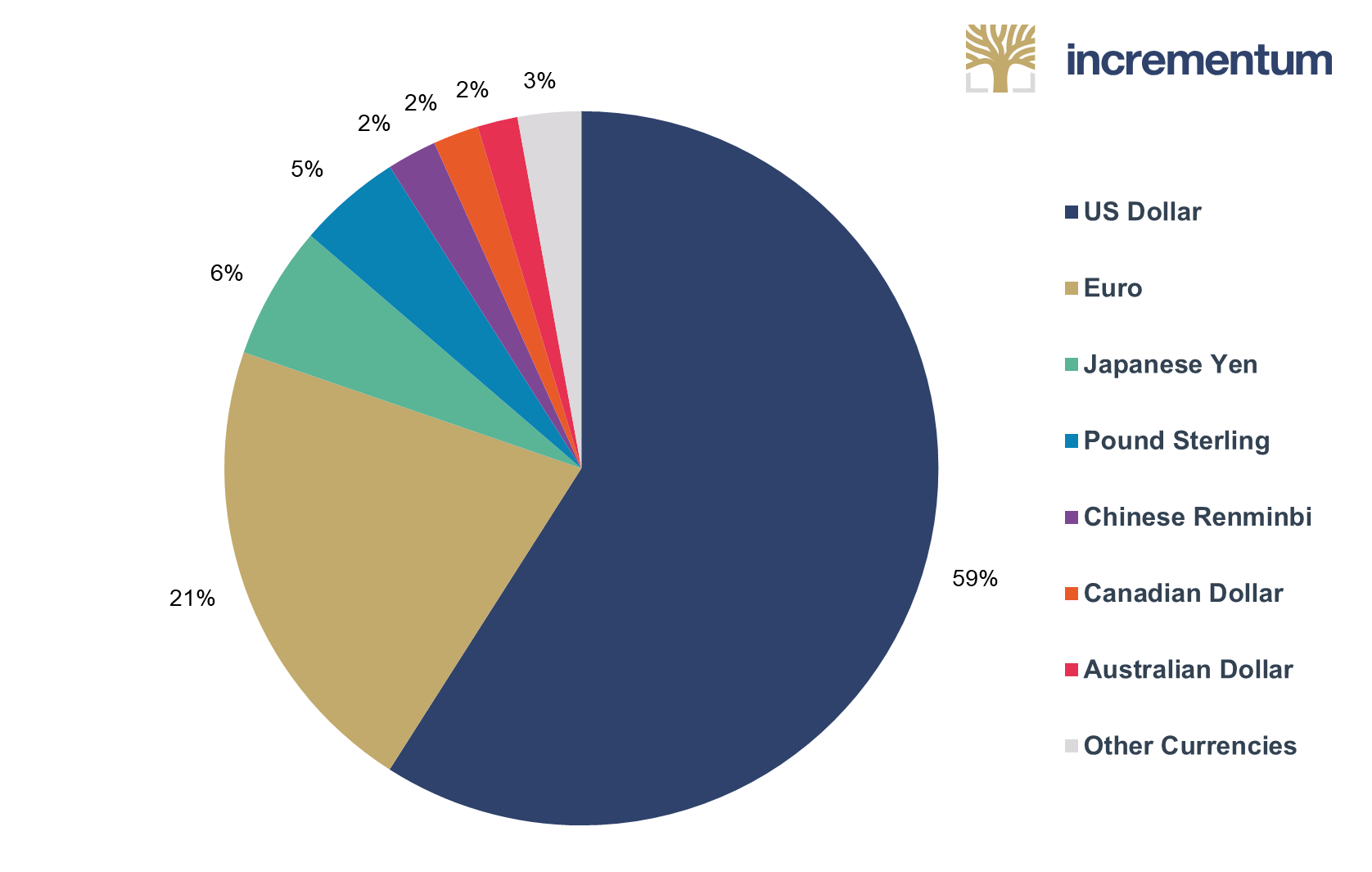

But change is happening. In March, the International Monetary Fund (IMF) reported that the share of US dollars in international currency reserves has recently fallen significantly to a level last seen in 1995. As a result, the US dollar currently accounts for around 59% of currency reserves. The share of the euro has risen from 20.5% to 21.2%, and that of the yuan from 2.1% to 2.3%. (At the end of 2019, the Chinese currency was still at 1.9%.) Canadian banker Bipan Rai of CIBC put it this way: “This is a slow burn theme, but we are of the view that we’re eventually headed into a ‘multiple reserve currency’ framework over time.” [18]

US Dollar Share of Global Reserve Currencies, 2000-2020

Source: IMF, Incrementum AG

We share this assumption. The fact that, alongside Russia, China is now also issuing eurobonds says a lot.[19] And Brussels’ ambitious plans to issue joint bonds of the euro countries on a grand scale for the first time in the wake of the Covid-19 crisis could further strengthen the euro’s position. Without common eurobonds, the European currency will be doomed to be number two forever.[20] The new EU Covid-19 recovery fund “will facilitate diversification out of the US dollar by offering liquid, high-rating, euro-denominated debt” [21], said Valentin Marinov, an analyst at French bank Credit Agricole.

The fact that the Europeans do not use the euro as an instrument of their power, as the Americans do, also makes the euro attractive to China, Russia and other countries. In the words of Vladimir Zotov, a director of the Ural Bank for Reconstruction and Development, “If exports and imports between them are more or less the same, it does not matter that much which currency is used. The countries must agree that both their national currencies are equal, or find a common currency, like the Euro.” [22]

That Europe itself has been working for decades to break away from the overpowering US and at least pay for its own imports and exports in euros is something we have known at least since former EU Commission President Jean-Claude Juncker’s legendary farewell speech in September 2018:

“It is absurd that Europe pays for 80% of its energy import bill – worth 300 billion euro a year – in US dollars when only roughly 2% of our energy imports come from the United States. (…) The euro must become the face and the instrument of a new, more sovereign Europe.”[23]

The End of the US Dollar – Yet Again?

The idea that the US dollar could be replaced as the world’s reserve currency is certainly not new. There are new proponents of that idea in every financial crisis – even in the US itself, where there is more freedom of speech than in Russia, China or Saudi Arabia. At the height of the Covid-19 crisis, it was Yale economist Stephen Roach who attracted attention with a particularly negative US dollar scenario. The “era of exorbitant privilege is coming to an end”, the economist wrote in a Bloomberg article in June 2020: “For almost 60 years, the world complained but did nothing about it. Those days are over.” [24] The phrase exorbitant privilege was coined by former French Finance Minister and President Valery Giscard d’Estaing. He wanted to articulate how unfair it is that the US can simply print the world’s reserve currency, but other states cannot. In the eyes of Europeans, this has led to an inflated standard of living in the USA, at the expense of the rest of the world.

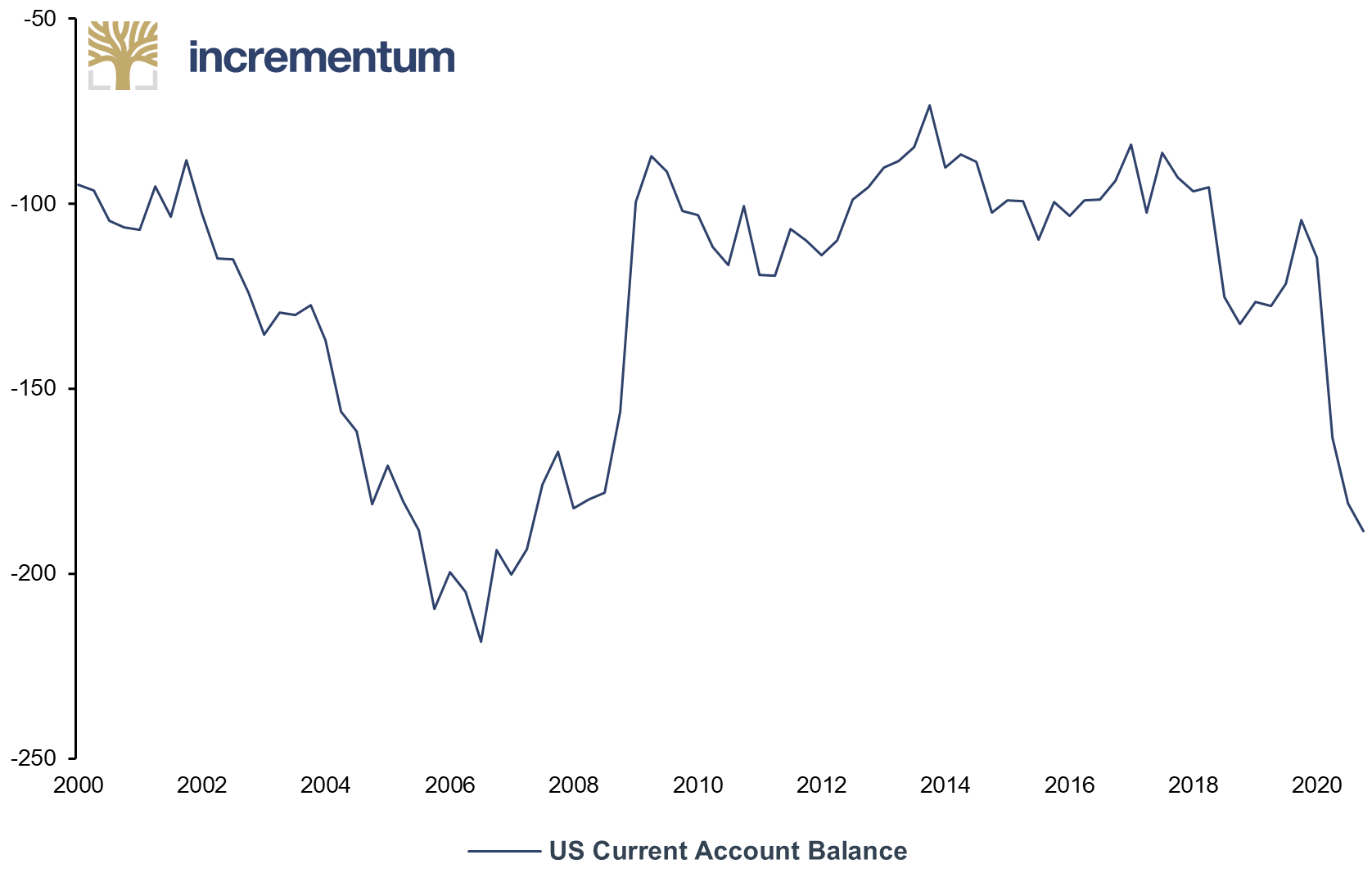

Roach argues that this period is now coming to an end. He expects a crash of the US dollar.[25] Like other economists outside the US, he observes first and foremost the enormous current account deficit of the United States and puts it in relation to the national savings rate: “The current-account deficit in the United States, which is the broadest measure of our international imbalance with the rest of the world, suffered a record deterioration in the second quarter.” [26]

For the savings rate, however, Roach looks not only at the deposits and savings balances of private households. He also deducts the US’s enormous budget deficits and comes to a sobering conclusion. Although the household savings rate has shot up in the pandemic, as opportunities for consumption have been constrained and the government has even sent out checks to households, the overall national net savings rate is negative, for the first time since the Great Financial Crisis of 2007/2008.

Roach expects the US trade deficit with the world to widen further and the euro to rise as a result. He expects the Federal Reserve to do little to counter the weakness of the US dollar. In fact, with its switch to “average inflation targeting”, the Federal Reserve has given itself the option of letting inflation rise above its 2% target on a sustained basis – to make up for lost inflation, so to speak.[27] The US trade deficit has reached levels we have not seen since the Great Financial Crisis. Roach expects the deficit to continue to grow.

US Current Account Balance, in USD bn, Q1/2000-Q4/2020

Source: Reuters Eikon, Incrementum AG

As of early April 2021, all US Covid-19 aid packages combined amount to about USD 5trn, or nearly a quarter of 2020 US gross domestic product. Roach notes:

“While not stimulus in the conventional sense, this fiscal injection breaks all modern records by a wide margin. The domestic saving rate, as a result, should plunge further below zero, putting the already wide current-account deficit under even more intense downward pressure.” [28]

The economist describes himself as a “euro skeptic”. But he sees the EUR 750bn recovery fund named “NextGenerationEU”, negotiated by Angela Merkel and Emanuel Macron during the Covid-19 crisis, as a decisive step toward a political union, which in turn supports the “most undervalued major currency in the world”, the euro. Economist and journalist Anatole Kaletsky even spoke of a “Hamiltonian moment” for Europe:

“Comparable to the 1790 agreement between Alexander Hamilton and Thomas Jefferson on public borrowing, which helped to turn the United States, a confederation with little central government, into a genuine political federation.” [29]

Stephen Roach considers the US dollar the “most overvalued major currency in the world”.[30] He expects a correction of about 35% versus other currencies during 2021: “I don’t think this is the end of the US dollar’s role as a dominant reserve currency – but it’s a step in that direction. I would flag the euro as the number one alternative, also the renminbi, gold and cryptocurrencies.” [31]

Roach received support at the end of March 2021 from none other than world-renowned US economist Kenneth Rogoff, who published a commentary entitled “The Dollar’s Fragile Hegemony” [32] In it, Rogoff argues that the appetite for US government bonds – and thus for the US dollar – has been insatiable so far, but that it need not always remain so. Especially not if China modernizes its monetary policy and relaxes its exchange rate regime:

“This does not mean that the Chinese renminbi will become the global currency overnight. Transitions from one dominant currency to another can take a long time. During the two decades between World Wars I and II, for example, the new entrant, the dollar, had roughly the same weight in central-bank reserves as the British pound, which had been the dominant global currency for more than a century following the Napoleonic Wars in the early 1800s.

Today, it seems to be an article of faith among US policymakers and many economists that the world’s appetite for dollar debt is virtually insatiable. But a modernization of China’s exchange-rate arrangements could deal the dollar’s status a painful blow.” [33]

The Role of Gold

Central banks remained net buyers of gold in 2020, but increasing their gold reserves was clearly not a priority for them. There was little buying, especially in the second half of the year, after Russia paused its gold purchases in April. Compared to 2019, gold purchases by central banks declined by almost 60%, but they were still net buyers. Yet, at only 270 tonnes, purchases were meager.[34] In 2019 they had amounted to almost 670 tonnes.[35]

However, it should not be forgotten that the price of gold reached a record high in the summer of 2020, which increased the metal’s importance for central banks’ reserves. Russia, which has always set the tone in terms of de-dollarization, now holds around 30% of its reserves in euros – and 22% each in gold and US dollars.[36]

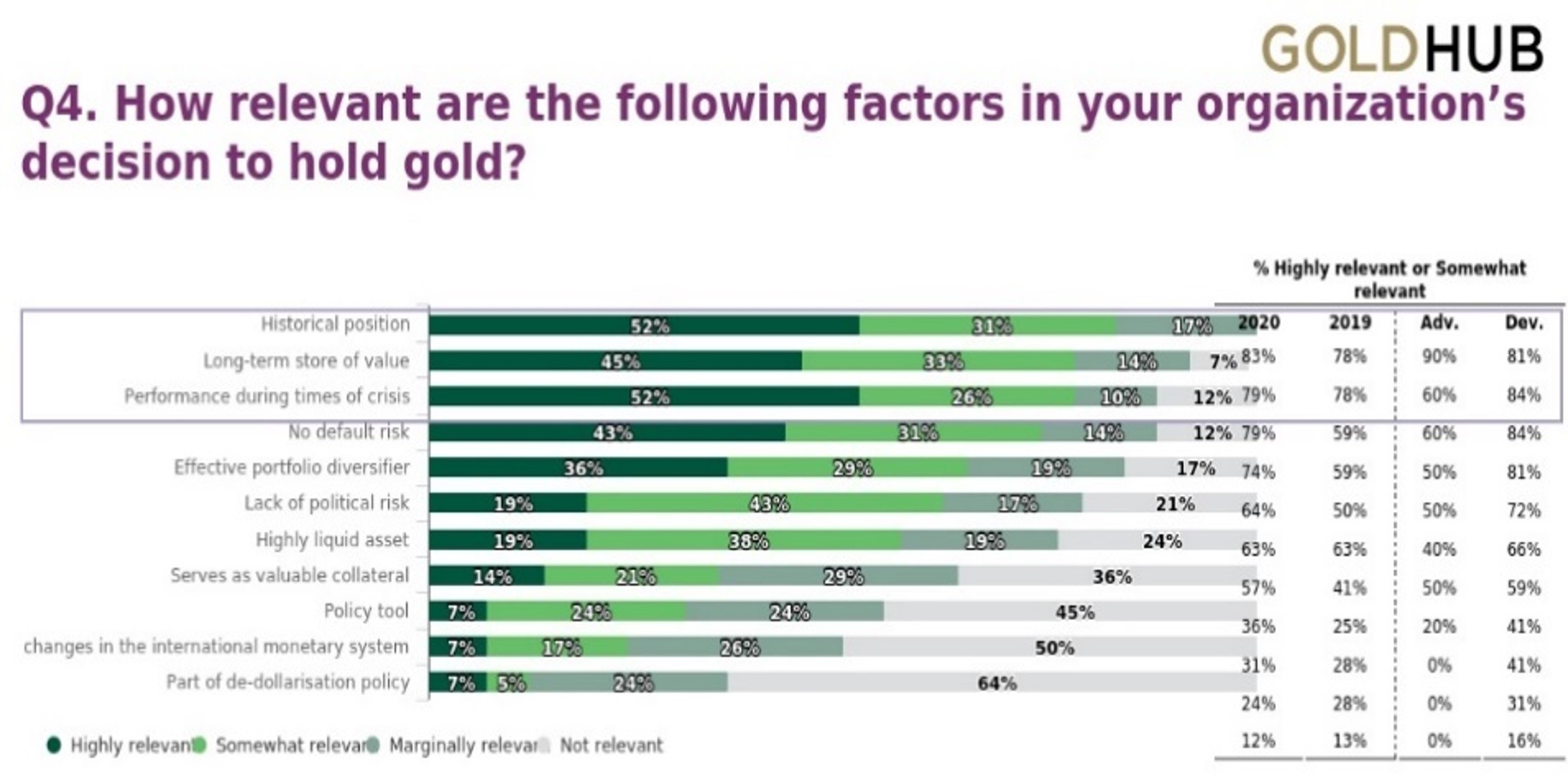

If you ask central bankers, as the World Gold Council did in 2020, why they hold gold, the answers are quite clear. Most relevant are the history of gold as a long-term store of value and the performance of gold in a crisis. However, 36% of central bankers openly stated that de-dollarization is of at least “marginal” relevance when buying gold.[37]

Source: World Gold Council

If you want to know more about why central banks buy gold, you can turn to the Polish central bank. It currently has around 230 tonnes in its vaults, after massive purchases in 2019. In the coming years, a further 100 tonnes are to be added, according to a statement from Warsaw in mid-March 2021.[38] The Polish central bank justifies their increase in gold reserves as follows: “Gold is the ‘most reserve’ of reserve assets: it diversifies the geopolitical risk and is a kind of anchor of trust, especially in times of tension and crises.” [39]

Now, you must know that Poland is not yet a member of the euro and that the euro countries together have more gold than any other currency area, including the US, which always ranks first in national statistics with 8,000 tonnes. Together, however, the euro countries own 12,000 tonnes, a figure that could grow with each new euro member. Hungary, as well not a member of the euro area, has not been idle, either, and has recently tripled its gold reserves. The country now holds 94.5 tonnes.

It is also no longer a secret that Europe, Russia, and China see gold as an alternative to the US dollar and have been eyeing the option of launching a new financial system based on gold for decades.[40] When the price of gold rose sharply in the summer of 2020, even Goldman Sachs analysts wrote:

“Real concerns around the longevity of the U.S. Dollar as a reserve currency have started to emerge (…) Gold is the currency of last resort, particularly in an environment like the current one where governments are debasing their fiat currencies and pushing real interest rates to all-time lows.“ [41]

Against this backdrop, it is highly interesting that voices have also recently been surfacing in the US advising the Federal Reserve or the US government to buy gold as part of the stimulus initiatives that are already underway. In the wake of the Covid-19 crisis, it was hedge fund manager Scott Minerd of Guggenheim Investments who raised this possibility.[42] But the idea is older and goes back to the (highly recommended) 2016 paper “Rumpelstiltskin at the Fed”, by former PIMCO strategist Harley Bassman.[43]

In it, he asks why the Federal Reserve – and other central banks – do not simply buy gold to stimulate inflation and the economy. After all, the quantitative easing that has been practiced up until now is often criticized because the money mostly gets stuck in the financial system and does not benefit consumers. Bassman’s proposal, based on stimulus programs from the Great Depression era, calls for the Federal Reserve to offer to buy gold from the public at a price well above the market price. Bassman cites USD 5,000 as a possible target price. He justifies this proposal as follows:

“A massive Fed gold purchase program would differ from past efforts at monetary expansion. Via QE, the transmission mechanism was wholly contained within the financial system; fiat currency was used to buy fiat assets which then settled on bank balance sheets. Since QE is arcane to most people outside of Wall Street, and NIRP seems just bizarre to most non-academics, these policies have had little impact on inflationary expectations. Global consumers are more familiar with gold than the banking system, thus this avenue of monetary expansion might finally lift the anchor on inflationary expectations and their associated spending habits.

“The USD may initially weaken versus fiat currencies, but other central banks could soon buy gold as well, similar to the paths of QE and NIRP. The impactful twist of a gold purchase program is that it increases the price of a widely recognized ‘store of value,’ a view little diminished despite the fact the US relinquished the gold standard in 1971. This is a vivid contrast to the relatively invisible inflation of financial assets with its perverse side effect of widening the income gap.” [44]

Of course, the idea of buying gold with freshly printed money to stimulate the economy is not new. Some call it “QE heavy”. True, it does not come up regularly in economists’ circles or in the mainstream media. But in Europe, too, it is talked about again and again. Back in November 2014, for example, then ECB Director Yves Mersch said that the ECB could buy gold as well as bonds to stimulate the economy.[45] And given the unorthodox approach of central banks since the Great Financial Crisis, which has escalated further in the Covid-19 crisis, no idea can simply be wiped off the table.

Why should not the US do what Russia and China have been doing for years, and what Poland and Hungary[46] and many other smaller countries are doing as well?[47]

We believe that both the ECB and the Federal Reserve are ready to buy gold as soon as they deem it opportune – and that the world will be shocked by this move. But even if a gold purchase would strengthen the role of the US dollar, this move to a neutral reserve asset, 50 years after Richard Nixon unpegged the US dollar from gold, would be a clear admission that the US dollar’s role as the sole reserve currency is over. This would also strengthen the euro, which is already backed by the world’s largest gold reserves.

Perhaps the US will fall back on their legendary pragmatism, skip gold, and go for Bitcoin. Our friend Luke Gromen recently voiced this idea:

“If I was working for the US government and they said, ‘Luke, what would you do to combat what China and Russia are doing with gold?’ It’s simple – I’d let Bitcoin run. I would have a harder reserve asset than gold and I would let it run. I would let it be and I would just stand aside, benevolent neglect. And I would let Bitcoin run.” [48]

The concept seems unquestionably exotic. But since the “world war of currencies” is increasingly being fought in the digital arena, nothing should be ruled out. After all, China also has a digital currency in its quiver. And it is further along than Europe or the USA.

China’s Digital Ambitions

“As China (and India) develop electronic, crypto, and peer-to-peer strategies, the epicentre of global economic power could shift.

China is working on a digital currency backed by its central bank that could be used as a soft- or hard-power tool. In fact, if companies doing business in China are forced to adopt a digital yuan, it will certainly erode the dollar’s primacy in the global financial market.”

Deutsche Bank

In February 2022, the world will once again be looking to China. That is always the case with sporting events of global significance: The host uses them to present its achievements on the world stage. At the 2022 Winter Olympics, to be held in the capital Beijing and elsewhere, one of these achievements will be the digital renminbi. No other country is further along in developing a central bank digital currency (CBDC) than China. There are several reasons for this.

- China sees the digital renminbi as another weapon in its fight against the dominance of the US dollar in Asia and the world.

- In the long term, China wants to replace the US as the global financial center and “banker to the world”.

- The digital renminbi is intended to give the Communist Party of China control over all payment flows and thus help perfect the monitoring of its own citizens.

- The digital renminbi is expected to break the dominance of the two previously used digital payment systems, Alipay and WeChat Pay.

- What is more, the digital renminbi is designed to ward off the threat posed by private currencies such as Facebook’s Diem and decentralized currencies such as Bitcoin.

China Continues to Expand Its Role as a Financial Center

The global Covid-19 pandemic has given a huge boost to digitization in general and, as it looks at the moment, has quite strengthened China. It has overtaken the US as the most important destination for foreign direct investment in 2020. Investments by foreign companies in the US in 2020 plummeted to USD 132bn, a drop of almost 50%, while those in China increased by 4% to USD 163bn.[49] Even the Wall Street Journal has written:

“The 2020 investment numbers underline China’s move toward the center of a global economy long dominated by the US – a shift accelerated during the pandemic as China has cemented its position as the world’s factory floor and expanded its share of global trade.” [50]

It is important to remember that we are talking about new inflows (flow). The amount of total investment in the US (stock) continues to exceed that in China many times over. But: Since peaking at USD 440bn in 2015, US foreign direct investment has fallen every year.

Bond investors are also discovering China. Many are looking east in search of yield. Foreign investors now hold Chinese government bonds worth almost USD 300bn. The PBoC reacted comparatively cautiously to the pandemic when it came to injecting money into the economy. Inclusion in global bond indices has also contributed to the growing appeal of the Chinese bond market, according to Citigroup. The bank’s analysts expect inflows of around USD 100bn a year over the next three years.[51]

Of course, the renminbi is also benefiting from growing demand from investors. It has long been known that Beijing wants to strengthen its currency wherever possible. As early as 2009, then central bank chief Zhou Xiaochuan openly complained about the dominant role of the US dollar in the world and called for a reform of the international monetary system.[52] Since then, the Chinese central bank has also been working on its digital currency. After seeing new records in foreign investment and demand for Chinese government bonds in 2020, the PBoC expressed satisfaction: “The allocation of the renminbi assets by foreign investors will be further facilitated.” And further, “making it possible for more foreign central banks and monetary authorities to hold renminbi [assets] as reserve assets.” [53]

USD/CNY, 01/2008-05/2021

Source: Reuters Eikon, Incrementum AG

To establish the renminbi as a long-term alternative to the US dollar, Beijing needs to create large and liquid bond markets. And that is exactly what Beijing is doing. True, it has only been seven years since China spooked investors by sharply devaluing its currency. But most analysts do not expect that to happen again and see China and the renminbi as an increasingly attractive place to invest.

China and the renminbi will only remain attractive in the long term if the central bank and government intervene less frequently, liberalize capital markets, and let the market determine the exchange rate. And all of that seems to be in the cards now, if you read the comments of analysts such as Gaurav Mallik, chief portfolio strategist at State Street Global Advisors:

“The inclusion of Chinese assets into major bond and equity indices is a very strong indication of the PBoC’s intentions around … the renminbi, and it clearly tells us that the central bank wants to move more towards liberalising its markets.” [54]

Central bank reserve managers are also looking for diversification opportunities and are increasingly turning to China’s bonds and its currency. However, the renminbi has not yet fully recovered from the shock of 2015 in terms of its international importance. Only 2% of global foreign reserves are held in renminbi, while about 60% are held in US dollars and 20% in euros. The share of the Japanese yen in reserves is also still more than twice as large as that of the Chinese national currency.

Global Reserve Currency Composition, Q4/2020

Source: IMF, Incrementum AG

What the E-Yuan Could Look Like

China already is a leader in digital payments. In 2019, Chinese used apps to pay for goods and services equivalent to just over USD 500trn. The volume was equivalent to 35 times GDP. By comparison, in the US, digital payments worth only about USD 100trn were made during the same period, which corresponds to around five times GDP.[55]

Cash is now so unpopular in China that the state is using it as a punishment. In late 2020, the state news agency Xinhua reported that a court in the southern Chinese province of Guangdong sentenced more than 2,400 offenders to be barred from all digital payments for five years. They are banned from using apps to make digital payments. Kenrick Davis of Sixth Tone writes:

“The punishment is tantamount to social exclusion in a country where mobile payments are employed in every area of life, from public transport to grocery shopping, household bills, health care, and tourism. Leading payment apps Alipay and WeChat are so dominant that the government has had to remind businesses that refusing cash is illegal.”[56]

Pilot e-yuan projects have already been launched in four cities, including the well-known industrial center of Shenzhen. Millions of Chinese were able to register for a lottery to receive one of the coveted red envelopes. These envelopes contained a gift of money in digital form: 200 yuan, which could be used in more than 3,000 stores via a smartphone wallet app.[57] The lottery was also one of the recipes for success in the introduction of Alipay and WeChat Pay, which currently dominate Chinese payment transactions. According to reports from China, the e-yuan will also help to target government funds and protect against corruption.[58]

A Digital Coin to Rule Them All?

The e-yuan is the polar opposite of Bitcoin. It was developed, issued, and ultimately mandated by a state. While it is intended to improve the international role and circulation of the Chinese national currency, it is also intended to improve the government’s control over its citizens.

At the same time, the Chinese leadership is using the e-yuan to put the tech giants Ant Group and Tencent in their place. With Alipay and WeChat Pay, they have helped to largely displace cash in China, but their power is a thorn in the side of the party. This became evident when Beijing prevented the planned IPO of Alibaba’s Ant Group at the last second. Jack Ma, the founder of Alibaba and Ant, had dared to criticize the state-owned banks and was severely punished for it.[59]

In practice, Chinese merchants are not forced to support Alipay and WeChat Pay. However, if an e-yuan is declared legal tender, no merchant may refuse it. Nevertheless, contradictions remain, and their resolution is still a long time coming. For example, it is a stated goal of China to use the e-yuan to slowly undermine the dominance of the US dollar. A director of a Chinese state bank is quoted by the Financial Times as saying: “A bigger goal of ours is to challenge the dominance of the US dollar in international trade settlement. But progress toward this will only be gradual.” [60]

Despite this goal, China has even formed a joint venture with the inherently US dominated SWIFT payment system to push the e-yuan. This new company, called Finance Gateway Information Services Co, is to integrate the digital currency into international systems. One partner in the joint venture is China’s Cross-Border Interbank Payment System (CIPS), which was originally founded as an alternative to SWIFT. Now they are working together.[61]

US think tanks and human rights activists have long warned against the control options offered by a digital central bank currency. It is well known that China’s leadership relies on control rather than trust vis-à-vis its people. But if the e-yuan is to help spread internationally, the question remains: Who outside China wants to use a currency that allows the Communist Party in Beijing to see every transaction?

Europe Is on Its Way to the E-Euro; the US Is Waiting

Unlike in China, where the government and central bank have long been on course in terms of developing a digital central bank currency, in the West there has so far been only debating, planning, and testing. The goal is still clear, as Augustine Carstens, head of the Bank for International Settlements (BIS), said recently. Carstens compared CBDCs to cash:

“A key difference with CBDC is that a Central Bank will have absolute control on the rules and regulations that will determine the use of that Central Bank liability, and we will have the technology to enforce that. This makes a huge difference to what cash is.” [62]

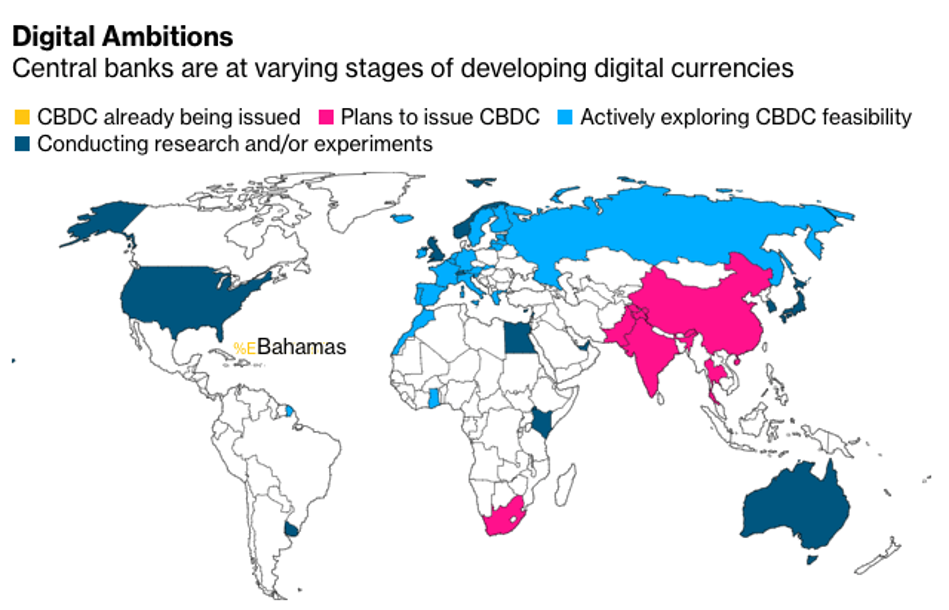

As the following chart from Bloomberg shows, among those central banks that have some form of digital central bank currency on their radar, there are currently three zones, apart from the Bahamas, that have already introduced a digital central bank currency. In Asia and South Africa, plans are already fixed and tests with CBDCs are underway. In Europe and Russia, plans are being prepared and central banks have made it clear that they see CBDCs as the future. In the US, the UK, Australia, and Japan – the core countries of the US dollar bloc – central banks are merely experimenting and see no reason to hurry.

Source: Bloomberg

In the euro zone plans for a CBDC are further along than in the US. ECB President Christine Lagarde makes no secret of the fact that she sees digital central bank currencies as the future. Even as IMF chief, she spoke out in favor of their introduction: “I think we should consider issuing a digital currency. There has to be a role for the state to supply the digital economy with money.” [63]

After a plan for what the digital euro could look like was unveiled in October 2020,[64] the consultation process on the digital euro was recently concluded.[65]The actual decision on whether and how the ECB wants to introduce the digital euro is to be made by mid-2022 at the latest, as Christine Lagarde wants to have introduced the e-euro in four years at the latest.[66] “It’s a technical endeavor as well as a fundamental change. We need to make sure that we’re not going to break any system, but to enhance the system”, Lagarde said. And: “We need to make sure that we do it right – we owe it to the Europeans.” [67]

It is already visible how tough the battle between the ECB and the traditionally cash-loving and skeptical Europeans will be. In addition to the technical implementation, many other questions remain unanswered. At the center is the question of what role the banking system will play if citizens can hold digital money directly in their own wallets. ECB Director Fabio Panetta shocked Europeans in February by announcing that digital balances over EUR 3,000 could be subject to a punitive tax to keep people using the banking system.[68] The media’s response to this announcement was clear: If that is how the ECB is going to go, it might as well not bother.

This was a classic false start. Which is a shame, because the ECB’s logic is sound in itself: When China releases a digital central bank currency, when Facebook tinkers with Diem (aka “Libra”), and when Bitcoin exists, the central bank cannot stand idly by. In October 2020, Panetta gave a speech that did not generate the excitement surrounding his 3,000-euro statement. He stated that a digital euro would be necessary considering changing payment habits:

“In particular, it would be needed in the event that citizens become reluctant to use cash as they go digital. This is not the situation we face today: cash is still the most common way of making retail payments in the euro area. However, its role as a payment instrument is diminishing – in some countries rapidly so – as consumers are increasingly paying electronically: as a proportion of all physical retail payments, cash payments decreased from 79% in 2016 to 73% in 2019. This trend has accelerated during the pandemic – with a vast majority of consumers expecting to continue using digital payments as often as they do now, or even to use them more often in the future. And because of this trend, we may see a further increase in the uptake of international card schemes and solutions such as payment wallets and apps developed by large technology firms.” [69]

Against this backdrop, Panetta said, the digital euro is a better way to protect the privacy of Europeans than a privately owned digital payment system ever could be:

“A digital euro would increase privacy in digital payments thanks to the involvement of the central bank, which – unlike private suppliers of payment services – has no commercial interests related to consumer data.” [70]

So, there is hope that the ECB will launch a different sort of digital currency than the Chinese leadership has done: a digital currency that protects the fundamental rights of its citizens instead of undermining them. But it is up to Europeans themselves to demand those “features”. Panetta knows this: “The value of money – in both physical and digital forms – is rooted in citizens’ trust. Acceptance by the public is crucial.” [71]

Much Criticism of Central Bank Digital Currencies

The bumpy introduction of the digital euro shows that many questions remain unanswered, and there are fears and concerns. As China’s example shows, digital money is a tool that can be used for surveillance. The economic aspects are also problematic. Above all, the idea of some economists that negative interest rates could be enforced with CBDCs – or even “deeply negative interest rates”, which Kenneth Rogoff proposes – scares many people.[72]

Rogoff is also considered an opponent of cash, which even now companies use to avoid negative interest rates. Advocates of free choice and cash fear CBDCs will displace cash to make way for even more extreme experiments in the monetary sphere. They see CBDCs as another weapon in the “war on cash”.

Another idea that is not going down well with those who are already worried about monetary stability: direct payments to citizens and so-called “helicopter money”:

“With closer integration of the monetary spigot and the end consumers and businesses, the central bank can much more easily issue credit or just outright cash-outs to the private individuals and commercial entities by simply ‘airdropping’ new tokens to the existing users. This would lead to disastrous consequences. Economies get easily addicted to central banks’ dope.” [73]

The list of unanswered questions and potential conflicts between banks and the population is therefore long. For this reason, Washington sees no reason to hurry and wants to wait and see how the digital experiences of others turn out – probably also because the US dollar is the dominant currency in the world anyway.

The Federal Reserve is currently asking itself whether it needs a digital central bank currency at all. As Federal Reserve Chairman Jerome H. Powell put it in March: “Does the public want, or need, a new digital form of central bank money to complement what is already a highly efficient, reliable and innovative payments arena?” [74]

Still, experiments by the Federal Reserve are currently underway in cooperation with the Massachusetts Institute of Technology (MIT): “The focus really is on developing and understanding the capabilities and limitations of the relevant technologies”, said Powell: “It’s not an attempt to create a prototype.” [75]

In this context, Powell’s assessment of Bitcoin is also of interest, especially when seen in light of Luke Gromen’s thoughts, which we have already mentioned: “It’s more a speculative asset, that’s essentially a substitute for gold, rather than for the US dollar” [76], Powell said.

Conclusion: What Is Joe Biden Going to Do?

Since the process of de-dollarization is a gradual, slow one, there is no conclusion to state, except that it will continue. All the trends we have observed in recent years have only been reinforced by the Covid-19 crisis and the response of central banks and politicians. Fifty years after the Nixon shock, even Saudi Arabia is openly turning toward China – and away from the US dollar.

The big, open question is: What will Joe Biden do? We must not forget that he was already confronted with all of this as Barack Obama’s vice president. And that under Obama there was a thoroughly constructive phase of rapprochement between East and West on the US dollar issue. We know from Robert Triffin that the “exorbitant privilege” will eventually become a burden – and that it is also in the interest of the US to end the sole dominance of the US dollar at some point.[77] What we do not know is how that transition might proceed and whether it could unfold reasonably peacefully. Biden’s government understands that China’s digital currency could pose a threat to the dollar – and is keeping an eye on developments. Specifically, they want to know if the digital currency could be a way to circumvent U.S. sanctions.[78] Which brings us back to Iran.

A central cornerstone of the negotiations between the US and the rest of the world under Obama was the so-called Iran deal, which was officially about Iran’s nuclear disarmament. But the negotiations on this subject were also the only forum in which the US, China, Russia, and the EU could talk about other issues without interference. And talk they did. We know that from John Kerry, then Obama’s Secretary of State. When asked in August 2015 what would happen if the Iran deal was scrapped, he replied:

“If we turn around and nix the deal and then tell them, ‘You’re going to have to obey our rules and sanctions anyway,’ that is a recipe, very quickly (…) for the American dollar to cease to be the reserve currency of the world.” [79]

As Joe Biden has returned to the Iran negotiating table – although the negotiations are initially only indirect – we can only advise our readers to prick up your ears and read between the lines. Because in addition to Iran’s nuclear program, the future of our monetary system is apparently being discussed in these talks.

[1] See Xu, Muyu und Tan, Florence: “Saudi Aramco to prioritise energy supply to China for 50 years, says CEO”, Reuters, March 21, 2021

[2] See “De-Dollarization 2020 –The Endgame Has Begun”, In Gold We Trust report 2020, “De-Dollarization: Europe Joins the Party”, In Gold We Trust report 2019, “De-Dollarization –From the Dollar to Gold, Via the Yuan and the Euro”, In Gold We Trust report 2018

[3] See Kibe, Hidemitsu: “Saudi Aramco hints at future yuan bonds in potential coup for China”, Nikkei Asia, November 21, 2021

[4] See Anderlini, Jamil: “China calls for new reserve currency”, Financial Times, March 24, 2009

[5] See Yap, Chui-Wei: “Shanghai Gold Exchange Launches International Board”, The Wall Street Journal, September 7, 2014

[6] See Chatterjee, Sumeet und Meng, Meng: “Exclusive: China taking first steps to pay for oil in yuan this year – sources”, Reuters, March 29, 2018

[7] Tétrault-Farber, Gabrielle und Osborn, Andrew: “Russia’s top diplomat starts China visit with call to reduce U.S. dollar use”, Reuters, March 22, 2021

[8] Krishnan, Ananth: “China, Russia look to deepen ‘best in history’ ties”, The Hindu, March 22, 2021

[9] See Blinova, Ekaterina: “Dumping the Dollar: Will China, Russia, Turkey, and Iran Create a New International Currency?”, Sputnik News, March 24, 2021

[10] O’Connor, Tom: “After US Talks Turn Tense, China Turns to Russia to ‘Advance Cooperation’”, Newsweek, March 22, 2021

[11] See “De-dollarization in overdrive: Russia & China boost settlements in national currencies to 25%”, RT News, January 3, 2021

[12] See “Iran, Russia and Turkey signal growing alliance”, Defcon Warning, March 26, 2021

[13] See Armistead, Louise: “Putin: Russia will join the Euro one day”, The Telegraph, November 26, 2010

[14] “Putin says Russia wants better ties with Europe”, Euractiv, January 27, 2021

[15] See Korsunskaya, Darya: “Russia, under fresh US sanctions threat, says ready to issue Eurobond soon”, Reuters, March 22, 2021

[16] See “Russia continues ditching US Treasuries as part of state de-dollarization policy”, RT News, January 20, 2021

[17] See Carter, Radigan: “Back to The Decentralized Future”, February 1, 2021

[18] Barton, Susanne und Sirtori-Cortina, Daniela: “Dollar’s Share of Global Reserves Sinks to Lowest Since 1995”, March 31, 2021

[19] See Choong Wilkins, Rebecca, Azevedo Rocha, Priscila und Zhou, Ina: “China Raises $4.75 Billion as Euro-Bond Sale Draws Bumper Bids”, Bloomberg, November 18, 2020

[20] See “EU sovereign bonds can reshape the bloc’s future”, Financial Times, July 23, 2020

[21] Barton, Susanne und Ainger, John: “Threat to Dollar’s Global Supremacy Revived by EU Stimulus Deal”, Bloomberg, July 21, 2020

[22] “Press review: US sanctions eroding dollar and Japan seeks to build bridges with Russia”, TASS Russian News Agency, February 8, 2021

[23] Jean-Claude Juncker: “State of the Union 2018 – The hour of European sovereignty”, September 12, 2018

[24] Roach, Stephen: “A Crash in the Dollar Is Coming”, Bloomberg, June 8, 2020

[25] See Roach, Stephen: “A Crash in the Dollar Is Coming”, Bloomberg, June 8, 2020

[26] Shalini, Nagarajan: “The US is facing a dollar collapse by the end of 2021 and an over 50% chance of a double-dip recession, economist Stephen Roach says”, Insider, September 24, 2020

[27] See “From inflation targeting to average inflation targeting”, Economic Research FRED Economic Data, November 9, 2020

[28] Roach, Stephen: “The Dollar’s Crash Is Only Just Beginning”, Bloomberg Quint, January 25, 2021

[29] Kaletsky, Anatole: “Europe’s Hamiltonian Moment”, Project Syndicate, May 21, 2020

[30] “‘The US dollar is the most overvalued major currency in the world’: Stephen Roach”, BNN Bloomberg, March 11, 2021

[31] “‘The US dollar is the most overvalued major currency in the world’: Stephen Roach”, BNN Bloomberg, March 11, 2021

[32] See Rogoff, Kenneth: “The Dollar’s Fragile Hegemony”, Project Syndicate, March 30, 2021

[33] Rogoff, Kenneth: “The Dollar’s Fragile Hegemony”, Project Syndicate, March 30, 2021

[34] See “Gold Demand Trends Full year and Q4 2020: Weak Q4 set the seal on an 11-year low for annual 2020 gold demand”, World Gold Council Gold Hub, January 28, 2021

[35] See “Gold Demand Trends Full year and Q4 2020: Weak Q4 set the seal on an 11-year low for annual 2020 gold demand”, World Gold Council Gold Hub, January 28, 2021

[36] See Golubova, Anna: “Russia’s gold reserves surpass its US dollar holdings for first time, says country’s central bank”, KITCO News , January 12, 2021

[37] See “2020 Central Bank Gold Reserve Survey”, World Gold Council Gold Hub, May 18, 2020

[38] See “Update 1 – Poland’s central bank wants to buy 100 tonnes of gold, governor says”, Reuters, March 15, 2021

[39] “Poland Wants More Gold”, Schiff Gold, March 16, 2021

[40] See “Europe Has Been Preparing A Global Gold Standard Since The 1970s”, Seeking Alpha, July 16, 2020

[41] Ainger, John and McCormick, Liz: “Goldman Warns the Dollar’s Grip on Global Markets Might Be Over”, Bloomberg, July 25, 2020

[42] See “’Break The Glass’ – Guggenheim’s Minerd Warns Fed May Start Buying Gold To Support Dollar Hegemony”, Corona Stocks, June 8, 2020

[43] See Bassman, Harley: “Rumpelstiltskin at the Fed”, Allianz PIMCO, April 2016

[44] Bassman, Harley: “Rumpelstiltskin at the Fed”, Allianz PIMCO, April 2016

[45] See Spence, Peter: “ECB could buy gold to revive economy”, The Telegraph, November 17, 2014

[46] See Frost, Natasha: “Gold is good. Gold is strong. Populist governments in Eastern Europe are stockpiling it”, Quartz, October 16, 2018

[47] See “Gold Demand Trends Full year and Q4 2020: Central Banks and other institutions”, World Gold Council Gold Hub, January 28, 2021

[48] “Bitcoin Outlook – Luke Gromen- Swan Signal Live E51”, YouTube Channel Swan Signal, February 23, 2021

[49] See Goldman, David: “Foreign companies are giving up on the United States and betting big on China, report says”, CNN Business, January 25, 2021

[50] Hannon, Paul und Jeong, Eun-Young: “China Overtakes US as World’s Leading Destination for Foreign Direct Investment”, The Wall Street Journal, January 24, 2021

[51] See Spratt, Stephen: “This Year Chinese Sovereign Bonds Became a Global Yield Play”, Bloomberg, December 7, 2020

[52] See Xiaochuan, Zhou: Reform the international monetary system, March 23, 2009

[53] “Booming demand for Chinese assets boosts renminbi’s global role”, Financial Times, October 7, 2020

[54] “Booming demand for Chinese assets boosts renminbi’s global role”, Financial Times, October 7, 2020

[55] See “Virtual control: the agenda behind China’s new digital currency”, Financial Times, February 16, 2021

[56] Kenrick, Davis: “In Cashless China, Criminals Are Punished With Payment App Bans”, Sixth Tone, November 12, 2020

[57] See Kharpal, Arjun: “China hands out $1.5 million of its digital currency in one of the country’s biggest public tests”, CNBC, October 12, 2020

[58] See Liao, Rita: “China’s digital yuan tests leap forward in Shenzhen”, Tech Crunch, October 12, 2020

[59] See “China halts $37bn Ant Group IPO, citing ‘major issues‘”, Financial Times, November 3, 2020

[60] “Virtual control: the agenda behind China’s new digital currency”, Financial Times, February 16, 2021

[61] See “Virtual control: the agenda behind China’s new digital currency”, Financial Times, February 16, 2021

[62] “Central Bank Digital Currencies will grant authorities “absolute control” over money”, Gold and Silver UK, March 26, 2021

[63] Hein, Christoph: “Lagarde fordert digitale Währungen” (“Lagarde Calls for Digital Currencies”), Frankfurter Allgemeine Zeitung, November 14, 2018

[64] See ECB: “Report on a Digital Euro”, October 2, 2020

[65] See ECB: “ECB publishes the results of the public consultation on a digital euro”, April 14, 2021

[66] See “Lagarde Says ECB Could Have Digital Currency Within Four Years”, Bloomberg, March 31, 2021

[67] Neumann, Jeannette and Lacqua, Francine: “Lagarde Says ECB Could Have Digital Currency Within Four Years”, Bloomberg, March 31, 2021

[68] See “EZB-Direktor will digitalen Euro: “Wir müssen dabei sein”” (“ECB Director Wants Digital Euro: “We Must Be Part of It””), Die Presse, February 9, 2021

[69] Panetta, Fabio: “A digital euro for the digital era”, BIS, speech of October 12, 2020

[70] Panetta, Fabio: “A digital euro for the digital era”, BIS, speech of October 12, 2020

[71] Panetta, Fabio: “A digital euro for the digital era”, BIS, speech of October 12, 2020

[72] See Rogoff, Kenneth: “The Case for Deeply Negative Interest Rates“, Project Syndicate, May 4, 2020

[73] Forgac, Tomas: “Why Central Bank Digital Currencies Are a Bad Idea”, Mises Institute, November 30, 2020

[74] Smialek, Jeanna: “Jerome Powell says the Fed won’t issue a digital currency without congressional approval”, The New York Times, March 22, 2021

[75] Smialek, Jeanna: “Jerome Powell says the Fed won’t issue a digital currency without congressional approval”, The New York Times, March 22, 2021

[76] Smialek, Jeanna: “Jerome Powell says the Fed won’t issue a digital currency without congressional approval”, The New York Times, March 22, 2021

[77] Wikipedia: Triffin Dilemma

[78] Mohsin, Saleha: “Bidens Team Eyes Potential Threat From China’s Digital Yuan”, Bloomberg, April 12, 2021

[79] Strobel, Warren: “Dollar could suffer if US walks away from Iran deal: John Kerry”, Reuters, August 11, 2015