Bringing it Home: Central Bank Gold Repatriation

“Put forth thy hand; reach at the glorious gold.”

William Shakespeare

- Since 2011, central banks worldwide have repatriated over 1,800 t of gold in multiple waves.

- Repatriation efforts span developed economies (Germany, Netherlands, Austria, Poland) and emerging markets (India, Türkiye, Venezuela), reflecting a global reassessment of gold’s strategic importance.

- The movement often involves internal political struggles, with state auditors and opposition politicians advocating for repatriation, while central banks typically resist these efforts.

- Several repatriation attempts have failed (Switzerland, Romania, Slovakia) or faced significant resistance even when partially successful (Germany, Austria, Netherlands), revealing central banks’ reluctance to change gold storage practices.

- According to World Gold Council and INVESCO surveys, this trend will likely accelerate as geopolitical concerns intensify through the decade’s end.

- Central banks are purchasing and repatriating gold due to growing geopolitical risks, financial weaponization through sanctions, and limited audit access to foreign-stored reserves.

Introduction

Gold repatriation refers to the process by which central banks move their physical gold reserves from the vaults of foreign gold custodians and back to vault storage within their own countries. As an observable phenomenon, gold repatriation gained significant momentum starting in 2011 and has continued to the present day, with many central banks jumping on board with the idea. Therefore, the gold repatriation trend can be seen as an interconnected phenomenon that has created a noticeable domino effect. While many countries have successfully repatriated gold, there are also countries where repatriation efforts faced resistance and failed due to central bank and political opposition, such as in Switzerland, Romania, and Slovakia.

The impulse to bring gold back into central banks’ possession has been driven by several factors, including geopolitical tensions and sanctions risks, a desire for economic sovereignty, the need for physical audits, and the erosion of trust among the world’s central banks.

In our In Gold We Trust report 2019, “Gold in the Age of Eroding Trust”, we explored several dimensions of the phenomenon of trust– trust in money, trust in the monetary system, and the consequences of the erosion of that trust – and we stated: “The breakdown of trust in the international monetary order is manifesting itself in the highest gold purchases by central banks since 1971 and the ongoing trend to repatriate gold reserves.” Since that observation was written in 2019, central bank gold purchases have reached even higher record annual highs, while the gold repatriation trend has persisted and is set to continue.

In the following sections, we analyse why central banks repatriate gold and how the broader trends shaping central bank behaviour – including the evolving dynamics of trust, sovereignty, and strategic reserve management – suggest that repatriation efforts will continue. We also look at recent gold repatriation operations, discussing the motivations behind these moves and how the withdrawal of gold from third-party custodians, such as from the New York Federal Reserve and the Bank of England, has notably reduced the gold inventories held in their vaults.

Triggers and Motivations

Central banks repatriate gold for a variety of interconnected reasons, mostly due to perceived risks of storing gold reserves with foreign custodians, which are mitigated by bringing the gold back home. Key triggers and motivations for gold repatriation are the following:

- Mitigating sanctions risk: With the US, the EU, and the G7 active in imposing sanctions and freezing and confiscating foreign reserves, central banks repatriate gold and keep it under sovereign control to prevent it from becoming frozen or sanctioned.

- Auditing: Some federal auditors have demanded physical gold audits. Since the New York Federal Reserve and Bank of England custodians prohibit physical audits, central banks are compelled to repatriate gold to be physically audited and verified.

- Concentration risk: State auditors can deem that holding a high percentage of central bank gold in a single foreign vault poses a concentration risk and can direct the central bank to repatriate gold to diversify its storage and reduce concentration risk.

- Doubts over gold’s existence: Lack of transparency from custodians such as the New York Federal Reserve has fueled suspicions about the availability of sufficient unencumbered gold to cover all customer gold claims. Germany’s ultraslow five-year repatriation from New York and Paris only heightened this distrust. Therefore, central banks withdraw and repatriate gold to prove that their gold holdings exist.

- Geopolitical tensions: Rising political and military conflicts, potential trade wars, and trade bloc realignments motivate central banks to move gold reserves to domestic storage to reduce exposure to international conflicts and asset freezes.

- Global momentum: When one central bank repatriates gold, others follow, concerned about being left vulnerable. These actions create momentum and a chain reaction, analogous to a game of musical chairs where no one wants to be the last man standing.

- Political pressure from politicians: In many cases, governments and their central banks have repatriated gold to partially appease and placate domestic political pressure and domestic grassroots campaigns.

- Counterparty risk: Physical gold has no counterparty risk, but this is only fully true when the gold is stored domestically rather than deposited abroad. The 2007/2008 global financial crisis triggered central banks to reappraise counterparty risk and reinforced the importance of unencumbered gold stored in domestic vaults.

- Currency crisis preparedness: The euro debt crisis of 2009–2012 focused central banks’ attention on currency crises and highlighted the importance of holding gold as a stable reserve during financial turmoil. Some central banks, such as the Dutch central bank, brought gold home to hedge against currency devaluation.

- Reducing coercion: Repatriating gold prevents foreign governments from pressuring central banks into using their foreign stored gold in swaps, loans and leases, or political or economic negotiations. Sovereign control minimises external influence over monetary policy.

- A strategic reserve asset: Gold is a central bank’s most strategic asset, with a rising value and the foundation of national wealth. Central banks increasingly realise that their gold is safest when stored domestically, free from external control or confiscation.

- A confidence-building measure: Repatriating gold strengthens national sovereignty and boosts public trust.

- Saving on gold storage costs: Gold custodians such as the Bank of England charge ongoing storage fees. Repatriation can reduce long-term costs despite upfront repatriation expenses for transport and insurance.

- Crisis scenarios: Keeping gold abroad during crises may expose it to seizure for bailouts or swaps. Repatriation ensures gold reserves avoid such vulnerabilities and remain under sovereign control during financial instability.

- Preventing gold being used in bailouts: Historical cases suggest some central banks were pressured into “gold sales” to close out unrepayable gold loans and cover bullion bank liabilities. Domestic storage avoids the pressure to contribute to cover such liabilities.

However, it is important to remember when listening to central banks’ pronouncements that they rarely criticise each other publicly, preferring to use diplomatic language when justifying gold repatriation instead of explaining their real motivations.

Practical reasons for central banks to store gold with third-party custodians

There are, however, some practical reasons why central banks continue to store gold in the traditional storage centres of the Bank of England in London, Banque de France in Paris, and the New York Federal Reserve in Manhattan. These include:

- Security and physical safety: These institutions are known for their highly secure vaults with advanced physical and surveillance security, and they have long-standing experience storing the gold reserves of many central banks.

- Liquidity and market access: The Bank of England in London offers central banks the ability to buy, store, and sell gold all in the same location and to earn income by accessing the gold lending and gold swap market operated by the commercial banks that also maintain gold accounts at the Bank of England. Gold can also be placed as collateral to raise foreign exchange.

- Diversification of storage risk: Storing a percentage of gold reserves in a stable foreign jurisdiction allows central banks to diversify storage risk, especially if their countries suffer political instability and civil unrest.

Central Bank Gold Surveys

While there have been some prominent gold repatriations since 2011 – which we will look at below – it’s important to note that central bank gold repatriation is an ongoing phenomenon, as is highlighted by the results of very recent central bank gold surveys.

In 2023, the annual “Invesco Global Sovereign Asset Management Study” of official sector institutions, which surveyed 57 central banks and 85 sovereign wealth funds, found that of the 43 central bank respondents who were buying gold during 2023, 68% said they held physical gold in their own country, compared with 50% in 2020. Most interestingly, 74% of respondents said they would hold physical gold in their own country by 2028. There has been a growing trend of central bank gold repatriation since the beginning of this decade, and the trend is set to continue well into the future.

One anonymous Western central banker quoted in the 2023 Invesco study said that his bank had previously held gold in London, but now that gold has been repatriated back to his home country:

“Gold has played a crucial role during the last couple of years. We increased the exposure 8–10 years ago and had it held in London, using it for swaps and to enhance yields, but we’ve now transferred our gold reserves back to our own country to keep it safe – its role now is to be a safe-haven asset.”

The fact that this central banker wanted to remain anonymous proves that central banks are repatriating gold under the radar, in addition to the central banks that have gone public. Central bank gold repatriation is like central bank gold buying – some of it is divulged in the public domain, some kept secretive.

The Invesco study also found that “central banks prefer to hold physical gold rather than gold ETFs or derivatives”, and that of 24 central banks that indicated they were increasing their gold reserves in 2023, a full 96% said this was because gold was a safe haven, while 38% were concerned about the “freezing of central bank assets” in light of the precedent set when the US, the EU, and G7 froze Bank of Russia FX reserves.

Central bank gold buying and repatriation trends are now inextricably linked and intertwined. Central banks are buying gold because of rising geopolitical risk and the weaponisation of reserves via sanctions. But they are also repatriating gold for these very same reasons.

This was picked up on in the 2023 IMF working paper on international gold reserves, “Gold as International Reserves: A Barbarous Relic No More?”, which stated that:

“…the decision to freeze foreign exchange reserves of the Russian central bank has highlighted the possibility that other central banks may respond by shifting a portion of their reserves from foreign exchange into gold, which can be repatriated and vaulted at home.”

Even more recently, the “Invesco Global Sovereign Asset Management Study 2024”, found that 60% of central banks “consider gold as a hedge against geopolitical turmoil” while 56% agreed that “the weaponisation of central bank reserves makes gold more attractive”.

The World Gold Council’s “2024 Central Bank Gold Reserves Survey” collated 70 central bank respondents, reflects similar themes, finding that geopolitical instability is among the top three reasons why central banks invest in gold, with 76% of emerging-market central banks indicating so. These are the central banks that represent the bulk of official-sector gold purchases.

This World Gold Council (WGC) survey found that the current themes increasingly motivating central banks to buy gold are (a) the performance of gold during times of crisis, (b) gold acting as a geopolitical diversifier, (c) gold’s lack of political risk, (d) increased concerns about sanctions, and (e) the rising political risk in advanced, i.e. Western, economies. Similar to the findings of the Invesco surveys, the themes identified by the WGC are also pushing central banks to repatriate gold.

The OMFIF’s “Global Public Investor 2024”, which surveyed 73 central banks, found that the two primary motivations of central banks are (a) holding gold in reserve portfolios are diversification (68% of respondents) and (b) as a hedge against geopolitical risk (40% of respondents). An even more recent OMFIF paper titled “Gold and the New World Disorder 2025–26 Perspectives” picks up on sanctions risk and states that:

“Even countries that are staunch American allies fear they may be caught up in the indirect effect of sanctions on third countries, which could jeopardise their holdings in dollars or other western currency assets in certain jurisdictions. The move into gold has been strengthened by doubts overshadowing other reserve currency alternatives.”

In this environment, says the OMFIF, gold has benefited, as “it is no one’s liability”. A similar theme is discussed in the World Bank’s 2024 “Gold Investing Handbook for Asset Managers”, which states that “geopolitical risk is a major factor for asset managers to consider, especially in emerging markets”. This is because “geopolitical events can have a significant impact on financial markets”, and these events have led to the freezing of central bank assets, e.g. assets of the central bank of Iran (USD 1.9bn frozen in 2010), Kazakhstan (USD 22.6bn frozen in 2017), Venezuela (USD 342mn frozen in 2020), Afghanistan (USD 7bn frozen in 2021), and the largest of them all, the Russian central bank, which saw an estimated USD 258bn was frozen in 2022. As the World Bank says of holding gold with foreign custodians, including the Bank of England, Federal Reserve, Banque de France, and BIS: “Political risks must be considered because gold accounts can be frozen”.

Time-series analysis of gold vault holdings data also highlights the continuing trend of gold repatriation, with gold analyst Jan Nieuwenhuijs finding in an article aptly titled “Repatriated Gold Reaches Historic Highs”: “The share of global official gold reserves not stored at the Federal Reserve and Bank of England has reached 78% in 2024, from 51% in 1972. This shift can be seen as a proxy for the West’s decline in financial dominance.”

Having explored central banks’broader trends, motivations, and current thinking regarding gold repatriation, we now turn to specific case studies where repatriation efforts were implemented, focusing on the triggers, details, and geopolitical contexts involved.

Gold Repatriation Case Studies

Venezuela: 160 tonnes

The first high-profile gold repatriation by a central bank this century was by the Venezuelan central bank, Banco Central da Venezuela (BCV), which took place between November 25, 2011, and January 30, 2012, during which 160 t of Venezuela’s gold was flown back from Europe to Caracas on 23 cargo flights.

Catalysed by the threat of US sanctions and a desire to reduce dependence on Western financial institutions, the BCV’s gold repatriation was a classic first mover advantage operation and set the scene for later repatriations by Germany and others while bringing the term gold repatriation into the zeitgeist.

Venezuela’s gold repatriation operation was triggered by President Hugo Chávez, who in August 2011 called for t of gold, i.e. 16,908 400-oz. bars, within a two month period.

This gold repatriation by the BCV to Caracas was part of a more general move by Venezuela that included moving international FX reserves away from Western financial institutions and investing them with banks in the BRICS countries of China, Russia, and Brazil.

Notably, the BCV’s gold repatriation announcement was made on August 17, 2011, two weeks after S&P had downgraded the sovereign credit rating of the US. At which point, Chavez claimed he was bringing the gold back to Venezuela because of the global financial crisis.

Logistics and Implementation

As a public supporter of Libyan leader Muammar Gaddafi, Chavez was also worried that the West might sanction Venezuela in the same way that the UN had sanctioned Libya in February 2011 when it froze the assets of Gaddafi and the Libyan government. Venezuela’s gold repatriation was also framed as a populist play to a domestic and South American audience and as a way of gaining sovereignty over the gold, with the then BCV President Nelson Merentes saying that “We want to protect our assets, which belong to all Venezuelan people”. According to Merentes, the Venezuelan gold repatriation logistical operation, which was known as “Patriotic Gold” (Oro Patrio), involved the participation of 500 people. Of the 23 flights, the first flight transported 5 t of gold, and the last flight brought 14 t, with the other 21 flights carrying an average of 6.7 t of gold each.

Strategic Motivations and Aftermath

In August 2011, Venezuela held 366 t of gold, with 156 t, or 42.3%, stored in the vaults of the BCV in Caracas and the remaining 210 t, or 57.7%, held abroad. Of the 210 t of gold abroad, 99.2 t was with the Bank of England, 12 t was on deposit with the Bank for International Settlements (BIS), 17.5 t was deposited with commercial bank J.P. Morgan, and another 83 t was lent out in “time deposits” spread out among five bullion banks, namely, Barclays, HSBC, Standard Chartered, the Bank of Nova Scotia, and BNP Paribas.

While Chavez and the BCV had called for all 210 t of gold to be brought back to Venezuela, in the end, only 160 t came back, with 50.87 t left in the Bank of England in London to be used in “international financial operations”. This decision to leave gold at the Bank of England would come back to haunt the BCV since this was the Venezuelan gold that the Bank of England then froze in 2018/2019 on instructions from the British Foreign Office, the US Treasury, and US State Department.

Germany: 674 tonnes

Venezuela’s gold repatriation in 2011/2012 helped spark Germany’s gold repatriation movement, as attention began to focus on the foreign storage locations of Germany’s gold managed by the Bundesbank.

In 2011, Germany held 3,396 t of gold, but only 31% was stored in Frankfurt, with the rest claimed to be held in custodian storage at the Federal Reserve in New York (1,536 t), the Bank of England in London (450 t), and the Banque de France in Paris (374 t). However, due to Bundesbank secrecy and a lack of audits, a cross-section of German politicians, federal auditors, and major German media outlets such as the daily newspaper Bild and the weekly magazine Der Spiegel began to ask questions.

In July 2011, Der Spiegel revealed that the Bundesbank rarely checked Germany’s New York gold reserves, visiting the Manhattan vaults only twice (in 2007 and 2011) and on both occasions with limited access. This revelation came after CSU politician Peter Gauweiler’s parliamentary inquiry, which led to a report by accounting professor Professor Jörg Baetge, accusing the Bundesbank of neglecting its audit obligations. In November 2011, Bild reported that the German Federal Audit Office (Bundesrechnungshof), acting on Baetge’s report, launched an investigation into the Bundesbank’s lack of oversight of Germany’s foreign-held gold.

In March 2012, Bild published an article on the German gold at the New York Federal Reserve Bank, labeling it an “unbelievable gold scandal” after Bild reporter Ralf Schuler and another German politician, Philipp Missfelder (CDU), had visited the Federal Reserve’s New York gold vault in Manhattan but were denied access. Missfelder then demanded a list of Germany’s gold bars from Bundesbank President Jens Weidmann, who claimed the list was secret and that inquiries would endanger the trust between the Bundesbank and the Federal Reserve.

The Campaign for Transparency

In early 2012, a German “Holt unser Gold heim!” campaign (“Bring our gold home!” or “Repatriate our gold!”), led by Peter Boehringer and Rolf Baron von Hohenhau, also pressured the Bundesbank for a full, independent audit of all of Germany’s gold and for its speedy repatriation from abroad. The campaign argued that 100% of the German gold should return to backstop the Bundesbank’s balance sheet and ensure future currency cover.

The campaign initiators – the 28 main signatories include industrialist Hans-Olaf Henkel, Jim Rogers, Egon von Greyerz, Dimitri Speck, and Ed Steer of GATA – had actually begun questioning the Bundesbank during Q4/2011, demanding a full physical gold audit and pointing out that such an audit had been overdue for decades.

In May 2012, the German Federal Audit Office completed its investigative report into the German gold, but a redacted version, edited at the Bundesbank’s insistence, was only released into the public domain in October 2012. The report was highly critical of the Bundesbank and demanded physical audits of Germany’s foreign gold, revealing that:

- Germany’s gold bar list at the New York Federal Reserve dated back to 1979/80.

- The New York Federal Reserve blocked central banks from viewing their gold.

- No physical audits had ever been conducted in New York, London, or Paris, with the Bundesbank relying on written confirmations.

In 2007, Bundesbank staff were only allowed into an anteroom of the New York vault, seeing no gold. In May 2011, auditors were shown gold in one compartment, with only a few bars pulled out and weighed.

The federal auditor’s report also referred to plans “to count and weigh the gold bars stored in one of the nine chambers at the Federal Reserve in New York”. In a panic, the Bundesbank pushed back, citing legal and confidentiality-based excuses, and instead proposed repatriating 50 t of gold annually for three years for examination. The board also tried to deflect audits, with Bundesbank board member Carl-Ludwig Thiele, for example, saying that the German gold was not stored with “dubious business partners” but with “highly respected central bankers”. The board of the Bundesbank at the time also included Jens Weidmann, Joachim Nagel, and Andreas Dombret.

Philipp Missfelder dismissed the Bundesbank’s deflectionary tactics, insisting that all German gold held abroad had to be repatriated and accounting laws adhered to. Another politician, Heinz-Peter Haustein (FDP), concurred, “All the gold has to be shipped back”.

The Delayed Return

In January 2013, the Bundesbank backtracked again and published a new “storage plan”, whereby it promised, on a slow-motion basis of 8 years and without any yearly targets, to transport 300 t of gold from New York to Frankfurt and 374 t of gold from Paris to Frankfurt by December 31, 2020.

This farcical 8-year gold repatriation plan was also met with widespread derision and strengthened suspicions that the German gold stored abroad had either disappeared or was involved in international gold swap arrangements with foreign central banks. What Deutsche Bank euphemistically referred to as “diplomatic difficulties” occurred a year later, in 2014. As it turned out, even the gold that was transported back to Germany from 2013–2017 wasn’t readily available and had to be gradually procured by the custodians – or unwound from gold swaps – and then moved from the Federal Reserve to the Bundesbank, as the following timeline highlights:

In 2013, the Bundesbank repatriated 37 t of gold, including 32 t from Paris and a mere 5 t of low-purity gold from New York, which was resmelted to obscure its origins. In 2014, 120 t were returned, including 85 t from New York, with 50 t of low-purity gold resmelted for the same reason. In 2015, 210 t were repatriated, 99 t of which were from New York. In 2016, 216 t were transferred, completing the 300-tonne return from New York and leaving 91 t in Paris. By August 2017, the final 91 t were transferred from Paris, completing the repatriation process a full 56 months after the 2013 plan was announced.

However, at no stage did the Bundesbank ever explain why its 300 t of gold transfers from New York took four years when Venezuela could repatriate 160 t from Europe on 23 cargo flights in just two months. Likewise, moving 374 t of gold from Paris to Frankfurt – less than 600 km – could have been completed in a few weeks. Strangely, no evidence or photos of any Bundesbank transfers, such as aircraft, armoured cars, or police security, ever surfaced during 2013–2017.

In reality, Germany’s gold repatriation was a long, drawn-out diversionary smokescreen by the Bundesbank to prevent any physical audits of any of the gold held in New York and London. The gold that was brought back over 4–5 years can thus be seen as a ploy to divert attention away from the gold that had not been returned from New York and London.

The repatriation of 674 t, or 28% of the foreign stored gold, did, however, dilute public pressure and appease political demands. At the same time, it also blocked the Federal auditors from counting and weighing any of the German gold bars claimed to be stored in nine vault chambers at the New York Federal Reserve.

Ongoing Concerns

The growing tensions between the US and the EU has reignited the discussion about repatriating the gold reserves stored in New York. For example, Marco Wanderwitz, a former CDU member of the German Bundestag, called for the immediate repatriation of 1,236 t of German gold, or almost 37% of the total German gold reserves, from New York.

Netherlands: 122.5 tonnes

Venezuela’s gold repatriation plans, announced in August 2011, also triggered scrutiny of the Dutch gold reserves managed by the Netherlands central bank, De Nederlandsche Bank (DNB). In September 2011, Dutch MP Ewout Irrgang questioned the Netherlands Treasury about the storage locations of DNB’s 612.5 t of gold, as such information was not publicly available. Irrgang asked: “Where is the physical gold of DNB? At which locations and how much is where? What is the reason that the gold is still at these locations?”

From Questions to Action

After six weeks, the Dutch Treasury department revealed that the Dutch gold was stored in New York, London, Ottawa, and Amsterdam but did not disclose the amount of gold held at each location. In January 2012, then DNB president Klaas Knot made known on a Dutch TV program that only 67 t of the Dutch gold, i.e. less than 11%, was stored in Amsterdam, with the rest held “abroad”. This evasiveness by Knot in not naming the foreign storage locations sparked political and public uproar. On the same TV program, Irrgang said it was reckless to keep 90% of Dutch gold abroad during times of financial instability – the euro area sovereign debt crisis was in full swing at that time – while Willem Middelkoop argued there was no reason not to repatriate the gold. When asked if the gold should be repatriated, Knot answered decisively “No”.

In December 2012, Dutch finance minister Jeroen Dijsselbloem finally confirmed the DNB’s gold storage locations: over 50% or 300 t of gold in New York, 20% in Ottawa, nearly 20% in London, and 11% in Amsterdam. At the same time, Dijsselbloem rejected the idea of repatriating the Netherlands gold and, echoing the Bundesbank’s strategy, claimed that it was stored at central banks with “excellent track records”.

The Secret Operation

However, in November 2014, the DNB than made a surprise announcement, saying that it had repatriated 122.5 t of gold from the New York Federal Reserve to Amsterdam, increasing its gold distribution to 31% in Amsterdam and New York and 20% each in Ottawa and London. The gold transport, implemented in secret, was only announced once it was completed.

While the DNB justified the move with vague reasons such as “to spread its gold stock in a more balanced way”, and so that the gold “may also have a positive effect on public confidence”, it also, in a veiled criticism of the New York Federal Reserve storage vault, stated that “it is no longer wise to keep half of our gold in one part of the world”.

Since this shift in stance contradicted earlier reassurances from Klaas Knot and Jeroen Dijsselbloem in 2012, it appears that the Bundesbank’s 2012/2013 gold repatriation plans triggered concerns at the DNB about the adequacy of gold inventories at the New York Federal Reserve, and prompted the DNB to initiate the repatriation. The DNB’s loss of confidence likely developed between 2012 and 2014 and was also influenced by fears over the European debt crisis.

Gold analyst Jan Nieuwenhuijs reported in November 2014 that the DNB began considering gold repatriation in 2012 but that, according to DNB sources, “the subject was rather sensitive”. A DNB team then visited the New York Federal Reserve in 2013 to inspect the gold, and by mid-2014, preparations began for the transfer. The gold was flown back in multiple batches during October and November 2014.

Germany, Netherlands, and the New York Federal Reserve data

Each month, the US Federal Reserve releases data on the amount of foreign-held gold, i.e. “earmarked gold”, at the New York Federal Reserve vault, per Table 3.13. Given that the Bundesbank (2013–2016) and De Nederlandsche Bank (2014) claimed to have withdrawn gold from the New York Federal Reserve over the same period, their reported combined withdrawals can be compared with the Federal Reserve’s recorded gold outflows.

In 2013, Germany reported withdrawing 5 t, matching the Federal Reserve’s data. In 2016, Germany reported 111 t, while the Federal Reserve recorded 113 t, a close match. In 2014, the DNB claimed to have withdrawn 122.5 t and the Bundesbank 85 t from the New York Federal Reserve’s vaults, totaling 207.5 t. However, Federal Reserve data shows only 176.8 t were removed, leaving a 30.7-tonne discrepancy. In 2015, the Bundesbank reported withdrawing 99 t, while Federal Reserve data recorded 129 t, an excess of 30 t. This suggests that either the 30 t reported in 2014 were actually withdrawn in 2015 or another entity supplied the Bundesbank with gold in 2014, which was later reimbursed by the Federal Reserve. This would mean that the Bundesbank only really received 55 t of gold from the Federal Reserve in 2014, 50 t of which it was forced to resmelt to disguise the bars’ origins, which suggests that the bars received were low-purity gold from the US Treasury’s gold holdings at the New York Federal Reserve.

Austria: 90 tonnes

In 2015, the domino effect of central bank gold repatriation continued when Austria’s central bank, Oesterreichische Nationalbank (OeNB), announced that it would repatriate 90 t of its foreign-stored gold from London to Austria, as well as redistribute another 50 t from London to Switzerland. At that time the OeNB held 280 t of gold, of which 80% or 224 t was stored at the Bank of England in London, 50 t in the vaults of the Austrian Mint (Münze Österreich) – a fully owned subsidiary of the OeNB – and the remaining 6 t in Switzerland.

The Court of Audit report

Austria’s gold repatriation was triggered by a report from the Austrian Court of Audit. While this report was published in February 2015, it was researched and written in 2014. It found that at year-end 2013, the OeNB had been storing 82% or around 178 t of its physical gold holdings at the Bank of England, a situation with “a high concentration risk”. The Austrian Court of Audit also found that:

- The gold depository contract with the Bank of England contained deficiencies.

- The OeNB had gold safekeeping agreements with four foreign depositories in total, three of which were in Switzerland; but these agreements were “in large part, deficient and inadequate with regard to the provisions on ensuring the value and existence of the gold holdings”.

- All four storage contracts lacked provisions to address the OeNB’s access to the gold depositories, and there was no way to carry out audits. As the auditors stated, “There was no concept for carrying out the audit for gold holdings stored abroad.”

The 2020 Storage Policy

In response to this report, a plan called the “2020 gold storage policy”, was drawn up that would see Austria relocate 50% or 140 t of its gold to the Vienna vaults of the OeNB and the Austrian Mint by 2020. 20% or 56 t of the gold would be relocated to Switzerland, while 30% or 84 t would remain in London.

Like the Bundesbank, the OeNB said that its gold transport operations would be “gradually implemented” over 4+ years, which again had no logical explanation when other central banks, such as the Netherlands and Venezuela, were able to move the same amount of gold in one to two months, the planned gradual implementation can be said to not be very ambitious.

The step-by-step implementation of the recommendations of the Court of Audit most likely explains why, although the repatriation of 90 t of gold from London to the OeNB vaults in Vienna started in 2015, it was only completed in early July 2018, i.e more than 3 years later. In 2018, following the repatriation of 90 t of gold from London, the OeNB then stored 140 t of gold in Vienna, of which 90 t was in the OeNB’s own vaults and 50 t in the vaults of the Austrian Mint.

Poland: 100 tonnes

One of Europe’s largest and most public gold repatriation operations in recent years was by the National Bank of Poland (NBP) in 2019. It involved transporting 100 t of gold from the Bank of England in London to the vaults of the NBP in the Polish cities of Poznan and Warsaw.

Strategic Decision and National Pride

In July 2019, the NBP made a surprise announcement that in the process of boosting its gold holdings to 228.6 t, it had purchased 100 t of gold in London and that it had made a “strategic decision” to transfer this 100 t in the form of 400-oz gold bars away from London and back to the NBP vaults in Poland.

While citing the need for storage diversification, the NBP also surprisingly alluded to the risks of storing gold with the Bank of England, saying that it was implementing the gold repatriation “in order to reduce geopolitical risk” and so as to avoid “loss of access to, or restrictions on, the free disposal of gold resources held abroad”. Notably, the NBP also said that it decided “taking into account the practices of other central banks”. The Polish gold repatriation would also, in the words of the NBP, “strengthen the credibility and secure the financial strength of our country even in extremely unfavourable conditions”.

Interestingly, 2019 was the 100th anniversary of the Polish currency, the złoty, which probably explains why the NBP chose to repatriate exactly 100 t back to Poland. The NBP even issued a bar-shaped gold coin, “The Return of Gold to Poland”, for collectors to commemorate the 100-tonne repatriation.

Eight Flights to Independence

While the announcement of Poland’s gold repatriation in July 2019 was itself notable, the actual repatriation of 100 t of gold in the months that followed was even more dramatic, though it was only confirmed by the NBP in late November 2019 after completion. It involved eight cargo flights from London to Poland over the months of August to November 2019, with each flight transporting 12.5 t of gold, i.e. 1,000 gold bars, for a total of 100 t (8,000 gold bars).

Hungary: 94.5 tonnes

In October 2018, Hungary’s central bank, Magyar Nemzeti Bank (MNB) announced that it had bought 28.4 t of gold in London, boosting its gold reserves from 3.1 t to 31.5 t and that it had repatriated all the gold to Budapest. Then, in 2021, the MNB announced that it had purchased a further 63 t of gold internationally, tripling its gold reserves to 94.5 t, and that all of this gold was also repatriated to Budapest in 2020 and 2021, as confirmed by MNB governor György Matolcsy.

Serbia: 13 tonnes

In 2021, Serbia’s central bank, the National Bank of Serbia (NBS), repatriated 13 t of gold from Bern, Switzerland, to Serbia’s capital Belgrade, 12 t of which it had bought internationally during 2020–2021, and 1 tonne that was inherited from Yugoslavia’s breakup. By July 2021, all NBS gold was stored in Serbia, amounting to 37 t at the time. According to the NBS Governor Tabaković, the gold was repatriated to Serbia at the request of Serbian president Aleksandar Vucic. Vucic justified his decision by saying one cannot know what might happen.

France: 219 tonnes

Between 2013 and 2016, the Banque de France repatriated 219 t of gold to Paris, increasing its domestic holdings from 91% to 100%. Before the repatriation, the remaining 9% was likely stored in London. By August 2016, the Banque de France reported holding all 2,435 t of gold in its Paris vaults. This discreet move, observable only through data in Banque de France statements, was likely driven by France’s decision to offer gold lending in collaboration with J.P. Morgan, eliminating the need for London storage. The Banque de France’s repatriation of these 219 t of gold during the 2010s was the second largest central bank repatriation of the decade, surpassing the Dutch central bank’s, yet it received little media attention.

Türkiye: ~200+ tonnes

In 2017 and 2018, Türkiye’s central bank, the CBRT, repatriated significant amounts of gold from the Bank of England (100+ t), the New York Federal Reserve (28.7 t), and the Bank for International Settlements (19 t), driven by distrust of foreign custodians, increasing geopolitical tensions, a Turkish lira crisis, and a desire to reduce reliance on the US dollar. During this period, the CBRT increased its domestic gold reserves by over 200 t, moving the gold to Borsa Istanbul, while Turkish commercial banks such as Halk Bank, Ziraat, and VakıfBank also repatriated over 120 t of gold from the Bank of England to the Borsa Istanbul, reflecting Turkish government policy. These commercial banks and Borsa Istanbul are all majority owned by the Turkish government via Türkiye’s sovereign wealth fund, Türkiye Wealth Fund (TVF).

India: 215 tonnes

Between early 2022 and late 2024, the Reserve Bank of India (RBI) discreetly repatriated 215 t of gold from the Bank of England in London back to its vaults in Nagpur and Mumbai in India, with the amounts repatriated accelerating throughout that period. These gold transport operations, only revealed in the RBI’s half-yearly “Report on Foreign Exchange Reserves”, began soon after the outbreak of the war in Ukraine in February 2022 and suggest that the RBI gold movements were in response to heightened sanctions risks, which is especially relevant given that India is a founding BRICS member. The RBI is the world’s 8th largest sovereign gold holder and now holds 510 t of its gold domestically, equivalent to 58% of the total.

Failed Gold Repatriation Attempts

In addition to many successful gold repatriation operations, there have been failures due mainly to political and central bank resistance. This is true in the cases of Switzerland, Romania, and Slovakia.

In Switzerland, the “Save Our Swiss Gold Initiative” (2013–2014), organised by the Swiss People’s Party (SVP), led to a referendum that sought to compel the Swiss National Bank (SNB) to store all of its gold domestically, hold at least 20% of its assets in gold, and prohibit gold sales. At the time, SNB held 1,040 t of gold, with 70% stored in Bern, 20% in London, and 10% in Ottawa. However, the referendum clearly failed, partly due to the bundling of three clauses into a single vote, but also due to active opposition and interference from the normally apolitical SNB and then SNB chairman Thomas Jordan.

Following Hungary’s repatriation of 30 t of gold in 2018, gold repatriation efforts appeared in Romania, Hungary’s neighbour to the east, where senior Romanian politicians Liviu Dragnea and Serban Nicolae from the then ruling Social Democratic Party (PSD) proposed a bill in 2019 to repatriate 60 t of Romania’s gold stored at the Bank of England. Despite initial success, with both legislative chambers (the Chamber of Deputies and the Senate) passing the bill, the National Bank of Romania (NBR) and its governor Mugur Isarescu strongly opposed it. Using questionable claims, they argued that storing gold abroad was essential for financial stability. The opposition National Liberal Party (PNL), also against the repatriation, referred the bill to the Constitutional Court, where the Court deemed the bill to be constitutional. However, following a change in government in 2019, where the PSD lost power and the PNL gained power, Romanian president Klaus Iohannis, who was also aligned with the central bank, then vetoed the bill and sent it back to parliament to get rejected. This led to the bill’s effective shelving, and the Romanian gold remained in London.

In Slovakia, Robert Fico, who has been Slovak prime minister since 2023, but who in late 2019 was part of the government opposition, led an effort to repatriate the country’s gold from London, citing Brexit risks and financial instability. At the time, 31.5 t of gold was held by Slovakia’s central bank, the Národná Banka Slovenska (NBS), at the Bank of England. However, a parliamentary motion to discuss repatriation failed. As of December 2023, nearly all of Slovakia’s gold remains in London. However, with Fico back in power, the issue could resurface.

Despite public and political support, these cases reveal how political opposition, central bank influence, and institutional resistance often obstruct gold repatriation efforts.

China and Russia

And finally, we will mention two of the world’s largest gold holders, China and Russia. The People’s Bank of China (PBoC) regularly buys gold internationally, mainly in London, and promptly moves it back to Beijing. However, since these buying and transporting operations are so secretive, they go under the radar and are not classified as gold repatriation operations. However, they effectively are repatriating and immunizing the PBoC’s gold from sanctions risk. Jan Nieuwenhuijs estimates that the PBoC has accumulated 1,000 t of gold since the West froze Russia’s FX reserves in early 2022.

Russia’s central bank has also been highly perceptive in recognizing sanctions risks and has steadily built its gold reserves from 400 t in 2007 to over 2,300 t today. By accumulating gold from domestic production and storing it exclusively in Moscow and St. Petersburg, Russia has strategically prepared for geopolitical threats and ensured that its gold holdings are also protected from Western sanctions and the weaponisation of the financial system.

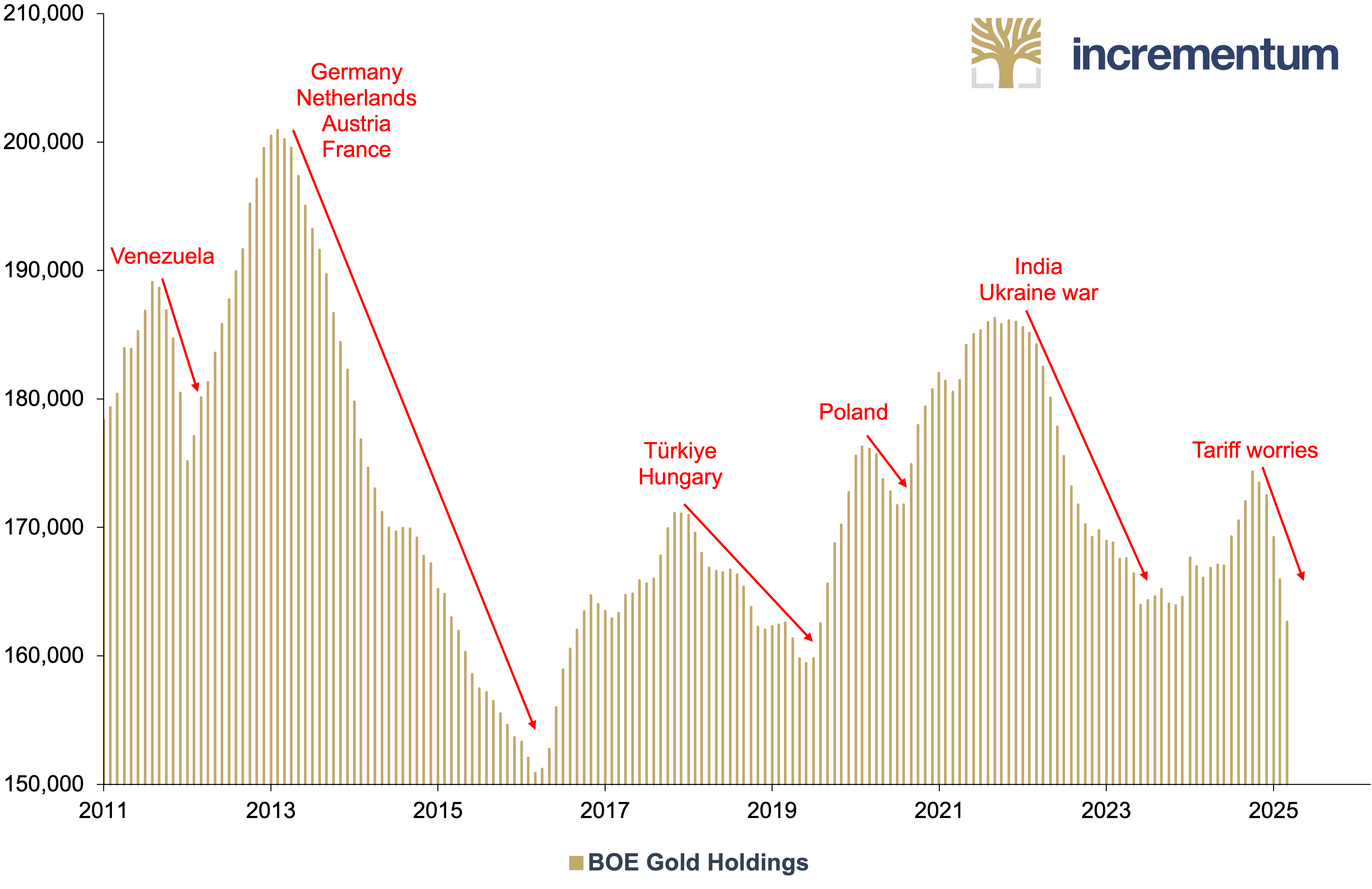

Bank of England Vault Data

As a gold custodian for both central bank and commercial bank customers, the Bank of England publishes end of month data on total gold held in its London vaults. Month-by-month changes in the data show net gold additions to or withdrawals from the vaults and reflect general trends over time.

Some observable trends are as follows: From August 2011 to January 2012, i.e. from Venezuela announcing to completing its 160-tonne gold repatriation, a sizeable 434 t of gold flowed out of the Bank of England vaults, suggesting that Venezuela’s actions likely prompted other central banks to follow suit and withdraw gold from London during that timeframe.

From March 2013 to March 2016, spanning the Bundesbank gold repatriation announcement in January 2013, the Dutch gold repatriation of 2014, and Austria’s repatriation announcement of May 2015, the Bank of England vaults saw consistent gold outflows every month, for a total net outflow of 1,557 t. This very large outflow suggests that other central banks understood the consequences of the German, Dutch and Austrian behavior, and also decided to remove gold from Western custodians.

In 2018, the Bank of England vaults saw a net outflow of 282 t of gold, most likely driven by significant repatriations by the Turkish central bank, Turkish commercial banks, and the first phase of Hungary’s gold transfer. Between April and June 2019, 98 t left the vaults, coinciding with the Polish central bank moving its gold to a G4S vault near Heathrow in preparation for repatriating 100 t to Poland between August and November 2019.

Triggered by Russia’s invasion of Ukraine, the Bank of England’s vaults also saw consistent monthly gold outflows from January 2022 to March 2023, with a net loss of 574 t. This is consistent with central banks perceiving heightened geopolitical and sanctions risks, and then likely repatriating gold for those reasons. The six months from April to September 2023 saw gold outflows of 73 t, which lines up nearly perfectly with the Reserve Bank of India’s gold repatriation of 71 t during that time.

The BOE’s holdings rose throughout the summer of 2024 and into the fall, peaking in October. Yet, they have declined since. Still, gold stocks in London’s commercial vaults have been increasing, which the LBMA attributes to gold moving from the BOE into the Loco London system.

BOE Gold Holdings, in Thousand Ounces, 01/2011–03/2025

Source: BOE, Incrementum AG

Conclusion – Not My Vault Keys, Not My Gold

Central bank gold repatriation is now an established trend and an accepted reality that continues to gain momentum, as proven by numerous central bank surveys. The West’s freezing of Russian FX reserves appears to have been a defining moment that shocked many of the world’s central banks into reassessing the importance of gold as a reserve asset.

Driven by a variety of motivations, ranging from facilitating audits and reducing reliance on foreign custodians to mitigating sanctions risk and strengthening economic sovereignty, gold repatriation also reflects the erosion of trust by central banks in each other and the global financial system, and the central banks’ attempts to find geopolitical safe havens.

Going forward, a continued deterioration of the geopolitical landscape and increased weaponisation of the US dollar and broader financial system will likely position gold repatriation as an even more important part of central bank reserve management and diminish the importance of the Western gold custodians as more gold finds its way back home.

Gold repatriation is much more than a set of logistical operations; it is a powerful message of central banks asserting sovereignty over their national wealth and signalling trust in physical gold held in their vaults while at the same time revealing the erosion of trust in the traditional financial institutions in the City of London and Manhattan.