Bitcoin & Gold – Our Multi-Asset Investment Strategy in Practice

“By combining them, investors benefit from the low correlation of the assets. In addition, they can use the volatility of Bitcoin to their advantage through rule-based rebalancing and thus reap the rebalancing bonus.”

In Gold We Trust report , 2019, p. 261

Key Takeaways

- We remain committed to our long-standing view that Bitcoin and gold are complementary assets.

- Although we believe that the role of digital stores of value will increase further, we do not expect Bitcoin to replace gold as a store of value.

- The live track record of our investment strategy consisting of Bitcoin and gold, has so far delivered outstanding investment results, meeting our high expectations.

- In our view, it is most effective to define a certain strategic allocation of cryptocurrencies and rebalance them regularly. This dampens the drawdown potential of cryptocurrencies within a portfolio and uses the volatility to the investors advantage.

- A combined crypto-gold portfolio seems to be particularly suitable for this purpose due to their relatively low correlation and the high volatility differential.

Back in 2015, we first included the topic of cryptocurrencies in our In Gold We Trust report. Since then, we have dealt intensively with this important topic in all its facets, devoting a separate chapter to it since 2016.[1] We continue the tradition this year. In our opinion, the increasing prevalence of cryptocurrencies in general and Bitcoin in particular has come about as a direct consequence of monetary climate change. Over the years, we have analyzed and reviewed a number of different aspects related to digital gold in our In Gold We Trust reports:

“Bitcoin and other cryptocurrencies are still in their infancy and it is very exciting to follow these developments. Time will tell whether other alternative currencies can establish themselves alongside gold in the long term, or whether cryptocurrencies will even usher in a new era with a revolutionized monetary system.” [2]

Many of our views on future developments eventually came to pass:

“Although Bitcoin and the underlying blockchain were originally designed to replicate the traits of gold that make it uniquely suited to be money, Bitcoin represents a unique asset class and can be an integral part of wealth management from the perspective of portfolio diversification.” [3]

Recently, the advantages and disadvantages of gold and Bitcoin have once again been discussed among investors and in various debates.[4] However, we do not want to compare gold with Bitcoin again this year, as we have already dealt with this topic in detail in the past. If you are interested in our thoughts, we would like to refer you to the chapter “Cryptos: Friend or Foe?” [5] in the In Gold We Trust report 2018, an analysis that has lost none of its topicality:

“…as we have tried to show in this chapter, gold and cryptocurrencies do not have to be viewed as opposites at all. Of course, each has its advantages and disadvantages. However, they complement each other and there is no reason to play one off against the other.” [6]

We remain committed to our long-standing view that Bitcoin and gold are complementary assets. Although we believe that the role of digital stores of value will tend to increase further, we do not expect Bitcoin to replace gold as a store of value.

In times of monetary climate change, the market for liquid, noninflationary assets is continuously growing. In the coming years, more and more capital will be looking for easily investable, quantitatively limited stores of value. In particular, rising price inflation rates and thus even lower real interest rates will further fuel the hunger for these value-preserving assets. In our view, being bullish on both assets is not a contradiction. On the contrary, a combined portfolio of digital and physical gold makes sense for many reasons. We expect these types of combined portfolios to be increasingly used, similar to how multi-asset portfolios now combine equity and bond asset classes. Here, too, a wide variety of combinations are conceivable, each of which can reflect a wide range of risk/return potentials.

Based on our conviction that portfolios consisting of precious metals and cryptocurrencies have an extremely promising risk/return potential, we have already launched two such investment strategies with different risk/return characteristics as investable mutual funds.[7]

Gold & Bitcoin – Stronger Together?

In this context, we would like to remind you of our contribution from the In Gold We Trust report 2019. In the chapter “Gold & Bitcoin – stronger together?” we pointed out in detail the advantages of a combined investment strategy of gold and Bitcoin.[8] Our suggestion was to combine the two assets in one portfolio and in case of strong deviations from the strategic asset allocation to return countercyclically to the initial positioning via an event-based rebalancing. For the rebalancing process, options can also play an important role to buy the underweighted assets by writing short puts and still achieve significant premium gains.[9] Analogously, covered calls can be written on the existing positions, which would have to be reduced anyway due to the overweighting.

The most important arguments for a rule-based, combined investment strategy at a glance:

- Reduction of volatility or of maximum drawdowns against cryptocurrencies

- Diversification effects and thus improved risk/return characteristics

- Maintaining an asymmetric payoff profile (right-skewed returns)

- Return optimization through systematic rebalancing (rebalancing bonus)[10]

- Significant cash flow income via an option writing overlay

To substantiate these theses, we analyzed a quantitative back-of-the-envelope calculation of a combined portfolio in 2019. We came to the following conclusion:

“By combining both assets, the investor benefits on the one hand from the low correlation of both assets; on the other hand he can use the volatility of Bitcoin to his advantage through a rule-based rebalancing. In addition, option strategies are also applicable, which generate an interesting return by collecting the option premiums and further lower the volatility.” [11]

Theoretical backtests should always be taken with a grain of salt when it comes to portfolio strategies. However, in the meantime, we have put the investment strategy into practice and have well over a year’s worth of data available for analysis. The task is to find out whether the combination of the two assets has also delivered in practice, i.e. after deduction of all fees and any implementation discrepancies due to the liquidity situation, etc., that we had expected ex-ante.

For the first investment strategy of this kind managed by us, we have chosen 25% Bitcoin and 75% gold as our strategic asset allocation.[12] When evaluating performance, we analyze all common risk/return ratios that allow risk-adjusted comparability of the price performance of the different investments. To ensure the best possible comparability, all ratios are based on logarithmic risk/return data.

Returns

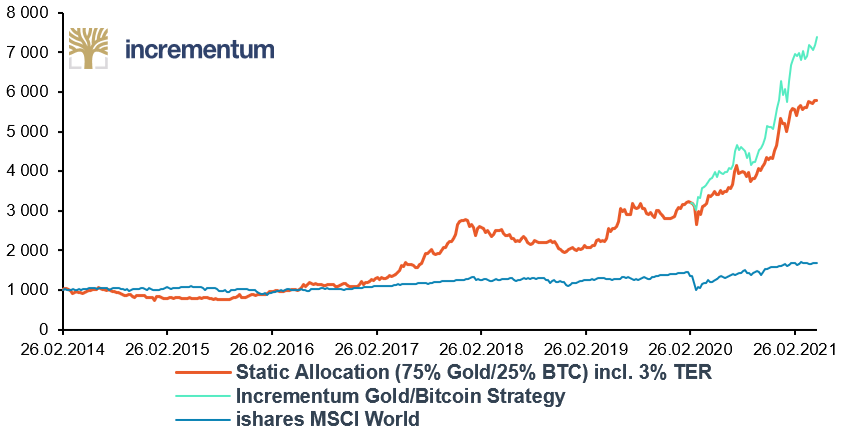

Let’s start with returns. We look at the historical returns of our strategic asset allocation compared to the returns of global equity markets. Additionally, we see the returns of the live track record of our strategy since the strategies launch on February 26, 2020.

Static Allocation (75% Gold /25% BTC) incl. 3% TER, Incrementum Gold/Bitcoin Strategy, and ishares MSCI World, 1,000 = 02/2014, 02/2014-05/2021

Source: Reuters Eikon, Incrementum AG

Since the launch of our strategy, the return is 131.2%. Gold posted a gain of 10.7% over the same period, Bitcoin of 520.9%. Our strategy was able to outperform the strategic asset allocation by 37.8 percentage points after deducting all costs.[13]

Distribution of Returns

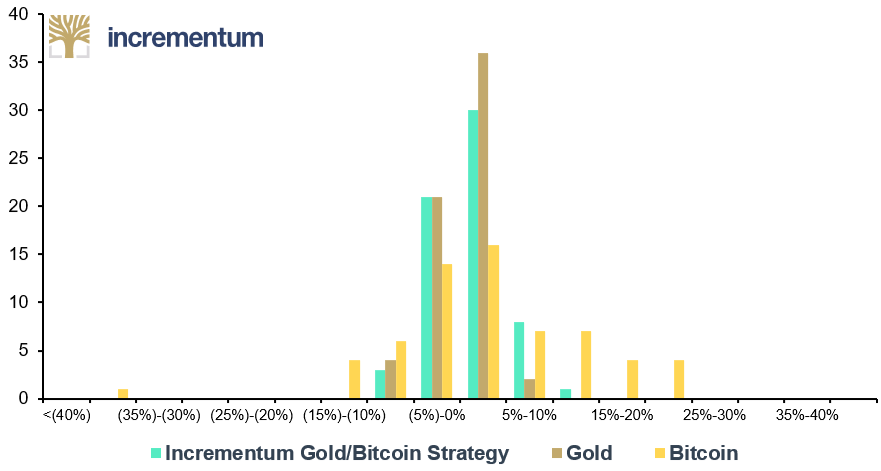

When it comes to the distribution of the returns, on the one hand one can observe that the strategies return distribution is similar to that of gold, except that it reflects the right-skewed nature of Bitcoin.

Distribution of log weekly returns of Gold, Bitcoin, and Incrementum Gold/Bitcoin Strategy, in %, 03/2020-05/2021

Source: Reuters Eikon, Incrementum AG

Risk

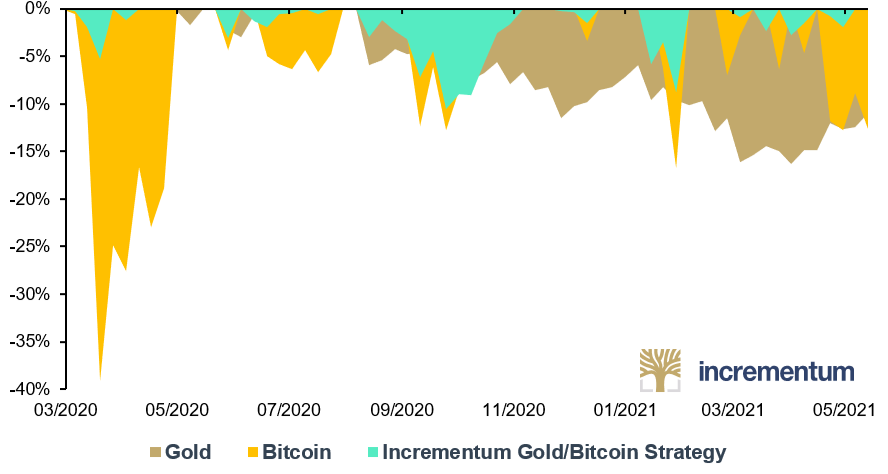

To assess risk, we look at the maximum drawdown. In our view, this is more informative than volatility, which does not adequately take into account any left-skewed moments in the distribution of returns.

Drawdown History of Gold, Bitcoin, and Incrementum Gold/Bitcoin Strategy, 03/2020-05/2021

Source: Reuters Eikon, Incrementum AG

Since the launch of our strategy, the “maximum drawdown” of Bitcoin was 39.1%, that of gold 16.3%, and that of our combined strategy 10.6%.

As discussed in the In Gold We Trust Report 2019, the combination of the two investments significantly reduced risk during the period under review. This is remarkable in that the strategy remarkably outperformed gold during the observation period.

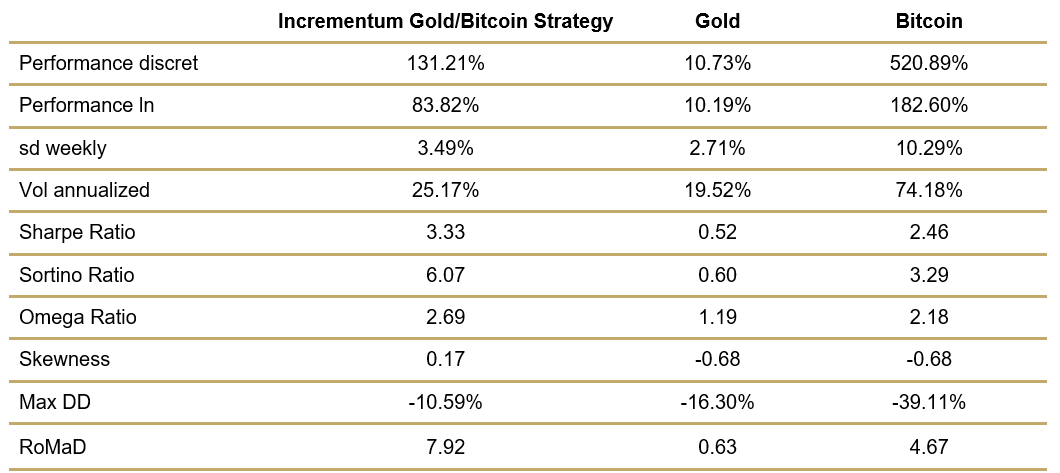

A risk-adjusted comparability of returns can best be quantified using the common risk/return figures. Here, we have calculated the Sharpe ratio[14], the Sortino ratio[15], the Omega ratio[16], and the return over maximum drawdown (RoMaD).[17]

Source: Reuters Eikon, Incrementum AG

All the risk/return ratios of our investment strategy were clearly superior to the two individual investments for the period under review. Of course, past performance does not allow any conclusions to be drawn about future performance.

Conclusion

We are convinced that a combination of selected cryptocurrencies – especially Bitcoin – within a diversified investment portfolio makes sense. The results achieved so far by our investment strategy clearly underline this thesis.

In our view, it is most effective to define a certain strategic allocation of cryptocurrencies and to rebalance them regularly. In this way, the high volatilities of the digital currencies can be dampened or used in favor of the investor. A combined crypto-gold portfolio seems to be particularly suitable for this purpose, as the relatively low correlation and the high volatility differential have a favorable effect on the so-called rebalancing bonus.

It is important to note, that past performance is no guarantee for future returns.

[1] See “Gold-Backed Tokens in 2020 – A Glimpse into The Future?”, In Gold We Trust report 2020, “Gold vs. Bitcoin vs. Stablecoins”, In Gold We Trust report 2019, “Gold and Bitcoin: Stronger Together?”, In Gold We Trust report 2019, “Crypto: Friend or Foe?”, In Gold We Trust report 2018, “In Bitcoin We Trust?”, In Gold We Trust report 2017, “Past, Present, and Future of the Monetary Order”, In Gold We Trust report 2015

[2] “Financial Repression: When the Grasping Hand of the State Runs Rampant”, In Gold We Trust report 2016, p. 111

[3] “In Bitcoin We Trust?”, In Gold We Trust report 2017, p. 114

[4] We also participated in a debate in this context and discussed with Saifedean Ammous, author of the book The Bitcoin Standard. The video of this conversation can be found here.

[5] See “Crypto: Friend or Foe?”, In Gold We Trust report 2018

[6] “Crypto: Friend or Foe?”, In Gold We Trust report 2018, p. 186

[7] See “The fruit of our labour – Our investment funds“, Incrementum AG

[8] See “Gold and Bitcoin: Stronger Together?”, In Gold We Trust report 2019

[9] When writing a put option, the writer commits himself to buy an asset at a defined price at a certain point in time and receives an option premium for it. Since an additional purchase is planned anyway in the case of an underweighting a premium can be generated via the writing for a transaction which one intends to carry out in the case of falling prices.

[1o] See Bernstein, William: “The Rebalancing Bonus: Theory and Practice”, 1996

[11] “Gold and Bitcoin: Stronger Together?”, In Gold We Trust report 2019, p. 261

[12] Meanwhile, we have launched a second, more dynamic strategy with a strategic allocation of 33% gold, 33% silver, and 33% cryptocurrencies.

[13] All return figures as of May 14, 2021

[14] The Sharpe ratio is the measure of risk-adjusted return of a financial portfolio. A portfolio with a higher Sharpe ratio is considered superior relative to its peers. It is measured as the excess portfolio return over the risk-free rate relative to its standard deviation.

[15] The Sortino ratio is a variation of the Sharpe ratio that differentiates harmful volatility from total overall volatility by using the asset’s standard deviation of negative portfolio returns – downside deviation – instead of the total standard deviation of portfolio returns.

[16] The omega ratio is a risk-adjusted performance measure calculated as the ratio of probability-weighted profits and losses.

[17] Return over maximum drawdown is the average return in a given period for a portfolio, expressed as a proportion of the maximum drawdown level. An investment with a RoMaD of 0.5 would be considered more attractive than one with a maximum drawdown of 40% and a return of 10% (RoMaD = 0.25)