Asteroid Mining and Deep-Sea Mining

Science Fiction or the Next Wave of Innovation in the Mining Space?

“Innovation opportunities do not come with the tempest but with the rustling of the breeze.”

Peter Drucker

- Deep-sea mining’s potential is vast, with 1,140 trillion dry tons (USD 200trn) of subsea mineral deposits presently available for extraction, according to the USGS.

- Pending the resolution of environmental and bureaucratic obstructions, deep sea mining could become commercially viable as soon as 2030, driven by demand for critical minerals.

- In 2023, asteroid mining made pioneering strides, after NASA’s OSIRIS-Rex mission returned with dirt samples, and its mission to asteroid 16 Psyche was embarked upon.

- When asteroid mining does become commercially viable, water and ice will be the priority, with gold potentially taking on an industrial role, as part of the “lunar economy”

Deep Sea Mining

The US Geological Survey (USGS) estimates that there are as much as 1,140 trillion dry tonnes of subsea mineral deposits presently available for extraction. Based on conservative estimates, this dwarfs terrestrial resources by a factor of 11 and amounts to a staggering value of at least USD 200trn.[1] Evidently, whilst not yet tapped into, the scale of the deep-sea mining opportunity is unrivalled. In addition, the distribution of resources across the world’s oceans is relatively broad-based.

Source: www.deepseamining.ac

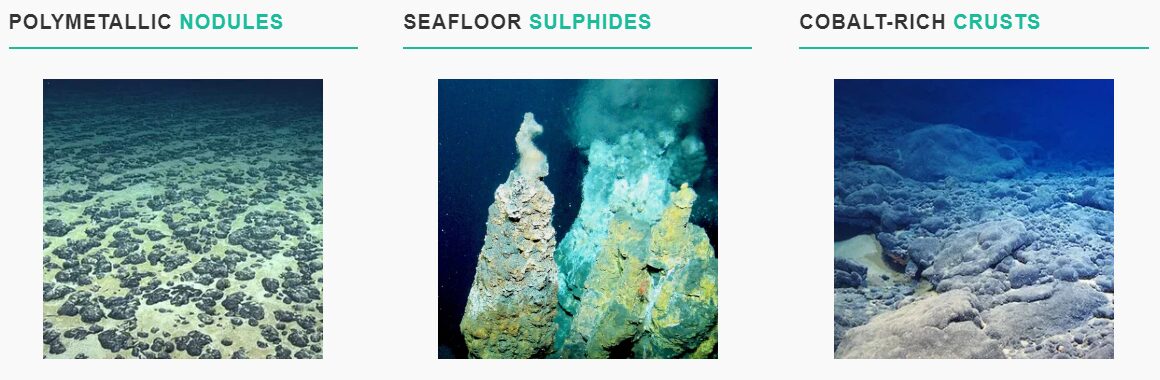

As for the geological constitution of the deep-sea deposits, the World Ocean Review categorises three main types. Firstly, there are polymetallic nodules, which are potato-shaped lumps that form on the deep abyssal plains of oceans and are high in quantities of manganese, nickel, copper, and cobalt. Secondly, there are cobalt-rich crusts: Formed by minerals precipitating out onto seamounts, these are mostly comprised of copper, nickel, manganese, and platinum. Thirdly, there are seabed massive sulphides. These are accumulations of minerals caused by geothermal activity, which are typically made up of copper, zinc, silver, and most relevantly, gold.

Source: www.deepseamining.ac

With all of this considered, it is important to note that deep-sea resource extraction is not a new process. Geologists have been aware of subsea minerals since 1873, and as oil and gas moved offshore in the late 1960s, so too did the mining industry.

Four offshore mining consortia formed in the early 1970s, including the Kennecott Consortium (Kennecott, Noranda, Consolidated Gold Fields and Mitsubishi), Ocean Mining Associates (a subsidiary of US Steel, amongst others), Ocean Management (partially owned by Schlumberger and Inco), and Ocean Minerals Company (formed with Lockheed, Billiton, Shell and Bos Kalis). These consortia successfully developed and tested a range of subsea mining technologies, but all failed to reach commercial production due to lack of regulatory environment and falling commodity prices, caused in part by the oil crisis.

The interim decades saw little technical progress. However, regulatory clarity improved, spurred by the signing of the United Nations Convention on the Law of the Sea (UNCLOS) in 1982 and the consequent formation of the International Seabed Authority (ISA) in 1994, which served to authorize and control development of mineral-related operations in the international seabed. The ISA began issuing subsea mineral exploration licenses in 2001 and has so far issued 30 exploration licenses to 22 contractors from a wide variety of countries, including Russia, China, Japan, Bulgaria, Cuba, France and India. The US is notably absent, as it has not ratified UNCLOS. Thus, it cannot sponsor exploration activity or guide developments at the ISA.

Notwithstanding this regulatory progress, extraction of metals from the deep-sea has been slow, with environmental backlash and bureaucracy standing in the way. More recently, a now-defunct deep sea mining company, Nautilus Minerals, was a victim of this environment. The Vancouver-based company was vying to develop its “Solwara 1” deep sea gold, copper and silver project off the coast of Papua New Guinea, but the project was plagued with community opposition and financial setbacks. Despite this, the tide is now changing due to a shortage of green metals – a trend that is pressuring stakeholders to take a second look at the seabed.

Source: www.deepseamining.ac

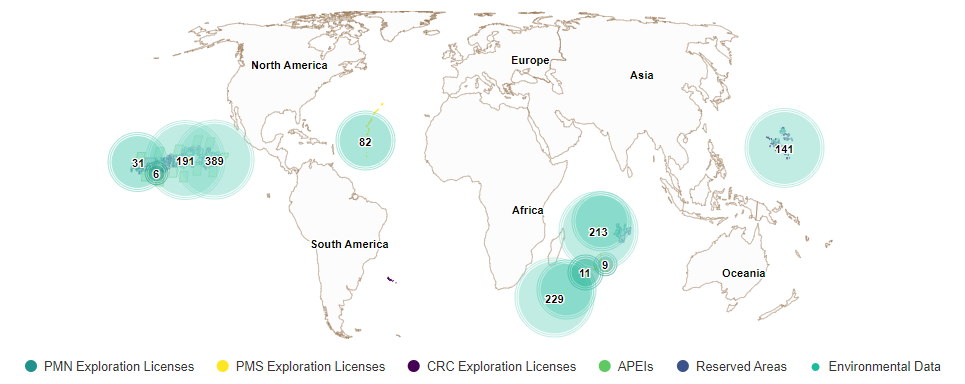

This trend is evidenced by Phillip Gales’ illuminating DeepData Explorer – a visual representation of the ISA’s publicly available DeepData resource. It illustrates the scale of the interest in deep sea mining, in the form of exploration licenses held by various governments and companies across the world.

In particular, the highest concentration of licenses pertains to the metal-rich treasure trove of the Pacific Ocean known as the Clarion-Clipperton Zone (CCZ). Here, The Metals Company (TMC), a Vancouver-based deep sea mining company with a vested interest in the CCZ, claims that tapping into the CCZ would be the equivalent of “Unlocking the World’s Largest Estimated Undeveloped Source of Battery Metals”. Furthermore, TMC posits that the CCZ’s seafloor contains over three times the global land reserves of nickel, over five times the land reserves of manganese, and over 12 times the land reserves of cobalt.

Nickel, Cobalt, Manganese Reserves

Source: TMC, Incrementum AG

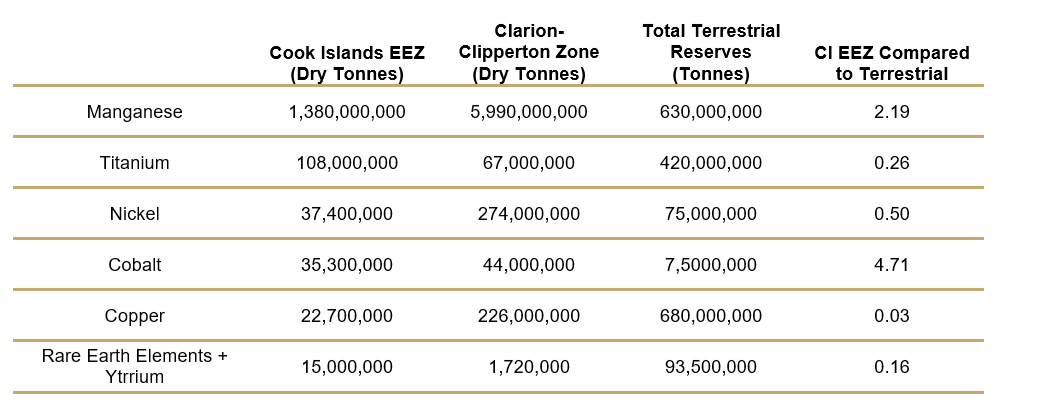

Importantly, the scale of the deep-sea mining opportunity does not end with the CCZ, as significant subsea mineral resources exist in a variety of areas around the world. These include the Penrhyn Basin near the Cook Islands, the Peru Basin around 200nm west of Peru and Chile, the Prime Crust Zone located in the North Pacific, as well as the Mid-Indian Ocean Ridge. Of these areas, the Cook Islands is arguably the one to watch. Here, recently adopted government commitments continue to edge the region towards commercial viability.

Estimated Cook Islands Resources

Source: deepseamining, Incrementum AG

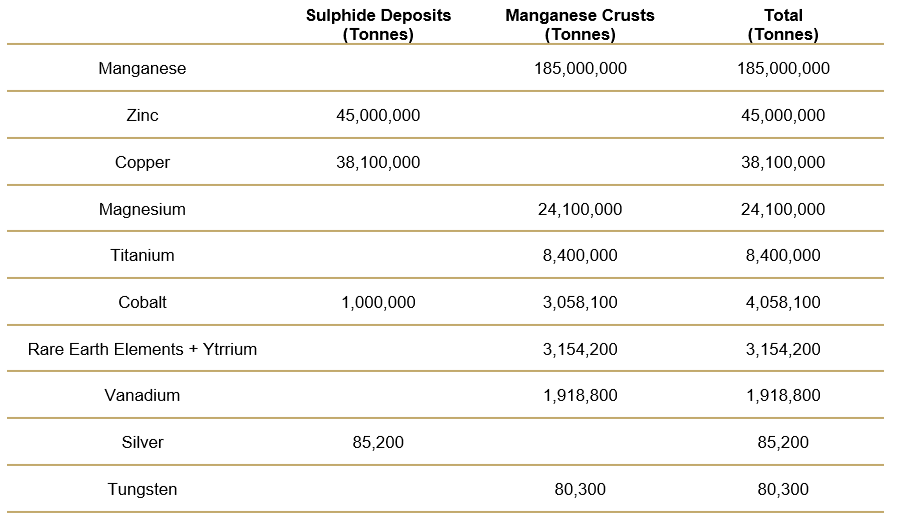

In addition to the Pacific, subsea minerals have been found in the seas around Europe, including in the Norwegian Exclusive Economic Zone (NEEZ) located in the North Sea. Here, as recently as January, Norway’s parliament voted in favour of opening its waters for commercial-scale deep-sea mining, which was swiftly countered by a letter from EU lawmakers urging Norway to reconsider. Regardless, this progress will be music to the ears of Norway-based deep sea mining company Loke Minerals, which is tapping into a resource that is purported to contain around 310 million tonnes of minerals, including around 3 million tonnes of rare earth elements, according to the Norwegian Offshore Directorate.

Estimated Norwegian EEZ Resources

Source: deepseamining, Incrementum AG

Moreover, US behemoths like Transocean are also entering the fray, as smaller firms such as Chatham Resources Phosphate and Manuka add to the competitive environment. In the same vein, Moana Minerals and CIIC are notable companies with exploration licenses in the Cook Islands EEZ, and European dredging companies like Allseas and DEME are active in building equipment.

Naturally, it is logical to focus on these private companies and the handful of capitalist countries that make the headlines. However, state-backed entities like China Minmetals, COMRA, Beijing Pioneer, JOGMEC (Japanese Metals), and the Indian Ministry of Earth Sciences also leverage huge state treasuries and unified industrial policies to quietly capture acreage and potentially dominate the seabed.

Meanwhile, capitalist fervour in the industry extends into banking, where specialist private equity firms like The Seafloor Minerals Fund are structuring investment entities for select investors to gain exposure to this space. The opportunity is certainly enticing for those with the risk appetite; work by the USGS in 2013 indicated that a 20,000km² license area of polymetallic nodules in the Cook Islands could support as many as seven concurrent mining operations, each operating for 20 years, producing around 2mn dry tonnes per site per year at an estimated value of USD 1,111 per ton. For context, TMC has 149,543km² of licenses for polymetallic nodules in the CCZ via their NORI and TOML subsidiaries. As a result, investors see the potential for many multi-billion-dollar subsea mineral super majors and are optimistic about significant returns in the future.

Source: www.deepseamining.ac

Ultimately, the scale of the resource in the aforementioned areas is precisely why deep-sea mining is being highlighted as an opportunity for Western nations to reduce their dependence on China and Russia for their critical metals supply. This is the opinion of Rep. Carol Miller, who, in March, pushed for US federal agencies to increase deep sea mining funding via the Responsible Use of Seafloor Resources Act of 2024, on the basis that the “United States should not be beholden to China for critical minerals”. A similar belief is shared by Walter Soggnes, CEO of Loke Minerals, who exclusively told us in an interview that “Deep sea mining is the vehicle for the West to decouple from China and Russia” [2].

Thus, on the surface, deep-sea mining appears to be a no-brainer for the West. However, wading into the water to obtain valuable commodities has not always been plain sailing, with public fear of environmental risks being the principal stumbling block. For example, the 2010 BP Deepwater Horizon spillage left a lasting stain on the resources industry: 11 men died, and the spill damaged large swathes of marine life, including the Kemp’s Ridley sea turtle, whose species plummeted to near extinction due to the spill. The conflation of risks in the public eye, particularly in the wake of offshore oil spills like Deepwater Horizon and ocean-related incidents like the Fukushima nuclear disaster, further adds to challenges standing in the way of deep-sea mining companies today.

Source: NOAA

In November 2023, Greenpeace docked a TMC vessel to protest against what they perceive as damage that deep-sea mining would do to undiscovered marine species. The protestors stayed on the vessel for a full week, until a ruling from a Dutch court ordered Greenpeace to disembark – an order they opted to obey by protesting on the water around the vessel.

Ironically, Greenpeace disrupted TMC when they were carrying out their 19th scientific test so far. As a byproduct of this research, which has drafted in academics from MIT, TMC are now confident that 92–98% of the “plume” from their pilot nodule collector vehicle either settled back down or rose only 2 meters above the sea floor. According to the research, this means the suffocating effect that the plume has on marine life has been overstated.

Source: The Metals Company, p. 40

Unsurprisingly, Greenpeace maintained their opposition, responding in a press release via a quote from Alex Rogers, professor of biology at Oxford University: “The Metals Company has cynically attempted to subvert a democratic process and push countries into accepting commercial-scale mining before sufficient science is available to make an informed decision”.

Of course, having their research disrupted by protestors is an inconvenience for TMC. However, it is not the most effective strategy devised by the environmental groups. That strategy has been to apply pressure through the mechanism of a deep-sea mining moratorium, which has resulted in companies and governments folding to their demands.

The UK government signed the deep-sea mining moratorium a month before COP28, making an immediate U-turn, having only just sponsored Loke Minerals for licenses in the CCZ. Additionally, Andrew Forrest committed his Fortescue Metals Group, the 8th largest mining company in the world, to a similar moratorium. Meanwhile, the world’s 2nd largest mining company, Rio Tinto, also came out in condemnation of deep-sea mining in their November 2023 statement:

Rio Tinto has no plans to carry out deep-sea mining activities. We believe that not enough is known about the impacts of deep-sea mining, and that it should not take place unless comprehensive scientific research refutes currently held evidence that it will create significant environmental and socio-economic implications.

Of course, there is an obvious non-environmental explanation why majors would not want deep-sea mining companies to succeed: It would flood the market with a supply that would likely quash the prices of the metals they mined. Naturally, it makes sense to see TMC CEO Gerard Baron respond to terrestrial miners combatively: “We’re not suggesting that this is a zero-impact activity, but what we are suggesting is that the impacts are a fraction compared to the land-based alternatives.”

Despite this opposition, the silence from the likes of BHP and Glencore on deepsea mining suggests they are at least considering the endeavour. This fits with the view of Loke Minerals CEO Walter Soggnes, who is of the opinion that “Eventually the major miners will partner with deep sea miners once they realise the opportunity” [3]. Frankly, whether the majors get involved with deep sea mining in the future will depend on the verdict of a UN-backed regulatory body, the International Seabed Authority (ISA), which has a legal mandate to deliver a code of practice for the deep-sea mining industry. However, whilst TMC expects this mining code to be finished in 2024 and adopted in 2025, the original deadlines set by the ISA in 2020 and 2023 were never met.

In summary, there are clearly still hoops to jump through before metals from the seabed enter the market. Although, if we extrapolate the current trajectory of progression and consider all the factors discussed, we expect to see the sparks of commercialisation to have been kindled by 2030. In the meantime, investors may wish to consider building their positions in deep sea mining companies before the commodity supercycle takes on an amphibious quality, extending itself from terrestrial practices and onto the seabed.

Initially, we expect growth in this nascent industry to stem from critical minerals, as licenses are principally being approved based on their ability to ensure energy security, amidst a time of geopolitical uncertainty. On the other hand, we recognise that gold exploration – whilst not presently an immediate priority for most deep-sea miners – could receive interest, as financial institutions seek a sturdy mast to tie themselves to amidst increasingly choppy monetary waters. For now, though, this threat is merely a drop in the ocean, as there are only 4.5 parts per billion of gold in the CCZ, and virtually nothing elsewhere, according to leading estimates.[4]

Asteroid Mining

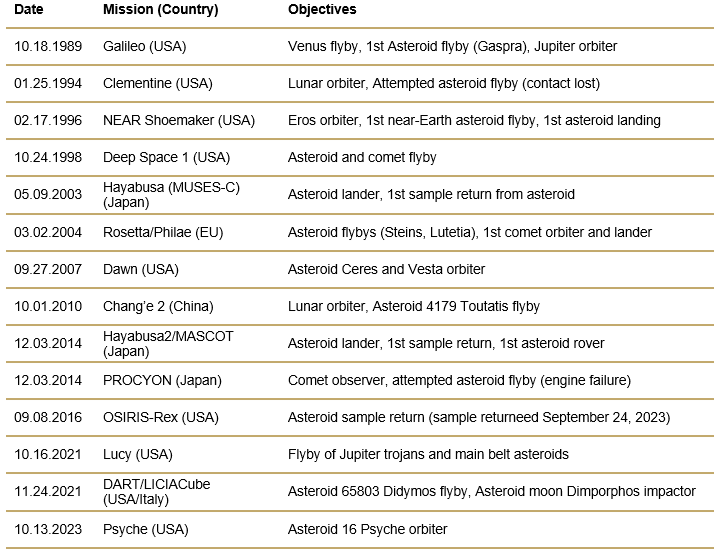

Without a doubt, November 24, 2023 marked mankind’s greatest step yet toward asteroid mining viability. That was the date when NASA’s and MIT’s “OSIRIS-REx” spacecraft arrived back from its 7-year voyage, carrying a 250-gram sample from near-earth asteroid Bennu. This marked the largest retrieval of asteroid material since Japan’s Hayabusa 2 mission returned 5 grams in 2020.

However, despite this success, the composition of both asteroid sample were not metal, but mostly dirt, dust, and rocks. Therefore, the first thing to bear in mind when it comes to asteroid mining of metals is that the industry is still very much in its infancy. That being said, material progress has been made toward commercial viability in the last three decades.

Asteroid Mining Progression Timeline

Source: eoportal, NASA, Incrementum AG

An example of this recent progress is NASA’s Lucy mission, which will become the first spacecraft to re-enter Earth’s vicinity from the outer solar system, when it returns from its trip to the Jupiter Trojan asteroids. A further example is the USItaly backed DART mission, which accomplished the first-ever asteroid deflection on September 26, 2022, successfully changing the motion of asteroid Dimorphos upon kinetic impact. Both developments were necessary for building the foundations for commercial asteroid mining. Particularly, the DART mission helps mitigate the existential risk of asteroid mining, as it demonstrates mankind’s ability to redirect the trajectory of asteroid fragments away from Earth. Despite this, neither DART nor Lucy present the biggest threat to the supply-demand balance of gold or other metals.

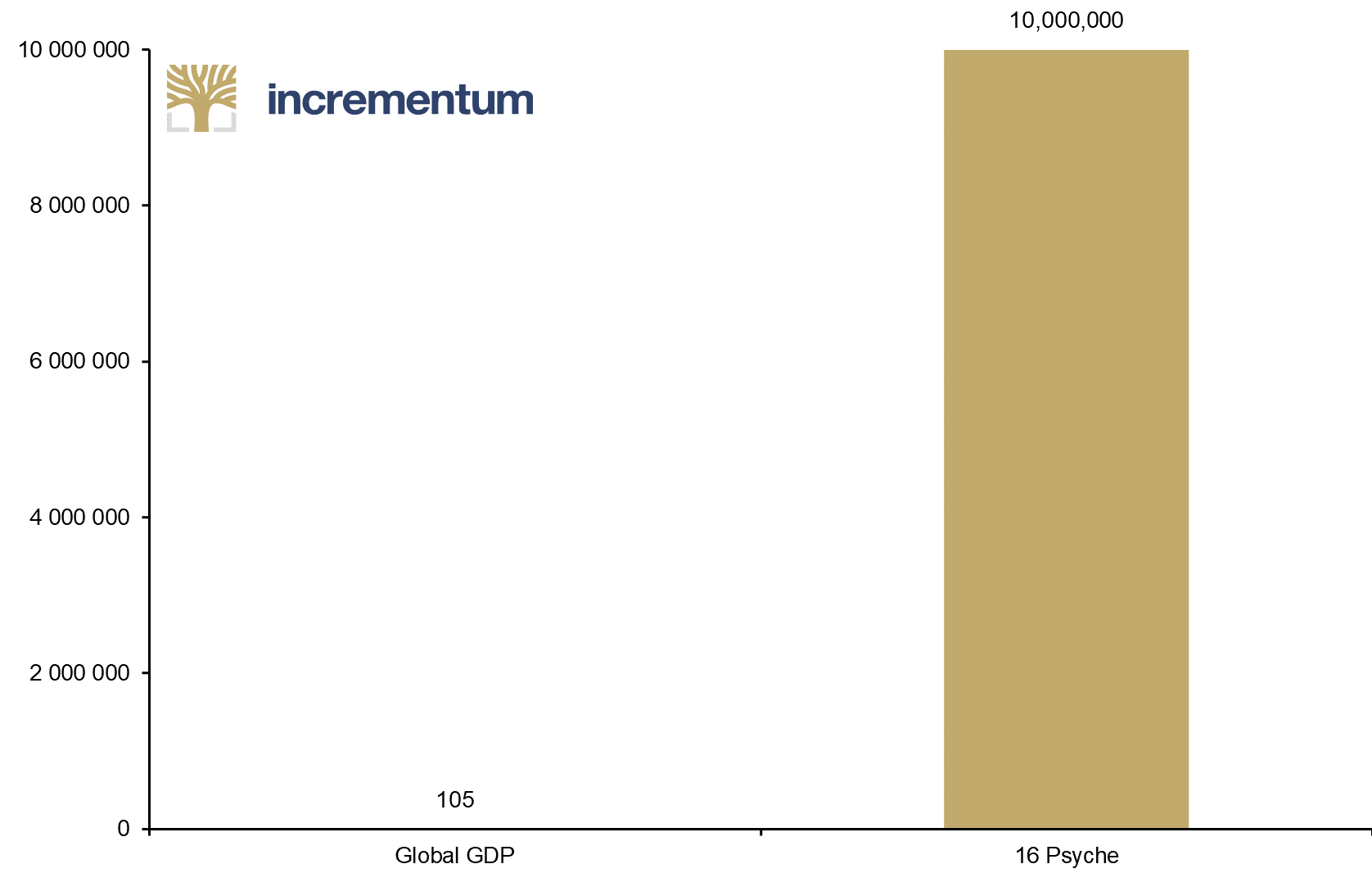

Instead, for the potential biggest “threat”, we must turn to NASA’s Psyche, a spacecraft that embarked on its maiden voyage on October 13th 2023 to study the eponymous asteroid, 16 Psyche. For context, the distance between 16 Psyche and Earth is 580 times the distance between Earth and Moon, whilst 16 Psyche has not even 0.5% of the surface area of the Moon. Moreover, 16 Psyche is classified as an M-type asteroid and is believed to have a 60% nickel-iron core, as well as significant veins of gold mineralization. Consequently, Forbes was one of the countless media outlets running with a USD 10,000 quadrillion total valuation for 16 Psyche – a figure that is not only 38.5 million times the value of the total gold supply on earth, but also 96.1 times the value of the USD 104trn global economy.

Global GDP and Value of 16 Psyche (log), in USD trn, 2023

Source: IMF, Forbes, Incrementum AG

It is no wonder, therefore, that 16 Psyche is being coined the “golden asteroid”. However, before droves of investors rush off to sell their gold, we should outline the limitations of the present 16 Psyche valuation methodology. Firstly, given the lack of concrete geological data, assumptions have been made based on metrics such as density, which cannot be relied upon to tell the full metallurgical story. Consequently, even leading academics cannot be 100% sure of 16 Psyche’s composition. For instance, the vice president of the Interplanetary Initiative at Arizona State University, Lindy Elkins-Tanton, stated in a recent academic paper: “Whether Psyche is a whole body or a rubble pile is unknown”, adding “There are still contradictions in the compilation of all current data”.[5]

In light of these insights, the USD 10,000 quadrillion value seems more like a stab in the dark than a realistic estimate. However, even if we assume the figures are accurate, there are still numerous reasons to suggest that commercial asteroid mining remains (light) years away.

Firstly, the current gold price would almost certainly not cover the AISC, a point confirmed by Bloomberg opinion columnist Javier Blas, who calculated that the price of a precious metal such as gold would need to jump 140,000-fold for asteroid mining to become profitable. Secondly, the incentive to secure a resource such as 16 Psyche is invalidated by the nature of its overabundance in gold. That is, miners would be foolish to spend billions of dollars on capital expenditure to mine the gold and arrange for its transportation back to Earth, as it would overwhelm the terrestrial gold supply, sending the gold price into the red, along with the miners’ bank balance.

Frankly, even if mining on 16 Psyche were to go ahead, the time it would take to return the gold to Earth would be relatively astronomical. Consider that the planning for 16 Psyche began way back in 2011, when a team of scientists began work on a preliminary report that eventually grew to 1,000 pages by 2016. Following this, NASA incorporated space marines into their program in 2017, marking the start of a 6-year R&D period that lasted until Psyche’s eventual launch in 2023. From here, the Psyche spacecraft is expected to dock with the asteroid in late July 2029, before arriving back on Earth around 2034. Such is the due diligence that goes into these pioneering projects that the research which ensues will likely take a further five years, taking us to 2039 before commercial mining of 16 Psyche becomes a viable proposition.

It is precisely these factors – the excessive lead times and substantial cost of gold delivery from asteroid to earth – that explain why mining industry experts do not foresee asteroid-mined gold becoming a threat to the terrestrial gold supply. Instead, the consensus is that, with time, asteroid-mined gold will become an increasingly significant asset of what Canadian Asteroid Mining Corporation CEO Daniel Sax refers to as a “huge paradigm shift towards a self-sustaining space economy” [6]. A similar view is shared by Emily King, founder of Prospector, an AIenabled search engine for institutional investors in the mining industry, who states that “Commercial extraction will be happening within the next two decades; however, the commercial space ecosystem is very much focused on how things will be used in space as opposed to bringing the resources back to Earth.” [7]

Sax, whose company is focused on contributing to the lunar infrastructure, also added, “The value in mining gold from asteroids would come down to its industrial value in space rather than the monetary incentives back on earth” [8], suggesting that the terrestrial gold price may be somewhat insulated from asteroid mining supply risks, at least until a robust industrial (or monetary) demand is sought in space.

Incidentally, gold is not currently being sought out in space at all and is missing from the exploration shopping lists of most asteroid miners today. According to Sax, this is because “For the most part, the focus is on ice, water, and helium 3 – the latter of which is used in fusion reactors and slotted to come online within the next 10 years” [9]. Therefore, when Neil deGrasse Tyson posits that the “The first trillionaire there will ever be is the person who exploits the natural resources of asteroids” (min 11:10), it is likely that he is referring to a different type of gold rush, driven by a demand for water and ice, and not necessarily for precious metals.

This conclusion is reinforced by examples such as the aforementioned OSIRIS-REx mission, whose prime motivation was to find water and ice, as well as by private space logistics start-up TransAstra, which recently received funding from NASA’s Innovative Advanced Concepts (NIAC) programme, specifically for the development of water and ice mining technologies. Here, whilst CEO Joel Sercel makes the case that it will eventually “make sense to harvest precious metals from smaller asteroids”, the immediate objective of TransAstra is to travel to an asteroid about the size of a house and extract from it some 100 tonnes of water – enough to fill a small backyard swimming pool. Given the cost of sending water into orbit, “that 100 tons of water is worth about $1 billion in space,” Sercel says, coinciding with King’s market bifurcation prediction of “a space economy where price is separate from the price determined on Earth”.[10] Thus, there is a possibility that asteroid mining activities may be relatively inconsequential for the prices of metals back on Earth, including gold.

Despite all of these challenges, the scale of the asteroid mining opportunity is undoubtedly attracting capital from places where traditional mining seldom ventures. Founded in 2022, asteroid mining company Astroforge – which is particularly targeting asteroids containing platinum group metals – is one of these entities. It raised a substantial USD 13mn of capital in May 2022. Similarly, a startup from the Colorado School of Mines, Lunar Outpost, raised USD 12mn last year to fund its rollout of robotic lunar rovers, with the school more broadly being a recipient of funding from NASA, specifically for the development of water and ice mining technologies.

On one hand, these start-ups’ ability to raise capital may be down to the implied attractiveness of asteroid mining versus terrestrial mining practices. In 2015, it became even more attractive, as the US passed the Commercial Space Launch Competitiveness Act. This replaced the 1967 Outer Space Treaty, which prohibited national governments from staking claims to control over “celestial bodies” such as the Moon. Since then, private companies have been less restricted and more incentivised to undertake mining work beyond Earth.

On the other hand, the real incentives for asteroid mining may lie in the sheer amount of IP attached, where huge volumes of potential patents – e.g. from AI applications and NASA’s recent patent listing for “modular” refining systems in space – are enticing investment. With the global market value of the asteroid mining industry forecasted to increase to some USD 3.87bn by 2025 – from USD 712mn in 2017 – the gravitational pull of this opportunity is not going away any time soon.

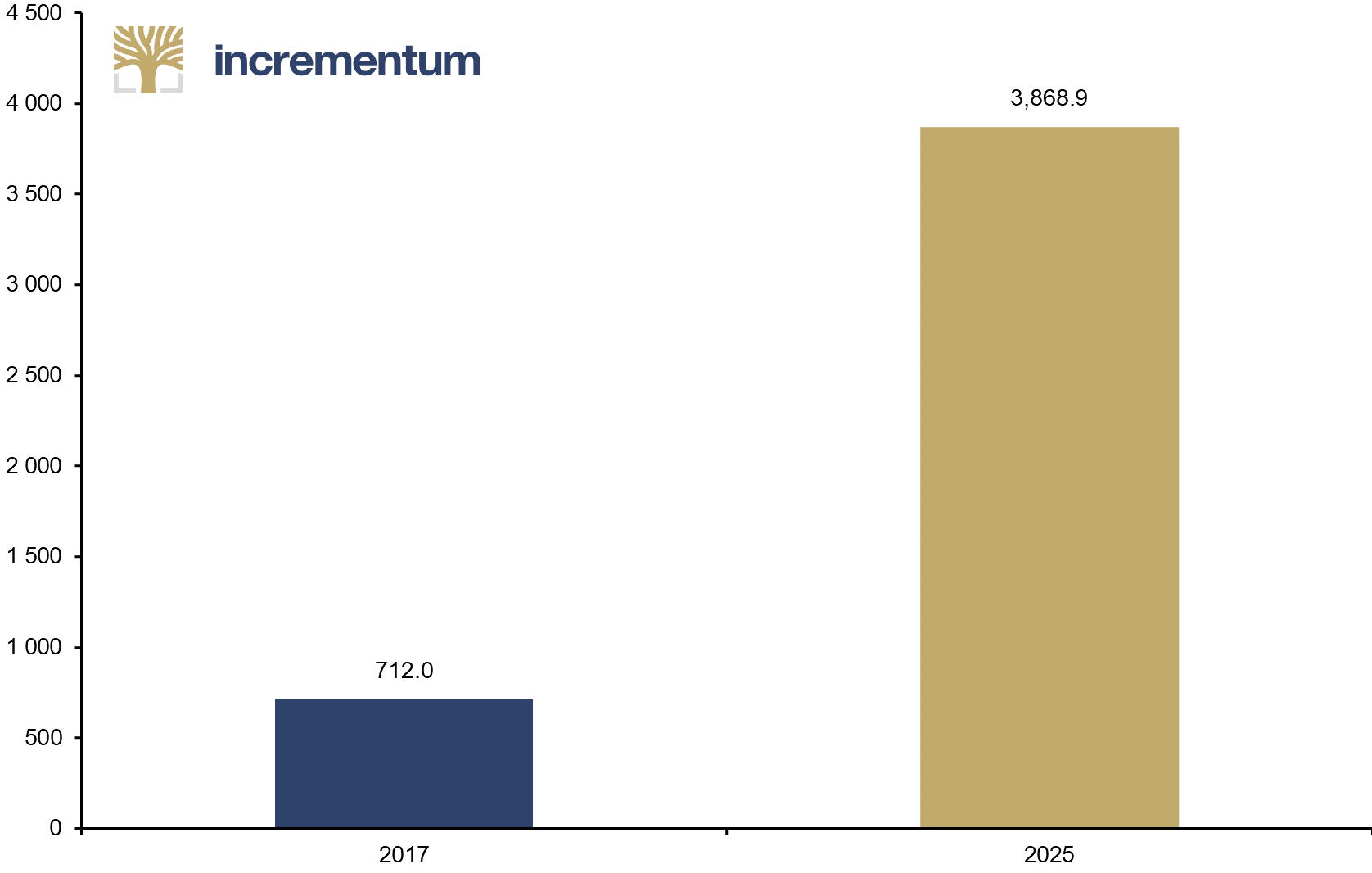

Market Value of Asteroid Mining, in USD mn, 2017–2025

Source: Statista, Incrementum AG

Conclusion

As alluded to earlier, commercial asteroid mining is more an inevitability than a probability, especially as trailblazing entrepreneurs such as Elon Musk continue to bang the drum for a future in which we exist as an interplanetary species. Meanwhile, the proximity of deep-sea mining to commercial viability appears closer than that of asteroid mining, as stakeholders will likely opt for practices sharing homogeneity with terrestrial mining and oil drilling practices, when the increasingly urgent need for commodities hits home.

Still, the question of interest for you, esteemed readers, pertains to whether the gold price will be negatively affected by the practices of either asteroid mining or deep-sea mining. In summary, we are of the disposition that the gold price will be largely insulated from the risks of a seabed-sourced or an asteroid-sourced oversupply.

This is because critical minerals will be the immediate priority for those scouring the seabed, as the world tentatively straddles the gap from brown to green energy. Meanwhile, the incentive structures to encourage asteroid mining are shaped towards creating a lunar economy, at least as things stand. Consequently, the terrestrial price of gold may dodge the proverbial bullet, as far as a flooding of the gold supply is concerned.

[1] Mizell, K. et. al.: “Estimates of Metals Contained in Abyssal Manganese Nodules and Ferromanganese Crusts in the Global Ocean Based on Regional Variations and Genetic Types of Nodules”, in: Sharma, R (ed.): Perspectives on Deep-Sea Mining, Springer, 2000, p. 54

[2] Interview with Walter Soggnes at Mines and Money London on November 29, 2023, conducted by Ted Butler.

[3] Interview with Walter Soggnes at Mines and Money London on November 29, 2023, conducted by Ted Butler.

[4] Mizell, Kira et al. “Estimates of Metals Contained in Abyssal Manganese Nodules and Ferromanganese Crusts in the Global Ocean Based on Regional Variations and Genetic Types of Nodules”, Perspectives on Deep-Sea Mining, 2022, p. 53–80

[5] Elkins-Tanton, Lindy T. et al.: “Observations, Meteorites, and Models: A Preflight Assessment of the Composition and Formation of (16) Psyche”, JGR Planets, Vol. 125, Nr. 3, March 2020

[6] Interview with Daniel Sax via Zoom on November 15, 2023, conducted by Ted Butler.

[7] Interview with Emily King on November 15, 2023, conducted by Ted Butler.

[8] Interview with Daniel Sax via Zoom on November 15, 2023, conducted by Ted Butler.

[9] Interview with Daniel Sax via Zoom on November 15, 2023, conducted by Ted Butler.

[10] Interview with Emily King on November 15, 2023, conducted by Ted Butler.