Ein monetärer Wendepunkt: Bitcoins Aufstieg zur strategischen Reservewährung

“From this day on, America will follow the rule that every Bitcoiner knows very well: Never sell your Bitcoin.”

Donald J. Trump

- The US Strategic Bitcoin Reserve is a historic event which confirms that the government of the world’s largest economy officially views Bitcoin as a monetary good. A revaluation of the gold certificates held by the federal government and deposited at the Federal Reserve could fund Bitcoin acquisitions in a budget-neutral manner.

- Nation-state adoption is accelerating, with approximately 2.5% of all Bitcoin now held by governments. As countries compete for strategic positioning, growing interest from middle powers and sovereign wealth funds could trigger a reflexive response.

- As sovereign and corporate adoption introduces more long-term holders, Bitcoin’s price action may decouple from tech stocks as it is increasingly viewed and utilized as a neutral reserve asset.

- Corporate treasury adoption of Bitcoin will likely continue to accompany government acquisitions, with companies like Strategy and GameStop issuing various types of securities to raise billions in capital for Bitcoin purchases.

- By innovatively structuring securities across different layers of the corporate capital structure — such as convertible bonds or preferred stock— companies can access new segments of the deeply liquid capital markets. This enables investors to gain Bitcoin exposure tailored to their individual risk preferences.

- As the global monetary system shifts, Bitcoin is increasingly positioned as a complementary reserve asset alongside gold. If current macro trends persist, a tenfold increase in Bitcoin’s price by 2030 lies well within the realm of possibility.

It’s fascinating to see what can happen in just one year in the world of Bitcoin. The pace of change is relentless, narratives evolve, and what once seemed radical can quickly become consensus. So, let’s address the elephant in the room immediately: the strategic Bitcoin reserve.

Last year, we presented a thought experiment, “freeBitcoin/freegold,” outlining a system where Bitcoin and gold are used to recapitalize an indebted and broken fiat system. Specifically, we wrote, “a rapidly appreciating reserve currency such as Bitcoin can contribute to a faster recapitalization of the overindebted system”. Who would have thought that only 12 months later, we would witness our thought experience becoming reality?

President Trump with David Sacks and Bo Hines; source: Wikimedia

But first, let’s go back a few steps and look at how the current situation has evolved. In 2023, the Presidential candidates Robert F. Kennedy Jr., Ron DeSantis, and Vivek Ramaswamy made headlines for their public support of Bitcoin. For the first time, there was a slim chance that citizens in the United States of America would elect a pro-Bitcoin President. On the other hand, Donald Trump had been explicitly negative about Bitcoin in the past and, at that time, still had not changed his stance.

However, by mid-2024, during his campaign for a second term, Trump’s stance had notably shifted. In July 2024, he became the first presidential candidate to accept digital assets as campaign donations and announced plans to establish a federal Bitcoin stockpile if re-elected. This change aligned with the Republican Party’s broader adoption of pro-cryptocurrency policies around the same time.

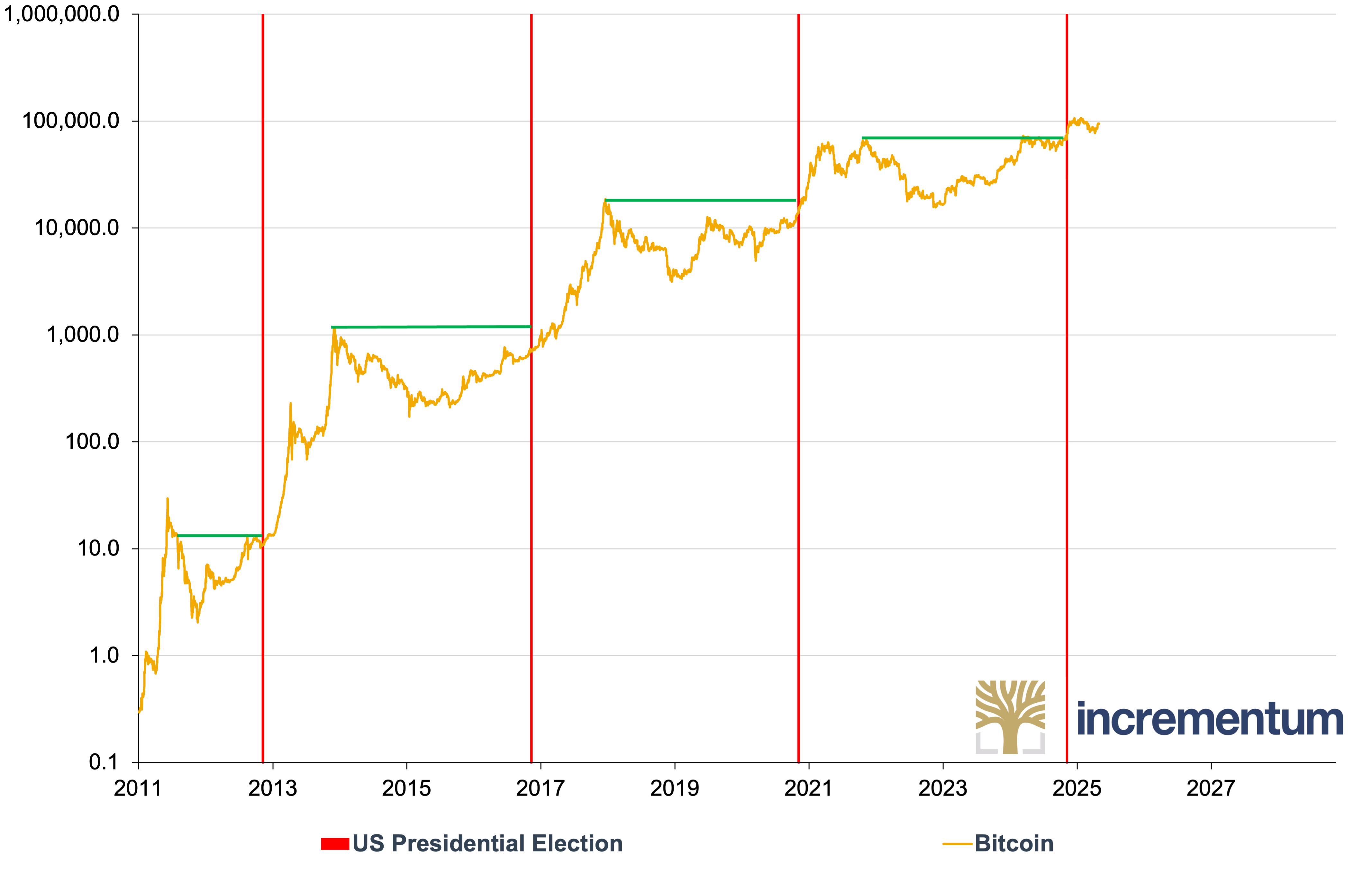

Bitcoin Price Development after US Presidential Election (log), in USD, 01/2011–04/2025

Source: blockchain.com, LSEG, Incrementum AG

Since becoming the 47th President of the United States, Donald Trump has upheld major promises to Bitcoin enthusiasts, including pardoning Silk Road creator Ross Ulbricht, who was serving a double life sentence in a US prison. Trump’s most considerable promise was the creation of a Strategic Bitcoin Reserve, which the President established in March via an executive order.

Now, game theory is kicking into an even higher gear. With the US officially recognizing Bitcoin as a strategic asset, other nations are unlikely to sit idly. The race to accumulate national reserves of the world’s most scarce digital asset has likely just begun. In a world of rising geopolitical tensions and declining trust in the creditworthiness of government debt, Bitcoin is emerging as not only a store of value but a tool for monetary positioning and sovereign leverage.

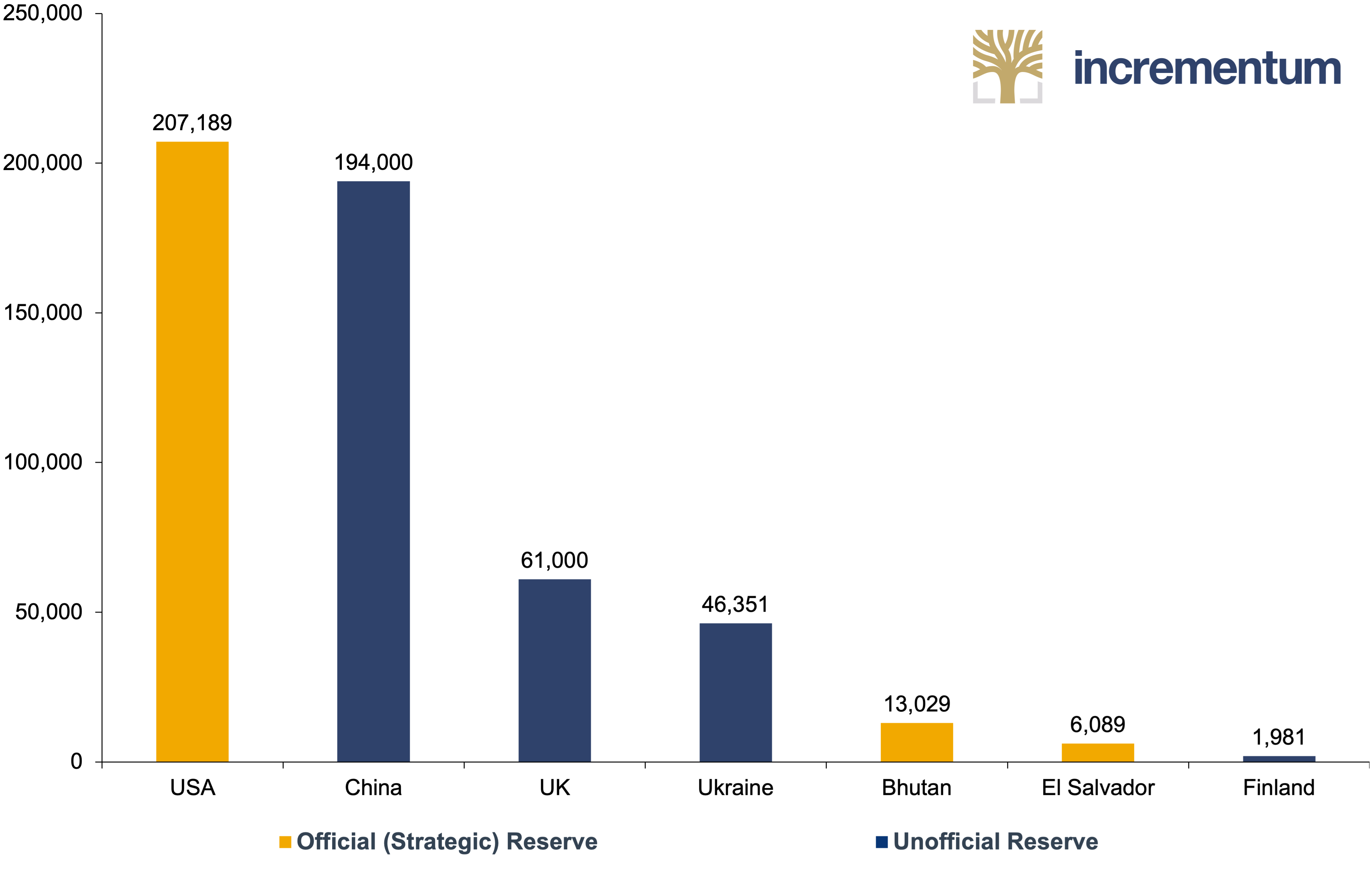

Bitcoin Holdings of Governments, in Bitcoins, 03/2025

Source: Bitbo, Incrementum AG

It is worth mentioning that, according to public records, the US already owns the most Bitcoin of any sovereign nation, at 207,189 BTC, and thus almost 1% of the final total BTC supply. China is a close second, at 194,000. The USA, China, Bhutan, El Salvador, Finland, and presumably Georgia own Bitcoin. Germany was on the list but sold 50,000 bitcoins in July of 2024 for roughly USD 57,600 per bitcoin, a move that was poorly timed. Of those nations, El Salvador and Bhutan actively purchase and mine Bitcoin, while the other countries have (so far) acquired Bitcoin by confiscating it from individuals and institutions during civil and criminal investigations. Abu Dhabi’s Mubadala Fund purchased USD 460mn worth of BlackRock’s spot Bitcoin ETF shares, according to a February 2025 13-F filing.

Overall, the amount of BTC owned by sovereign nations is likely larger than the publicly available figures. As of today, governments officially own around 2.5% of the total Bitcoin in circulation.

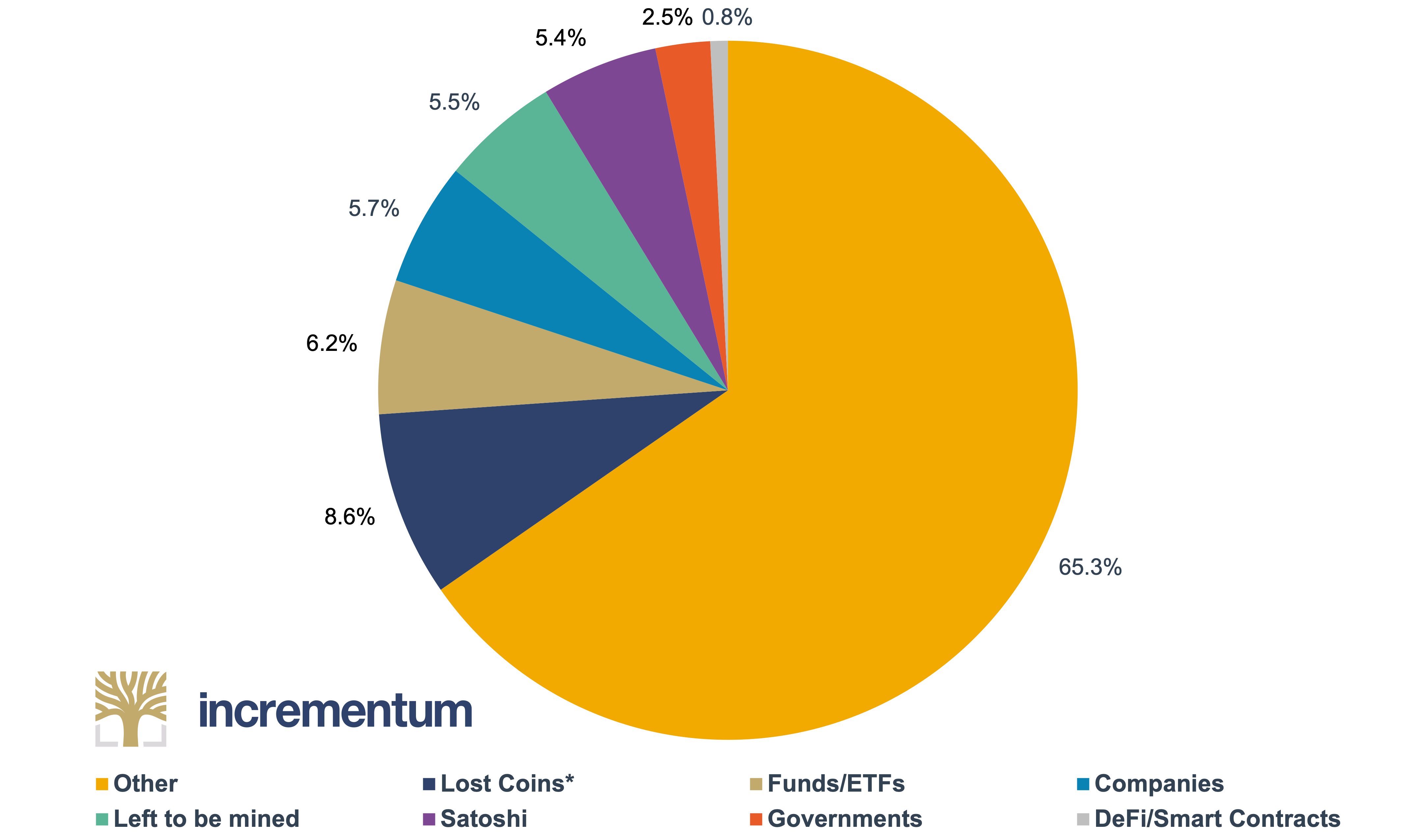

Distribution of Bitcoin Holdings, as % of Total Supply

Source: Bitbo, Chainalysis, Fortune, Incrementum AG

*Estimation by Fortune and Chainalysis

Fort Nakamoto? A national Bitcoin reserve in the United States

Following President Trump’s executive order to create a Strategic Bitcoin Reserve (SBR), the United States officially recognized Bitcoin as a strategic national asset. The executive order distinguishes between Bitcoin and altcoins, establishing the SBR specifically for Bitcoin and a separate Digital Asset Stockpile for altcoins, which may be sold. Unlike the altcoin stockpile, the executive order commits the United States not to sell Bitcoin deposited into the SBR. The executive order also centralizes the ownership and management of federal government holdings of Bitcoin and altcoins.

Yet, what is perhaps most interesting is that the executive order authorizes the Secretaries of Treasury and Commerce “to develop budget-neutral strategies for acquiring additional Bitcoin, provided that those strategies impose no incremental costs on American taxpayers”.

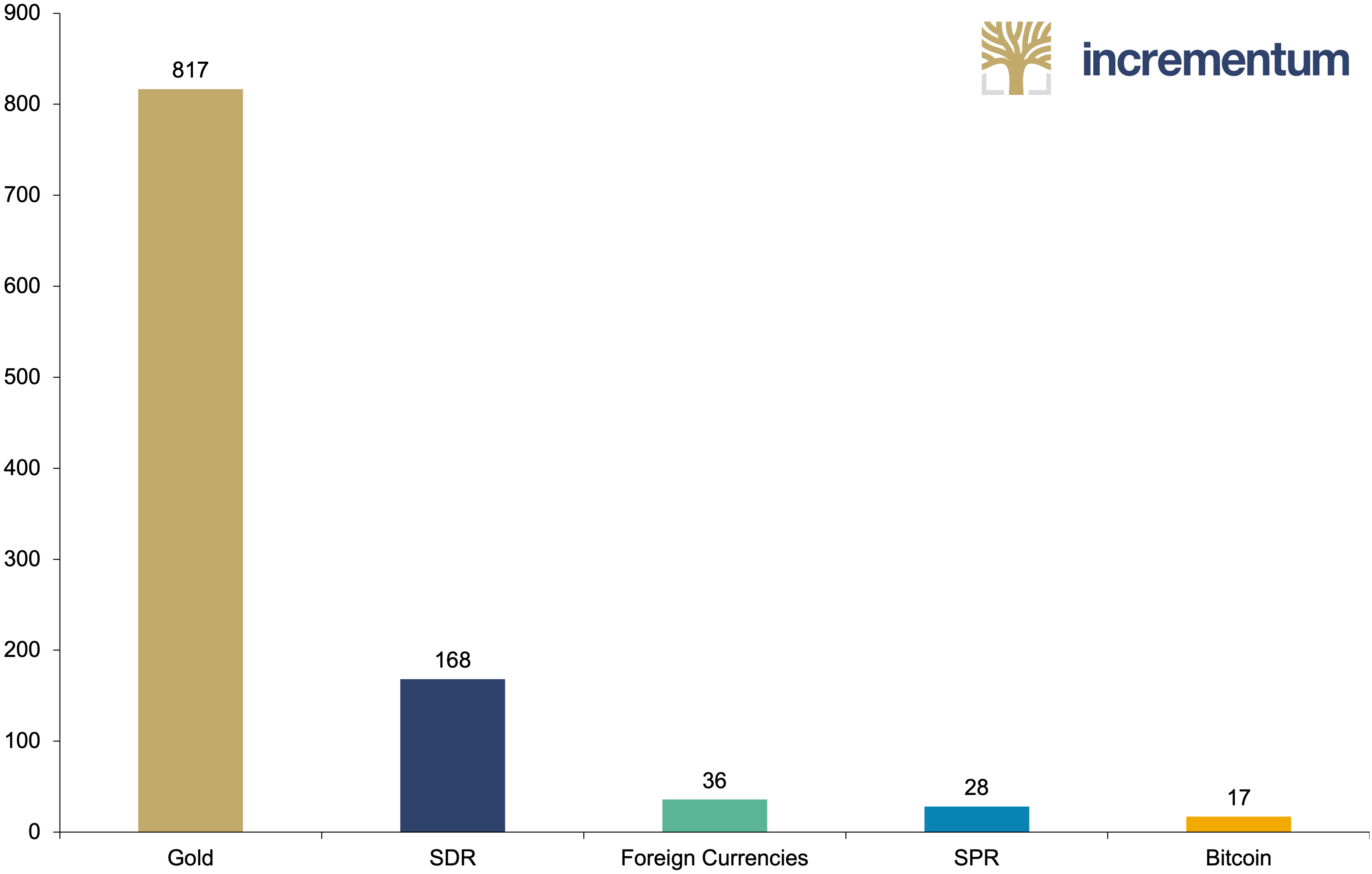

Strategic US Reserves, in USD bn, 03/2025

Source: US Treasury, Bitbo, LSEG, Incrementum AG

Several approaches have been proposed for building a national Bitcoin reserve without direct market purchases. The lowest-hanging fruit is simply retaining Bitcoin confiscated through law enforcement actions. Over the years, agencies have seized approximately 200,000 bitcoins from illicit actors. President Trump’s executive order reverses the previous administration’s practice of selling seized coins, which the executive order identifies as costing taxpayers USD 17bn. It directs agencies to deposit forfeited Bitcoin directly into the US Treasury.

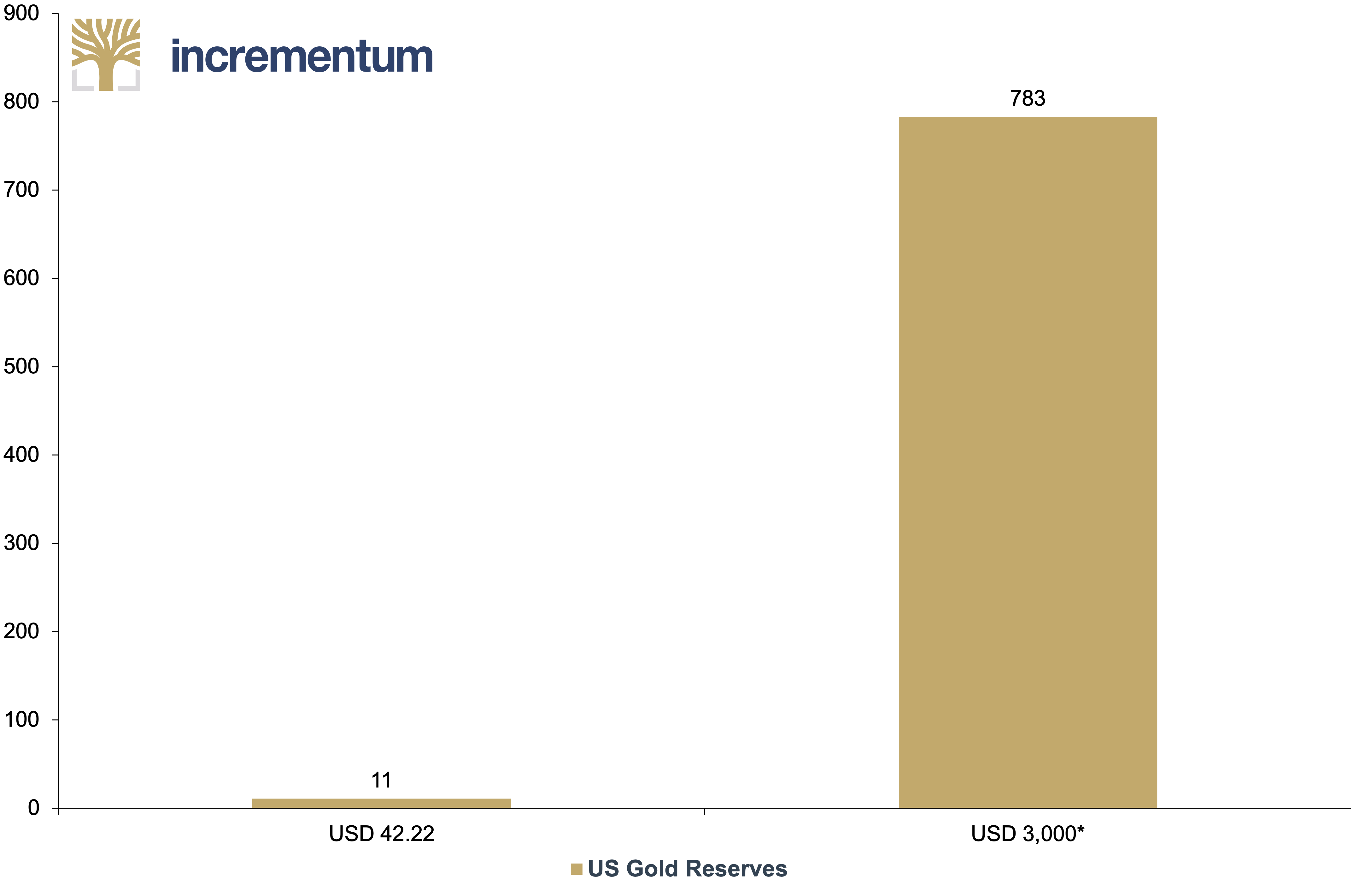

One intriguing approach to funding the Strategic Bitcoin Reserve without directly impacting taxpayers involves leveraging the Treasury’s significantly undervalued gold reserves. Rather than physically selling US gold reserves, the Treasury could revalue its 261.5mn ounces (8,133 t) of gold from the outdated statutory price of USD 42.22 per ounce closer to current market prices. For instance, a revaluation to a price of USD 3,000 would unlock almost USD 800bn in latent balance sheet strength. The mechanism for revaluation is established and straightforward. Under the Gold Reserve Act, the Treasury can “issue gold certificates against other gold held in the Treasury” at a value determined by the Secretary. The Treasury would then deposit these certificates at the Federal Reserve, which would credit the Treasury’s account with the equivalent dollar balances.[1]

US Gold Reserves, valued at USD 42.22 vs. USD 3,000* per ounce, in USD bn

Source: LSEG, Incrementum AG

*This figure is a purely illustrative example and is intended for demonstration purposes only.

Some of these funds could be allocated to Bitcoin purchases without adding to the national debt or requiring additional taxpayer dollars. Wyoming Senator Cynthia Lummis proposed utilizing such revaluation gains to fund the Strategic Bitcoin Reserve. In a November 2024 CNBC interview, the Senator stated:

We have reserves at our 12 Federal Reserve banks, including gold certificates that could be converted to current fair market value. They’re held at their 1970s value on the books. And then sell them into Bitcoin; that way we wouldn’t have to use any new dollars to establish this reserve.

A more experimental approach involves collecting certain taxes, fees, or tariffs directly in Bitcoin. Today, importers pay billions in tariffs, and the Trump administration is keen to raise the revenue that tariffs generate. A portion of these payments could be remitted in Bitcoin, creating a steady stream of Bitcoin flowing into federal coffers without requiring open-market purchases. This strategy has historical precedents. In the 19th century, customs duties and duties on imports (tariffs) had to be paid in gold or silver, which helped build America’s precious metals reserves.

Another potential mechanism is to use the Exchange Stabilization Fund (ESF), which traditionally manages foreign currency operations, gold, and other financial instruments for the Treasury. Bitcoin-denominated debt could theoretically fall under the ESF’s purview. The Treasury could purchase debt instruments repaid in Bitcoin upon maturity.

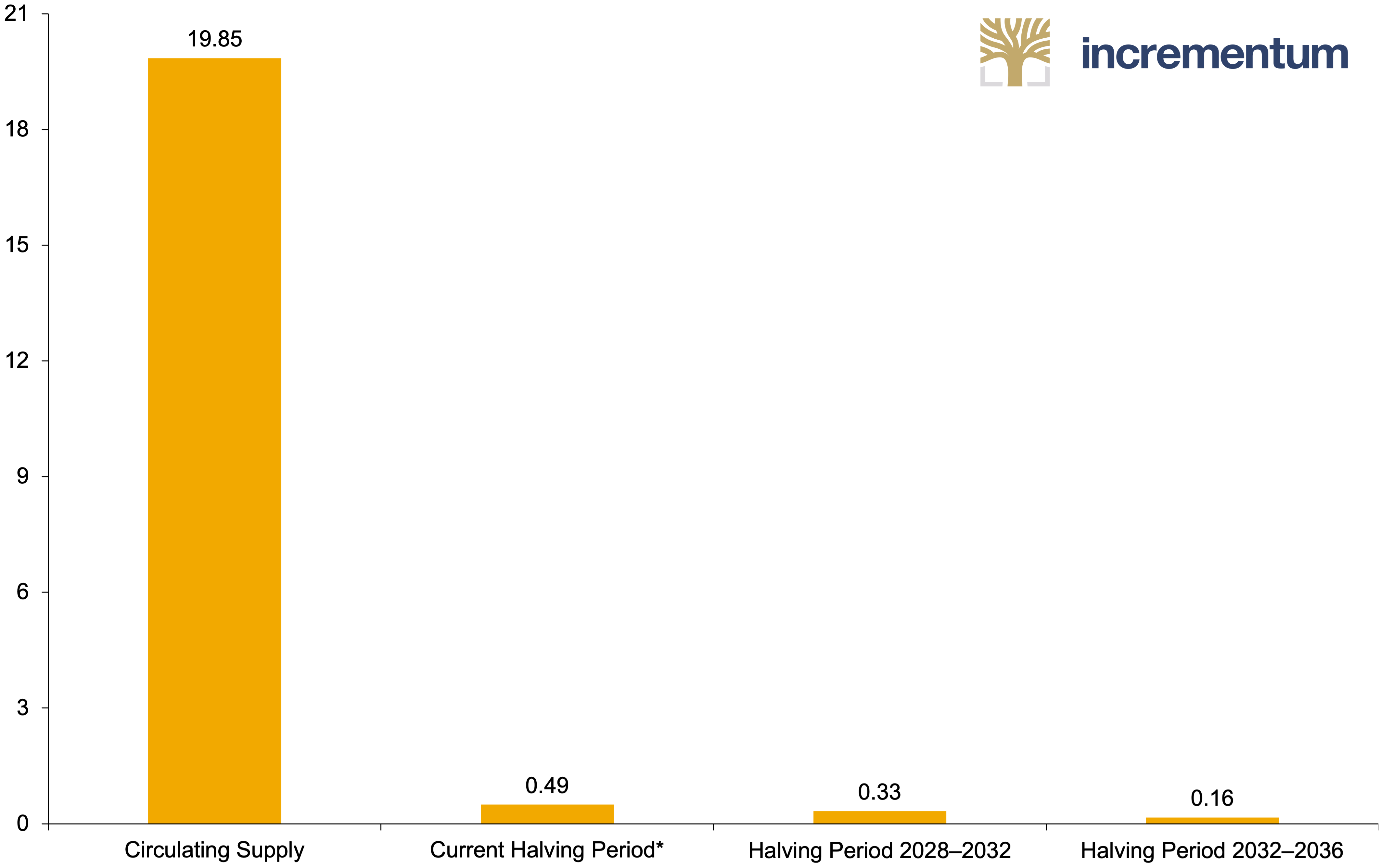

Beyond the ESF, following Bhutan’s example of using hydroelectric power to mine Bitcoin, the US could potentially build or partner with large-scale mining operations in energy-rich regions like Texas. While this requires an initial capital investment, profitability may outweigh costs, reducing the overall budget impact. However, the amount of Bitcoin available via the mining process is quite limited. At this stage, adding a significant stockpile via this route is impossible.

Current Bitcoin Supply and Creation During Halving Periods, 04/2025

Source: Blockpit, Incrementum AG

*Adjusted for the coins already mined from 04/2024–04/2025.

From a geopolitical standpoint, a US Bitcoin reserve may trigger what game theorists call a reflexive response – otherwise known as FOMO – where other nations’ fear of missing out prompts them to begin implementing their formal acquisition programs. El Salvador, the world’s first country with an official Bitcoin strategy, was relatively small-scale; but the United States’ move signals that Bitcoin is now a serious strategic asset on the global stage in the new geopolitics of resources.

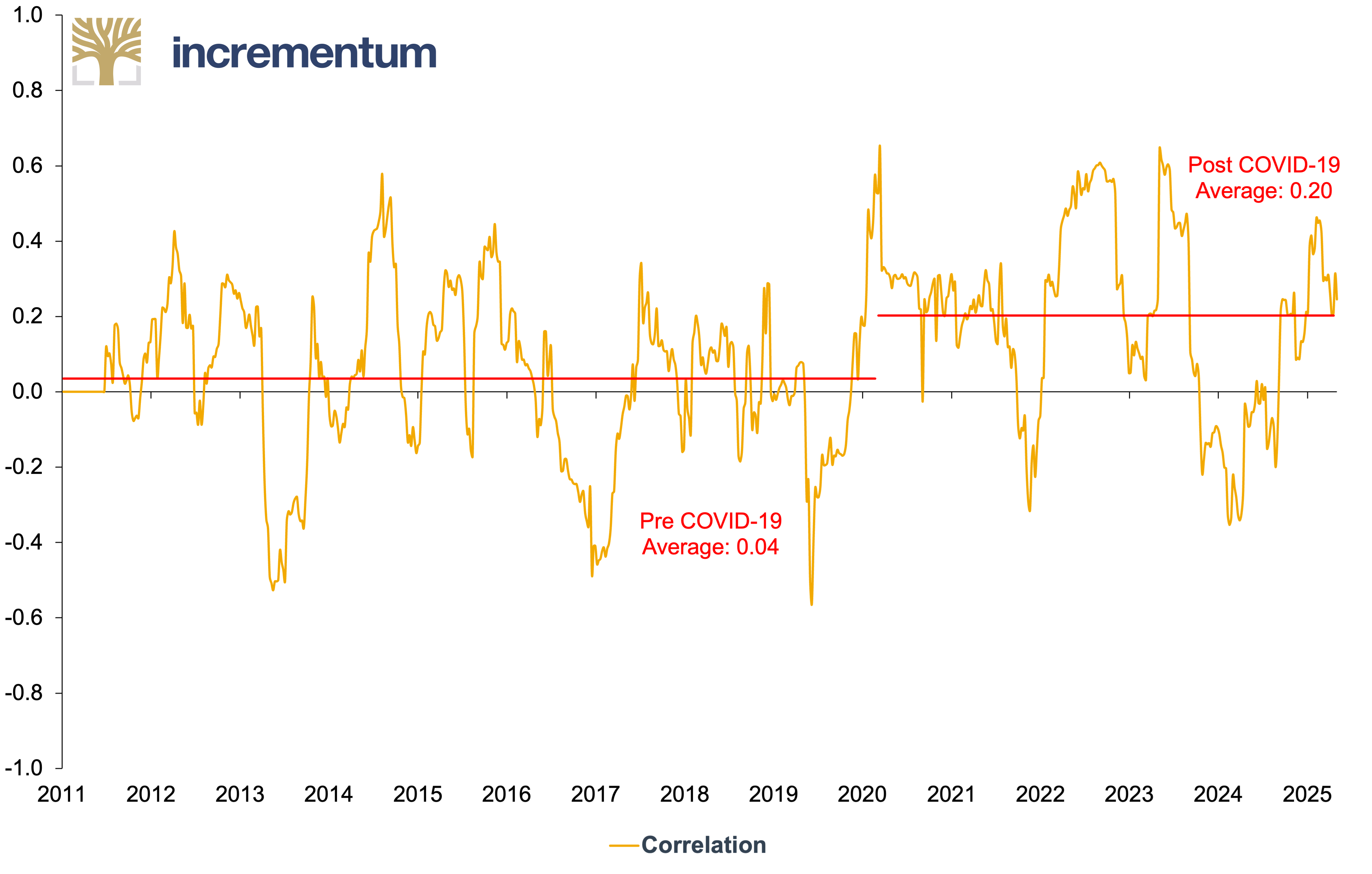

Bitcoin’s evolution into a sovereign reserve asset could also change its market behavior, potentially decoupling its price movements from traditional tech equities. In the past, Bitcoin has been positively correlated with the Nasdaq, generally behaving as a risk-on investment.

Weekly 6-Month Rolling Correlation of Bitcoin and Nasdaq 100, 07/2011–04/2025

Source: LSEG, Incrementum AG

However, a new market dynamic may emerge as nations follow the United States in establishing strategic Bitcoin reserves. Sovereign adoption introduces a different class of holders with multi-decade time horizons and strategic motivations, as opposed to short-term position rotations, potentially reducing Bitcoin’s correlation with tech stocks. The price discovery mechanism could transform as these sovereign players introduce persistent baseline demand independently of traditional market cycles. This would represent a new chapter in Bitcoin’s market maturity – from retail speculation to institutional adoption to sovereign reserve asset – potentially changing its valuation as investors recognize its role as a neutral, non-sovereign reserve asset in an increasingly multipolar world.

Fifty Bitcoin experiments: state-level reserve initiatives

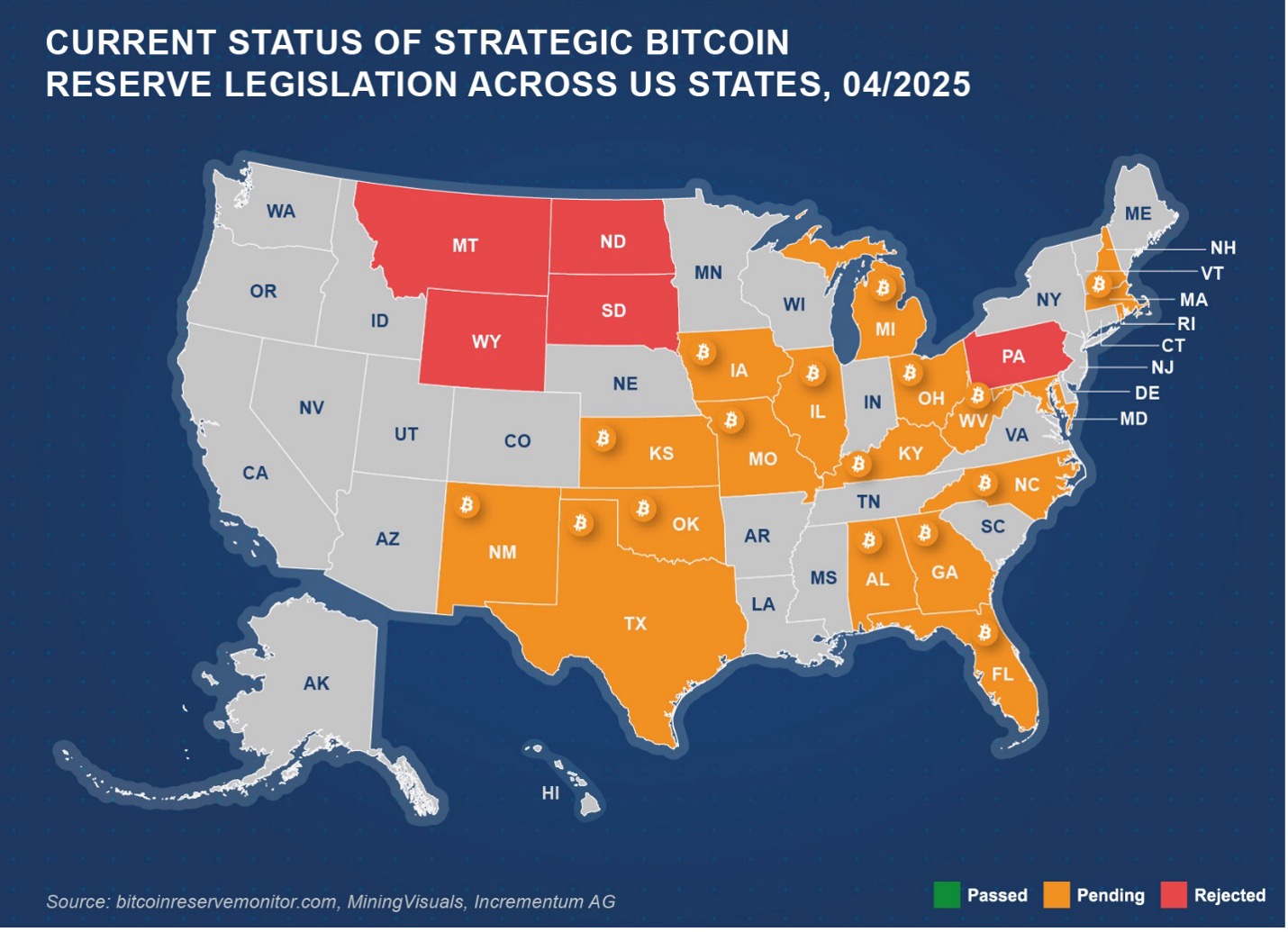

A growing number of national and state policymakers in the United States are exploring the idea of a state-level SBR. Momentum for reserves and other Bitcoin-friendly policies has been accelerating at the state level, particularly in states like Arizona and Utah, which are advancing legislation to purchase and hold Bitcoin in state treasuries. Some proposals extend to pensions and other public funds, while others focus solely on setting aside Bitcoin in rainy day or surplus accounts. As of this writing, most bills remain in the early stages. However, the overall trend reveals a shift toward viewing Bitcoin as a treasury asset that could strengthen a government’s balance sheet.

Several common themes have emerged in these state-level initiatives. First, nearly all of the bills refer to Bitcoin’s capacity for long-term appreciation as a buffer against inflation or macroeconomic stress. Second, at 1% to 10% of existing reserve funds, many of these proposals envision allocating a modest percentage to Bitcoin so as not to disrupt current investment policies. Third, legislators emphasize the need for custody arrangements and regulatory oversight, although specific implementation details vary.

Bitcoin reserve legislation has been proposed in 26 states so far, and estimates for the amount of BTC those states would have to purchase if the legislation were to pass are 262,577 BTC, roughly USD 25bn at current market prices. Currently, there are 19 pending proceedings.

A few states have dropped their proposals due to political disagreements or uncertainty about custody and volatility. Even so, the pattern indicates that Bitcoin is moving into the public finance conversation in a way that was nearly unthinkable just a few years ago.

The Corporate Bitcoin Rush

While nation state adoption is a new phenomenon, corporations have been stacking Bitcoin for several years now. In the past year an increasing number of publicly listed companies have begun adopting Bitcoin as part of their corporate treasuries, following the initial trail blazed by MicroStrategy in mid-2020. These Bitcoin treasury strategies reflect a broader recognition that Bitcoin’s scarcity and track record of appreciation make it a balance-sheet enhancer. Block, Metaplanet, Semler Scientific, and the popular media platform Rumble have made strategic Bitcoin allocations. Metaplanet, a publicly traded Japanese company currently executing a Bitcoin treasury strategy, is up over 4,000% over the last few months, since President Donald Trump’s son Eric joined its board of advisors.

During this bull market, the corporate adoption trend of Bitcoin has been accelerating at a faster pace than that of government initiatives. GameStop, a household name in retail, closed its USD 1.3bn convertible note offering in April, including full exercise of the USD 200mn greenshoe option, providing USD 1.48bn in net proceeds explicitly earmarked for Bitcoin purchases. The video game retailer’s move mirrors that of Strategy, and when GameStop made the announcement, Strategy CEO Michael Saylor tweeted, “Welcome to Team Bitcoin, @RyanCohen,” to the GameStop CEO. This pattern is not spreading through the US alone but occurring globally, with France’s The Blockchain Group adding another 580 Bitcoins to its treasury in March 2025, as its stock has risen 225% since launching its Bitcoin strategy in November 2024. Meanwhile, HK Asia Holdings recently became the first publicly traded company in Greater China to implement a Bitcoin treasury strategy.

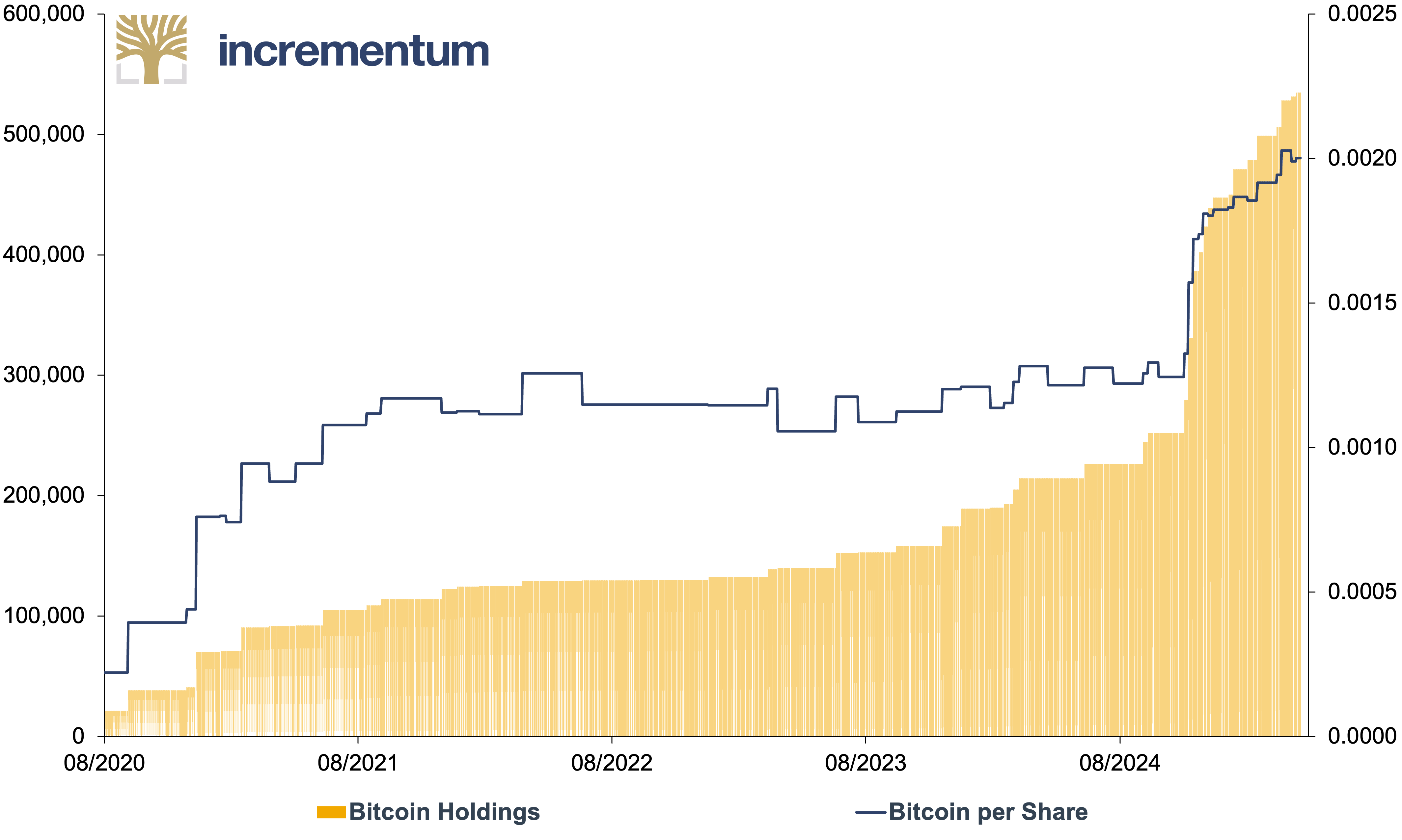

A key idea emerging from these strategies is Bitcoin yield, first introduced by Strategy to illustrate how shareholders may receive an increasing Bitcoin exposure over time. The concept tracks changes in total Bitcoin held relative to a company’s fully diluted share count. The BTC-per-share metric can increase as the firm raises capital through equity, convertible debt, or other instruments and channels it into more Bitcoin. Although yield here does not refer to dividend income, the metric is intended to help gauge whether share issuances are accretive in terms of long-term Bitcoin accumulation.

Strategy Bitcoin Holdings (lhs), in Coins, and Bitcoin per Share (rhs), 08/2020–04/2025

Source: bitcointreasuries.net, Incrementum AG

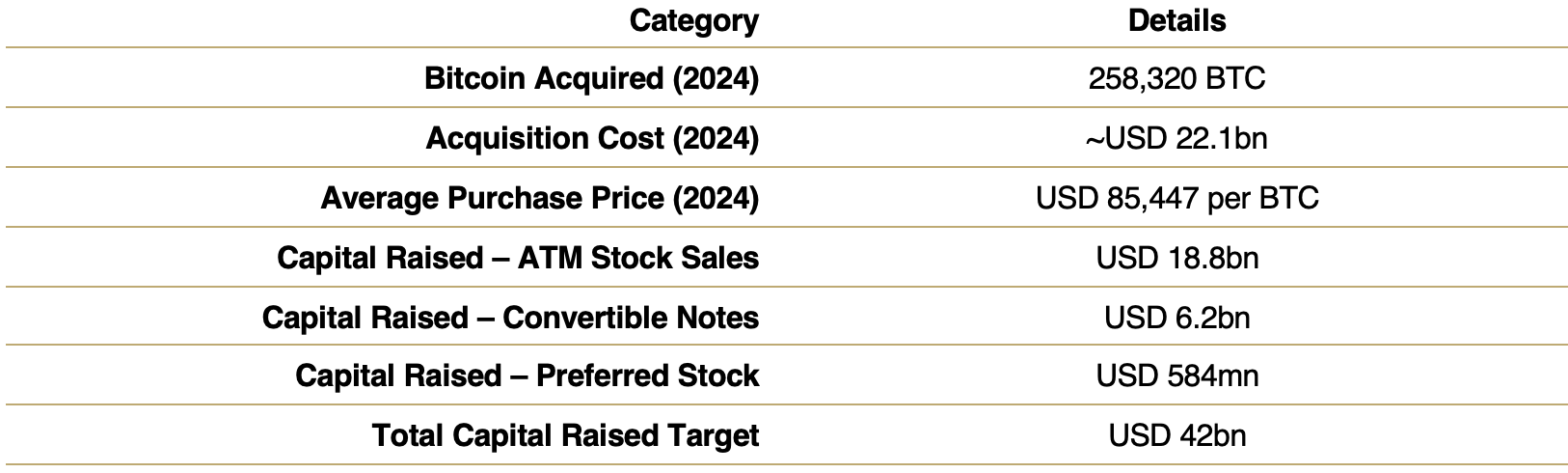

No company embodies the Bitcoin treasury strategy more completely than Strategy itself. Initially, a business intelligence software firm, it has evolved into a publicly traded Bitcoin vehicle. Through a series of convertible bond offerings at low or even zero coupon rates, Strategy has borrowed billions of dollars using capital market inefficiencies – where convertible note buyers value the embedded volatility – to fund additional Bitcoin purchases.

Strategy Bitcoin Acquisition and Capital Markets Activities, 2024

Source: Fourth Quarter 2024 Earnings Presentation, February 5, 2025, Incrementum AG

The company recently issued perpetual preferred stock, trading under ticker STRK, designed to pay an 8% dividend but also to offer conversion features into Strategy’s common stock. Strategy’s model combines the assumption that cheap credit and traditional finance inefficiencies will continue, with the belief that Bitcoin will continue to appreciate, and the interest Strategy owes on its debt and equity commitments will not put the company at risk or in a position where it needs to sell off its Bitcoin holdings.

Ultimately, Strategy’s approach can be seen as an innovative balance sheet strategy. By tapping capital markets to accumulate Bitcoin, publicizing a form of “Bitcoin yield,” and issuing instruments like perpetual preferred shares or convertible bonds, the company is utilizing Bitcoin as a liquid reserve asset that enables a range of balance-sheet arbitrage opportunities. If demand for specific securities such as convertible bonds is strong, the firm can issue these instruments at a premium to the underlying Bitcoin exposure. The proceeds can then be used to purchase additional Bitcoin, effectively generating more Bitcoin per dollar raised. This dynamic represents a kind of quasi-Bitcoin yield, driven not by Bitcoin itself but by the structure and timing of capital markets issuance.

Nevertheless, there are risks associated with this business model. If Bitcoin’s price were to decline over an extended period of time, Strategy’s leveraged exposure could place strain on its finances. Additionally, the structure might give rise to an asset-liability mismatch, particularly if the maturity profile or cost of capital begins to diverge significantly from the performance of its Bitcoin holdings. That said, concerns about an imminent collapse may be overstated. In practice, the firm has demonstrated a consistent ability to hold through downturns and to refinance or roll over maturing obligations effectively.

We have recently seen several companies adopt some kind of Bitcoin treasury strategy. However, ultimately, the number of firms that can viably pursue such a model will remain limited. Differences in jurisdictional frameworks and the design of innovative – though invariably risky – balance sheet structures may allow for a handful of viable approaches, but widespread replication is unlikely.

One reason is that investor demand for these securities is likely to diminish once enough liquid instruments with differentiated risk-return profiles already exist. Additionally, in the event of a bear market, we would expect to see a natural consolidation among Bitcoin treasury firms, further reducing the viable universe.

Time for BitBonds?

BitBonds, also referred to as ₿ Bonds, are a financial instrument proposed by Andrew Hohns of Newmarket Capital that combines fixed-income with Bitcoin exposure. Hohns and others have initially conceptualized BitBonds as a bond that the US Treasury would issue to reduce the interest burden, grow the SBR in a budget-neutral fashion, create a tax-advantaged savings vehicle for families, and reduce the debt over time as Bitcoin appreciates.

Under Hohn’s framework, the Treasury would issue a BitBond with a stated face amount and maturity period where 90% of the proceeds fund normal operations, i.e. government spending or corporate activities, while 10% purchases Bitcoin. These bonds would pay lower interest rates than traditional bonds – potentially just 1% compared to the current 4.1% for 10-year Treasuries – reducing the Treasury’s interest expenses. At maturity, investors receive their principal, a guaranteed minimum return, and a share of Bitcoin’s appreciation. This lowers the borrowing costs for the issuer and provides upside exposure to Bitcoin with limited downside risk for the investor.

While the current BitBonds proposals are for sovereign debt, corporate treasurers could apply the same principles. Companies already struggling with negative real yields on cash holdings could issue corporate BitBonds at favorable rates, building Bitcoin positions without shocking shareholders with direct purchases. For corporations interested in Bitcoin acquisitions but concerned about volatility impacting quarterly earnings, BitBonds are a structured approach that smooths exposure while potentially lowering overall financing costs. The mathematics is compelling: A corporation issuing a 5-year BitBond at 2% instead of conventional debt at 5% would save 3% annually on 90% of the principal. Even if Bitcoin’s value declines by 50%, the company will still achieve net savings compared to traditional financing while establishing a Bitcoin position. If Bitcoin appreciates as it has historically, the returns could be substantial.

For treasury managers exploring Bitcoin allocation strategies, BitBonds could become an alternative to Strategy’s Bitcoin acquisition approach, as the issue of excess volatility is solved. As Bitcoin’s appeal grows, more-complex products such as BitBonds will likely further Bitcoin adoption among corporations that recognize the need for hard-asset exposure but do not want to HODL a large direct position over time.

Spot ETFs, the Halving, and a Decoupling?

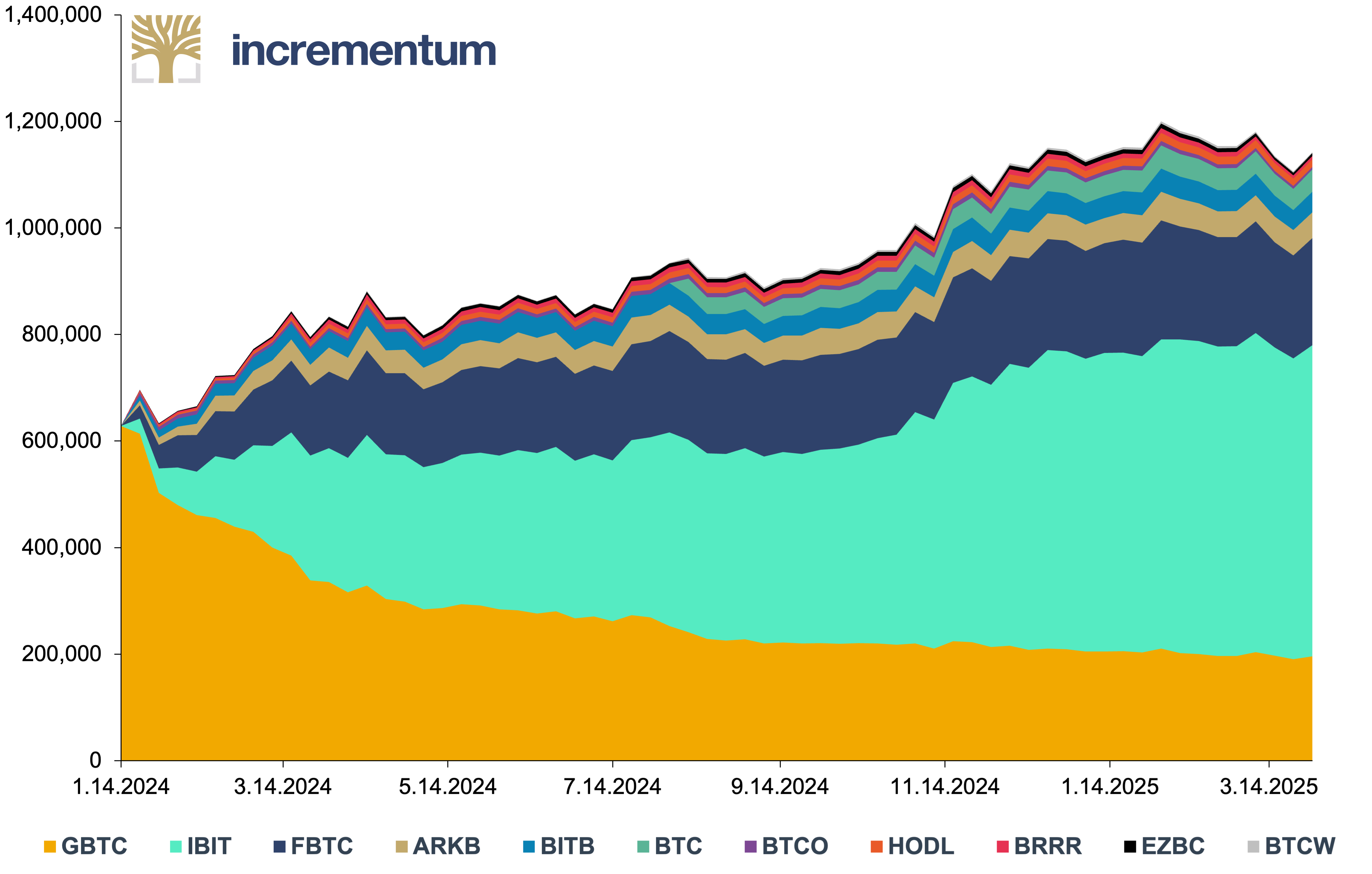

During the recent market “chop” that has been attributed to the global trade war, Bitcoin has demonstrated unusual resilience, with price movements that have not mirrored the Nasdaq. This emerging decoupling appears driven by several factors: broader institutional participation through spot ETFs, the halving cycle, and Bitcoin’s growing appeal as a neutral reserve asset amid geopolitical tensions – or, put differently, its increasing mainstream recognition as a store of value. Despite the recent uncertainties, Bitcoin ETF holdings continued to increase incrementally.

Spot Bitcoin ETF Holdings, in Bitcoin, 01/2024–03/2025

Source: LSEG, Incrementum AG

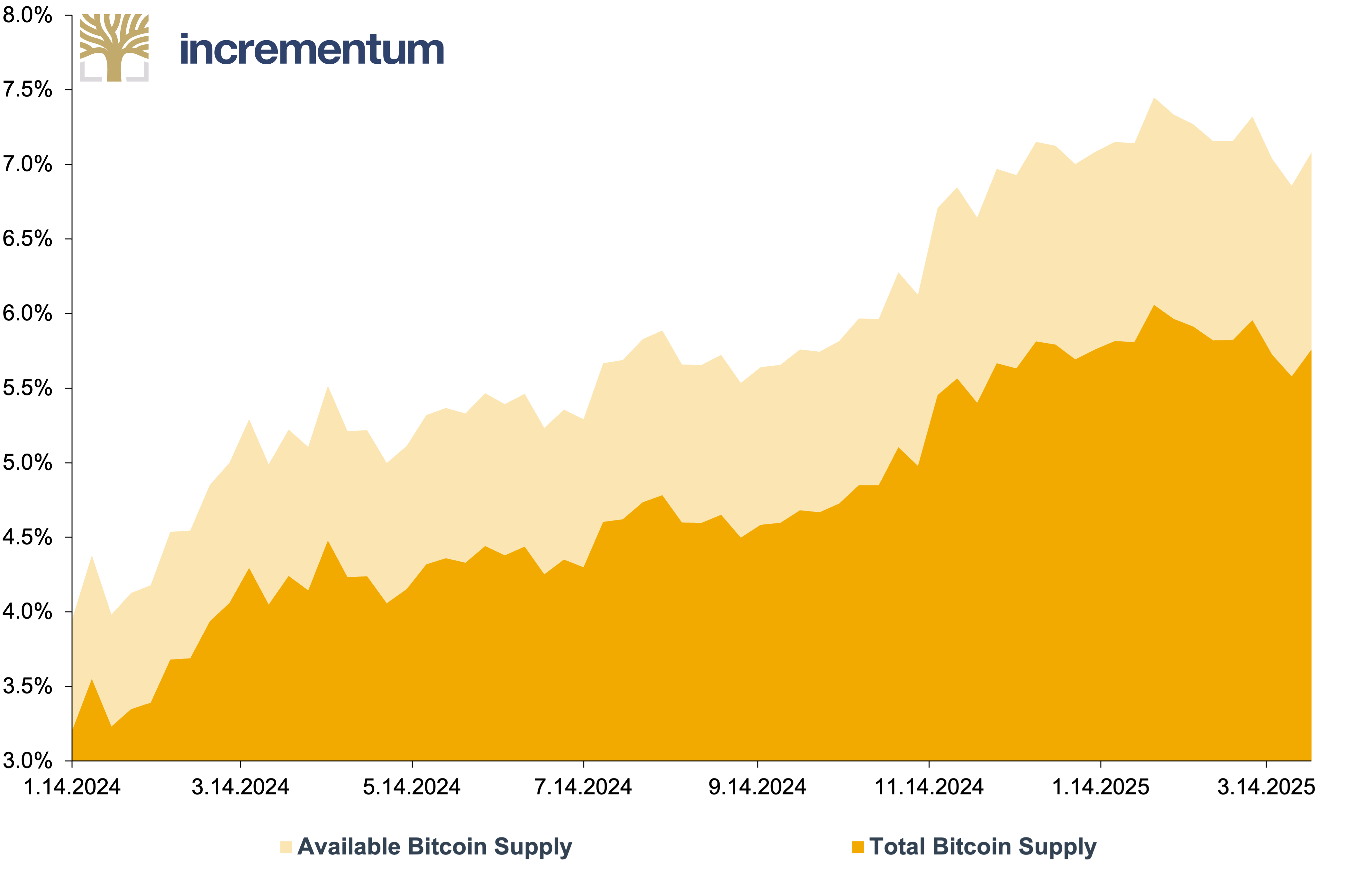

The April 2024 halving, which we covered in the chapter “The New Playbook for Bitcoin” in the In Gold We Trust report 2024, reduced the block reward from 6.25 to 3.125 BTC per block. As of this writing, over 95% of all 21mn bitcoins has been mined. Yet, comparing Bitcoin’s performance to previous halving cycles, the effects from this cycle appear to be relatively muted. This aligns with our thesis from last year, which is that the impact of halving cycles on price may diminish over time. Last year, we also identified that spot Bitcoin ETF approval would reduce legal risk and drive market acceptance. Since then, BlackRock, Fidelity, and others have firmly established themselves in the Bitcoin ecosystem. Their regulatory influence has contributed to an environment where Bitcoin bans or other adverse government actions have become increasingly unlikely. Currently, more than 5% of all Bitcoin is held by US Bitcoin ETFs.

ETF Holdings in % of Bitcoin Supply, 01/2024–03/2025

Source: LSEG, Incrementum AG

The record-breaking inflows to spot ETFs have created a new political reality. With millions of institutional and retail investors now having Bitcoin exposure through these vehicles, politicians face significant disincentives when considering anti-Bitcoin policies. The diverse coalition of Bitcoin stakeholders now includes traditional hedge funds, investment banks, ETF issuers, and a growing segment of retail voters. Bitcoin’s political risks in developed markets have reached historical lows and continue diminishing as the asset class becomes further embedded in the mainstream financial infrastructure. Traditional financial managers will likely create more complex structured products beyond the simple spot ETFs.

A New Frontier for Bitcoin Miners

Bitcoin mining stocks have traditionally been viewed as a high-beta bet on Bitcoin. In our view, an active approach is essential when considering an allocation to Bitcoin miners within a portfolio. Like gold miners, Bitcoin mining companies face operational, regulatory, and market risks. Still, in the current bull market for both Bitcoin and gold, a performance allocation – for the same reason as a performance gold allocation – may be compelling. This strategy consists of assets with the potential to outperform Bitcoin during Bitcoin bull markets, such as Bitcoin mining stocks and Bitcoin treasury companies like Strategy and Metaplanet.

While miners remain a core component of performance Bitcoin, new industry trends such as Bitcoin treasury companies, high-performance computing (HPC), hashrate derivatives, and the rise of spot Bitcoin ETFs have begun to reshape the dynamics of Bitcoin miners as a strategic investment. Historically, Bitcoin mining stocks have outperformed Bitcoin in bull markets due to their operating leverage, fixed-cost structures, and the speculative nature of capital inflows.

Performance Comparison of Bitcoin, and Bitcoin Miner (log), in USD, 100 = 02/2022, 01/2020–04/2025

Source: LSEG, Incrementum AG

However, recent trends indicate that miners may no longer move as directly with Bitcoin. The introduction of spot Bitcoin ETFs in 2024 provided institutional investors with a direct vehicle for BTC exposure, reducing the need for mining stocks as a proxy. Simultaneously, the emergence of hashrate derivatives allows miners to hedge their revenue streams, reducing their dependence on the spot price.

Bitcoin, and Valkyrie Bitcoin Miners ETF, 100 = 29.12.2023, in USD, 01/2024–04/2025

Source: LSEG, Incrementum AG

Another key development is the growing intersection between Bitcoin mining and HPC. As the demand for AI-driven computing power rises, some miners are allocating resources to AI and data center operations. Firms like Hive, IREN, Hut 8, and Core Scientific have already begun integrating HPC workloads alongside Bitcoin mining, changing their valuation models. The release of DeepSeek, an open-source Chinese AI model that supposedly required substantially less compute to train, caused Bitcoin mining stocks to drop heavily on the news as investors feared the negative impact on HPC demand. If this trend continues, HPC-focused mining stocks will trade more like data centers or energy infrastructure companies than strictly Bitcoin-correlated assets.

The introduction of spot ETFs and other Bitcoin structured products, hashrate derivatives, and HPC introduces an important question: Will miners remain a viable high-beta Bitcoin bull market play, or will their diversification into HPC among other market changes make them less relevant as a performance Bitcoin allocation?

Despite these structural shifts, miners remain dependent on Bitcoin price movements. However, as the industry matures, active selection becomes even more critical. Many miners have recently underperformed Bitcoin, as J.P. Morgan’s recent analysis of US-listed mining stocks demonstrates. Investors seeking more exposure to Bitcoin’s upside in 2025 must carefully navigate an evolving landscape where mining stocks provide a less straightforward method to amplify their exposure to Bitcoin’s movements. While we believe miners can outperform Bitcoin in certain phases of the market cycle, a more tactical and selective approach will likely be required going forward.

Bitcoin and the Next Monetary Cycle: A Scenario-Based Outlook

Considering the growing convergence of macro narratives around gold and Bitcoin, and within the context of our Big Long thesis, we see it as timely and relevant to extend our existing gold price model to include a relative valuation framework for Bitcoin. For years, we have closely monitored the relative value ratio between Bitcoin and gold, as both assets, according to arguments we have made, consistently serve overlapping functions as stores of value. From our perspective, the ratio of their respective market capitalizations offers a reasonable and intuitive quantitative metric for comparison.

The dominant trend over the past 15 years has been a rise in the market capitalization of both assets. However, Bitcoin’s growth has consistently outpaced that of gold. As a result, the Bitcoin/gold market cap ratio has climbed—albeit along a volatile path—from virtually zero to around 10%. This development reflects the growing adoption of Bitcoin as a store of value, particularly among younger investors, institutions, and, increasingly, sovereign actors. We believe this trend is likely to continue. While both assets are expected to gain further relevance within a shifting monetary landscape, we anticipate that Bitcoin’s relative growth will continue to outpace that of gold over the next five years.

Our In Gold We Trust report 2020, “The Dawning of a Golden Decade”, introduced a gold price projection based on monetary expansion (M2) and the implicit gold coverage ratio. This model produced a probability-weighted gold price expectation of roughly USD 5,000 by 2030, with upside potential toward USD 8,900 in more inflationary or stagflationary scenarios.

By modeling Bitcoin’s market cap as a share of gold’s, we can construct a relative valuation matrix. Assuming gold reaches our baseline target of about USD 5,000 by 2030, this would imply a total market cap of approximately USD 38trn for gold. Depending on Bitcoin’s adoption trajectory, scenarios in which Bitcoin captures 10%, 25%, 50%, or even 100% of gold’s market cap yields price levels ranging from ~USD 185,000 to ~USD 1,850,000 per BTC.

Gold/Bitcoin Matrix: Gold (x-axis), in USD, and % of Gold’s Market Cap (y-axis), 12/2030*

Source: World Gold Council, coinmarketcap.com, Incrementum AG

*Based on the expected Bitcoin supply at end of 2030 and gold supply at end of 2030, assuming an annual supply growth of 1.5%.

This matrix does not represent a price prediction per se, but rather a scenario-based framework – rooted in our established gold model – that offers a clearer sense of what relative revaluations of non-sovereign hard assets might look like by decade’s end.

If we map out this scenario over time, we find that it aligns with a pattern of diminishing marginal adoption, hence diminishing returns. This is consistent with a power-law dynamic often observed in network-based assets. Within this framework, the speed of the relative growth of Bitcoin compared to gold slows but continues to expand meaningfully in absolute (nominal) fiat currency terms. We don’t believe that Bitcoin’s market cap will reach parity with gold’s in the foreseeable future. However, given the current macro environment—as outlined in detail above—continued growth to approximately 50% of gold’s market capitalization by 2030 appears reasonable to us within a bullish scenario.

Market Cap of Gold and Bitcoin (lhs), in USD bn, and Bitcoin/Gold Market Cap Ratio (log, rhs), 01/2013–12/2030*

Source: LSEG, World Gold Council, coinmarketcap.com, Incrementum AG

*Based on the expected Bitcoin supply at end of 2030 and gold supply at end of 2030 assuming an annual supply growth of 1.5%.

What makes this trajectory particularly noteworthy is that, despite slowing relative adoption, nominal price increases remain significant. This is primarily because we assume that the overall size of the gold market will continue to grow in the coming years. In other words, this scenario builds not just on Bitcoin’s relative positioning but also on the broader macro trend of fiat currency debasement and the revaluation of neutral reserve assets. Bitcoin and the next monetary cycle are likely to be closely intertwined. In a bullish scenario, as outlined above, a nominal Bitcoin price increase in the ballpark of 10x by 2030 appears conceivable.

Conclusion

Some market participants were initially disappointed by the lack of immediate large-scale purchases and upward price movements following President Trump’s Strategic Bitcoin Reserve announcement. Yet, this perspective misses the signal within the noise: Bitcoin has been officially recognized as strategically important to the world’s largest economy.

The Strategic Bitcoin Reserve will likely trigger a cascade of responses across the global stage. It is reasonable to expect other major economies to establish strategic Bitcoin reserves. Despite current restrictions, even China may be forced to reconsider its stance in the new world of economic statecraft. As Grayscale Research notes, Chinese policymakers are already allowing expanded Bitcoin and altcoin activity in Hong Kong under the one country, two systems framework; and recent discussions in China’s Supreme Court about the legal treatment of digital assets suggest it may be considering a policy shift.

With its vast sovereign wealth funds, the Middle East represents another frontier. As Dubai transformed into a global gold trading hub, we expect several Gulf states to move beyond spot Bitcoin ETF purchases to direct Bitcoin acquisition, establishing the region as a critical “node” for Bitcoin finance. This move fits within the broader pivot by middle powers seeking to enhance their wealth and decouple from the great powers in an increasingly multipolar economic landscape.

On the corporate front, Bitcoin is being embraced even more rapidly. The actions of Strategy, GameStop, and others are likely just the beginning. In the next few years, we predict that at least one Fortune 50 company – perhaps Apple, Microsoft, or a major Japanese corporation famous for holding lots of cash like Nintendo – will allocate a meaningful portion of their treasury to Bitcoin. This could happen directly but also indirectly with Bitbonds, which solve the problem of excessive volatility.

Sovereign and corporate movements may change Bitcoin’s market behavior over time. As Bitcoin transitions into a strategic reserve asset, we expect a decoupling from the Nasdaq and tech stocks. However, we are sticking to our view that the volatility will not fall significantly, since Bitcoin is pure liquidity and will be influenced by the inflationary and deflationary ebbs and flows of the current monetary system.

The overall trajectory of Bitcoin’s price seems bright: As the global monetary system evolves, Bitcoin is increasingly viewed as a complementary reserve asset alongside gold. In the bullish scenario we outlined – Bitcoin’s Big Long, so to say – , a tenfold increase in Bitcoin’s price by 2030 lies well within the realm of possibility.

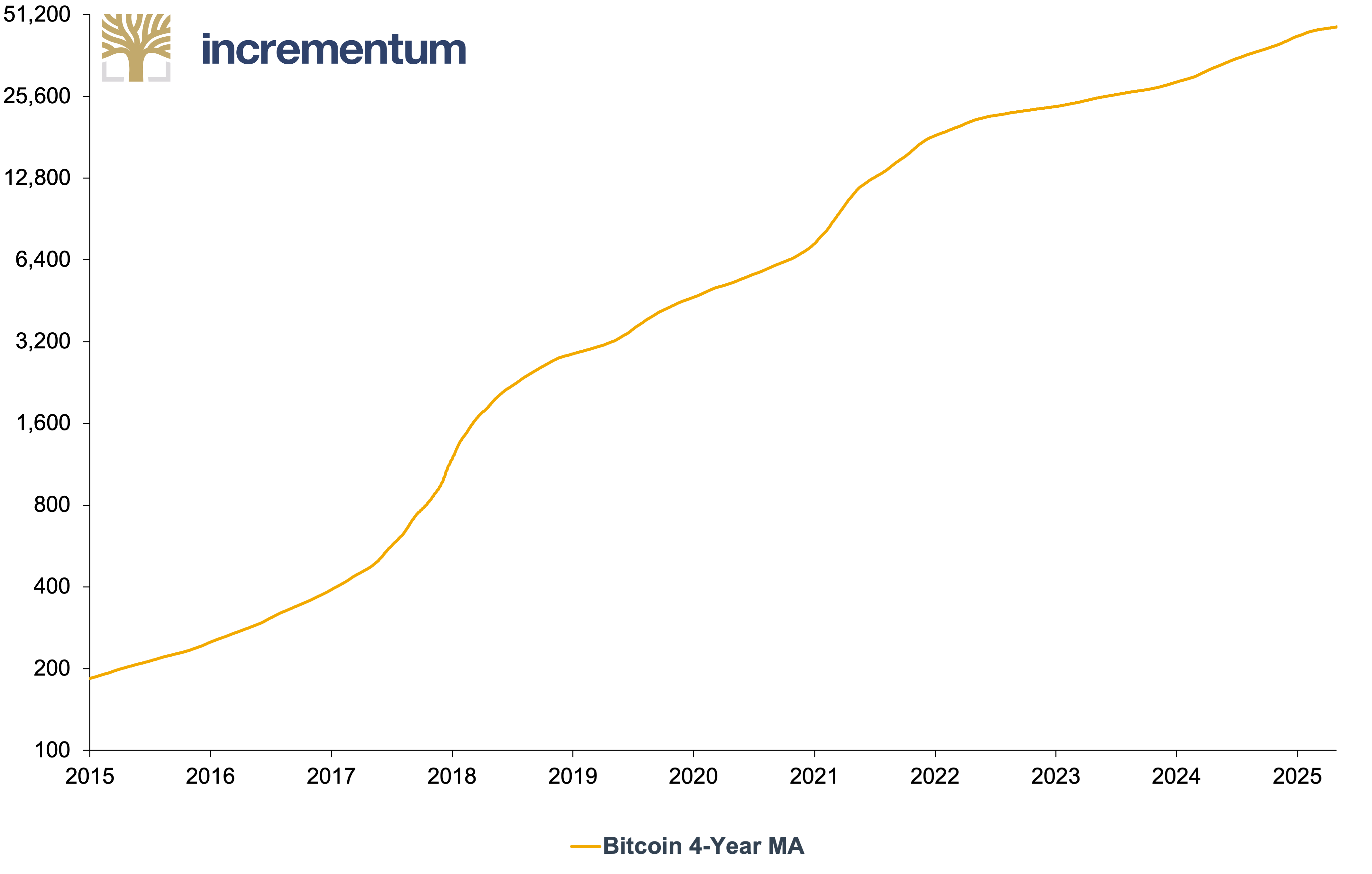

Bitcoin 4-Year MA (log), in USD, 01/2015–04/2025

Source: blockchain.com, LSEG, Incrementum AG

[1] See the chapter “Dollar Milkshake Meets Golden Anchor: Mar-a-Lago and the New Economic Order” in this In Gold We Trust report